Sample Category Title

New Zealand Dollar Shrugs as Inflation Expectations Rise

- New Zealand inflation expectations rise to 2.83%

- China’s inflation decreases for the first time since February 2021

The New Zealand dollar is showing limited movement on Wednesday, trading at 0.6060 in the European session.

New Zealand inflation expectations nudge higher to 2.83%

Like most major central banks, the Reserve Bank of New Zealand has been waging a long and tough battle against inflation by raising interest rates. CPI fell to 6.0% in the second quarter, down from 6.7%. That’s certainly good news, but let’s remember that inflation is still rising sharply and is much higher than the RBNZ’s 2% target.

The central bank is also concerned about inflation expectations, which can become embedded when inflation is high and translate into even higher inflation. Wednesday’s 2-year inflation expectations release showed a rise to 2.83% in the third quarter, up from 2.79% in the second quarter. One-year inflation expectations fell to 4.17% in Q3, down from 4.17% in Q2.

The data indicates that inflation expectations remain high, and that perception could make the life of policy makers more difficult in the fight to bring down inflation. The RBNZ has a long way to go before inflation falls to the 2% target, and that will likely mean further rate hikes unless inflation levels fall sharply. The RBNZ held rates at 5 .50% in July and meets next on August 16th.

China’s CPI indicates deflation

China is experiencing a bumpy recovery, and that is bad news for the global economy. Commodity currencies such as the New Zealand dollar are sensitive to Chinese economic releases and a soft Chinese trade release on Tuesday sent NZD/USD lower by as much as 80 basis points. The bad news continued on Wednesday as China’s CPI for July declined by 0.3% y/y, down from 0.0% in June and just above the consensus estimate of -0.4%. This marked the first decrease in CPI since February 2021 and points to weakness in the Chinese economy, which will likely mean less demand for New Zealand exports, a negative scenario for the New Zealand dollar.

NZD/USD Technical

- NZD/USD continues to put pressure on support at 0.6031. Below, there is support at 0.5964

