Sample Category Title

USD/CHF: Dollar Softens Despite Surge in Treasury Yields

- Safe-haven flows likely to head Swiss franc and gold’s way as US debt concerns and liquidity concerns grow

- A week filled with Fed speak will see Wall Street focus on Fed Chairman Jerome Powell’s speech on Thursday

- Empire Manufacturing contracted in October: -4.6 vs -6.0 eyed; Outlook for prices fell to a 3-year low

Something doesn’t seem right on Wall Street. The dollar is falling even as Treasury yields at the long-end of the curve surge as uncertainty persists on stickier inflation fears and rising debt levels. Much attention remains on the Israel-Hamas war, which is seeing diplomatic efforts try to prevent this war from expanding.

It is clear that the surge in commodities and rising default risks will drag down earnings expectations. It seems this is as ugly as earnings expectations are going to get. Despite efforts to prevent the Israel-Hamas war from spreading into the Middle East, Wall Street is hesitant to go full bull mode given the deteriorating profit outlook for this earnings season. Upside for stocks should be limited given all the geopolitical uncertainties.

US Data

The latest Empire Manufacturing survey showed activity returned to contraction territory. Both prices paid and received eased, supporting the case that the disinflation narrative is in place. The manufacturing sector is close to stabilizing, but for that to continue energy prices need to cool down. The upcoming week of economic data is expected to show the US economy is slowing. US retail sales are expected to show inflation and dwindling bank accounts led to softer consumption. Any upside surprises will be associated with strong back-to-school sales buying and the end of the peak summer travel season with Labor Day vacationing.

USD/CHF Daily Chart

Price action on the USD/CHF daily chart is breaking below two key support levels, the uptrend line that started in early August and below the 200-day SMA. King dollar might struggle for safe-haven flows against the franc. If Treasury market liquidity concerns remain the primary driver for the bond market, the franc could rally towards the 0.8600 level. Major upside resistance remains at the 0.9200 level.

BTC/USD: Bitcoin Volatile on False SEC Approval of ETF

- CoinGlass reported that $72 million worth of short positions were liquidated on the spike higher from the false SEC approval news

- US Government holds around 200,000 bitcoins, worth over $5 billion

- SEC refrains from asking court to change decision on Grayscale bitcoin ETF

Bitcoin’s surge above $30,000 quickly disappeared after Blackrock refuted earlier reports that the SEC approved their spot Bitcoin ETF. Cointelegraph earlier tweeted a Bitcoin ETF was approved and has since issued an apology and announced an internal investigation. Blackrock was quick to correct the misinformation on CNBC.

Bitcoin is still higher by 4.5% on the day as optimism remains that Bitcoin is still getting close to that elusive SEC spot Bitcoin approval. Bitcoin has been trapped in a frustrating range since the spring. Crypto adoption has struggled and competition from Central Bank Digital Currencies are growing.

British Pound Eyes UK Employment Release

- UK releases employment data on Tuesday

- BoE’s Bailey says rate decisions will be tight

The British pound has started the week in positive territory. In the European session, GBP/USD is trading at 1.2166, up 0.17%. The pound had a rough week, falling by 0.74% after a hotter-than-expected US inflation report saw the US dollar climb sharply.

It’s a busy week in the UK, with employment data on Tuesday, followed by inflation on Wednesday and retail sales on Friday. The Bank of England will be watching closely, with the inflation report being the key release of the three. The BoE meets next on November 2nd after pausing at the September meeting. The decision marked the first time after 14 consecutive rate increases that the BoE held rates. The move was a close call, with a 5-4 vote in the Monetary Committee Policy.

UK job growth, wages expected to ease

The BoE’s rate hikes have cooled the economy and job growth has dropped off sharply. Job creation fell by 207,000 in the three months to July, the sharpest job decline since September 2020. This sharp downtrend is expected to continue, with an estimate of a loss of 195,000 for the three months to August.

At the same time that job growth is falling, wage growth remains very strong. Average earnings including bonuses rose 8.5% y/y in the three months to July, and the market estimate for the three months to August stands at 8.3%. High wage growth is contributing to inflation, which currently stands at 6.7%. That figure is the lowest since February 2022 but is the highest in the G-7 and nowhere near the BoE’s 2% target.

