Sample Category Title

Central bank leaders signal continued inflation battle

In an engaging dialogue at ECB forum, central bank leaders from across the globe hinted at the ongoing struggle against inflation, with an emphasis on the need for continued restrictive monetary policy.

Christine Lagarde, President of ECB, highlighted the necessity of sustained effort in the face of inflation, saying, "We still have more ground to cover." She underlined the lack of "tangible evidence" that domestic prices, a key indicator of underlying inflation, were stabilizing and starting to fall.

Meanwhile, Fed Chair Jerome Powell echoed this sentiment, asserting that, despite the current restrictive stance, monetary policy "may not be restrictive enough and it has not been restrictive for long enough." Leaving the door open for consecutive rate hikes, he said, "I wouldn't take moving in consecutive meetings off the table at all."

Andrew Bailey, Governor of BoE, justified last week's significant 50 basis point rate hike, attributing it to the persistence of inflation and labor market pressures. He stated, "The cumulative data... caused us to conclude that we had to make really quite a strong move."

On the other hand, Kazuo Ueda, Governor of BoJ, projected a temporary slowdown in inflation due to diminishing effects of past import price increases. However, he forecasted an inflation uptick into 2024, albeit admitting less confidence about this second phase. Ueda mentioned that confirmation of this second inflationary surge could be a "good reason to shift policy."

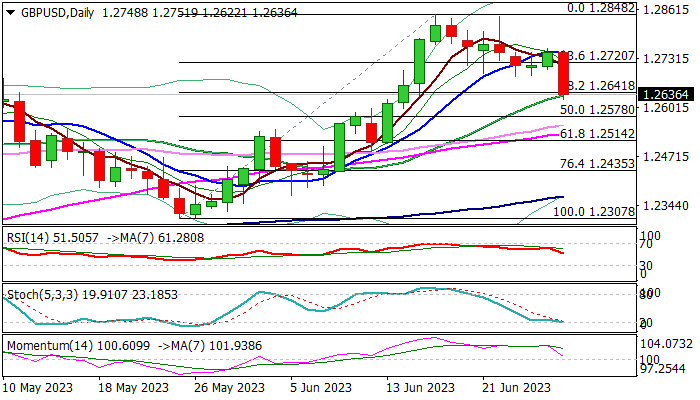

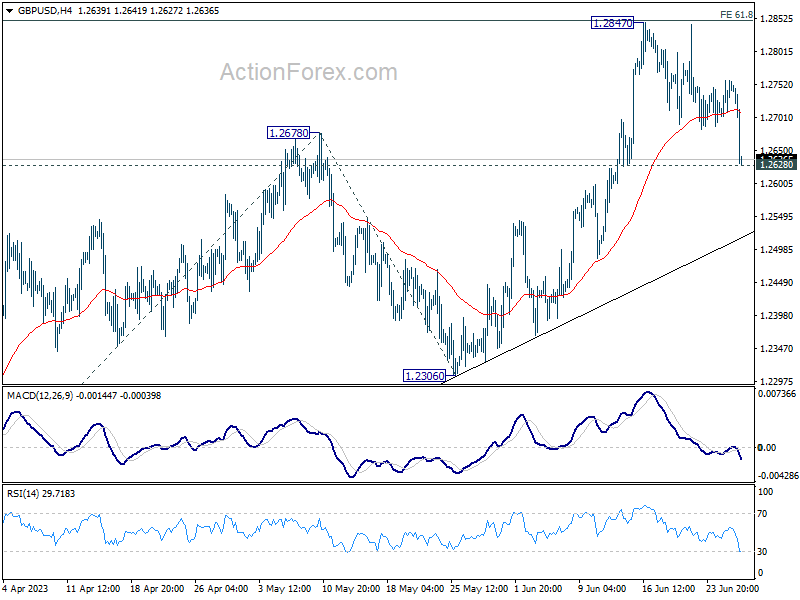

GBP/USD: Cable Loses Ground and Dips Nearly 1%

Cable was sharply down on Wednesday, losing 0.9% until early US session, as pound was weaker against all major counterparts.

