Sample Category Title

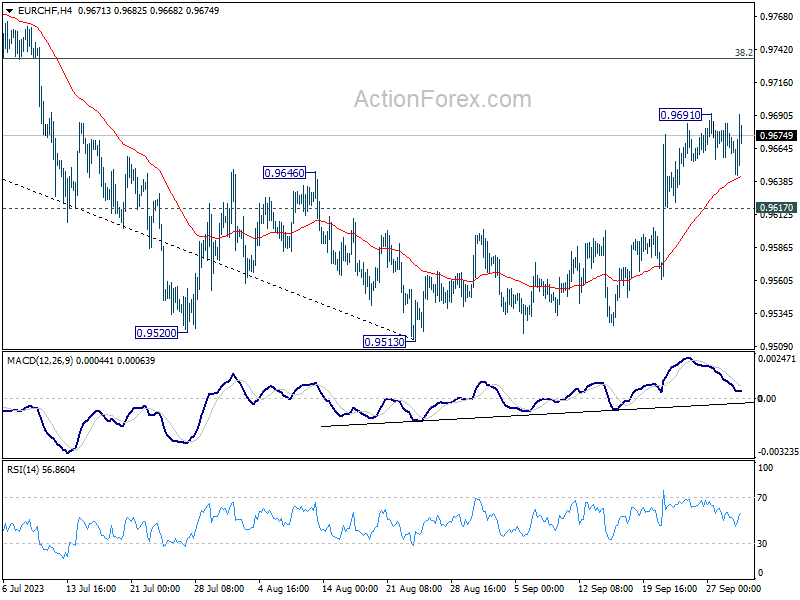

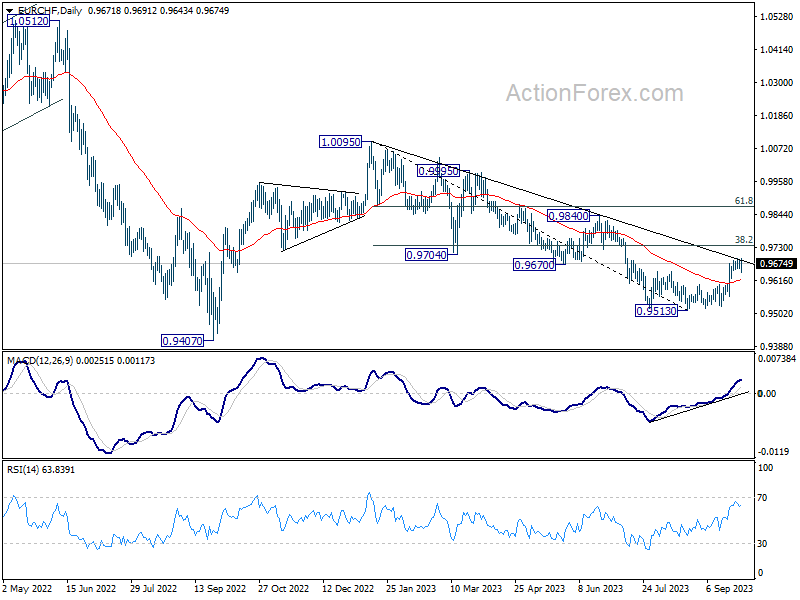

EUR/CHF Weekly Outlook

EUR/CHF edged higher to 0.9691 last week but turned sideway since then. Initial bias remains neutral this week first, and outlook is unchanged. Further rally is expected as long as 0.9617 support holds. Above 0.9691 will resume the rebound form 0.9513 to 38.2% retracement of 1.0095 to 0.9513 at 0.9735. However, firm break of 0.9617 will turn bias back to the downside for retesting 0.9513 low.

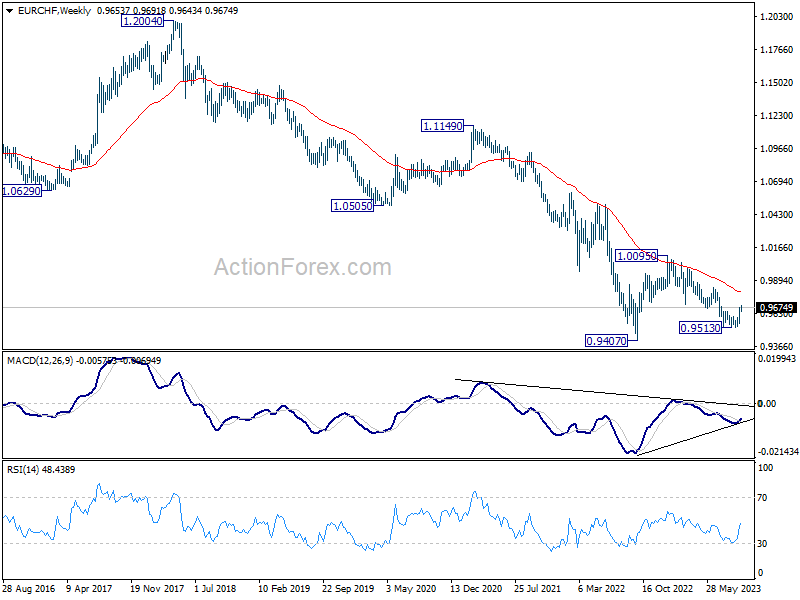

In the bigger picture, medium term outlook will stay bearish as long as the cross is capped well below falling 55 W EMA (now at 0.9804). That is, down trend from 1.2004 (2018 high) could still resume through 0.9407 (2022 low). However, sustained trading above the 55 W EMA will raise the chance that 0.9470 is already a long term bottom. Further rise would then be seen to 1.0095 resistance to indicate bullish trend reversal.

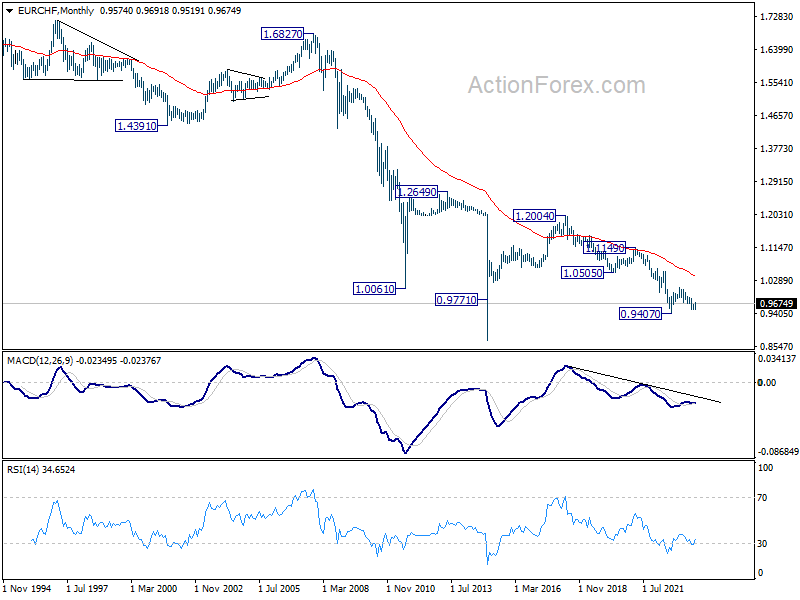

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0394). Break of 1.0095 resistance is needed to be the first sign of bottoming, or the multi-decade down trend is expected to continue.

The Weekly Bottom Line: Yields Realign to Higher-for-Longer

U.S. Highlights

- Revisions to GDP data left Q2 growth unchanged, but consumer spending growth was cut in half. Monthly consumer spending data showed that following at strong gain in July, real consumer spending slowed in August.

