Sample Category Title

US 100 Cash Index Edges Lower; Key Levels Ahead

- US 100 cash index remains under bearish pressure

- Prepares to test the September lows as geopolitics dictate sentiment

- Momentum indicators point to a continuation of the current move

The US 100 cash index is trying to record its fifth consecutive red candle for the first time since April. The bears continue to take advantage of the current bearish sentiment that is fuelled by unfolding geopolitical developments. Their main target appears to be a lower low, below the recent 14,430 low, in order to keep the developing series of lower lows and lower highs intact.

The bears are now also enjoying the support of the momentum indicators. The Average Directional Movement Index (ADX) is edging higher, above its 25-threshold, revealing a weak bearish trend in the market. Similarly, the RSI has again dipped below its midpoint, but it does not appear ready to test its recent lows. More importantly, the stochastic oscillator is edging lower in a vertical fashion towards its oversold territory, building a good gap from its moving average and sending a bearish signal.

With their confidence sky-high, the bears are preparing to test the busy 14,346-14,382 area, which is populated by the October 4, 2021 low and the 61.8% Fibonacci retracement level of the November 22, 2021 – October 13, 2022 downtrend. If successful, they could then set sail for the 13,957-14,075 region that is defined by the April 29, 2021 high and 200-day simple moving average (SMA).

On the flip side, the bulls are trying to stop the current downleg. They could try to defend the 14,346-14,382 area and then stage a rally towards the 15,031-15,112 region set by the 50- and 100-day SMAs. Even higher, they could test the resistance set by the July 19, 2023 descending trendline and the busy 15,257-15,411 area.

To sum up, the US 100 cash index bears are firmly in control of the market, taking advantage of the fragile market sentiment and targeting another lower low.

ECB Meets But No Fireworks Expected

- The ECB rate-setting meeting dominates this week’s busy schedule

- Market does not expect a rate change; focus on statement and overall rhetoric

- Decision will be announced on Thursday 12.15 GMT, press conference at 12:45 GMT

ECB travels to Greece for another meeting

The European Central Bank is holding its penultimate meeting for 2023 on Thursday, a week before the Fed gathering. This fact alone increases the pressure on the ECB to avoid shocking the market with its announcements. To be fair, unlike September, this gathering is expected to generate fewer headlines, especially as the market is assigning a 1% probability for a 25bps rate move; a rather odd situation considering the current rate hiking cycle is theoretically still alive.

This market expectation reflects the numerous dovish comments from ECB officials since the September meeting. Even the more hawkish ECB members, for example France’s Villeroy, have been vocal that no extra rate hikes are needed at this stage. This stance could be part of an agreement made at the September gathering between hawks and doves for a final rate hike in exchange for less hawkish rhetoric from the uberhawks.

Market fully prices in a rate cut in mid-July 2024

However, the market is a firm believer that the ECB will not hike again during this current tightening cycle. Similar to the Fed pricing, the next fully priced-in rate move is expected to be a 25bps rate cut at the July 2024 meeting. While this could be confirmed, the geopolitical developments could completely shift the monetary policy outlook. A possible escalation in the Middle East could exponentially increase the risk of another rally in oil and gas prices, like the ones seen in 2022 that caused exceptionally high inflation rates over the past 18 months.

Therefore, at this week’s meeting the ECB is expected to appear slightly less dovish than currently anticipated. It costs little to the President Lagarde et al to keep the door open for a December or even for a first-quarter of 2024 rate move if global supply issues threaten another jump in inflation and/or second-round effects continue to keep inflation at levels not consistent with the targeted price stability.

Alternatively, a discussion for an earlier stop of PEPP reinvestments, from the current end-2024 target, could also do the trick of informing the market that the ECB is in waiting-mode but not ready to signal the end of its tightening bias.

ECB needs time to evaluate the situation

Patience will probably be the key word at the meeting as the ECB wants more time in order to evaluate geopolitical developments and their economic implications, and allow the past rate hikes to feed through the system. President Lagarde has been quite vocal about the strong transmission of monetary policy changes but with the M3 money supply dropping to negative territory, there is increasing risk of a more protracted downturn than currently anticipated by the ECB, further complicating the economic outlook and giving rise to “stagflation” headlines.

In addition, the new ECB staff forecasts will be available in December. There have been a couple of comments from ECB officials stating their confidence that the 2% target will be met by 2025 after the September forecasts had inflation dropping to 2.1% by end-2025.

Moreover, with the final ECB meeting for 2023 scheduled for December 14, two more inflation reports and the preliminary GDP prints for the third quarter of 2023 will be published by then. A plethora of upside surprises at these data releases along with an unwanted and persistent rally in oil and gas prices could tick many boxes for another, possibly final, rate hike by the ECB.

