Sample Category Title

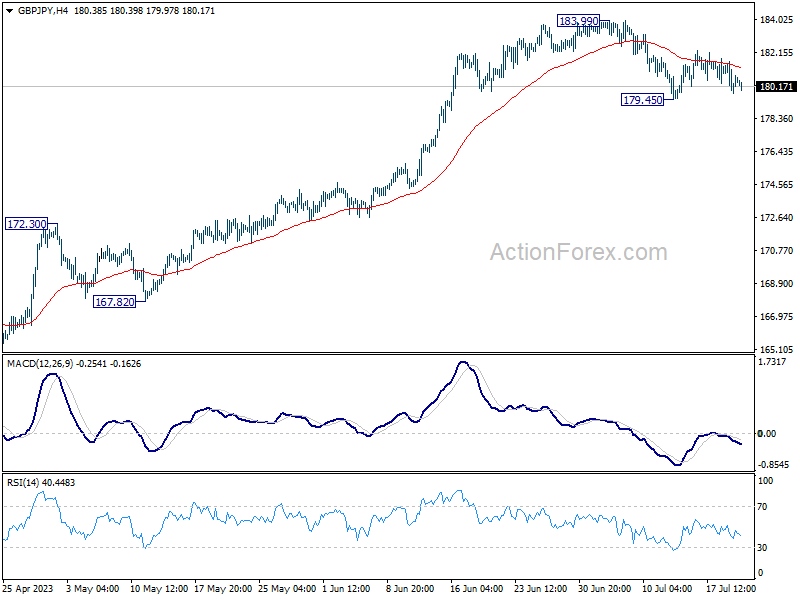

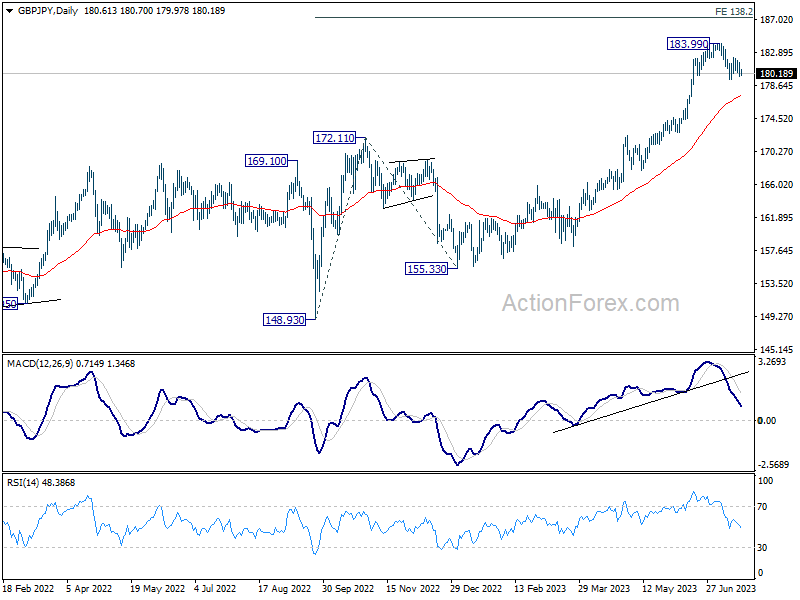

GBP/JPY Daily Outlook

Daily Pivots: (S1) 179.83; (P) 180.74; (R1) 181.64; More...

Intraday bias in GBP/JPY remains neutral for the moment. On the downside, break of 179.45 will resume the correction from 183.90 to 55 D EMA (now at 177.39). On the upside, firm break of 183.99 high will resume larger up trend to 187.36 projection level.

In the bigger picture, as long as 172.11 resistance turned support holds, up trend from 123.94 (2020 low) is expected to continue. On resumption, next target is 138.2% projection of 148.93 to 172.11 from 155.33 at 187.36, and then 195.86 (2015 high). Nevertheless, firm break of 172.11 will argue that larger correction is already underway.

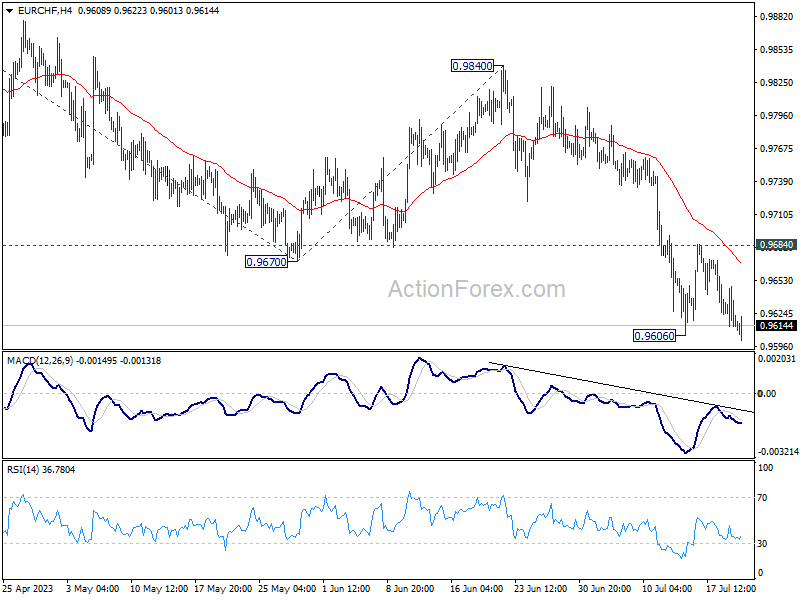

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9605; (P) 0.9627; (R1) 0.9640; More...

