Sample Category Title

ADP Report Another Huge Blow to Fed Pause Hopes, Jobless Claims in Line

Federal Reserve policymakers may well be dreading tomorrow's jobs report now after today's ADP number once again obliterated estimates, coming in more than double the consensus forecast.

That's almost become the norm on payrolls day but FOMC policymakers, along with investors, may have been hoping the tide would now turn after such as intense tightening cycle over the last 18 months. But if the ADP report is anything to go by, we're headed for another red-hot jobs report.

If a rate hike this month wasn't already nailed on, it probably is now. The ADP isn't often a great precursor to the NFP number but this is a report you simply can't ignore. I'm sure everyone will be revising up their expectations on the back of it and wondering just how much longer this labour market resilience can last. How high must rates go?

Jobless claims crept up again but were just about in line with expectations and still probably lower than what many will have anticipated at this stage. Next up is JOLTS and it will take something seriously shocking to bring balance back to this debate. It's no longer a question of if the Fed hikes this month but how many more after that?

Despite positive momentum, Oil falls short once more

Oil prices are retreating in risk-averse trade today. The ADP report has clearly had a negative impact given it likely means we're facing another red-hot jobs report tomorrow and the prospect of higher rates for longer.

It also came at an opportune time, with the price flirting with the peak from two weeks ago, only to turn south having fallen just shy of surpassing it. That means we're seen yet another failed new high or low in recent weeks and the gradual consolidation, roughly between $72-$77 is still in play.

This time it was close and there was good momentum going into the ADP release but it seems the jobs number was just too big. A repeat performance tomorrow could cement that and undo the efforts of the Saudis and Russians earlier this week in seeking to drive the price higher.

Is Gold vulnerable to another big break?

Gold's brief rebound is seemingly over, with the price already struggling around $1,930-$1,940 before ADP delivered a hammer blow to it. The yellow metal is back trading just above $1,900, a level that's now looking very vulnerable ahead of tomorrow's jobs report.

If it manages to hold above in the interim, a hot report could be the straw that breaks the camel's back. Suddenly it will become a question of whether another hike in September is unavoidable against the backdrop of such a hot labour market. These aren't the only figures that matter but they do significantly weaken the case for another pause.

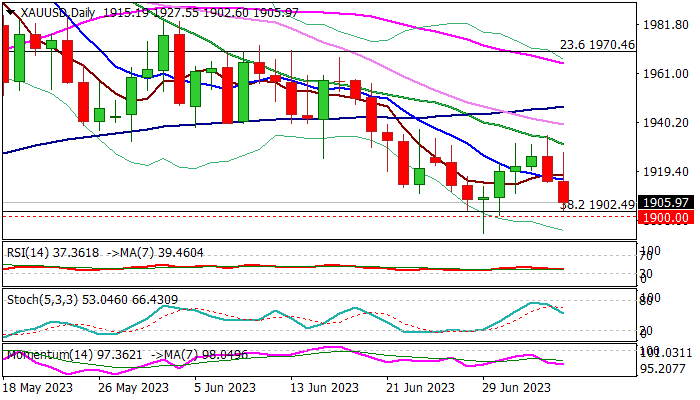

XAU/USD: Gold Falls Sharply on Upbeat US Private Sector Payroll Data

Gold price fell sharply on Thursday, after US ADP private payrolls rose way above expectations in June (497K vs 228K f/c and downwardly revised May figure from 278K to 267K).

Upbeat data point to strong labor market, despite growing fears of recession, due to high borrowing cost and improve the overall sentiment, prompting traders into riskier assets, which lifted the dollar index

The yellow metal was down over $20 immediately after release of US ADP report and cracked the upper boundary of strong support zone between $1902 and $1892 (Fibo 38.2% of $1614/$2080 / psychological / June 29 spike low).

Sustained break through $1900 support zone would generate strong bearish signal for continuation of larger downtrend, paused for a mild correction during the past week and expose targets at $1863/$1847 (200DMA (Fibo 50% of $1614/$2080).

Weak technical picture on daily chart (14-momentum in negative territory / most of MA’s in bearish configuration) add to bearish near-term outlook, though strong headwinds are still to be expected at $1900 zone.

Near-term action needs to stay below 10DMA ($1916) to keep fresh bears in play and guard upper pivots at $1930/34 (falling 20DMA / July 5 top).