- 0.6129 and 0.6196 are the next resistance lines

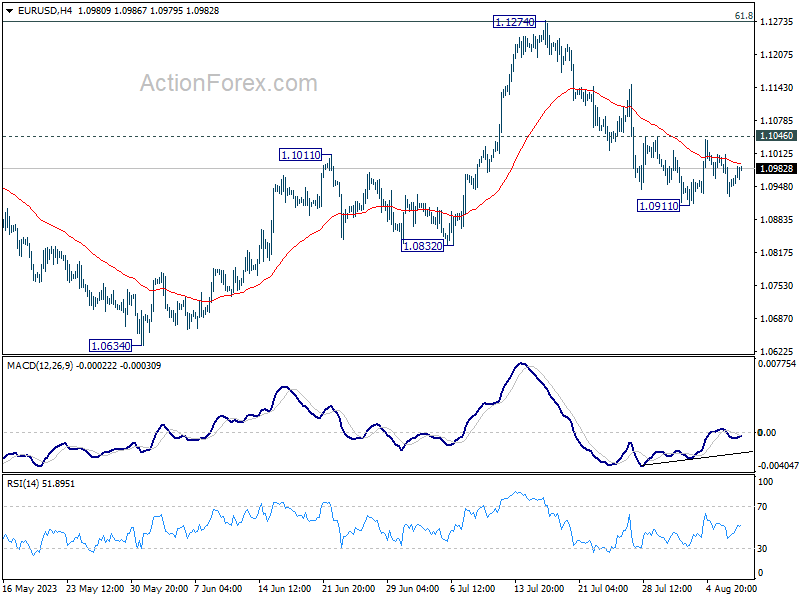

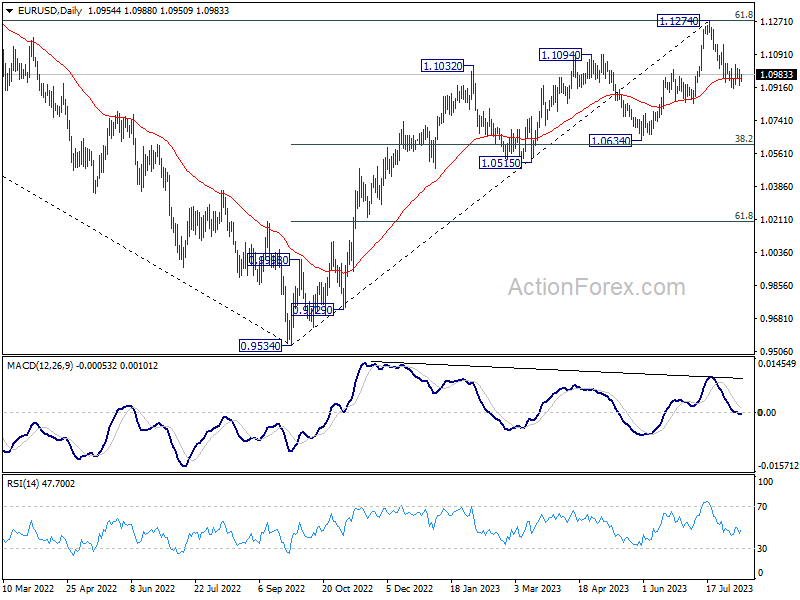

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0920; (P) 1.0966; (R1) 1.1002; More...

Intraday bias in EUR/USD stays neutral for the moment. On the downside, break of 1.0911 will resume the fall from 1.1274 to 1.0832 support. Sustained trading below there will target 1.0609/34 cluster support. However, firm break of 1.1046 minor resistance will argue that pull back from 1.1274 has completed, and bring stronger rebound.

In the bigger picture, a medium term top could be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.0966) will bring deeper correction to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation.

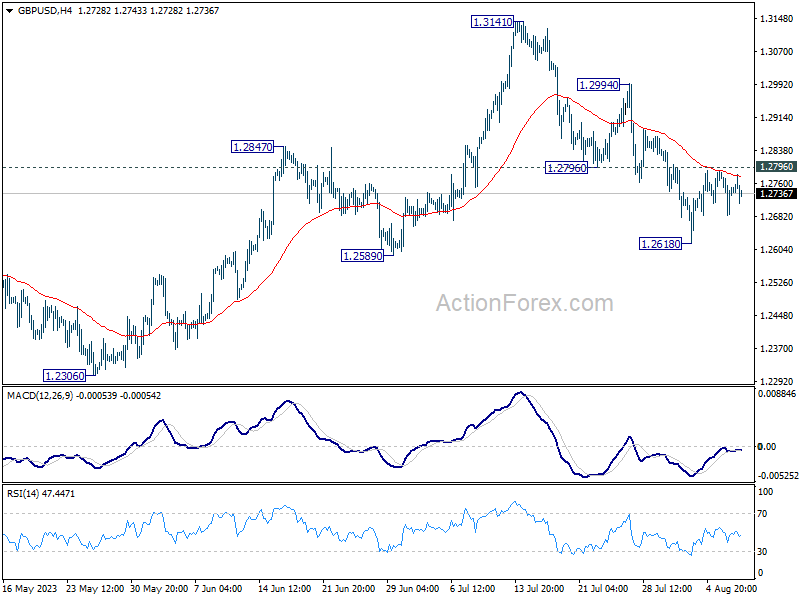

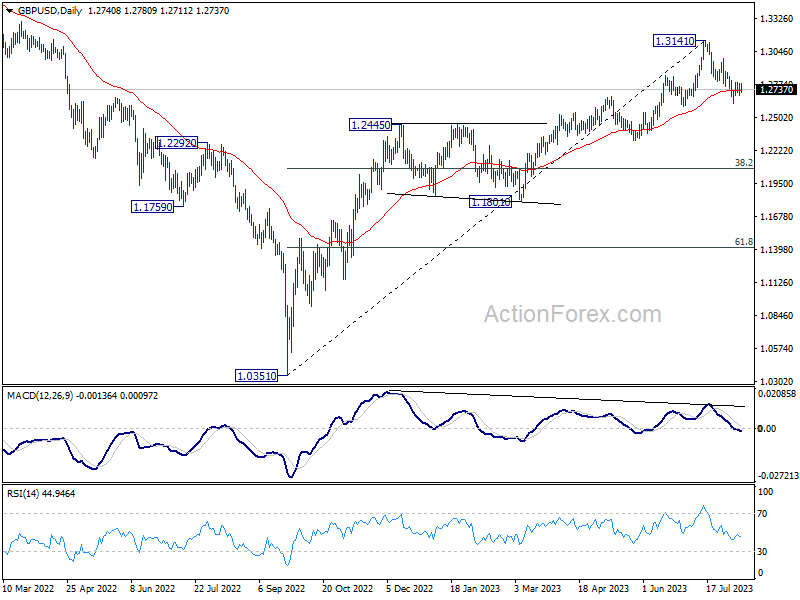

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2692; (P) 1.2740; (R1) 1.2795; More...

