Sample Category Title

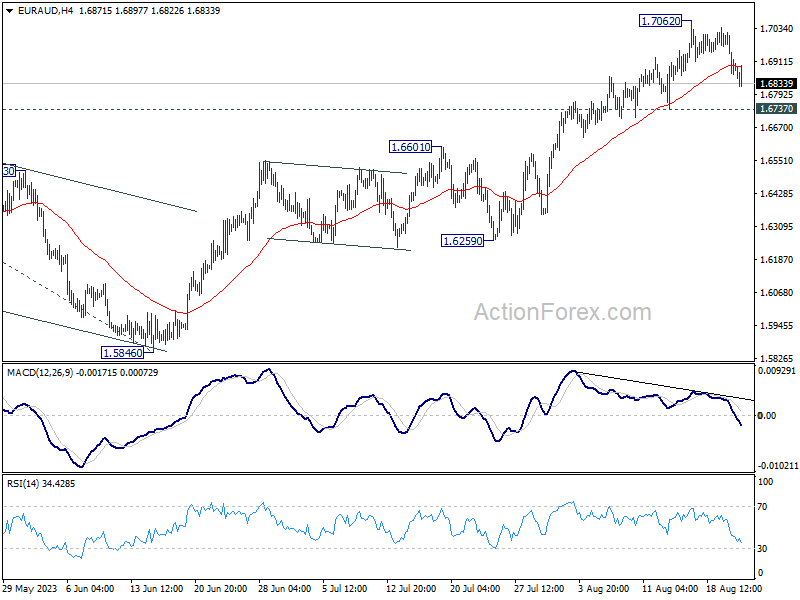

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6829; (P) 1.6925; (R1) 1.6983; More...

While EUR/AUD's retreat from 1.7062 extends lower, downside is contained above 1.6737 support so far. Intraday bias remains neutral and outlook stays bullish for now. On the upside, firm break 1.7062 will resume larger up trend from 1.4281 to 1.7377 projection level.

In the bigger picture, the rise from 1.4281 (2022 low) is in progress. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. For now, outlook will stay bullish as long as 1.5846 support holds, even in case of another pull back.

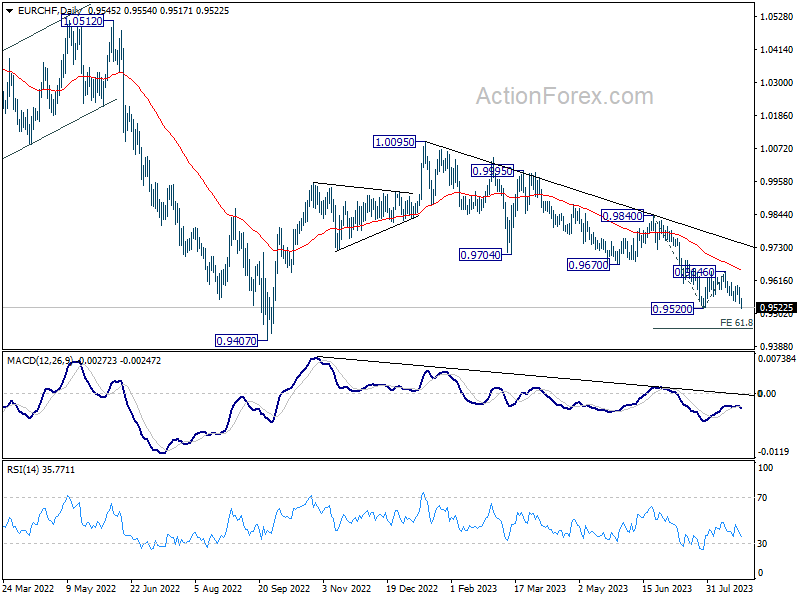

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9528; (P) 0.9560; (R1) 0.9582; More...

EUR/CHF's break of 0.9520 support indicates resumption of larger fall from 1.0095. Intraday bias is back on the downside. Next target is 61.8% projection of 0.9840 to 0.9520 from 0.9646 at 0.9448. On the upside, break of 0.9599 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9849). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9670 support turned resistance holds, in case of strong rebound.

