Sample Category Title

WTI Oil: Prices Accelerate Lower on Fresh Demand Concerns

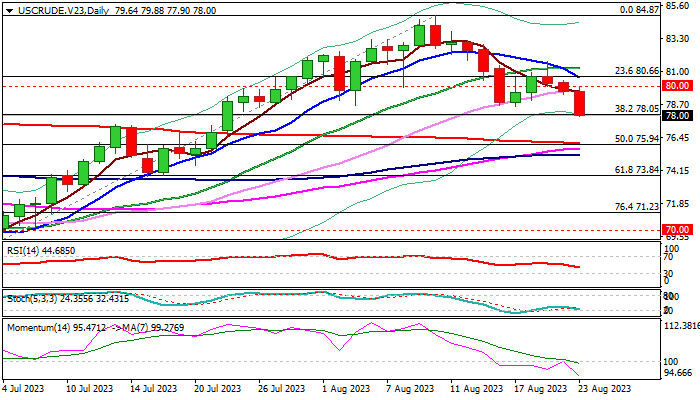

WTI oil price fell around 1.6% on Wednesday after weak manufacturing data from Japan, Eurozone and Great Britain (PMI’s stay in contraction territory below 50 threshold) raised concerns about demand and further soured near-term sentiment.

Acceleration of a bear-leg off $81.71 (Aug 21 recovery peak) broke through $78.58 (Aug 17 higher low) and cracked pivotal Fibo support at $78.05 (38.2% of $67.02/$84.87) generating fresh bearish signal for deeper drop (signal to be confirmed on close below $78.05) towards next targets at $76.03/$75.94 (200DMA/50% retracement).

Weakening technical structure on daily chart (14-d momentum remains in negative territory and started fresh decline, south-heading RSI below neutrality zone and multiple bear-crosses of 5/10/20/30DMA’s) contribute to bearish near-term outlook.

Resistances at $78.58/$79.02 (Aug 17/18 lows) should cap and keep intact upper pivots at $80.00/66 (psychological/10DMA) violation of which would sideline bears.

Res: 78.58; 79.02; 79.62; 80.00.

Sup: 76.41; 76.02; 75.17; 74.50.

Rate Expectations Pared Back as PMIs Point to Recession

European stocks have given back the bulk of their gains this morning as flash PMI data points to a possible recession over the remainder of the year.

The UK readings were particularly stark, with both the services and manufacturing PMIs falling well short of forecasts and the former deep into contraction territory. What's more, the weakness was quite widespread from new orders to hiring, which suggests we're not just talking about a blip in the data, but rather the prospect of a recession in the second half of the year.

From the Bank of England's perspective, there's a lot within the data that will be viewed as encouraging, with slower employment resulting in less tightness in the labour market and lower prices paid across manufacturing and services sectors indicating easing inflationary pressures, in theory at least.

The surveys alone won't be enough to convince the MPC and another rate hike in September looks a near-certainty but beyond that, traders have been paring back expectations on the back of these releases, with only one more then priced in this year.

ECB may be convinced to hold in September after latest data

The data from the eurozone was no more promising, particularly Germany - the bloc's largest economy - which has had a harder year than most and looks likely to continue to do so going into next year.

There was a slight and unexpected improvement in the manufacturing number, albeit from a very low base and it still remains deep in contraction territory. But services contracted against expectations and the number was some way below forecasts and the July reading.

Interest rate probabilities were pared back in the eurozone this morning too, with traders viewing the meeting in a few weeks as a coin toss between standing pat and another 25 basis point hike. Another hike is far from guaranteed in the cycle and today's data certainly supports the case for pausing to see what impact past tightening has had.

European PMIs see oil accelerate lower

Oil prices are drifting lower again this morning on the back of the European PMIs and in a sign that traders may have an eye on Jackson Hole later this week. Economic resilience has been a key feature globally this year but we may finally be seeing interest rates taking their toll just as traders began to accept they may need to stay higher for longer.

Policymakers have been at the more hawkish end of the spectrum for some time and traders were increasingly coming around to the idea that rates won't fall as soon or as quickly as they hoped. Today's numbers may help the case for that not to be the case but they'll need to be backed up by plenty of hard data to convince central banks.

Supply restrictions have enabled prices to move into a higher range over the last month but that will only be sustained as long as economies continue to display the kind of resilience they have until now. Avoiding a recession was the goal of central banks but now it may be a case of aiming to keep it shallow.

Will central banks maintain hawkish stance at Jackson Hole?

Gold has pared losses over the last few days to trade around $1,900, with traders eyeing Jackson Hole for hints about future monetary policy moves. The event has, on occasion, been used as a platform to communicate a significant shift in approach, and with the Fed and others nearing or at the end of their tightening cycles, there's every chance it's used in a similar manner again.