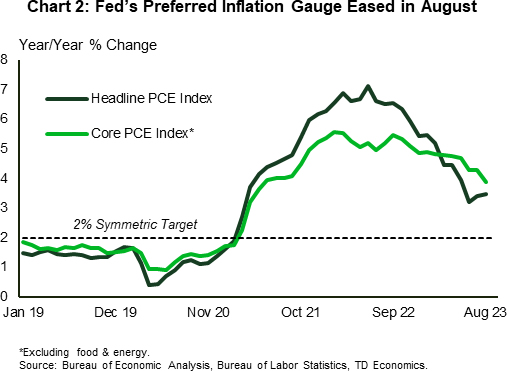

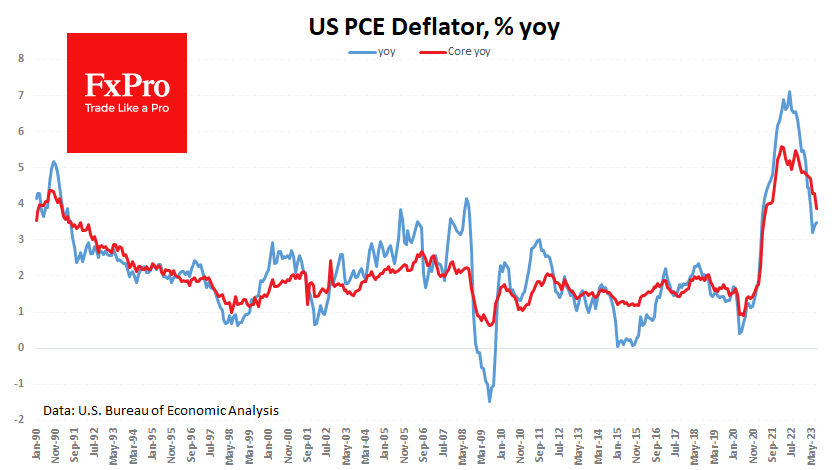

- The Fed’s preferred inflation gauge, the core Personal Consumption Expenditures (PCE) deflator, eased from 4.3% year-on-year to 3.9% in August. However, headline PCE inflation ticked up a notch as energy costs surged higher on the month.

- Pending home sales, which lead existing home sales by 1-2 months fell a sharp 7.1% in August, as mortgage rates crept above 7% that month.

Canadian Highlights

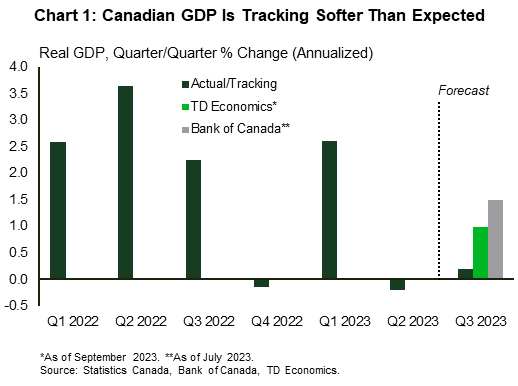

- The monthly GDP report suggests that growth remained stagnant in the third quarter – slower than expected in our recent forecast.

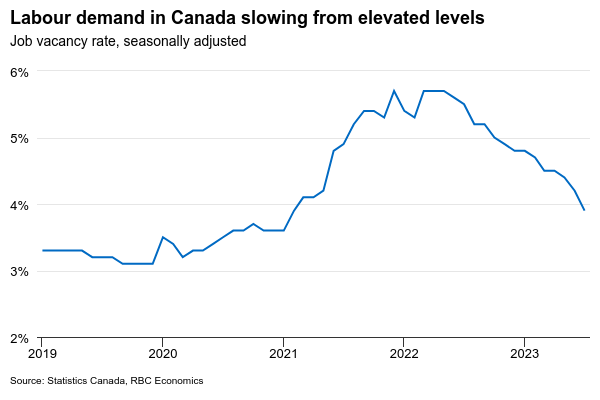

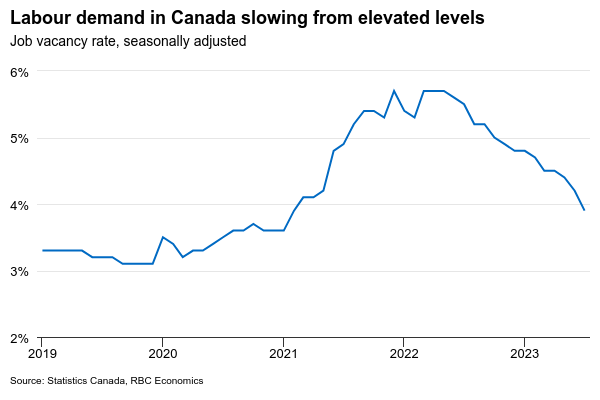

- The labour market is finding a better balance, with payroll employment remained largely unchanged and job vacancy rates reaching the lowest level since May 2021.

- Acceleration in July’s average weekly earnings is one data trend that doesn’t fit the pause story. The Bank of Canada will watch closely the next week’s more timely wage report for September.

U.S. – Yields Realign to Higher-for-Longer

The Fed has been beating the drum to the “higher for longer” interest rate tune for a while. Following last week’s FOMC projections, investors are recalibrating their expectations more in line with this view. Long-term treasury yields pushed higher in the week, with the 10-Year yield rising temporarily to a new 15-year high on Thursday, before easing to 4.53% at time of writing – still almost 10 basis points above last week’s close. Equity markets trended lower through the week, but managed to recoup most of the lost ground after Friday’s soft inflation print.

Revisions to GDP data led to a minor growth upgrade for the first quarter, but left the second unchanged. However, the picture was more nuanced underneath. Most notably, second quarter consumer spending growth was cut in half, to only 0.8% q/q (ann.). August’s Personal Income and Spending data out Friday help fill in the picture for the third quarter. Real disposable personal income fell for the third month in a row in August, while real spending (PCE) growth eased to 0.1% month-on-month (m/m), following a strong 0.6% m/m gain in July. That strength early in the quarter will still make for a strong showing for the consumer, however many hurdles are looming for the fourth quarter (see forecast). Our view is that consumer spending and economic growth will cool along with the weather this autumn, with September’s pullback in consumer confidence reinforcing this view.

Housing, which was the first part of the economy to weaken in the face of rate hikes, continues to struggle. Pending home sales, which lead closed sales by 1-2 months, fell a very sharp 7.1% (m/m) in August (Chart 1). This suggest that existing home sales could soon test new post-2010 lows. The shortage of existing homes for sale has been an added obstacle for transactions. Until recently, homebuyers appeared to have found some solace in the new home market, aided by healthier inventories and builder incentives. But with mortgage rates creeping above 7% in August, this sector is also feeling the pinch. New home sales (an inherently volatile series) trended lower that month. Daily measures show that mortgage rates have risen even higher recently and are now hovering in the 7.4%-7.6% range, a level that will surely further limit the pool of homebuyers.

Besides the challenges faced by the consumer, the UAW’s decision Friday to expand its strike and the increasing likelihood for a government shutdown next week, mark two other major potholes for the economy heading into the fourth quarter (see report). The shutdown would not only act as a drag on growth but would also delay access to key economic data, with next week’s payrolls report and the October 12th (CPI) inflation report the next two major items on the list. Having timely access to these reports is crucial with inflation still running well above target.

Thankfully, Friday’s PCE report carried some good news on the inflation front, with the Fed’s preferred inflation gauge easing from 4.3% to 3.9% year-on-year in August(Chart 2). However, the headline measure moved in the opposite direction, given an acceleration in food and energy costs. With the price of crude oil creeping higher to $93 per barrel, energy costs are likely to continue putting upward pressure on the headline measure over the near-term. All in all, it’s still a mixed picture, one that may be further complicated by a government shutdown.

Canada – More Evidence for A Pause

As we draw closer to the Bank of Canada’s next rate decision on October 25th, market participants are digging into the latest data to gauge what the Bank will do. This week's data provided some supporting evidence for a pause, although next week's jobs report will likely bear a heavier weight in the final decision. For now, markets have shifted their bets for another rate hike from a 50% chance to a 35% one.

Fresh off the press, the monthly GDP report suggests that growth remained stagnant in July and edged up just 0.1% month-on-month in August. With two months of data for the third quarter in hand, real GDP growth is tracking only 0.2% (annualized) – below our recent forecast(Chart 1). This suggests that the recovery from wildfire impacts in the mining and accommodation and food services sectors wasn't enough to weigh against the drag from the B.C. ports strike, and more restrictive monetary policy. Worryingly, the manufacturing sector contracted for the second month in a row, accounting of the largest share of today's drag. But there too, Statistics Canada pointed out that the B.C. port strike contributed to weakness in the chemicals industry, which contributed to manufacturing's soft showing.

The labour market is also finding a better balance, supporting our view that the bank will remain on pause. According to the Survey of Employment Payrolls and Hours (SEPH) for the month of July, labour demand continued to ease. Job vacancy rates declined markedly, reaching a low not seen since May 2021. Weakness was broad-based, but sectors bearing the brunt of this decline included retail trade and accommodation services, which suggests that cooling is migrating to the biggest recent contributors to labour demand. Since May 2022 (when job vacancies reached their peak) the number of unfilled positions fell by more than 30%, with vacancies in accommodation and food services and trade contributing more than a third of this decline (Chart 2).