Intraday bias in GBP/USD remains neutral for the moment. On the downside, below 1.2618, and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, firm break of 1.2796 will indicate that the pull back has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2726) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

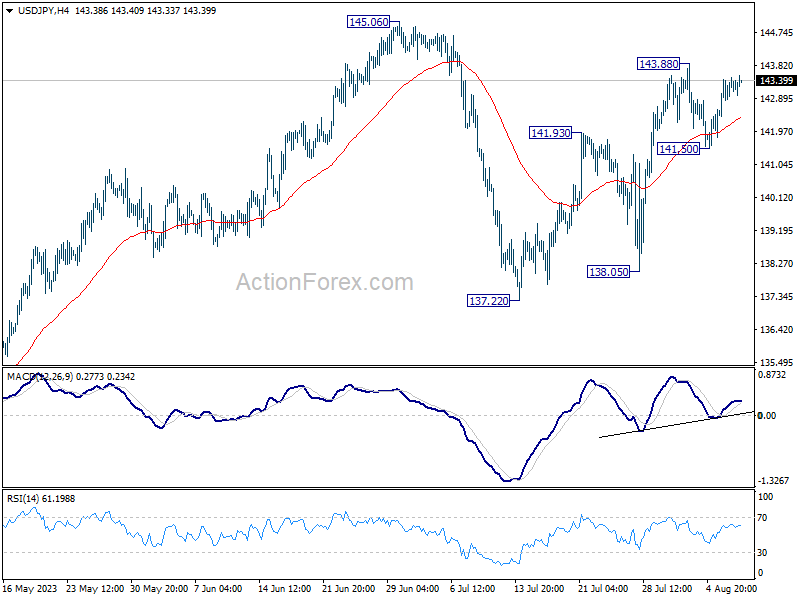

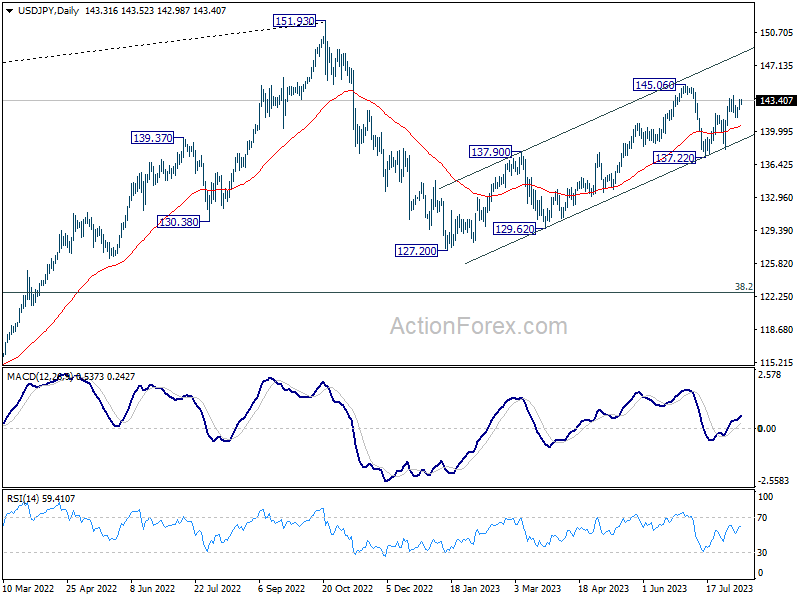

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.69; (P) 143.10; (R1) 143.78; More...

Range trading continues in USD/JPY and intraday bias stays neutral. On the upside, break of 143.88 will resume the rebound from 137.22 to retest 145.06. Decisive break there will resume whole rally from 127.20. On the downside, however, break of 141.50 will turn bias back to the downside for 55 D EMA (now at 140.60).