That said, the prospect of the Fed and others becoming suddenly dovish is not realistic. While they may indicate the tightening cycle is likely over, which would be a big shift in the communication, they will almost certainly push back at the prospect of rate cuts in the foreseeable future.

Considering gold has been forced lower by the prospect of higher rates for longer, it would likely take an attempt to cool that speculation to trigger a significant recovery. Confirmation on the other hand may contribute further to its decline, potentially solidifying the break below $1,900.

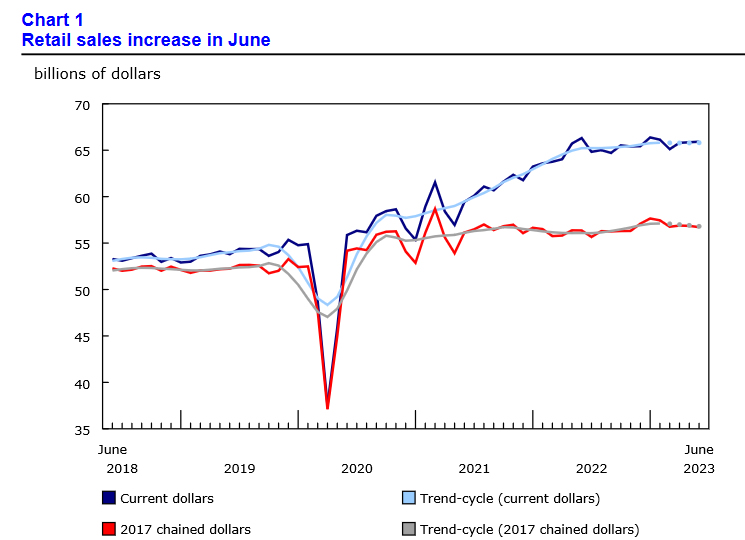

Canada: Retail Sales Eke Out Another Gain in June Finishing Second Quarter on a Weaker Note

Retail sales rose 0.1% month-on-month (m/m) in June, coming in a tad stronger than the flat reading reported in Statistics Canada's advance estimate. May's print was revised down to 0.1% m/m from 0.2% reported originally.

Adjusting for inflation, the volume of retail sales was 0.1% lower on the month.

Defying expectations, sales at motor vehicle and parts dealers accelerated, gaining 2.5% m/m on the back of strong demand for new cars and following an upwardly revised reading of 1.1% m/m in May (vs. 0.8% reported earlier). This category accounts for all of today's headline growth.

Receipts at gasoline stations and fuel vendors were 0.3% higher on the month but bearing a small weight they had little impact on the headline number

Excluding sales at car dealerships and gas stations, core retail sales were down 0.9% in June, below the consensus estimate of a 0.3% m/m increase. The only two categories that reported gains were miscellaneous store retailers (+1.1% m/m) and sales at furniture and home furnishings stores (+ 0.1% m/m).

The rest of the categories were in the red, with the deepest declines reported by electronics and appliance stores (-3.4% m/m) and building materials and garden equipment dealers (-1.4% m/m), general merchandise stores (-1.4% m/m), and food and beverage stores (-0.9% m/m)

E-commerce sales, which are not included in the headline tally, grew 1.1% m/m in June after an upwardly revise growth of 2.3% in May. We expect that July's reading will be supported by generous incentives of Canada's Amazon Prime days.

Statistics Canada's advanced estimate points to a solid reading of 0.4% in July.

Key Implications

Following a soft reading in May, today's marginal gains gets the second quarter's to -0.1% annualized – a notable step down from a 2.6% pace in Q1. This puts personal consumption expenditures on track for 1% annualized growth in Q2. Looking ahead, spending might still regain its footing with the help of government's grocery rebates. These were aimed at supporting lower-income households that typically have a higher propensity to consume. Like Stats Canada's advance estimate, our internal data points to a rebound in monthly spending in July.

However, by demonstrating more resilience they'll pay the price of higher cost of future borrowing (and spending). The cumulative effect of 475 basis points on interest rate hikes is only starting to have real impact on households' budgets. As more mortgages roll over at higher rates, homeowners will divert more of their income towards debt servicing. This means that retail sales could be the next in line to roll over.

