Sample Category Title

Jackson Hole Symposium to Shape Dollar’s Path

The Fed’s annual economic symposium will kick off on Thursday, but the highlight will be Chairman Powell’s flagship speech on Friday. With US yields trading at their highest levels of this cycle, his signals on interest rates could either add fuel to this rally or trigger a correction, driving the dollar accordingly.

Fed summer camp

Once every year, Fed officials are joined by foreign central bankers and academics at their summer retreat in Jackson Hole for a symposium to discuss monetary policy and economic trends. Since this platform has been used in the past to signal major strategy shifts, markets see it as an unofficial FOMC meeting.

As such, the emphasis will be on what Jay Powell says about the path of interest rates. Futures markets currently assign only a 15% probability for another rate increase in September, even though incoming data has been particularly strong in recent weeks.

Economic growth is tracking at a 5.8% annualized pace this quarter according to the Atlanta Fed, consumers continue to spend, and the unemployment rate remains subdued near a five-decade low. Meanwhile, home prices are hitting new record highs in many parts of the country, so the cooldown in rents that the Fed has long awaited might prove elusive.

In other words, the US economy is running hot and with energy prices also moving higher lately, there are credible concerns that inflation might not cool down to its 2% target anytime soon.

What can Powell say?

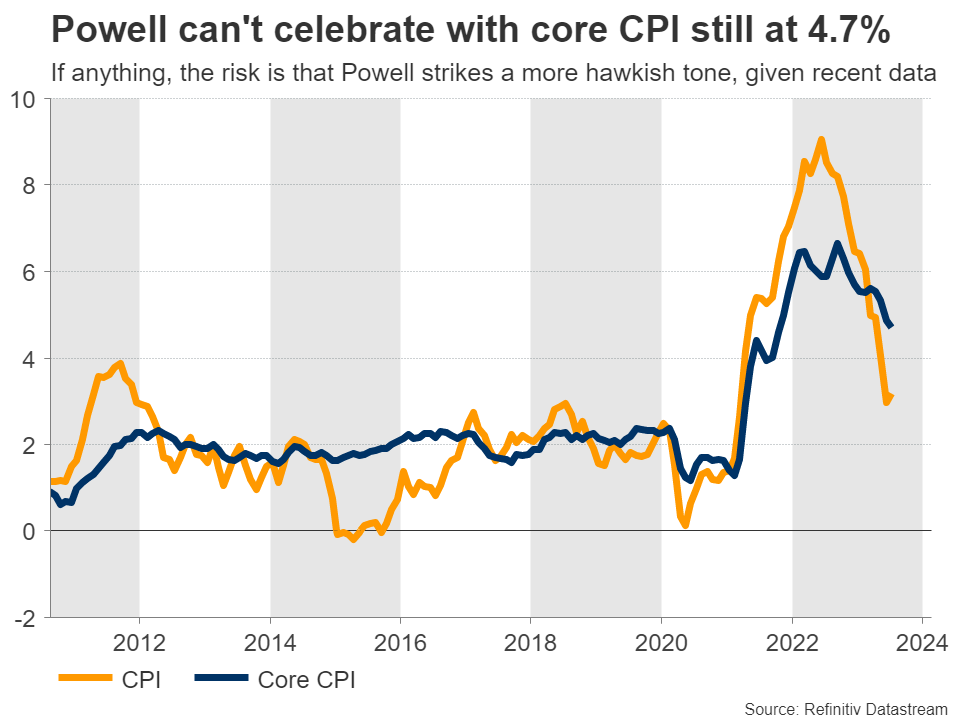

Overall, Powell is likely to keep his options open. While there has been serious progress on the inflation front, core inflation still running at 4.7% and with several signs it might remain elevated, it is probably too early for the Fed chief to take a victory lap and declare ‘mission accomplished’.

He was preaching data dependence at the July FOMC meeting three weeks ago and will likely maintain that approach. However, considering the strength in the data flow lately, the risk is that he strikes a more hawkish tone this time, emphasizing the prospect of a ‘higher for longer’ regime for rates.

