Sample Category Title

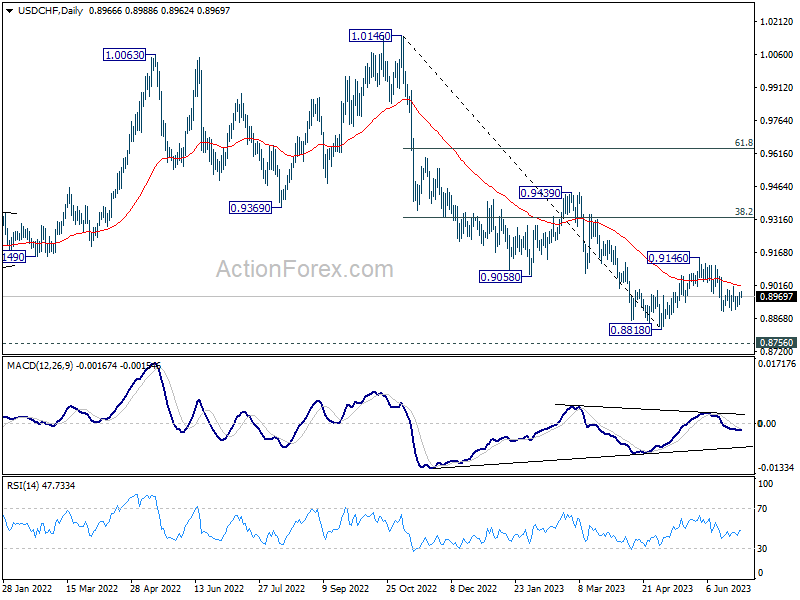

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8937; (P) 0.8962; (R1) 0.8995; More...

Intraday bias in USD/CHF remains neutral as sideway trading continues. On the downside, break of 0.8900 will resume the fall from 0.9146 to 0.8818 low or below. But for now, strong support is still expected from 0.8756 long term support to bring rebound. On the upside, above 0.9011 will bring stronger rise towards 0.9146 resistance.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming.