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

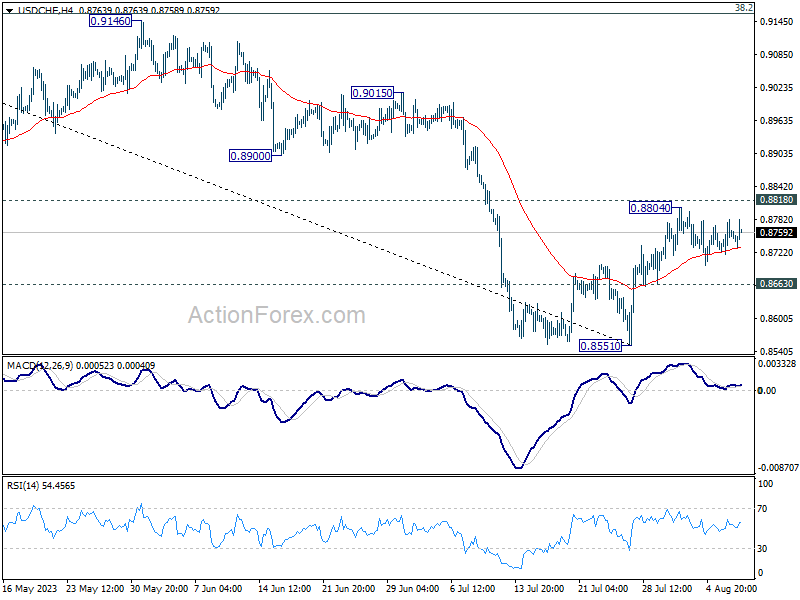

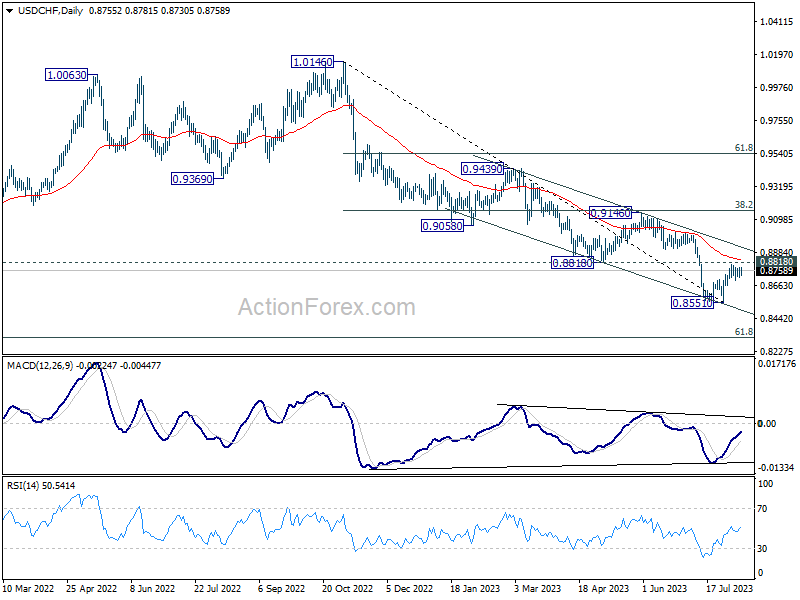

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8720; (P) 0.8752; (R1) 0.8785; More....

USD/CHF recovers mildly after hitting 55 4H EMA, but remains bounded in range. Intraday bias stays neutral at this point. On the downside break of 0.8663 minor support should confirm rejection by 0.8818 and turn intraday bias back to the downside for retesting 0.8551 first. Nevertheless, decisive break of 0.8818 will carry larger bullish implication, and target 0.9146 cluster resistance next.

In the bigger picture, down trend from 1.0146 is seen as in progress as long as 0.8188 support turned resistance holds. Next target is 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317. However, sustained break of 0.8818 should indicate medium term bottoming, and bring stronger rise back to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160), even as a correction.

Dollar and Euro Navigate Narrow Waters in Quiet Markets

Dollar has regained some prominence in today's trading, albeit just as a part of this week's oscillating trends. A majority of major currency pairs and crosses are confined within yesterday's trading ranges. The day's lull is evident, with a notable absence of significant economic announcements from Europe and US. Additionally, leading central bankers have remained silent.

In the broader currency landscape, Euro has also made modest gains against both Sterling and Swiss Franc but remains within familiar ranges. As it stands, Swiss Franc and Sterling are the worst performers for the day, while commodity currencies are mixed.

