Sample Category Title

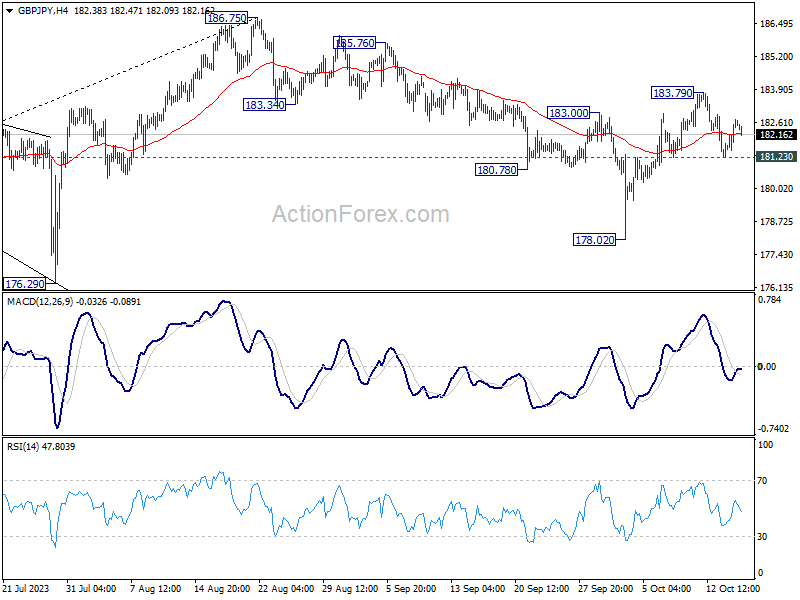

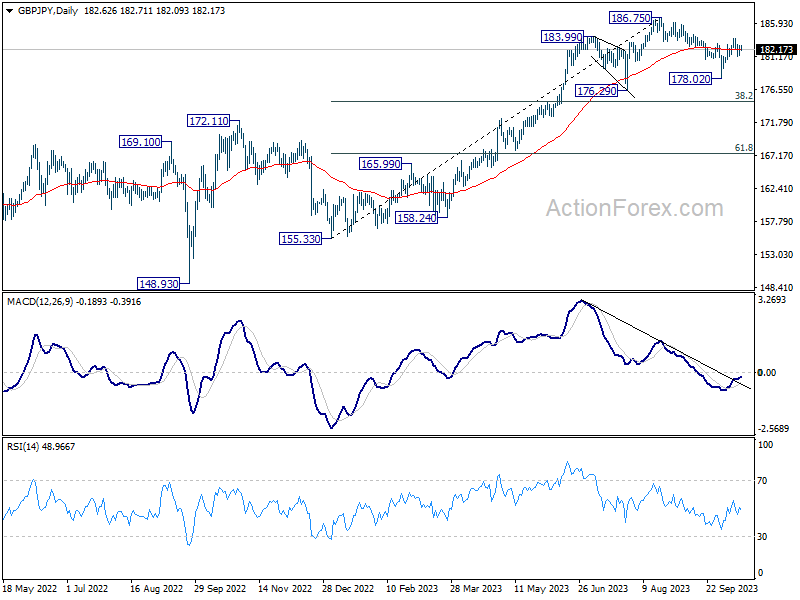

GBP/JPY Daily Outlook

Daily Pivots: (S1) 181.71; (P) 182.22; (R1) 183.19; More...

Intraday bias in GBP/JPY remains neutral and outlook is unchanged. The favored case is still that correction from 186.75 has completed at 178.02. Above 183.79 will resume the rise from 178.02 to retest 186.75 high. However, break of 181.23 will dampen this view, and turn bias back to the downside for 178.02 instead.

In the bigger picture, fall from 186.75 is seen as a corrective move only. As long as 176.29 support holds, larger up trend from 123.94 (202 low) should still be in progress. Break of 186.75 will target 195.86 (2015 high). Nevertheless, firm break of 176.29 will confirm medium term topping, and bring lengthier and deeper consolidations.

