Sample Category Title

UK Inflation Offers Hope for the Bank of England

It's been a long time coming but inflation in the UK is finally on the decline and in a rare show of good news, it's falling at a faster pace than expected on both the headline and core levels.

We haven't been treated to many reports like this over the last couple of years, and even when we have any enthusiasm has quickly been extinguished. But this feels different. Without wanting to fall victim to the "this time it's different" mantra that often precedes a terrible turn of events, there is something more promising about this shift.

It follows similar declines in the US and the eurozone in recent months, both of which were sharper than expected and at the headline and core level. Unless this is a blip across the board, which is possible, it may be a sign that inflation is on a path to more modest and sustainable levels.

Of course, there's still an awfully long way to go and the central bank is not going to declare victory on the back of one release. But those wild interest rate forecasts of 6.5%+ that we've been seeing may start to be pared back, perhaps quite significantly as it becomes clear that favourable base effects combined with lower energy and food inflation and the impact of past hikes start to have a substantial impact on the data.

The pound has fallen quite heavily on the back of the release which probably reflects those expectations now being pared back. I don't want to get too carried away but peak rate expectations may now be behind us which could make for a more hopeful second half of the year.

I say I don't want to get carried away but then, upon seeing the release, I was immediately reminded of the famous Office US "It's happening!" scene that is so often widely circulated on social media so perhaps I also, in the words of Michael Scott, need to stay calm.

Oil flat but recent developments have been positive

Oil prices are a little flat early in the European session after bouncing back a little on Tuesday. Since breaking above the recent range highs late last week, oil prices have been a little choppy although importantly they have held above that prior range and, in the case of Brent crude, seen support around the previous highs.

That could be viewed as a bullish technical signal, although that will naturally depend on a number of other factors including the economic data and what producers are doing. Both have been favourable for prices recently, helping Brent break back above $80 for the first time in almost three months.

Gold eyeing another move above $2,000?

Gold broke higher again on Tuesday after briefly paring gains late last week and early this. Lower yields and a weaker dollar are continuing to boost its appeal on the back of some more promising inflation data and lower interest rate expectations.

The yellow metal broke above $1,960 yesterday before running into some resistance around $1,980. It's now closing in on $2,000 which is the next major barrier to the upside, a break of which may suggest traders have turned bullish on gold after two months of declines.

Is Bitcoin looking vulnerable after yesterday's break?

Bitcoin is back above $30,000 today but looking vulnerable to another dip below. Broadly speaking, the cryptocurrency has been range-bound over the last month but it has drifted toward the lower end of this and the move below $30,000 yesterday may have made some nervous. If we do see a significant break lower, the next key area of support may be found around $28,000.

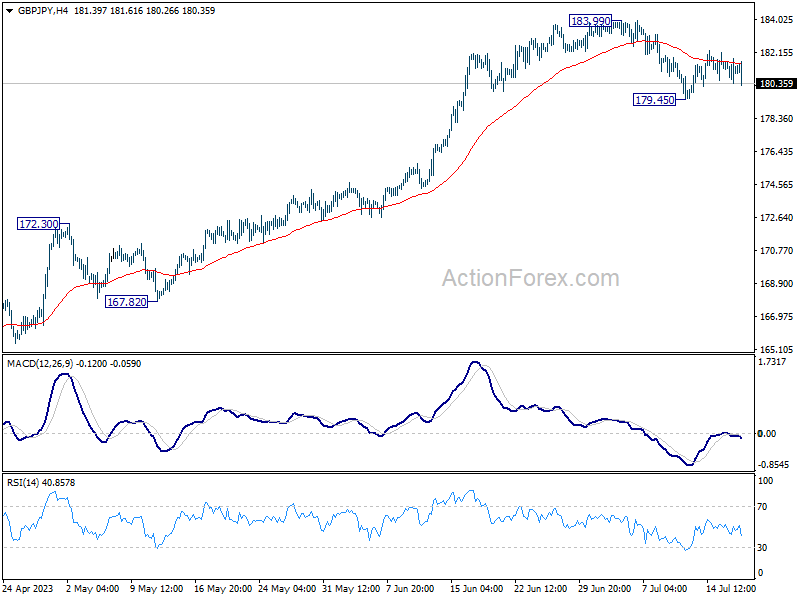

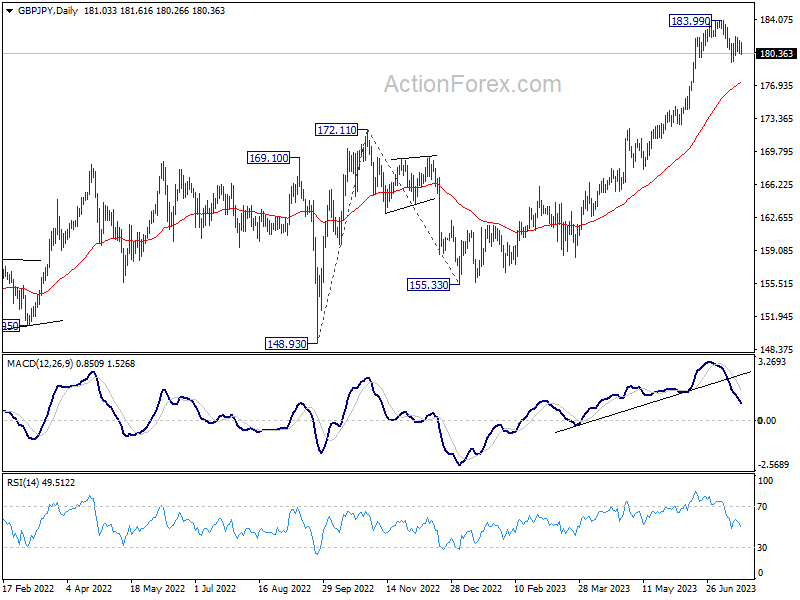

GBP/JPY Daily Outlook

Daily Pivots: (S1) 180.28; (P) 181.07; (R1) 181.76; More...

