Sample Category Title

Fed Collins: Be patient and not get ahead of data

Boston Fed President, Susan Collins, offered a cautionary stance on the current monetary policy trajectory in her latest remarks. Addressing the possibility of further rate hikes, Collins noted, "We may be near, we could even be at a place where we would hold" and not lift rates further.

While not ruling out the possibility of future hikes, Collins emphasized a measured approach, stating, "But certainly additional increments are possible, and we need to look holistically and be really patient right now and not try to get ahead of what the data will tell us as it unfolds."

On the topic of inflation, Collins expressed her confidence in the Federal Reserve's capabilities, saying she is "hopeful Fed can bring inflation back to 2% in a reasonable amount of time."

However, she cautioned against making premature judgments about potential rate cuts, remarking it's "premature to send a clear signal about the timing of rate cuts."

How Much Trouble China’s Economy In and Is There Risk for Global Contagion?

China has long been the world’s growth engine, but that status is under threat as its economic recovery has hit a major stumbling block and the high-growth era seems to be well and truly over. Exports are falling, consumers aren’t spending much, bank lending is slowing and the crisis in the property sector only seems to be deepening. Can the Chinese government navigate its way out of this mess, which is partly its own doing, or is there more pain to come?

The post-financial crisis credit boom

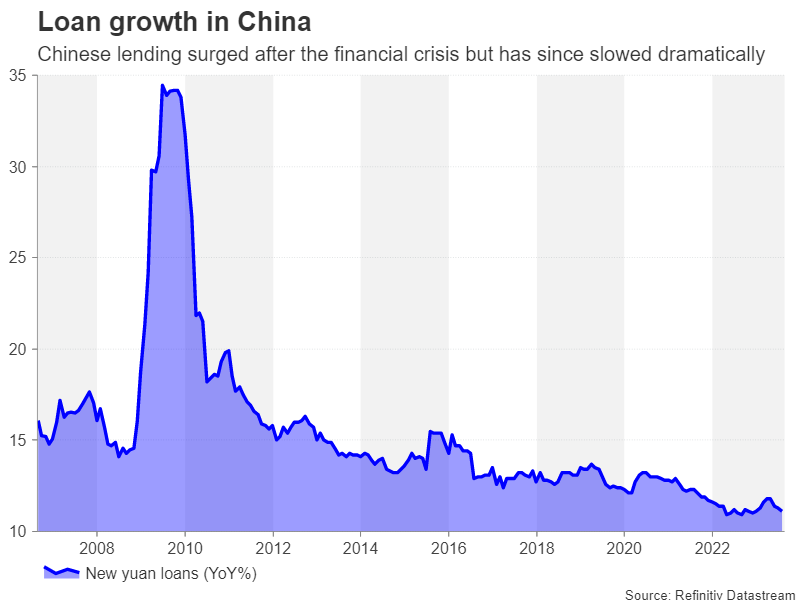

It could be said that China’s current troubles have been a long time coming. Whilst the slowdown became more pronounced after the pandemic, the root of the problem in fact goes back to the 2008 financial crisis. Just as other governments around the world resorted to extreme measures to boost their economies amid a global recession, Beijing came up with its own unorthodox policies to expand credit.

This inadvertently gave rise to the country’s infamous shadow banking sector, through which lending surged and set the stage for an unsustainable property bubble. To be fair to the government, it has made various efforts over the years to deleverage the highly indebted economy. But each attempt has brought about an unduly slowdown in growth accompanied by some form of market panic, forcing authorities to either backtrack some of their reforms or to find alternative backdoor channels for new stimulus.