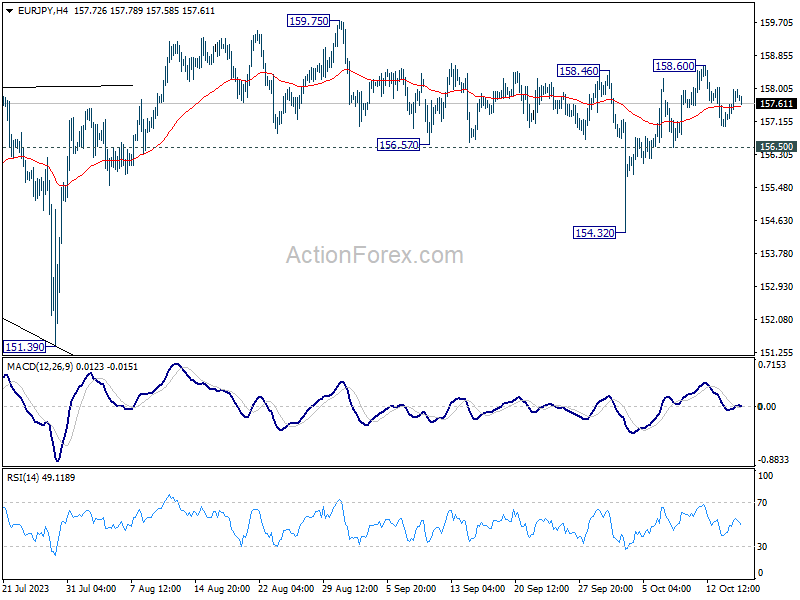

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.28; (P) 157.63; (R1) 158.24; More....

Intraday bias in EUR/JPY stays neutral for the moment and outlook is unchanged. The favored case is still that correction from 159.75 has completed at 154.32. Above 158.60 will resume the rise from 154.32 and target 159.75 high. However, break of 156.50 will dampen this view, and bring another fall to extend the corrective pattern from 159.75.

In the bigger picture, price actions from 159.75 are views as a corrective pattern. As long as 151.39 support holds, rise from 114.42 (2020 low) is expected to continue through 159.75 at a later stage. Nevertheless, firm break of 151.39 will confirm medium term topping, and bring lengthier and deeper correction.

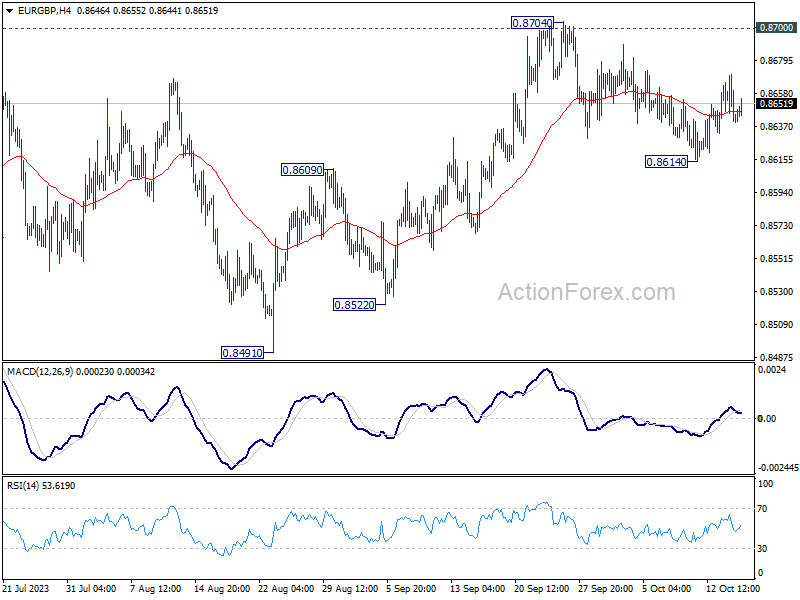

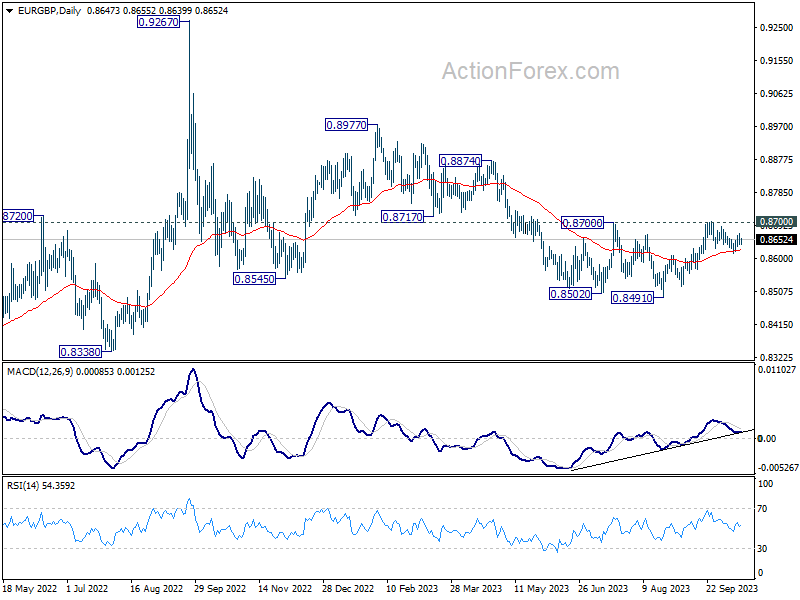

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8632; (P) 0.8652; (R1) 0.8663; More....