Intraday bias in GBP/JPY stays neutral first. On the downside, break of 179.45 will resume the correction from 183.90 to 55 D EMA (now at 177.27). On the upside, firm break of 183.99 high will resume larger up trend to 187.36 projection level.

In the bigger picture, as long as 172.11 resistance turned support holds, up trend from 123.94 (2020 low) is expected to continue. On resumption, next target is 138.2% projection of 148.93 to 172.11 from 155.33 at 187.36, and then 195.86 (2015 high). Nevertheless, firm break of 172.11 will argue that larger correction is already underway.

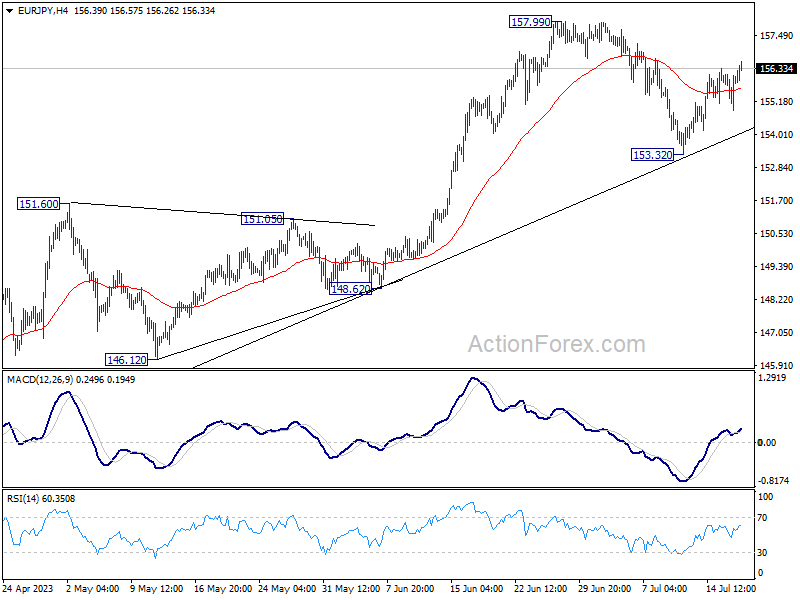

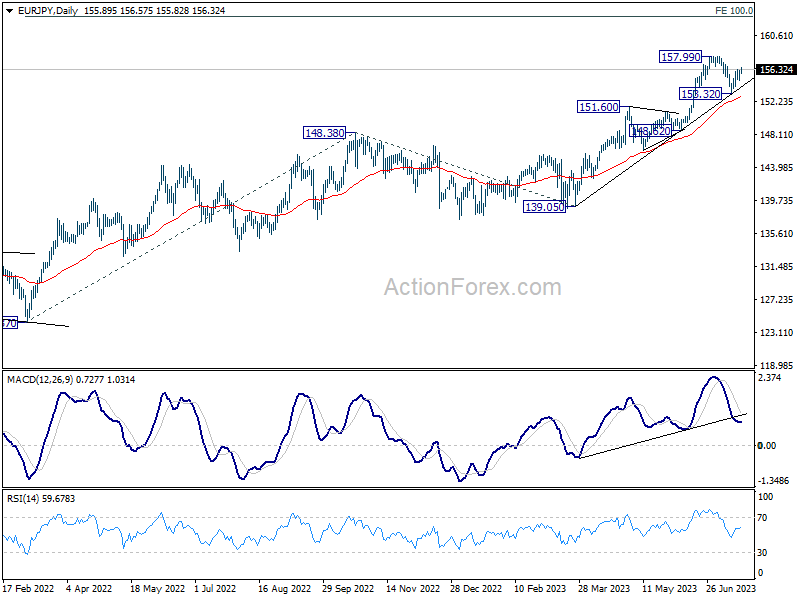

EUR/JPY Daily Outlook

Daily Pivots: (S1) 155.14; (P) 155.64; (R1) 156.41; More....

Intraday bias in EUR/JPY stays mildly on the upside, as rebound from 153.32 is in progress for retesting 157.99 high. Firm break there will resume larger up trend. On the downside, break of 153.32 will extend the pull back from 157.99 to 55 D EMA (now at 152.87) and possibly below.

In the bigger picture, as long as 151.60 resistance turned support holds, rise from 114.42 (2020 low) is in progress. On resumption, next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. Nevertheless, sustained break of 151.60 will argue that larger correction is already underway.