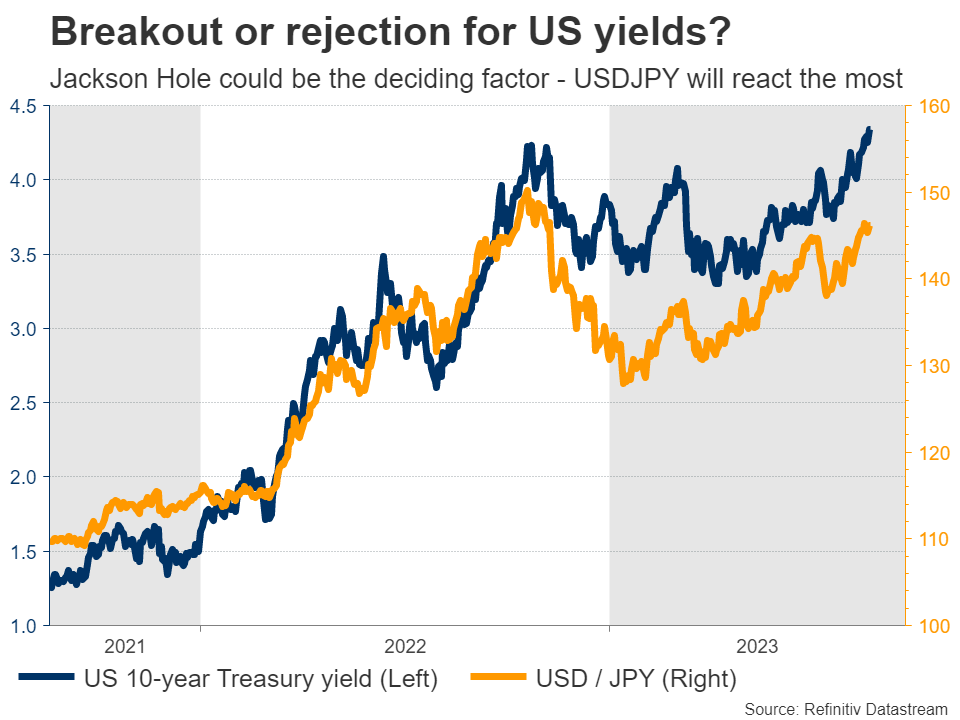

If Powell puts more emphasis on the prospect of keeping interest rates elevated for a longer period or on raising rates again in September, that could amplify the upward pressure on US yields, turbocharging the dollar.

Dollar/yen is extremely sensitive to rate differentials, as the Bank of Japan still has not raised rates, so any spike in US yields might be reflected in this pair the most. A potential break above this year’s high at 146.60 could add momentum to the pair’s upward trend.

That said, Japanese authorities will likely become more vocal about FX intervention if dollar/yen approaches the 150.00 region in a hurry, so any advances might not be linear.

The big picture

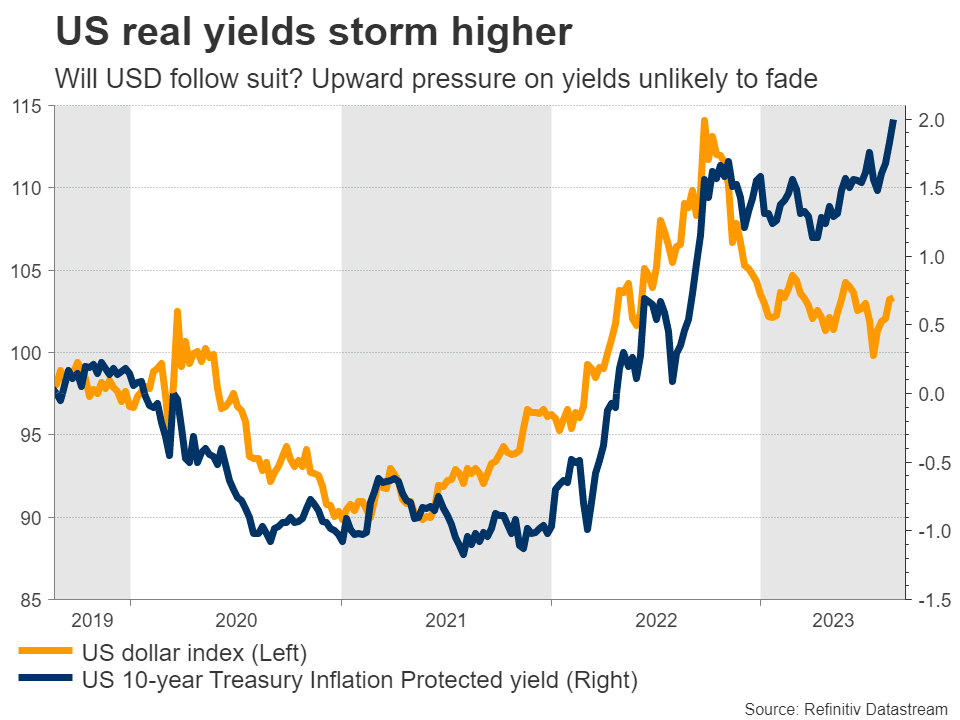

All told, the outlook for the US dollar seems promising. With real US yields hitting their highest levels since 2009 this week, the dollar is becoming an increasingly attractive investment destination.

And this upward pressure on yields is unlikely to fade without a crisis. The Treasury is flooding the markets with new debt issuance, the Fed continues to unwind its own bond portfolio through quantitative tightening, and there are whispers that even China is unloading some of its Treasuries to raise reserves and defend its sinking currency.