The one area that doesn't tick the box in the Bank of Canada's checklist for a pause is average weekly earnings, which picked up the pace in July just as average weekly hours declined. Juxtaposed with the decline in job vacancies, it makes one wonder if this wage increase is sustainable or just a temporary blip. The sentiment from the CFIB small Business Barometer suggests that there might be more staying power, as average wage increase plans for the next 12 months registered a small uptick in September. With that, small business optimism tumbled to its lowest since the pandemic began, signaling apprehension about future economic conditions among business owners. We'll get more timely data on wage growth next Friday with September's Labour Force Survey.

All said, while the path ahead for the economy remains nuanced, this week's data provides a solid case for the Bank of Canada to stay on the sidelines.

Canadian Unemployment Rate Likely Edged Up Again in September

Surging Canadian population growth is helping to fill open positions, and will continue to boost the count of employed workers – we look for a 25k increase in employment in September to be reported next week. But the broader macroeconomic backdrop is continuing to soften. Controlling for population growth, GDP has contracted for four straight quarters on a per-person basis – including a 3.5% (annualized) per-capita decline in Q2. And labour markets have been absorbing new worker supply at a slower pace as demand slows. The number of job vacancies in Canada is still above pre-pandemic levels but has been declining for more than a year after peaking in May 2022. The unemployment rate has begun to rise, climbing to 5.5% over July and August from 5.0% in the spring. We look for another tick up to 5.6% in September with growth in the labour force growth again outpacing that of employment.

Evidence is building that earlier rapid and aggressive interest rate hikes from the Bank of Canada are finally having their intended impact on the broader economy, with consumers pulling back on spending while labour demand softens. The last Canadian inflation print showed some concerning reacceleration in broader measures of price growth – a concerning trend for the Bank of Canada as their only mandate is to get inflation back to a 2% rate. But inflation lags the economic cycle, and softening in labour markets should reassure the central bank that further easing in price pressures will follow. Wage growth has remained surprisingly firm – and will continue to see increases for unionized employees in particular, as contracts that were agreed to before the spike in prices are renegotiated. But we expect broader wage pressures will slow as the unemployment rate edges higher.

Week ahead data watch

The next round of U.S. payroll employment data will likely show the unemployment rate holding steady at 3.8%, and employment up by 177K, slightly below the 187K add in August. Labour market conditions remain tight with initial jobless claims trending at low levels. But signs of slowing demand including falling job openings mean we can continue to expect conditions to slow.

A U.S. government shutdown is widely expected to start this weekend but is expected to have a limited broader impact on the economy. Shutdowns can impact economic data temporarily, but only a portion (a large chunk of U.S. federal government spending is from mandatory spending programs, like social security, and it is just discretionary spending subject to annual spending approvals that is impacted). A relevant point of comparison is the 2019 shutdown, which lasted for 34 days, and resulted in only a 0.02% reduction in GDP according to the CBO.

We expect the Canadian trade deficit to narrow in August, oil prices increased by 7% during that month, contributing to most of the export growth.

The U.S. Advance economic indicators report showed that the goods deficit shrunk by $6.6B in August, with exports increasing by 2.2%, and imports declining by 1.2%. Looking at category details, auto exports were down 8.1% from the prior month, and industrial supplies exports went up by 4.9% in August.

Weekly Economic & Financial Commentary: “Soft Landing” Narrative Challenged

Summary

United States: "Soft Landing" Narrative Challenged

- Following last week's FOMC meeting, where the emphasis remained on incoming data guiding the Fed's interest rate path going forward—especially in regard to the duration in which rates may remain elevated—the data calendar heated up this week with plenty of indicators providing insight as to whether the Fed's forecast of a "soft landing" is plausible.

- Next week: Construction Spending (Mon.), ISM Manufacturing & Services (Mon. & Wed.), Employment (Fri.)

International: Eurozone Inflation Slows, Eurozone Growth Remains Subdued

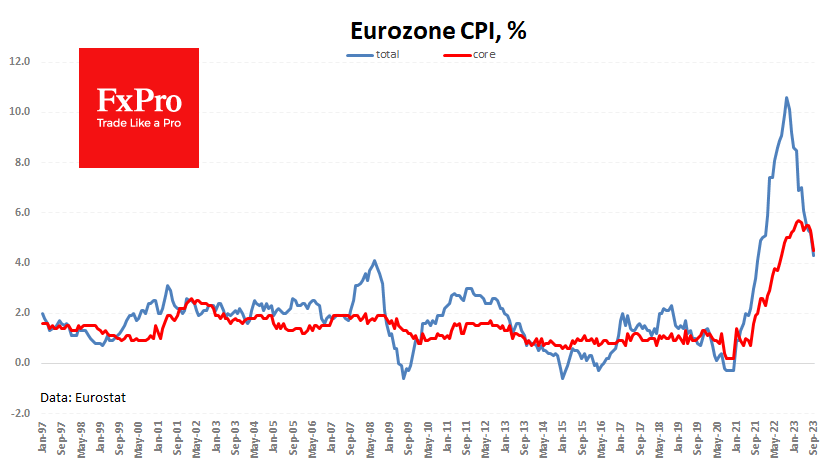

- Eurozone inflation slowed sharply in September as the headline CPI slowed to 4.3% year-over-year and the core CPI slowed to 4.5% year-over-year. Meanwhile, a drop in Eurozone September economic confidence pointed to still-subdued growth trends. Together, we believe slowing inflation and subdued growth will see the European Central Bank keep its Deposit Rate steady at 4.00% at its next monetary policy announcement in late October.

- Next week: Japan Tankan Survey (Mon.), Australia Policy Rate (Tue.), New Zealand Policy Rate (Wed.)

Credit Market Insights: Catching Up, but Not There Yet

- The Federal Reserve released the Distributional Financial Accounts overview last week, providing second-quarter estimates of the distribution of household wealth in the United States by the five percentile groups of wealth, income, age, education and race.

Topic of the Week: At Stake in the Strikes

- Autoworkers were on strike for the second week amid ongoing negotiations between the UAW and all three major domestic automakers. With the strike relatively contained, the initial hit to production should be relatively mild, though it may make it more difficult to tame inflation amid a pause in vehicle disinflation and an expected jump in labor compensation costs, challenging the timing in which inflation can return to target.

Summary 10/2 – 10/6

Monday, Oct 2, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q3 | 6 | 5 |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q3 | 5 | 9 |

| 23:50 | JPY | Tankan Non - Manufacturing Index Q3 | 24 | 23 |

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q3 | 22 | 20 |

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | 13.40% | |

| 00:00 | AUD | TD Securities Inflation M/M Sep | 0.20% | |

| 00:30 | JPY | Manufacturing PMI Sep F | 48.6 | 48.6 |

| 06:30 | CHF | Real Retail Sales Y/Y Aug | -1.80% | -2.20% |

| 07:30 | CHF | Manufacturing PMI Sep | 40.5 | 39.9 |

| 07:45 | EUR | Italy Manufacturing PMI Sep | 45.6 | 45.4 |

| 07:50 | EUR | France Manufacturing PMI Sep F | 43.6 | 43.6 |

| 07:55 | EUR | Germany Manufacturing PMI Sep F | 39.8 | 39.8 |

| 08:00 | EUR | Italy Unemployment Aug | 7.70% | 7.60% |

| 08:00 | EUR | Eurozone Manufacturing PMI Sep F | 43.4 | 43.4 |

| 08:30 | GBP | Manufacturing PMI Sep F | 44.2 | 44.2 |

| 09:00 | EUR | Eurozone Unemployment Rate Aug | 6.40% | 6.40% |

| 13:30 | CAD | Manufacturing PMI Sep | 48.0 | |

| 13:45 | USD | Manufacturing PMI Sep F | 48.9 | 48.9 |

| 14:00 | USD | ISM Manufacturing PMI Sep | 47.9 | 47.6 |

| 14:00 | USD | ISM Manufacturing Prices Paid Sep | 48.9 | 48.4 |

| 14:00 | USD | ISM Manufacturing Employment Index Sep | 48.5 | |

| 14:00 | USD | Construction Spending M/M Aug | 0.60% | 0.70% |

| 21:00 | NZD | NZIER Business Confidence Q3 | -63 | |

| 23:01 | GBP | BRC Shop Price Index Y/Y Aug | 6.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q3 | |

| Forecast: 6 | Previous: 5 | ||

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q3 | |

| Forecast: 5 | Previous: 9 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Index Q3 | |

| Forecast: 24 | Previous: 23 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q3 | |

