Sample Category Title

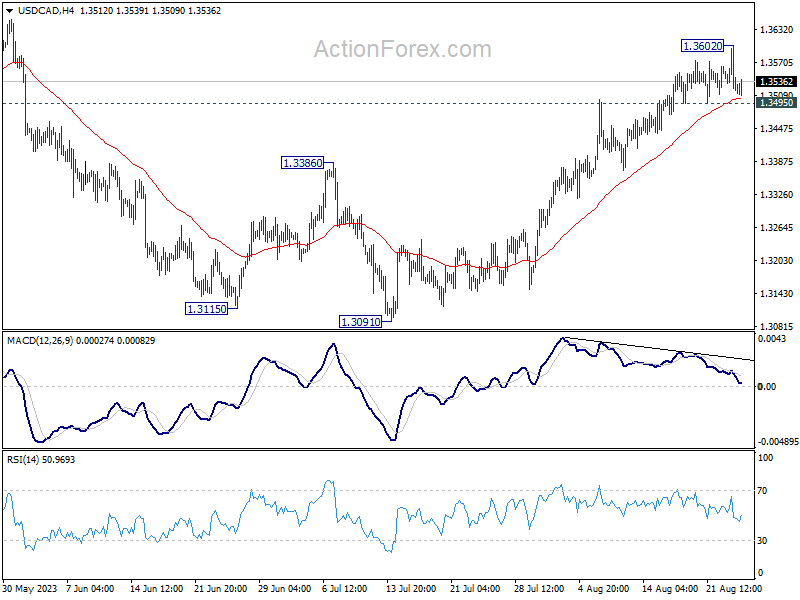

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3495; (P) 1.3550; (R1) 1.3579; More....

Intraday bias in USD/CAD is turned neutral again as it retreat after rising to 1.3602. Above 1.3602 will resume the whole rally from 1.3091 to 1.3653 resistance first. Decisive break there will confirm that correction from 1.3976 has completed, a target a test on this high. However, break of 1.3495 will indicate short term topping, on bearish divergence condition in 4H MACD, and turn bias to the downside for deeper pull back.

In the bigger picture, price actions from 1.3976 are viewed as a corrective fall only. Upon completion, rise from 1.2005 (2021 low) would resume through 1.3976. Next target is 61.8% projection of 1.2005 to 1.3976 from 1.3091 at 1.4309. In case of another fall, downside should be contained by 61.8% retracement of 1.2005 to 1.3976 at 1.2758.

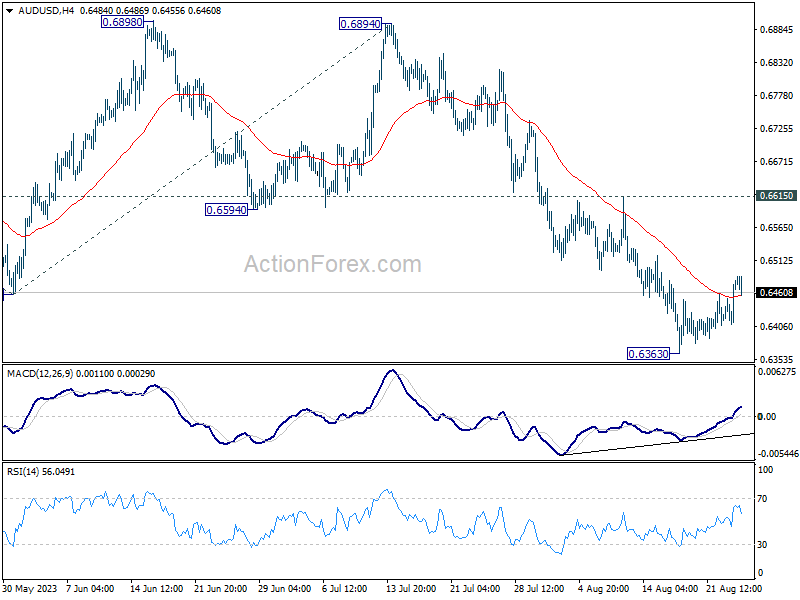

AUD/USD Daily Report

Daily Pivots: (S1) 0.6434; (P) 0.6458; (R1) 0.6506; More...

AUD/USD's recovery from 0.6363 continues today and intraday bias remains neutral at this point. While stronger recovery cannot be ruled out, upside should be limited by 0.6615 resistance. Break of 0.6363 will resume larger fall from 0.7156 to 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195.

In the bigger picture, current development argues that the down trend from 0.8006 (2021 high) is still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