EUR/CHF's is resuming recent decline by breaking through 0.9606. Intraday bias is back on the downside. The fall from 1.0095 would target 100% projection of 0.9995 to 0.9670 from 0.9840 at 0.9515. On the upside, break of 0.9684 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, medium term outlook is staying bearish as the pair is capped below falling 55 W EMA (now at 0.9913). Down trend form 1.2004 (2018 high) is in favor to extend through 0.9407 at a later stage. Nevertheless, decisive break of 38.2% retracement of 1.1149 to 0.9407 will raise the chance of bullish trend reversal.

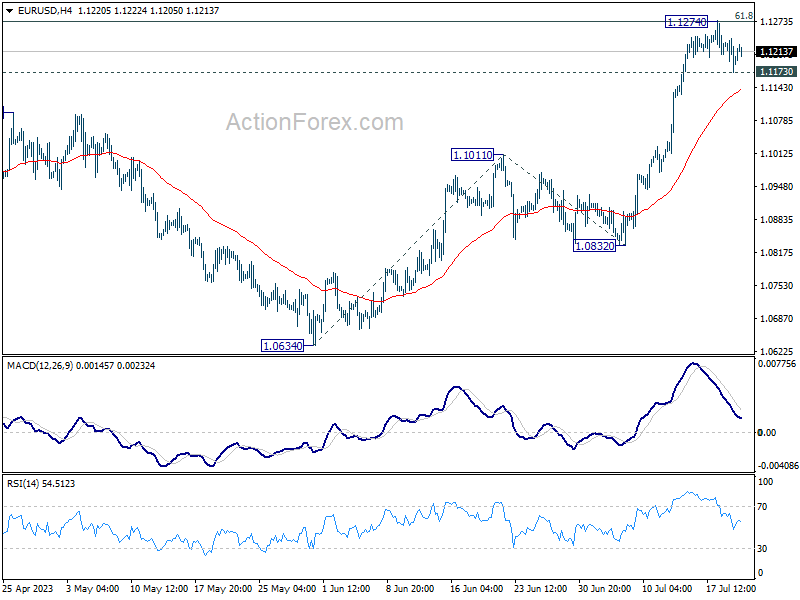

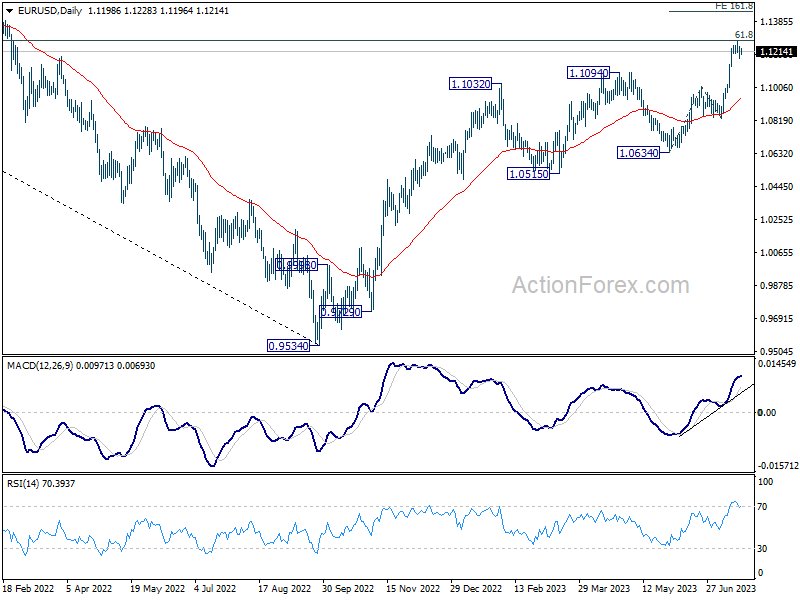

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1171; (P) 1.1206; (R1) 1.1237; More...

EUR/USD dipped to 1.1173 but quickly recovered. Intraday bias remains neutral at this point. On the downside, break of 1.1173 minor support will indicate rejection by 1.1273 fibonacci level. Intraday bias will be back on the downside for deeper pull back to 55 4H EMA (now at 1.1140) and below. Nevertheless, sustained break of 1.1273 will extend larger up trend to 161.8% projection of 1.0634 to 1.1011 from 1.0832 at 1.1442 next.

In the bigger picture, as rise from 0.9534 extends, focus is now on 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next. Meanwhile, outlook will continue to stay bullish as long as 1.0832 support holds, even in case of deep pull back.