Alarm bells are ringing in the property sector

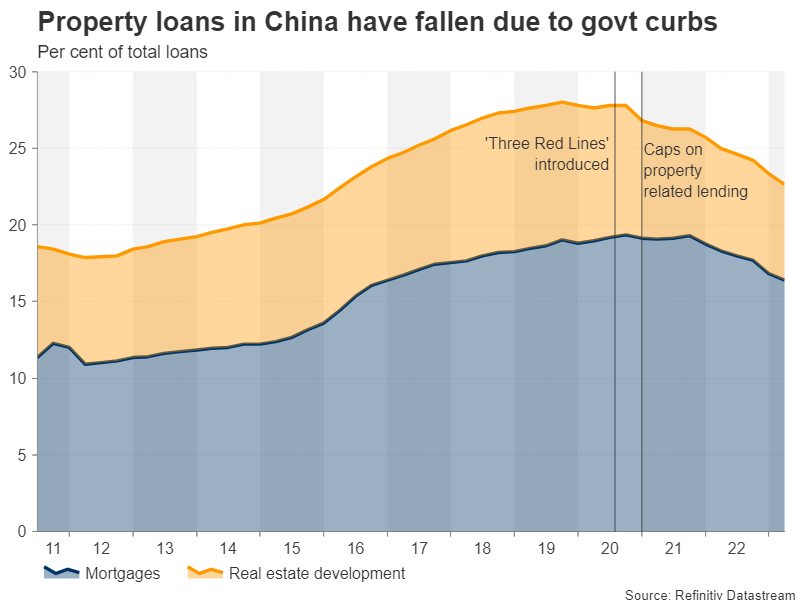

In many ways, the current crisis is no different, yet there are three distinctions that can be made this time round that ought to be raising alarm bells in Beijing. First, the property sector is facing collapse amid some high-profile defaults and many other big developers also drowning in debt.

The government recently eased borrowing restrictions for home buyers and announced more support for ailing developers. But the scandal of unfinished projects is so widespread that buyers have no confidence in the market and half-measures by authorities won’t be enough to prevent existing new homeowners from stopping their mortgage payments nor for potential homeowners to part with their cash. This makes it almost inevitable that more real estate developers will default in the coming months.

A worsening debt problem

But what can the government do about it? Calls for a massive stimulus package keep getting louder but this would only risk fuelling more debt. Doing nothing is also not an option as shadow banks, many of which are state backed, are highly exposed to the property market. Should the real estate crisis spill over to the shadow banking sector, it could spark a broader liquidity crunch in the economy. There are already signs that some trust companies are struggling to meet the payments on their investment products due to liquidity problems.

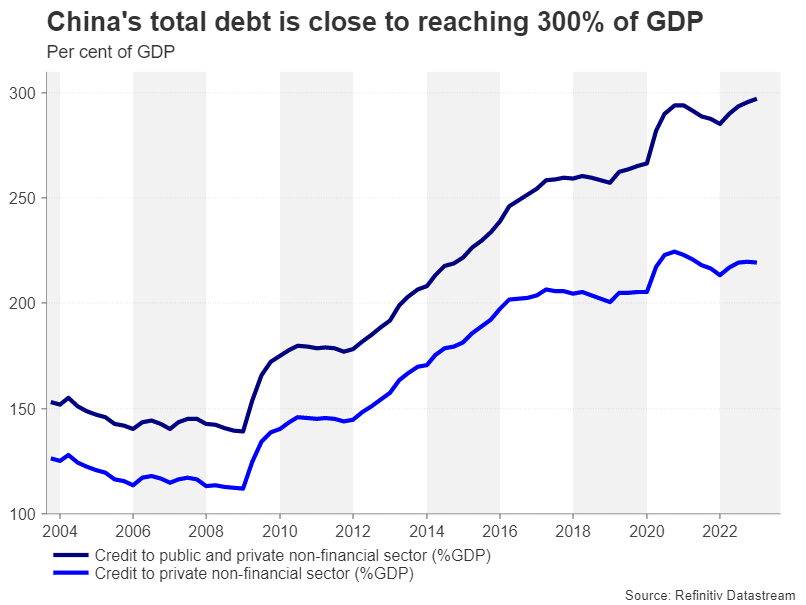

And this takes us to the second distinction about why China’s latest economic woes are more severe than previous ones. China has one of the highest debt-to-GDP ratios in the world, running close to 300% when both public and private credit is combined. What this effectively means is that Beijing has limited scope to boost the economy through more lending, putting policymakers in a bind.