Intraday bias in EUR/GBP is turned neutral with current retreat. On the upside, decisive break of 0.8700/4 resistance will resume the rebound from 0.8491, and carry larger bullish implications. Nevertheless, break of 0.8614 will turn bias to the downside to resume the fall from 0.8704 instead.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Decisive break of 0.8700 resistance will argue that this decline has completed with three waves down to 0.8491. Rise from 0.8491 could then be another leg inside the pattern and targets 0.8977 and above. However, rejection by 0.8700 will keep the down trend alive for another fall through 0.8491 at a later stage.

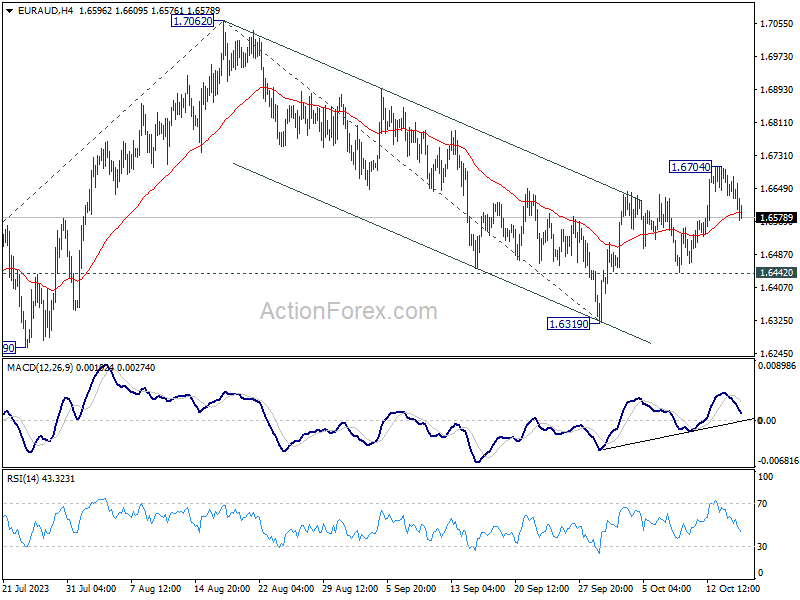

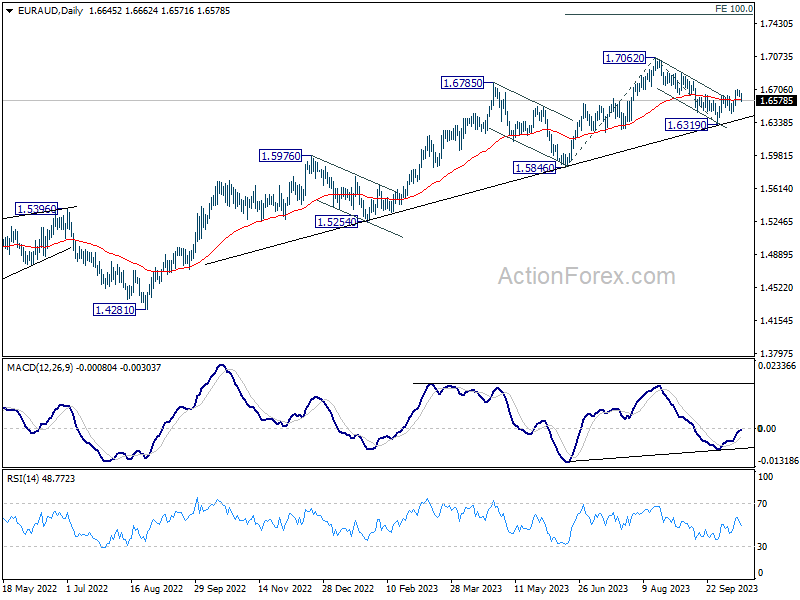

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6619; (P) 1.6659; (R1) 1.6689; More...

Intraday bias in EUR/AUD remains neutral for the moment. Outlook is unchanged that correction from 1.7062 has completed at 1.6319. Above 1.6704 will resume the rise from 1.6319 to retest 1.7062 high. However, firm break of 1.6442 will dampen this view and turn bias back to the downside for 1.6319 support instead.

In the bigger picture, the strong support from medium term rising trend line indicates that rise from 1.4281 (2022 low) is still in progress. On resumption, next target is 100% projection of 1.5846 to 1.7062 from 1.6319 at 1.7353. In any case, outlook will stay bullish as long as 1.6319 support holds.