| Forecast: 22 | Previous: 20 | ||

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | |

| Forecast: | Previous: 13.40% | ||

| 00:00 | AUD | TD Securities Inflation M/M Sep | |

| Forecast: | Previous: 0.20% | ||

| 00:30 | JPY | Manufacturing PMI Sep F | |

| Forecast: 48.6 | Previous: 48.6 | ||

| 06:30 | CHF | Real Retail Sales Y/Y Aug | |

| Forecast: -1.80% | Previous: -2.20% | ||

| 07:30 | CHF | Manufacturing PMI Sep | |

| Forecast: 40.5 | Previous: 39.9 | ||

| 07:45 | EUR | Italy Manufacturing PMI Sep | |

| Forecast: 45.6 | Previous: 45.4 | ||

| 07:50 | EUR | France Manufacturing PMI Sep F | |

| Forecast: 43.6 | Previous: 43.6 | ||

| 07:55 | EUR | Germany Manufacturing PMI Sep F | |

| Forecast: 39.8 | Previous: 39.8 | ||

| 08:00 | EUR | Italy Unemployment Aug | |

| Forecast: 7.70% | Previous: 7.60% | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Sep F | |

| Forecast: 43.4 | Previous: 43.4 | ||

| 08:30 | GBP | Manufacturing PMI Sep F | |

| Forecast: 44.2 | Previous: 44.2 | ||

| 09:00 | EUR | Eurozone Unemployment Rate Aug | |

| Forecast: 6.40% | Previous: 6.40% | ||

| 13:30 | CAD | Manufacturing PMI Sep | |

| Forecast: | Previous: 48.0 | ||

| 13:45 | USD | Manufacturing PMI Sep F | |

| Forecast: 48.9 | Previous: 48.9 | ||

| 14:00 | USD | ISM Manufacturing PMI Sep | |

| Forecast: 47.9 | Previous: 47.6 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Sep | |

| Forecast: 48.9 | Previous: 48.4 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Sep | |

| Forecast: | Previous: 48.5 | ||

| 14:00 | USD | Construction Spending M/M Aug | |

| Forecast: 0.60% | Previous: 0.70% | ||

| 21:00 | NZD | NZIER Business Confidence Q3 | |

| Forecast: | Previous: -63 | ||

| 23:01 | GBP | BRC Shop Price Index Y/Y Aug | |

| Forecast: | Previous: 6.90% | ||

Tuesday, Oct 3, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Building Permits M/M Aug | 3.30% | -8.10% |

| 03:30 | AUD | RBA Interest Rate Decision | 4.10% | 4.10% |

| 06:30 | CHF | CPI M/M Sep | 0.00% | 0.20% |

| 06:30 | CHF | CPI Y/Y Sep | 1.80% | 1.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Building Permits M/M Aug | |

| Forecast: 3.30% | Previous: -8.10% | ||

| 03:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 4.10% | Previous: 4.10% | ||

| 06:30 | CHF | CPI M/M Sep | |

| Forecast: 0.00% | Previous: 0.20% | ||

| 06:30 | CHF | CPI Y/Y Sep | |

| Forecast: 1.80% | Previous: 1.60% | ||

Wednesday, Oct 4, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | NZD | RBNZ Interest Rate Decision | 5.50% | 5.50% |

| 07:45 | EUR | Italy Services PMI Sep | 50 | 49.8 |

| 07:50 | EUR | France Services PMI Sep F | 43.9 | 43.9 |

| 07:55 | EUR | Germany PMI Sep F | 49.8 | 49.8 |

| 08:00 | EUR | Eurozone Services PMI Sep F | 48.4 | 48.4 |

| 08:30 | GBP | Services PMI Sep F | 47.2 | 47.2 |

| 09:00 | EUR | Eurozone PPI M/M Aug | 0.60% | -0.50% |

| 09:00 | EUR | Eurozone PPI Y/Y Aug | -7.60% | |

| 09:00 | EUR | Eurozone Retail Sales M/M Aug | -0.50% | -0.20% |

| 12:15 | USD | ADP Employment Change Sep | 155K | 177K |

| 13:45 | USD | Services PMI Sep F | 50.2 | 50.2 |

| 14:00 | USD | ISM Services PMI Sep | 53.6 | 54.5 |

| 14:00 | USD | Factory Orders M/M Aug | 0.20% | -2.10% |

| 14:30 | USD | Crude Oil Inventories | -2.2M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | NZD | RBNZ Interest Rate Decision | |

| Forecast: 5.50% | Previous: 5.50% | ||

| 07:45 | EUR | Italy Services PMI Sep | |

| Forecast: 50 | Previous: 49.8 | ||

| 07:50 | EUR | France Services PMI Sep F | |

| Forecast: 43.9 | Previous: 43.9 | ||

| 07:55 | EUR | Germany PMI Sep F | |

| Forecast: 49.8 | Previous: 49.8 | ||

| 08:00 | EUR | Eurozone Services PMI Sep F | |

| Forecast: 48.4 | Previous: 48.4 | ||

| 08:30 | GBP | Services PMI Sep F | |

| Forecast: 47.2 | Previous: 47.2 | ||

| 09:00 | EUR | Eurozone PPI M/M Aug | |

| Forecast: 0.60% | Previous: -0.50% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Aug | |

| Forecast: | Previous: -7.60% | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Aug | |

| Forecast: -0.50% | Previous: -0.20% | ||

| 12:15 | USD | ADP Employment Change Sep | |

| Forecast: 155K | Previous: 177K | ||

| 13:45 | USD | Services PMI Sep F | |

| Forecast: 50.2 | Previous: 50.2 | ||

| 14:00 | USD | ISM Services PMI Sep | |

| Forecast: 53.6 | Previous: 54.5 | ||

| 14:00 | USD | Factory Orders M/M Aug | |

| Forecast: 0.20% | Previous: -2.10% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -2.2M | ||

Thursday, Oct 5, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Aug | 8.61B | 8.04B |

| 06:00 | EUR | Germany Trade Balance (EUR) Aug | 14.3B | 15.9B |

| 06:45 | EUR | France Industrial Output M/M Aug | -0.40% | 0.80% |

| 08:30 | GBP | Construction PMI Sep | 49.9 | 50.8 |

| 11:30 | USD | Challenger Job Cuts Y/Y Sep | 266.90% | |

| 12:30 | USD | Initial Jobless Claims (Sep 29) | 204K | |

| 12:30 | USD | Trade Balance (USD) Aug | -65.1B | -65.0B |

| 12:30 | CAD | Trade Balance (CAD) Aug | -1.4B | -1.0B |

| 14:00 | CAD | Ivey PMI Sep | 50.8 | 53.5 |

| 14:30 | USD | Natural Gas Storage | 90B | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Aug | 1.50% | 1.30% |

| 23:30 | JPY | Overall Household Spending Y/Y Aug | -4.30% | -5.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Aug | |

| Forecast: 8.61B | Previous: 8.04B | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Aug | |

| Forecast: 14.3B | Previous: 15.9B | ||

| 06:45 | EUR | France Industrial Output M/M Aug | |

| Forecast: -0.40% | Previous: 0.80% | ||

| 08:30 | GBP | Construction PMI Sep | |

| Forecast: 49.9 | Previous: 50.8 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Sep | |

| Forecast: | Previous: 266.90% | ||

| 12:30 | USD | Initial Jobless Claims (Sep 29) | |

| Forecast: | Previous: 204K | ||

| 12:30 | USD | Trade Balance (USD) Aug | |

| Forecast: -65.1B | Previous: -65.0B | ||

| 12:30 | CAD | Trade Balance (CAD) Aug | |

| Forecast: -1.4B | Previous: -1.0B | ||

| 14:00 | CAD | Ivey PMI Sep | |

| Forecast: 50.8 | Previous: 53.5 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 90B | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Aug | |

| Forecast: 1.50% | Previous: 1.30% | ||

| 23:30 | JPY | Overall Household Spending Y/Y Aug | |

| Forecast: -4.30% | Previous: -5.00% | ||

Friday, Oct 6, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Aug P | 109 | 108.2 |

| 05:45 | CHF | Unemployment Rate Sep | 2.10% | 2.10% |

| 06:00 | EUR | Germany Factory Orders M/M Aug | 1.50% | -11.70% |

| 06:45 | EUR | France Trade Balance (EUR) Aug | -8.9B | -8.1B |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Sep | 694B | |

| 08:00 | EUR | Italy Retail Sales M/M Aug | 0.00% | 0.40% |

| 12:30 | USD | Nonfarm Payrolls Sep | 168K | 187K |

| 12:30 | USD | Unemployment Rate Sep | 3.70% | 3.80% |

| 12:30 | USD | Average Hourly Earnings M/M Sep | 0.30% | 0.20% |

| 12:30 | CAD | Net Change in Employment Sep | 28.0K | 39.9K |

| 12:30 | CAD | Unemployment Rate Sep | 5.60% | 5.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Aug P | |