Bank of England Governor Bailey said on Friday that future rate decisions would continue to be tight. The central bank is keeping its options open, and Deputy Governor Broadbent said last week that it was an “open question” whether the Bank would raise rates again. Broadbent noted that energy prices were dropping, which would likely inflation back to the 2% target by 2025. The issue facing Broadbent and his colleagues at the BoE is whether inflation will fall fast enough without any further hikes or will the BoE have to tighten further.

GBP/USD Technical

- GBP/USD is testing resistance at 1.2164. Above, there is resistance at 1.2202

- 1.2066 and 1.1973 are providing support

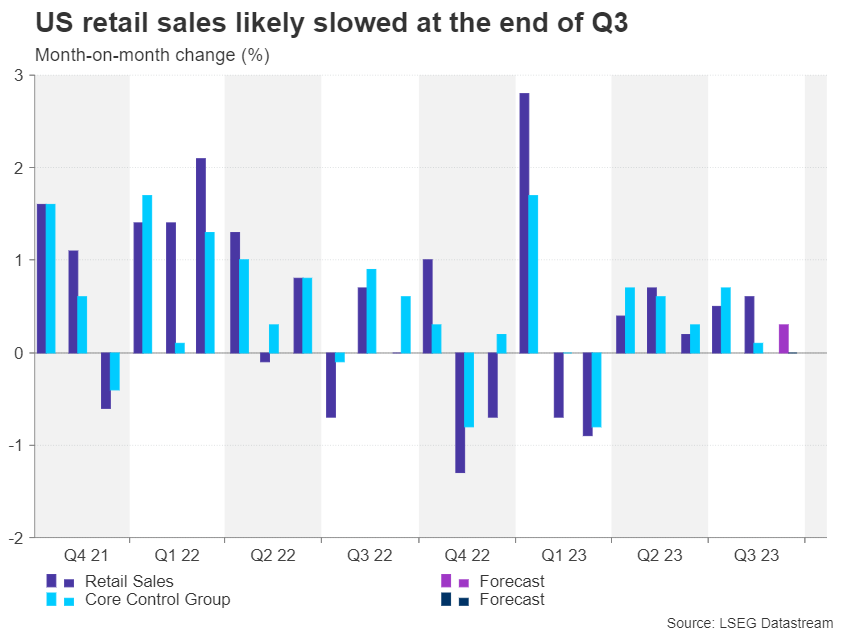

Dollar to Seek Direction from US Retail Sales as Yield Rally Stalls

- Retail sales in America likely grew at a more moderate pace in September

- Will the data support a Fed pause in November?

- Or will it fuel the rally in yields and the dollar when it’s out on Tuesday (12:30 GMT)

Is consumer spending starting to cool?

The US economy has been chugging along quite nicely in 2023 despite hitting several bumps on the road and Fed policy becoming more restrictive than what many investors had anticipated at the start of the year. The Atlanta Fed’s GDPNow forecast model is estimating third quarter growth of 5.1% - that’s well above the recent average of just above 2.0%.

Consumption has been the main driver of this exceptionally strong growth, which is unusual at this late stage of the tightening cycle. This week’s retail sales data will be key in gauging whether consumer spending kept up pace towards the end of the quarter.

After rising by 0.6% month-on-month in August, retail sales are forecast to have grown by a much more moderate pace of 0.3% in September. Excluding automobile sales, retail sales are expected to have edged up 0.2% m/m, while the core figure that strips out gasoline, building materials and food services in addition to autos is projected to have been flat in September, which would suggest households have started to tighten their belts.

Powell may have final say before Fed blackout

Slowing consumer spending isn’t the only risk to growth beyond the third quarter. The possibility of a government shutdown, ongoing strike action and tightening financial conditions could all weigh on growth in the final three months of the year.