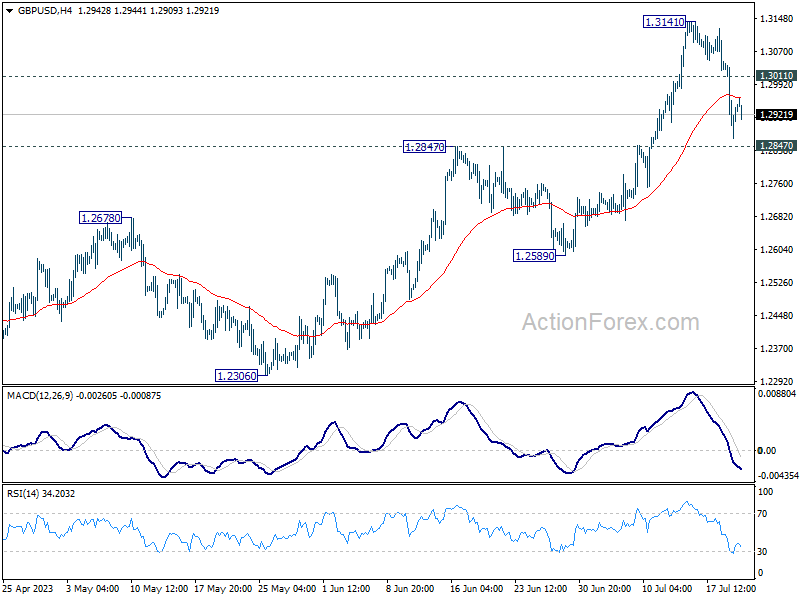

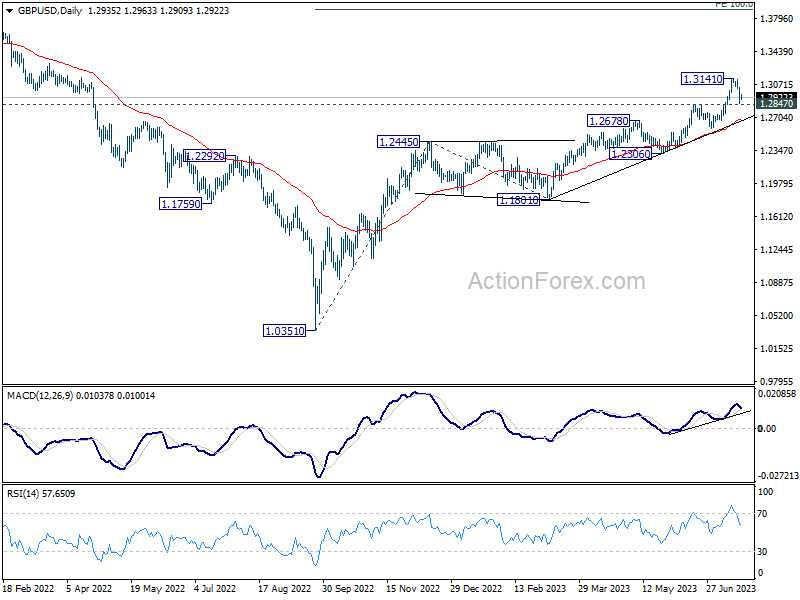

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2857; (P) 1.2951; (R1) 1.3034; More...

Intraday bias in GBP/USD stays neutral for the moment. Near term outlook will stay bullish as long as 1.2847 resistance turned support holds. On the upside, above 1.3011 minor resistance will turn bias back to the upside for retesting 1.3141 high. Nevertheless, decisive break of 1.2847 will argue that larger correction is underway and target 1.2589 support next.

In the bigger picture, rise from 1.0351 medium term bottom (2022 low) is in progress. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. Break there will target 1.4248 key long term resistance (2021 high) next. This will now remain the favored case as long as 1.2678 resistance turned support holds.