Fresh bears broke below the floor of the recent range (1.2684) and cracked key near-term supports at 1.2641/34 (Fibo 38.2% of 1.2307/1.2848 / rising 20DMA).

Firm break of these levels would generate bearish signal for deeper pullback from new 2023 high (1.2848), left after larger bulls stalled under strong barriers, provided by 200WMA and monthly Ichimoku cloud base.

Sharp loss of bullish momentum weakens the structure on daily chart, increasing risk of deeper pullback, which could be triggered on firm break of 1.2641/34 pivots.

Daily Kijun-sen and 50% retracement of 1.2307/1.2848, mark next significant support at 1.2578, followed by Fibo 61.8% (1.2514) and top of thinning daily cloud at 1.2485.

Broken range floor (1.2684) reverted to resistance which should limit upticks and keep near-term bias with bears.

Res: 1.2684; 1.2720; 1.2735; 1.2759.

Sup: 1.2600; 1.2578; 1.2530; 1.2514.

Sunset Market Commentary

Markets

German Bunds started with some minor outperformance following the release of Italian June inflation data. They kick-off the national series in the run-up to Friday’s EMU publication. EU harmonized CPI slowed as expected from 0.3% M/M to 0.1% M/M with the Y/Y-figure declining slightly more than forecast (8% to 6.7% vs 6.8% expected). The minimal deviation was sufficient to generate a small bid in German Bunds in the run-up to the key panel discussion (ECB Lagarde, Fed Powell, BoE Bailey & BoJ Ueda) at the ECB’s annual forum in Sintra despite bullish risk sentiment on stock markets. Any market references have been cut off at 3:30 pm CET. German yields shed 3 to 4 bps with the belly of the curve outperforming the wings. US yields lose 2 to 3 bps across the curve. Key European gauges added up to 0.8% at the moment ahead of the US opening bell. The impact from a Bloomberg story on peripheral spreads was tiny, if any. In the article, sources close to the matter suggested that hawkish ECB members wanted to accelerate running down the balance sheet by either actively selling bonds from the APP portfolio or by phasing out the reinvestment policy from the Pandemic Emergency Purchase Programme. The single currency is again somewhat weaker than the greenback, changing hands around 1.0925. Sterling underperforms (EUR/GBP at 0.8650 from 0.86) on talks that officials are talking about contingency plans including a temporary nationalization of the country’s biggest water supplier, Thames water. Several ECB members talked on the sidelines of the Sintra forum and we retain the comments from an often dovish vice-president, de Guindos. He stated the obvious by labelling a July rate hike “fait accompli” and added that September is “open”. More ground has to be covered on rates. His economic assessment suggested an inclination to keep hiking. Core inflation could be stickier than thought, labour market dynamics are impressive and de Guindos expects the summer season in Europe to be very good, having an impact on the services sector.

News & Views

Norwegian retail sales surprisingly rebounded in May, rising by 1.2% M/M. This marks the biggest monthly rise since November last year. April sales was also upwardly revised from -1.2 M/M to only -0.1% M/M. The rise in sales was relatively broad-based with substantial gains in automotive fuel (+3%), ICT equipment (4.2%) and sales of other household equipment (4.2%). This rise was partially countered by a 2.2% monthly contraction in cultural and other recreation goods. The data suggest, admittedly tentative, signs of resilience of the Norwegian consumer. In its June monetary policy report, the Norges Bank downwardly revised its private consumption forecast for 2023 from -0.5% to -1.6% due to weaker purchasing power. The NB expected a decline in goods consumption while services were still forecasted to show a weak rise. With both underlying and headline inflation at 6.7% signs of consumer resilience support the case for further Norges Bank tightening. In its monetary policy report, the NB indicated that another rate hike in August is likely. The cycle peak policy rate was seen at 4.25% later this year (currently 3.75%). The krone gained temporary post the retail data but gains soon evaporated. At EUR/NOK 11.84, the currency remains weak/weaker than the NB hopes for.