The latest round of selloff in US Treasuries and other government bonds has led to a significant tightening in financial conditions, as long-term Treasury yields have surged to pre-financial crisis era levels. More importantly, this hasn’t gone unnoticed at the Fed and officials appear to all be in agreement with one another that the jump in long-term borrowing costs since the last FOMC meeting in September broadly amounts to an equivalent 25-basis-point rate hike.

However, investors have yet to hear from the Fed chief himself, so Jay Powell’s address on Thursday before the Economic Club of New York could be crucial. Powell may well use his speech to guide market expectations before the blackout period for the October 31-November 1 meeting begins at the weekend.

Dollar might shrug off retail sales data

For the markets, the retail sales numbers are not expected to be a game changer as the odds of a November rate hike are virtually zero. However, a stronger-than-expected report on the back of the solid payrolls and CPI readings could nevertheless bolster the case for a December move, or at the very least, lead investors to scale back some of their aggressive bets for rate cuts in 2024.

Any fresh boost for the US dollar could push the euro towards the $1.04 level, which marks the 50% Fibonacci retracement of the September 2022-July 2023 uptrend.

But if retail sales disappoint or Powell endorses his colleagues’ views and signals that interest rates have likely peaked, the euro could easily rebound towards its 50-day moving average just above the $1.07 handle.

Safe-haven support for the greenback

Investors should be wary, though, not to completely rule out the chance of another rate hike as a Fed pause is conditional on the 10-year yield remaining elevated near 5.0%, while the Israel-Gaza war is seen as maintaining upside risks to inflation, with oil prices already lifted by the conflict.

The latter even has a two-sided effect on the greenback as it’s generating demand for safe havens. Any pullback in yields might therefore not spark a proportionately sized selloff in the dollar as long as geopolitical tensions are brewing.

Sunset Market Commentary

Markets

Indications that Israel was about to bring boots on the ground in Gaza (City) unsettled markets last Friday as they went into a weekend full of geopolitical uncertainty. Israel eventually didn’t pull the trigger, officially because of the bad weather forecast. Diplomacy, meanwhile, shifted into higher gear over the past few days with the US taking the lead. They are keen to avoid the regional spat to escalate into a wider one that may involve the likes of Iran. It’s enough to bring back some calm to financial markets for the time being, if anything because there was little other news to turn attention to. Stocks in the Asian-Pacific area endured some selling pressure still but equities in Europe stabilized (EuroStoxx50 +0.2%) after sliding about 1.5% end last week. Wall Street opens with gains up to 0.7% (Dow Jones). The rally in oil (supply fears) halted while the one in gold even went marginally in reverse (-0.5%). Core bonds fell with US Treasuries underperforming Bunds. US yields added up to 8.4 bps at the longest maturities. German rates rose between 0.8-4.9 bps, making the curve a bit less inverse. Peripheral yield spreads vs Germany’s 10y yield ease a few bps. Italy’s (credit) risk premium remains above 200 bps though. Italian central bank and ECB governing council member on Friday said that the current increase doesn’t require an ECB response (through its TPI facility), meaning he thinks it’s justified considering the country’s fundamentals. Italian PM Meloni’s cabinet today agreed on the new budget law which won’t bring the deficit not below the 3% threshold until 2026, year later than previously planned and the reason why spreads, particularly in Italy, started rising sharply.

Dovetailing with risk appetite increasing at the start of the week, the US dollar is losing a few ticks against most peers. DXY drops from 106.648 to 106.4. EUR/USD rises from 1.0507 at the open to 1.054, around today’s highest. The greenback even loses marginally against the yen. USD/JPY is filling offers at 149.43. In the G10 zone, the Swedish krone is outperforming. EUR/SEK slips towards 11.53. The Polish zloty in Central-Europe gets a significant boost from the election victory for the pro-European opposition parties, led by former prime minister Tusk. Even the Hungarian forint profits a little. Poland under the outgoing PiS government has consistently vetoed the EU’s vote-stripping rule-of-law procedure against Hungary (and vice versa). Losing his key ally, investors assume premier Orban now to dial back his staunch opposition. It’s a long shot but in the end it could lead to the long-awaited disbursement of billions of locked-up European funds. Sterling stabilizes around EUR/GBP 0.865 as it goes into an interesting economic update later this week. Tomorrow’s labour market report serves as the kick-off.