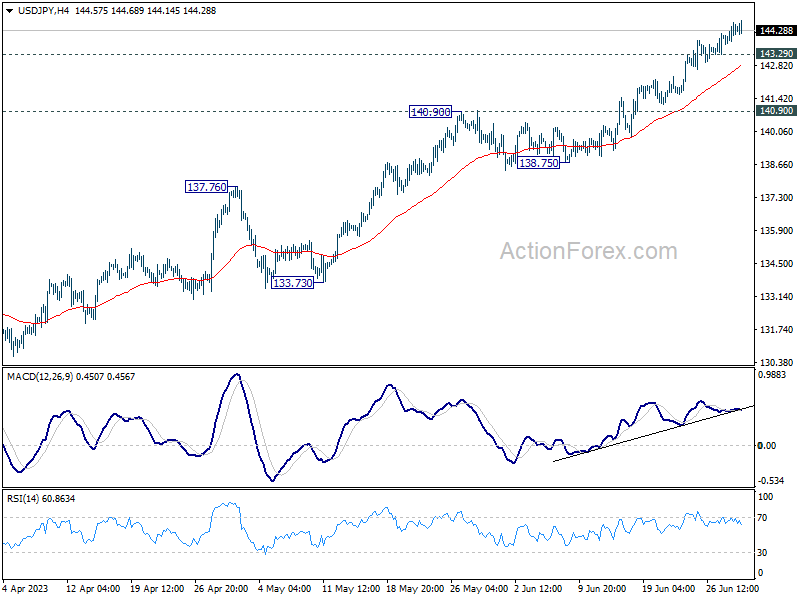

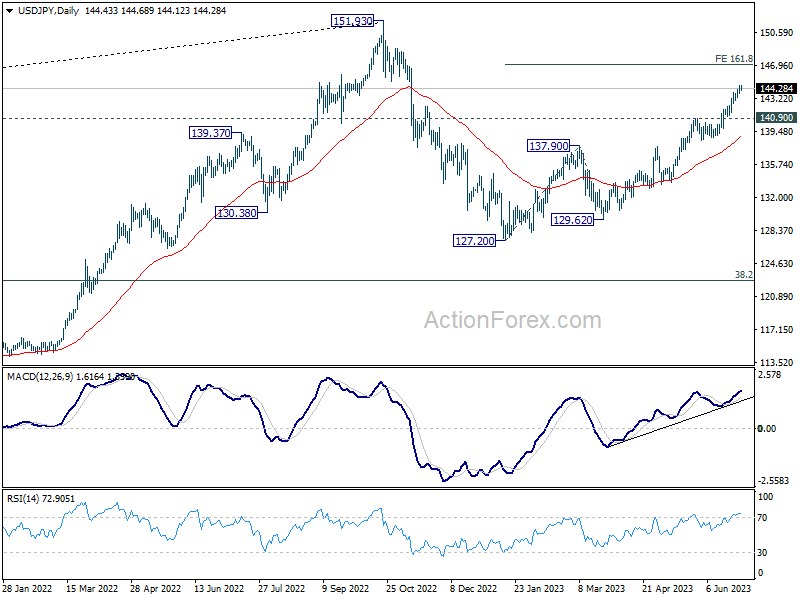

USD/JPY Daily Outlook

Daily Pivots: (S1) 143.94; (P) 144.28; (R1) 144.83; More...

Intraday bias in USD/JPY remains on the upside for the moment. Current rise from 127.20 should target 161.8% projection of 127.20 to 137.90 from 129.62 at 146.93. On the downside, below 143.29 minor support will turn bias again and bring consolidations. Down further rally will remain in favor as long as 140.90 resistance turned support holds.

In the bigger picture, rise from 127.20 is currently seen as the second leg of the corrective pattern from 151.93 high. Further rally is expected as long as 137.90 resistance turned support holds, to retest 151.93. But strong resistance could be seen there to limit upside. Break of 137.90 will indicate the the third leg has started back towards 127.20.