The euro could get a strong boost from a more hawkish ECB

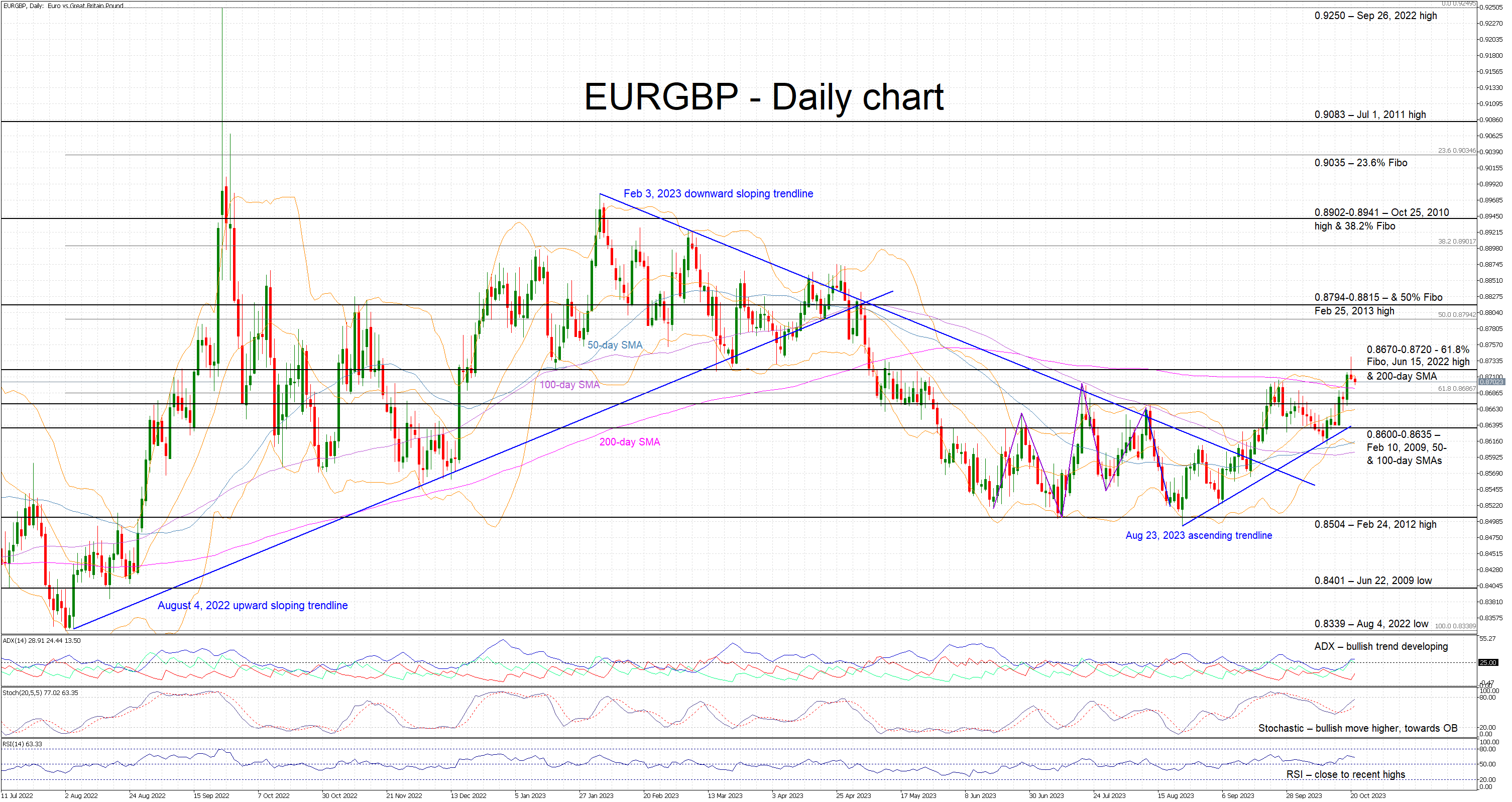

After being on the backfoot for most of 2023, the euro-pound pair has been moving along an ascending trend since the September lows, despite the ECB’s change of stance and weaker economic data releases. With the market expecting a balanced meeting, the recent newfound euro strength could get a real boost from a more hawkish ECB. This outcome could result in a rally towards the 0.8794-0.8815 area, opening the door for 0.9800 level. On the flip side, an eventless meeting could cause a smaller market reaction but potentially offer the excuse to the euro bears to stage a move towards the 0.8600 area.

