Sample Category Title

Sterling Diving While Dollar Rebounds, Aussie Staying Weak

Forex markets today are leaning towards mild risk-off sentiment, with traders cautiously awaiting comments from leading central bankers at the ECB forum. This cautious sentiment, interestingly, does not seem to be having a substantial effect on the stock or bond markets yet.

British Pound is experiencing fresh selling, despite expectations of hawkish messages from the head of BoE. Meanwhile, Australian and New Zealand dollars are faring even worse, as they continue to suffer from the aftermath of disappointing Australian CPI data.

On the other hand, Dollar is showing signs of strength at present. Yen is trying to recovery, but still lacks convincing momentum. Euro and Swiss Franc lag slightly behind the greenback and Yen. Let's see how much the picture would change after the central bankers' speeches.

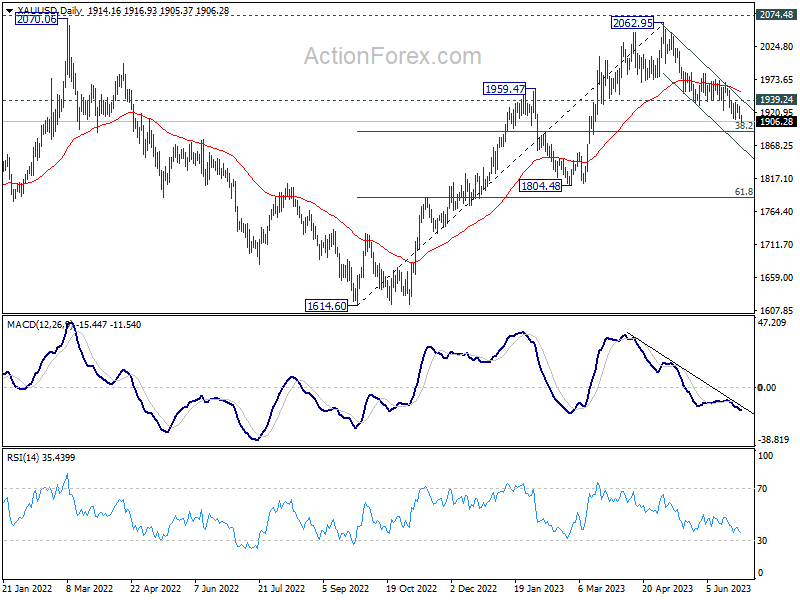

Technically, Gold's fall from 2062.95 is also extending lower today, on the back of Dollar's recovery. Next focus will be on whether there is enough support from 38.2% retracement of 1614.60 to 2062.95 at 1891.68 to bring rebound. Break of 1939.24 minor resistance will be the first sign of bottoming. However, sustained break of 1891.68 would open up deeper fall to 1804.48, and possibly to 61.8% retracement at 1785.86.

In Europe, at the time of writing, FTSE is up 0.71%. DAX is up 0.70%. CAC is up 0.77%. Germany 10-year yield is down -0.035 at 2.325. Earlier in Asia, Nikkei rose 2.02%. Hong Kong HSI rose 0.12%. China Shanghai SSE closed flat. Singapore Strait Times rose 0.06%. Japan 10-year JGB yield rose 0.138 to 0.388.