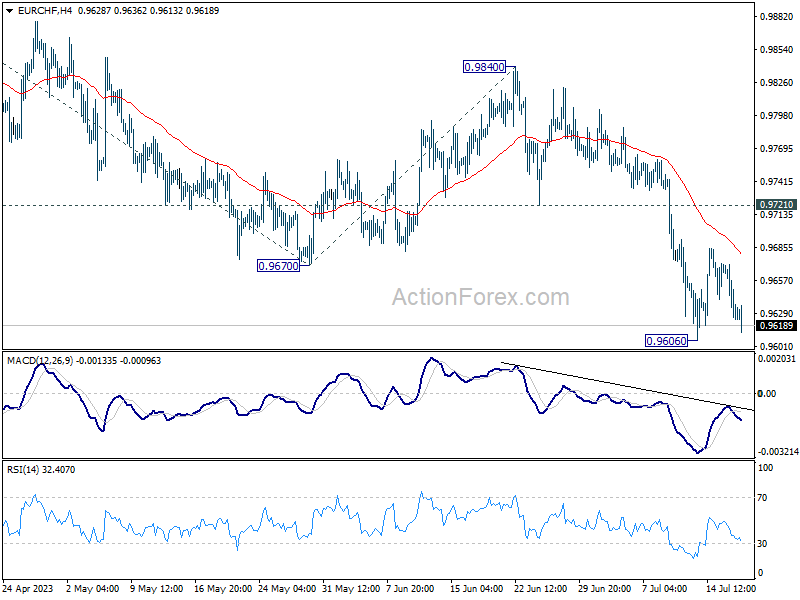

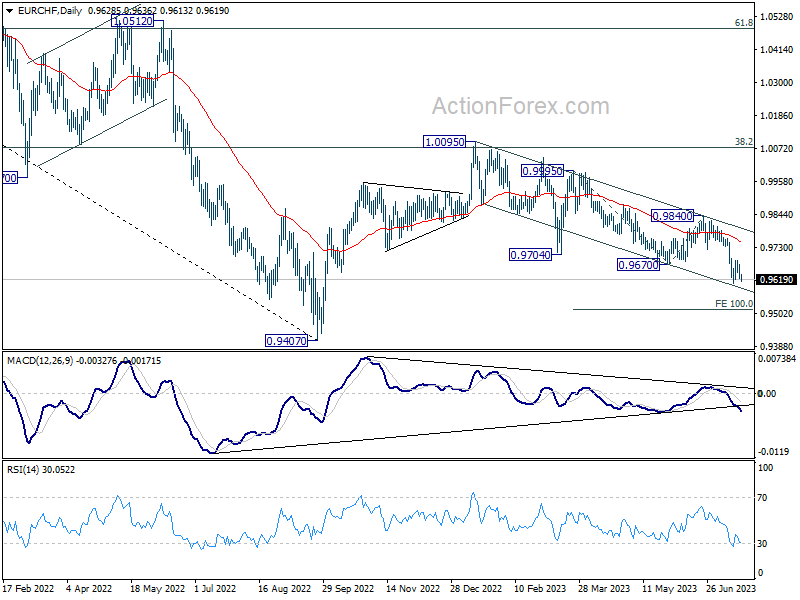

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9612; (P) 0.9643; (R1) 0.9659; More...

Intraday bias in EUR/CHF remains neutral for the moment, and outlook stays bearish with 0.9721 support turned resistance intact. On the downside, break of 0.9606 will resume larger decline from 1.0095 to 100% projection of 0.9995 to 0.9670 from 0.9840 at 0.9515.

In the bigger picture, medium term outlook is staying bearish as the pair is capped below falling 55 W EMA (now at 0.9913). Down trend form 1.2004 (2018 high) is in favor to extend through 0.9407 at a later stage. Nevertheless, decisive break of 38.2% retracement of 1.1149 to 0.9407 will raise the chance of bullish trend reversal.