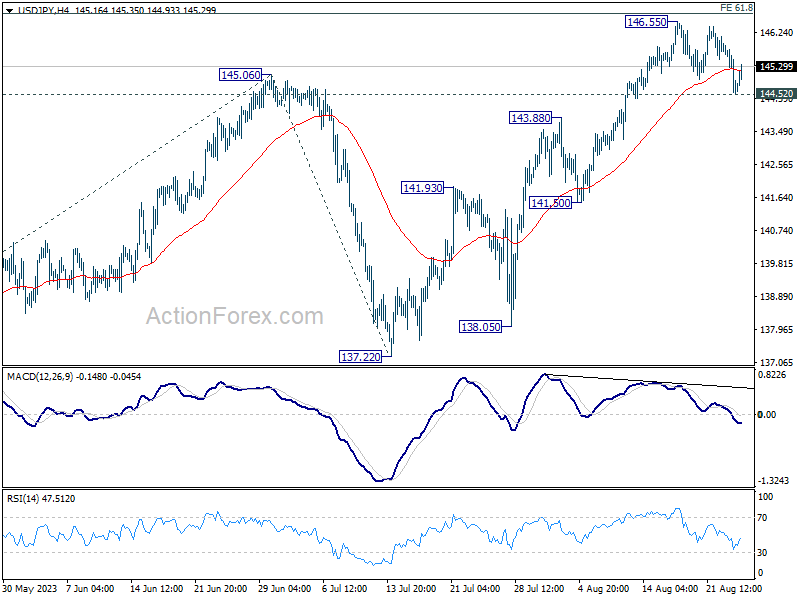

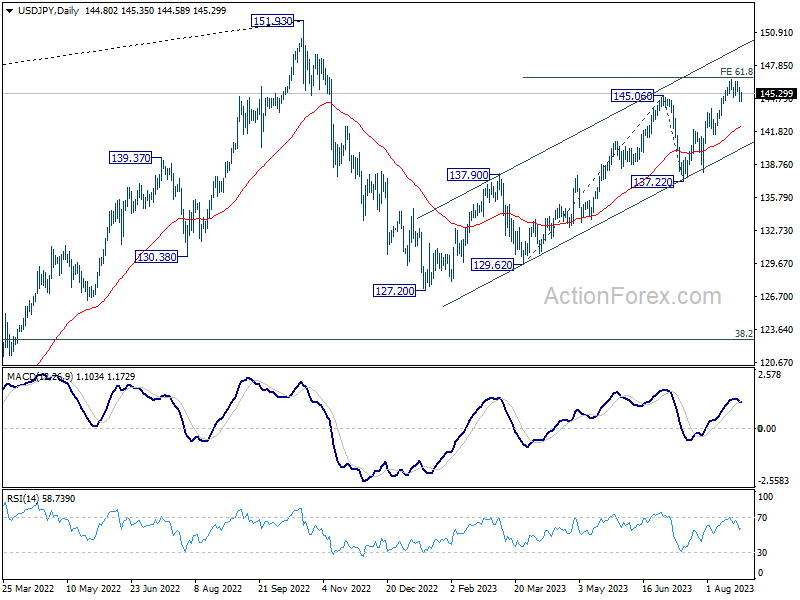

USD/JPY Daily Outlook

Daily Pivots: (S1) 144.29; (P) 145.10; (R1) 145.65; More...

USD/JPY quickly recovered after dipping to 144.52 and intraday bias stays neutral first. On the upside, sustained break of 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76 will pave the way to retest 151.93 high. However, considering bearish divergence condition in 4H MACD, firm break of 144.52 support will be a sign of reversal, and turn bias back to the downside for 55 D EMA (now at 142.30).

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

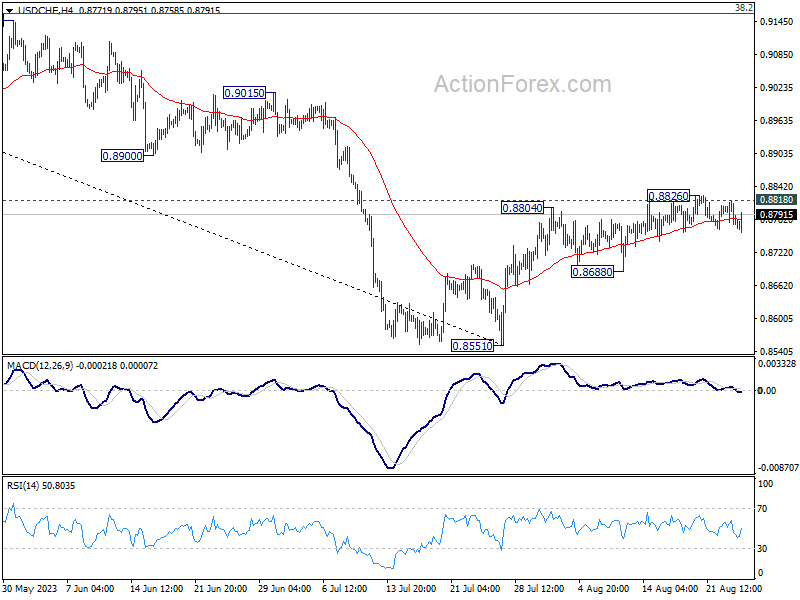

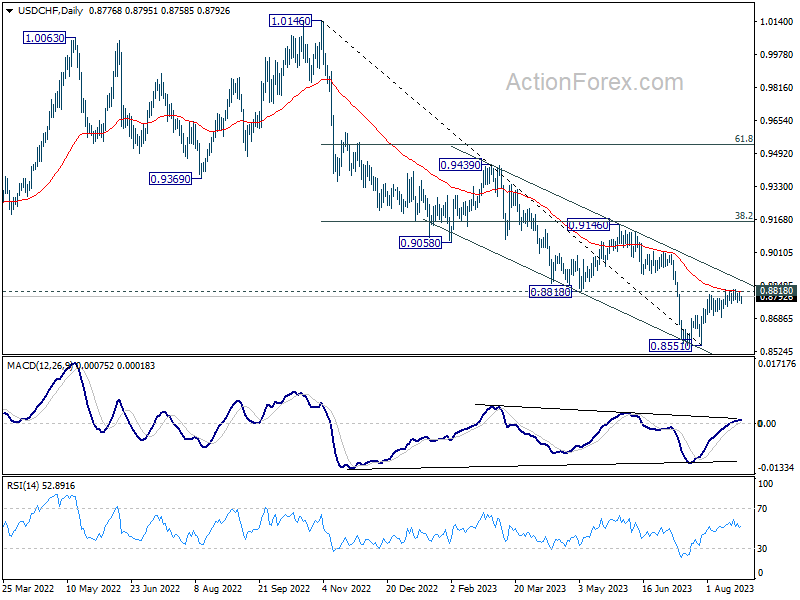

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8763; (P) 0.8790; (R1) 0.8806; More....