Monetary data published by the ECB showed a further slowdown of money supply and credit as the ECB continues its cycle of monetary tightening. M3 money supply growth slowed from 1.9% Y/Y in April to 1.4% Y/Y in May. Regarding the credit dynamics, the annual growth rate of loans to the private sector decreased to 2.8% in May from 3.3% in April. Among the borrowing sectors, the annual growth rate of adjusted loans to households decreased to 2.1% in May from 2.5% in April, while the annual growth rate of adjusted loans to non-financial corporations decreased to 4% in May from 4.6% in April.

Yen Weakness: When Will BOJ Intervene?

Overnight, the USDJPY rose to the 144 handle which it hadn't seen since November of last year. This new weak point in the Japanese currency is just the latest in a long trend that has been going on since April. That's when markets came to the conclusion that the new head of the BOJ was actually serious about keeping easing policy in place.

But, understanding that the currency is now approaching the levels that last prompted the BOJ to step in, there is a rising question: When will authorities do something to stop the decline in the yen? Technically, it's actually the Ministry of Finance that steps in to shore up the currency, but it does so by instructing the BOJ to act. So, when will the BOJ do something?

Where the core issue lies

The main problem for Japanese authorities is squaring ultra-low interest rates to shore up the economy with an increasingly weaker currency that threatens to blow up inflation. Japan is facing a problem that it hasn't had to deal with in a long time, and it might take too long for authorities to adjust to a new reality.

With Japan doubling down on ultra-low rates and other central banks continuing to hike, there is increasing downward pressure on the yen. Carry-trade is now in vogue, where people sell yen and buy other currencies to take advantage of the difference in interest rates. The most effective and permanent way to deal with the problem of a weaker yen would be to get rid of the ultra-low interest rate policy. But, it appears that Japanese authorities are not near to doing that. At least, that's what the market is betting on, pushing the USDJPY higher and higher.

Something has to break

The last time the currency pushed towards these levels, Japanese officials tried to "jawbone" it down, by saying they were "intensely monitoring" the situation or were "concerned" about the exchange rate. But the currency was allowed to drift above the 150 handle before something was actually done, with the BOJ stepping in on behalf of the Ministry of Finance to buy a relatively small amount of the currency. This helped curtail the free-fall.

But, it wasn't until the BOJ made the surprise move of widening the band on YCC that things turned around. The BOJ tried to pass the move off as "policy neutral" because it widened the band both into positive and negative. But since all the pressure was on the upside, in practice it was a move towards tightening. It was also seen as the first step that would be taken to get rid of YCC, which is an easing mechanism. After that, the next step would be moving towards tightening, either with an interest rate hike or slowing down the amount of bonds being bought.

When will it happen this time around?

The issue now is that widening of the YCC already happened, so the BOJ doesn't have that tool at its disposal. Presumably it could widen the range again, but the effect might not be as pronounced, as investors might not be convinced it's a credible move towards tightening. The other option would be joint intervention between the Fed and the BOJ, something that Japanese authorities have hinted at with talk of "coordination".

In the end, however, it seems that Ueda is favorably disposed towards tightening - just not yet. The position of the BOJ might be to try to hold the line until the next GDP reading, to see if growth is actually manifesting. In the end, the whole point of the easing is to get "organic" inflation, not inflation caused by higher import costs from a weak currency. The question is whether the market will force Ueda to make his move ahead of schedule.

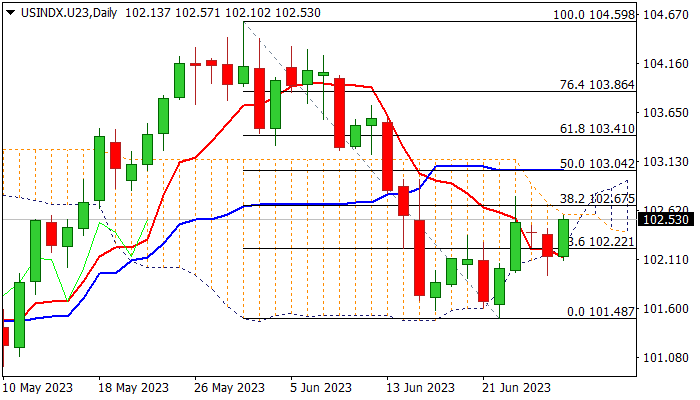

Dollar Index Regains Traction and Attacking Key Near-Term Barriers

The dollar index rose on Wednesday, as greenback regained traction on fresh weakness of index’s major components – Euro and British pound.