As market participants await tomorrow's US CPI data – assuming they aren't enjoying a summer break – several technical level come to the fore. These include 1.1046 minor resistance for EUR/USD, 1.2796 for GBP/USD, 0.8663 minor support in USD/CHF, and 141.50 minor support for USD/JPY. Simultaneous break of these levels could be a strong indication of selling momentum in the greenback.

In Europe, at the time of writing, FTSE is up 0.65%. DAX is up 0.77%. CAC is up 0.92%. Germany 10-year yield is up 0.046 at 2.515. Earlier in Asia, Nikkei dropped -0.53%. Hong Kong HSI rose 0.32%. China Shanghai SSE dropped -0.49%. Singapore Strait Times rose 0.12%. Japan 10-year JGB yield dropped sharply by -0.0465 to 0.565.

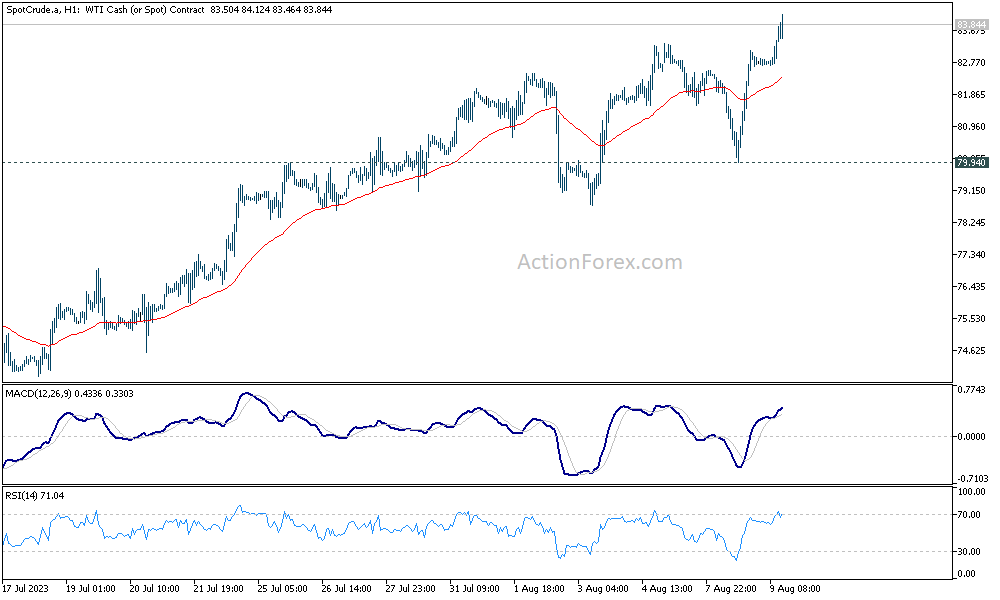

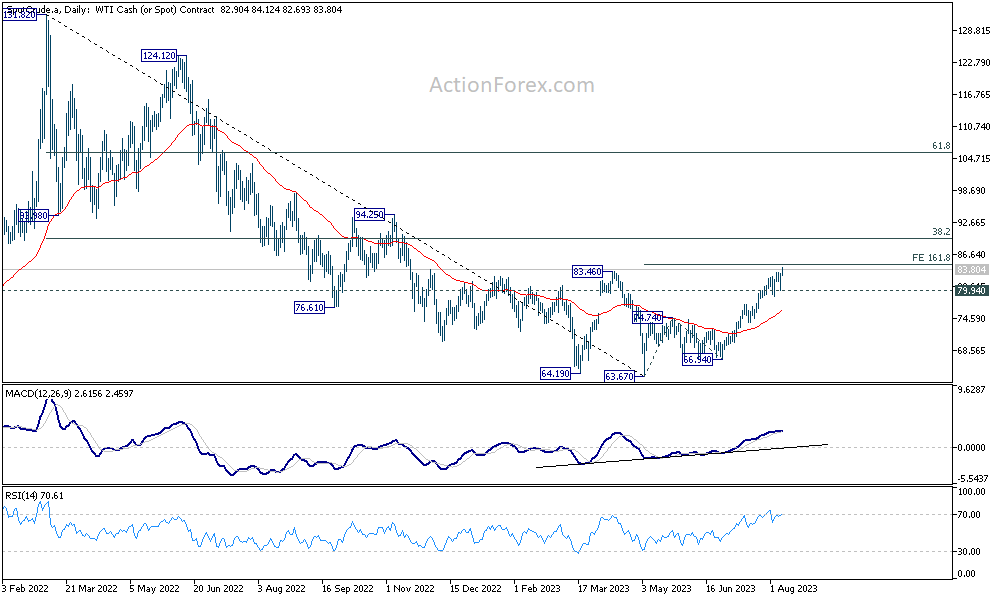

WTI hits highest level this year, targeting 85 next

WTI crude oil continued its impressive rally, marking its highest price point for the year. This surge comes in the wake of Saudi Arabia's firm stance, as the nation's cabinet confirmed yesterday its unwavering support for the precautionary strategies adopted by OPEC+.

Adding weight to this commitment, just last week, Saudi Arabia prolonged its voluntary slash in production by a significant 1 million barrels daily until the end of September. Besides, Russia further bolstered the market sentiment by announcing a reduction in oil exports by 300,000 bpd for September.

Technically, near term outlook in WTI will now stay bullish as long as 79.94 support holds. Next target is 161.8% projection of 63.67 to 74.74 from 66.94 at 84.85, and possibly above.

However, barring any dramatic development, strong resistance should be seen from 38.2% retracement of 131.82 (2022 high) to 63.67 (2023 low) at 89.70 to limit upside, at least on first attempt.