| Forecast: 109 | Previous: 108.2 | ||

| 05:45 | CHF | Unemployment Rate Sep | |

| Forecast: 2.10% | Previous: 2.10% | ||

| 06:00 | EUR | Germany Factory Orders M/M Aug | |

| Forecast: 1.50% | Previous: -11.70% | ||

| 06:45 | EUR | France Trade Balance (EUR) Aug | |

| Forecast: -8.9B | Previous: -8.1B | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Sep | |

| Forecast: | Previous: 694B | ||

| 08:00 | EUR | Italy Retail Sales M/M Aug | |

| Forecast: 0.00% | Previous: 0.40% | ||

| 12:30 | USD | Nonfarm Payrolls Sep | |

| Forecast: 168K | Previous: 187K | ||

| 12:30 | USD | Unemployment Rate Sep | |

| Forecast: 3.70% | Previous: 3.80% | ||

| 12:30 | USD | Average Hourly Earnings M/M Sep | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 12:30 | CAD | Net Change in Employment Sep | |

| Forecast: 28.0K | Previous: 39.9K | ||

| 12:30 | CAD | Unemployment Rate Sep | |

| Forecast: 5.60% | Previous: 5.50% | ||

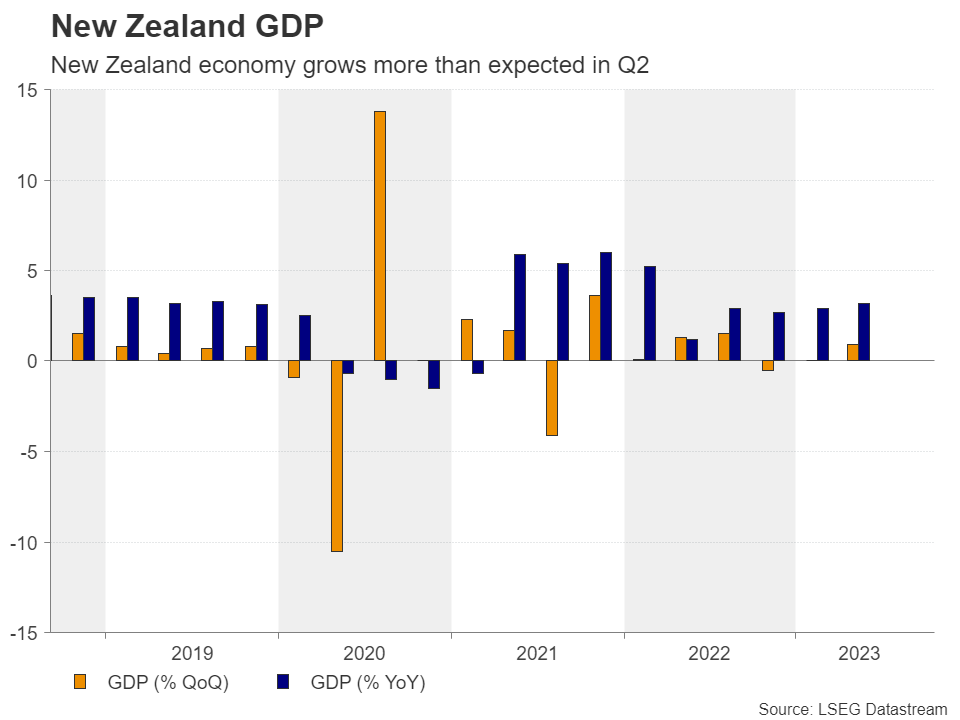

Will RBNZ Opt for a Hawkish Hold?

- RBNZ expected to hold rates steady for the third straight meeting

- However, Q2 GDP data sparks hopes for another hike by year end

- Kiwi traders to look for changes in the Bank’s language

- The decision will be released on Wednesday at 01:00 GMT

Stellar economic performance revives hike bets

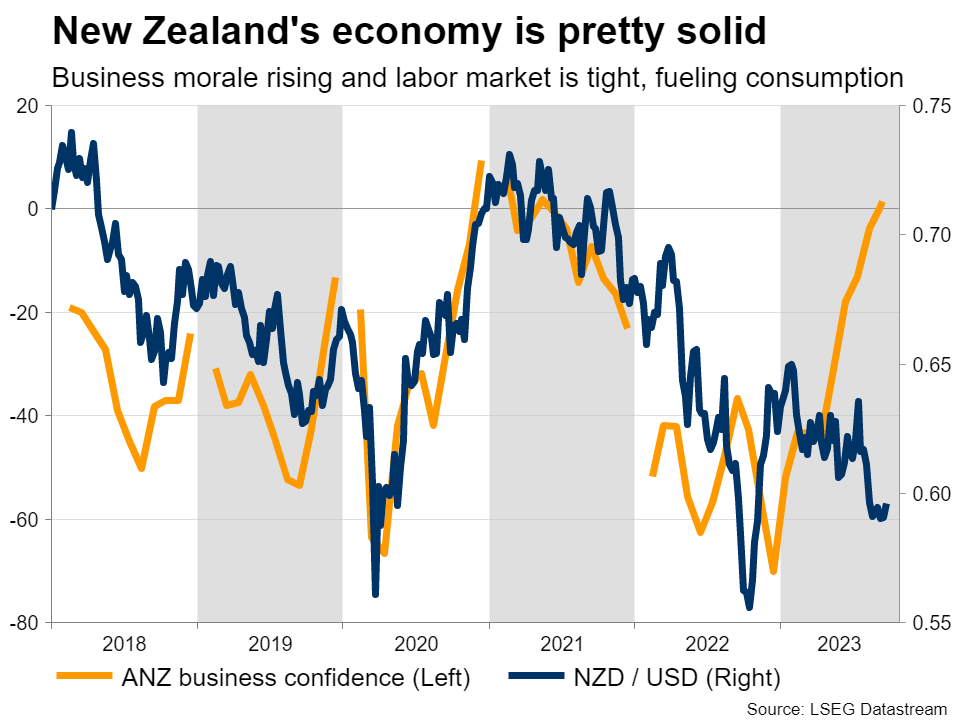

Back in August, the Reserve Bank of New Zealand (RBNZ) decided to maintain the Official Cash Rate (OCR) at 5.5%, adding that the current level of interest rates is constraining spending and thereby inflation pressures, also expressing confidence that with rates staying at restrictive levels for some time, inflation will return to the 1-3% target range.

Back then, they noted that the economy is evolving broadly as expected, with activity continuing to slow in parts of the economy that are more sensitive to interest rates. However, just last week, GDP data revealed that the economy grew by nearly double the anticipated pace in Q2, after stagnating in the first three months of the year. Although this appears to be a relief for the current government, which is under fire for how they’ve been handling the economy ahead of an election on October 14, it may worry the central bank which likely needs slower growth to achieve its inflation goal.