Traders will wait for Friday’s release of US non-farm payrolls data for June, to get more details about the condition of US labor market.

Res: 1916; 1930; 1934; 1946.

Sup: 1900; 1892; 1871; 1863.

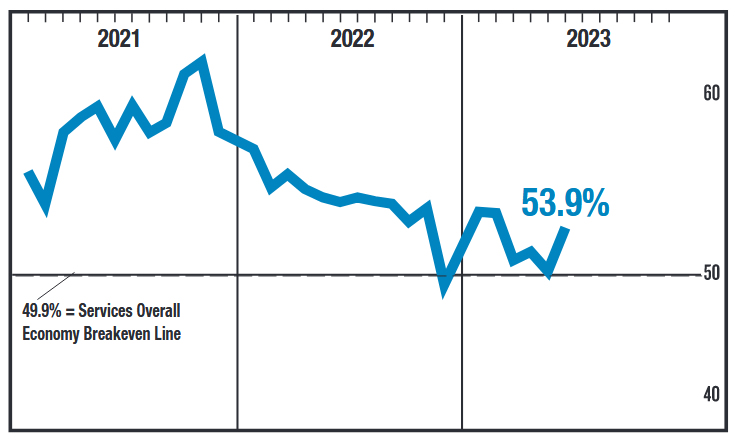

US ISM services rose to 53.9, corresponds to 1.4% annualized GDP growth

US ISM Services PMI rose from 50.3 to 53.9 in June, above expectation of 51.3. Business activity/production jumped from 51.5 to 59.2. New orders rose from 52.9 to 55.5 Employment rose from 49.2 to 53.1. Prices dropped from 56.2 to 54.1.

ISM said, "The past relationship between the Services PMI and the overall economy indicates that the Services PMI for June (53.9 percent) corresponds to a 1.4-percent increase in real gross domestic product (GDP) on an annualized basis."

Sunset Market Commentary

Markets:

Markets took off this morning where they ended yesterday: by selling bonds. The move started as US traders returned from the 4th of July Holiday and accelerated a first time after a technical break of the 10y yield above 3.85/3.87%. FOMC Minutes delivered a second blow by showing more disagreement than expected over the Fed’s skip strategy. Some favoured a 25 bps rate hike, but accepted the status quo. Minutes showed a lot of references to resilient inflation and resilient growth with the influential staff now reducing the odds of a recession later this year to 50/50. Most Fed governors are now in the camp of at least two more rate hikes this year, as Fed Chair Powell also confirmed at a conference at the end of last month. For the umpteenth time this cycle, markets are positioned very dovish confirmed to Fed talk. For the umpteenth time, they have to reposition higher. Interestingly, the long end of the curve is suffering as well with real yields driving the move. Markets come to terms with the (even) higher for (even) longer idea with the theoretical concept of neutral rate (equilibrium rate given price stability and full employment) being rethought. Instead of the long-assumed 2.5% for the US, it is likely going to be higher. Core bonds immediately found themselves on a slippery slope this morning with early US eco releases making it a triple whammy. The US ADP labour market report showed another astonishing amount of net job gains (+497k vs +225k expected) in June while US jobless claims more or less leveled (248k from 239k vs 245k expected) below the psychologic 250k barrier. US yields add 5 bps (30-yr) to 15 bps (2-yr) at the time of writing. The US 2-yr yield broke through 5%, setting a new cycle peak at 5.12% (highest since 2006). The next target stands at 5.26% which is the 2006 high. The US 10-yr yield pushed above 4%, eying the YTD high at 4.09%. UK Gilts and German Bunds joined the sell-off. UK yields rise by more than 10 bps across the curve. The UK 2-yr and 10-yr yields set new cycle highs at respectively 5.5% and 4.66%. German yields increase by 8.1 bps to 12.2 bps with the belly of the curve underperforming the wings. From a technical point of view, the German 10-yr yield finally leaves key resistance at 2.56% behind. The YTD/cycle high stands at 2.77%. Rising real rates are taking their toll on stock markets. Main European benchmarks lose more than 1.5%. In FX space, it’s again very quiet amongst majors. Sterling slightly outperforms both the euro and the dollar. Moves in cable (GBP/USD) and EUR/USD are technically insignificant, but EUR/GBP tested the 0.8518 YTD low. The Japanese yen is stuck between risk-off flows and rising core bond yields. The US non-manufacturing ISM and JOLTS job openings will still be released later today with official payrolls on offer tomorrow.