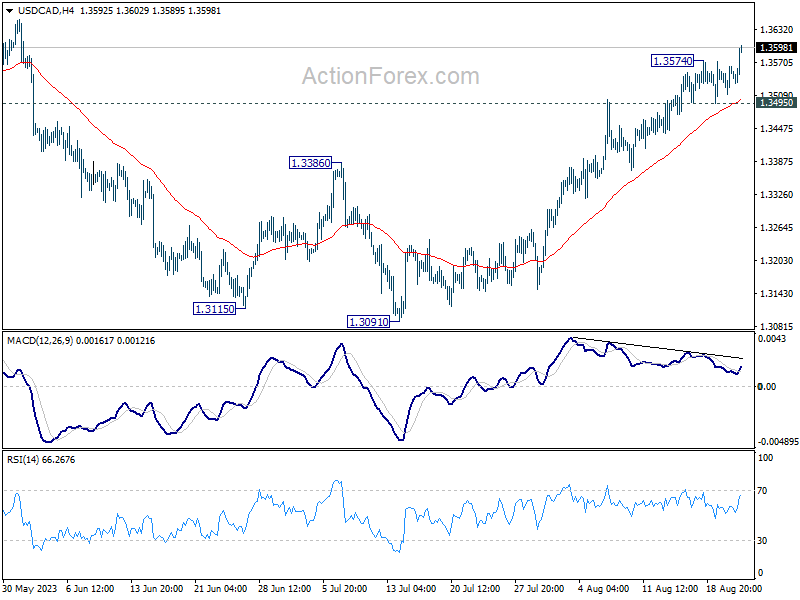

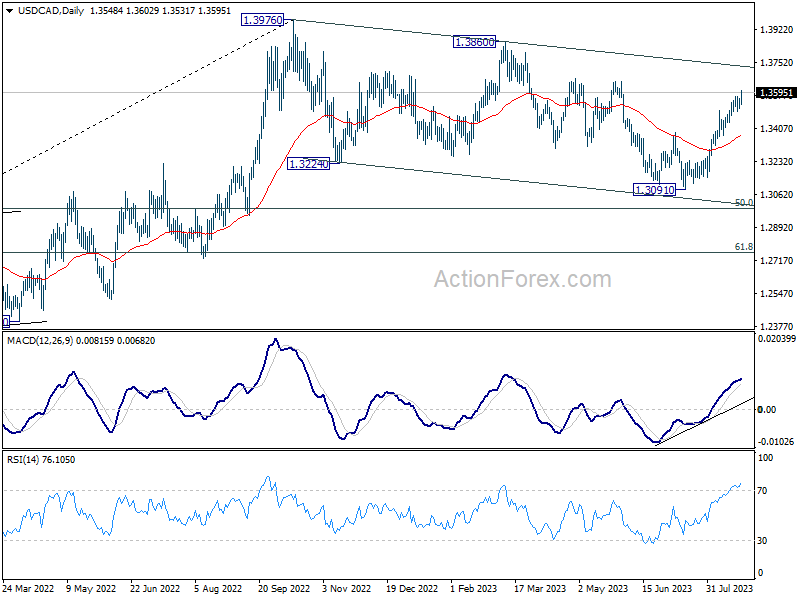

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3521; (P) 1.3543; (R1) 1.3573; More....

USD/CAD's rally resumed after brief consolidations and intraday bias is back on the upside for 1.3653 resistance first. Decisive break there will confirm that correction from 1.3976 has completed, a target a test on this high. On the downside, break of 1.3495 support is needed to indicate short term topping. Otherwise, outlook will remain cautiously bullish in case of retreat.

In the bigger picture, price actions from 1.3976 are viewed as a corrective fall only. Upon completion, rise from 1.2005 (2021 low) would resume through 1.3976. Next target is 61.8% projection of 1.2005 to 1.3976 from 1.3091 at 1.4309. In case of another fall, downside should be contained by 61.8% retracement of 1.2005 to 1.3976 at 1.2758.