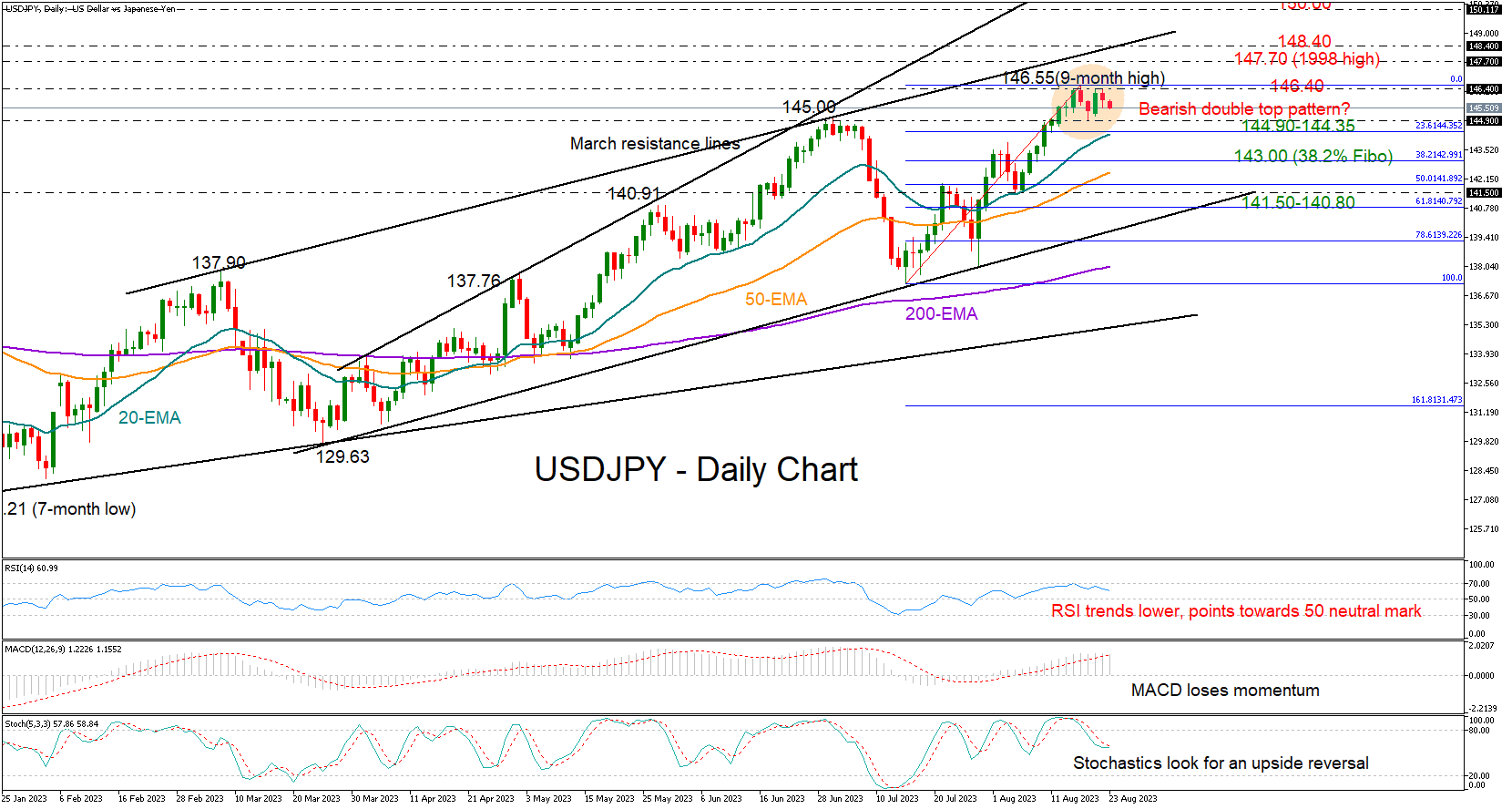

Will USDJPY Stage a New Bearish Cycle?

USDJPY topped twice around the 146.40 barrier from last November, but a negative trend reversal cannot be warranted yet.