News & Views:

The UK June Decision Maker Panel survey (DMP) showed that realized output price inflation slowed from 7.6% in May to 6.9% in June. The DMP covers prices from firms across the whole economy, not just consumer-facing firms. The trend decline develops rather slowly (3-month moving average 7.3% from 7.6%). Over the next year, businesses expect output price inflation to ‘fall’ to 4.9%, down from 5.1% May. One-year ahead CPI inflation expectations decreased to 5.7% from 5.9%. However, expectations for three-year ahead CPI inflation increased slightly (by 0.2 ppts) to 3.7%. Current CPI perceptions of firms were close to the 8.7% actual CPI. Annual unit cost growth was unchanged at 9.4% while expected unit cost growth again accelerated from 6.4% to 6.9%. Expected wage growth was also slightly higher at 5.3%. 47% of firms reported that the overall level of uncertainty facing their business was high or very high. Both sales and price uncertainty increased slightly in the monthly series, although the three-month moving averages decreased for both series. Price uncertainty remains at relatively high levels.

The US trade deficit narrowed from $74.5bn to $69bn in May. The decline occurred as imports (0.8% M/M) dropped much faster than exports (-2.3% Y/Y), with the decline mainly driven by consumer goods and industrial supplies. The goods balance deficit improved from $96.2bn to $91,26bn. At the same time the US services balance improved slightly further from $21.58bn to $22,28bn. The petroleum balance eased slightly from $2.98bn to $2.34bn. The US petroleum balance already trades in positive territory since March last year.