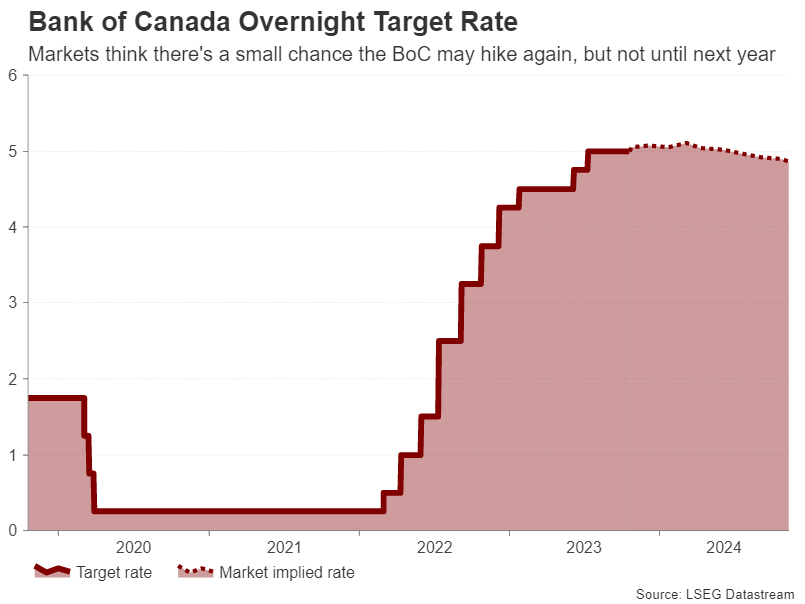

Bank of Canada to Likely Stay on Pause After Dip in Inflation

- BoC expected to hold rates at 5.0% after surprise fall in CPI

- But persisting wage pressures mean future hike not off the table

- Quarterly forecasts also eyed when decision is announced Wednesday, 12:30 GMT

No change in rates expected

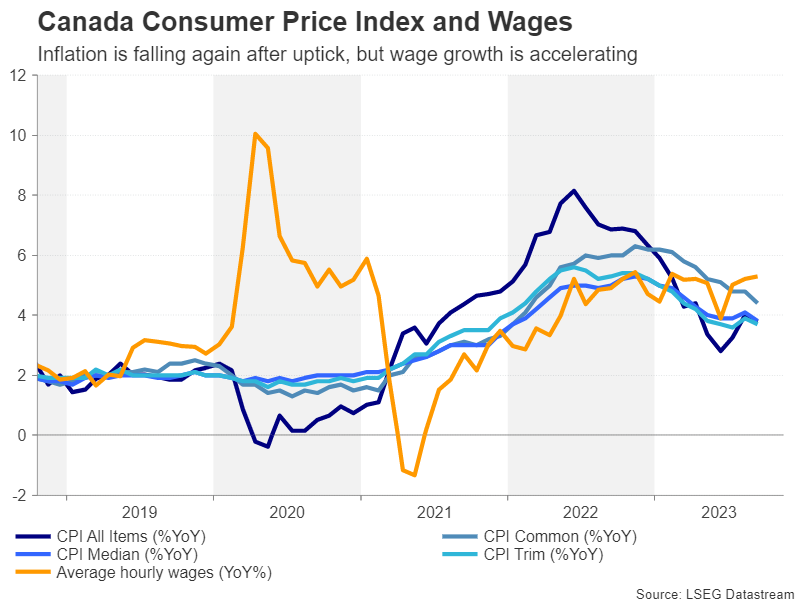

The Bank of Canada looks set to keep its overnight rate unchanged at 5.0% at its October meeting amid more sluggish-than-expected growth and signs that inflation is cooling off again. Rates in Canada last went up in July when headline inflation had started to creep up following the rise in oil prices. But the effects from higher energy costs appear to be dissipating as the consumer price index increased by less than expected in August.

For policymakers, however, their main focus is the underlying picture for inflation and the size of excess demand in the economy. On these two fronts, there is plenty of reason for the BoC to keep its guard up as far as the risk to inflation is concerned. Two measures of core inflation – CPI trim and CPI median – have been somewhat flat in recent months. The other core metric – CPI common – has been steadily falling all year, although it has come under scrutiny lately for its reliability. Thus, it’s too early to be able to judge from the inflation data alone that price pressures are well and truly contained.

Strong jobs market is supporting consumers

Aside from the stickiness in core inflation, the other thing troubling the BoC is that excess demand remains too high. GDP growth may have moderated from the strong levels seen at the beginning of the year, but consumption has stayed fairly robust on the back of a tight labour market. Despite a slight uptick in the jobless rate, the Canadian economy has created more than 100k jobs over the past two months, and more importantly, wage growth has been picking up, which is supportive of household spending.

In the July Monetary Policy Report, the Bank didn’t seem to be worried about wage pressures, but this was before the last two sets of upbeat jobs numbers. It’s likely that policymakers won’t sound quite so placid about wage risks in the October report as wage growth accelerated to 5.3% y/y in September. The July forecasts also saw inflation hitting the Bank’s 2% target in 2025. If the October projections are revised higher and CPI is anticipated to take longer to fall to 2%, that would leave the option of further rate hikes firmly on the table.

Additional rate hike not seen until March 2024

However, if there will be another rate increase, traders think this would be some time away as they’ve priced in only a 10% probability for the October meeting and the biggest distribution (around 35%) for a 25-basis-point move is currently assigned for March 2024.

As things stand, the softer-than-expected CPI report has bought the Bank of Canada some valuable time, allowing policymakers to assess the risks better amid the many uncertainties hanging over the outlook. The recent outbreak of violence in the Middle East has cast a shadow over the global economy, while domestically, high household debt remains a concern. The housing market is another potential headwind as the mini rebound enjoyed during the Spring appears to be over and home prices have started to head south again.