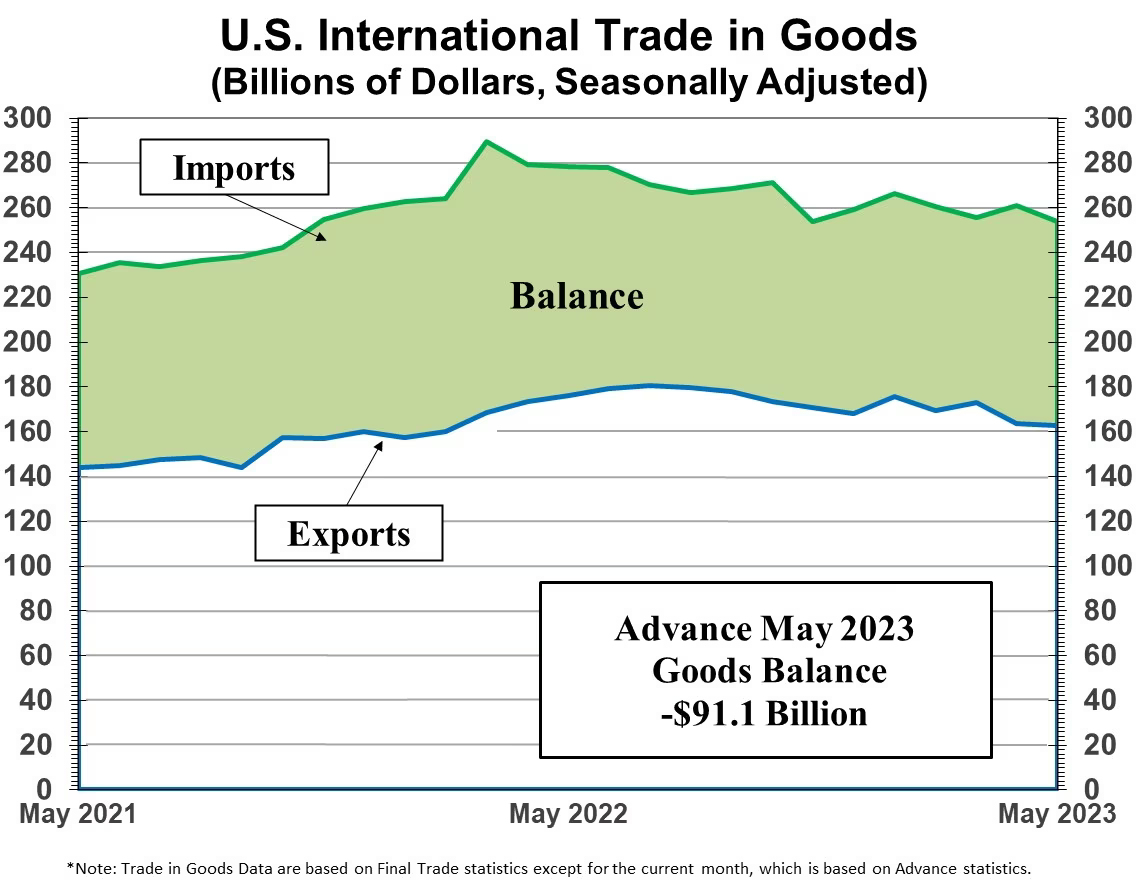

US goods exports down -7.5% yoy in May, imports down -8.8% yoy

US goods exports dropped -7.5% yoy to USD 162.84B in May. Goods imports dropped -8.8% yoy to USD 253.98B. Goods trade deficit came in at USD -91.1B, versus expectation of USD -92.3B.

Wholesale inventories fell -0.1% mom to USD 912.9B. Retail inventories rose 0.8% mom to USD 787.7B.

ECB de Guindos: July a hike fait acommpli, September open

ECB Vice President Luis de Guindos has provided a somber outlook for the Eurozone's economic performance, emphasizing both stubborn inflation pressures and slower economic growth in an interview with Bloomberg TV in Sintra, Portugal.

When discussing the ECB's potential interest rate policy moves, de Guindos indicated that the decision to hike rates in July seems to be a "fait accompli", while the situation for September is "open".

De Guindos voiced his concerns about underlying inflation, which he expects to prove more stubborn than currently anticipated. The Vice President linked these persistent pressures to a potentially strong summer tourist season that could drive services costs higher.

Regarding the economy, "the data that we are receiving about growth are not very good," he confessed, adding that "some of these downside risks have started to materialize and are becoming much more visible."

ECB Vasle: Burden of proof for Sep in non-necessity of more hike

ECB Governing Council member Bostjan Vasle has emphasized the need for further monetary tightening in the face of persistent inflation, speaking on the sidelines of the ECB Forum.

"Given the persistence of inflation, we need to keep tightening monetary policy at our next meeting," Vasle stated.

Beyond July, the decision to further hike rates will be "data-dependent". However, Vasle conveyed that the "burden of proof" lies in data indicating "further rate hike is not needed instead that it is needed."

Vasle dismissed arguments that weaker growth readings might ease the ECB's fight against inflation. He asserted, "All these suggest that growth developments are not significantly different than our most recent projections."

The ECB official also expressed concerns over expectations that corporate profit margins might decline and absorb the impact of wage hikes, terming such a prospect as bearing significant risks.

"The labour market is strong and consumption is resilient. So firms might continue to enjoy pricing power, especially because demand is too strong to push down margins," he said.