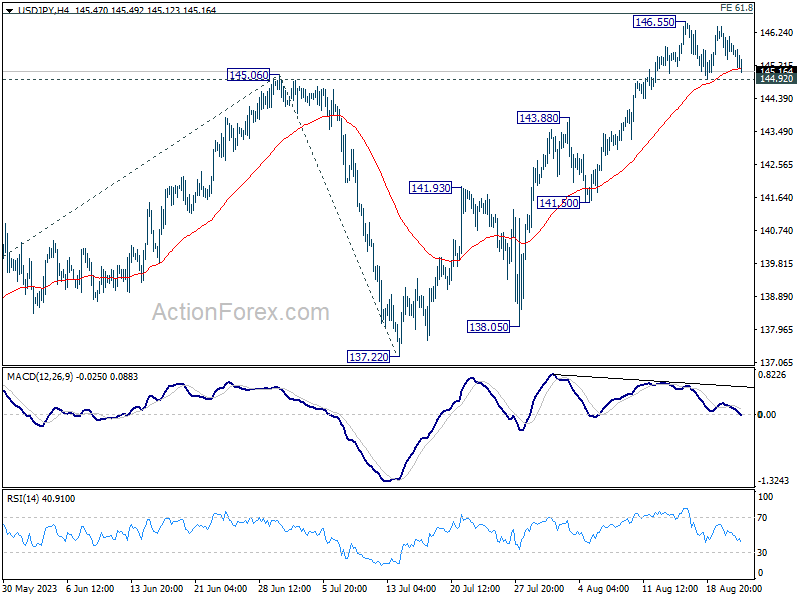

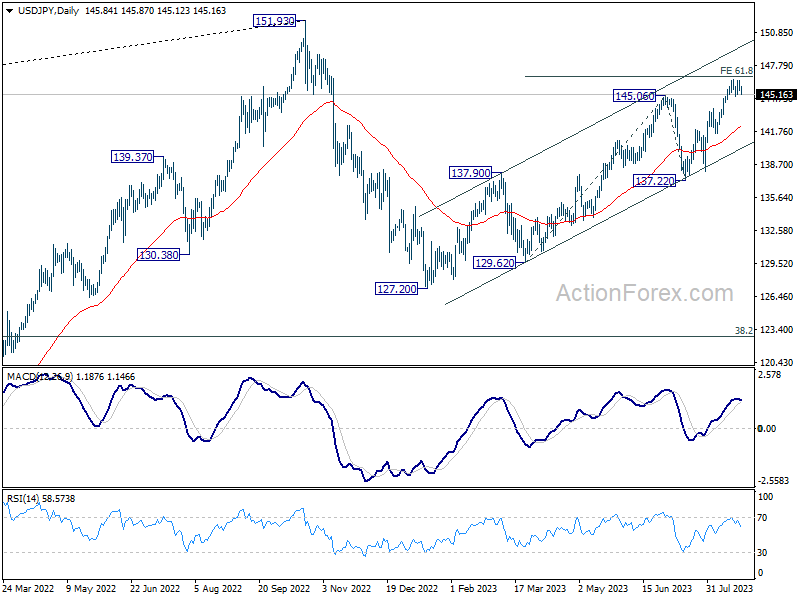

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.46; (P) 145.93; (R1) 146.36; More...

Intraday bias in USD/JPY remains neutral as it's still bounded in sideway trading. On the upside, sustained break of 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76 will pave the way to retest 151.93 high. However, considering bearish divergence condition in 4H MACD, firm break of 44.92 support will be a sign of reversal, and turn bias back to the downside for 55 D EMA (now at 142.09).