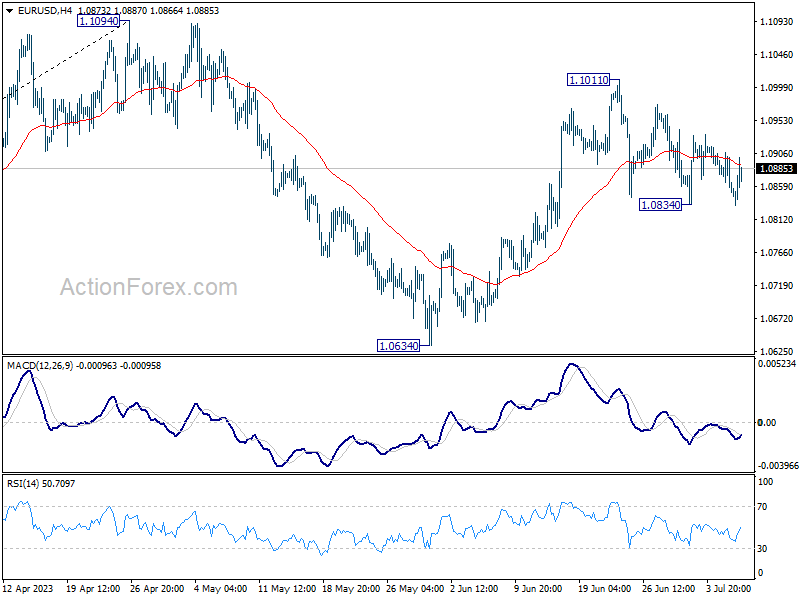

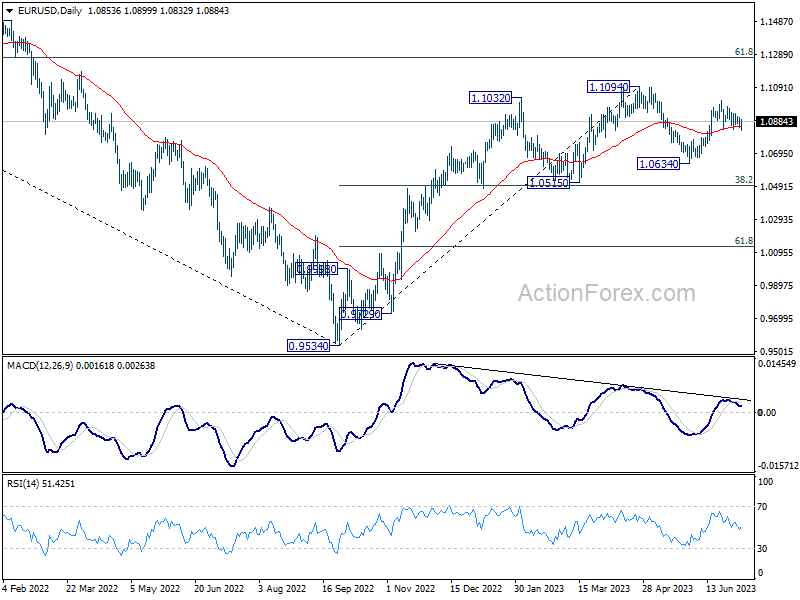

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0834; (P) 1.0871; (R1) 1.0891; More...

Intraday bias in EUR/USD remains neutral as sideway trading is still in progress. On the upside, break of 1.1011 will resume the rise from 1.0634 and target 1.1094 resistance. Decisive break there will resume larger up trend from 0.9534 to 1.1273 fibonacci level. However, firm break of 1.0834 will turn bias to the downside for 1.0634 support instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

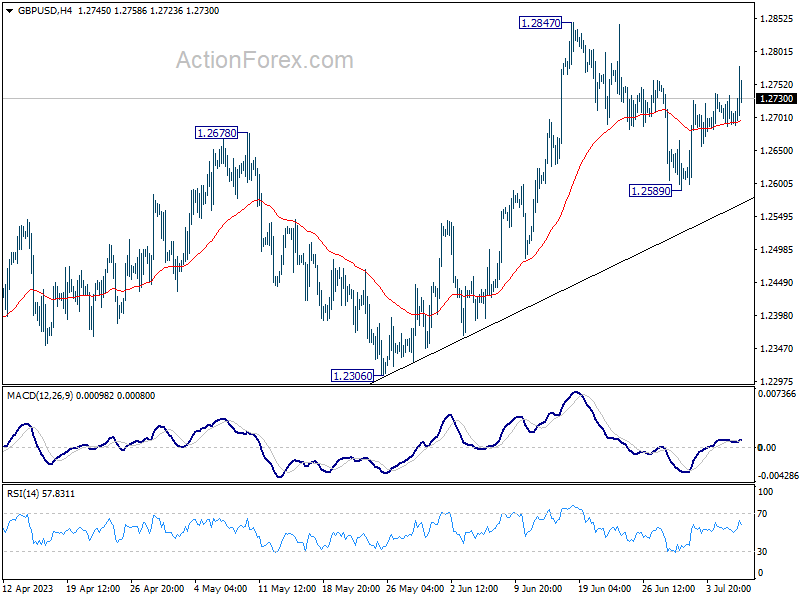

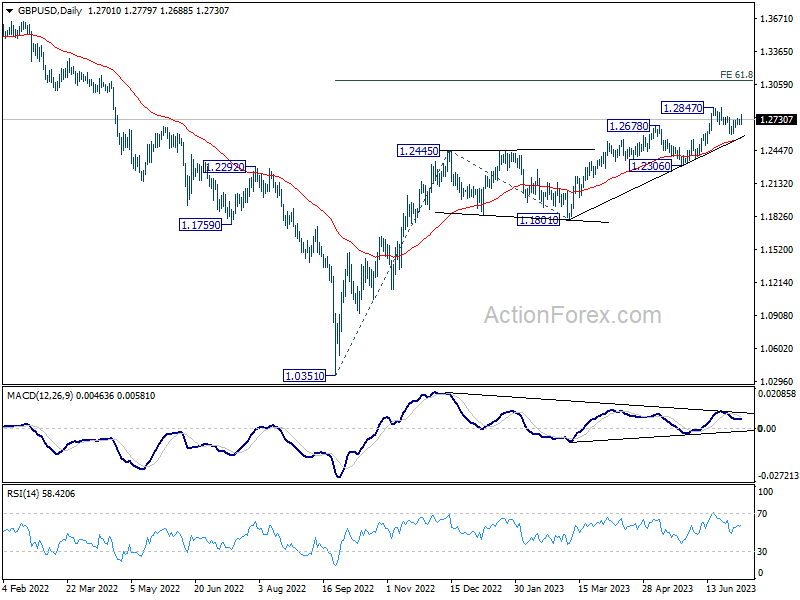

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2683; (P) 1.2709; (R1) 1.2730; More...