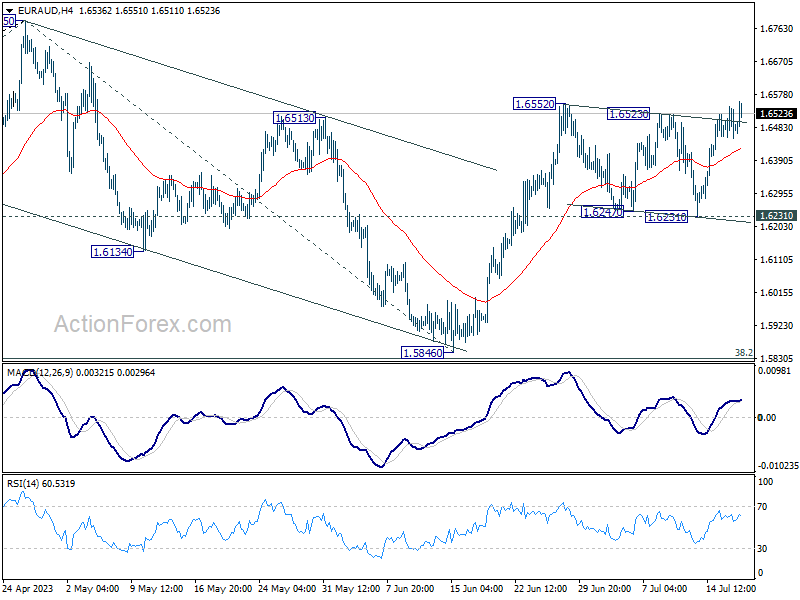

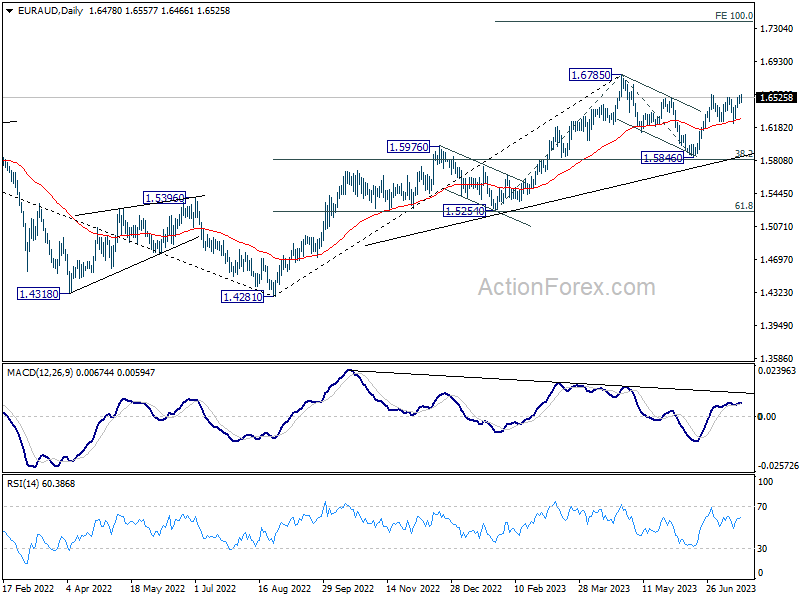

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6438; (P) 1.6491; (R1) 1.6536; More...

Focus stays on 1.6552 resistance in EUR/AUD. As noted before, correction from 1.6785 should have completed with three waves down to 1.5846. On the upside, break of 1.6552 will target a retest on 1.6785 high next. This will remain the favored case as long as 1.6231 support holds, even in case of another dip.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rise resumption. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. On the other hand, rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

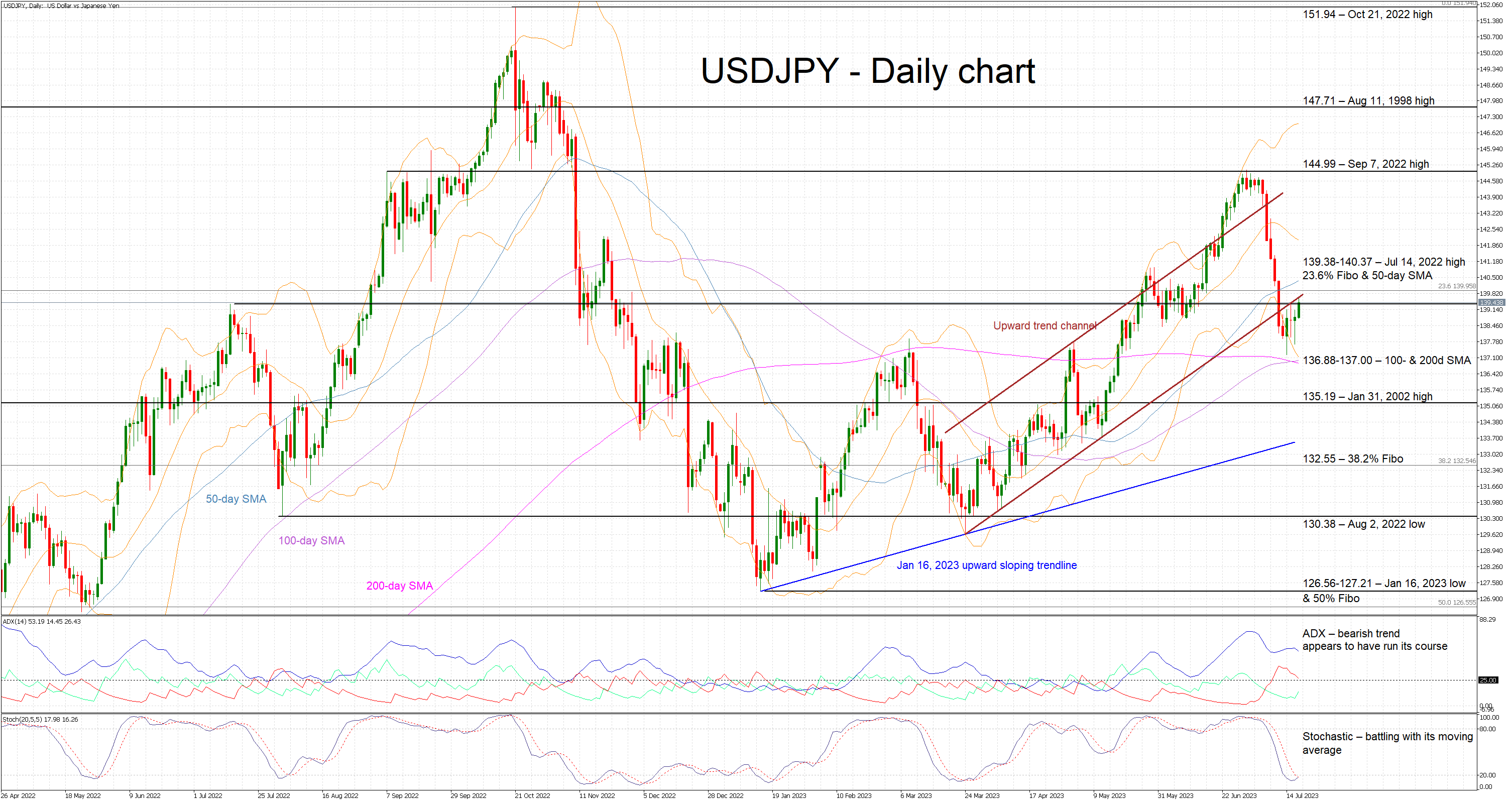

USDJPY Resumes Advance; Prepares to Test a Key Resistance Area

USDJPY is trading higher again today following a significant correction that muted the growing intervention talk. The pair is preparing to enter a very busy area as the bulls are trying to regain market control and take advantage of the continued simple moving averages (SMAs) convergence for their own benefit.