Germany Gfk consumer sentiment fell to -25.4, first setback after eight increases

German Gfk Consumer Sentiment for July fell from -24.4 to -25.4, below expectation of 23.0. In June, economic expectations fell from 12.3 to 3.7. Income expectations fell from -8.2 to -10.6. Propensity to buy improved from -16.1 to -14.6.

"The current development in consumer sentiment indicates that consumers are once again more uncertain. This is reflected in the fact that the propensity to save increased again this month," explains Rolf Bürkl, GfK consumer expert.

"After eight consecutive increases, the consumer sentiment must suffer a first setback. Continued high inflation rates, currently at around six percent, are noticeably eroding the purchasing power of households and preventing private consumption from making a positive contribution."

Australia CPI slowed to 5.6% yoy in May, lowest in more than a year

Australia monthly CPI slowed notably from 6.8% yoy to 5.6% yoy in May, below expectation of 6.1% yoy. That's also the lowest reading in more than a year since April 2022. Excluding volatile items and travel, CPI also ticked down from 6.5% yoy to 6.4% yoy.

The most significant contributors to the annual increase in the monthly CPI indicator in May were Housing (+8.4 per cent), Food and non-alcoholic beverages (+7.9 per cent), and Furniture, household equipment and services (+6.0 per cent). Partly offsetting the rise was a fall in Automotive fuel (-8.0 per cent).

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8573; (P) 0.8593; (R1) 0.8618; More...

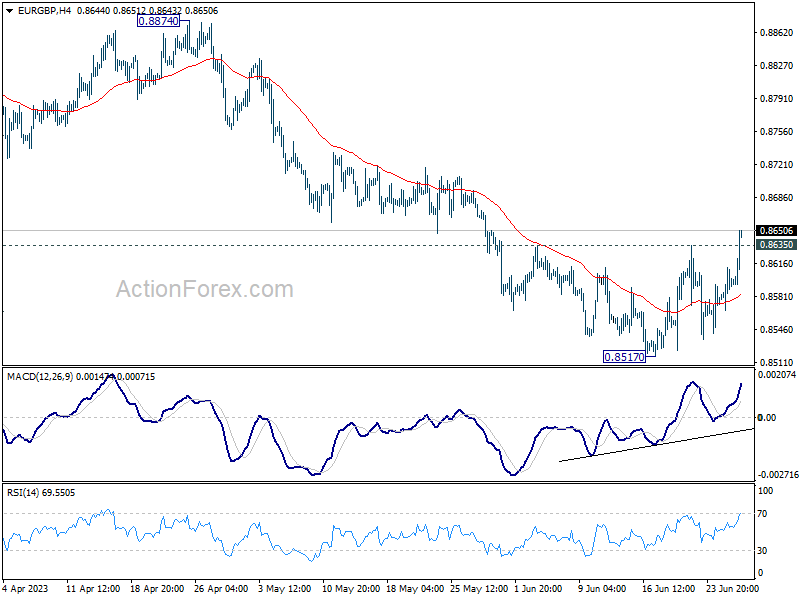

EUR/GBP's break of 0.8635 resistance confirms short term bottoming at 0.8517, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for 55 D EMA (now at 0.8658) and above. For now, as long as 0.8717 support turned resistance holds, fall from 0.8977 could still have another leg through 0.8517 before completion. However, firm break of 0.8717 will turn outlook bullish for 0.8977 resistance next.