Intraday bias in GBP/USD remains neutral even though it's trying to extending the recovery from 1.2589. On the upside, firm break of 1.2847 will resume larger up trend from 1.0351 to 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. On the downside, though, break of 1.2589 will extend the fall from 1.2847 to 55 D EMA (now at 1.2558).

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

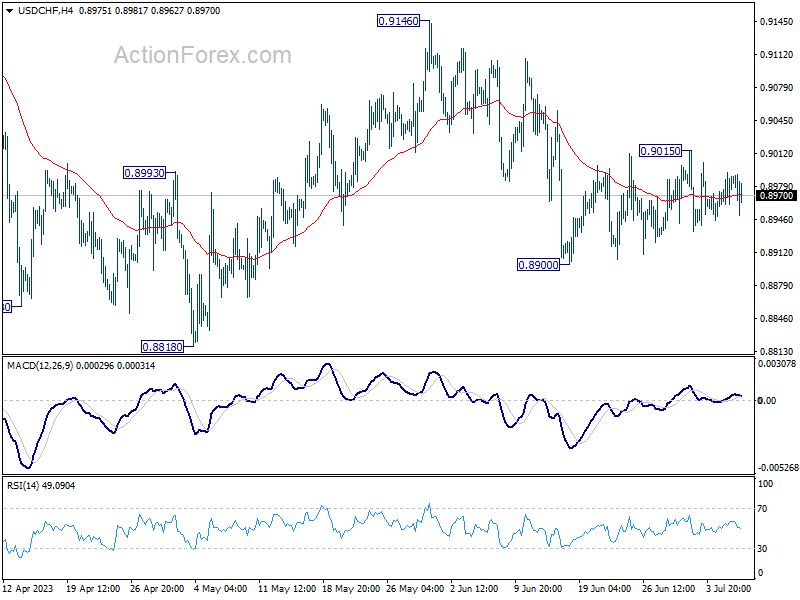

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8968; (P) 0.8982; (R1) 0.9001; More...

USD/CHF is still extending sideway trading and intraday bias remains neutral, while further decline is in favor. On the downside, break of 0.8900 will resume the fall from 0.9146 to 0.8818 low or below. On the upside, above 0.9015 will bring stronger rise towards 0.9146 resistance instead.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). While further decline cannot be ruled out, strong support is expected from 0.8756 long term support to bring reversal. Firm break of 0.9146 resistance should confirm medium term bottoming.