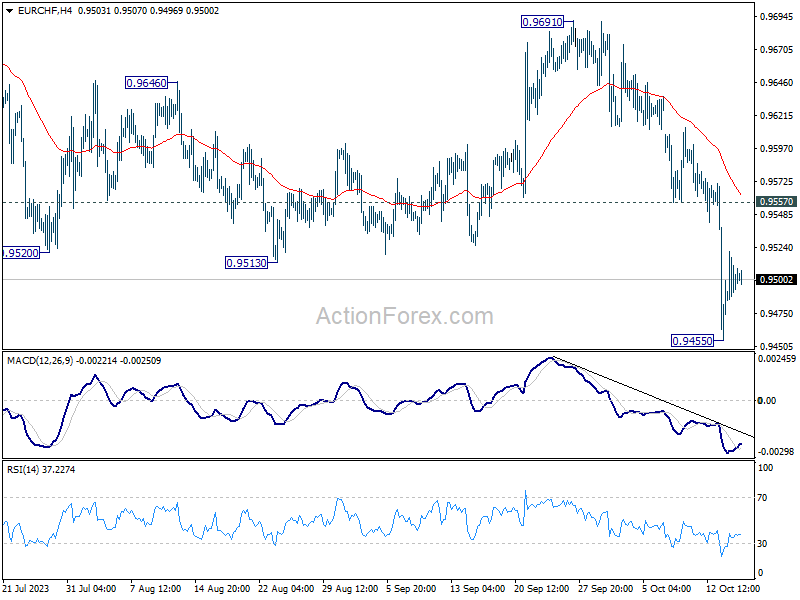

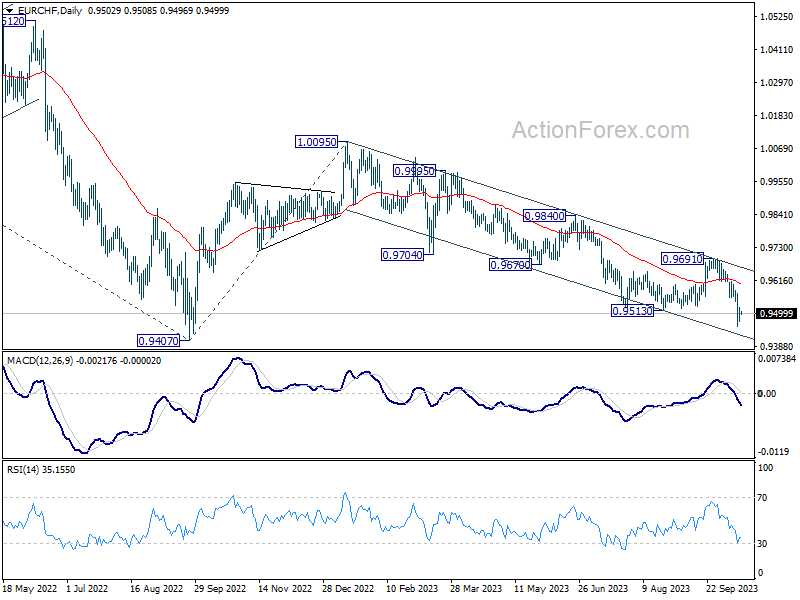

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9482; (P) 0.9502; (R1) 0.9526; More...

Intraday bias in EUR/CHF is turned neutral as consolidation from 0.9455 is extending. Further decline is expected with 0.9557 resistance intact. Below 0.9455 will resume larger decline from 1.0095 to 0.9407 medium term bottom. Nevertheless, break of 0.9557 will indicate short term bottoming and bring stronger rebound.

In the bigger picture, medium term outlook remains bearish with the cross capped well below falling 55 W EMA (now at 0.9782). Firm break of 0.9407 (2022 low) will confirm resumption of larger down trend from 1.2004 (2018 high). Next target will be 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. On the upside, break of 0.9691 resistance is needed to indicate medium term bottoming. Otherwise, outlook will stay bearish.

De-escalation Narrative Could Still Color Trading Today

Markets

Markets kicked off the week in good spirits. Betting on a US led de-escalation of the conflict in the Middle East, stocks bounced 0.3% in Europe and up to 1.2% in the US (Nasdaq). Core bonds pared last week’s gains, pushing yields in the US 4.3 to 10.5 bps higher with the long end underperforming. Germany followed by adding 1.7-6.6 bps in a similar curve shift. ECB’s Lane in an interview published after-market said the central bank must be open to further action if new shocks emerge that are sufficiently large or persistent. He added that rate cuts are still “quite some distance” from now. FOMC voting member Harker repeated his preference for keeping rates steady for a while at the current elevated levels. Both oil (on supply fears) and gold (safe haven flows) took a breather from Friday’s surge. The US dollar was sold against all majors. DXY fell from 106.579 to 106.243. EUR/USD added half a big figure to close at the day’s highest at 1.056. Sterling settled back above GBP/USD 1.22 with some minor knock-on effects on EUR/GBP (slightly lower close, at 0.8643). BoE chief economist Pill in a speech kept a balanced tone between not being complacent but wanting to avoid overtightening as much of the rate increases still have to pass through.