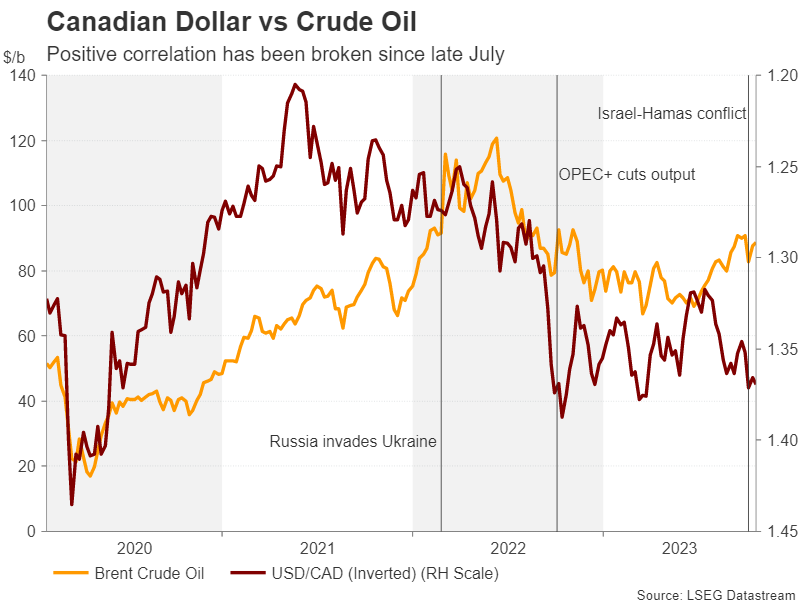

Loonie unable to reap rewards of oil rally

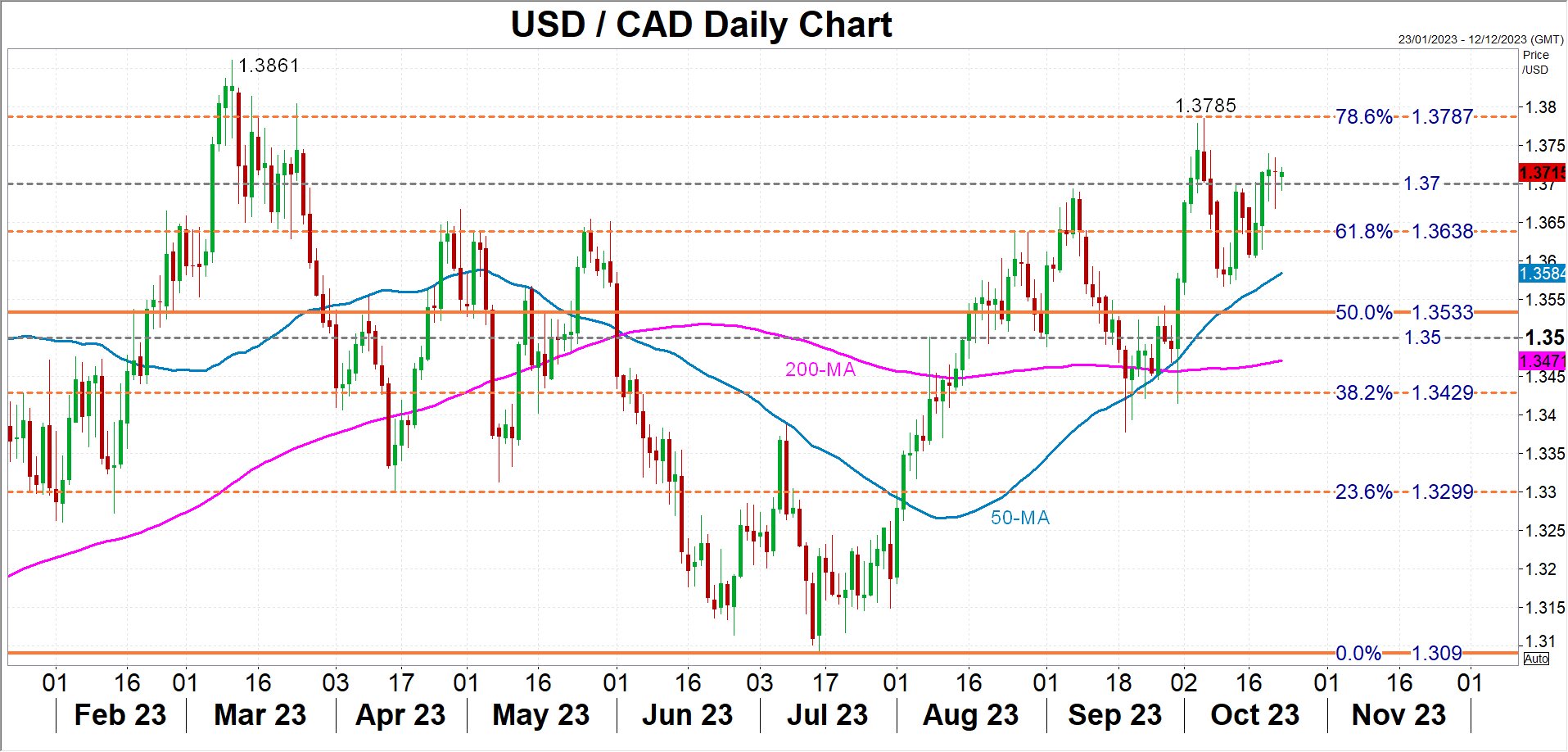

Nevertheless, the balance for monetary policy seems to be tilted towards further tightening as the rally in crude oil is a boost not only for energy prices and inflation but also for Canada’s own oil exports. A hawkish hold is therefore the most likely outcome on Wednesday, and this could positively affect the Canadian dollar.

In such a scenario, dollar/loonie could slip towards its 50-day moving average at 1.3584, with a test of the 1.3500 level possible if there is some added weakness in the greenback or a further spike in oil prices. However, if there is no tweak in the BoC’s language, dollar/loonie could edge up towards the October 5 top of 1.3785, which would then turn attention to the March 10 high of 1.3861.

It’s worth noting, though, that the loonie’s positive correlation with oil prices is sketchy at best and the relationship has been broken since late July. A more hawkish Fed is partly to blame for this, but the other factor is the increased risk aversion in the markets, which tends to work against risk-sensitive currencies like the loonie.

Bitcoin Has Approached a Critical Watershed

Market picture

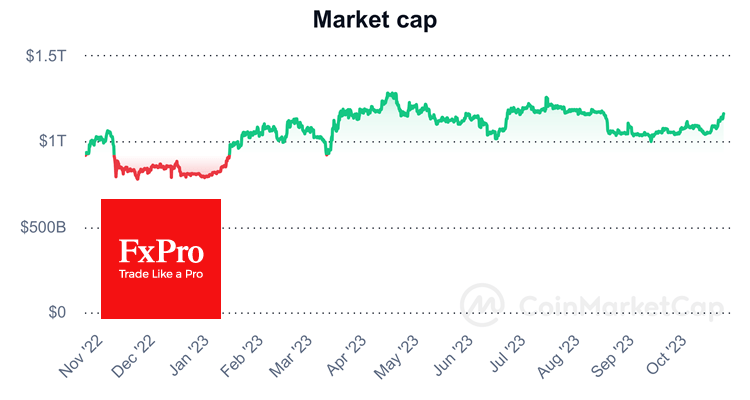

Over the past seven days, the crypto market has gained over 8.3%, bringing its capitalisation to $1.17 trillion, the highest since mid-August.