Fresh advance fully reversed Tuesday’s dip and generated an initial signal that two-day pullback is likely ending.

Thinning daily cloud twists on Thursday and attracts fresh bulls, though we need to see a clear break of pivotal barriers at 102.58/67 (cloud top / Fibo 38.2% of 104.59/101.48) to signal bullish continuation of the upleg from 101.48 (Jun 22), which will be confirmed on sustained break above 100DMA (102.81).

Traders await comments from Fed Chair Powell for more clues about the central bank’s action in the near future, as prevailing tone was so far hawkish, but policymakers also need to consider the negative impact of high borrowing to economic growth and recession threats.

Technical signals on daily chart are mixed, with repeated upside failure to keep the downside vulnerable, while sustained break higher would strengthen near-term structure.

Res: 102.81; 103.04; 103.41; 103.72.

Sup: 102.40; 101.94; 101.48; 100.99.

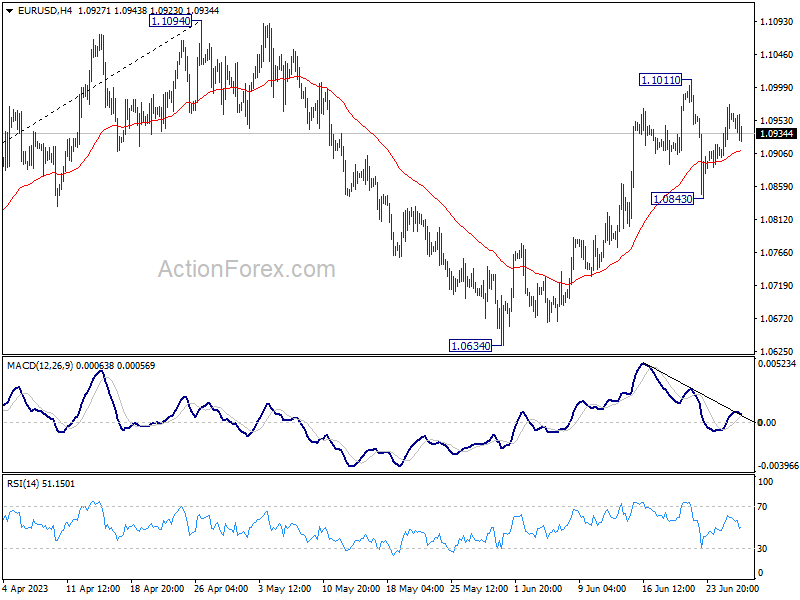

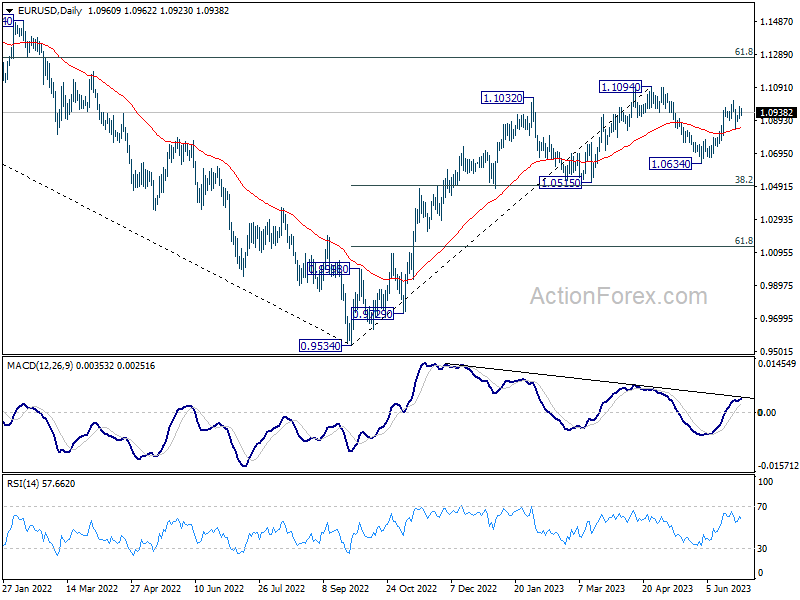

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0916; (P) 1.0947; (R1) 1.0991; More...