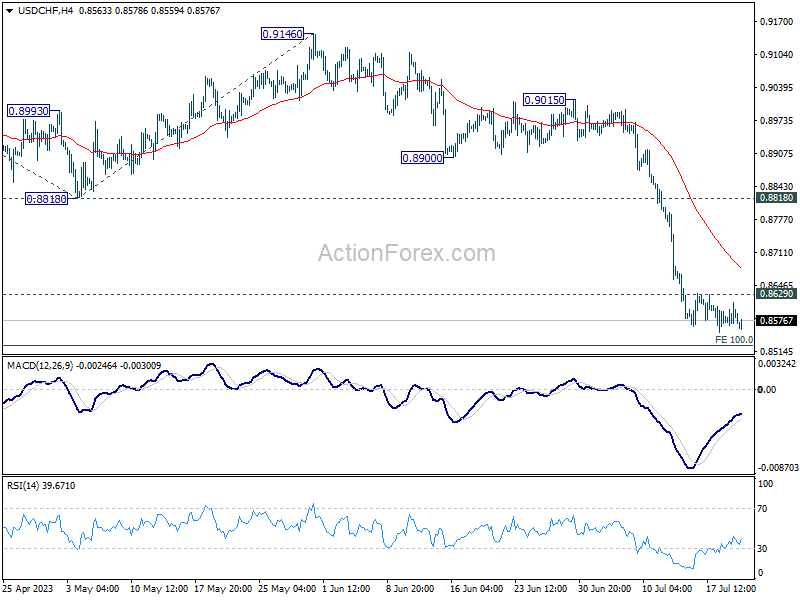

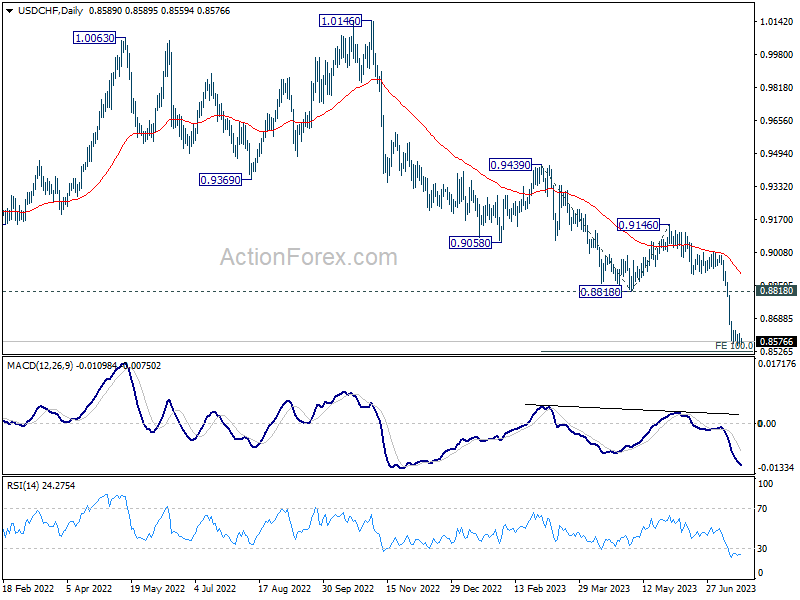

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8563; (P) 0.8588; (R1) 0.8610; More...

Further decline cannot be ruled out in USD/CHF. However, some support could be seen from 100% projection of 0.9439 to 0.8818 from 0.9146 at 0.8525 to bring rebound. Break of 0.8629 minor resistance will turn bias to the downside for 55 4H EMA (now at 0.8683) and above.

In the bigger picture, the break of 0.8756 (2021 low) indicates break out from the long term range pattern. For now, medium term outlook will stay bearish as long as 0.9146 resistance holds. Further fall would be seen to 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317 next.

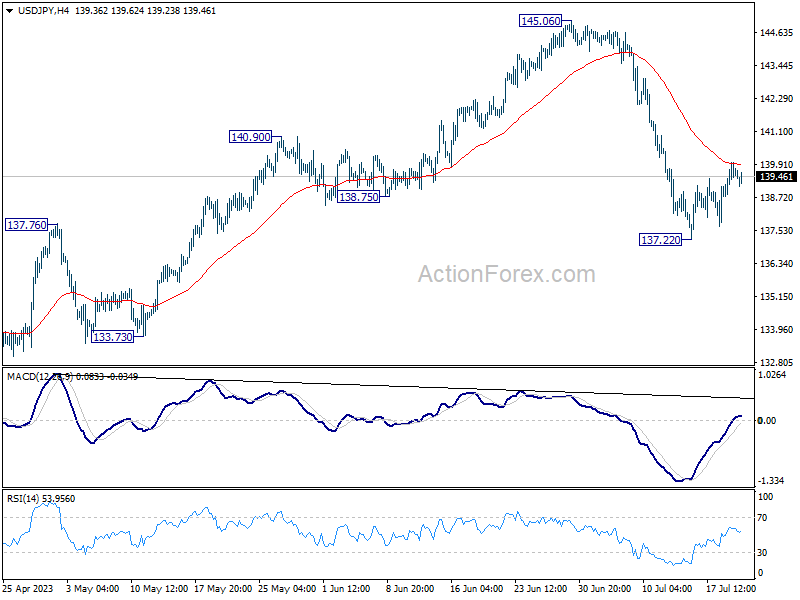

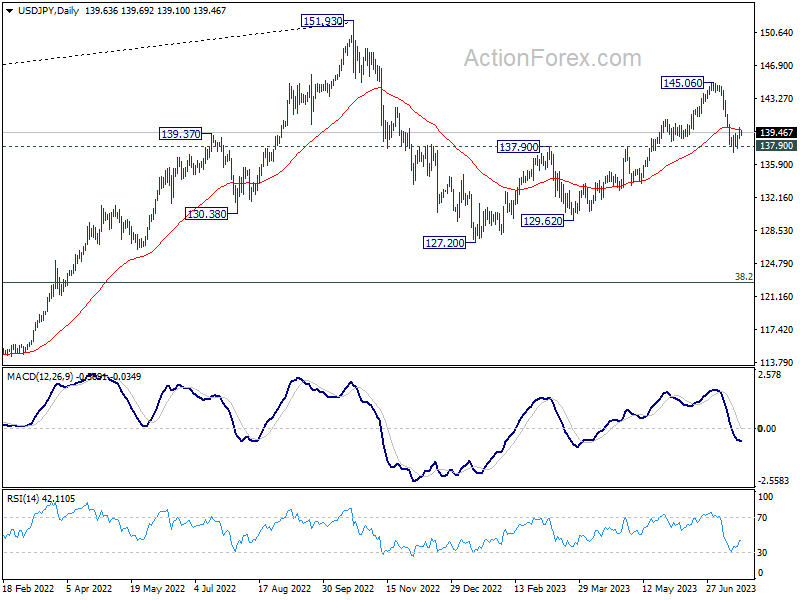

USD/JPY Daily Outlook

Daily Pivots: (S1) 138.97; (P) 139.48; (R1) 140.19; More...