The market has reached a plateau where it stabilised from late June to mid-August. The dive back then was due to the spike in government bond yields, which suppressed global risk appetite.

This factor is no longer an obstacle and may even be playing into crypto’s hands. But we must warn that such a link can only work while the stock market’s retreat is relatively organised. A solid risk-off momentum will almost inevitably trigger institutional selling in crypto.

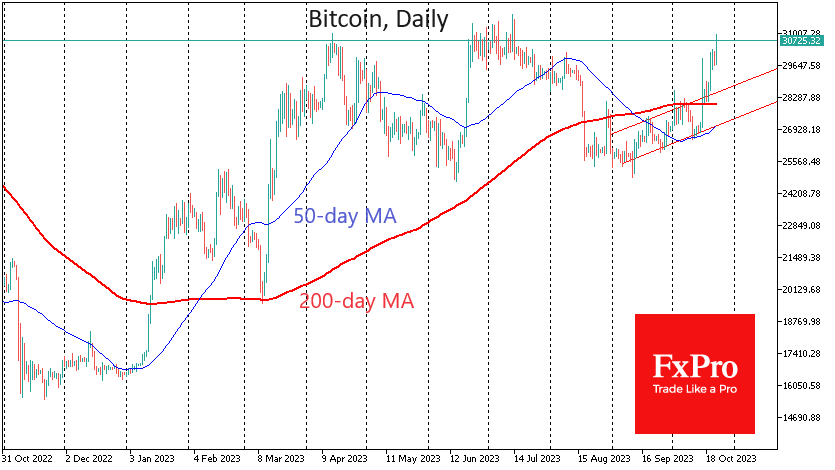

Bitcoin has gained over 10% in the last seven days, making the previous week the best in four months. On Monday morning, the price climbed to nearly $31K, close to highs not seen since July. This is a significant turning point. Bitcoin reversed from here in April and June, accelerating the sell-off in June 2022, but Bitcoin was actively bought back from these levels from January to July 2021. A consolidation above $31K could force the bears to capitulate and quickly send the price into the $40K area.

News Background

The crypto winter will soon be over, according to Morgan Stanley. The bull market could start as early as next year. The April halving should drive the new rally. However, there are also potential risks that could disrupt historical cycles, the bank warns.

It is doubtful that the crypto industry will flourish as long as there is a lack of liquidity in the market due to the high cost of money. The crypto spring will come, but only after a soft landing in the US, YouHodler believes.