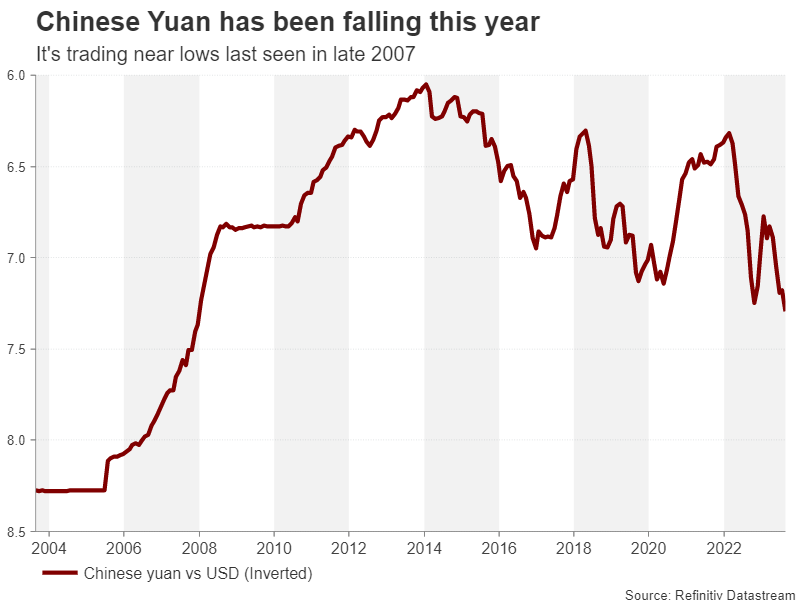

The fact that the government has been reluctant to bring out the big guns demonstrates its unease about adding to the soaring debt mountain. Policymakers’ dilemma has been made worse by speculative attacks on the yuan. The Chinese currency has depreciated by around 5.5% in the year-to-date on the back of the weakening economic outlook. This has tied the hands of the People’s Bank of China when it comes to how much it can cut interest rates at a time when slashing borrowing costs would be the appropriate policy response. The incremental cuts in interest rates have so far had a negligible effect in lifting sentiment, underscoring the need for bolder action.

Exports no longer a growth engine

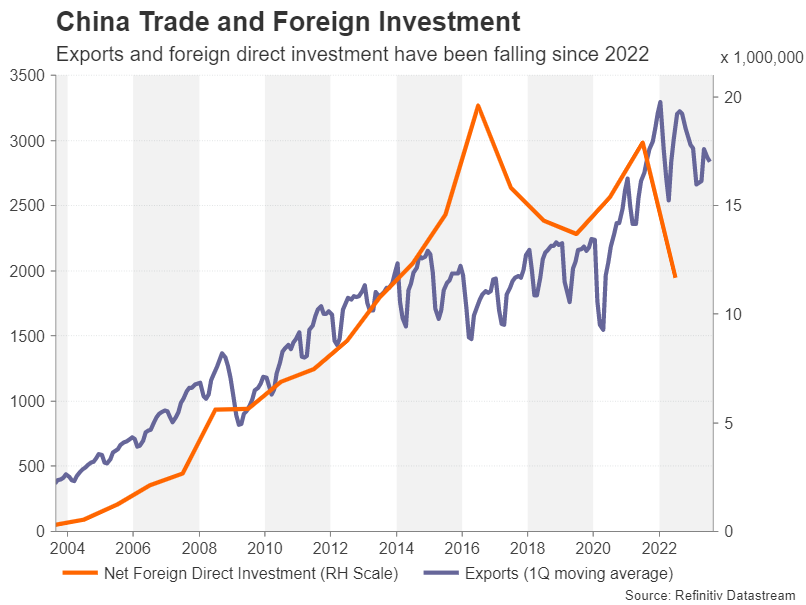

In a further blow for policymakers, exports - the backbone of the economy – have been quite sluggish over the past year and can no longer be relied upon to shore up growth in the hour of need. This brings us to the final point about why the risk of contagion, not just across the entire Chinese economy, but globally as well, is so high.

Although it’s true that rising interest rates in China’s main trading partners are dampening demand for Chinese manufactured goods, it’s not the only cause for the country’s deteriorating external balance. Exports have been on a downward trend since the beginning of 2022 and foreign direct investment last year was the lowest since 2013.

Trump’s trade war lives on

Trade restrictions imposed by the United States finally appear to be taking a toll on Chinese exports. But this isn’t the only setback. Other Western nations are also becoming increasingly wary about doing business with China, while Washington is additionally targeting investment in the country, specifically by US tech firms.

This can partly be explained as a legacy of Trump era policies, which the Biden administration has not only embraced, but also taken to the next level. But Beijing’s more aggressive foreign and domestic policies under Xi Jinping are also a factor as to why China has lost some of its business allure internationally.

The impact on China’s current account balance has been limited, as imports have also been falling during this period. Nonetheless, without substantial new inflow of foreign investment to generate more jobs and demand for exports dwindling, China is running out of options to kick-start growth.

The dreaded devaluation option

With the property mess and rising unemployment weighing on consumer sentiment, and businesses having the added headache of regulatory crackdowns, China is having a major confidence crisis right now and it could only be a matter of time before authorities realize that there may be just one way out of it.

China has yet to contemplate currency devaluation. Its attempts at stemming the yuan’s depreciation suggests this is not a preferred option. However, this has more to do with maintaining stability in financial markets and not being dictated by market forces than not wanting to use the exchange rate to stimulate growth.