On a simpler level, the US economy is superior to its competitors at this stage from a growth perspective. China is battling a severe economic slowdown and business surveys suggest Europe is headed downhill too, perhaps towards a technical recession later this year.

Over time, this economic divergence between the world’s largest economies is likely to be reflected in exchange rates, especially if US yields rise further.

FTSE and Hangseng Should Act As a Floor for the Indices

Indices sold off last week, while some Indices reached extreme Fibonacci extension areas from the highs in 3 or 7 swings, it remains to be seen whether correction in the Indices is over or will extend. Today, we will take a look at Elliott wave sequences in two Stock Markets like FTSE from UK and Hangseng from Hong Kong to determine if the downside in Indices is over or will extend more and will also present the most likely path along with the timing for the Indices to turn higher.

FTSE Incomplete Elliott Wave Sequence

FTSE chart above shows the sequence of swings down from 2.16.2023 and 4.21.2023 highs respectively. FTSE selling since 7.31.2023 peak managed to break below 7.7.2023 peak and a break of this low has created an incomplete bearish sequence in the FTSE Index against 7.31.2023 peak. Even when it has not yet broken below 3.20.2023 low, 5 swings down from 4.21.2023 high means next bounce should fail below 7.31.2023 high for 1 more leg lower toward 7097.26 – 6847.29 area and hence why we think 3.20.2023 low will eventually give up. Ideal path is once cycle from 7.31.2023 high ends, a bounce in 3 or 7 swings to fail for 1 more leg lower.

Hangseng Incomplete Elliott Wave Sequence

The chart above has Hangseng showing 5 swing down from 01.27.2023 peak which is an incompete bearish sequence against 7.31.2023 peak and calls for more downsided as far as 7.31.2023 high remains intact. Price is approaching 0.618 – 0.764 Fibonacci extension area (17488 – 16782) of the decline from 01.27.2023 peak to 5.31.2023 low projected lower from 731.2023 peak. This is the idea area to end 5th swing after which we expect a bounce to correct the decline from 7.31.2023 peak and then another leg lower toward 15691 – 14581 area to complete 7 swings sequence down from 01.27.2023 peak. Ideal path is once cycle from 7.31.2023 high ends, a bounce in 3 or 7 swings to fail for 1 more leg lower.

By looking at incomplete sequences in FTSE and Hangseng, it is easy to conclude that pull back in rest of the Indices should not be over yet, they should see a bounce to correct the decline from their respective July peaks followed by another leg lower. Extreme areas in FTSE ( 7097.26 – 6847.29 ) and Hangseng (15691 – 14581) should act as a floor and provide the timing for the Indices to turn higher again in a larger 3 waves at minimum.

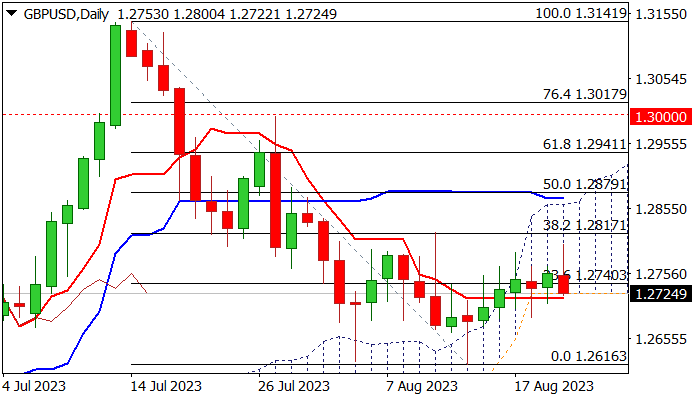

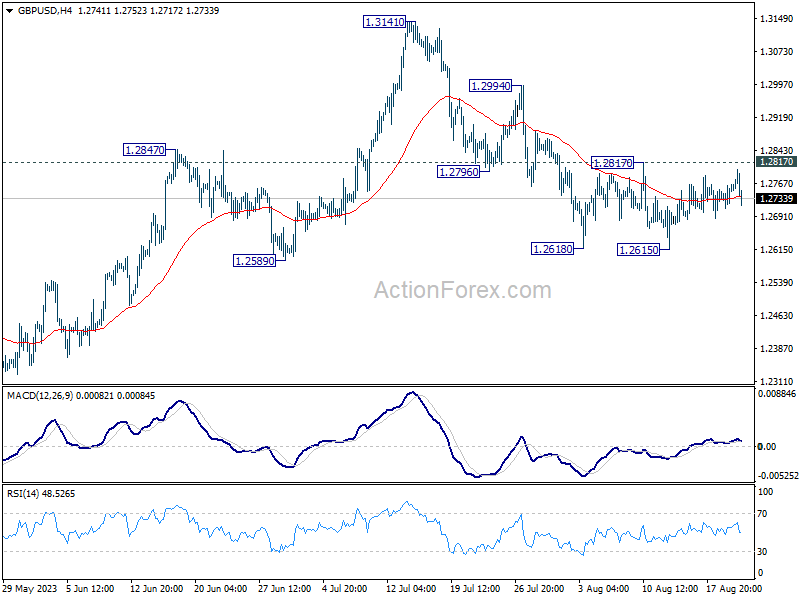

GBP/USD: Risk of Recovery Stall on Close Below Cloud Base

Cable continues to move within thickening daily cloud and hit new marginally higher two-week high on Tuesday, but quick pullback warns that bulls might be losing traction.