According to Bloomberg, Grayscale and BlackRock have filed updated applications to launch a spot Bitcoin ETF.

The SEC has voluntarily dropped charges against Ripple CEO Brad Garlinghouse and co-founder Chris Larsen. Ripple Labs’ general counsel called the SEC’s action a capitulation.

Bitcoin Breaks Psychological Level of $30k

On Friday-Sunday, the price of BTC/USD several times exceeded the round level of 30,000, but the excess was short-lived; soon, the price rolled back down. But the pressure of the bulls did not weaken, and since the beginning of Monday, the price of bitcoin rose above 37,000.

A combination of bullish factors contributed to the rise in bitcoin prices:

→ the threat of a financial crisis in the USA. Congress without a speaker, the budget has not been approved, the S&P-500 is near its 5-month low. Legendary investor Peter Schiff expresses the opinion that a crisis is inevitable due to the actions of the Fed.

→ Expectations that the SEC will approve a bitcoin ETF in the near future, and this will open bitcoin to institutional investors. According to JPMorgan, this will happen within a few months. Positive signals will come from BlackRock and VanEck, which have filed bids.

→ Refusal by the SEC to claim against Ripple Labs.

→ Geopolitical tensions in the Middle East. Bitcoin is gaining relevance as an asset that can become a safe haven for capital.

The graph shows that:

→ the former resistance of 28,100 served as a support for a successful attack on USD 30k;

→ bitcoin price actions since mid-September have formed an ascending channel.

At the peak of the morning bullish momentum on October 23, the BTC/USD rate reached the upper limit of this ascending channel. From a short-term point of view, the price may roll back due to the activation of sellers in the area of the highs of the year and the upper border of the specified channel. But given the fundamental background, it is permissible to assume that the bulls are capable of new achievements.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Gold Pulls Back after Touching 2,000

- Gold surges to a 5-month high on geopolitical tensions

- Retreats slightly before claiming the 2,000 psychological mark

- Momentum indicators suggest overbought conditions

Gold has been in a steep uptrend after bouncing off its October low, jumping back above crucial technical regions such as the 200-day simple moving average (SMA) and posting a fresh five-month peak of 1,997. However, bullion experienced a minor correction due to reaching overbought levels.

Should buying interest persist, the July peak of 1,987 could initially curb bullion's upside. Conquering this barricade, the bulls might aim at the 1,997-2,000 range that is defined by the recent five-month high and the crucial psychological mark. A break above that territory could bring the April resistance of 2,032 under examination.

On the flipside, bearish actions could send the price lower to test the February high of 1,959, which could now act as support. Sliding beneath that floor, gold could challenge the June hurdle of 1,932 that overlaps with the 200-day SMA. Should that barricade also fail, the spotlight could turn to the September support of 1,901, which also held strong in June.

All in all, gold seems to be under relentless upside pressure, which has pushed the price in overbought levels. Although the short-term oscillators are hinting that the advance is overstretched, fresh geopolitical concerns may add more fuel to the latest rally.