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

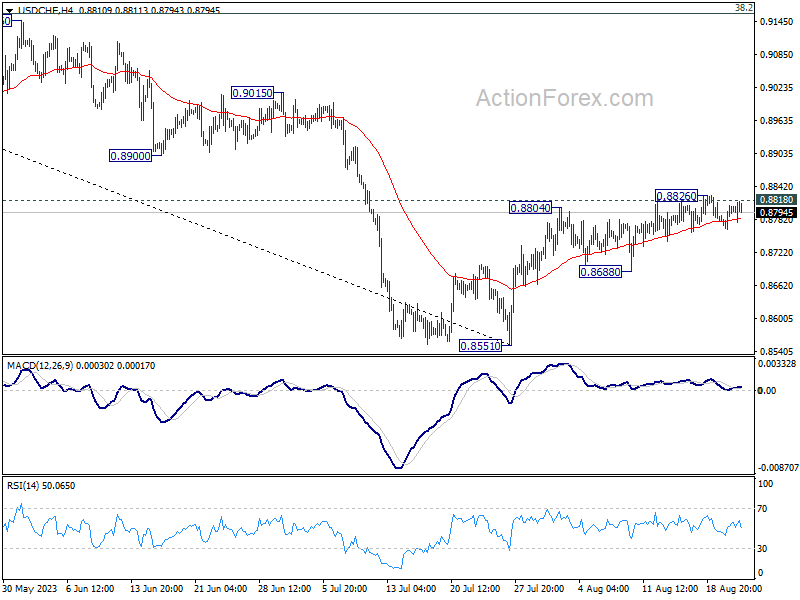

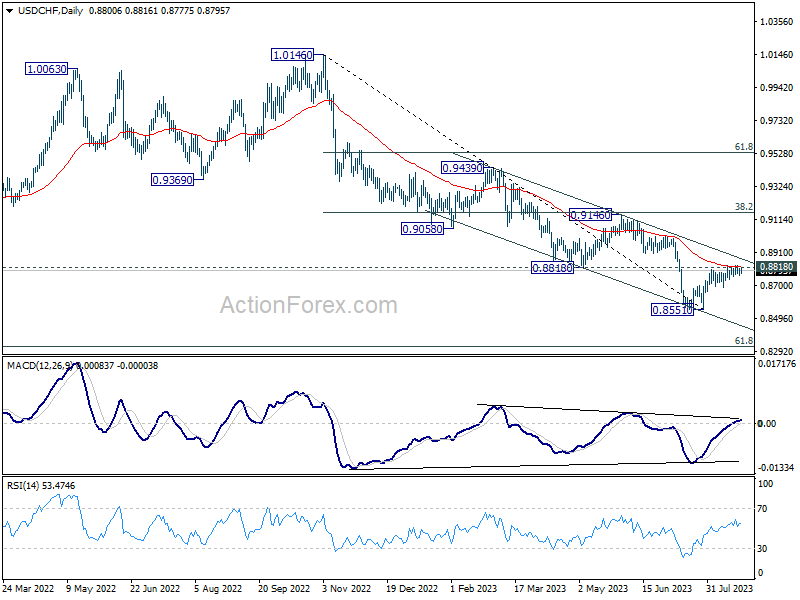

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8777; (P) 0.8794; (R1) 0.8821; More....

No change in USD/CHF's outlook as range trading continues. Intraday bias remains neutral for the moment. On the upside, decisive break of 0.8818 support turned resistance will carry larger bullish implication, and target 0.9146 cluster resistance next. However, break of 0.8688 support will indicate rejection by 0.8818, and turn bias back to the downside for retesting 0.8551 low.

In the bigger picture, a medium term bottom could be in place at 0.8551 already, on bullish convergence condition in D MACD. Sustained trading above 0.8818 support turned resistance will bring further rise to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160), even as a correction. Nevertheless, break of 0.8851 will resume the down trend from 1.0146 instead.

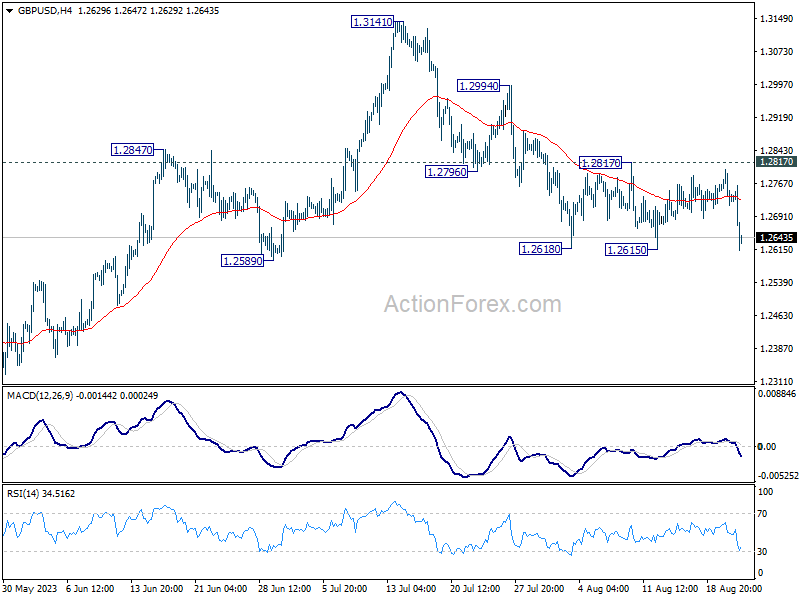

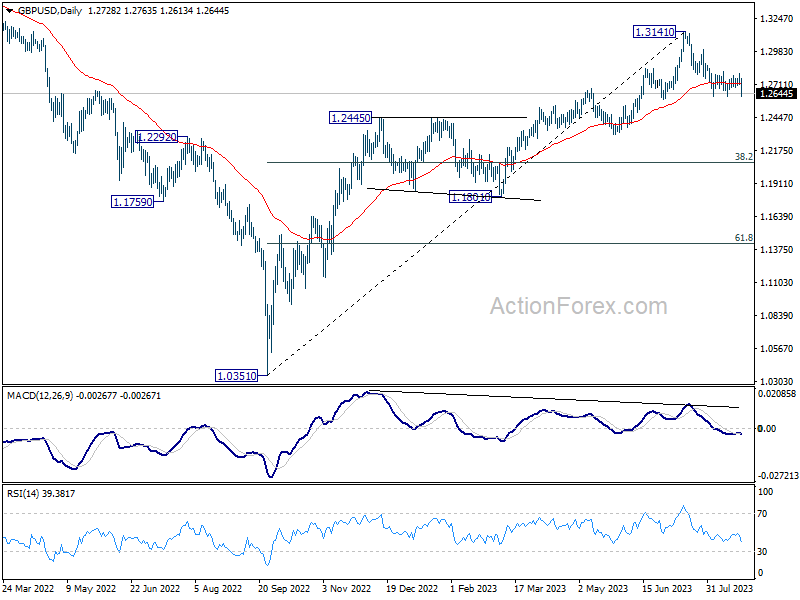

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2701; (P) 1.2750; (R1) 1.2782; More...