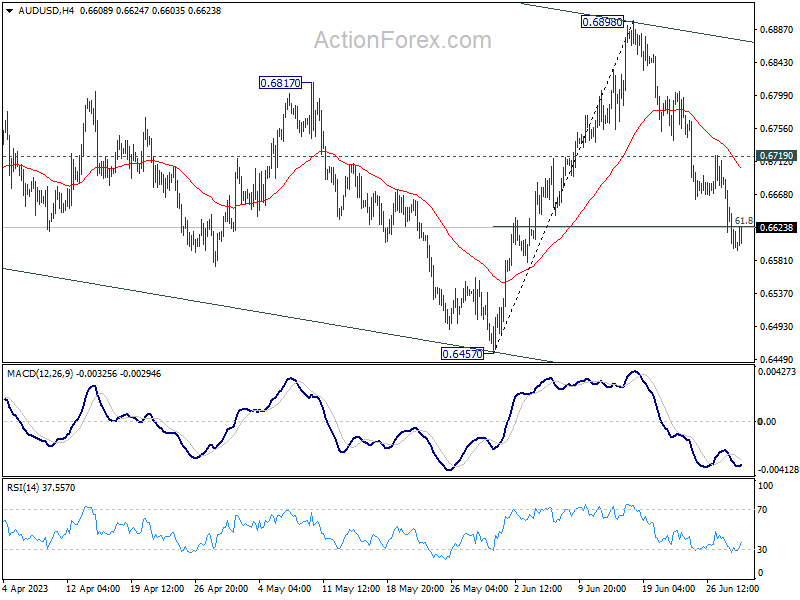

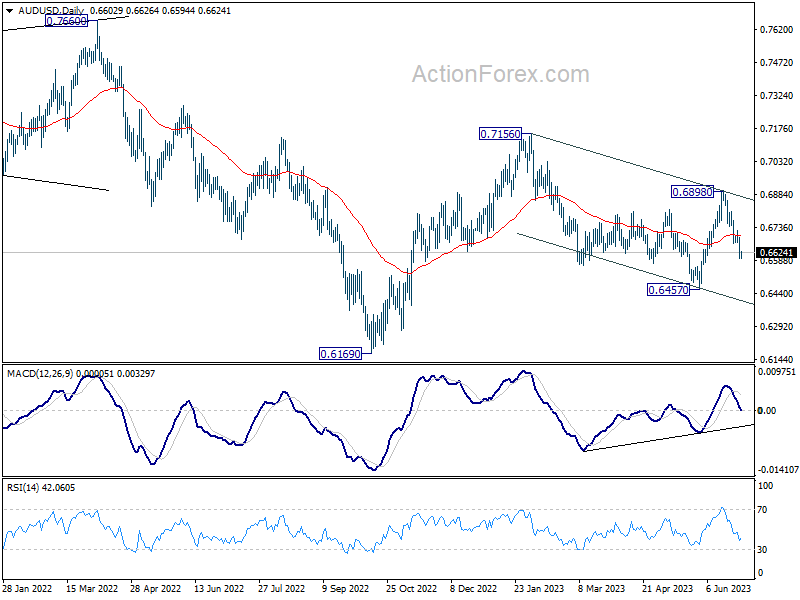

AUD/USD Daily Report

Daily Pivots: (S1) 0.6568; (P) 0.6629; (R1) 0.6661; More...

Intraday bias in AUD/USD stays on the downside at this point. Sustained break of 61.8% retracement of 0.6457 to 0.6898 at 0.6625 will path the way back to 0.6457 key support level. On the upside, above 0.6719 resistance will turn intraday bias neutral again first.

In the bigger picture, outlook is mixed up by the deeper than expected pull back from 0.6898. Still, price actions from 0.7156 are seen as a correction to rebound from 0.6169. Break of 0.6457 will resume the fall towards 0.6169 low. On the upside, though, break of 0.6898 resistance will argue that rise from 0.6169 is ready to resume through 0.7156.

Fed Powell: A long way to go to bring inflation down to 2%

In a speech today, Fed Chair Jerome Powell underscored the ongoing battle with inflation, asserting, "Inflation pressures continue to run high, and the process of getting inflation back down to 2 percent has a long way to go."

He added that "a strong majority of Committee participants expect that it will be appropriate to raise interest rates two or more times by the end of the year," referring to the latest dot plot.

Powell painted a mixed picture of the U.S. economy. He noted that "recent indicators suggest that economic activity has continued to expand at a modest pace." He also pointed to the effects of higher interest rates and slower output growth on business fixed investment.

His comments also highlight the persistent tightness in the labor market. "Over the past three months, payroll job gains have been robust," Powell said, adding that "labor demand still substantially exceeds the supply of available workers." Nevertheless, he also observed "some easing in nominal wage growth, and declining vacancies."