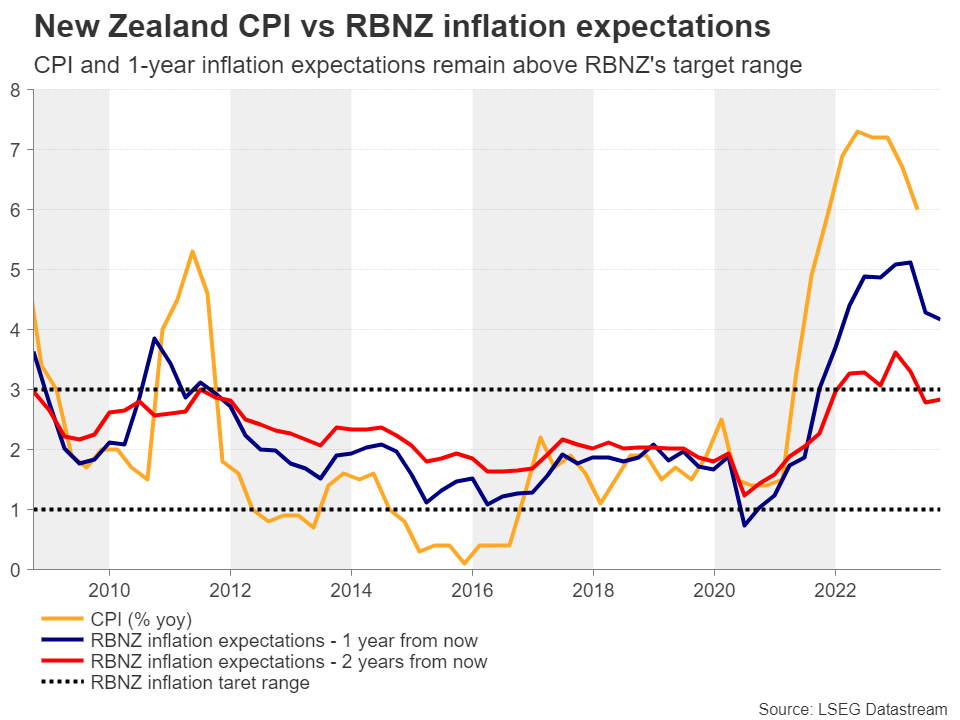

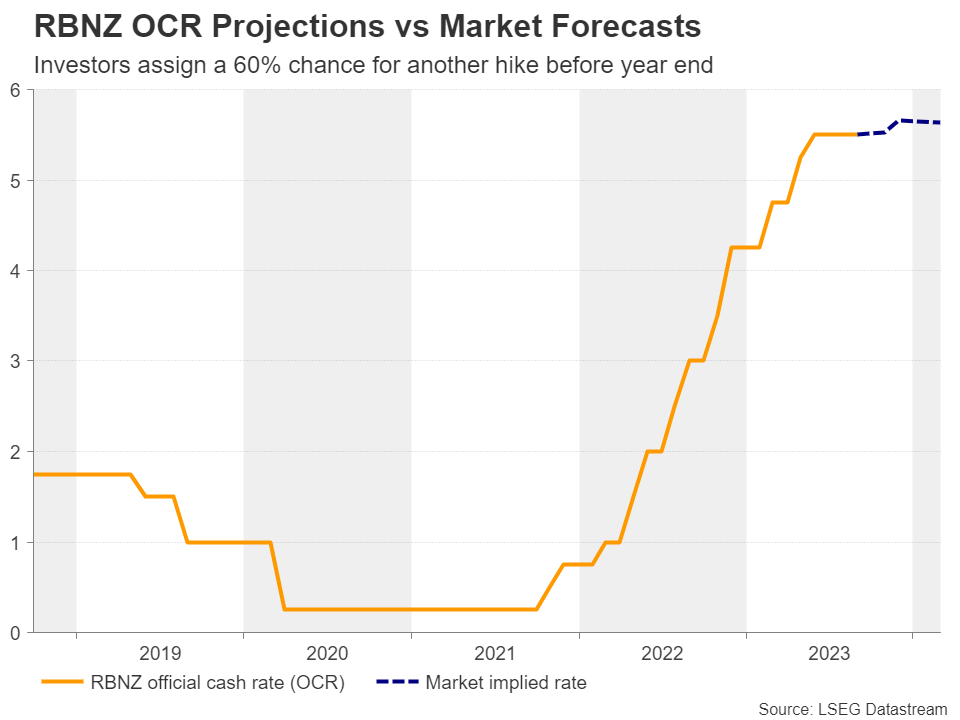

With the Bank projecting that the economy would slip into recession in the second half of 2023 and the data offering no such sign, investors have begun pricing in around a 60% probability for another quarter-point hike by the end of the year as the stronger economic performance, combined with the latest rally in oil prices, adds upside risks to the nation’s 6% inflation rate. Yes, 1-year inflation expectations are much lower, but still above the Bank’s target, with only the 2-year projection lying slightly below the upper bound of the 1-3% target range.

Will officials adopt a more hawkish language?

For Wednesday’s meeting, investors are 90% confident that policymakers will refrain from acting, and should this be the case, they may dig into the statement of hints on whether the Bank will open the door to another hike.

All that suggests that, even if the Bank stands pat, the meeting could be a live one. The kiwi may slide in the case of policymakers abstaining from commenting on the possibility of additional hikes, as those expecting more may be disappointed. The opposite may be true should they bring to the table the likelihood of more action.

Given that this will be one of the shorter meetings that are not accompanied by updated economic projections, and that policymakeres may prefer to have the CPI numbers for Q3 in hand before examining whether higher rates are needed, the former outcome may be more likely. The November gathering appears to be a wiser choice for proceeding with any policy or language changes.

Kiwi traders may get disappointed

The kiwi has been in a recovery mode the last couple of days against the US dollar, but this was mainly due to the dollar pulling back, perhaps as traders are rebalancing their portfolios and liquidating some long-dollar positions on the last trading of the quarter.

A potentially dovish RBNZ could keep that recovery in check and bring the kiwi back under pressure. That said, given that monetary policy is not the only variable in the equation of the risk-linked currency, traders may have more than the RBNZ decision to examine. The challenges facing China, the world’s second-largest economy and New Zealand’s main trading partner, as well as concerns about the economic performance of Europe and the UK, could constitute another element of anxiety, and thereby add extra weight on the currency.

Kiwi/dollar headed towards key resistance

Kiwi/dollar rallied above the 0.5985 zone today, confirming a temporary bottom at around 0.5855. However, the pair looks to be headed towards the very important zone of 0.6080, which acted as the lower end of the sideways range that contained most of the price action between February and August. The bulls may get rejected there if indeed the RBNZ appears dovish, with the potential subsequent decline aiming for another test at 0.5985. A break lower could encourage extensions towards the low of September 6, at 0.5855.

On the upside, even if kiwi/dollar climbs above the 0.6080 barrier, the picture would not be painted positive. Such a move may only signal the pair’s return within the aforementioned range, and thereby turn the outlook to neutral.

Week Ahead – Dollar Shines ahead of Nonfarm Payrolls

- Dollar cruises higher, nonfarm payrolls on Friday will be crucial for this rally

- Early indicators point to another solid month for the US labor market

- Central bank decisions in Australia and New Zealand will also be in focus

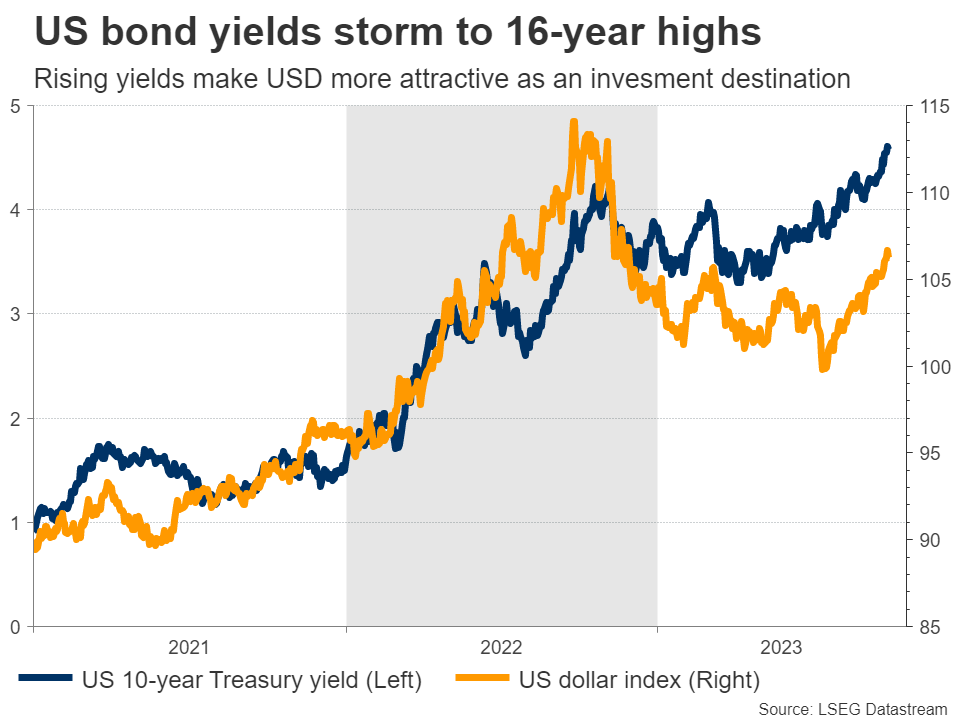

Dollar goes on a rampage

The US dollar rally has gone into overdrive lately. Empowered by a stunning rise in US yields, solid economic fundamentals, and safe haven flows, the dollar has charged higher to record 11 consecutive weeks of gains against the euro.