Immediate focus is now on 1.2615 support in GBP/USD with today's steep fall. Decisive break there, and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, break of 1.2817 minor resistance will indicate that the pull back from 1.3141 has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2723) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

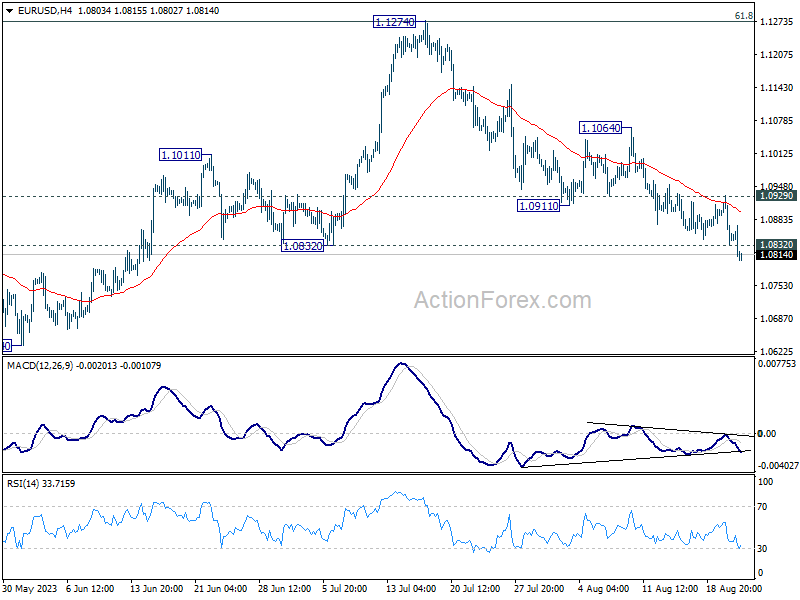

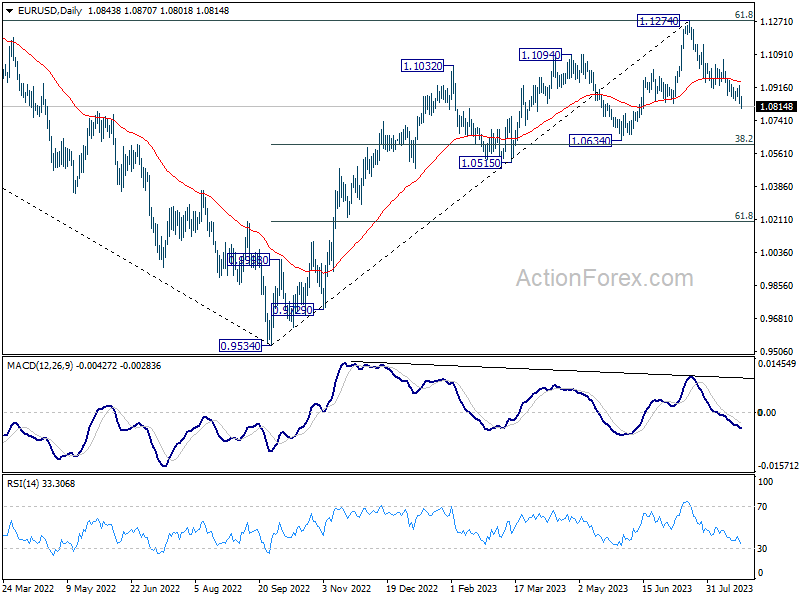

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0809; (P) 1.0870; (R1) 1.0907; More...

EUR/USD's fall from 1.1274 resumes today by breaking 1.0832 support. Intraday bias is back on the downside for 1.0609/34 cluster support next. For now, break of 1.0929 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay mildly bearish in case of recovery.

In the bigger picture, a medium term top should be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Fall from there is seen as a correction to the uptrend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.

PMI Woes Shoot Euro and Sterling Down; Yen and Dollar Seize the Opportunity

Sterling and Euro faced a sharp drop today after alarming PMI readings unveiled an unanticipated rapid decline in the service sectors of both the UK and Eurozone. The days of service-driven economic growth seem to be in the rearview mirror, with signs indicating probable contractions in the third quarter for both regions. Canadian Dollar also felt the weight, taking a hit after core retail sales showed a larger-than-expected contraction, making it the day's third weakest currency.

In a turn of events, Yen emerged as the day's star performer, capitalizing on the notable drops in German and UK benchmark yields. Dollar, riding on the coat-tails of Yen's performance, positioned itself as the second strongest, followed by Swiss Franc. This shift suggests a growing trend towards risk-averse sentiment in the market. Meanwhile, both Aussie and Kiwi present a mixed bag, but display vulnerability against their Dollar and Yen counterparts.