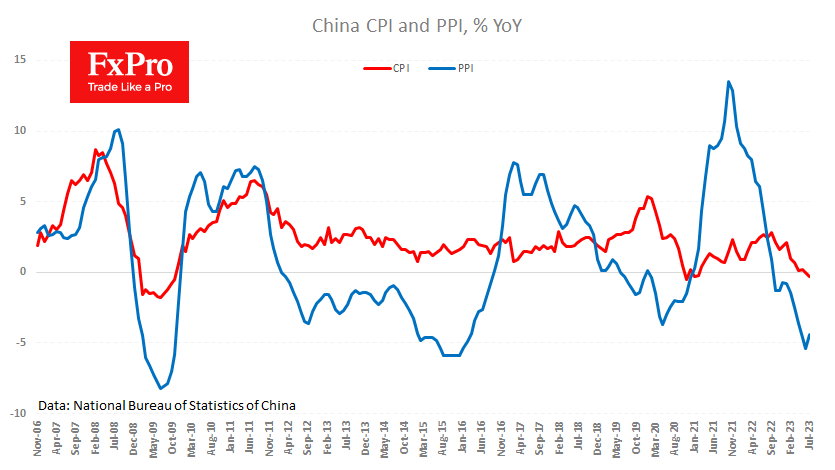

China CPI down -0.3% yoy, first negative since 2021

China's CPI for July registered a drop of -0.3% yoy, marking its first decline since February 2021. Although this result is slightly better than the market's expectation of a -0.4% drop, it underscores the economic headwinds faced.

Core inflation measure, which excludes the often erratic food and energy costs, showed a rise to 0.8% yoy from a mere 0.4% yoy. This points to some underlying demand within the economy, albeit muted.

A deeper dive into CPI reveals that food prices have seen a -1% fall yoy, a sharp contrast to the 2.3% yoy rise observed in the previous month. On the other hand, non-food prices climbed 0.5% yoy last month, bouncing back from a -0.6% yoy.

Dong Lijuan, chief statistician at the NBS, commented, "With the impact of a high base from last year gradually fading, the CPI is likely to rebound gradually."

On the PPI front, situation remains challenging. PPI improved from -5.4% yoy to -4.4% yoy in July. This figure not only missed market expectations, which stood at -3.8% yoy, but also marked the tenth straight month of negative readings.

RBNZ business survey points to lower inflation expectations, steady interest rates

As seen from the latest Quarterly RBNZ Survey of Expectations, businesses have slightly tapered their inflation expectations in the near term but wage inflation expectations were on the rise. RBNZ OCR is expected to be unchanged at the current 5.50% through the quarter.

Expectations for annual inflation one year ahead have moderated, moving from 4.28% to 4.17%. However, a two-year horizon sees a marginal uptick in these expectations, which have climbed from 2.79% to 2.83%.