The momentum indicators appear to be mostly on the bulls’ side at this stage. The Average Directional Movement Index (ADX) is edging lower today, confirming a much weakened bearish trend in the market but still remaining at elevated levels compared to its recent history. Crucially, the stochastic oscillator is attempting to break above both its oversold territory and moving average. If successful, a strong bullish signal will be sent.

Having said that, the bulls are ready for another upleg. They would have to clear the resistance set by the lower boundary of the recent upward trend channel and the busy 139.38-140.37 area. This is populated by the July 14, 2022 high, the 23.6% Fibonacci retracement level of the March 9, 2022 - October 21, 2022 uptrend and the 50-day SMA. The path then looks clear until the September 7, 2022 high at 144.99.

On the flip side, the bears are trying to avoid a return to the recent USDJPY highs. They appear willing to defend the 139.37-140.37 range and, if successful, stage a move towards the 136.88-137.00 area that is defined by the 100- and 200-day SMAs. Even lower, the January 31, 2002 high at 135.19 is unlikely to trouble them.

To sum up, the bulls are trying to reassert their dominance, but the stochastic oscillator’s next move will play a key role in the next USDJPY leg.

Softer-than-Expected UK Inflation Sends Cable Below 1.30

The rally in US stocks extended on the back of good bank earnings and AI. BoFA and Morgan Stanley joined the club of big banks beating analyst expectations. BoFA’s fixed income and equity trading posted a surprise gain and covered a slight miss on its net interest income, while Morgan Stanley’s wealth management came to the rescue. Charles Swab on the other hand reported 7% deposit outflows but its shares surged 13%, yes 13% yesterday on expectation of deposit growth by year-end.

Then, Microsoft jumped up to 6% to a fresh all-time-high yesterday as progress on the regulatory front regarding the acquisition of Activision Blizzard, and the news that its Microsoft 365 Copilot, based on OpenAI’s artificial intelligence, will be broadly available and cost $30 per month per user got investors rushing back to the stock and extend the November-to-date rally to 72%! Microsoft’s AI bet has been disruptive this year, and the company is making huge progress in turning the buzz into profit as quickly as possible, and they have a great chance of success. Microsoft’s AI will be a perfect assistant for $30 per month and Microsoft will cash in – and the weak dollar outlook could further help boost revenue.

Zooming out, the bank and AI rally pushed both the S&P500 and Nasdaq 100 to fresh highs since the first months of 2022. Nasdaq 100 is now in the overbought territory, the technical indicators call for correction, and the upcoming modification in the Magnificent Seven’s weightings in the index should pull the valuation down, but the positive trend’s strength remains impressive, and supported by both better-than-expected earnings, and economic data.

On the data front, the softer-than-expected retail sales and production data from the US came to soften the Federal Reserve (Fed) hawks’ hands yesterday, and kept the US yields downbeat, which also helped boost stock valuations in parallel to earnings.

Today, Goldman Sachs will try to beat the expectations that it threw under a bus over the past few weeks, so that the stock price could get away despite a worst quarter in years, Netflix will reveal how well its password sharing ban ramped up subscriptions and Tesla will reveal how much money the company earned by selling a record number of cars at discounted prices to increase market share. There is potential for good surprises for both, but expectations for Netflix and Tesla are strong, so they will certainly be harder to beat than the banks – which had rather soft expectations walking into this earnings season.

Yet Goldman didn’t only dampened expectations regarding its results but also lowered its recession odds from 25% to 20%. A latest survey of economists on Wall Street Journal also revealed that the probability of a downturn fell from 61% to 54% for the US. Weakening recession odds is good news for energy investors, and it keeps demand in oil upbeat. The barrel of US crude is back above the $75pb level this morning despite a smaller decline reported by the API report this week on US inventories compared to what was penciled in by analysts. But we need some good news from China for energy and mining assets to encourage some persistent rotation from AI, because AI just keeps on giving.

In the FX

The US dollar index consolidates at the lowest levels since April 2022, as the oversold market conditions certainly encourage short-term traders to pause and take a breather. Also helping are some dovish comments from European Central Bank’s (ECB) Knot yesterday, who said that monetary tightening beyond next week’s meeting is not guaranteed, while at least two 25bp hikes were seen as almost a done deal by markets until yesterday. Ignazio Visco also hinted that inflation could ease more quickly than the ECB’s latest projections. So the comments sent the German 2-year yield to a 3-week low. The EURUSD bounced lower after hitting 1.1275, and rising dovish voiced from the ECB could keep the EURUSD within the 1.10/1.12 range into the next policy decision.

Across the Channel, inflation numbers freshly came in this morning, revealing that inflation in Britain eased to 7.9% in June versus 8.2% expected by analysts and 8.7% printed a month earlier. Core inflation on the other hand fell below the 7% mark last month. Cable slipped below 1.30 as a kneejerk reaction as softer inflation tempered Bank of England (BoE) hawks. But even with a softer-than-expected figure, inflation in Britain remains high and stickier than in other Western economies, and that keeps odds for further BoE action sensibly more hawkish than for other major central banks. The BoE raised its policy rate to 5% at its latest meeting, and is expected to continue toward 6.5 to 7% range in the next few months. If inflation slows, the peak rate will be pulled to 6-6.5% range, but not lower. And rising rates, that weigh on mortgages in Britain where Brits must renew mortgages every 2-5 years, pressure housing market and fuels the worst living crisis in decades, combined with political shakes into next year’s elections are all factors that could stall the rally in sterling against major peers. Cable benefited from a broad-based weakness in the US dollar since last September dip, but gaining field above the 1.30 mark could prove difficult.