The RSI has changed direction to the downside after peaking near its 70 overbought mark, while the MACD has slowed down in the positive area. Still, the latter has not crossed below its red signal line, while the Stochastic oscillator is poised for an upside reversal soon after retreating below its 80 overbought level, witnessing some persisting buying interest.

Sellers might wait for the price to drop below 144.90 before they initiate a new bearish cycle. Some may even wait until it falls below the 20-day exponential moving average (EMA) at 144.30, which helped the market earlier this month. The 23.6% Fibonacci retracement of the latest upleg is at the same location. Therefore, a clear close lower is expected to trigger a fast decline towards the 38.2% Fibonacci of 143.00. If the pressure on the price continues below the 50-day EMA, it may fall somewhere between 141.50 and 140.80.

In the bullish scenario, where the pair accelerates above 146.40, it may encounter resistance within the 147.70-148.30 region, formed by the 1998 high and the tentative ascending line from March. The 148.80 region has been quite restrictive during October-November 2022. Hence, a move above that wall might be a prerequisite for an advance towards the 150.00 psychological number.

In short, USDJPY bulls are facing a double top situation after six-weeks of gains and ahead of the Jackson Hole symposium. While the bearish pattern is flagging some caution, sellers may stay on the sidelines until they see a decline below the 144.90-144.30 zone.

EUR/USD Testing 1.0830 Support for Wave (A)

EURUSD came down as expected to a new low after wave 4 corrective rise so price is now seen in wave back, back at 1.0830 support. Therefore, the wedge shape may suggest limited weakness and slow price action in weeks ahead, as wave (A) can be coming to an end, but more weakness will show up after wave (B) rally that can show up in sessions ahead. As such, we think that higher degree correction is still underway and it can be much deeper as EURUSD pair might have completed a five-wave rise at around 1.1280 back in July. However, we will once again turn bullish on the euro once the corrective A-B-C drop will come to an end, but at the moment that's clearly not the case yet.

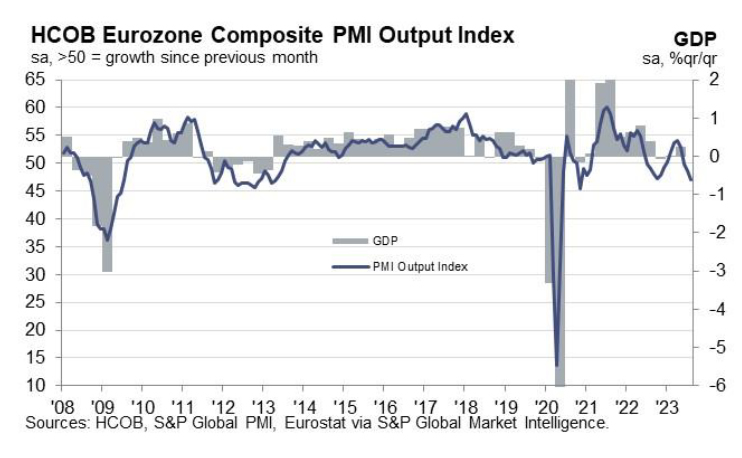

Eurozone PMI composite fell to 33-mth low, services downturn mirroring manufacturing

Eurozone PMI Manufacturing rose from 42.7 to 43.7 in August, above expectation of 42.8. However, the services sector took a hit, with its PMI descending to a 30-month low of 48.3 – the first contraction witnessed since December. Consequently, the Composite PMI declined to 47.0, its lowest in 33 months, and, excluding pandemic months, since April 2013.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, weighed in that services downturn is now mirroring the lackluster performance of manufacturing. He anticipates a -0.2% contraction in the Eurozone's Q3 based on current indicators.

August's data echoes ECB President Christine Lagarde's warning about rising wages and declining productivity potentially boosting inflation. "as a result, the ECB may be more reluctant to pause the hiking cycle in September," de la Rubia commented.

Despite the broader decline, there's a semblance of hope for manufacturing. The sector's PMI showed minor improvement, hinting at a potential gradual recovery by early next year.