More long-term views, reflected in the five and ten-year ahead inflation expectations, both indicate a pullback, dropping to 2.25% (from 2.35%) and 2.22% (from 2.28%), respectively.

A notable area of concern stems from the annual wage inflation expectations. Over the course of both one and two years, these expectations are on the rise. For the year ahead, expectations climbed from 4.80% to 5.04%, and for the two-year mark, they increased from 3.53% to 3.66%.

Regarding monetary policy, the survey results indicate a stable outlook on the OCR. By the close of the September 2023 quarter, businesses anticipate OCR to average around 5.53%, a minimal climb from the prior quarter's estimate of 5.47%. A one-year ahead mean estimate rose 32 basis points to 5.16% from the previous 4.84%.

Average one-year ahead GDP growth forecast surged to 1.02%, up from previous 0.48%. Moreover, businesses seem to be projecting continued momentum, with two-year ahead GDP growth expectations reaching 1.95% from preceding 1.66%.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8720; (P) 0.8752; (R1) 0.8785; More....

USD/CHF recovers mildly after hitting 55 4H EMA, but remains bounded in range. Intraday bias stays neutral at this point. On the downside break of 0.8663 minor support should confirm rejection by 0.8818 and turn intraday bias back to the downside for retesting 0.8551 first. Nevertheless, decisive break of 0.8818 will carry larger bullish implication, and target 0.9146 cluster resistance next.

In the bigger picture, down trend from 1.0146 is seen as in progress as long as 0.8188 support turned resistance holds. Next target is 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317. However, sustained break of 0.8818 should indicate medium term bottoming, and bring stronger rise back to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160), even as a correction.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | CNY | CPI Y/Y Jul | -0.30% | -0.40% | 0.00% | |

| 01:30 | CNY | PPI Y/Y Jul | -4.40% | -3.80% | -5.40% | |

| 03:00 | NZD | RBNZ Inflation Expectations Q/Q Q3 | 2.83% | 2.79% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Jul P | -19.80% | -21.70% | -21.10% | |

| 12:30 | CAD | Building Permits M/M Jun | 6.10% | 2.30% | 10.50% | |

| 14:30 | USD | Crude Oil Inventories | 2.1M | -17.0M |

China Deflation and Commodity Currency Outlook

For so many countries, getting inflation down has been a real challenge. So, a bit of deflation might be seen as a good thing. But the opposite of inflation is also a problem for an economy. And the existence of deflation in a period when the economy is supposed to be growing, can be a significant warning sign.

Yesterday, China reported an annual CPI of -0.3%, which was actually higher than the -0.4% expected. An important portion of that could be down to base effects, because the monthly rate grew once again at 0.2%. But the fact that the world's second largest economy is seeing deflation right after reporting a significant slowdown in trade can be a problem for the global economy.

Markets are under pressure

There were several issues that have continued to hurt risk appetite through the start of the week, such as the downgrade of several US banks. But the situation in China is apparently the largest factor driving markets lately, as investors are once again pricing in the chance of a global recession. Just that now it seems more likely to be due to China underperforming than the US.

Typically, August is a growth month for markets, fueled by summer optimism with many risk events taken off the table. The reversal in fortunes usually doesn't come until September. But, the summer might be ending a little early this year, as risk shifts away from the US towards China. To further emphasize that trend, 499 of the S&P 500 components have reported as of yesterday, with over 80% beating earnings estimates, with an average beat of 7%. That exceeds the inflation rate of the period, suggesting US major corporations are seeing growing profits.

The China risk

Meanwhile, a slowing economy despite the Chinese government's best efforts to push domestic demand seems to be the best explanation for the recent deflation reports. Headline inflation benefited from an increase in fresh food supplies. But what concerns global markets is that factory-gate inflation was negative. That means slowing demand for Chinese-made industrial products.

The other major driver of falling prices in China was a drop in commodity prices, driven by slowing demand. That could have knock-on effects on China's major suppliers, notably the Australian dollar. China has continued to buy many commodities, including crude - but that buying has gone to stockpiles, as domestic demand remains weak. With Chinese factories selling less, as measured in fewer exports, demand for raw materials remains under pressure.

What about gold?

Besides commodities, China is the world's largest retail buyer of gold. The central bank keeps adding to its gold reserves. But, with a slowing economy, Chinese citizens are less likely to have extra capacity to buy gold. Additionally, a strengthening currency reduces the motivation to buy gold, as well.