Asian stock markets copy paste WS’s performance. South Korea (+1.1%) outperforms in a quiet trading session. The kiwi dollar risks losing NZD/USD 0.59 on weaker-than-expected Q3 inflation (see headline below). The Aussie counterpart enjoys some bids following minutes from the previous RBA meeting. They included a new phrase which states that the RBA has a low tolerance for a slower return to the inflation target than currently expected. AUD/USD rises to 0.6354 though gains were bigger earlier. The US dollar is in a slightly better place than yesterday. Core bonds extend Monday’s decline with US cash yields in many cases already back above the levels prior to Friday.

We think the de-escalation narrative could still color trading today, keeping (long-term) yields on an upward path within their sideways trading ranges. The upper bound is capped at 3.02% in Germany and 4.88% in the US (10-y). A gentle risk-on mood is usually USD-negative but it being this fragile we don’t expect it to weigh (substantially) on the greenback. The economic calendar contains US retail sales. Barring a major downside surprise it shouldn’t interfere with the current market trends. This morning’s UK’s labour market report was an incomplete one with official employment growth and unemployment rates only due by next week. For now, we only see wages (ex-bonus) growing bang in line with expectations (7.8% y/y in the three months through August) and an early September employment growth gauge missing expectations (-11k vs +3k expected with the previous figure revised downwards). Sterling erased a kneejerk move lower to trade unchanged around EUR/GBP 0.865 in a first reaction.

News and Views

Inflation in New Zealand printed softer than expected in Q3 even as the pace of quarterly price rises accelerated and inflation remains well above the 1-3% target of the Reserve Bank of New Zealand. Headline CPI rose 1.8% Q/Q, reducing the Y/Y measure from 6.0% to 5.6%. Tradable goods inflation rose 1.8% Q/Q and 4.7% Y/Y (from 5.2%). Prices of non-tradables increased 1.7% M/M and 6.3% (down from 6.6%). Transportations costs jumped 7.1% Q/Q and contributed almost 1 ppt to the monthly rise. Housing and utilities costs rose 1.7% Q/Q. Prices of recreation and culture were 0.8% higher compared to the previous quarter. Healthcare costs declined 1.0% Q/Q while food prices gained 0.9% Q/Q. The 5.6% Y/Y inflation marked the lowest level since Q3 2021 and was also below the RBNZ expectation for inflation around 6.0%. The RBNZ at its early October policy meeting kept its policy rate unchanged at 5.5%. Markets after the publication of the data reduced expectations for a potential final rate hike at the November meeting to below 20%. The 2-y government bond yield declined 3.2 bps to 5.6%. NZD/USD declined from the 59.3 area to currently 59.00.

In interview at the IMF and World Bank annual meeting in Marrakech covered by the Financial Times, French finance Minister Lemaire was quoted that France was prepared to step up spending cuts and to pursue further structural reforms as rising bond yields are forcing governments to reduce deficits. In concreto, Le Maire indicated that he would try to add €1 bln of extra spending cuts in addition to the €16 bln of measures that were already set out in the 2024 budget proposal last month. The 2024 budget sees a deficit of 4.4% GDP and the deficit is only expected to fall below the EU’s 3.0% target by 2027.

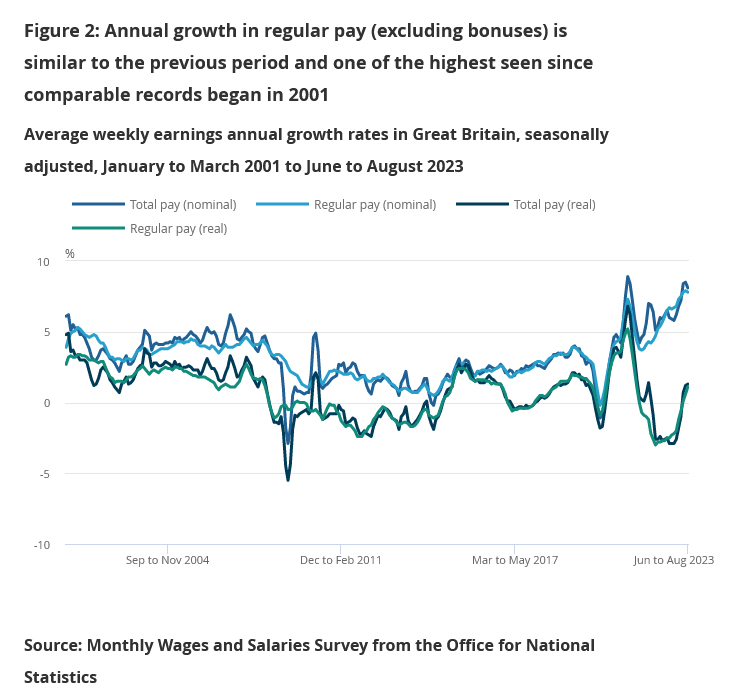

UK regular pay growth matches expectations at 7.8%

UK's annual growth in regular pay, excluding bonuses, stood in line with market expectations, clocking in at 7.8% in the three months to August. However, when accounting for bonuses, the total pay's annual growth was slightly tepid at 8.1%, missing the market forecast of 8.3%.