A notable contributor to the downturn was Germany's swift service sector contraction which fuels the discussion of "Germany being the sick man of Europe."

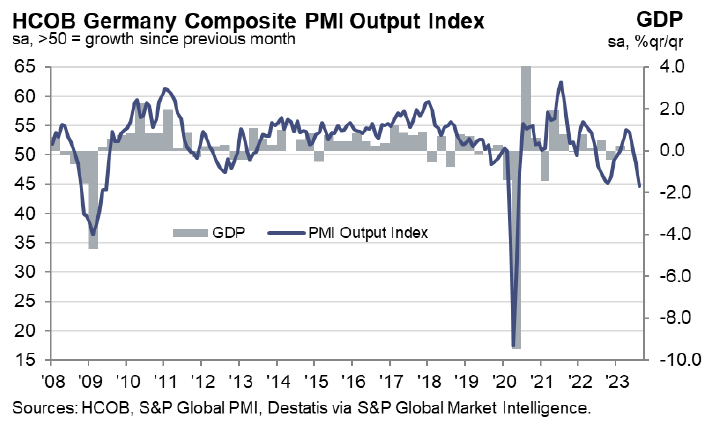

Germany PMI services fell to 9-month low, hope of rescue evaporated

Germany PMI Manufacturing ticked up from 38.8 to 39.1 in August. PMI Manufacturing Output fell from 41.0 to 39.7, a 39-month low. PMI Services tumbled sharply from 52.3 to 47.3, a 9-month low. PMI Composite dropped from 48.5 to 44.7, a 39-month low.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said:

"Any hope that the service sector might rescue the German economy has evaporated. Instead, the service sector is about to join the recession in manufacturing, which looks to have started in the second quarter. Our GDP nowcast model, which incorporates the PMI flash estimate, now indicates a deeper fall of the whole economy than it did before, at almost -1%.

"Stagflation is an ugly thing. However, it's exactly what is happening to the services economy, as activity has started to shrink while prices have shot up again, even picking up pace. When inflation cannot be tamed in the eurozone's biggest economy, this is bad news for the ECB.

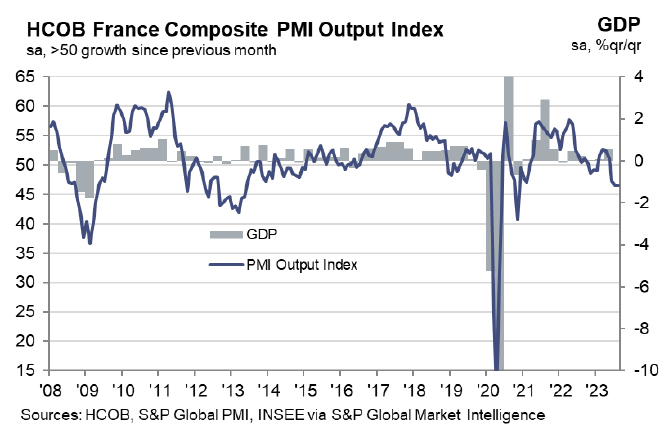

France PMI services down to 30-mth low, economy probably contracts in Q3

France's Manufacturing PMI rose to 46.4 in August, up from 45.1. However, Services sector presented concerns, declining to a 30-month low at 46.7, with the Composite PMI holding steady at 46.6.

Norman Liebke of Hamburg Commercial Bank noted, "The French economy is facing challenges, potentially leading to a contraction in the third quarter," he stated.

A noticeable decline in global demand impacts France, with foreign new orders below the desired 50-point expansion mark. Companies have been tapping into backlogs due to the decline in new orders. Liebke also highlighted a subdued growth in employment, the slowest since January 2021.

Notably, a stark contrast is evident in input prices. The services sector saw a surge, primarily due to wage growth, whereas manufacturing experienced a drop, influenced by reduced energy and raw material costs.

A similar trend is showing in output prices too, and "suggests the core rate, where service prices play a crucial role, could prove to be stubborn."