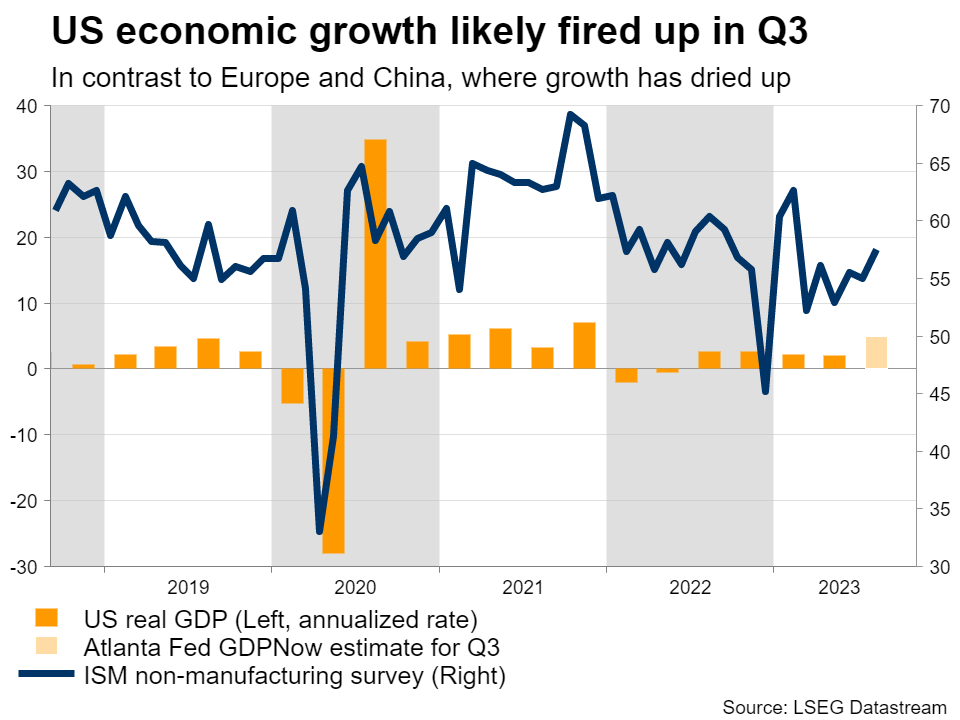

In a nutshell, the United States appears much more resilient than any other region. Incoming data releases continue to reaffirm the strength of the US economy, while in contrast, Europe is suffering a sharp slowdown in economic growth and China is still dealing with the implosion of its property sector.

This differential in economic growth is increasingly pushing investors towards the United States, and the impressive rally in US yields lately has made the dollar even more attractive from an interest rate perspective.

Hence, the dollar offers the ‘full package’ at the moment - the highest real rates among the major economies, the strongest economic growth, and safe haven qualities thanks to its reserve currency status. Meanwhile, there’s a lack of attractive alternatives in the FX arena, as every other major currency is dealing with its own problems.

Next week’s data releases will either add more fuel to this rally or trigger a correction, with the main event being the US employment report on Friday. Forecasts suggest nonfarm payrolls rose by 150k in September, less than the previous month but still a decent number overall.

Meanwhile, the unemployment rate is projected to have ticked back down to 3.7%, while wage growth is expected to have picked up some steam in monthly terms. If the forecasts are met, this would be yet another dataset reinforcing the Fed’s message that interest rates could remain higher for longer.

As for any surprises, most early indicators point to another solid month for the US labor market. Applications for unemployment benefits fell sharply in September, so there were no signs of any mass worker layoffs. Similarly, business surveys from S&P Global signaled a reacceleration in employment growth.

Speaking of business surveys, the ISM manufacturing index is due on Monday, ahead of the non-manufacturing PMI on Wednesday. In the political scene, the government will shut down this weekend unless a funding deal is reached in Congress. That said, markets usually ignore these shutdowns, as investors view them as political theater. For markets to care, it would need to be a prolonged shutdown that dampens economic growth.

RBA and RBNZ decisions

Crossing into Australia, the Reserve Bank will conclude its meeting early on Tuesday, the first one under the new Governor, Michelle Bullock. Even though data releases have been rather strong lately, with the labor market enjoying a substantial recovery in August and inflation reaccelerating, markets assign less than a 10% probability to a rate increase.

That’s mostly because the latest signals from the central bank itself show a preference for keeping rates unchanged. The latest RBA minutes preached patience, as rates have already risen quickly and the full impact of all this tightening has not been felt yet.

A decision to keep rates unchanged would argue for a negative reaction in the Australian dollar, but nothing dramatic, as this is the market’s baseline scenario already.

In neighboring New Zealand, the central bank will announce its own decision on Wednesday. The market-implied probability for a rate increase is also around 10%, but it might still be an exciting event as the economy has outperformed expectations lately. Hence, the question is whether the RBNZ will set the stage for another rate hike in November.

Inflation seems to be gaining momentum again. Even though inflation cooled a little in the second quarter, the jobs market remained very tight, with record levels of labor force participation and an explosion in population growth helping to boost demand. In addition, the depreciation of the New Zealand dollar in recent months coupled with the sharp rise in oil prices will also help to refuel inflation.

Against this backdrop, the RBNZ will likely keep rates unchanged, but perhaps signal that a rate increase in November is a real possibility. Markets assign a 60% chance to that scenario, and if this probability moves any higher in the aftermath, it could lift the currency somewhat.

That said, there’s an election in two weeks, so the risk is that the RBNZ does not deliver any clear signals, to avoid interfering. Either way, the general outlook for the kiwi dollar seems grim, even if the currency spikes higher after the RBNZ. The slowdown in global growth and the deterioration in risk sentiment will likely keep a lid on any rallies.

Chinese data releases will be in focus too. China is the largest trading partner of both Australia and New Zealand, so these currencies are very sensitive to developments in China, where the latest business surveys will be released over the weekend.

Elsewhere, Japan’s Tankan business survey for Q3 will hit the markets on Monday, while in Canada, the employment report for September will see the light on Friday.

US and European Inflation Slowdown Give Much-Needed Relief

Recent reports from Europe and the US have highlighted a slowdown in inflation. The slowdown in price growth triggered a wave of purchases of risk assets in the hope that central banks would not have to keep rates at restrictive levels for too long.

In the eurozone, overall inflation in September decreased from 5.2% to 4.3% y/y, and Core PCE slowed from 5.3% to 4.5%. In both cases, the data is below expectations. And this immediately revitalised expectations that the ECB would no longer need to raise rates. Expectations of looser monetary conditions are favourable for the stock market. Ironically, it also supports the euro’s rise, directly correlating with stock indices.

The US released its estimate of personal income and spending. The Fed focuses specifically on the price deflator from this report as it estimates a much broader consumer basket. The price deflator, excluding food and energy, fell to 3.9% y/y, the lowest over two years. The overall price deflator accelerated slightly to 3.5% from 3.4% a month earlier.

Despite this slowdown, Americans are saving less and less. The savings rate fell to 3.9% in August, a new low this year. Also visible is how income growth has stalled in recent months while spending is creeping up. By April, spending had risen 2.2% and disposable income 0.8%.

Weekly Focus – Bond Yields Increasing

This week, we have seen a significant increase in bond yields in both the US and Europe. Markets are reducing expectations for rate cuts from central banks, which are now priced to happen only slowly. This follows signals from the central banks themselves that they are still ready to combat inflation which remains too high.

In our view, uncertainty over the economic outlook remains large, and we see a significant risk that the interest rate outlook will have to be adjusted lower again. There has been a serious tightening of financing conditions both in the US and the euro area, and the market move towards higher yields is tightening conditions further. Current market pricing implies a very soft landing for the economy, and history shows that such expectations are often too optimistic.

On the inflation side, we got the preliminary September data for the euro area, where the y/y inflation rate declined from 5.2% to 4.3%. This decline was largely driven by base effects, but the m/m increase in both headline and core price indices also declined and landed close to 0.2%, which is close to consistent with 2% annual inflation. This is a volatile measure but nevertheless good news for the ECB.

Large government borrowing is also behind the increase in bond yields. This week, we had downwards revisions to the outlook for public finances in France and Italy, but Germany lowered its estimated borrowing requirement for this year.

One reason behind higher bond yields could also be expectations of monetary policy tightening in Japan through an easing of the yield curve control. We agree that this is likely to happen in the not too distant future, however inflation in Japan slowed from 2.8% to 2.5% y/y in September. The quarterly Tankan business survey due Monday and wage data Friday will be key to judge the longer term inflation momentum.

In China, property developer Evergrande returned to the headlines with news that it had missed a bond payment and scrapped creditor meetings. This is not helpful to the efforts for revitalising home buying and hence the construction part of the economy, and is adding to concerns over growth. Note that the coming week is the Golden Week holiday in China.

A US government shutdown might be a reality from Monday if the US Congress fails to either pass a budget agreement or a resolution to continue with the old budget temporarily. A shutdown would mean a sharp reduction in government spending until it is resolved and could have a somewhat negative effect on growth if it lasts more than a few weeks, but it is not a threat to the US meeting its debt payments like the debt ceiling problem earlier this year was. Also, a shutdown would mean that government statistics such as the coming week's job report and job openings are not published, whereas private sector data such as the ISM and the ADP employment report are not affected. If we do get data, it could be very important for whether or not the soft landing narrative persists.