When adjusted for inflation using CPI including owner occupiers' housing costs (CPIH) - the real terms annual growth showcased a rise of 1.3% for total pay from June to August. Similarly, the regular pay's real terms annual growth registered a 1.1% increase.

A sector-wise dissection revealed that finance and business services led the pack with the most robust annual regular growth rate at 9.6%. Manufacturing sector followed closely with an impressive 8.0% growth rate. This surge in the manufacturing sector's pay growth is noteworthy, marking one of its highest annual regular growth rates since the inception of comparable records in 2001.

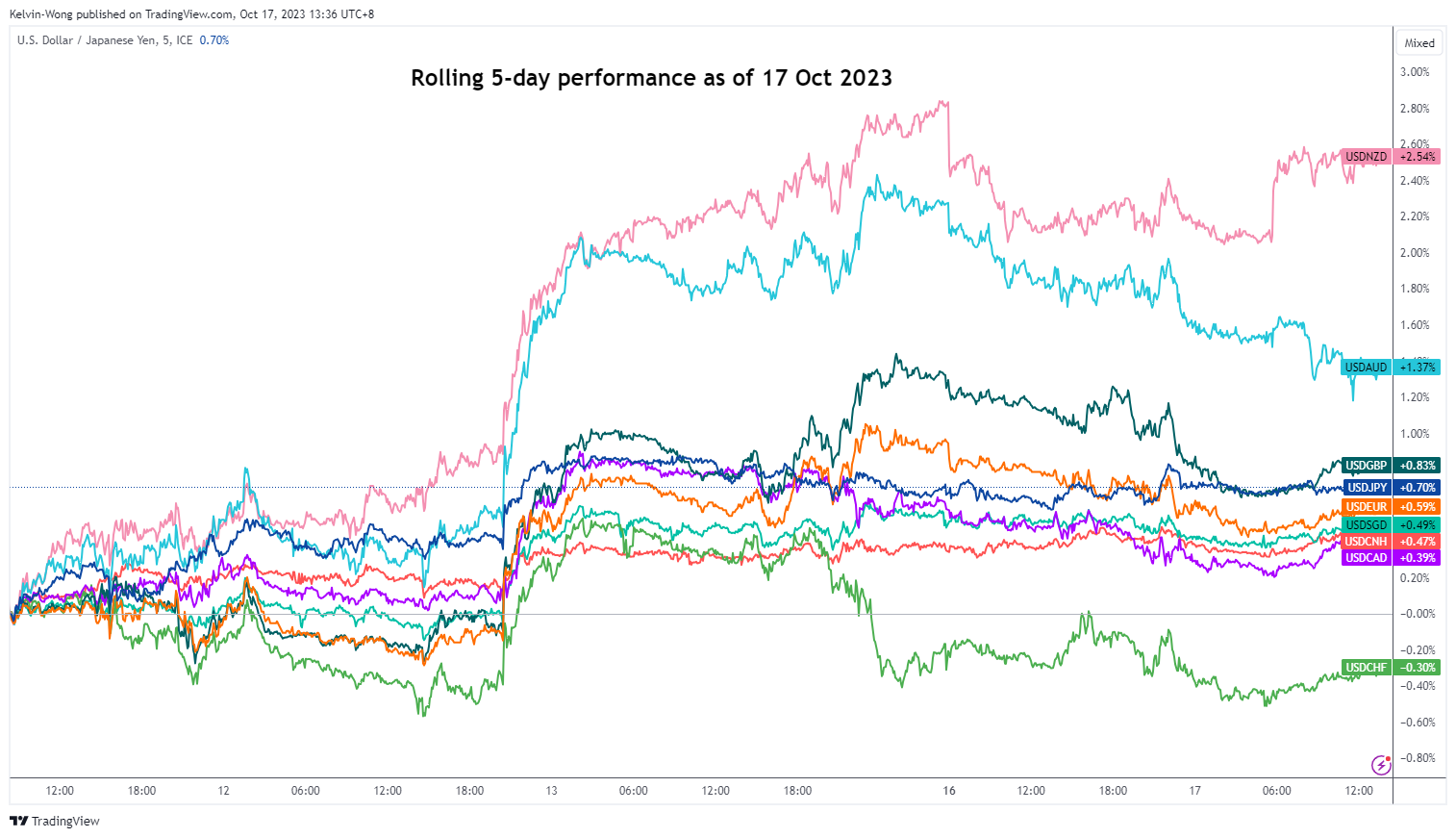

EUR/NZD Technical – Start of a New Potential Bullish Impulsive Up Move

- The Kiwi dollar (NZD) has been the worst performer among the US dollar major pairs in the past five days.