Intraday bias in USD/JPY remains neutral and outlook is unchanged. Strong resistance is expected from 55 4H EMA (now at 139.87) to complete the recovery from 137.22. Break of 137.22 and sustained trading below 137.90 resistance turned support will confirm the larger bearish case, and target 127.20 and below. Nevertheless, sustained trading above 55 4H EMA will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 145.06 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Sustained break of 137.90 resistance turned support should confirm this case and target 127.20 (2023 low) and below. For now, this will remain the favored case as long as 145.06 resistance holds, even in case of strong rebound.

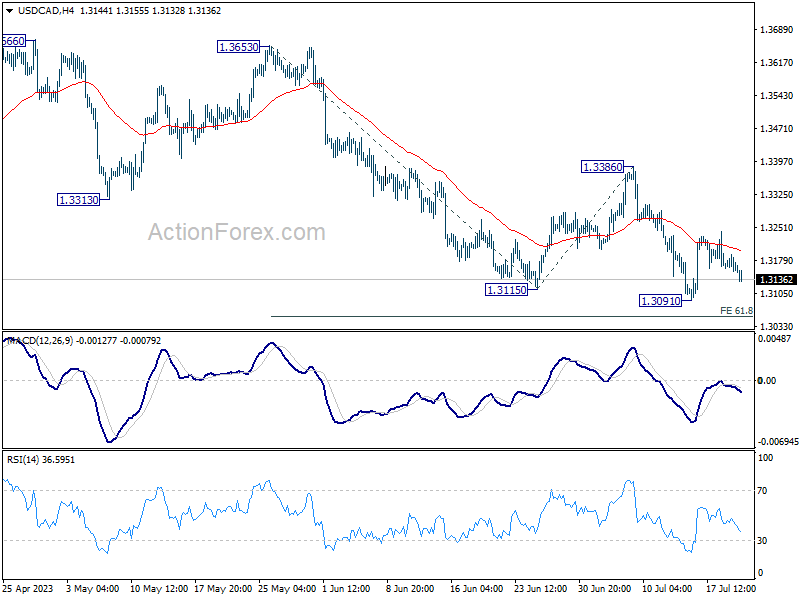

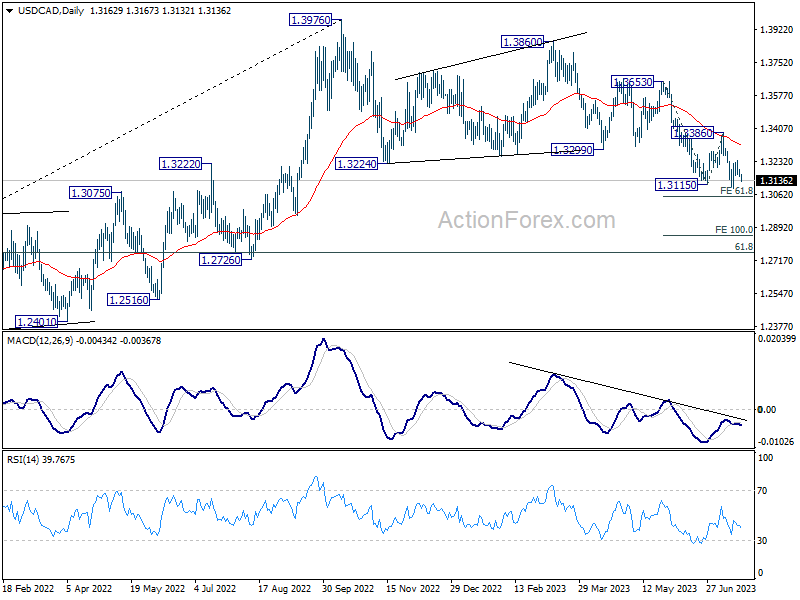

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3142; (P) 1.3193; (R1) 1.3218; More....

USD/CAD is staying in range above 1.3091 and intraday bias stays neutral at this point. With 1.3386 resistance intact, outlook stays bearish. On the downside, break of 1.3091 will larger decline to 61.8% projection of 1.3653 to 1.3115 from 1.3386 at 1.3054. However, firm break of 1.3386 will indicate near term reversal and turn outlook bullish.

In the bigger picture, price actions from 1.3976 are viewed as a correction to up trend from 1.2005 (2021 low) only. But even so, deeper decline is expected as long as 1.3386 resistance holds. Further fall could be seen to 61.8% retracement of 1.2005 to 1.3976 at 1.2758. Meanwhile, break of 1.3386 will be a sign that the correction has completed and bring stronger rally back to retest 1.3976.