USD/CHF is still extending sideway trading and intraday bias stays neutral. On the upside, decisive break of 0.8818 support turned resistance will carry larger bullish implication, and target 0.9146 cluster resistance next. However, break of 0.8688 support will indicate rejection by 0.8818, and turn bias back to the downside for retesting 0.8551 low.

In the bigger picture, a medium term bottom could be in place at 0.8551 already, on bullish convergence condition in D MACD. Sustained trading above 0.8818 support turned resistance will bring further rise to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160), even as a correction. Nevertheless, break of 0.8851 will resume the down trend from 1.0146 instead.

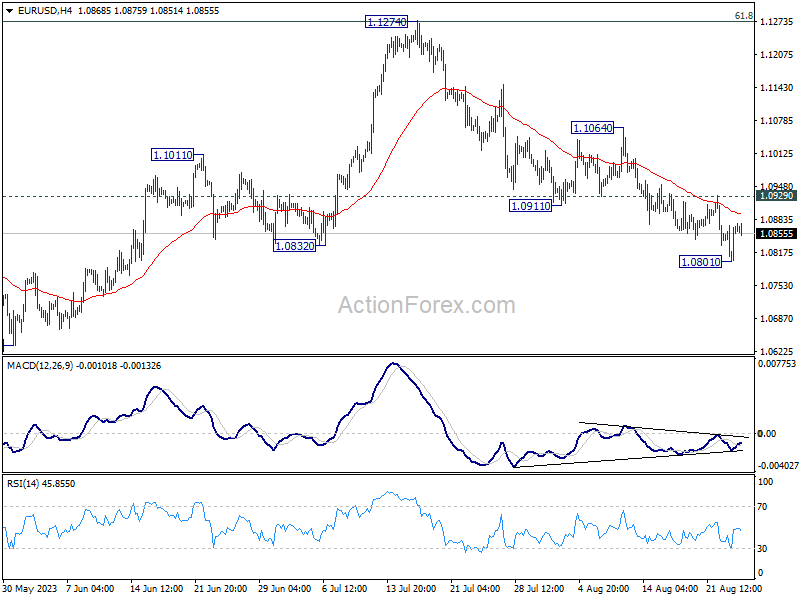

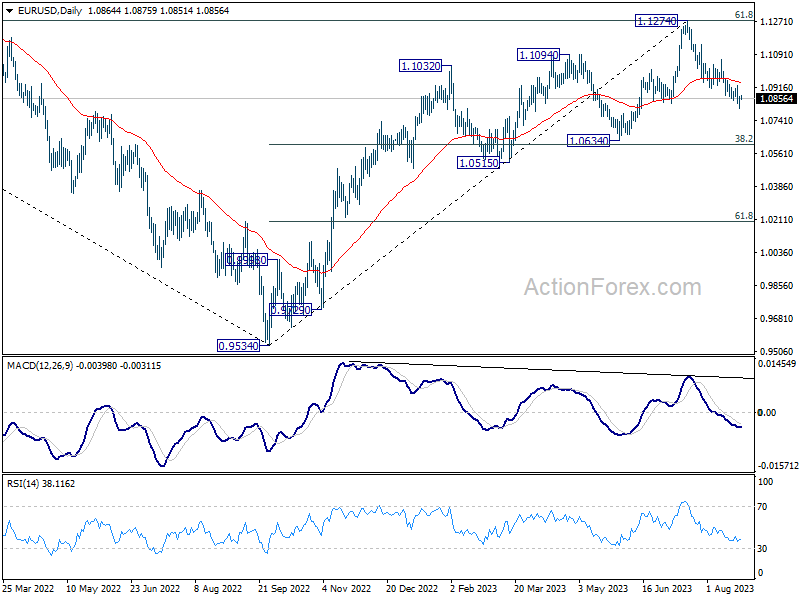

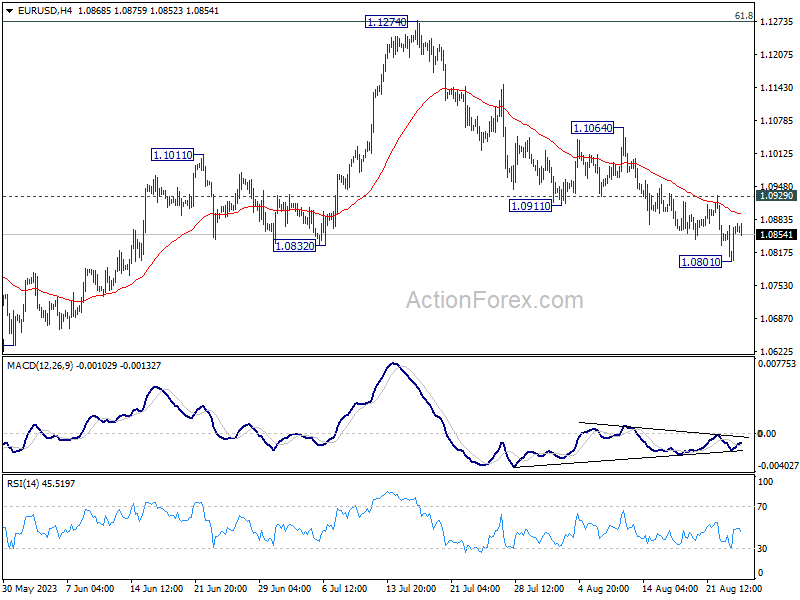

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0820; (P) 1.0846; (R1) 1.0888; More...