Near-term action is expected to keep slight bullish bias while holding above cloud base (1.2725) reinforced by daily Tenkan-sen, however, today’s action is so far shaped in red candle with long upper shadow which signals strong offers and weighs on recovery.

The downside is expected to remain vulnerable while the price stays under pivotal Fibo barrier at 1.2817 (38.2% of 1.3141/1.2616), violation of which would generate fresh bullish signal for extension towards key resistances at 1.2860/71 (daily cloud top / Kijun-sen).

Conversely, close below cloud top would generate initial signal of recovery stall and shift near-term focus lower.

Res: 1.2800; 1.2817; 1.2879; 1.2941.

Sup: 1.2717; 1.2708; 1.2686; 1.2659.

Sunset Market Commentary

Markets:

In a repeat of previous sessions, the core bond sell-off slowed and even went slightly into reverse during a rather dull European trading session. The peace lasted again until the start of US trading when Treasuries started slipping away without strong trigger. Intraday US yield changes are currently close to zero compared to yesterday’s record closing highs, but they are pushing for a break above 5% (2-yr), 4.5%(5-yr), 4.34% (10-yr) and 4.42% (30-yr). The US 10-yr real yield remains stuck around 2%. Simultaneously the dollar started rallying while stock markets came off their intraday rebound highs. EUR/USD fell back from around 1.0930 to currently 1.0860. A disappointing second tier Philly Fed non-manufacturing activity index (-13.1 from 1.4) went unnoticed. Later today, we still get July existing home sales and the more important August Richmond Fed manufacturing index. Richmond Fed Barkin (non-voter) spoke at an event hosted by the Danville Pittsylvania County Chamber of Commerce. His speech was a repeat of the one delivered earlier this month where he suggested that the greater-than-expected easing in inflation in June may be an indication that the US economy can have a soft landing, returning to price stability without a damaging recession. During the Q&A he argued against the idea of changing the inflation target as it risks triggering (another) bond sell-off in a sign of a loss of credibility. Later today, Chicago Fed Goolsbee and Washington Fed Bowman participate in a debate on youth unemployment so they normally won’t touch on monetary policy. Most Fed governors stay low in the run-up to the Jackson Hole meeting at the end of the week. Over the past years, Fed Chair Powell delivered some important messages at this symposium, ranging from changes to the Fed’s inflation target (allowing over- and undershoots) in 2020, over the message that the Fed wasn’t in a hurry to raise rates as economies reopened after the pandemic in 2021 to last year’s eight-minute market scare that the Fed would keep raising interest rates. This year’s focus will much more be on how monetary policy will play out after reaching a peak level and what factors might kickstart rate cuts and on what time horizon. In a lengthy WSJ article, the author and close Fed-source often dropped 3% for core inflation as some kind of arbitrary threshold. Currently, the Fed’s preferred PCE core deflator is still running at 4.1% Y/Y suggesting no inclination at all to let the inflation guard down. On the contrary.

News & Views:

Belgian consumer confidence dipped slightly in August. At -7, the consumer confidence indicator remains close to its long-term average. The very marginal drop in the indicator stems from less favourable expectations regarding the economic situation in general (-17 from -13) and changes in unemployment in particular (20 from 15). Despite the less optimistic outlook on the macroeconomic front, households’ assessments of their own future financial situation have remained unchanged from the previous month (0). On the other hand, they have revised their savings intentions upwards (11 from 5).

August Confederation of British Industry survey data showed that the balance indicator for output in the manufacturing sector dropped sharply from +3 to -19, the lowest level since September. The indicator of new orders also declined from -9 to -15 while the indicator of average selling prices suggests a further cooling of inflation in the manufacturing sector, easing further from 18 to 8. Other data from the Office for National Statistics (ONS) today showed a lower than expected borrowing by the UK government. In July the deficit was reported at £4.3 bn down from £17.9 bn in June. The PSNB in the financial year to July 2023 was £56.6bn, £13.7bn more than in the same four-month period last year but £11.3bn less than the £68bn forecast by the Office for Budget Responsibility (OBR). Public sector net debt was £2,578.9bn at the end of July 2023 and provisionally estimated at around 98.5% of the UK’s annual GDP. Data also showed that the UK government transferred a record £14.3bn to the Bank of England in July to cover losses related to the BoE’s QE asset purchases over the previous years.