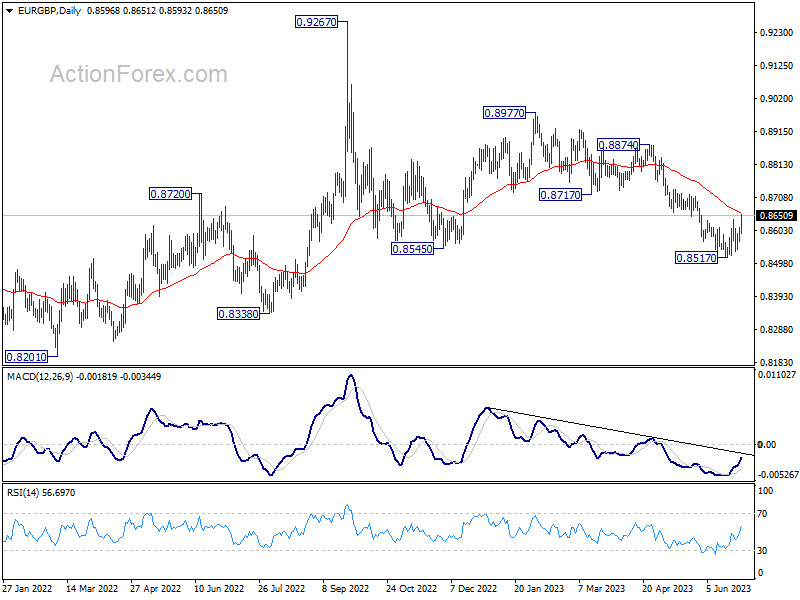

In the bigger picture, the down trend from 0.9267 (2022 high) is still in progress. It's seen as part of the long term range pattern from 0.9499 (2020 high). Deeper fall could be seen towards 0.8201 (2022 low). But strong support should be seen from there to bring reversal. This will now remain the favored case as long as 0.8717 support turned resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y May | 5.60% | 6.10% | 6.80% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Jul | -25.4 | -23 | -24.2 | -24.4 |

| 08:00 | CHF | Credit Suisse Economic Expectations Jun | -30.8 | -32.2 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y May | 1.40% | 1.50% | 1.90% | |

| 12:30 | USD | Goods Trade Balance (USD) May P | -91.1B | -92.3B | -96.8B | |

| 12:30 | USD | Wholesale Inventories May P | -0.10% | 0.10% | -0.10% | |

| 14:30 | USD | Crude Oil Inventories | -1.4M | -3.8M |

US goods exports down -7.5% yoy in May, imports down -8.8% yoy

US goods exports dropped -7.5% yoy to USD 162.84B in May. Goods imports dropped -8.8% yoy to USD 253.98B. Goods trade deficit came in at USD -91.1B, versus expectation of USD -92.3B.

Wholesale inventories fell -0.1% mom to USD 912.9B. Retail inventories rose 0.8% mom to USD 787.7B.

CHFJPY Hits Fresh Record High as Yen Falls Apart

CHFJPY hit its highest levels in at least four decades this week, since official records began. The pair is flying higher and higher into uncharted territory as the relentless uptrend has gone into overdrive. That said, most indicators suggest CHFJPY is increasingly overbought and might be subject to a correction before the rally resumes.

Momentum oscillators such as the RSI have risen to extreme levels on the weekly chart, and there seems to be some divergence forming, as the pair continues to rise but the RSI seems to be flatlining. Similarly, the MACD is at very elevated levels and CHFJPY is also trading near its upper weekly Bollinger band, a testament to how forceful the uptrend has been.

A potential pullback in the price could stall near the 155.50 region, which acted as resistance on the way up and may now serve as support. Even lower, the spotlight would shift to 151.40, an area that capped the rally in late 2022.

Now in case the pair simply continues moving higher into unmapped waters, the focus would turn to round psychological numbers that might halt the advance, at least temporarily. Specifically, the 170.00 level would attract some attention. If that’s violated too, the rally could stretch towards 174.00, which is the 261.8% Fibonacci extension of the late 2022 - early 2023 correction.

In short, CHFJPY is in a clear and powerful uptrend, although momentum indicators warn that the rally is a little stretched at this stage.

All Eyes on ECB Forum as Central Bank Heads Join Panel Discussion

Equity markets are cautiously higher in Europe while the US is poised to open relatively flat as we await appearances from the heads of the Fed, ECB, BoE and BoJ.

Fed Chair Jerome Powell, ECB President Christine Lagarde, BoE Governor Andrew Bailey, and BoJ Governor Kazuo Ueda are due to take part in a panel discussion at the ECB Forum on Central Banking around the opening bell in the US and their comments could set the tone for the rest of the day.

Often in these situations, policymakers will stick to the script, preferring to leave big announcements for meetings and certain high-profile events. But with so many heads appearing at the same time, there's every chance at least one says something that will either rattle or stimulate the markets.

To make this event more intrguing, they're all contending with very similar issues and yet their individual situations are quite different, which could make the discussion all the more interesting.

The Fed is arguably closest to the end of its tightening cycle and will probably be the first to cut rates, the ECB appears to be making some progress but is also more pessimistic than many on how much more is needed, the BoE is in a mess, frankly, and the BoJ may simply watch as the whole thing passes it by.

It really is quite fascinating and it will be interesting to hear what each has to say about the current environment. Especially with the Fed and ECB until now adopting a more hawkish stance than most, the BoE coming across less hawkish but recently being forced to pivot back to larger hikes, and the BoJ pushing back against any hawkish expectation in the markets.