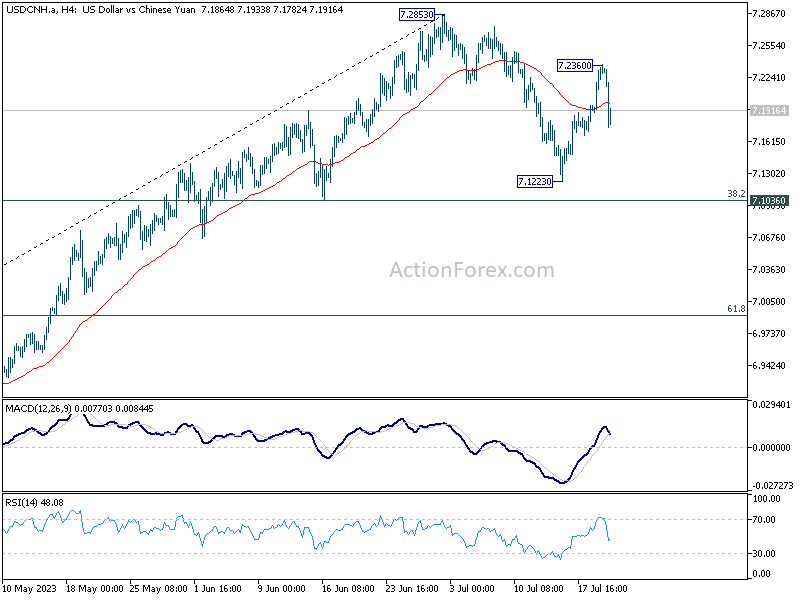

China Set Daily Fixing for USD/CNY Much Stronger than Expected

Markets

UK markets scaled back Bank of England tightening bets after June CPI numbers. After four consecutive months of substantial upward surprises, they declined more than forecast. At 7.9% Y/Y for the headline reading and 6.9% Y/Y for the core gauge, the UK central bank’s jobs remains far from done though. We stick to our August 50 bps rate hike call even as UK money markets reduced the odds to 50/50. The expected policy rate peak is lowered from 6% to 5.75%. UK Gilts in a daily perspective outperformed vs German Bunds and US Treasuries. UK Gilts yields fell by 10 bps (30-yr) to 19 bps (2-yr). EU and US bonds in a Pavlov-reaction joined the Gilt rally, but eventually retraced their steps. German yields rose by 1.6 bps (2-yr) to 5.2 bps (10-yr), even undoing part of the ECB Knot triggered downleg on Tuesday (neutral comments on outcome September ECB meeting coming from a hawkish voice). From a technical point of view, the German 10-yr yield received support from the 200d moving average which earlier came to the rescue in March, May and June (2x). The uptrend line connecting April/May/June/July lows remains in place as well. US yields ended 0.2 bps (2-yr) to 5.4 bps (30-yr) lower with disappointing housing data playing a temporary role. Sterling underperformed with EUR/GBP temporarily rising towards 0.87 before closing at 0.8657. The King’s money remains in the defensive this morning. Cable fell back below 1.30 to close at 1.2940. EUR/USD closed at 1.1201 from an open at 1.1228, further establishing a topping off pattern after a test of 1.1274 resistance earlier this week. Stock markets ended mixed with the US slightly outperforming. Today’s eco calendar remains thin with US weekly jobless claims the main event. Consensus expects a stabilization around 240k. Prints in the direction of 260k can trigger another dovish market reaction. Corporate earnings can influence trading via risk sentiment. US equity futures are down following misses by Netflix and by Tesla.

News and views

Australian employment again grew at a faster than expected pace in June. The Australian economy added a net 32.6k jobs, down from a 76.5k gain in May, but more than the 15k rise expected. The rise was entirely due to full time job growth. Part-time jobs declined modestly (-6.7k). The unemployment rate stays at 3.5%, near the all-time low (3.4%) reached in October last year. The number of unemployed people declined 11k. The Australian bureau of statistics assessed that “The rise in employment in June saw the employment-to-population ratio remain at a record high 64.5%, reflecting a tight labour market in which employment has recently increased in line with population growth. In addition to there being over a million more employed people than before the pandemic, a much higher share of the population is employed. In June 2023, 64.5% of people 15 years or older were employed, an increase of 2.1 percentage points since March 2020.” Tight labour market conditions continue to put pressure on the Reserve bank of Australia to further raise its policy rate at the Aug 1 policy meeting, after pausing at 4.1% early July. The Australian 2-y yield jumped 11.9 bps to 3.98% after a decline in line with global market developments of late. The Aussie dollar gained from the AUD/USD 0.6770 area before the data release to currently trade near 0.683.

The People’s Bank of China set its daily fixing for USD/CNY much stronger than expected. According to a Bloomberg survey, the deviation/bias was the strongest since November of last year. The fixing is another sign that the PBOC is unhappy with recent yuan weakness, which at the same time is a ‘logical consequence’ of China keeping a more supportive monetary policy compared to most other major central banks. Aside from the stronger fixing, the PBOC also changed some rules with respect to capital inflows as it allowed banks to borrow more overseas, supporting capital inflows. There was also market talk of large lenders selling foreign currency in the domestic FX market to support the yuan. USD/CNY currently trades near 7.1775 compared to a close near 7.223 yesterday.