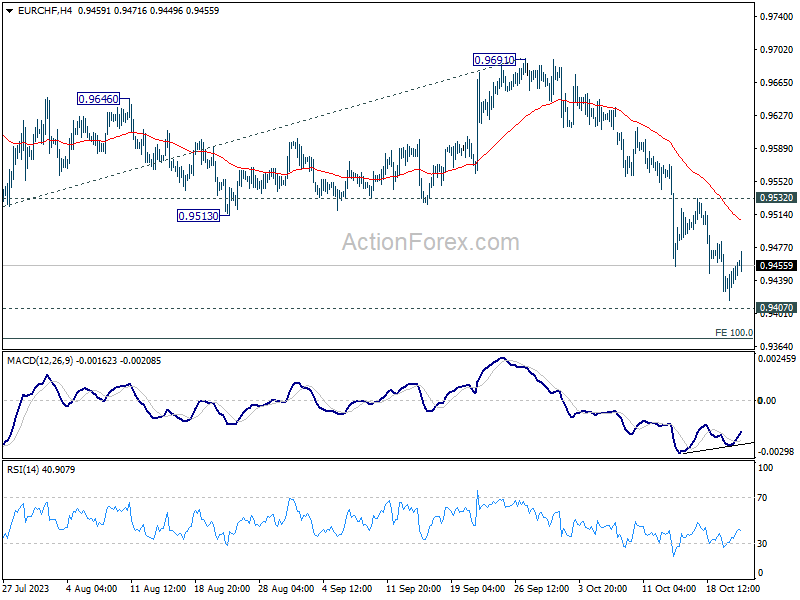

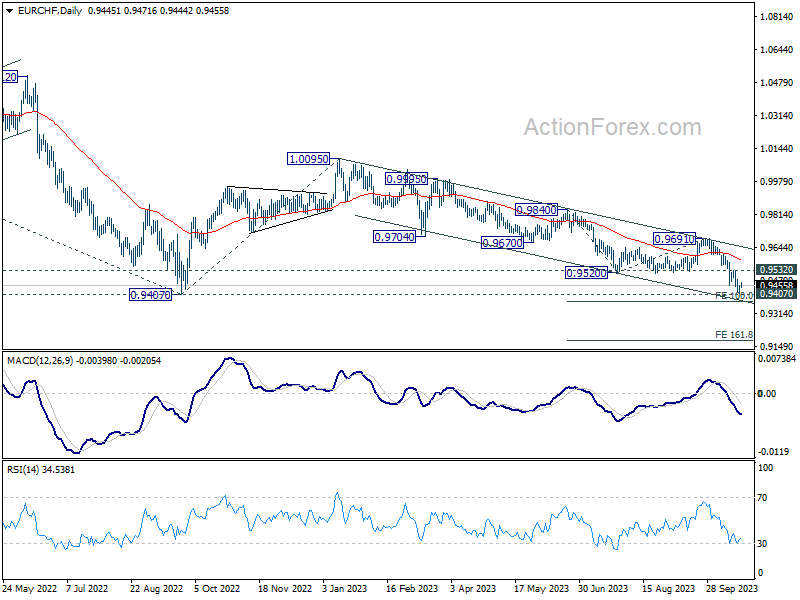

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9428; (P) 0.9443; (R1) 0.9467; More...

Intraday bias in EUR/CHF remains neutral for some more consolidations. But outlook stays bearish as long as 0.9532 resistance holds. On the downside, decisive break of 0.9407 medium term bottom will confirm resumption of larger down trend. Next near term target will be 100% projection of 0.9840 to 0.9520 from 0.9691 at 0.9499, and then 161.8% projection at 0.9179.

In the bigger picture, down trend from 1.2004 (2018 high) is still in progress. Decisive break of 0.9407 will confirm resumption, and target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. On the upside, break of 0.9691 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish.

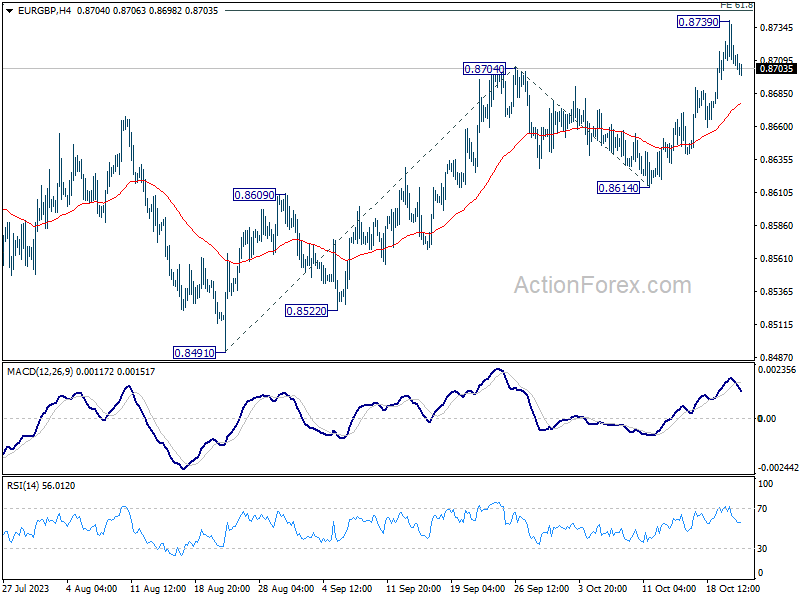

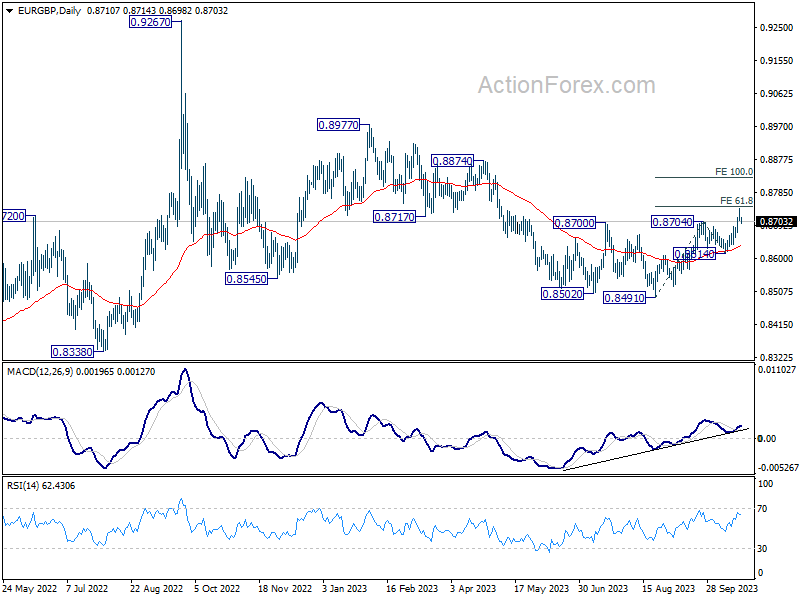

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8695; (P) 0.8717; (R1) 0.8732; More....