Intraday bias in EUR/USD is turned neutral again as it recovered quickly after dipping to 1.0801. Further fall is expected as long as 1.0929 resistance holds. Below 1.0801 will resume the decline from 1.1274 to 1.0609/34 cluster support next. Nevertheless, break of 1.0929 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, a medium term top should be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Fall from there is seen as a correction to the uptrend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.

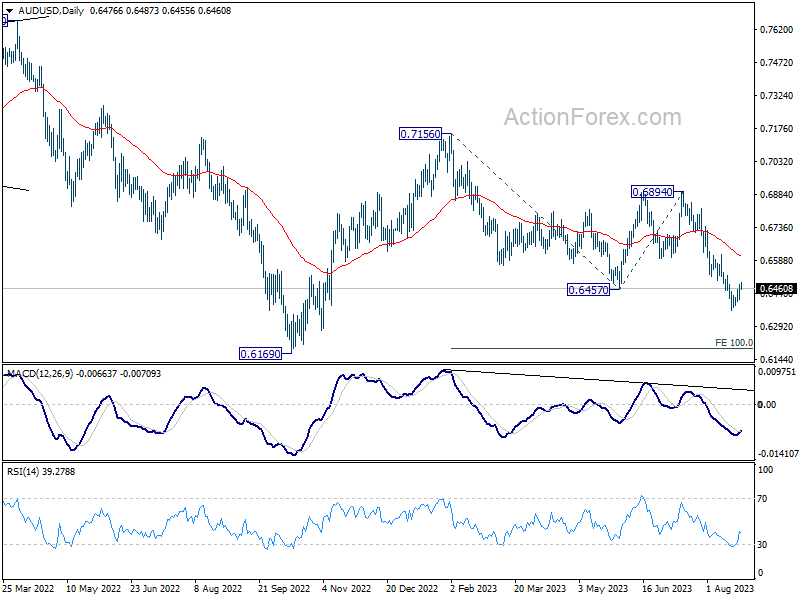

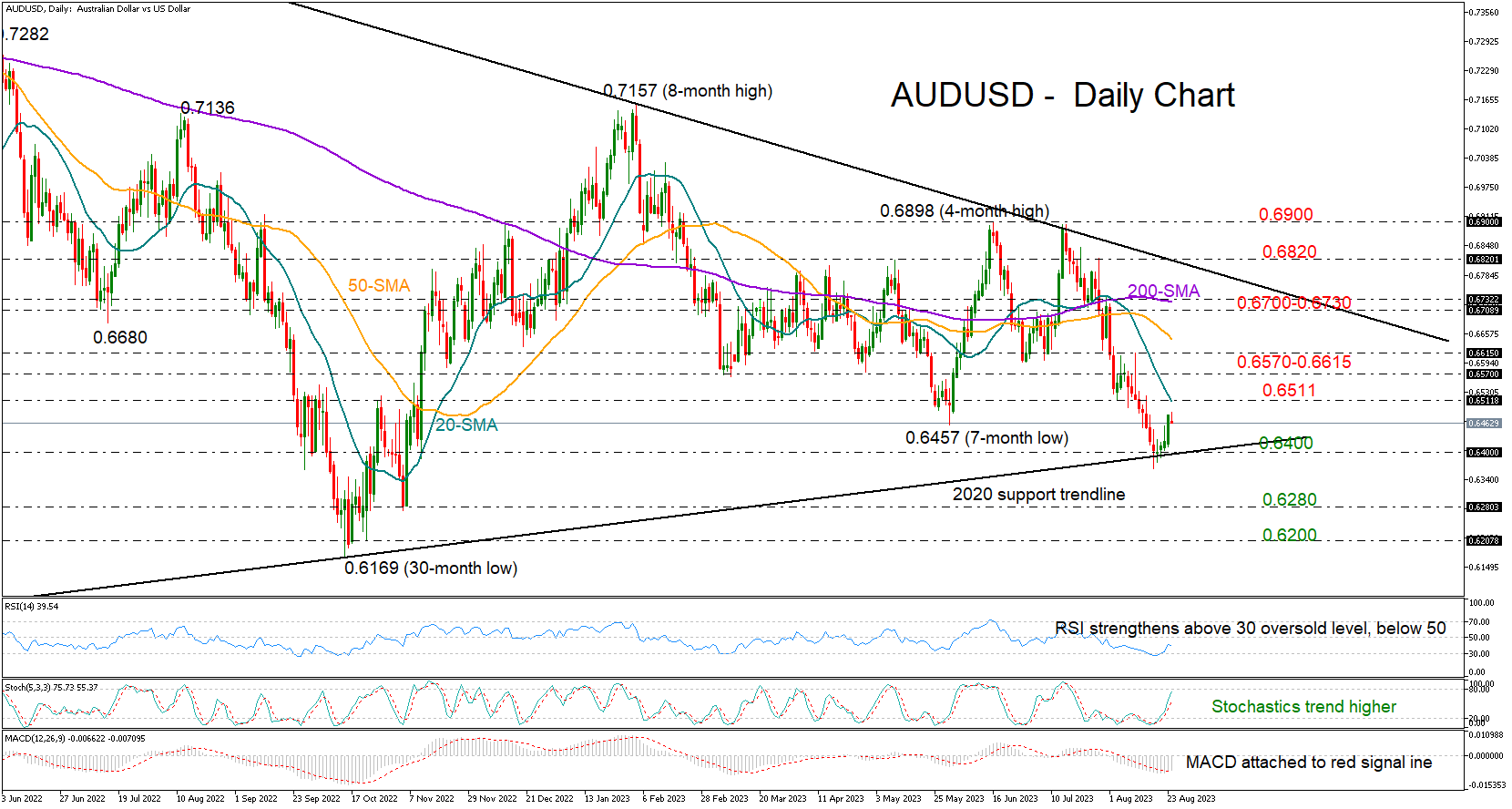

AUDUSD Steps on the 2020 Support Trendline

AUDUSD stayed above the 2020 support trendline after testing it for the third time since the pandemic fallout. This happened after a bearish five-week streak that caused the price to drop to a nine-month low of 0.6363.

The pair is set to post its first weekly gain in five weeks as the price picks up positive momentum towards its 20-day simple moving average (SMA) at 0.6511. The upside reversal in the RSI and the Stochastic oscillator are promoting the upturn in the price, though the former is clearly below its 50 neutral mark, while the MACD is attached to its red signal line despite gradually improving, both preserving some skepticism about how sustainable the rebound in the price is.