Range trading continues in EUR/USD and intraday bias stays neutral. Strong support from 55 D EMA (now at 1.0838) retains near term bullishness. Break of 1.1011 will resume the rally from 1.0634 and target 1.1094 resistance. Decisive break there will resume larger up trend from 0.9534.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

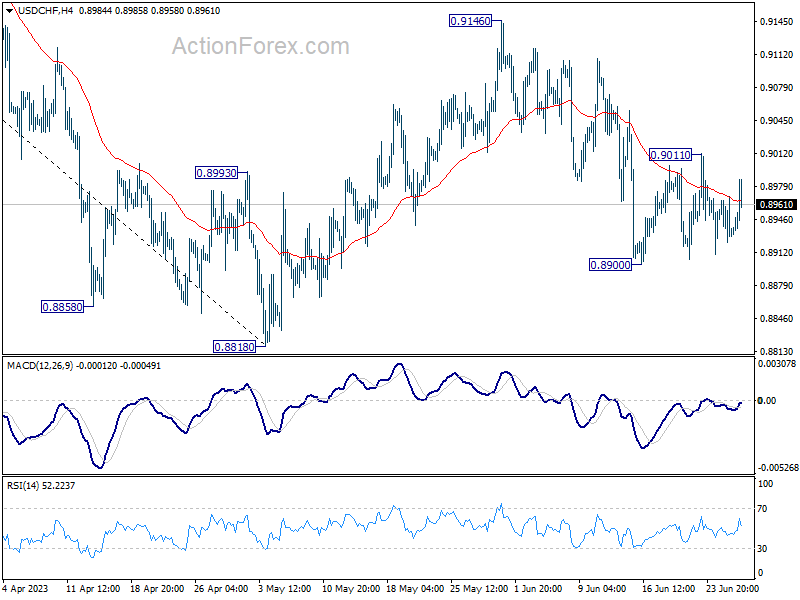

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8917; (P) 0.8944; (R1) 0.8963; More...

Range trading continues in USD/CHF and intraday bias stays neutral. On the downside, break of 0.8900 will resume the fall from 0.9146 to 0.8818 low or below. But for now, strong support is still expected from 0.8756 long term support to bring rebound. On the upside, above 0.9011 will bring stronger rise towards 0.9146 resistance.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming.