The biggest obstacle to devaluating the yuan is the threat of drawing the ire of Washington. Still, if in a few months or even a year from now, the existing policy measures do little in lifting growth and external demand remains subdued, the government might feel justified to turn to its last resort.

A weaker yuan would immediately boost exports as well as free the central bank to pursue looser monetary policy. It wouldn’t solve the property crisis, but it could alleviate the problem by generating more jobs and lowering the debt burden on the economy.

Beijing unlikely to turn West

There is an alternative way of course of achieving all this and that is to mend ties with the West, particularly the US, and to open the domestic market to foreign companies. But such a shift is unlikely to happen anytime soon, if ever.

With the government determined to prevent a large-scale market fallout and at the same time wanting to avoid going down the road of bailouts and handouts, this approach of drip-feed stimulus may well end up being the worst-case scenario as it could lead China towards a Japan-style stagnation.

Could a Lehman-style collapse be a good thing?

However, if a major property developer or even a shadow bank were to collapse, whilst this would undoubtedly have huge ripple effects domestically and globally, it would at least necessitate the government to respond more forcefully, bringing about an economic turnaround sooner rather than later.

As things stand, there is little concern in US and European markets about a spillover from the turmoil in China’s real estate sector. The main worry is the prolonged drag on the global growth outlook.

Aussie and Asian stocks feel the pain

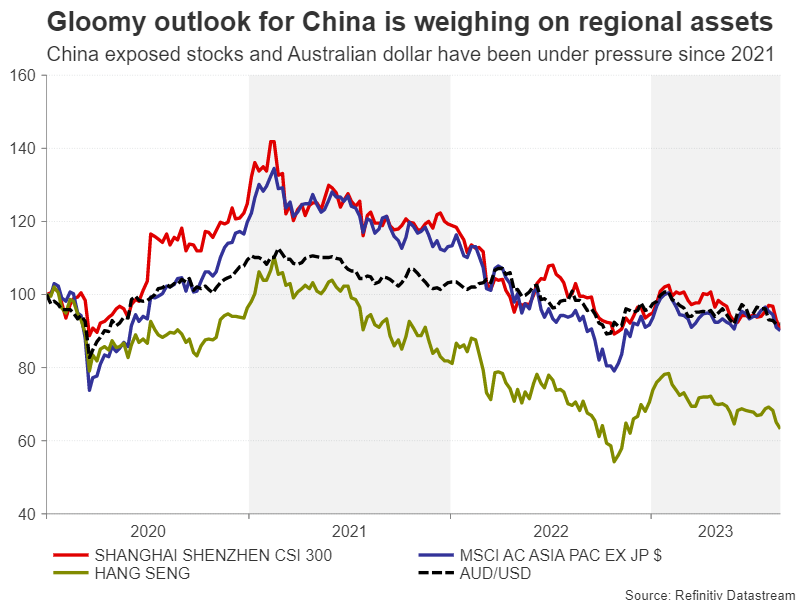

However, for countries that are highly exposed to the Chinese economy such as Australia and New Zealand, their currencies have already been underperforming this year due to the ongoing uncertainties. The slowdown in China was likely a significant factor in the Reserve Bank of Australia’s earlier-than-anticipated pause in its tightening campaign.

The biggest impact, though, has been on regional stock markets. The MSCI AC Asia index (ex. Japan) has declined by over 30% since the 2021 peak when the reopening rally came to a halt. This is in line with falls of around 37% for China’s benchmark CSI 300 index. Worst hit has been Hong Kong’s Hang Seng index, which has plummeted by more than 40%.

Fed Harker: We’ve Probably Done Enough

Philadelphia Fed President, Patrick Harker, shared his insights on the current stance of Fed's monetary policy. Addressing the topic of monetary tightening, Harker said, "Right now, I think that we've probably done enough because we have two things going on."

Elaborating further, Harker mentioned the twin pillars that have influenced his perspective: "The Fed funds rate increases — they are at a restrictive level, so let's keep them there for a while. And also we are continuing to shrink our balance sheet that is also removing accommodation."

Looking to the future, Harker emphasized a data-driven approach, noting, "I see us staying steady throughout the rest of this year, next year is data driven." When prompted about the potential timing of a rate cut, he candidly stated, "Can't predict when Fed will cut rates."