Oil prices hold in recent range

Oil prices are edging higher again today after once again sliding back toward the range lows of the last few months. What's interesting is that, as we've seen previously, Brent crude failed to reach the previous low. It's now the fourth time that's happened in recent months and suggests we are potentially in a prolonged period of consolidation, with little sign yet of further downside momentum building.

That may of course change as the environment changes, which can happen quite rapidly these days, but for now it looks stuck in that lower range between $70-$80, perhaps even $72-$77.

Can Gold hold above $1,900

Gold is slipping again this week after initially breaking below its recent range just over a week ago. It's now falling to a new three-month low and appears to be closing in on $1,900 which could represent the next big test of support for the yellow metal.

Appetite for gold has dwindled as investors have increasingly come around to the reality that not only could more rate hikes be in the pipeline, but rate cuts this year are now highly unlikely. Inflation is proving even more stubborn than expected on the way down and that's bad news for gold.

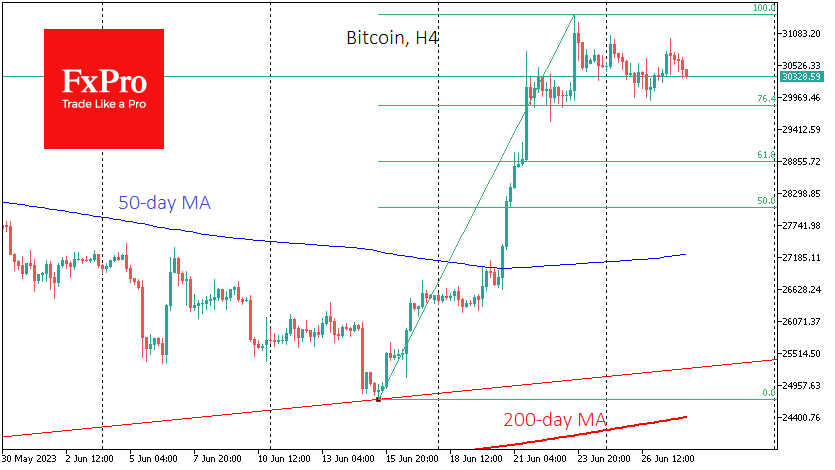

Is Bitcoin going to take off from here?

Bitcoin has steadied between $30,000 and $31,000 in recent days after surging on the back of encouraging ETF filings. The SEC lawsuits against Binance and Coinbase have not been forgotten but they've certainly drifted into the background and been overtaken by far more promising news flow.

It would appear the cryptocurrency has good momentum once more and the community may well be wondering if this could be the kind of development that sees enthusiasm for cryptos surge again. It's obviously been a fantastic year for bitcoin so far but the sell-off since mid-April was another reminder that it doesn't come without major setbacks.

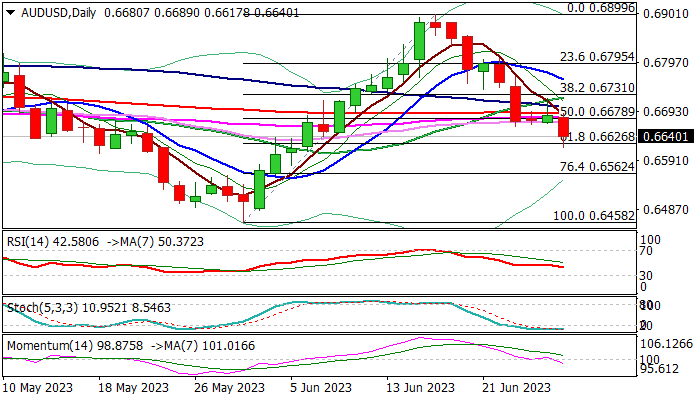

AUD/USD: Aussie Dollar Falls Further on Australian May CPI Well Below Expectations

Australian dollar accelerated lower and hit three-week low in early Wednesday’s trading, signaling continuation of larger downtrend which paused in past two days.

Strong decrease in Australian inflation (May 5.6% vs 6.1% f/c; Apr 6.8%) reduces possibilities for another rate hike in the policy meeting next week, making the Aussie dollar less attractive for investors.

Fresh weakness confirmed bearish signal on break of 200DMA and cracked next pivotal supports at 0.6626 (Fibo 61.8% of 0.6458/0.6899 / weekly cloud base), though bears may slow the pace as daily studies are oversold.