Intraday bias in EUR/GBP remains neutral at this point. Downside of retreat should be contained well above 0.8614 support to bring another rally. Firm break of 0.8746 will target 100% projection of 0.8491 to 0.8704 from 0.8614 at 0.8827 next.

In the bigger picture, current development suggests that whole down trend from 0.9267 (2022 high) has completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. This will now remain the favored case as long as 0.8614 support holds.

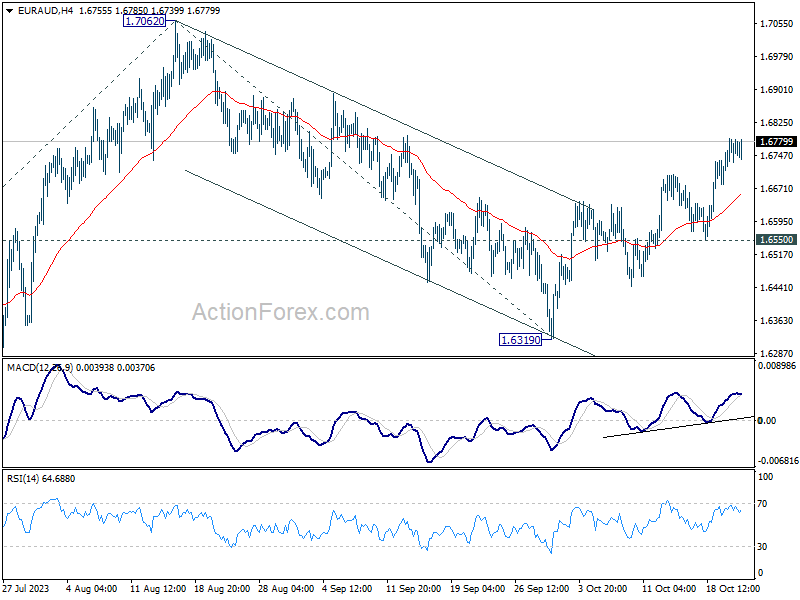

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6731; (P) 1.6762; (R1) 1.6807; More...

Intraday bias in EUR/AUD stays on the upside for retesting 1.7062 resistance. Decisive break there will confirm larger up trend resumption. Next target is 100% projection of 1.5846 to 1.7062 from 1.6319 at 1.7353. On the downside, break of 1.6550 support is needed to indicate completion of the rebound. Otherwise, near term outlook will stay mildly bullish even in case of retreat.

In the bigger picture, the strong support from medium term rising trend line indicates that rise from 1.4281 (2022 low) is still in progress. Sustained break of 1.7062 will pave the way to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. In any case, outlook will stay bullish as long as 1.6319 support holds.

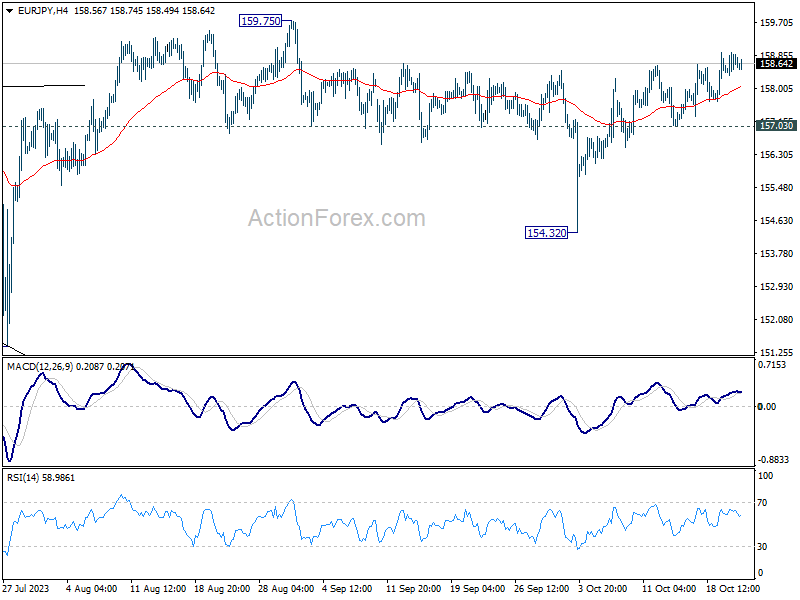

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.30; (P) 158.62; (R1) 159.05; More....

Intraday bias in EUR/JPY stays mildly on the upside for the moment. Further rise would be seen to retest 159.75 resistance. Decisive break there will resume larger up trend. On the downside, break of 157.03 support is needed to signal completion of the rebound. Otherwise, further rally will remain in favor in case of retreat.

In the bigger picture, price actions from 159.75 are views as a corrective pattern. As long as 151.39 support holds, rise from 114.42 (2020 low) is expected to continue through 159.75. Next target will be 100% projection of 124.37 to 148.38 from 139.05 at 163.06.