If the bulls surpass the 20-day SMA, the next hurdle could occur nearby within the 0.6570-0.6615 constraining zone, where the price stalled a couple of times during the previous months. Above that, the recovery could stretch towards the 0.6700 round level and the restrictive 200-day SMA at 0.6730. Yet, the market's main objective is to break the resistance trendline from April 2022 at 0.6820 after two forceful rejections this year.

Should sellers retake control, the 2020 support trendline would come back under the spotlight near 0.6400. If that floor collapses this time, with the pair diving below the 0.6363 low too, the decline could power up towards the 0.6280 mark taken from October-November 2022. Even lower, the bears are expected to stage another battle within the 0.6169-0.6200 territory and near 30-month lows.

In a nutshell, AUDUSD has again set the foundation for its next bullish phase near the 2020 support trendline, though more efforts will be needed to achieve a bullish bias.

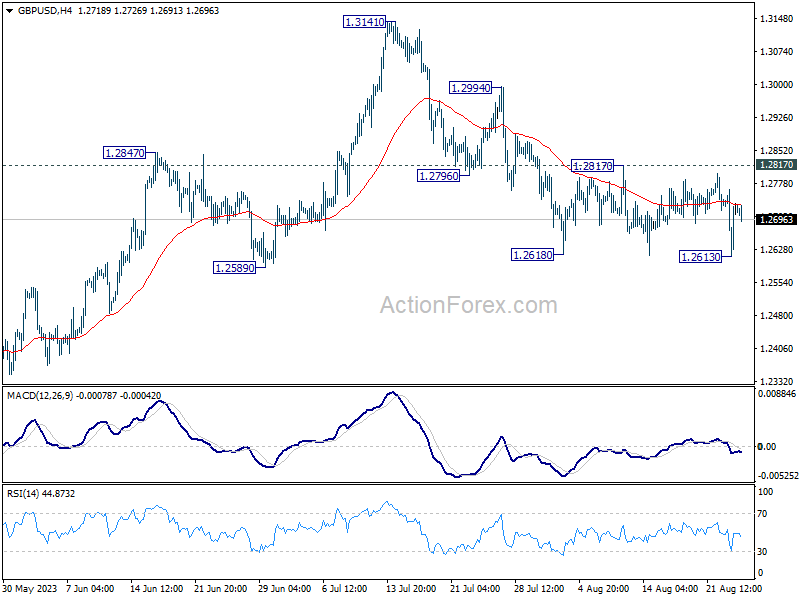

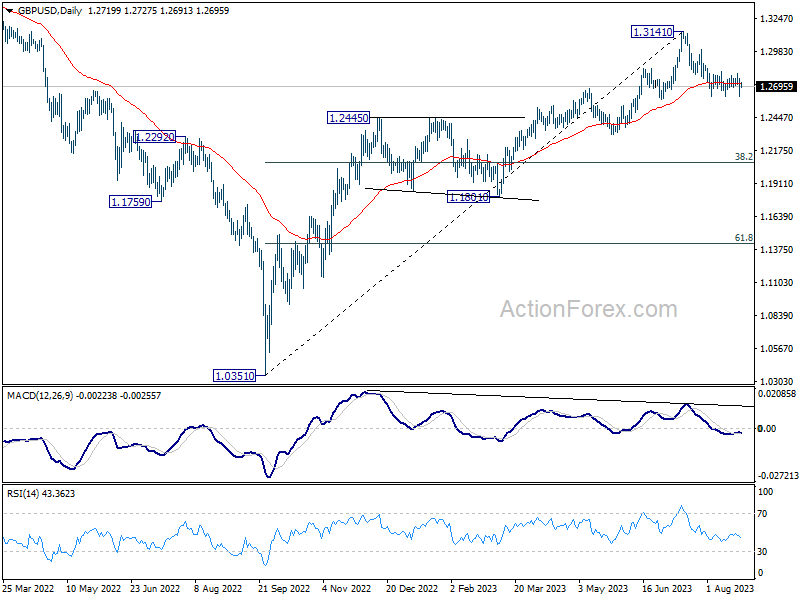

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2638; (P) 1.2702; (R1) 1.2788; More...