Technically, WTI crude oil's break of 79.06 support today suggests that fall from 84.91 has resumed. Deeper decline is now expected as long as 82.15 resistance holds, to 100% projection of 84.91 to 79.06 from 82.15 at 76.30. Decisive break there will bolster that case that whole rebound from 63.67 has finished too, and target74.74 resistance turned support next. Any downside acceleration in WTI might further strain the already-pressured Canadian Dollar.

In Europe, at the time of writing, FTSE is up 0.67%. DAX is down -0.09%. CAC is down -0.06%. Germany 10-year yield is down -0.0748 at 2.570. Earlier in Asia, Nikkei rose 0.48%. Hong Kong HSI rose 0.31%. China Shanghai SSE dropped -1.34%. Singapore Strait Times rose 0.45%. Japan 10-year JGB yield is up 0.0058 at 0.677.

Canada retail sales up 0.1% mom in Jun

Canada retail sales rose 0.1% mom to CAD 65.9B in June, above expectation of 0.0% mom. Excluding gasoline stations and fuel, motor vehicle and parts dealers, sales were down -0.9% mom. In volume terms, retail sales dropped -0.2% mom.

For Q2 as a whole, sales were unchanged in value terms, and down -0.8% qoq in volume terms.

Advance estimate suggests that sales rose 0.4% mom in July.

UK PMI composite fell to 31-mth low, inflation fight carries a heavy cost

UK PMI Manufacturing fell from 45.3 to 41.5 in August, a 39-month low, and missed expectation of 45.1. PMI Services fell from 51.5 to 48.7, a 7-month low, below expectation of 50.8. PMI Composite fell from 50.8 to 47.9, a 31-month low, and first contraction since January.

Chris Williamson, S&P Global Market Intelligence's Chief Business Economist, commented on the data's implications: "The early PMI survey for August suggests that inflation should moderate further in the months ahead, but also indicates that the fight against inflation is carrying a heavy cost in terms of heightened recession risks.

The numbers tell a story of a stalling economy. The service sector's earlier signs of rejuvenation are waning, and the manufacturing sector's decline is becoming more pronounced. Williamson added that the data suggests a -0.2% contraction in GDP for Q3."

He also alluded to the broader monetary implications, noting, "While a further hike in interest rates in September looks to be on the cards, the August PMI data will add to speculation that rates could soon peak."

Eurozone PMI composite fell to 33-mth low, services downturn mirroring manufacturing

Eurozone PMI Manufacturing rose from 42.7 to 43.7 in August, above expectation of 42.8. However, the services sector took a hit, with its PMI descending to a 30-month low of 48.3 – the first contraction witnessed since December, and missed expectation of 50.5. Consequently, the Composite PMI declined to 47.0, its lowest in 33 months, and, excluding pandemic months, since April 2013.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, weighed in that services downturn is now mirroring the lackluster performance of manufacturing. He anticipates a -0.2% contraction in the Eurozone's Q3 based on current indicators.

August's data echoes ECB President Christine Lagarde's warning about rising wages and declining productivity potentially boosting inflation. "as a result, the ECB may be more reluctant to pause the hiking cycle in September," de la Rubia commented.

Despite the broader decline, there's a semblance of hope for manufacturing. The sector's PMI showed minor improvement, hinting at a potential gradual recovery by early next year.

A notable contributor to the downturn was Germany's swift service sector contraction which fuels the discussion of "Germany being the sick man of Europe."

Germany PMI Manufacturing ticked up from 38.8 to 39.1 in August. PMI Manufacturing Output fell from 41.0 to 39.7, a 39-month low. PMI Services tumbled sharply from 52.3 to 47.3, a 9-month low. PMI Composite dropped from 48.5 to 44.7, a 39-month low.

France's Manufacturing PMI rose to 46.4 in August, up from 45.1. However, Services sector presented concerns, declining to a 30-month low at 46.7, with the Composite PMI holding steady at 46.6.

Japan PMI manufacturing ticked up to 49.7, services rose to 54.3

In August, Japan's Service PMI climbed from 53.8 to 54.3, while the Manufacturing PMI saw a slight increase from 49.6 to 49.7, just above anticipated figures. The Composite PMI also edged up from 52.2 to 52.6.

Andrew Harker, from S&P Global Market Intelligence, pointed out the robust performance of the service sector, driven by consistent new order growth. In contrast, manufacturing only marginally rebounded but remained below the growth threshold.

Despite the overall rise in new orders, manufacturing employment remained flat, ending its 28-month growth streak. Additionally, heightened oil prices impacted both sectors, causing the steepest rise in input costs in four months. Notably, business confidence dwindled in both domains due to longer-term economic uncertainties.