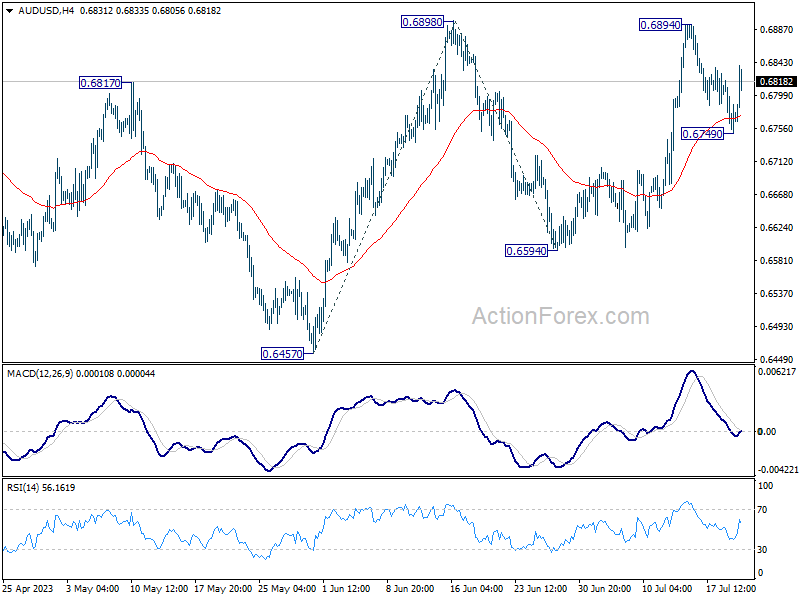

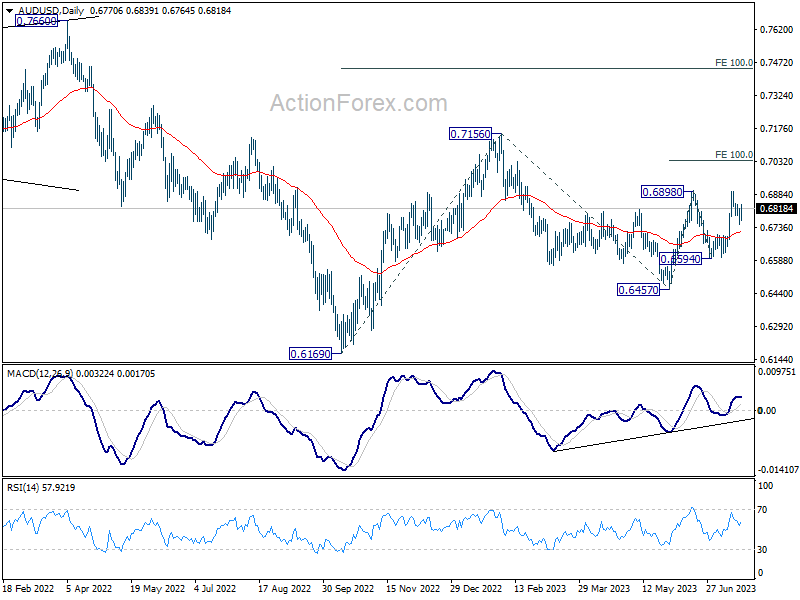

AUD/USD Daily Report

Daily Pivots: (S1) 0.6741; (P) 0.6780; (R1) 0.6811; More...

AUD/USD rebounds notably after drawing support from 55 4H EMA, but stays below 0.6894/8 resistance zone. Intraday bias remains neutral for the moment. On the upside, decisive break of 0.6898 resistance will firstly confirm resumption of rise from 0.6457. Secondly, that should also confirm completion of the fall from 0.7156 at 0.6457. Next target will be 100% projection of 0.6457 to 0.6898 from 0.6594 at 0.7035, and then 0.7156 resistance.

In the bigger picture, price actions from 0.7156 are seen as a correction to the rebound from 0.6169 (2022 low). Break of 0.6898 resistance will argue that rise from 0.6169 is ready to resume through 0.7156. Next target will be 100% projection of 0.6169 to 0.7156 from 0.6457 at 0.7444. For now, this will be the favored case as long as 55 D EMA (now at 0.6703) holds.

Australian Dollar Rebounds Notably on Employment Data, Resurgence in Copper and Yuan

Australian Dollar is making a notable rebound today, largely supported by strong employment data, rebound in Copper price, and a resurgence in Chinese Yuan. In tandem, New Zealand Dollar is closely trailing the second strongest performer. British Pound languishes as the worst performer, still feeling the drag from yesterday's lower-than-expected UK CPI Data. Dollar and Japanese Yen are also experiencing weakness, seemingly reacting to the extended rally in US stock markets overnight. Euro and Canadian Dollar display mixed performance at the moment.

In an interesting development, People's Bank of China announced an increase in a parameter on cross-border corporate financing under its macro-prudential assessments. This strategic move is aimed at enhancing cross-border financing and continuing to expand the sources of cross-border funds for businesses and financial institutions. Analysts interpret this step as a clear intention to maintain RMB above 7.2 handle.

USD/CNH pull backed sharply from 7.2360 today. But overall technically outlook is unchanged. Price actions from 7.2853 are seen as a corrective pattern for now. Strong support from 55 D EMA (now at 7.132) maintains near term bullishness. As long as 7.1036 cluster support holds (38.2% retracement of 6.810 to 7.2853 at 7.1037), another rise is still in favor through 7.2853 to 7.3745. If realized, resumed selloff in CNH would exert some pressure on Aussie again.

In Asia, Nikkei closed down -1.23%. Hong Kong HSI is down-0.06%. China Shanghai SSE is down -0.84%. Singapore Strait Times is up 0.02%. Japan 10-year JGB yield is down -0.0009 at 0.466. Overnight, DOW rose 0.31%. S&P 500 rose 0.24%. NASDAQ rose 0.03%. 10-year yield dropped -0.0047 to 3.742.

BoE Ramsden: CPI inflation remains much too high

BoE Deputy Governor Dave Ramsden said yesterday, "CPI inflation has begun to fall significantly but remains much too high. The Monetary Policy Committee has consistently stressed that monetary policy decisions will address the risk of more persistent strength in domestic wage and price settling."