GBP/USD is still bounded in established sideway pattern from 1.2618, despite yesterday's volatility. On the downside, firm break of 1.2613 and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, break of 1.2817 minor resistance will indicate that the pull back from 1.3141 has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2723) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

Forex Markets Await Jackson Hole Cues; Dollar’s Position Remains Uncertain

The foreign exchange are mostly stable today, with major currency pairs and crosses staying confined within the boundaries set yesterday. Both Sterling and Euro have had a lackluster week, emerging as the weakest performers. US Dollar, while subdued, still fares better, positioned ahead of Canadian Dollar as the third least impressive for the week.

In an unexpected turn, Australian Dollar has taken the lead as this week's strongest contender, with New Zealand Dollar following closely. Yen, meanwhile, is mixed amidst these shifts.

Today's economic docket is relatively thin, spotlighting only US jobless claims and durable goods orders. However, neither is anticipated to induce significant market ripples. Instead, all eyes are glued to the unfolding developments at the Jackson Hole Symposium.

On the technical front, the Dollar's momentary surge from yesterday lost momentum just as swiftly. Yet, the greenback hasn't witnessed any pressing sell-off. As long as 1.0929 minor resistance in EUR/USD and 1.2817 in GBP/USD hold, further rally is expected in the greenback. Break of 1.0861 and 1.2613 temporary lows will suggest Dollar buyers are back in.

In Asia, Nikkei closed up 0.87%. Hong Kong HSI is up 1.87%. China Shanghai SSE is up 0.18%. Singapore Strait Times is up 0.28%. Japan 10-year JGB yield is down -0.0158 at 0.662. Overnight, DOW rose 0.54%. S&P 500 rose 1.10%. NASDAQ rose 1.59%. 10-year yield dropped -0.13 to 4.198.

Eyes on NASDAQ's next move after Nvidia's earnings triumph boosts confidence

Investor sentiment is given a strong lift as Nvidia's earnings results demolish expectations, despite a high bar set for the AI darling. The strong performance was driven by its data center business, which includes the A100 and H100 AI chips that are needed to build and run artificial intelligence applications like ChatGPT. The company also said it expects fiscal third-quarter revenue of about USD 16B, suggests sales in the current quarter will grow 170% from the year-earlier period.

NASDAQ traders jumped the gun and pushed the index up 1.59% on close, before the Nvidia's earnings announcement. The development now argues that pull back from 14446.55 has completed at 13161.76, just ahead of the medium term channel support, as well as 38.2% retracement of 10982.80 to 14446.55 at 13123.39.

More importantly, if this turn out to be true, rise from 10088.82 should then remain intact for another high above 14446.55. The upside momentum for the rest of the week, in particular in reaction to Fed Chair Jerome Powell's Jackson Hole speech, would be watched to decide the odds of this bullish scenario.

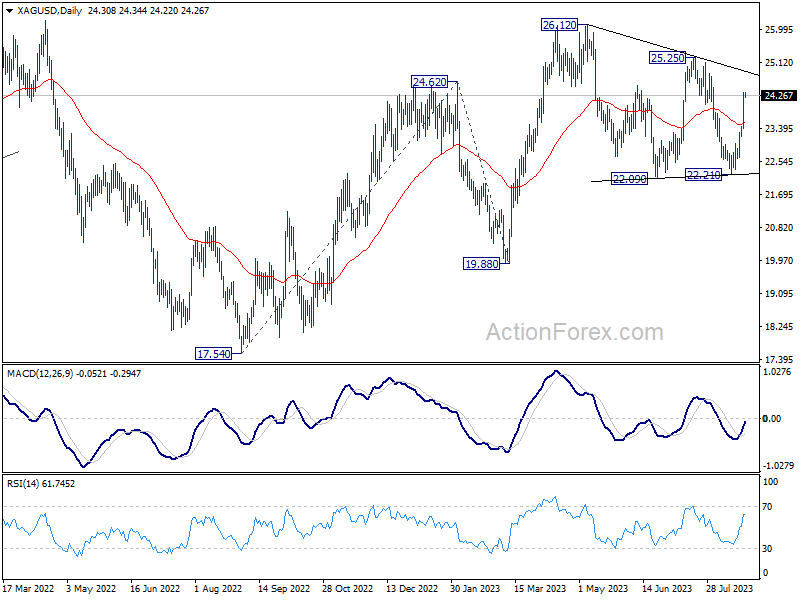

Silver accelerates up, taking Gold higher

Silver's impressive rally intensified yesterday, pulling Gold upwards in its wake. This surge seems to be a direct response to the retracement of benchmark treasury yields in both the US and Europe, which were affected by less-than-stellar PMI figures. Market sentiment is now swaying towards the belief that major central banks might be quickly approaching the finale of their tightening cycle. All eyes are set on upcoming Jackson Hole Symposium. While the spotlight is certainly on the speech by Fed Chair Jerome Powell, insights and comments from other prominent central bankers are also poised to influence market directions.

Technically, Silver's strong break of 55 D EMA affirms the case that consolidation pattern from 26.12 has completed with three waves to 22.21. Further rise is now expected as long as this 55 D EMA (now at 23.56) holds, to 25.25 resistance first. Decisive break there should confirm this bullish case, and should also resume whole up trend from 17.54 (2022 low). Next target would be 100% projection of 17.54 to 24.62 from 19.88 at 26.96.