With investors piling into safe havens like the dollar, commodities priced in dollars including gold, could come under renewed pressure. Crude being the notable exception, as a more resilient than expected US economy has seen increasing demand from the world's largest consumer.

WTI hits highest level this year, targeting 85 next

WTI crude oil continued its impressive rally, marking its highest price point for the year. This surge comes in the wake of Saudi Arabia's firm stance, as the nation's cabinet confirmed yesterday its unwavering support for the precautionary strategies adopted by OPEC+.

Adding weight to this commitment, just last week, Saudi Arabia prolonged its voluntary slash in production by a significant 1 million barrels daily until the end of September. Besides, Russia further bolstered the market sentiment by announcing a reduction in oil exports by 300,000 bpd for September.

Technically, near term outlook in WTI will now stay bullish as long as 79.94 support holds. Next target is 161.8% projection of 63.67 to 74.74 from 66.94 at 84.85, and possibly above.

However, barring any dramatic development, strong resistance should be seen from 38.2% retracement of 131.82 (2022 high) to 63.67 (2023 low) at 89.70 to limit upside, at least on first attempt.

Australian Dollar Edges Higher after Mixed Confidence Data

- Australian consumer confidence declines, business confidence steady

- Fed member Harker says Fed may be done raising rates

The Australian dollar has bounced back on Wednesday and is trading at 0.6552, up 0.13%. AUD/USD slipped 0.45% on Tuesday and dropped to its lowest level since June 1st.

Australian consumer confidence slips, business mood stays steady

Australia’s consumers remain deeply pessimistic about economic conditions. The Westpac consumer sentiment index declined in August by 0.4% to 81 points, well below the 100 level which divides optimists and pessimists. In July, the index rose 2.7%. Consumer sentiment fell despite the Reserve Bank of Australia’s decision in July to hold rates steady for a second straight month. The RBA has raised rates by some 400 basis points in the current cycle and high borrowing costs continue to dampen consumer sentiment.

Business confidence also remains low, but the situation is somewhat better. The National Bank Business Confidence (NAB) index for July improved to 2, up from a downwardly revised -1 in June. This was the highest level since January. The zero level divides optimists from pessimists. Business conditions eased slightly to 10, indicating that businesses continue to show resilience to higher borrowing costs. The strength of the business sector is an encouraging sign that the economy could avoid a hard landing despite the RBA’s aggressive tightening cycle.

Fed’s Harker eyes rate cuts in 2024

Fed member Harker said on Tuesday that the Fed might be done raising rates, “absent any alarming new data”. Harker said that rates would need to stay at the current high levels “for a while” and went as far as saying that the Fed would likely cut rates at some point in 2024. Harker was careful not to express an opinion about the September decision, but the Fed rate hike odds are just 14%, according to the FedWatch tool. The Fed raised rates in July, and Fed Chair Powell has signalled that he would raise rates one more time a stance that is clearly more hawkish than that of the markets.

AUD/USD Technical

- There is resistance at 0.6607 and 0.6700

- 0.6475 and 0.6382 are providing support

What China’s Weak Inflation Tells Us

China’s CPI was 0.3% lower year-on-year in July, which the media has rushed to call deflation, while by definition, it is a sustained price fall. It is more accurate to discuss disinflationary pressures caused by one-off factors, including last year’s high base. For example, a 26% fall in pork prices has contributed to the current decline.

Producer prices fell by 4.4% YoY last month, down from 5.4%. A reversal of the upward trend is likely. Of course, much of the downward pressure on prices in recent months has been due to weak demand for goods inside and outside China.

This is to the benefit of global central banks, as the fall in producer prices seen since October in the so-called “world’s factory” is helping to reduce global inflationary pressures. This effect is leveraged by the 7.5% fall in the yuan against the dollar since the start of the year. In such an environment, central banks may continue to receive “good surprises” from inflation reports and stop their hikes sooner than previously thought.

However, questions may arise about whether this is the start of a competitive devaluation as China competes for markets amid the acceleration of other major regional economies, such as India. At the same time, the fall in prices in China does not signal an imminent policy reversal by the Fed, ECB, or Bank of England, which are fighting rising costs for services, not goods, and slowing their economies is not an option.