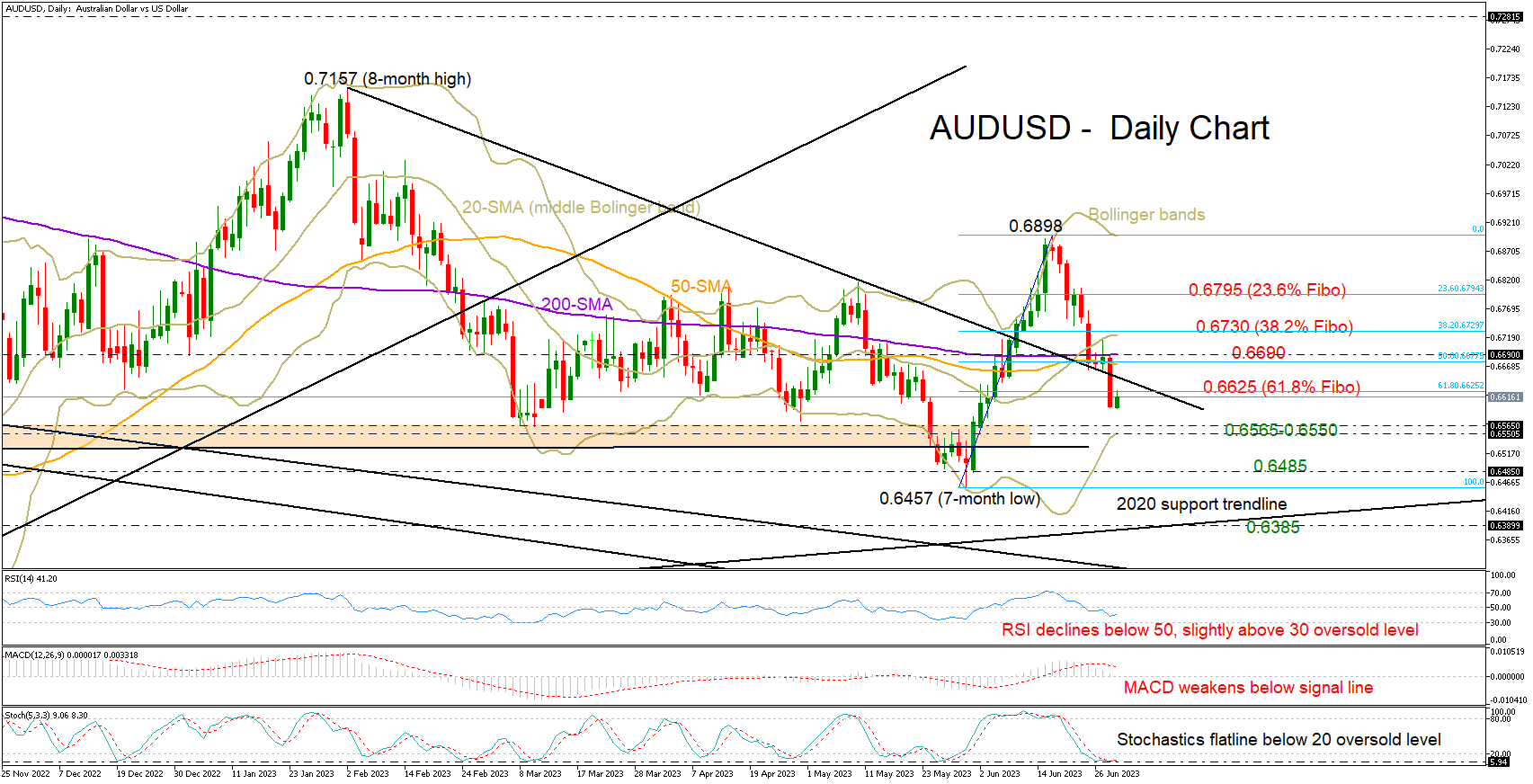

AUDUSD Erases June’s Upleg; Bias Bearish

AUDUSD sank to a three-week low of 0.6596 on Wednesday as the bulls could not find enough buyers to jump above the 200-day simple moving average (SMA) at 0.6690.

The pair is marking its second negative week, having trimmed more than half of June’s bull run to 0.6898.

Downside pressures could persist in the coming sessions as the technical indicators continue to slope southwards. The falling RSI has yet to reach its 30 oversold level, while the MACD remains negatively charged below its red signal line. That said, the stochastic oscillator has flattened near its previous lows, suggesting selling interest could fade soon.

The lower Bollinger band could prompt some consolidation within the 0.6565-0.6550 region, where the price faced limitations several times from the end of 2022 onwards. Failure to pivot here could direct the market back to May’s lows registered within the 0.6485- 0.6457 zone. A decisive close lower could stretch the February-May downtrend towards the 2020 support trendline seen around 0.6385.

On the upside, the 61.8% Fibonacci retracement of June’s bullish wave is currently capping the price around 0.6625. The resistance trendline is within short distance too, while the 50- and 200-day simple moving averages (SMAs) could be more challenging, cementing again the ceiling around the 50% Fibonacci mark and the 0.6690 bar. If the bulls breach that wall this time, the recovery could pick up steam towards the upper Bollinger band and the 38.2% Fibonacci of 0.6730. Then, another notable increase could take place, lifting the price up to the 23.6% Fibonacci of 0.6795.

In brief, the short-term risk for AUDUSD remains skewed to the downside, with support expected to develop within the 0.6565-0.6550 area.

AUD Drifts Lower

AUD/USD tests key support

The Australian dollar slumps as slowing inflation could let the RBA ease its hawkish stance. The exchange rate continues to lose ground after it failed to stay above the brief consolidation over 0.6670. 0.6580 at the start of the bullish breakout earlier this month is a crucial level to keep the June rebound valid. The RSI’s oversold condition may trigger a ‘buy-the-dip’ behaviour in this demand zone, but the bulls will need to clear 0.6690 before they could hope for a meaningful rebound, or 0.6500 could be the next target.