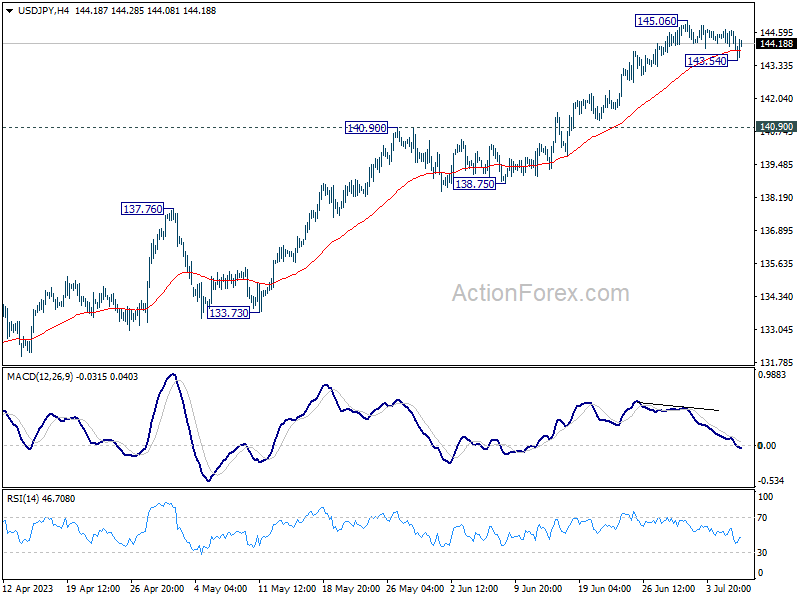

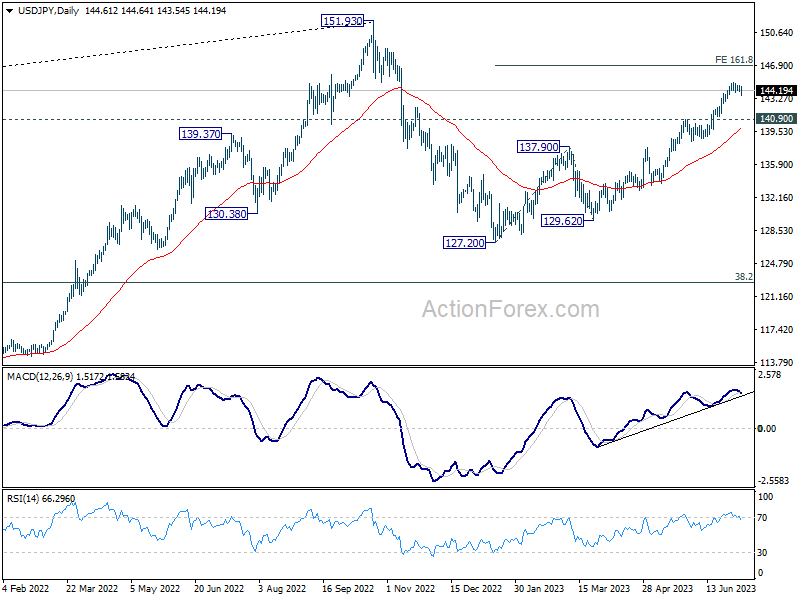

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.26; (P) 144.49; (R1) 144.91; More...

Intraday bias in USD/JPY is turned neutral again as it recovered quickly after dipping to 143.54. Overall outlook remains bullish with 140.90 resistance turned support intact. Break of 145.06 will resume larger rise to 161.8% projection of 127.20 to 137.90 from 129.62 at 146.93. On the downside, break of 143.54 will turn bias to the downside for deeper correction.

In the bigger picture, rise from 127.20 is currently seen as the second leg of the corrective pattern from 151.93 high. Further rally is expected as long as 138.75 support holds, to retest 151.93. But strong resistance could be seen there to limit upside. Break of 138.75 will indicate the the third leg has started back towards 127.20.

Strong ADP Shoots Yield Higher and Hammers Stocks, But Dollar Indecisive

Today's release of US ADP jobs data, showing stellar job growth yet continuing slowdown in wage growth, has left Dollar traders seemingly indecisive. Treasury yields have surged post-release, with 2-year year yield hitting its highest level since 2007 and benchmark 10-year yield breaking 4% threshold. US futures have also seen a tumble, driven by expectations of extended Fed tightening. However, Dollar's rebound against Yen has been mild at best, and the greenback is facing an uphill struggle against Euro and Sterling. This indicates a complex interplay of risk aversion and rising yields on Dollar.

The more consistent development is that Canadian Dollar's extended selloff, and Australian Dollar is also trading lower. On the other hand, Sterling has emerged as the front-runner for the day, supported by continued buying against Euro during European trading session. Euro and Swiss Franc are also on the firmer side. Yen suffers some selloff in early US session and looks vulnerable to further decline ahead.