News & Views

Polish core inflation (net of food and energy prices) fell by 0.1% M/M in September while markets expected a stabilization. The Y/Y-figure fell from 10% to 8.4% (vs 8.6% forecast). Inflation excluding administered prices fell by 0.5% M/M to 6.8% Y/Y (from 8.9%). The so-called 15% trimmed mean (excluding the impact of 15% of the price basket characterized by the highest and lowest growth rates) was running at 9.3% Y/Y (from 11%). The Polish zloty doesn’t react to today’s inflation numbers, being up around 1.5% against the euro (EUR/PLN 4.47) following this weekend’s parliamentary election which resulted in an opposition victory for pro-EU parties rallied around ex-PM Tusk’s Civic Platform.

The NY Fed’s Empire Manufacturing Survey fell from 1.9 to -4.6 in October (vs -6 expected). New orders (-4.2 from 5.1) fell slightly, just like shipments (1.4 from 12.4). Unfilled orders declined (-19.2 from -5.2), and delivery times (-6.4 from 2.1) shortened. Inventories (-2.1 from -6.2) held broadly steady. Labor market indicators pointed to a slight increase in both employment (3.1 from -2.7) and the average workweek (2.2 from -5). The pace of input price increases was similar to last month (25.5 from 25.8), while selling price increases moderated (11.7 from 19.6). Looking ahead, firms remained relatively optimistic about the six-month outlook (23.1 from 26.3).

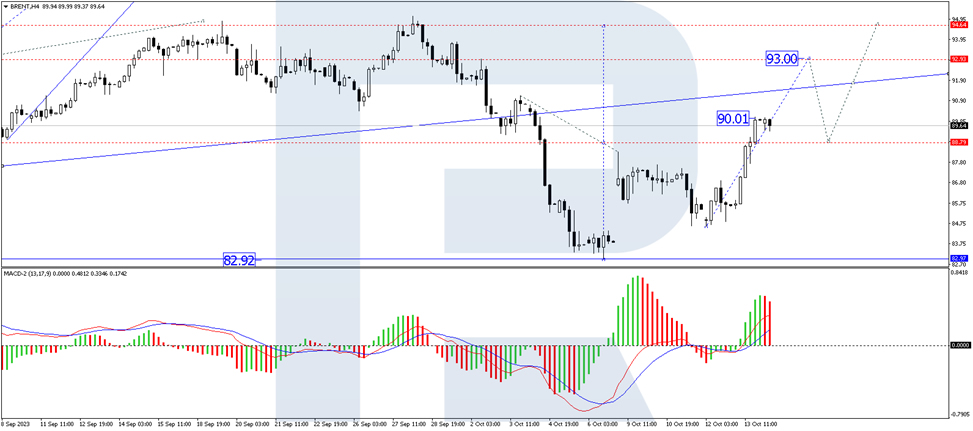

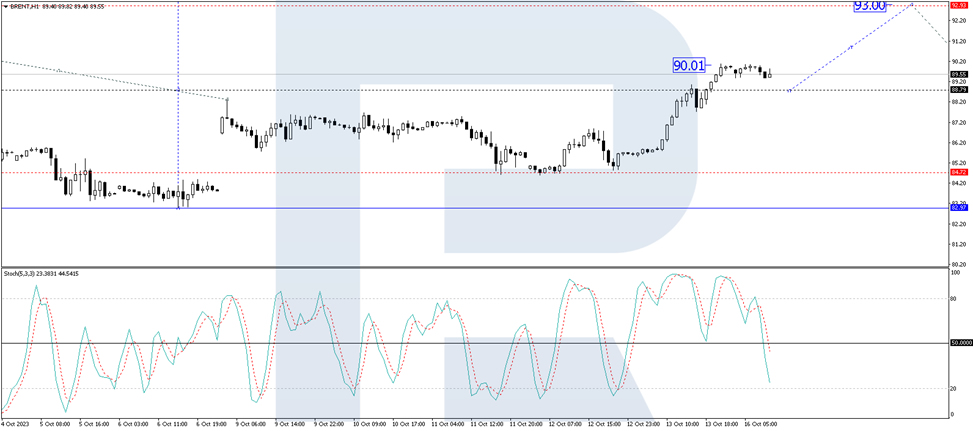

Technical analysis: Brent Returns to a Rally

The crude oil market continues the buying momentum it started on Friday. As we begin this new week of October, the price of a Brent barrel has reached 91.00 USD.