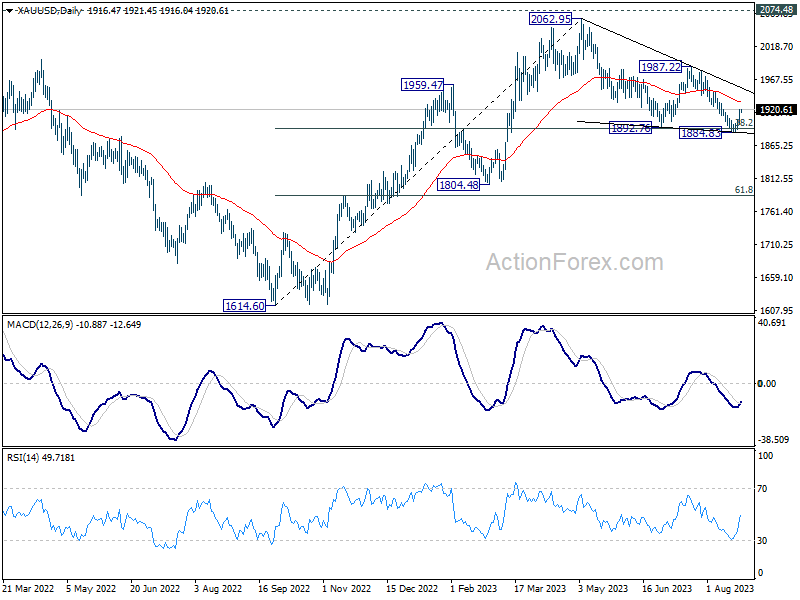

As for Gold, a short term bottom is in place at 1884.83, with D MACD crossed above signal line. Further rebound is now in favor to 55 D EMA (now at 1932.52). Sustained break there will argue that whole corrective pattern from 2062.95 has completed with three waves down to 1884.83, after defending 38.2% retracement of 1614.60 to 2062.95 at 1891.68. Stronger rally would then be seen to 1987.22 resistance to confirm this bullish scenario.

Looking ahead

US jobless claims and durable goods orders will be released today. But attention will definitely be on news flows out of Jackson Hole Symposium.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2638; (P) 1.2702; (R1) 1.2788; More...

GBP/USD is still bounded in established sideway pattern from 1.2618, despite yesterday's volatility. On the downside, firm break of 1.2613 and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, break of 1.2817 minor resistance will indicate that the pull back from 1.3141 has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2723) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 12:30 | USD | Initial Jobless Claims (Aug 18) | 241K | 239K | ||

| 12:30 | USD | Durable Goods Orders Jul | -4.00% | 4.60% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Jul | 0.20% | 0.50% | ||

| 14:30 | USD | Natural Gas Storage | 35B |

Today’s Eco Calendar Unlikely to Inspire Trading

Markets

Global PMI’s called off ongoing tests of key technical resistance levels (cycle highs) in core bond yields. Both the August EMU and UK composite gauges flashed the recession alarm, diving below the 50 boom/bust mark as the services sector joined the ongoing slump in manufacturing. Unfortunately for Europe, this is accompanied by sector input prices and wages increasing at an accelerated pace. As a result, the ECB may be more reluctant to pause the hiking cycle in September than the headline PMI figures suggest. The biggest drag came from a steep drop in the German services sector. The UK downward surprise was even bigger than the European one with July and August PMI’s suggesting a 0.2% Q/Q GDP decline in Q3 so far. Companies reported reduced orders and a further pull-back in hiring. Price pressures are moderating, but not at a sufficient pace to keep the BoE from hiking in September. Core bonds rallied (short squeeze) with German yields ending 9.5 bps (30-yr) to 13.5 bps (5-yr) lower. UK gilt yields tanked 13.9 bps (30-yr) to 19.2 bps (5-yr). The euro lost ground on first national releases with both EUR/USD and EUR/GBP losing first support levels at 1.0834 and 0.8504 respectively. The break in EUR/GBP was rapidly undone by the UK PMI, but also EUR/USD returned to opening levels to eventually close at 1.0863. The 200d moving average around 1.08 proved to tough to crack. European stock markets eventually closed near unchanged not knowing whether to cheer for the fallback in rates or to worry about weak PMI’s. The US PMI decreased as well, but both services and composite measures held above the 50-line. The release didn’t provoke much additional market reaction. In other economic news, the Bureau of Labour Statistics downwardly revised payroll growth in the year through March by 306k. That’s less than the 500k whisper number and doesn’t fundamentally change the underlying picture of a resilient and robust US labour market. US yields fell 7.7 bps (2-yr) to 13.2 bps (10-yr) yesterday. US equity markets rallied up to 1.1% for the S&P and 1.6% for Nasdaq, anticipating strong results by Nvidia. The latter even exceeded lofty expectations after US close, sending the share another 6% higher in after-market trading and lifting spirits in Asian trading this morning. Today’s eco calendar is unlikely to inspire trading with July durable goods orders and weekly jobless claims. Speeches by Philly Fed Harker and by Boston Fed Collins are wildcards. Overall market positioning is again more neutral after yesterday’s correction and going into tomorrow’s key Jackson Hole speeches. It lowers the probability to see high profile technical breaks in FI/FX and stock markets.