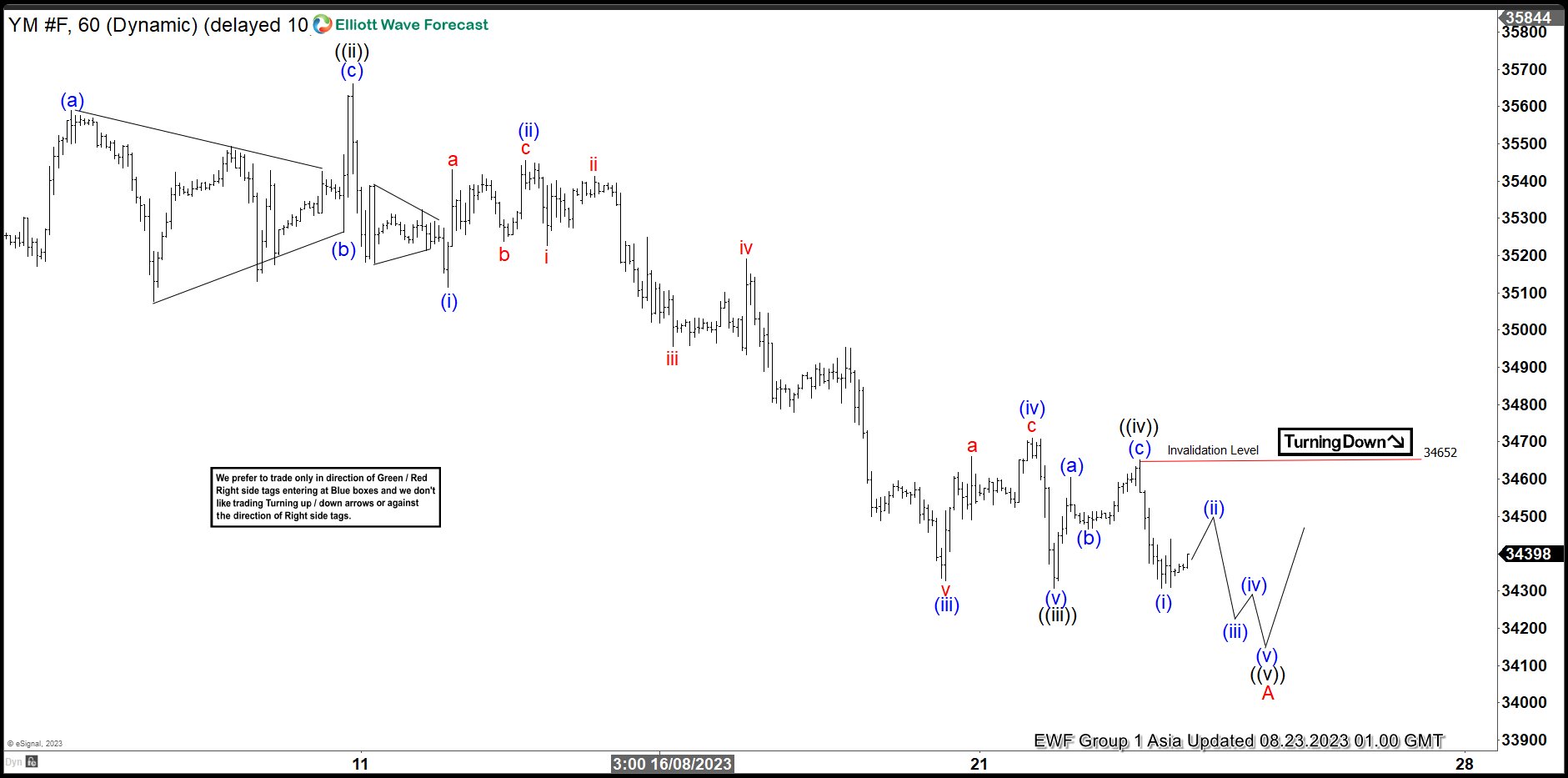

Dow Futures (YM_F) Looking for Corrective Rally Soon

Short Term Elliott Wave view in Dow Futures (YM_F) suggests that cycle from 7.27.2023 high is mature and about to complete soon as 5 waves impulse. Down from 7.27.2023 high, wave ((i)) ended at 35076 and rally in wave ((ii)) ended at 35660. Index extended lower in wave ((iii)) as another impulse in lesser degree. Down from wave ((ii)), wave (i) ended at 35115 and rally in wave (ii) ended at 35456.