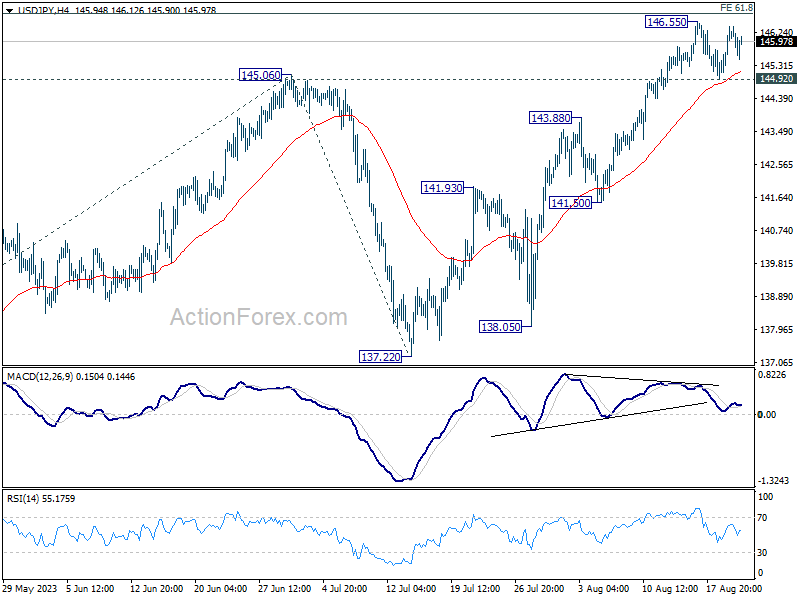

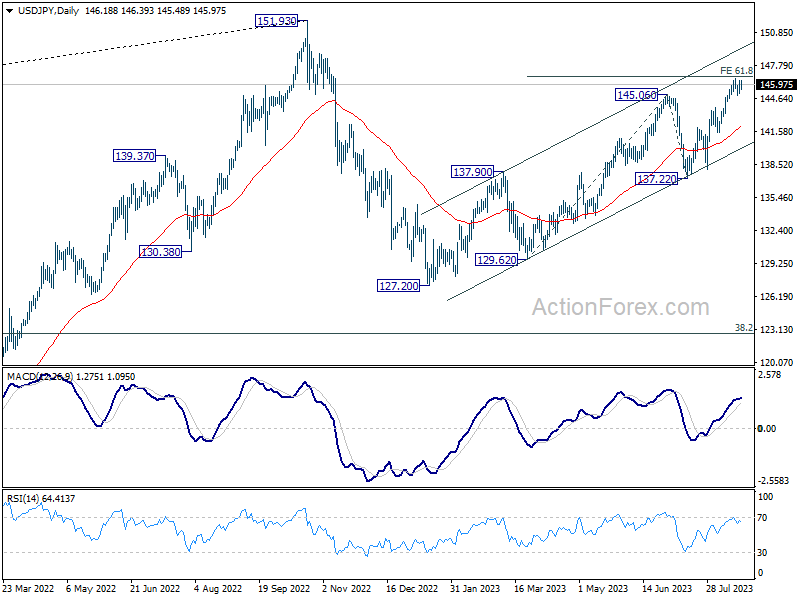

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.92; (P) 145.40; (R1) 145.87; More...

Intraday bias in USD/JPY stays neutral for the moment. On the upside, sustained break of 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76 will pave the way to retest 151.93 high. However, considering bearish divergence condition in 4H MACD, firm break of 44.92 support will be a sign of reversal, and turn bias back to the downside for 55 D EMA (now at 141.95).