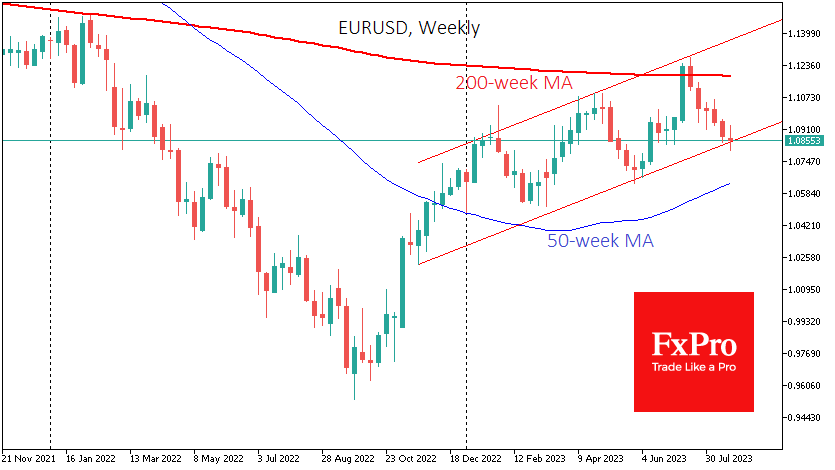

EURUSD’s Battle for the Trend

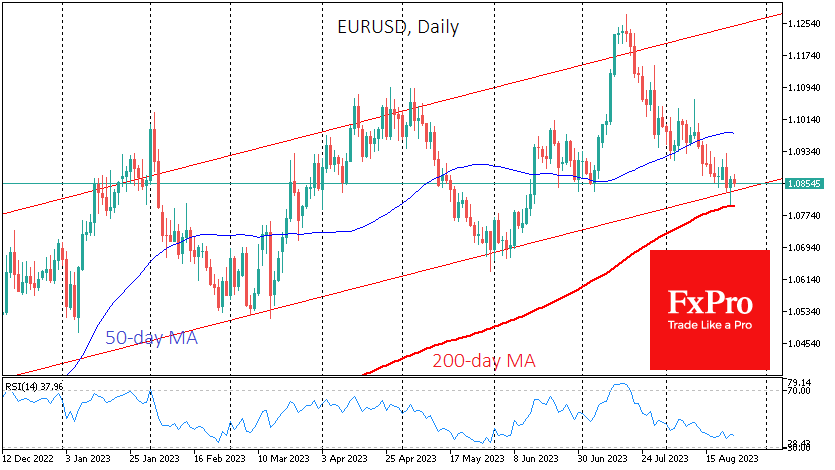

There is an important battle for the long-term trend in the euro-dollar pair. The central bank speeches in Jackson Hole on Friday have enough potential to break or reinforce the direction of the past 11 months.

EURUSD is trading near the 1.0850 level during European trading following Wednesday’s notable moves. The single currency was hit by a sell-off following weak German services PMI data, dragging down the Eurozone Composite PMI.

In minutes, the single currency fell back to the psychologically important round 1.08 level. This is also where the 200-day moving average passes through. These technical factors have rekindled interest in the euro among sellers.

We should also not forget the positive correlation between the single currency and equity indices. The latter’s positive traction helped the EURUSD fully recover, although the move did not develop on Thursday.

The EURUSD is now clinging to the lower boundary of the bullish corridor of the past few months, from which it also reversed in March and early June.

Most likely, the bears haven’t had their last word yet, as the pair hasn’t reached the over-sold region on the daily RSI, even after five and a half weeks of declines, leaving the potential for further drop.

Technically, the bearish reversal followed a failed attempt to break above the 200-week average at 1.12. The single currency has been trading below this since November 2021.

The bears also have the 50-day moving average, which acts as a medium-term trend, on their side. Earlier this month, it turned from support to resistance, taking eight trading sessions. It is, therefore, not surprising that the tug-of-war is intensifying as we approach the long-term trend indicator, the 200-day.

So far, we are seeing more signals in favour of further declines in the pair. However, the most prudent tactic would be to wait for the EURUSD to make a decisive move away from the 200-day moving average. The direction of this breakout promises to be the most accurate indicator of where the pair is headed in the coming months.

If the bulls win, we could see the pair rally to 1.1050 within a few weeks and consolidate the uptrend for months.

A strong EURUSD move below 1.08 in the coming days would be a resounding defeat for the bears, opening a quick path to 1.0650 and the prospect of further weakening the pair to parity in the coming quarters.