Consolidation should stay capped under 200DMA (0.6690) to keep bears intact for final break of 0.6626 pivots and bearish continuation towards 0.6562 (Fibo 76.4%) and 0.6500 (round-figure) in extension.

Res: 0.6678; 0.6690; 0.6705; 0.6731.

Sup: 0.6626; 0.6600; 0.6562; 0.6500.

AUD/JPY Technical: Minor Downtrend Remains Intact

- Recent two weeks of price actions in AUD/JPY have evolved into a minor downtrend.

- Key resistance on the minor downtrend stands at 96.00.

- Near-term supports are at 94.80 and 94.00.

This is a follow-up on our earlier analysis, “AUD/JPY Technical: At the risk of a minor pull-back” dated 19 June 2023.

The AUD/JPY has dropped as expected and almost hit the 94.80 support (printed a current intraday low of 95.15 in today’s Asia session).

Today’s fall in the AUD/JPY has been reinforced by a softer Australia’s monthly CPI data for May, which slowed down to an annualized rate of 5.6% from 6.8% in April and came in below expectations of 6.1%.

The slowdown in monthly inflation growth in Australia has tempered the expectations of another rate hike by the RBA in the upcoming monetary policy decision meeting held next week, 4th July.

As of 28 June, the ASX 30-day interbank cash rate futures has priced in a chance of 16% of a 25 basis points (bps) hike on the cash rate to 4.35%, down from a 23% chance priced yesterday, 27 June.

Evolving in a short-term descending channel

Fig 1: AUD/JPY minor short-term trend as of 28 Jun 2023 (Source: TradingView, click to enlarge chart)

The price actions of AUD/JPY have continued to evolve in a short-term descending channel in place since its 19 June 2023 high of 97.67 which indicates that its minor downtrend phase remains intact.

The key short-term pivotal resistance stands at 96.00 which is defined by the upper boundary of the short-term descending channel and the former minor swing low of 27 June 2023.

No clear signs of bearish exhaustion

The hourly RSI has remained below a corresponding pull-back resistance at the 44 level and has not displayed any bullish divergence signal at its oversold region.

A break below 94.80 (also the 20-day moving average) exposes the next support at 94.00 (psychological level & the 50% Fibonacci retracement of the minor up move from 1 June 2023 low to 19 June 2023 high).

On the other hand, a clearance above 96.00 negates the bearish tone to see the next resistance coming in at 96.80.

Aussie Slides to 3-Week Low as CPI Falls Sharply

- Australian inflation declines more than expected

- AUD/USD slides in response to the inflation report

- US Consumer Confidence jumps

The Australian dollar is sharply lower on Wednesday. In the European session, AUD/USD is trading at 0.6636, down 0.75%. Earlier, the Australian dollar touched a low of 0.6618, its lowest level since June 7th.

Australian CPI falls to 5.6%

Australia’s inflation was expected to fall in May, but the decline was sharper than expected. Headline CPI tumbled to 5.6% y/y in May, down from 6.8% and below the consensus of 6.1%. Inflation has now dropped to its lowest level in 13 months. Core inflation also fell, as Trimmed Mean CPI declined to 6.1% y/y, down from 6.7%, the lowest level in seven months.

The inflation release sent the Australian dollar sharply lower, as the markets have priced in a higher chance of a pause at the July meeting, at around 70%. The inflation report was a gift-wrapped present for the Reserve Bank of Australia, which surprised the markets with a rate hike earlier this month.

The meeting minutes indicated that the decision was a close call between a hike and a pause, with high inflation being a key factor in the decision to raise rates. With core inflation falling sharply, the RBA may have the excuse it needs to take a pause and provide some relief to consumers and businesses who are groaning under the weight of high rates.

In the US, there were further signs of a strong economy. Durable Goods Orders and New Home Sales were higher and beat expectations, and Conference Board Consumer Confidence jumped in June from 102.5 to 109.7, its highest level since January 2022. These strong releases will provide support for the hawkish Fed, which has signalled that it plans to raise rates twice more in the coming months.