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

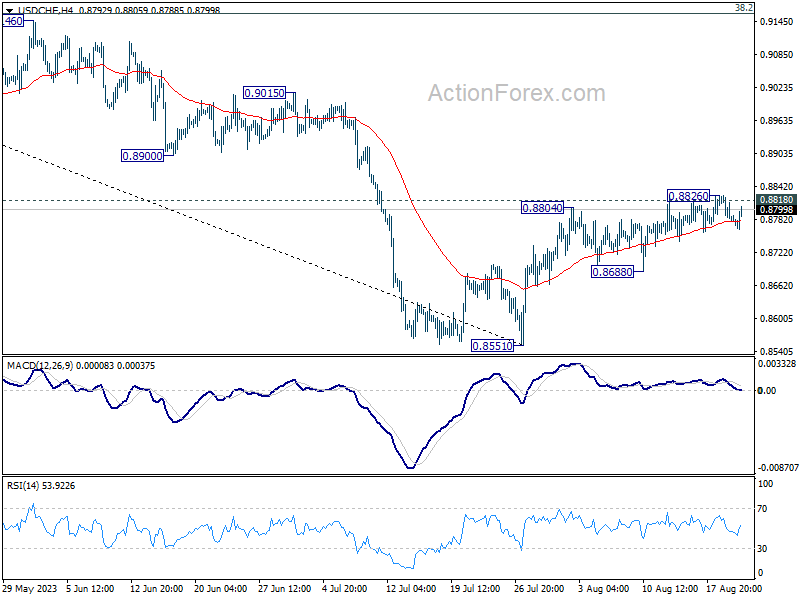

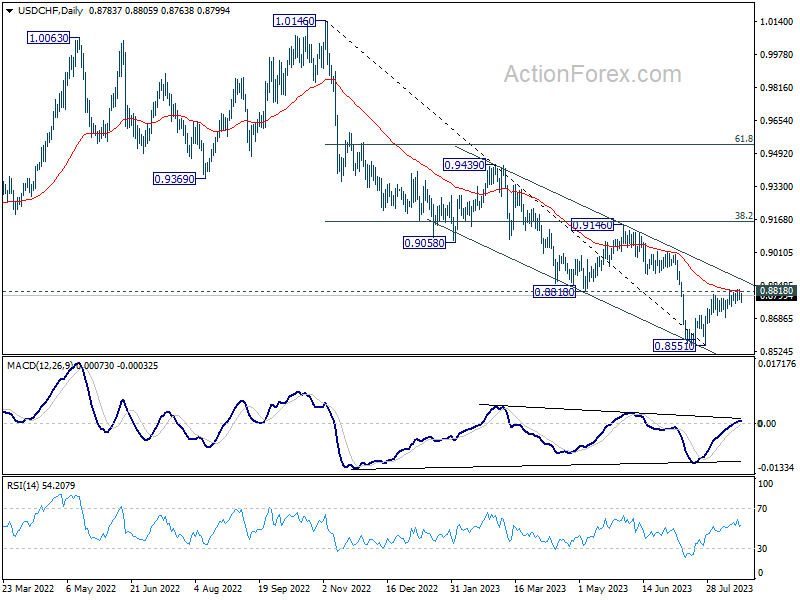

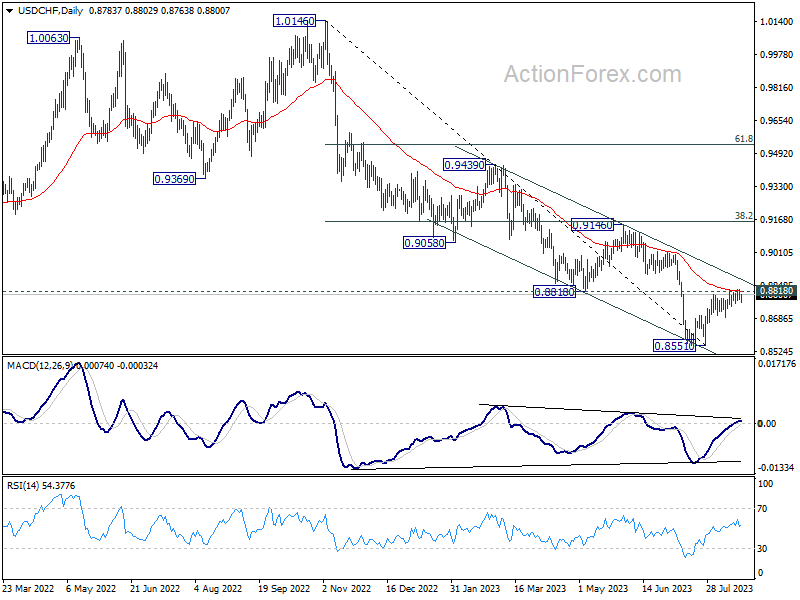

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8767; (P) 0.8797; (R1) 0.8815; More....

Intraday bias in USD/CHF stays neutral at this point. On the upside, decisive break of 0.8818 will carry larger bullish implication, and target 0.9146 cluster resistance next. However, break of 0.8688 support will indicate rejection by 0.8818, and turn bias back to the downside for retesting 0.8551 low.

In the bigger picture, a medium term bottom could be in place at 0.8551 already, on bullish convergence condition in D MACD. Sustained trading above 0.8818 support turned resistance will bring further rise to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160), even as a correction. Nevertheless, break of 0.8851 will resume the down trend from 1.0146 instead.