Sunset Market Comentary

Markets:

Trading today developed in some kind of interlude as investors pondered the consequences of yesterday’s disappointing PMI’s while at the same time looking forward to the insights from Fed Chair Powell (and ECB president Lagarde) at the Kansas City Fed Jackson hole symposium tomorrow. According to the PMI’s, activity is cooling sharply especially in EMU and the UK. The loss of momentum in the US proved less aggressive. At the same time, an ongoing rise in input costs (especially wages) reaccelerated price rises despite faltering growth. Quite an uncomfortably stagflation mix as centrale bankers have to guide markets on the final stage of their tightening cycle. Regarding today’s data, US weekly jobless declined further/more than expected from 239k to 230k, suggesting ongoing labour market resilience. Headline US July durable goods orders declined a bigger than expected -5.2% M/M (-4% expected) after a strong +4.4% June reading. Capital goods shipments also printed slightly below expectations (-0.2% M/M), but given the volatile nature of these data series, the report still didn’t bring any market relevant message. US yields are ‘rebounding’ 3-4 bps across the curve., with the 2-y yield trying to regain the 5% barrier. German yields maintained yesterday’s decline, changing less than 2 bps across the curve. Equities again show a mixed picture on both sides of the Atlantic. The Eurostoxx 50 at the open tried some catching up with yesterday’s WS gains, but the rebound failed miserably (currently -0.3%). EMU investors apparently stay cautious on recessionary fears, despite yields coming off recent lows. US equites outperform with the S&P 500 opening in green (+0.25%) after yesterday’s rebound.

On FX markets, the dollar yesterday briefly corrected on lower core yields and a better (US-driven) risk sentiment. However, the greenback today again convincingly retakes its rally since mid-July. Maybe yesterday’s (US) data aren’t the trigger yet for Powell to already formally prepare markets for the end of the central bank’s anti-inflationary crusade. EUR/USD at 1.0825 again drops below the 1.0834 support and is nearing yesterday’s low at 1.0804. DXY is closing in on the reaction top just below 104. Similar story for USD/JPY (145.85) with the 146.56 recovery top on the horizon. As was the case yesterday, sterling underperformed the euro. EUR/GBP further rebounded from the 0.854 area to currently trade near 0.857. Very weak UK CBI data on retailing only illustrated the BoE dilemma of fighting unacceptably high inflation with recessionary risk looming. In a broader perspective, almost all smaller currencies (AUD/USD 0.643; NZD/USD 0.5925, EUR/SEK 11.92, EUR/NOK 11.59) face strong headwinds against the majors (USD, Euro) as liquidity conditions are at risk of tightening further.

News & Views:

The Turkish central bank (CBRT) raised its policy rate by a much bigger than expected 750 bps, from 17.5% to 25%. Consensus expected a further increase towards 20%. After two meetings of undershooting forecasts, the central bank now does the opposite. They decided to continue the monetary tightening process in order to establish the disinflation course as soon as possible, to anchor inflation expectations, and to control the deterioration in pricing behavior. Recent indicators point to a continued increase in the underlying trend of inflation, but the committee still expects that disinflation will happen in 2024 (towards the 5% inflation target) in line with the Inflation Report. Monetary tightening will be further strengthened as much as needed in a timely and gradual manner until a significant improvement in the inflation outlook is achieved. In addition to the increase in the policy rate, the Committee will continue to make decisions on quantitative tightening and selective credit tightening to support the monetary policy stance. The Turkish lira strengthens significantly today with EUR/TRY falling from near record level above 29.50 to currently 27.75, the strongest TRY level since June.

Crypto: Bull-Run Now Or Later?

Bitcoin surged by more than 3% to reach over $26,600, recovering from losses incurred in the previous week's drop. Ether also rose by 3.5%, approaching the $1,700 level. Solana's SOL token jumped by almost 7% after integration with Shopify's Solana Pay, enabling USDC stablecoin payments. NEAR, the token of the Near Protocol, gained over 6% following its integration with crypto lender Nexo. Major alternative cryptocurrencies like Cardano's ADA, Polkadot's DOT, and Binance's BNB saw gains of 3% to 5%. Despite these recoveries, experts differ on the future outlook, with some foreseeing a prolonged downtrend due to technical and fundamental factors, while others like Pantera Capital believe Bitcoin won't stay at low prices for long.

BTCUSD - D1 Timeframe

Bitcoin has had quite an eventful couple of days starting from the previous week. The huge decline in price of Bitcoin may at this time have reached it’s terminal point. This is due to the fact that price is currently trading around a demand zone on the Daily timeframe, with additional confluence from the;

Trendline support;

Pivot zone on the daily timeframe; and

The Bullish array of the moving averages.