CPI Not Enough for RBNZ to Change Wait-and-See Stance

Markets

Dutch ECB member Knot either delivered the most targeted or the most unlucky comments of the month. The ECB hawk took stage just as the blackout curtain was about to drop. Targeted if his aim was to trigger a last-minute repricing on ECB policy rate expectations. Using his hawkish fame to put a more neutral message out. Low volume trading helped amplify moves. Unlucky is he believed that following the party line “data dependent for September” would go unnoticed on a day where the main countdown was to the TDF’s sole ITT. Either way, core bonds gained ground with Europe outperforming. After July, markets discounted a 2nd 25 bps rate hike by the ECB in September or October ahead of the Knot comments. That’s now pushed forward to December. German yields dropped 8 to 13 bps across the curve with the front end slightly outperforming. The German 10-yr yield tests the incoming trend line, connecting March and June lows. The bigger technical test support comes from the 200d moving average (currently 2.3%) which provided support in March, May and June (2x). US Treasuries shadowed the move in European bonds with some additional volatility around the release of June retail sales. They came in mixed with the headline figure (0.2% M/M) below consensus, but upward provisions to May and a better outcome for the retail control group (core sales) providing counterweight. US Treasuries eventually returned close to opening levels during US dealings. Changes on the US yield curve ranged between +2.5 bps (2-yr) and -3.3 bps (30-yr). EUR/USD for a third session straight closed virtually unchanged at 1.1229, this time following a test of key resistance at 1.1274 though (62% retracement on US rise between 2021 and 2022). The pair is showing signs of (technical) topping off.

USD/JPY this morning extends gains towards 139.50. BoJ governor Ueda tried to frontrun Friday’s inflation numbers by saying that the whole monetary policy stance remains unchanged unless the premise (price goal view & functioning of bond market) shifted. Sterling cedes ground (EUR/GBP 0.8650) after June inflation numbers finally offer some relief (headline 7.9% Y/Y from 8.7% Y/Y; core 6.9% Y/Y from 7.1% Y/Y). We don’t think that it will be sufficient for the BoE to shy away from a second consecutive 50 bps rate hike early August though. Core bond (futures) profit.

News and views

In an appearance before the budgetary committee of parliament, Vice Governor of the Czech National Bank Eva Zamrazilova said that monetary conditions in the Czech Republic are now sufficiently tight. From now on the question for the CNB MPC is when it will be possible to start easing. This is a change of tone with the policy guidance the CNB held until after the June policy meeting when CNB members warned that market speculation on interest rate cuts could be premature. Zamrazilova repeated that the CNB won’t be able to cut interest rates before it is certain that inflation is really safely heading to 2%. According to the CNB analysis, the strong crown made a significant contribution to current tight monetary conditions, but Zamrazilova now indicated that it could weaken approximately one crown from a current reference level of EUR/CZK 23.88. This is a more pronounced depreciation that expected in the May CNB macroeconomic forecast. The CNB holds its next policy meeting on August 3. At that meeting there will also be a new macroeconomic update available.

New Zealand inflation slowed to 1.1% Q/Q and 6% Y/Y in Q2 compared to 1.2% Q/Q and 6.7% in Q1. Consensus expected a more pronounced decline. Especially the monthly dynamics still suggests persistent underlying price pressure. Tradeable inflation rose from 0.7% Q/Q to 0.8% Q/Q. Non-tradeable inflation, seen as a pointer for domestic inflation slowed from 1.7% Q/Q to 1.3% Q/Q (vs 1% Q/Q consensus) resulting in only a marginal decline in the Y/Y measure from 6.8% to 6.6%. In the broader basket, main drivers of quarterly price rises where food, residential construction and rents. The 2y New Zealand government bond yield rose 5.3 bps to 5.24%. Today’s data probably won’t be enough for the RBNZ to openly change its wait-and-see stance after announcing the end of the rate hike cycle in May (5.5%). The kiwi dollar gained temporary after the release but already more than reversed those gains to currently trade near NZD/USD 62.6.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8589; (P) 0.8602; (R1) 0.8627; More...