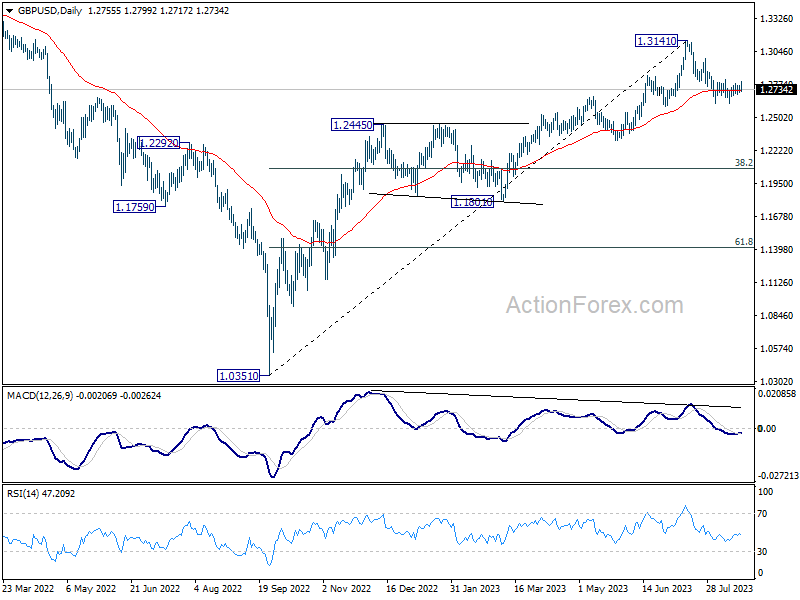

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2723; (P) 1.2745; (R1) 1.2779; More...

Outlook in GBP/USD is unchanged as sideway trading is in progress. Intraday bias stays neutral at this point. On the downside, firm break of 1.2615, and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, break of 1.2817 minor resistance will indicate that the pull back from 1.3141 has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2723) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

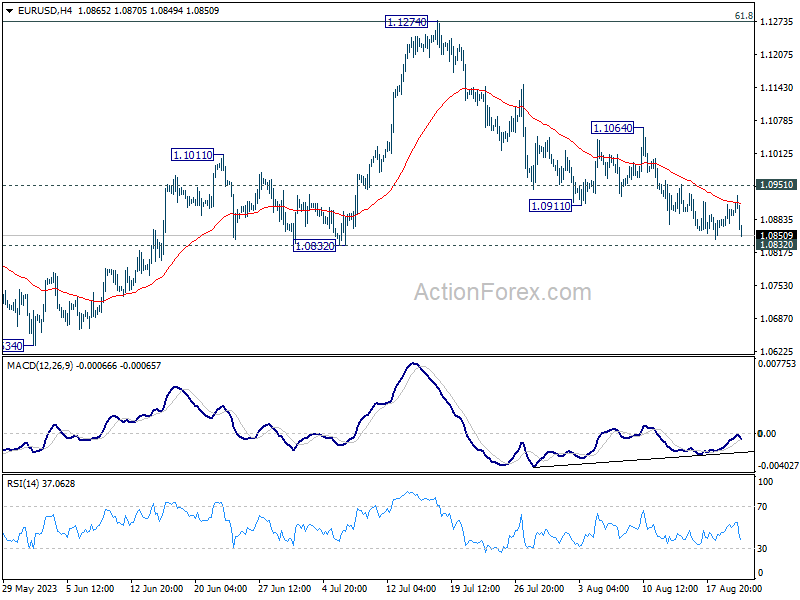

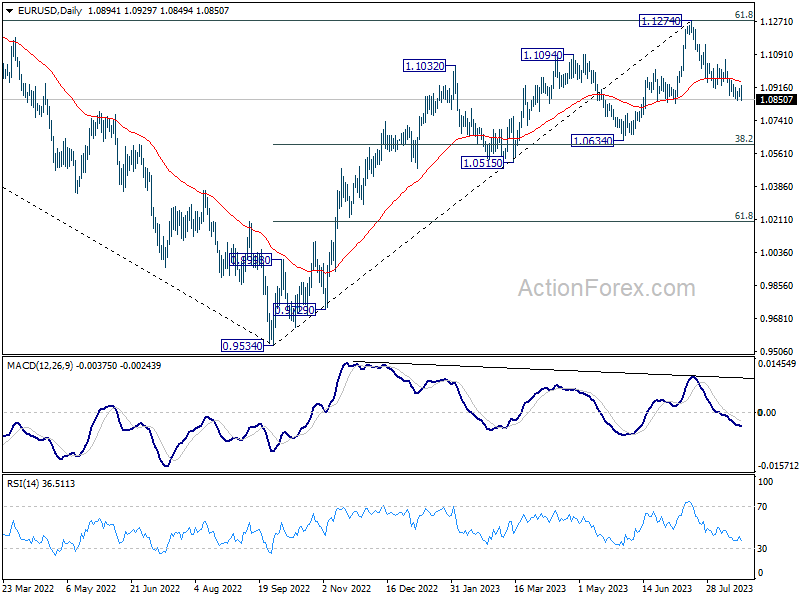

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0873; (P) 1.0893; (R1) 1.0917; More...

EUR/USD dips notably after rejection by 55 4H EMA, but stays above 1.0832 support. Intraday bias remains neutral first. On the downside, decisive break of 1.0832 support will resume the fall from 1.1274 and target 1.0609/34 cluster support next. On the upside, above 1.0951 minor resistance will turn intraday bias to the upside for stronger recovery.