Analyst’s Expectations:

- Direction: Bullish

- Target: $29,000

- Invalidation: $25,000

ETHUSD - D1 Timeframe

Similar to Bitcoin, we had a slight drop in price of Ethereum also, dropping from its previous high at $1,880 to as low as $1,500. The current price action, however, seems to be heading towards the demand zone on the daily timeframe, since that is the most probable move before a bullish revival. The Fibonacci retracement tool is expected to present ample support in favour of this bullish revival at the 76% and 88% respectively. In the meantime, the most logical course of action is to wait.

Analyst’s Expectations:

- Direction: Bullish

- Target: $1,830

- Invalidation: $1,345

LTCUSD - D1 Timeframe

Despite not being as popular as the previous two we’ve looked into so far, Litecoin (LTCUSD) could yet provide ample opportunity to investors looking for a more affordable investment opportunity in the crypto markets, and quite possibly a better ROI option. At the moment, Litecoin has given off an initial reaction from the pivot zone on the daily timeframe, with a trendline support lying just below the wick. This means we can begin to expect a bullish impulse from LTCUSD in the near-term, once a clear change of market structure has been observed on the lower timeframes.

Analyst’s Expectations:

- Direction: Bullish

- Target: $82

- Invalidation: $53

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

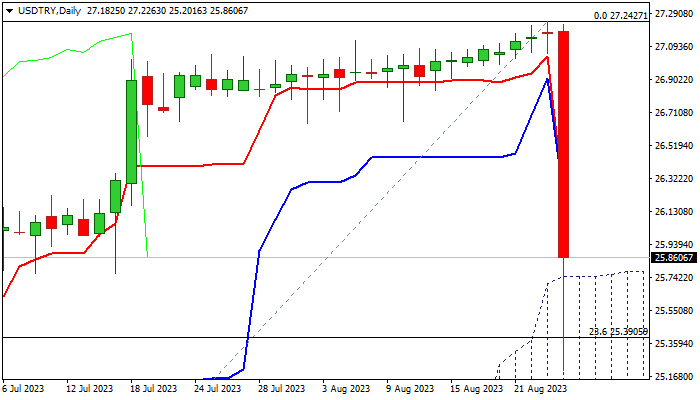

USD/TRY: Turkish Lira Surges after the CBRT Shocked Markets with 750 Basis Points Rate Hike

USDTRY was sharply lower on Thursday, falling two full figures so far, following unexpectedly big CBRT’s rate hike.

Steep fall from new record high (27.242) posted on Wednesday, hit so far the lowest in nearly two months, with prospects for deeper drop, as lira received strong support from the central bank’s latest decision.

The CBRT shocked markets on Thursday by decision to raise interest rates by 750 basis points to 25% vs widely expected 250 basis points hike to 20%.

The decision sparked a rarely seen lira’s rally (the biggest daily advance since Dec 20, 2021) and signal a radical turn in the CBRT’s approach to monetary policy.

Turkish policymakers, among which are three new members, showed unity in making decision and confirmed readiness to act accordingly and in a timely manner to cool high inflation which hit 48% this month.

The subsequent market reaction was very positive, and boost hopes that lira’s larger fall might be running out of steam, as today’s decision shows that the central bankers are determined to put inflation under control and also marks a U-turn from their recent unorthodox approach.

USDTRY was down around 7% in immediate reaction to the central bank’s surprise decision and hit its lowest point in almost two months.

Fresh weakness penetrated thick ascending daily Ichimoku cloud (spanned between 23.206 and 25.751) with close within the cloud to reinforce fresh bearish signals and open way for lira’s further recovery.

Firm break of cracked initial Fibo support at 25.390 (23.6% of 19.390/27.242) would increase bearish pressure and expose next pivotal support at 24.244 (Fibo 38.2%).

Profit-taking after a sharp fall may slow bears, but upticks are expected to be limited and offer better opportunities for selling USDTRY, after the CBRT’s decision changed overall sentiment and made lira attractive for investors after a long time.

Res: 26.222; 26.645; 26.942; 27.242.

Sup: 25.751; 25.390; 25.201; 24.754.

Japan Yen’s Mini-Rally Fizzles, Tokyo Core CPI Next

- Tokyo Core CPI expected to tick lower to 2.9%

- US to release jobless claims and durable goods orders later on Thursday

USD/JPY put together a mid-week rally with gains of 1% but is considerably lower on Thursday. In the European session, USD/JPY is trading at 145.72, up 0.60%.

Markets eye Tokyo Core CPI

Japan releases Tokyo Core CPI on Friday, the third inflation report in just over a week. The previous two releases were for July, but Tokyo Core CPI is the first indicator of August inflation, hence its importance.