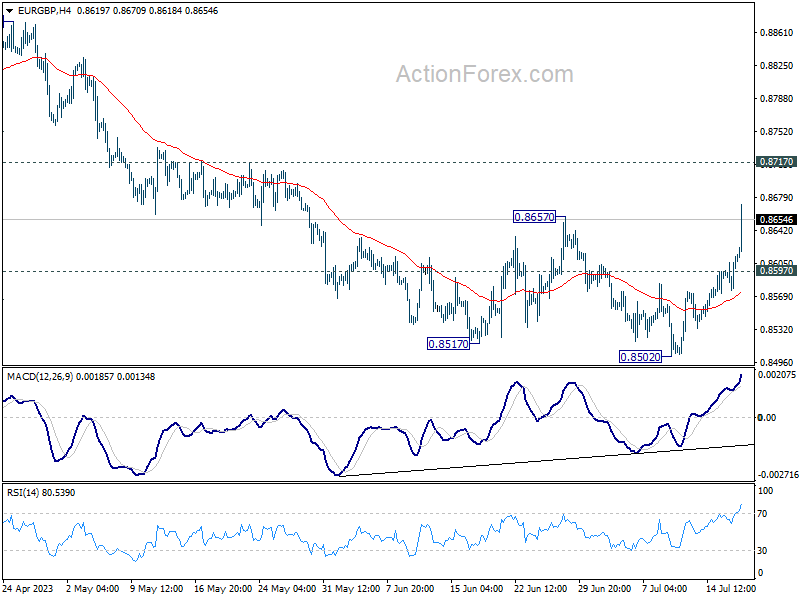

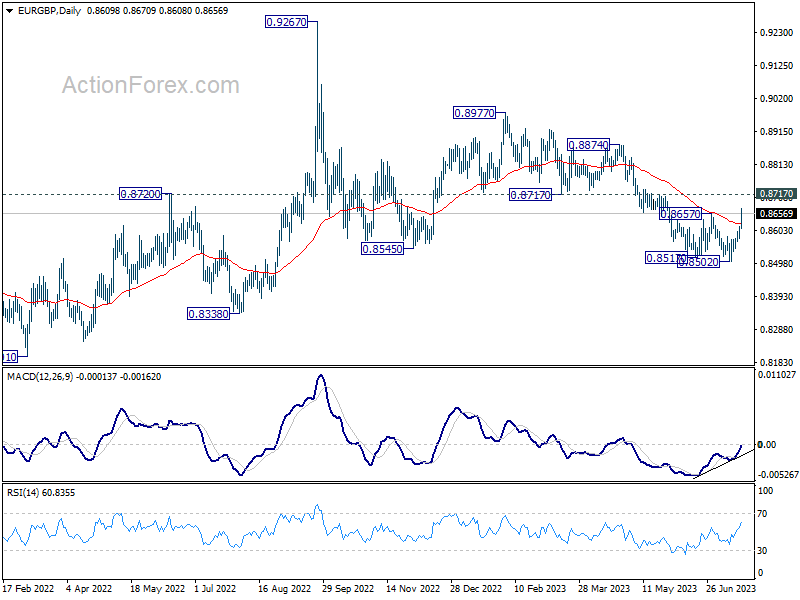

EUR/GBP's strong rally and break of 0.8657 resistance confirms short term bottoming at 0.8502, on bullish convergence condition in 4H and D MACD. Current development argues that fall from 0.8977 might have completed its five-wave sequence. Intraday bias is back on the upside for 0.8717 support turned resistance first. Sustained break there will solidify this case and target 0.8977 resistance next. On the downside, though, below 0.8597 will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest o f0.9267 high. Nevertheless, break of 0.8502 will resume the decline towards 0.8201 (2022 low).

Sterling Takes a Dive as UK Inflation Data Ease Some Pressure on BoE

Sterling falls sharply following the release of June's UK CPI figures which revealed faster than expected slowdown in both headline and core inflation. Despite the persistent high inflation levels, these figures suggest BoE may not need to raise interest rates as aggressively as previously anticipated by some economists, potentially easing some monetary policy pressures. In response to the inflation data, notable decreases were observed in both German and US benchmark yields, potentially giving Yen and Swiss Franc a little favor ahead.

Elsewhere in the current markets, Kiwi and Aussie are following the Pound as next weakest. Japan's Nikkei does follow US markets higher today, but other Asian markets are just sluggish. Canadian Dollar is the relatively stronger one for now, followed by Swiss Franc and Dollar while Euro is mixed.

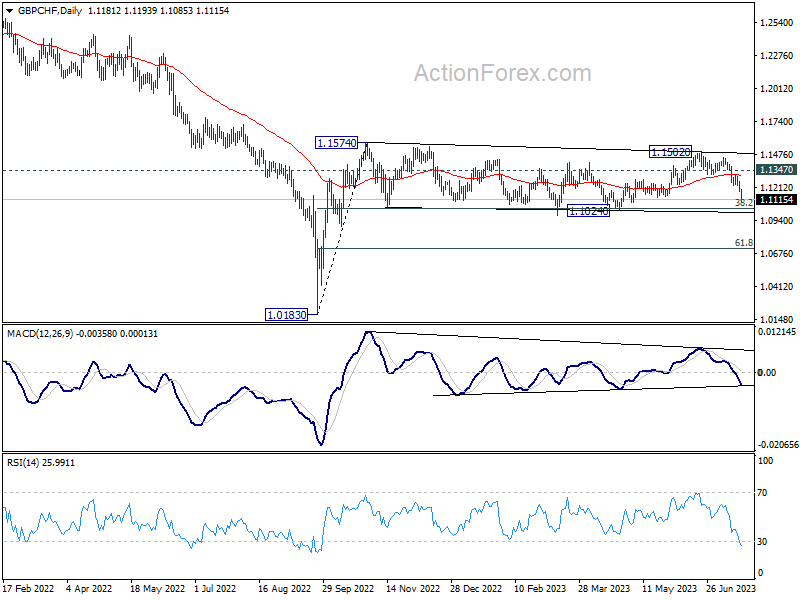

Technically, EUR/GBP's strong rally and break of 0.8657 resistance confirms shot term bottoming at 0.8502. The development also raises the chance of larger bullish reversal.. As GBP/CHF is diving hard today, focus is back on 1.1024 support, which is close to 38.2% retracement of 1.0183 to 1.1574. Strong support could still be seen from there this time. But decisive break there could prompt steeper selloff in GBP/CHF to 61.8% retracement at 1.0174. Weakness in Sterling could then spread from these two crosses to other pairs.

In Asia, Nikkei closed up 1.24%. Hong Kong HSI is down -0.42%. China Shanghai SSE is down -0.01%. Singapore Strait Times is up 0.55%. Japan 10-year JGB yield is down -0.015 at 0.472. Overnight DOW rose 1.06%. S&P 500 rose 0.71%. NASDAQ rose 0.76%. 10-year yield dropped -0.008 to 3.789.