Index extended lower in wave (iii) towards 34328 and rally in wave (iv) ended at 34709. Final leg wave (v) ended at 34308 which completed wave ((iii)). Rally in wave ((iv)) ended at 34645 as a zigzag structure. Up from wave ((iii)), wave (a) ended at 34605, wave (b) ended at 34465, and wave (c) higher ended at 34645 which completed wave ((iv)). Down from wave ((iv)), wave (i) ended at 34307. Short term rally should fail in 3 or 7 swing against 34645 for further downside within wave ((v)). Once the 5 waves decline ends, it should complete wave A in larger degree. Then the Index should rally in wave B to correct decline from 7.27.2023 high in 3 or 7 swing before the decline resumes.

Dow Futures (YM_F) 60 Minutes Elliott Wave Chart

YM_F Elliott Wave Video

https://www.youtube.com/watch?v=Vuosu8BQjj4

Investors Turn More Nervous Going into Friday’s Jackson Hole

Markets

The curve move in the US differed somewhat from previous sessions yesterday as it turned more inverse. Technical resistance levels do their part at the (very) long end. The US 10-yr and 30-yr yields shed 1.4 bps and 4.7 bps respectively, failing to take out 4.34% and 4.45% for now. The front end underperformed with yields rising by up to 4.5 bps for the 2-yr which closed above the psychological 5% mark (5.05%) for only the third time since 2007. Investors turn more nervous going into Friday’s Jackson Hole address by Fed Chair Powell. They gradually come to terms with the idea of higher policy rates for even longer, while simultaneously doubting their (the money market) view that the Fed policy rate already peaked. We stressed on many occasions the diverging view between Fed June Dots (2 additional hikes in 2023; one already implemented) and Minutes of the July policy meeting (most participants still have upward inflation risks as prime reason of concern & recession in H2 2023 no longer base case scenario) and US money markets attaching only a 16% probability to a September 25 bps rate hike. This still means room for more underperformance at the front end of the curve if Powell gives the go-ahead. Persistently high core inflation should be the trigger.

The underperformance of the front end of the US yield curve pushed the trade-weighted dollar for another test of the July high at 103.57, but a break didn’t occur. The greenback closed at 103.56. EUR/USD fell from an open at 1.0896 to 1.0846 after a first real test of the July low at 1.0834. EUR/GBP followed the slide in EUR/USD with a close at 0.8518. The YTD low at 0.8504 is near, but untested. European stock markets still managed a positive close despite waning intraday momentum while US indices closed flat to 0.5% lower. Today’s focus is on global PMI’s. There’s room for improvement especially in Europe following two months of weak figures. This could add some more selling pressure at the front end of the yield curve while temporary helping the euro in its battle of survival above first support lines.

News and views

New Zealand’s total volume of retail sales fell 1.0% in the June 2023 quarter. This fall comes after declines of 1.6% and 1.1% in the March 2023 and December 2022 quarters respectively. 11 of the 15 retail industries had lower sales volumes in the June 2023 quarter compared with the March quarter. The largest contributors to the fall in the June 2023 quarter were food and beverage services, down 4.4%, and hardware, building, and garden supplies, down 4.8%. Without adjusting for seasonal patterns and price effects, the value of total retail sales was $29bn in the June 2023 quarter, up 2.5% ($725mn) compared with the June 2022 quarter. Last week, the RBNZ left its policy rate unchanged at 5.5%, but indicated that the policy rate needs to stay at restrictive levels for the foreseeable future to ensure that CPI inflation will return to the 1-3% target range. Today’s data might ease the RBNZ’s fear that activity doesn’t slow as needed to reach the inflation target. The data had little impact on the kiwi dollar. After a protracted decline over the previous month, NZD/USD today stabilizes near 0.595.