Australian PMI hits 19-month low, but concerns on inflation and strong employment rise

Australia's August PMI data showed a concerning decline across sectors. The Manufacturing PMI slightly decreased from 49.6 to 49.4, while Services PMI dropped to a 19-month low of 46.7. Composite PMI, reflecting both sectors, also declined to a 19-month low of 47.1.

Warren Hogan, Chief Economic Advisor at Judo Bank, drew attention to the employment sector's resilience. He noted, "Despite weakening PMI figures, the employment index remains positive, indicating robust labour demand across both manufacturing and services."

With businesses maintaining optimism, they might resist workforce reductions even amidst economic slowdowns. "As aggregate demand is supported by ongoing employment growth... it might mean a further substantial lift in interest rates could be required at some stage in the next 6-12 months," he added.

Inflation remains a key concern. After 2022 disinflation trend, 2023 has shown a halt in the falling price indexes. The current data suggests an inflation rate of about 4%, overshooting the RBA's 2-3% target range.

Hogan also noted wage growth concerns. Even with modest official growth figures, he cautioned that wage pressures might exceed RBA's forecasted 4% annual growth for 2023. "This may mean firm tightening bias to the RBA's policy deliberations for the rest of the year."

NZ retail sales volume down -1.0% qoq in Q2, value down -0.2% qoq

New Zealand's retail sales volume for Q2 plummeted by -1.0% qoq, settling at NZD 25B. This decline starkly contrasts with market forecasts which had anticipated a milder contraction of just -0.2% qoq. A broad-based slump was evident, as 11 out of 15 industries reported reduced seasonally adjusted sales volumes.

Highlighting the sectors that bore the brunt of this downturn, food and beverage services saw a sharp decline of -4.4%. Hardware, building, and garden supplies trailed closely, recording a -4.8% drop. These sectors emerged as the primary drags on the overall sales volume for the quarter.

While sales volume took a hit, retail sales value also showed signs of weakness, contracting -0.2% qoq to land at NZD 30B. Once again showcasing the breadth of the downturn, seven out of 15 industries registered a fall.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0809; (P) 1.0870; (R1) 1.0907; More...

EUR/USD's fall from 1.1274 resumes today by breaking 1.0832 support. Intraday bias is back on the downside for 1.0609/34 cluster support next. For now, break of 1.0929 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay mildly bearish in case of recovery.

In the bigger picture, a medium term top should be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Fall from there is seen as a correction to the uptrend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Q/Q Q2 | -1.00% | -0.20% | -1.40% | -1.60% |

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q2 | -1.80% | -0.10% | -1.10% | -1.60% |

| 23:00 | AUD | Manufacturing PMI Aug P | 49.4 | 49.6 | ||

| 23:00 | AUD | Services PMI Aug P | 46.7 | 47.9 | ||

| 00:30 | JPY | Manufacturing PMI Aug P | 49.7 | 49.6 | 49.6 | |

| 07:15 | EUR | France Manufacturing PMI Aug P | 46.4 | 45.2 | 45.1 | |

| 07:15 | EUR | France Services PMI Aug P | 46.7 | 47.3 | 47.1 | |

| 07:30 | EUR | Germany Manufacturing PMI Aug P | 39.1 | 38.7 | 38.8 | |

| 07:30 | EUR | Germany Services PMI Aug P | 47.3 | 51.5 | 52.3 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Aug P | 43.7 | 42.8 | 42.7 | |

| 08:00 | EUR | Eurozone Services PMI Aug P | 48.3 | 50.5 | 50.9 | |

| 08:30 | GBP | Manufacturing PMI Aug P | 42.5 | 45.1 | 45.3 | |

| 08:30 | GBP | Services PMI Aug P | 48.7 | 50.8 | 51.5 | |

| 12:30 | CAD | Retail Sales M/M Jun | 0.10% | 0.00% | 0.20% | 0.10% |

| 12:30 | CAD | Retail Sales ex Autos M/M Jun | -0.80% | 0.30% | 0.00% | -0.30% |

| 13:45 | USD | Manufacturing PMI Aug P | 48.9 | 49 | ||

| 13:45 | USD | Services PMI Aug P | 52.4 | 52.3 | ||

| 14:00 | USD | New Home Sales Jul | 708K | 697K | ||

| 14:00 | EUR | Eurozone Consumer Confidence Aug P | -14 | -15 | ||

| 14:30 | USD | Crude Oil Inventories | -2.9M | -6.0M |

Canada retail sales up 0.1% mom in Jun

Canada retail sales rose 0.1% mom to CAD 65.9B in June, above expectation of 0.0% mom. Excluding gasoline stations and fuel, motor vehicle and parts dealers, sales were down -0.9% mom. In volume terms, retail sales dropped -0.2% mom.

For Q2 as a whole, sales were unchanged in value terms, and down -0.8% qoq in volume terms.

Advance estimate suggests that sales rose 0.4% mom in July.