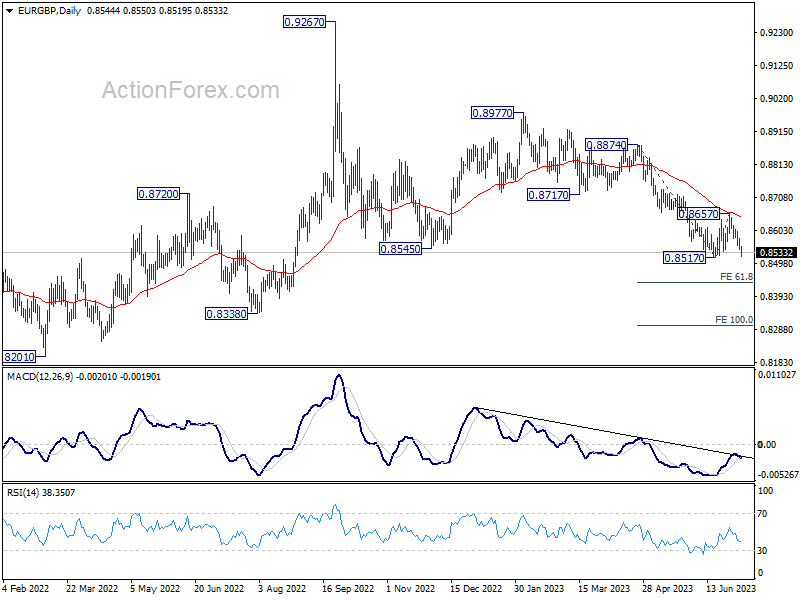

Technically, EUR/GBP looks ready to break through 0.8517 support to resume the decline from 0.8977. In this case, next target will be 61.8% projection of 0.8874 to 0.8517 from 0.8650 at 0.8436. GBP/JPY might take the lead on breaking through 183.99 temporary top. GBP/USD could follow later and breaks through 1.2847 resistance.

In Europe, at the time of writing, FTSE is down -1.69%. DAX is down -1.64%. CAC is down -2.31%. Germany 10-year yield is up 0.1261 at 2.607. Earlier in Asia, Nikkei dropped -1.70%. Hong Kong HSI dropped -3.02%. China Shanghai SSE dropped -0.54%. Singapore Strait Times dropped -1.10%. Japan 10-year JGB yield rose 0.0246 to 0.412.

US ADP surged 497k, but wages growth continues to ebb

US ADP private employment grew 497k in June, well above expectation of 250k. By industry, goods-producing jobs increased 124k while service-providing jobs rose 373k. By establishment size, small companies added 299k jobs, medium companies added 183k, large companies cut -8k.

Annual pay growth of job-stayers slowed from 6.6% yoy to 6.4% yoy. For job-changers, pay gains slowed for the 12th straight month to 11.2% yoy, slowest pace since October 2021.

"Consumer-facing service industries had a strong June, aligning to push job creation higher than expected," said Nela Richardson, chief economist, ADP. "But wage growth continues to ebb in these same industries, and hiring likely is cresting after a late-cycle surge."

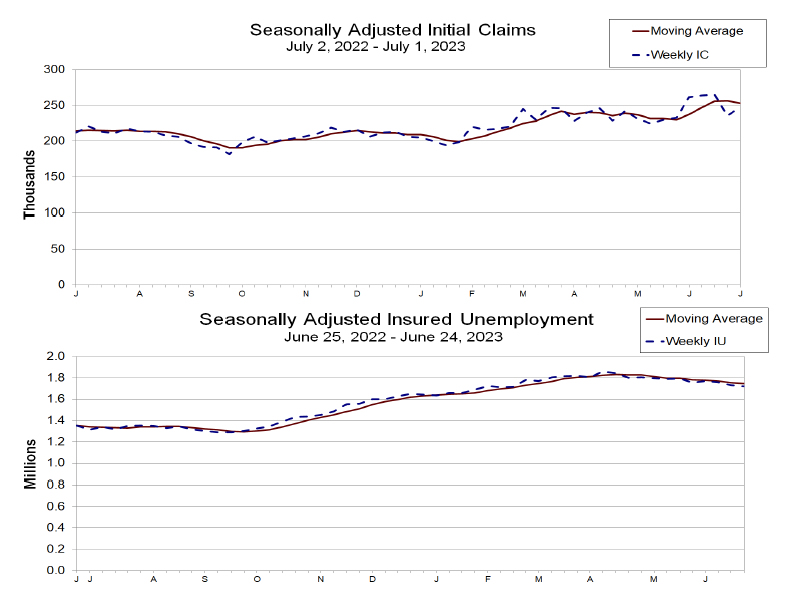

US initial jobless claims rose to 248k, slightly below expectation

US initial jobless claims rose 12k to 248k in the week ending July 1, slightly below expectation of 249k. Four-week moving average of initial claims dropped -3.5k to 253k.

Continuing claims dropped -13k to 1720k in the week ending June 24. Four-week moving average of continuing claims dropped -9k to 1747k.

Eurozone retail sales flat in May, EU down -0.1% mom

Eurozone retail sales volume was unchanged in May, compared with the prior month. Volume of retail trade decreased by -0.5% mom for food, drinks and tobacco and by -0.3% mom for automotive fuels, while it increased by 0.1% mom for non-food products.