News and views

The Bank of Korea this morning unanimously decided to keep its policy rate unchanged at 3.5%. The BoK last raised its policy rate in January. In new forecasts, the central bank expects the economy to grow 1.4% this year (unchanged from May). Growth for next year was slightly downwardly revised from 2.3% to 2.2% reflecting the impact of slower growth in China. Consumer price inflation this year is still seen at 3.5%, but core was slightly upwardly revised to 3.4%. Next year, inflation is expected at 2.4%. At the news conference, Governor Rhee admitted that there might be arguments to give more weight to growth, but inflation remains the most important with financial stability also an important topic. The BoK is concerned over high levels of consumer debt. According the Rhee, six board members kept the door open for one more rate hike if necessary. The won recently lost against a strong dollar. It strengthened to USD/KRW 1321 this morning, to be compared with a ST low of 1343 last week.

In an interview with the newspaper Hospodarske Noviny, Czech central Bank Member Jan Kubicek indicated that sales of returns on the CNB’s foreign reserves will be done in a way that will affect the FX market as little as possible. The sales of returns shouldn’t have the effect of FX interventions. Sales are a way to manage the bank’s balance sheet. They are not a policy tool. Kubicek also indicated that the CNB sees the neutral long term nominal interest rate at a level of near 3%.

Weak PMI Data Set Tone for Markets

Market movers today

The data calendar is relatively light today, with US capital goods orders and weekly jobless claims as the most interesting.

Also, we will get a rate decision from the Central Bank of Turkey, where we are likely to see a hike from the current 17.5% as inflation is again accelerating. We have no guidance about the size of the hike, and analyst expectations range from 100bp to 250bp. We expect that hikes will continue and the rate eventually reach 25%.

The 60 second overview

Weak PMI for the US and euro area: PMI data disappointed yesterday in both the US and Euro area pushing bond yields lower while supporting equities as expectations for further hikes from the Fed and ECB were scaled back. In the US Composite PMI dropped to 50.4 in August from 52.0 in July with declines in both manufacturing and services. The European PMI figures also came out much weaker than expected with services showing renewed signs of slowing. The German Services PMI numbers stood out with a massive 5 index points decline, which has only happened three times before with the latest being in March 2020 during the Covid-19 lockdown.

Chinese markets calm down: In China financial stress has calmed somewhat for now as equities has rebounded around 3% from the low reached on Tuesday. It is supported by improving global risk sentiment and strong tech performance as tech companies deliver decent earnings and a stronger outlook, while having very low valuations after the past years' violent sell-off. With selling pressure easing bottom fishers have come back and drive the gains in stocks. However, the underlying problems in Chinese housing and the shadow banking system are still there and financial stress could come back if we get more bad news on this front. New home prices in July saw a bigger decline than in the past months and with the stress on China's developers the downward pressure on new home prices could intensify as they aim to sell more homes to raise cash.

Nvidia beat expectations: Speaking of tech, the leader of AI chips, Nvidia, crushed already high expectations with better-than-expected Q2 earnings and stronger guidance than seen by analysts. Earnings have quadrupled over the past year as the company is at the centre of the new AI drive.

Prigozhin reported dead in plane crash: Head of the Russian Wagner Group Yevgeny Prigozhin died in a plane crash yesterday together with other leaders of the Wagner Group, see Reuters. His fate was increasingly uncertain after he staged a mutiny earlier this year and his death leaves open what the future of the Wagner Group will be.

BRICS set to expand amid disagreements: BRICS leaders meeting in South Africa are struggling to finalise criteria for admitting new members into the club amid disagreements on how high the bar should be. While China seems to work on a wider expansion, India has supposedly in last minute suggested a GDP per capita criteria, which may exclude some potential members. The BRICS stated goal is to champion the interests of the Global South while several of the members have stressed it is not an organisation to oppose G7.

Equities: Global equities rose yesterday, and the non-top-down driven market ended. PMIs the triggered the lift to equities, not as one would expect in 19 out of 20 times because of strong PMIs but instead because of weak PMIs. The weak PMI's resulting in yields plummeting across the curve and across countries. Hence, the fear of too high inflation and central overtightening fell and triggered the equity rally. As expected, materials and energy underperforming in this this inflations-relief rally. In US +0.5%, S&P 500 +1.1%, Nasdaq +1.6% and Russell 2000 +1.0%. Asian market continuing higher this morning and the same is the case for European and US futures. Market optimism fuelled by the Nvidia earnings report out after the US close yesterday.

FI: European bonds rallied on yesterday's weak PMI data, with the 10Y German government bond yield declining by close to 13bp throughout the day and the EUR swap curve (2s10s) reinverting a few bps. The ECB pricing was much impacted by the weak signals. Markets are now pricing in a 3% probability of a 25bp hike at the September meeting (vs. 55% prior to the PMIs), while the peak deposit rate is trading 7bp lower at 3.90%. The 5y5y EUR inflation swap rate declined by 3bp to 2.60% during the session, which is, though, still close to the highest level recorded since 2009.

FX: EUR/USD seesawed through yesterday's session taking its cue from PMI figures from first the Euro Area and then the US. In the end, the cross closed slightly higher on the day. The GBP weakened on the back of signs of deteriorating growth momentum, and after a couple of weeks' strong GBP performance we decided yesterday to close our tactical short of GBP/CHF.

Credit: Credit indices continued to perform yesterday where iTraxx Xover tightened more than 10bp and Main 2.3bp. Primary market activity remains relatively low, but a few transactions were priced, including German auto parts manufacturer, Continental.

Nordic macro

This morning Statistics Sweden (SCB) releases Q2 construction data where the focus is mainly on dwellings starts, vendor Byggfakta's indicator suggest a bottoming out of starts in Q2. In addition, SCB releases the Q2 Savings Barometer which is a preliminary estimate of household savings and balance sheets later published in Financial Accounts.