US Oil grinds demand zone

WTI crude jumped after the EIA reported a bigger-than-expected inventory drop. The price saw bids in the demand zone 66.00-67.00 as buyers struggle to keep their recent gains. A series of short-term downward breakouts indicates a strong bearish bias and could be grinding buyers’ gears. The psychological level of 70.00 is the first resistance and the bears could be looking to double down at rebounds. Only a new high above 72.60 would brighten up the mood. Otherwise, 65.00 would be the next stop when selling resumes.

Nasdaq 100 bounces back

The Nasdaq 100 recoups losses supported by recent upbeat US economic data. The index came across some buying interests over the 20-day SMA (14700) after it fell back from a 15-month high (15280). Profit-taking has driven the quote lower but there is no sign of liquidation. Overall sentiment remains exceedingly bullish and trend followers would be eager to jump in in the hope of pushing towards the all-time high. 14870 is the closest support and 15060 the first obstacle to lift, then a close above 15280 would resume the climb.

Inflation (Headline and Core) Should Reaccelerate Due to Base Effects

Markets

In yesterday’s Sintra panel discussion with ECB Lagarde, Fed Powell, BoE Bailey and BoJ Ueda, the former three all reiterated the need to hike rates further as the economy, and in particular the labor market, withstands previous tightening rather well. Powell referred to the dot plot which pencils in two more hikes and did not want to exclude moving on consecutive meetings. The intraday yield rebound that this triggered didn’t last though. US Treasuries finished around the highs for the day, pushing yields between 3.4-6.5 bps lower. The German yield curve turned slightly less inverse with changes of -3 (30-y) to -5.6 bps (2-y). A negligible 0.1 ppt miss in the y/y Italian HICP yesterday accelerated a trend already in place. Returning to the discussion, Ueda was the odd one out. He said inflation expectations and wage-setting behavior have changed for the good but there needs to be greater certainty on the outlook for prices in 2024 before considering a tweak to policy. European and US stock markets parted ways with the former adding 0.92% (EuroStoxx 50) but the latter trading mixed in a -0.22% to +0.27% range. The dollar was better bid. It extended and, unlike yields, retained gains after Powell’s comments. EUR/USD tested but closed above 1.09. USD/JPY moved further north and is closing in on the 145 barrier. Sterling slid on reports of a potential temporary and costly nationalization of the UK’s biggest water supplier. EUR/GBP took out 0.86 to close at 0.8637.

Australian and Japanese retail sales beat expectations in Asian dealings this morning (cf. infra). China fixed its currency stronger than expected as the yuan yesterday continued to slide. USD/CNY this morning nevertheless trades at the highest level since November last year with some dollar strength at play as well. Core bonds trade weaker. US cash yields add a few bps.

The ECB’s symposium drew to a close yesterday. Attention shifts to the economic calendar, containing US jobless claims, European economic confidence and inflation readings of several European member states including Belgium, Spain and Germany. Because of its weight in the European index, the latter will be closely watched. Inflation (headline and core) should reaccelerate due to base effects following the introduction of a cheap transport ticket one year ago for three months. Even if it is statistical in nature, it keeps inflation even more elevated for the coming period. Quickening inflation normally wouldn’t come as a surprise but it should protect (European) yields’ downside nevertheless. The German 10-y yield is nearing support from the upward sloping trendline again. Against this background we look for the euro to be better able to withstand current dollar strength.

News and views

The 23 biggest US banks passed the yearly stress test conducted by the US Federal Reserve. In the stress scenario, banks need to show that they have big enough capital buffers to withstand an extreme economic scenario. This year’s scenario included the unemployment rate jumping to 10%, commercial real estate prices falling 40% and house prices tumbling 38% with the short-term interest rate falling back near 0.0%. The test estimated that US banks would lose up to $541 bn, but it still would leave them with enough required capital. According to the Vice-Fed Chair for supervision Michel Barr the stress test confirms that the banking systems remains strong and resilient.