AUD/USD Technical

- There is resistance at 0.6729 and 0.6822

- 0.6593 and 0.6518 are providing support

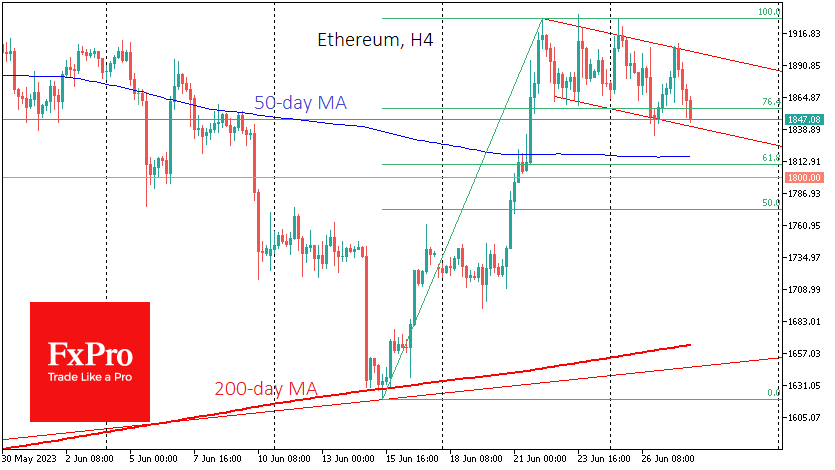

Ethereum’s Downward Bias

Market picture

Cryptocurrency market capitalisation fell 0.2% over the past 24 hours, losing ground since the start of the day on Wednesday but remaining within the range of $1.16-1.20 trillion since last Thursday. The market remains in a “Greed” mood, according to the Fear and Greed Index.

Bitcoin has been squeezed in the $30.0-30.8K range, above a similar consolidation in April, and has settled into an overall uptrend. The shorter-term picture, however, suggests potential correction exists, with short-term targets in the $29.8K area (76.4% of the rally since mid-June), but a pullback to $28.9K (61.8%) is more likely. This should not put the bullish trend in question but will fuel further buying.

Ethereum is trading in a corridor with a slight bearish bias, correcting 4% from its 22 June high to $1860. The development of a corrective pullback here sets the stage for a decline to the $1800-1810 area. A critical round level and the 61.8% line from the last rally to the 50-day moving average are concentrated here.

News background

Miners are selling their accumulated Bitcoin reserves. According to Glassnode’s calculations, BTC miners sent exchanges $128 million worth of cryptocurrency. This figure represents 315% of their daily production, a record.

The average income of a standard airdrop hunter was $9384 per address (median was $6497). According to a joint study by X-explore and crypto journalist Colin Wu, the premium segment had figures of $18,935 and $14,288.

According to The Block’s sources, Fidelity Investments is preparing to file a spot bitcoin ETF. Management companies BlackRock, WisdomTree, Invesco and Valkyrie filed to launch a spot bitcoin ETF in June.

The eight largest financial institutions in the US are “actively working” to provide clients with access to Bitcoin and other cryptocurrencies. Their assets under management total $27 trillion, CoinShares estimates.

ECB Vasle: Burden of proof for Sep in non-necessity of more hike

ECB Governing Council member Bostjan Vasle has emphasized the need for further monetary tightening in the face of persistent inflation, speaking on the sidelines of the ECB Forum.

"Given the persistence of inflation, we need to keep tightening monetary policy at our next meeting," Vasle stated.

Beyond July, the decision to further hike rates will be "data-dependent". However, Vasle conveyed that the "burden of proof" lies in data indicating "further rate hike is not needed instead that it is needed."

Vasle dismissed arguments that weaker growth readings might ease the ECB's fight against inflation. He asserted, "All these suggest that growth developments are not significantly different than our most recent projections."

The ECB official also expressed concerns over expectations that corporate profit margins might decline and absorb the impact of wage hikes, terming such a prospect as bearing significant risks.

"The labour market is strong and consumption is resilient. So firms might continue to enjoy pricing power, especially because demand is too strong to push down margins," he said.

ECB de Guindos: July a hike fait acommpli, September open

ECB Vice President Luis de Guindos has provided a somber outlook for the Eurozone's economic performance, emphasizing both stubborn inflation pressures and slower economic growth in an interview with Bloomberg TV in Sintra, Portugal.

When discussing the ECB's potential interest rate policy moves, de Guindos indicated that the decision to hike rates in July seems to be a "fait accompli", while the situation for September is "open".

De Guindos voiced his concerns about underlying inflation, which he expects to prove more stubborn than currently anticipated. The Vice President linked these persistent pressures to a potentially strong summer tourist season that could drive services costs higher.

Regarding the economy, "the data that we are receiving about growth are not very good," he confessed, adding that "some of these downside risks have started to materialize and are becoming much more visible."