On the central bank front, we will get rate decisions in Poland, Australia and New Zealand.

Week Ahead – US Government Shutdown, RBA and RBNZ Rate Decisions, Weekend Data

US

This will be a busy week in the US with a looming government shutdown, an expanding UAW strike, a lot of Fed speak, and an NFP report that could show hiring fell to the lowest levels since early 2021. The September jobs report is expected to show hiring slowed from a 187,000 pace to 170,000. Despite the loosening of the labor market, the unemployment rate is expected to tick lower to 3.7%, and wage pressures are expected to increase on a monthly basis from 0.2% to a 0.3% pace.

The Fed will be making the rounds as nine members make appearances. On Monday, Chair Powell and Harker take part in a roundtable talk with business owners and community leaders in Pennsylvania. Williams and Mester also speak at separate events on Monday. Tuesday contains one speech by Bostic. On Wednesday, Bowman speaks at a banking conference and Goolsbee appears at the Chicago Payments Symposium. On Thursday, Mester talks at the Chicago Payments event and Daly speaks at the Economic Club of NY.

Eurozone

There’s very little of note next week, just a collection of tier two and three economic releases, the bulk of which being final PMIs. ECB President Christine Lagarde will also make an appearance which will be of interest in light of the September inflation data.

UK

Another quiet week for the UK, with tier-three economic data dominating. There are some BoE appearances but broadly speaking and barring any surprises, next week is not expected to be one for the record books.

Russia

A very quiet week with just the manufacturing and services PMI surveys being released.

South Africa

No major economic releases or events next week with only the whole economy PMI of note alongside a few tier-three releases.

Turkey

Inflation data will be of interest next week although at this point it may not have a big impact on the outlook for interest rates. At around 60% and with the lira at record lows, further large hikes will likely be necessary, regardless.

Switzerland

The SNB likely ended its tightening cycle with an attempted hawkish hold in September but as is the case with other central banks, that will depend on the data. With that in mind, there are a few economic releases of note this coming week. The September CPI number is the most obvious, while unemployment, retail sales, and the manufacturing PMI will also be of interest.

China

Key manufacturing and services PMI data for September will be released over the weekend before China’s financial markets are shut for the Golden Week holiday starting next Monday, 2 October.

The NBS manufacturing & services PMIs will be out on Saturday, 30 September. After better-than-expected prior PMI numbers as well as retail sales and industrial production for August, market participants will be scrutinizing the September PMI data for further hints of an easing of deflationary spiral risk.

The consensus is expecting a slight recovery to 50 (expansion mode) for manufacturing activities from 49.7 in August. Also of interest will be the sub-components such as new orders and production that rose to their highest level since March 2023 at 50.2 and 51.9 respectively in August. Services activities as measured by the NBS non-manufacturing PMI is forecasted to improve further to 52 from 51 in August.

The private sector compiled Caixin manufacturing and services PMIs for September consisting of more small and medium enterprises will be released on Sunday. A further improvement is expected here as well with the manufacturing PMI seen at 51.2 versus 51 previously, and the services PMI at 52.6 versus 51.8 a month earlier.

India

The manufacturing PMI for September will be released on Tuesday and is expected to dip to 57 from 58.6 in August. In addition, the services PMI is released on Thursday is expected to ease as well to 59 from 60.1 in August. That would be the second consecutive month of growth slowdown after a 13-year high of 62.3 printed in July.

On Friday, India’s central bank, the RBI will announce its monetary policy decision; the consensus is no change at 6.5% for its policy rate which would be the fourth consecutive month of standing pat.

Australia

After an uptick in the CPI to 5.2% in the year to August from 4.9% (the lowest level in 17 months), market participants will now focus on the Melbourne Institute’s monthly inflation gauge for September on Monday. It is expected to increase to 0.4% m/m from 0.2% in August.

On Tuesday, it’s the RBA monetary policy decision with the consensus expecting no change to its policy cash rate at 4.1%, extending its rate pause to a fourth consecutive month. Based on the pricing on the ASX 30-day interbank cash rate futures as of 28 September, there’s a 7% chance of a 25 basis points cut to 3.85%, the same as a week earlier.

The balance of trade data for August will be out on Thursday with the trade surplus expected to widen to A$9 billion from A$8.04 billion in July.

New Zealand

The RBNZ’s monetary policy decision will be released on Wednesday and no change is expected to its official cash rate at 5.5%. That would be the third consecutive month of no change due to a weak external demand environment that could hamper exports.

Japan

On Monday, the Q3 Tankan large manufacturers and non-manufacturing indices will be released. The sentiment for large manufacturers is expected to improve further to +6 from + 5 in Q2. In a similar fashion, the mood of the large non-manufacturers is expected to rise to +24 from +23 in Q2.

Data on household spending, average cash earnings, and the preliminary reading of the leading economic index for August will be released on Friday. In the recent Bank of Japan (BoJ) ex-post monetary policy decision press conference, Governor Ueda specifically mentioned that growth in wages needs to see further improvement before annualized inflation can maintain a sustainable rate above 2%.

Therefore, the average cash earnings data is likely to be closely watched and is forecasted to dip slightly to 1.2% y/y in August from 1.3% in July.

Singapore

Two key data to focus on; the preliminary Q3 URA Property Index on Monday and retail sales on Thursday.

A further deceleration is expected in retail sales to 0.8% y/y in August from 1.1% in July. That would mark the weakest growth since January 2023.

Economic Calendar

Saturday, Sept. 30

Economic Data/Events

- China manufacturing PMI, non-manufacturing PMI

- US Congress deadline to pass a federal spending measure

- Helsinki Security Forum continues

Sunday, Oct. 1

Economic Data/Events

- China Caixin manufacturing PMI, Caixin services PMI

- US government shutdown to start if funding lapses

- UK Conservative Party Conference begins

Monday, Oct. 2

Economic Data/Events

- US construction spending, ISM manufacturing

- Australia Melbourne Institute inflation

- European final manufacturing PMI: Eurozone, Germany, France and the UK

- Eurozone unemployment

- Japan Tankan business sentiment survey

- New Zealand building permits

- Singapore home prices

- Spain unemployment

- Bank of Japan releases report on September monetary policy meeting

- Fed Chair Jerome Powell and Philadelphia Fed President Patrick Harker in a roundtable discussion with workers, small business owners and community leaders in York, Pennsylvania

- Fed’s Mester speaks on economic outlook at the 50 Club of Cleveland monthly meeting

- Fed’s Williams speaks at 2023 Environmental Economics and Policy Conference

- ECB’s Centeno and de Cos speak at conference on financial stability at the Bank of Portugal

- BOE’s Mann speaks at Redburn/Rothschild Event

- Annual Adipec conference starts in Abu Dhabi

Tuesday, Oct. 3

Economic Data/Events

- Australia building approvals

- RBA rate decision: Bullock’s first meeting as governor; expected to keep rates steady at 4.10%

- India manufacturing PMI

- Mexico international reserves

- US light vehicle sales

- Fed’s Bostic speaks on the economic outlook at Leadership Atlanta’s alumni roundtable

- ECB’s Šimkus and chief economist Lane speak at Lithuania’s central bank conference

Wednesday, Oct. 4

Economic Data/Events

- US factory orders, ADP employment

- Eurozone services PMI, retail sales, PPI

- New Zealand rate decision: Expected to keep rates steady at 5.50%

- Poland rate decision: Expected to cut rates

- Russia GDP

- ECB monetary policy conference in Frankfurt with President Lagarde, de Guindos, and Panetta

- Fed’s Goolsbee speaks at his bank’s annual payments symposium

- Fed’s Bowman speaks at community banking research conference at the St. Louis Fed

Thursday, Oct. 5

Economic Data/Events

- US trade, initial jobless claims

- Australia trade

- France industrial production

- Singapore retail sales

- Spain industrial production

- Thailand CPI

- Third meeting of the European Political Community in Spain

- Fed’s Daly speaks at the Economic Club of New York

- Fed’s Mester speaks at Chicago Fed’s annual payments symposium

- ECB’s de Guindos chairs keynote speech session at monetary policy conference

- BOE deputy governor Broadbent speaks on a panel at the ECB conference

- APAC Family Office Investment Summit starts

Friday, Oct. 6

Economic Data/Events

- US September Change in Nonfarm Payrolls: 170Ke, vs 187K prior; Unemployment Rate: 3.7%e v 3.8% prior; Average Hourly Earnings M/M: 0.3%e v 0.2% prior

- Canada unemployment

- France trade

- Germany factory orders

- India rate decision: Expected to keep repurchase rate steady at 6.50%

- Japan household spending

- Informal meeting of EU heads of state or government in Spain