Activity in the Japanese manufacturing sector in August stayed slightly in contraction territory with the Jibun Bank manufacturing PMI printing at 49.7 from 49.6 in July. The services PMI showed growth improving further from 54.3 to 53.8. Andrew Harker of S&P Global Market intelligence said “Growth across the Japanese private sector picked up pace during August, with the service sector again driving the overall expansion amid ongoing improvements in new orders”. With overall new orders continuing to rise, firms upped their staffing levels accordingly. The weakness in manufacturing demand acted to deter hiring there, however, with no change in employment ending a 28-month sequence of factory job creation. On prices Harker said “rising oil prices were a key feature across the latest survey, with firms across both manufacturing and services reporting an impact on input costs. Overall, input prices increased at the fastest pace in four months”. The Japanese 10-y government yield set a new cycle high at 0.68% this morning. The yen gains marginally with USD/JPY trading near 145.6.

Japan Kicks Off PMI Day on a Strong Note

Market movers today

Today we get preliminary August flash PMI's for France, Germany and the total euro area, as well as for the UK and the US. In July, manufacturing PMIs were very weak in the euro area and service PMIs were declining, which is a major argument for those arguing against further rate hikes from the ECB. In the US, data for August so far has been very mixed and today's release should create some clarity on the direction of the US economy after what looks to have been a fairly strong July.

We also get euro area consumer confidence and US new home sales in July. The latter follows existing home sales out yesterday showing a 2.2% monthly decline.

The 60 second overview

Japan recovery: The Japanese economy has continued on a fairly strong note in August with the service sector re-accelerating as service PMI increased to 54.3 from 53.8 in July. This blows some new life into the reflation narrative in Japan after disappointing private spending in Q2. Indices for output prices in both service and manufacturing edged slightly lower but both remain around 54, also indicating sustained inflationary pressures. The manufacturing sector remains somewhat sheltered from the global manufacturing recession as the weak yen supports the exports sector. Manufacturing PMI remains below the 50 threshold but edged slightly higher to 49.7 in August.

US: The 10y UST yield continues to trade above 4.30%, supported by persistently upbeat US macro data, which the Richmond Fed's Barkin described as 'impressive' in his comments yesterday. Notably, the latest uptick does not reflect significantly higher implied probability of the Fed delivering another rate hike, but rather longer-dated real yields rising further, which could imply markets turning increasingly bullish on the US economy not just in the near-term, but also for the coming years. In H1, growth in investments into public infrastructure and private high-tech manufacturing boosted GDP above expectations, fuelled by the fiscal stimulus measures seen in 2021-2022. And while we still remain sceptical of the current soft landing optimism, yesterday we published a paper in which we discuss the potential implications of a prolonged boom in investments and rise in productivity. Read more from Research US - Could investment boom pave the way for a soft landing? 22 August

Equities: Global equities higher yesterday, despite US dragging down in a still very selective and not top-down driven rotation. Consumer cyclicals, utilities and materials outperforming at the same day is not a very common combination and highlights the lack of strong macro drivers. That is up for a change in the coming days with much more heavy weight macro data and monetary policy focus on the agenda. In US yesterday, Dow -0.5%, S&P500 -0.3%, Nasdaq +0.1% and Russell 2000 -0.3%. Asian markets are rather directionless this morning with less China related news and Japanese flash PMIs coming in very close to expectation and very close to last month's reading. Futures at both sides of the Atlantic are a tad higher this morning.

FI: There was again a rebound in European government bond yields as 10Y German government bond yields declined some 5bp yesterday and the EGB curves bull flattened from the long end. Short-dated US Treasury yields rose 4bp, while 30Y yields declined 4bp.

FX: EUR/USD headed lower yesterday, currently around 1.0850, as European yields dropped whereas US counterparts remained more or less unchanged. Mostly quiet trading on the day, but Scandies and especially the SEK strengthened early in the session and managed to keep their gains even though risk sentiment turned somewhat towards the close.

Credit: Performance of credit indices was solid with iTraxx Xover tightening almost 7bp and Main 1.7bp following a streak of seven consecutive days of widening. Primary market activity remained mostly confined to issuance from banks though E.ON priced a dual-tranche EUR transaction (both in green format).