The risk of an escalation in the conflict in the Middle East has noticeably increased, but commodity prices are in no hurry to correct. This means that the market sees a relatively high likelihood of complications.

Earlier forecasts from OPEC, the US Ministry of Energy, and the IEA had indicated moderate optimism about fuel demand in 2024. However, current expectations have become even more conservative.

The current price levels for crude oil seem justified, given the global risks.

Brent technical analysis

On the Brent H4 chart, prices have made a movement to 90.00 within a wave of growth. Today, the market is correcting to 89.00. Once this level is reached, a new upward wave to 93.00 could begin. This is a local target. Next, a correction to 89.00 might start (with a test from above), followed by growth to 95.00. Technically, this scenario is confirmed by the MACD, with its signal line above zero, firmly pointing upwards. The indicator is expected to reach new highs.

On the Brent H1 chart, prices have risen to 90.00. A corrective movement to 88.80 is forming today. A decline to 88.00 is not excluded. Next, a wave of growth to 90.00 might begin. Technically, this scenario is confirmed by the Stochastic oscillator, with its signal line currently pointing firmly downwards to 20. Next, it is expected to rise to 50, break this level, and reach the 80 mark.

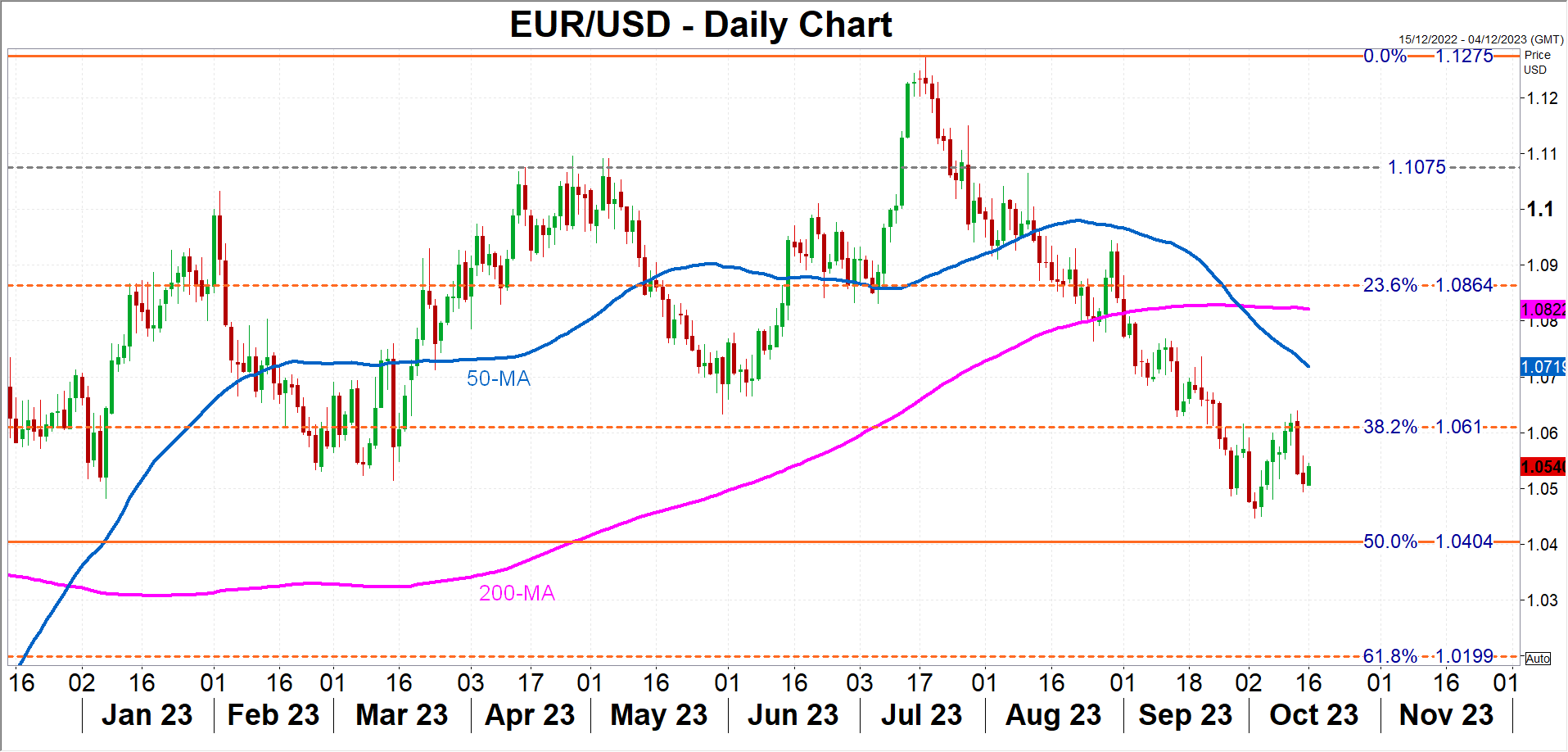

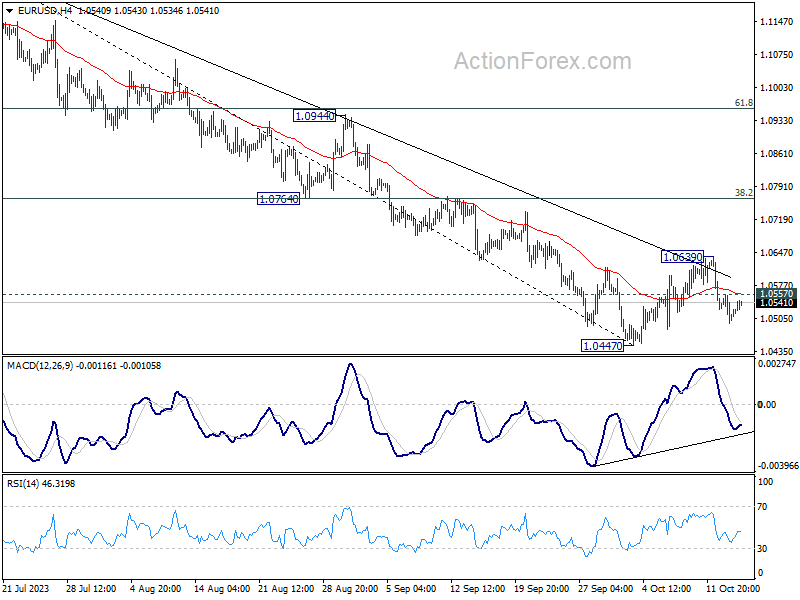

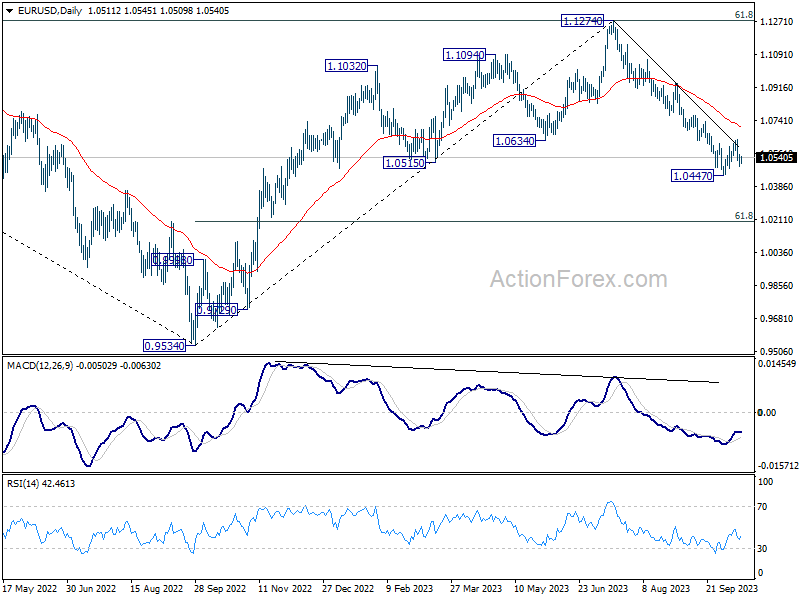

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0483; (P) 1.0521; (R1) 1.0545; More...