He went on to warn, "If there is evidence of more persistent pressures, then further tightening in monetary policy would be required."

Ramsden also mentioned BoE's efforts in reducing its holdings of gilts and corporate bonds, which he expects to decrease by a total of GBP 100B by October. However, he pointed out that the central bank has almost completely run off its portfolio of corporate debt, possibly paving way for it to sell more government bonds.

In light of these factors, Ramsden stated, "These factors support a carefully considered increase in the pace of reduction in the stock of gilts in the 12 months ahead." However, he also stressed caution, noting, "I emphasize careful — like the MPC, I want Quantitative Tightening (QT) to set a gradual and predictable pace for unwind and to let it operate in the background, after all."

Japan's export to US up 11.7% yoy in Jun, to EU up 15%, to China down -11%

Japan's exports rose by 1.5% yoy to JPY 8744B in June. The significant rise in exports to US by 11.7% yoy and to EU by 15.0% yoy was offset by the -11.0% yoy decline in exports to China (marking the most significant drop since January).

Rise in US-bound exports was primarily driven by shipments of cars and mining machinery. Meanwhile, dip in exports to China was attributed the decreased shipments of steel, chips, and nonferrous metal, which led to an overall double-digit decline.

Japan's imports contracted by -12.9% yoy to JPY 8701B. The decrease in value of imports is primarily linked to drop in crude, coal, and liquefied natural gas.

As a result, Japan recorded a trade surplus of JPY 43B, the first such instance in nearly two years since July 2021.

In seasonally adjusted term, exports rose 3.3% mom to JPY 8269B. Imports rose 0.5% mom to JPY 8822B. Trade balance reported JPY -553B deficit, versus expectation of JPY -550B.

Australia employment grew 32.6k, but demand met by people working more hours

Australian's June employment data showed persistent tightness in the job markets. The 32.6k growth in employment significantly surpassed expectations of 15.0k. Employment-population ratio remained at record high. Monthly hours worked outpaced employment growth, suggesting that labor demand was met by people working more hours.

Among the 32.6k job growth, rise of 39.3k full-time employment was offset by a decrease of -6.7k in part-time roles. Unemployment rate remained steady at 3.5%, below expectation of 3.6%. Participation rate dipped slightly from 66.9% to 66.8%. Monthly hours worked rose 0.3% mom, faster than growth in employment at 0.2% mom.

Bjorn Jarvis, ABS head of labour statistics, stated: "The rise in employment in June saw the employment-to-population ratio remain at a record high 64.5 per cent, reflecting a tight labour market in which employment has recently increased in line with population growth."

He further emphasized that the current labour market is stronger than it was prior to the pandemic. Jarvis elaborated, "In addition to there being over a million more employed people than before the pandemic, a much higher share of the population is employed. In June 2023, 64.5 per cent of people 15 years or older were employed, an increase of 2.1 percentage points since March 2020."

Jarvis also highlighted the ongoing demand for labour, saying: "The strength in hours worked since late 2022, relative to employment growth, shows the demand for labour is continuing to be met, to some extent, by people working more hours."

AUD/USD Daily Report

Daily Pivots: (S1) 0.6741; (P) 0.6780; (R1) 0.6811; More...

AUD/USD rebounds notably after drawing support from 55 4H EMA, but stays below 0.6894/8 resistance zone. Intraday bias remains neutral for the moment. On the upside, decisive break of 0.6898 resistance will firstly confirm resumption of rise from 0.6457. Secondly, that should also confirm completion of the fall from 0.7156 at 0.6457. Next target will be 100% projection of 0.6457 to 0.6898 from 0.6594 at 0.7035, and then 0.7156 resistance.

In the bigger picture, price actions from 0.7156 are seen as a correction to the rebound from 0.6169 (2022 low). Break of 0.6898 resistance will argue that rise from 0.6169 is ready to resume through 0.7156. Next target will be 100% projection of 0.6169 to 0.7156 from 0.6457 at 0.7444. For now, this will be the favored case as long as 55 D EMA (now at 0.6703) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Jun | -0.55T | -0.66T | -0.78T | -0.77T |

| 01:30 | AUD | NAB Business Confidence Q2 | -3 | -4 | ||

| 01:30 | AUD | Employment Change Jun | 32.6K | 15.0K | 75.9K | 76.5K |

| 01:30 | AUD | Unemployment Rate Jun | 3.50% | 3.60% | 3.60% | 3.50% |

| 06:00 | CHF | Trade Balance (CHF) Jun | 4.82B | 4.23B | 5.48B | |

| 06:00 | EUR | Germany PPI M/M Jun | -0.30% | -0.40% | -1.40% | |

| 06:00 | EUR | Germany PPI Y/Y Jun | 0.10% | 0.00% | 1.00% | |

| 08:00 | EUR | Eurozone Current Account (EUR) May | 2.5B | 3.6B | ||

| 12:30 | USD | Initial Jobless Claims (Jul 14) | 245K | 237K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Jul | -15.5 | -13.7 | ||

| 14:00 | USD | Existing Home Sales Jun | 4.27M | 4.30M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jul P | -16 | -16 | ||

| 14:30 | USD | Natural Gas Storage | 45B | 49B |