EU retail sales fell -0.1% mom. Among Member States for which data are available, the largest monthly decreases in the total retail trade volume were registered in Slovenia (-5.3%), Luxembourg (-4.5%) and Poland (-3.7%). The highest increases were observed in Romania (+3.3%), Portugal (+3.2%) and Sweden (+1.6%).

BoE Bailey can't tell when interest rates start to come down

In an interview with BBC's Newsround, BoE Governor Andrew Bailey retrained from providing a definite timeline for potential decreases in interest rates. Instead, he emphasized the necessity of bringing inflation under control.

"I can't give you a date as to when interest rates start to come down because that really depends upon what happens over the period of time ahead, but getting inflation down is the most important thing that we have to do," Bailey stated.

Offering a glimmer of optimism, Bailey noted a discernible reduction in inflation. He predicted a noticeable fall in inflation rates and affirmed the bank's dedication to lowering it to their target level of 2%.

Inflation "has already started to come down and I expect ... quite a marked fall in inflation, we'll notice it. What we have to do is set the interest rate to get it all the way down to 2%," he expounded.

UK PMI construction fell to 48.9, contracts on rising borrowing costs and weaker housing market

UK's construction sector faced a downturn in June as PMI fell from 51.6 in May to 48.9, falling short of 50.9 expectation. This marks the first contraction in construction activity in five months, driven primarily by the fastest decline in residential work witnessed in over three years.

Tim Moore, Economics Director at S&P Global Market Intelligence, explained the contraction, stating, "Weaker housing market conditions in the wake of higher borrowing costs acted as a major constraint on UK construction output in June." According to him, the steep downturn in residential work since May 2020—excluding the slump during lockdown—has been the most rapid in over 14 years.

On a positive note, input prices decreased for the first time since January 2010, a potential silver lining for the construction sector. Additionally, supplier performance improved at its fastest pace in 14 years, signalling some resilience despite the prevailing industry headwinds. However, recent contraction raises concerns about the health of construction sector amidst rising borrowing costs and a cooling housing market.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.26; (P) 144.49; (R1) 144.91; More...

Intraday bias in USD/JPY is turned neutral again as it recovered quickly after dipping to 143.54. Overall outlook remains bullish with 140.90 resistance turned support intact. Break of 145.06 will resume larger rise to 161.8% projection of 127.20 to 137.90 from 129.62 at 146.93. On the downside, break of 143.54 will turn bias to the downside for deeper correction.

In the bigger picture, rise from 127.20 is currently seen as the second leg of the corrective pattern from 151.93 high. Further rally is expected as long as 138.75 support holds, to retest 151.93. But strong resistance could be seen there to limit upside. Break of 138.75 will indicate the the third leg has started back towards 127.20.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) May | 11.79B | 10.70B | 11.16B | |

| 06:00 | EUR | Germany Factory Orders M/M May | 6.40% | 1.50% | -0.40% | 0.20% |

| 08:30 | GBP | Construction PMI Jun | 48.9 | 50.9 | 51.6 | |

| 09:00 | EUR | Eurozone Retail Sales M/M May | 0.00% | 0.20% | 0.00% | |

| 11:30 | USD | Challenger Job Cuts Jun | 25.20% | 286.70% | ||

| 12:15 | USD | ADP Employment Change Jun | 497K | 250K | 278K | 267K |

| 12:30 | USD | Initial Jobless Claims (Jun 30) | 248K | 249K | 239K | 236K |

| 12:30 | USD | Trade Balance (USD) May | -69.0B | -68.2B | -74.6B | |

| 12:30 | CAD | Trade Balance (CAD) May | -3.4B | 1.5B | 1.9B | 0.9B |

| 13:45 | USD | Services PMI Jun F | 54.1 | 54.1 | ||

| 14:00 | USD | ISM Services PMI Jun | 51.3 | 50.3 | ||

| 14:30 | USD | Crude Oil Inventories | -2.0M | -9.6M |

US initial jobless claims rose to 248k, slightly below expectation

US initial jobless claims rose 12k to 248k in the week ending July 1, slightly below expectation of 249k. Four-week moving average of initial claims dropped -3.5k to 253k.

Continuing claims dropped -13k to 1720k in the week ending June 24. Four-week moving average of continuing claims dropped -9k to 1747k.