In the bigger picture, a medium term top should be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Fall from there is seen as a correction to the uptrend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.

Euro Lags in Muted Markets; Eyes on Upcoming PMI Data

Euro is currently the weakest major currency in very quiet markets today, with little of note from the economic calendar. Meanwhile, other European majors are soft too, with Sterling just performing slightly better than Swiss Franc. Meanwhile, the rebound in metal prices is helping Aussie recover, while Kiwi is following. Yen is reversing earlier selloff but there is no sign of a sustainable rebound yet. The markets might just wait for tomorrow's PMI data from major economies to come back to life.

Technically, Dollar is mixed for now without a clear near term direction. USD/CHF continues to press 0.8818 support turned resistance, which now coincides with 55 D EMA (now at 0.8818). Sustained break there will be a strong signal that it's at least correcting the down trend from 1.0146. Stronger rally should be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). However, rejection by 0.8818 and 55 D EMA will maintain near term bearishness for another fall through 0.8551 low. Clarity on the direction should emerge in the next few days.

In Europe, at the time of writing, FTSE is up 0.51%. DAX is up 0.99%. CAC is up 0.97%. Germany 10-year yield is down -0.0246 at 2.677. Earlier in Asia, Nikkei rose 0.92%. Hong Kong HSI rose 0.95%. China Shanghai SSE rose 0.88%. Singapore Strait Times rose 0.19%. Japan 10-year JGB yield rose 0.0163 to 0.672.

Fed Barkin emphasizes need to uphold 2% inflation target for credibility

Richmond Fed President Thomas Barkin voiced his perspective on the importance of adhering to its 2% inflation target today. He emphasized the paramountcy of maintaining the institution's credibility with the public, noting, "We have one big weapon and that is credibility."

Elucidating on the choice of the 2% benchmark, Barkin said, "There is nothing magic about 2 except that when you set that as a target you probably want to achieve it."

In the broader discussion on the economy, Barkin offered a tempered view. Should the US head into a recession, he anticipates it to be on the "less-severe" side of the spectrum. Moreover, he indicated that while the Fed remains vigilant, it aims to not get overly swayed by transient market fluctuations.

BoJ Ueda meets PM Kishida: Exchange-rate volatility not discussed

In a meeting today, BoJ Governor Kazuo Ueda and Prime Minister Fumio Kishida discussed a range of financial topics. However, in a post-meeting address to the media, Ueda clarified that the recent volatility of exchange rates was not a focal point of their conversation. He stated, "There wasn't anything in particular discussed today," in response to inquiries regarding the topic.

The backdrop to this meeting was Dollar's significant surge over 145 Yen mark. To provide some historical context, when the currency reached this level in September 2022, it prompted Japan's inaugural Yen-buying intervention operation in nearly a quarter of a century, since 1998.

During their dialogue, Ueda shed light on BoJ's recent decision to ease its hold on long-term interest rates, lifting the cap on 10-year JGB yield from 0.50% to 1.00%. Prime Minister Kishida expressed understanding and agreement with the central bank's decision, Ueda remarked.

Highlighting the periodic nature of such high-level meetings, Ueda noted that the recent gathering was in line with the tradition maintained by his predecessor, Haruhiko Kuroda. Such consultations, held once every few months, aim to facilitate discussions on prevailing economic and financial landscapes.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0873; (P) 1.0893; (R1) 1.0917; More...

EUR/USD dips notably after rejection by 55 4H EMA, but stays above 1.0832 support. Intraday bias remains neutral first. On the downside, decisive break of 1.0832 support will resume the fall from 1.1274 and target 1.0609/34 cluster support next. On the upside, above 1.0951 minor resistance will turn intraday bias to the upside for stronger recovery.

In the bigger picture, a medium term top should be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Fall from there is seen as a correction to the uptrend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | CHF | Trade Balance (CHF) Jul | 3.13B | 4.50B | 4.82B | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jul | 3.5B | 3.4B | 17.7B | 17.1B |

| 08:00 | EUR | Eurozone Current Account (EUR) Jun | 35.8B | 10.2B | 9.1B | 7.9B |

| 14:00 | USD | Existing Home Sales Jul | 4.15M | 4.16M |

Fed Barkin emphasizes need to uphold 2% inflation target for credibility

Richmond Fed President Thomas Barkin voiced his perspective on the importance of adhering to its 2% inflation target today. He emphasized the paramountcy of maintaining the institution's credibility with the public, noting, "We have one big weapon and that is credibility."

Elucidating on the choice of the 2% benchmark, Barkin said, "There is nothing magic about 2 except that when you set that as a target you probably want to achieve it."

In the broader discussion on the economy, Barkin offered a tempered view. Should the US head into a recession, he anticipates it to be on the "less-severe" side of the spectrum. Moreover, he indicated that while the Fed remains vigilant, it aims to not get overly swayed by transient market fluctuations.