The Bank of Japan closely follows core inflation, which excludes fresh food, as it is considered a more accurate estimate of underlying price pressures than headline inflation. But which way is core inflation headed? Last week, National Core CPI eased to 3.1% in July, down from 3.3% in June. However, BoJ Core CPI followed this week with a gain of 3.3%, up from 3.0%.

Tokyo Core CPI eased to 3.0% in July, marking the 14th consecutive month above the Bank of Japan’s 2% target. This is a sign that inflationary pressures remain strong. Little change is expected for August, with a consensus estimate of 2.9%.

The BoJ has insisted that inflation is transient and that without evidence that high inflation is sustainable, such as stronger wage growth, it will not tighten policy. Still, there is speculation that unless inflation falls significantly, we could see the central bank make a shift in policy, especially if the yen remains at such low levels.

USD/JPY Technical

- USD/JPY is testing resistance at 145.54. Above, there is resistance at 146.41

- There is support at 144.51 and 143.64

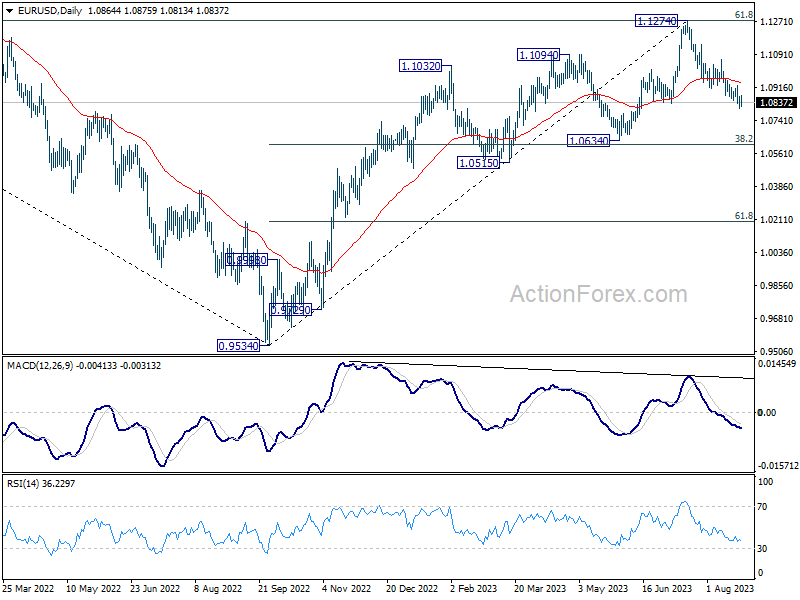

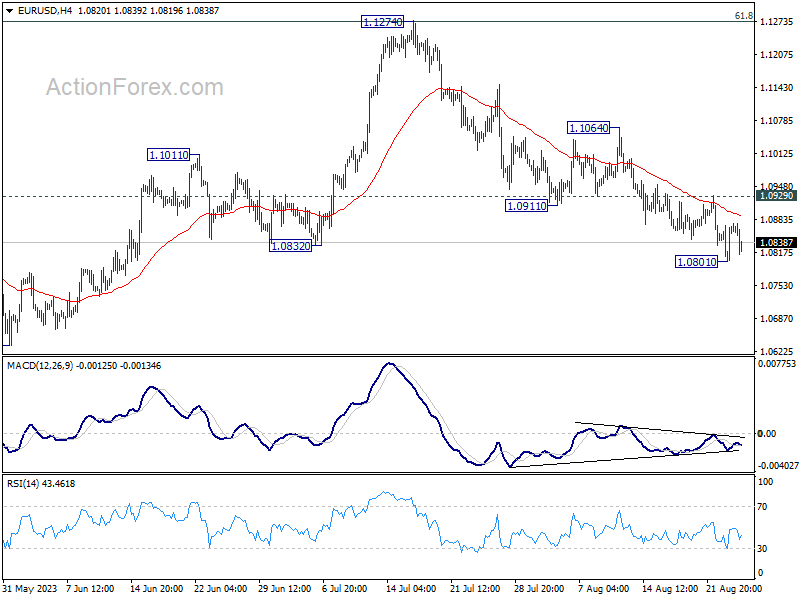

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0820; (P) 1.0846; (R1) 1.0888; More...

Intraday bias in EUR/USD remains neutral for the moment. Further fall is expected as long as 1.0929 resistance holds. Below 1.0801 will resume the decline from 1.1274 to 1.0609/34 cluster support next. Nevertheless, break of 1.0929 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, a medium term top should be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Fall from there is seen as a correction to the uptrend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.