With 1.0557 minor resistance intact, intraday bias in EUR/USD stays mildly on the downside. Deeper fall would be seen to retest 1.0447. Firm break there will resume whole fall from 1.1274 and target 1.0199 fibonacci level. On the upside, above 1.0557 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.0639 resistance holds.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0708) holds, in case of rebound.

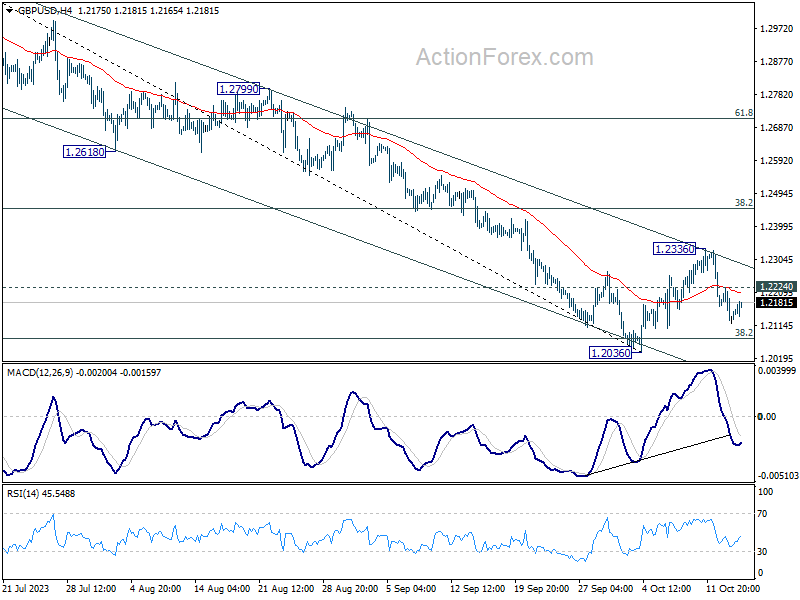

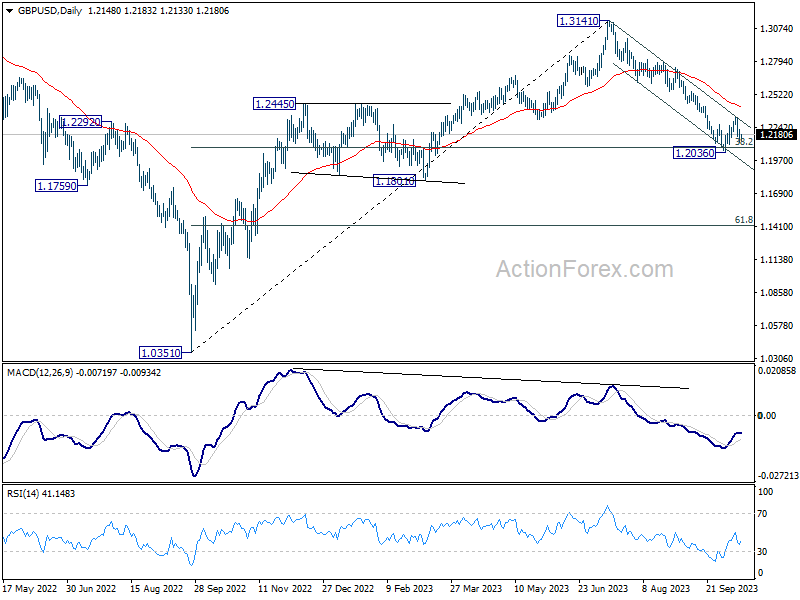

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2104; (P) 1.2164; (R1) 1.2206; More

With 1.2224 minor resistance intact, intraday bias in GBP/USD stays mildly on the downside. Deeper fall would be seen to retest 1.2036 low. Firm break will resume whole decline from 1.3141 for 1.1801 support next. On the upside, above 1.2224 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.2336 resistance holds.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2418) holds, in case of rebound.