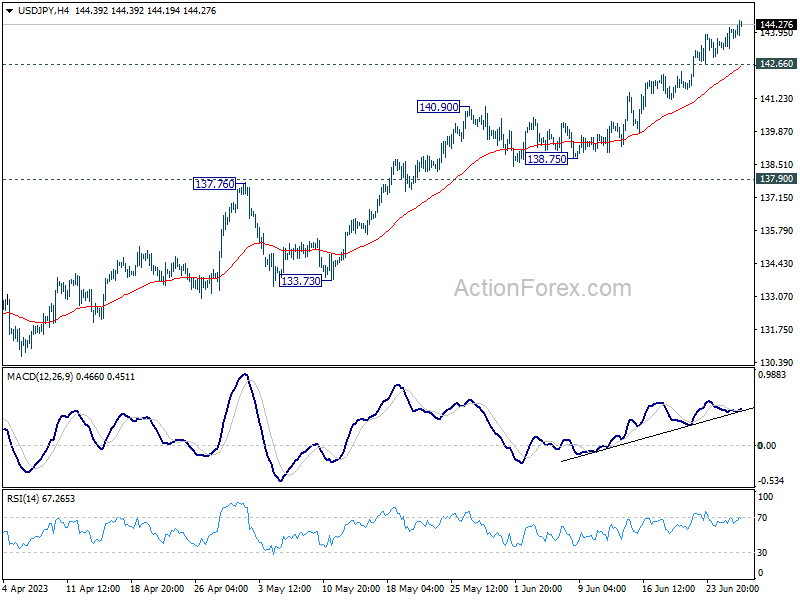

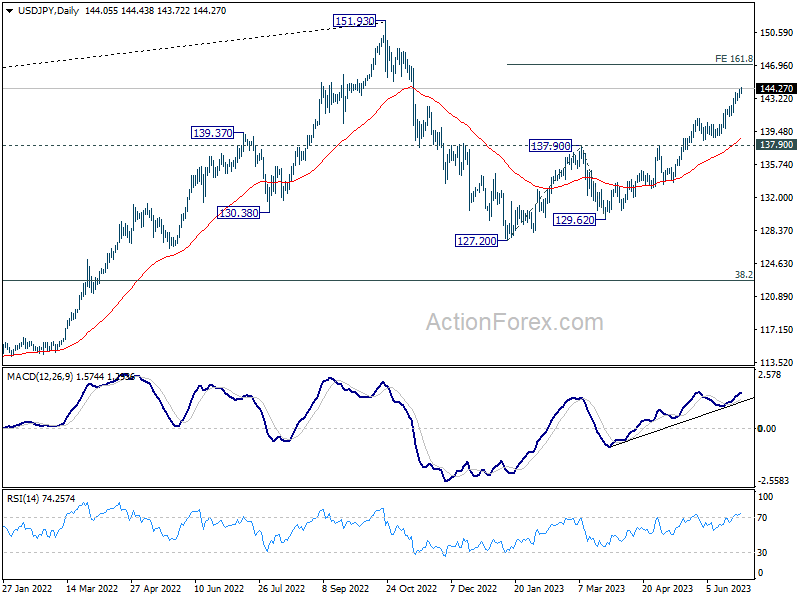

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.52; (P) 143.84; (R1) 144.40; More...

USD/JPY's rally is still in progress and intraday bias stays on the upside at this point. Current rise from 127.20 should target 161.8% projection of 127.20 to 137.90 from 129.62 at 146.93. On the downside, below 142.66 minor support will turn bias neutral again and bring lengthier consolidations first.

In the bigger picture, rise from 127.20 is currently seen as the second leg of the corrective pattern from 151.93 high. Further rally is expected as long as 137.90 resistance turned support holds, to retest 151.93. But strong resistance could be seen there to limit upside. Break of 137.90 will indicate the the third leg has started back towards 127.20.

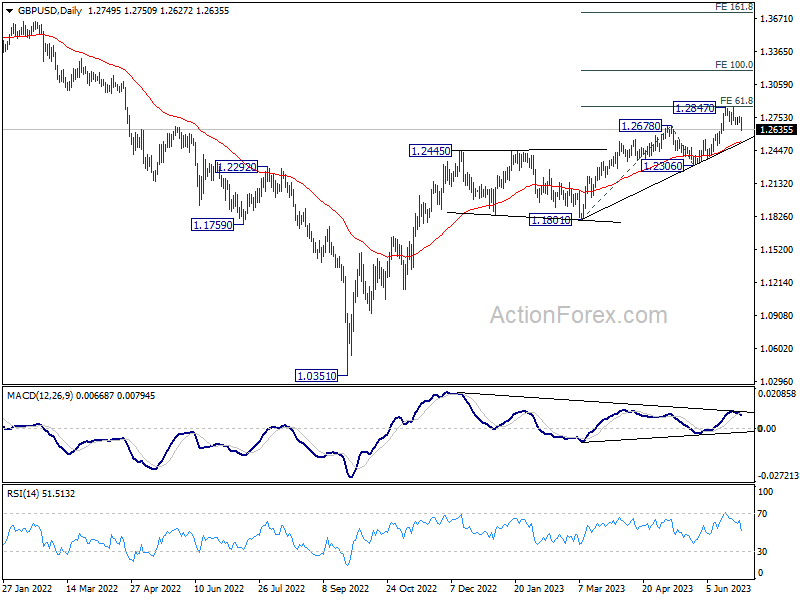

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2715; (P) 1.2738; (R1) 1.2771; More...

Immediate focus is now on 1.2628 support in GBP/USD. Break there will bring deeper fall to 55 D EMA (now at 1.2526). Considering bearish divergence condition in D MACD, sustained break of the EMA will argue that it's already in correction to larger up trend and target 1.2306 support. Nevertheless, rebound from current level will retain near term bullishness for up trend resumption through 1.2847 later.