- A further slowdown in New Zealand’s Q3 CPI (5.6% y/y versus 6% y/y in Q2) reinforces RBNZ’s current stance of maintaining its key policy official cash rate unchanged at 5.5%.

- A less hawkish RBNZ may put further downside pressure on the NZD that supports an ongoing major uptrend phase in the EUR/NZD cross pair.

- Watch the 1.7820 key short-term pivotal support on the EUR/NZD.

The Kiwi dollar (NZD) has been the weakest performer among the US dollar major pairs ex-post New Zealand’s general election held over the weekend which saw a change in government towards the centre-right National Party.

Fig 1: USD major pairs rolling 5-day performance as of 17 Oct 2023 (Source: TradingView, click to enlarge chart)

Based on a 5-day rolling performance basis as of 17 October 2023, the USD/NZD has recorded a gain of +2.5% at this time of the writing reinforced by a slowdown in inflationary pressures in New Zealand where its Q3 consumer inflation rate released today inched down to 5.6% y/y from 6% y/y in Q2 and below consensus expectations of 5.9% y/y.

This latest set of CPI data marks the third consecutive quarter of inflationary pressures cooldown from a 22-year high of 7.3% y/y printed in Q2 2022 that supports New Zealand’s central bank, RBNZ current stance of keeping the official cash rate unchanged at 5.5% for a period of time, so far it has held the policy rate steady for three consecutive monetary policy meetings with next upcoming meeting on 29 November.

The ongoing weak performance of the USD/NZD against other US dollar major pairs has led to a resurgence of bullish impulsive sequences in several variable quoted NZD cross pairs such as the EUR/NZD.

Bullish reversal right at major ascending channel support

Fig 2: EUR/NZD major & medium-term trends as of 17 Oct 2023 (Source: TradingView, click to enlarge chart)

The 7-week of corrective decline seen in the EUR/NZD cross pair from its 21 August 2023 high of 1.8462 to its recent 10 October 2023 low of 1.7508 is likely to have ended where price actions staged a significant bullish reversal of + 336 pips in a span of five days right at a key medium-term support of 1.7510 that confluences with the key upward sloping 200-day moving average and the lower boundary of the major ascending channel in place since 12 April 2022 low of 1.5880.

In conjunction, the daily RSI indicator flashed a prior bullish divergence condition at its overbought region on 9 October and now inched higher above the 50 level. These observations suggest the potential revival of medium-term bullish momentum where price actions of the EUR/NZD may kick start of fresh multi-week bullish impulsive up move sequence within its major uptrend phase that is still intact since the April 2022 low of 1.5594.

Cleared above 20-day moving average

Fig 3: EUR/NZD minor short-term trend as of 17 Oct 2023 (Source: TradingView, click to enlarge chart)

The EUR/NZD has also cleared above its 20-day moving average and retested it yesterday, 16 October before it inched up to print a “higher high” as seen on the 1-hour chart.

This current set of up moves suggests that the EUR/NZD is likely to be oscillating within a short-term uptrend phase in place since 10 October 2023 depicted by the minor ascending channel.

Watch the 1.7820 key short-term pivotal support to maintain the bullish tone for the next intermediate resistances to come in at 1.7980 and 1.8030 (50-day moving average, the upper boundary of the minor ascending channel and Fibonacci extension level).

On the flip side, a break below 1.7820 negates the bullish tone for a slide back to retest the immediate support zone of 1.7740/1.7700 (20-day moving average and 50% Fibonacci retracement of the current up move from 10 October 2023 low to 17 October 2023 current intraday high of 1.7902).

Bond Yields Moving Higher Again

Market movers today

The most important data release of today will be the US September retail sales and industrial production. While higher gasoline prices likely lifted headline retail sales, declines in leading services sector indicators and early credit card data suggest that consumption growth has still slowed down from August. Consensus expects control group sales, which exclude the volatile car, gasoline, building material and restaurant sales, to have remained unchanged in nominal terms, which would imply contraction in real goods consumption volume.

Retail sales, industrial production and fixed investment data will also be released for China overnight alongside the Q3 GDP. Consensus expects GDP growth at 1.0% q/q, which would keep China on track to reach the official 5% growth target for 2023 as a whole.

On the side of leading indicators, German October ZEW index is due for release, and it is expected to signal still subdued investor sentiment.

From central banks, ECB's de Guindos and Centeno as well as the Fed's Williams, Bowman and Barkin will be on the wires.

The 60 second overview

US equity prices rose yesterday while bond prices fell/yields rose as the diplomatic efforts to stop an escalation of the conflict between Hamas and Israel continues. President Biden will travel to Israel in order for the crisis not to escalate. The US Treasury curve once again bear steepened, and US Treasury yields have risen modestly in Asian trading hours where Asian equity markets have followed the positive trend from US yesterday.