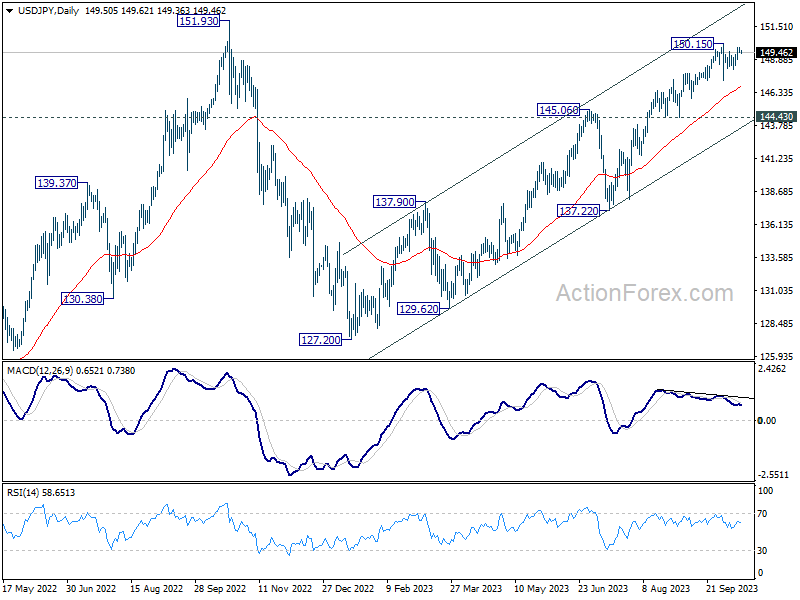

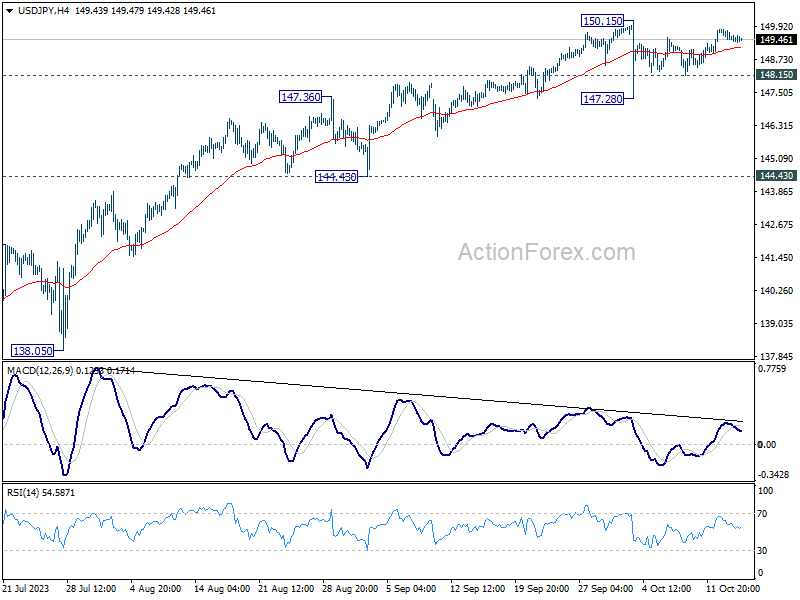

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.41; (P) 149.62; (R1) 149.79; More...

USD/JPY is still bounded in consolidation from 150.15 and intraday bias remains neutral for the moment. On the downside, below 148.24 minor support will turn bias to the downside for another down leg through 147.28. On the upside, firm break of 150.15 will resume larger up trend to test 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.