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

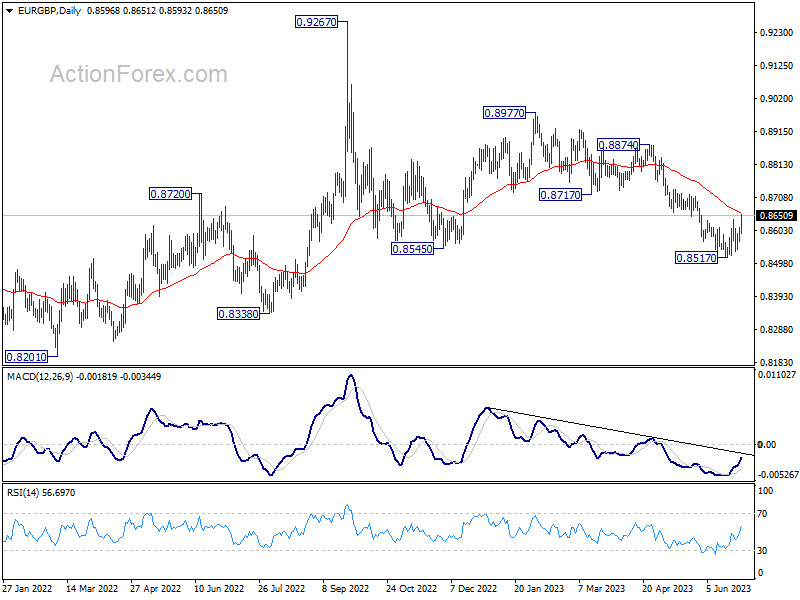

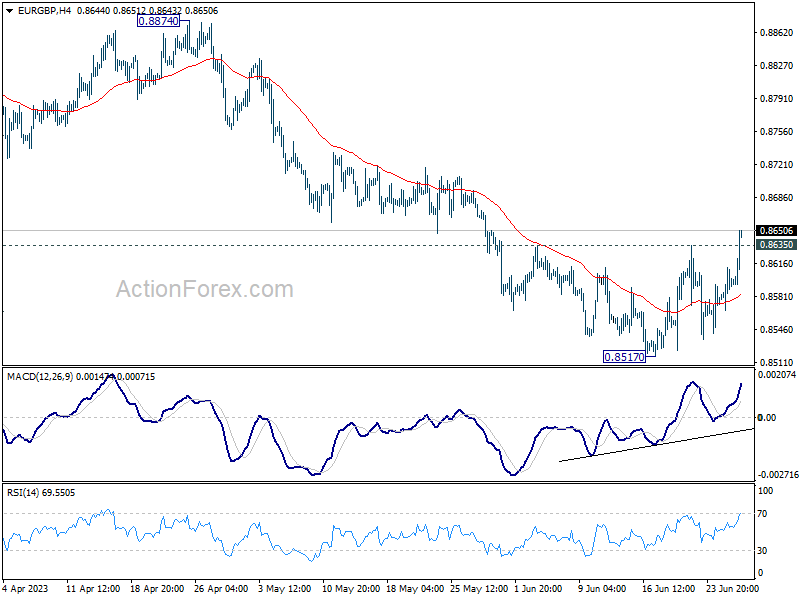

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8573; (P) 0.8593; (R1) 0.8618; More...

EUR/GBP's break of 0.8635 resistance confirms short term bottoming at 0.8517, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for 55 D EMA (now at 0.8658) and above. For now, as long as 0.8717 support turned resistance holds, fall from 0.8977 could still have another leg through 0.8517 before completion. However, firm break of 0.8717 will turn outlook bullish for 0.8977 resistance next.

In the bigger picture, the down trend from 0.9267 (2022 high) is still in progress. It's seen as part of the long term range pattern from 0.9499 (2020 high). Deeper fall could be seen towards 0.8201 (2022 low). But strong support should be seen from there to bring reversal. This will now remain the favored case as long as 0.8717 support turned resistance holds.