UK CPI eased to 7.9% in Jun, core CPI down to 6.9%, both below expectations

UK CPI slowed from 8.7% yoy to 7.9% yoy in June, below expectation of 8.2% yoy. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 7.1% yoy to 6.9% yoy, below expectation of staying unchanged at 7.1% yoy.

CPI goods slowed from 9.7% yoy to 8.5% yoy. CPI services also eased from 7.4% yoy to 7.2% yoy.

On a monthly basis, CPI rose just 0.1% mom, down from May's 0.7% mom. Falling prices for motor fuel led to the largest downward contribution to the monthly change.

Also released, RPI came in at 0.3% mom, 10.7% yoy, versus expectation of 0.3% mom, 10.9% yoy. PPI input was at -1.3% mom, 2.7% yoy. PPI output was at -0.3% mom, 0.1% yoy. PPI core output was at -0.20% mom, 3.00% yoy.

New Zealand's Q2 CPI beats expectations despite slowdown

New Zealand's CPI experienced a slightly slowed but stronger-than-expected rise in Q2, registering 1.1% qoq increase compared to Q1's 1.2% qoq. This exceeded the anticipated 0.9% qoq rise for the quarter. Year-on-year inflation also surpassed expectations, with 6.0% yoy rise as opposed to expected 5.9% yoy, despite slowdown from 6.7% yoy in the previous quarter.

StatsNZ, New Zealand's pointed out that food prices, which rose 2.2% qoq and 12.3% yoy, were the primary drivers of Q2 annual inflation rate. Rising prices for vegetables, ready-to-eat food, and dairy products like milk, cheese, and eggs played a significant role. Housing and household utilities, another crucial sector, experienced quarterly increase of 1.2% qoq and 6.0% yoy increase annually.

On analyzing the CPI data further, it was found that excluding food, inflation increased by 4.6% yoy. Excluding housing and household utilities, it increased by 6.1% yoy. When excluding alcoholic beverages and tobacco, the annual increase stood at 5.9% yoy. CPI increased by 6.1% yoy when food, household energy, and vehicle fuels were excluded.

Australia leading index records 11th consecutive negative month

Australia's Westpac Leading Index rose to -0.51% in June from -1.01% in May, marking the eleventh consecutive negative print. This trend indicates that the Australian economy is likely to operate below its potential trend over the six to nine months outlook.

In light of these results, Westpac maintains a modest forecast for Australian economic growth. It expects modest expansion of 0.3% over the year to June 2024, with contraction in consumer spending of -0.2%.

Commenting on the upcoming RBA meeting on August 1, Westpac anticipates a 25 bps hike in interest rate. It noted, "By the August meeting we expect that the Board will be dealing with an inflation read still above 6%; an unemployment rate registering nearly 1ppt below the Board's current estimate of full employment; and the recent report from the national accounts showing unit labour costs growing at 7.9% over the year."

Looking ahead

Eurozone will release June CPI final. US will release building permits and housing starts too.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8589; (P) 0.8602; (R1) 0.8627; More...

EUR/GBP's strong rally and break of 0.8657 resistance confirms short term bottoming at 0.8502, on bullish convergence condition in 4H and D MACD. Current development argues that fall from 0.8977 might have completed its five-wave sequence. Intraday bias is back on the upside for 0.8717 support turned resistance first. Sustained break there will solidify this case and target 0.8977 resistance next. On the downside, though, below 0.8597 will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest o f0.9267 high. Nevertheless, break of 0.8502 will resume the decline towards 0.8201 (2022 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q2 | 1.10% | 0.90% | 1.20% | |

| 22:45 | NZD | CPI Y/Y Q2 | 6.00% | 5.90% | 6.70% | |

| 00:30 | AUD | Westpac Leading Index M/M Jun | 0.10% | -0.30% | ||

| 06:00 | GBP | CPI M/M Jun | 0.10% | 0.40% | 0.70% | |

| 06:00 | GBP | CPI Y/Y Jun | 7.90% | 8.20% | 8.70% | |

| 06:00 | GBP | Core CPI Y/Y Jun | 6.90% | 7.10% | 7.10% | |

| 06:00 | GBP | RPI M/M Jun | 0.30% | 0.30% | 0.70% | |

| 06:00 | GBP | RPI Y/Y Jun | 10.70% | 10.90% | 11.30% | |

| 06:00 | GBP | PPI Input M/M Jun | -1.30% | -0.20% | -1.50% | -1.20% |

| 06:00 | GBP | PPI Input Y/Y Jun | -2.70% | -3.30% | 0.50% | |

| 06:00 | GBP | PPI Output M/M Jun | -0.30% | -0.30% | -0.50% | |

| 06:00 | GBP | PPI Output Y/Y Jun | 0.10% | 1.60% | 2.90% | 2.70% |

| 06:00 | GBP | PPI Core Output M/M Jun | -0.20% | -0.20% | -0.30% | -0.50% |

| 06:00 | GBP | PPI Core Output Y/Y Jun | 3.00% | 2.80% | 4.10% | 3.90% |

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | 5.50% | 5.50% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun F | 5.40% | 5.40% | ||

| 12:30 | USD | Building Permits Jun | 1.48M | 1.49M | ||

| 12:30 | USD | Housing Starts Jun | 1.47M | 1.63M | ||

| 14:30 | USD | Crude Oil Inventories | -2.0M | 5.9M |