The oil price has remained stable, while gold prices have begun to decline after a solid rise when the conflict began last week.

There is again focus on the Chinese company Country Garden and the possibility of a USD-denominated bond that may default today.

ECB continues to be hawkish as both Lane and Lagarde have stated the ECB must act if inflation does not come down due to more shocks to inflation and keep an eye on oil prices given the potential inflation risk. Today, there are plenty of ECB speakers and the market will be watching for more comments on inflation and monetary policy.

Equities: Unusual trading occurred yesterday! Yields and equities were higher at the same time as earnings taking investors' focus. Now, this is the typical behaviour; higher long-end yields, higher equities, but this relationship has been broken down since inflation emerged 2021. US closed up 1.1% and Europe 0.2%. Cyclicals outperformed, primarily consumer discretionary, communication and industrials, but all sectors were higher. Asian markets are higher this morning too, led by Japan, but US futures have dipped to negative.

FI: The US curve once again bear-steepened with 10Y Treasury yields rising some 8-9bp and 2Y Treasury yields rising 4bp. In the European markets there was a similar bear steepening with 2Y German yields rising 2bp and 10Y rising 4-5bp. However, the spread between Italian bonds and core-EGBs tightened despite the recent concerns over Italian government debt levels and a sustained rise in Italian yields above 5%.

FX: The latest IMM report (16 October) showed that JPY, AUD and CAD remain in stretched short territory and the recent days have not changed that as AUD/USD trades at 0.6350, USD/JPY is stuck in the mid 149s and USD/CAD remains above 1.36 this morning. EUR/USD has edged higher toward the 1.0550 area. NOK/SEK dropped below parity as EUR/SEK and EUR/NOK traded in opposite directions.

Credit: Yesterday, credit spreads were increasingly supported towards the end of the trading day by an underlying positive tone ahead of the Q3 earnings season, sending iTraxx Main 1.5bp tighter to close at 83.9bp, while Xover was tighter by 6bp to close at 445.6bp. The primary market activity was muted due to company black-out prior to reporting.

No Escalation Not Good Enough

Stocks gained, and bonds fell yesterday on US and allies’ efforts to deescalate tensions in the Middle East. Yet Israel told the US ‘to embrace for a long war’.

We know that no matter how bad the situation gets in the Middle East, the way, and the intensity with which the market perceives the news will gradually decrease, and risk assets like gold and Swiss franc will eventually give back gains. But, right now, it is still too early to lower one’s guard, as Israel hasn’t said its last word yet. The risk of an Israeli offensive remains high, and there is a strong possibility of a sharp decline in appetite if diplomatic efforts fail.

From a price perspective, gold remains in ambush a touch lower than its 200-DMA and could rapidly jump to and above the $2000 per ounce mark in case of further bad news from the Middle East. The US 10-year yield could quickly snap back to 4.50%, and oil could hop. Yesterday, the overall market relief led oil prices lower. News that the US and Venezuela are set to resume talks with a strong potential for Biden administration to ease sanctions against the Venezuelan oil helped. But upside risks prevail. Iranian implication in tensions could send the barrel of oil above $100pb.

A risky place

The Gaza situation is not helping to improve relations between the US and China since China picked the Palestinian side in the conflict. Therefore, it’s little surprising that the US considers further curbs on China’s access to advanced semiconductors, or to machines that build the advanced semiconductors, if nothing, to make sure that China doesn’t get the cutting-edge technology available for its military. Nvidia gained yesterday despite the news, but chip stocks are a risky place, not only due to a potentially escalating chip war between the US and China, but also because, Israel plays an important role in the production of advanced chips, and tensions in Israel could further disturb the global supply chain for chips.

Data watch: Strong US Retail Sales could boost appetite if Fed rate expectations remain contained

A potential return to low-risk assets could boost demand in US sovereigns in the short run, but the faith of US bonds is also tied to the economic data and what the Federal Reserve (Fed) will, or will not do in the coming meetings in the context of its own war against inflation. It’s clear that a further escalation of tensions in Gaza, and a sustainable positive pressure in oil prices should boost inflation expectations and fuel rate hike bets for the year end. However, no more hike remains the base case scenario for now.

On the data front, the Empire Manufacturing index showed a slower-than-expected contraction in October, and the retail sales data for September will be released today. The number could be a strong one, given that September tends to be a good month for spending as children return to school. A strong data could fuel optimism if Fed speakers continue to hint at the end of monetary policy tightening. Note that strong US spending has been one major pillar that explains why the US economy remained so resilient to the Fed’s aggressive tightening campaign. But behind the curtains, we see important vulnerability. The IMF data shows that unlike some European nations including Germany, France and the UK, the American savings took a very severe dive to pre-pandemic levels. And now that money is becoming rare, spending should slow, and help the Fed keep inflation on track towards its 2% target.