The Australian Bureau of Statistics reported stronger than expected May retail sales. Sales rose 0.7% M/M vs a 0.1% rise expected. Sales were 4.2% higher y/y. “Retail turnover was supported by a rise in spending on food and eating out, combined with a boost in spending on discretionary goods. This latest rise reflected some resilience in spending with consumers taking advantage of larger than usual promotional activity and sales events for May.”, ABS said. The report is one of last inputs before next week’s RBA policy decision. For now markets still only see about 20% chance of a new additional rate hike with further steps expected later this year. The Aussie dollar this morning holds near recent lows near the AUD/USD 0.66 big figure. May retail sales in Japan this morning also printed higher than expected at 1.3% M/M and 5.7% Y/Y. Data show resilience in consumer spending in Japan as well, but at least for now the BoJ doesn’t hint at a change in policy yet. The yen remains in the defensive this morning with USD/JPY holding the short-term top in the 144.6 area.

Fed Got Greenlight for More Hikes

US and European stocks were up on Wednesday. The US chipmakers dampened appetite across the Atlantic Ocean on news that the Biden Administration will bring more restrictions to the US chipmakers’ exports toward China, but Nasdaq still eked out gains.

Unfortunately for Nvidia, its A800 chips which were launched as a response to last year’s export ban could be included in the new set of restrictions. Nvidia stock fell yesterday, but not as bad as premarket trading suggested. Taking a closer look to Nvidia’s revenue per region, revenue slowed by around $2bn in China amid the chip export ban last year, but the fall in Chinese revenue was compensated with a doubling revenue for the US. This means that, even though the Chinese growth potential is weakened, there is potential to grow business for Nvidia. For others, AMD was almost flat, and Micron was up following an upbeat forecast for the current period amid the easing chip glut.

Same, same

The major central bankers’ speeches were the same background music. The Federal Reserve’s (Fed) Powell, the Bank of England’s (BoE) Bailey, and the European Central Bank’s (ECB) Lagarde agreed that their fight against inflation wasn’t done yet, and that more rate hikes are on the pipeline.

What was interesting however was that the Bank of Japan’s (BoJ) Ueda didn’t necessarily think that the Fed, the BoE and the ECB overtightened, while he, on his end, didn’t move an inch to fight back inflation. What’s even funnier is, Powell, Bailey and Lagarde acknowledged that their policy actions come with a lagging effect, but BoJ’s Ueda joked saying that because Japan hasn’t started hiking yet, the lag effect could be ‘at least 25 years’. I don’t know if it makes you laugh or cry, but it made the central bankers, and the yen shorts laugh.

The dollar yen is now at the highest levels since November last year, a touch below the 145 mark, and on its way toward higher waters. Yet, a rapid and extended period of yen depreciation remains concerning for Japanese officials and could end up with direct FX intervention to halt bleeding. That’s one risk that the short yen positions carry right now, as the yield differential plays clearly in favour of further yen selling.

Elsewhere, sentiment in euro was weak yesterday on the back of a mixed set of data. The Italian PPI fell much slower than expected in May, but consumer price inflation eased more than expected. The ECB’s money supply slowed, and loans to the private sector grew slower than expected as a sign of tighter credit due to higher rates. Germany will reveal its own inflation figures today, and we could see an uptick in German inflation according to a consensus of analyst expectations. It would be bad news for the ECB. So many hikes, and so many more promised by the ECB, and inflation is hanging around.

It is because the Fed, ECB and BoE’s balance sheets remain the elephant in the room, and they are the reason why economies don’t react efficiently to interest rate hikes, and inflation doesn’t slow at the desired speed. Yes, the Fed, ECB and BoJ’s combined balance sheet size has been shrinking since last year, but total assets remain indisputably HIGH - almost 50% higher than pre-pandemic levels. So, you bet, the higher rates don’t do much harm to the economy, except for those who have to renew their mortgages.

For the ECB however, the fact that the cheap loans are drying out could achieve some faster results. But it could trigger a divergence between core and periphery, widen the spread between Germany and the periphery and the latter could slow down the euro’s appreciation.

Fed’s stress test gives the greenlight for more hikes

The US banks passed the Fed’s stress test, giving a greenlight to the Fed for more rate hikes. The US banks gained in the afterhours trading, with Bank of America and Wells Fargo leading gains, but the new regulations regarding capital requirements will likely hold back investors from full heartedly going back to banks.

Crude jumps

Crude oil jumped off below the $67pb level on the back of an almost 10mio barrel decline in US crude inventories last week. There is now a triple bottom formation at around the $67pb level, and that could throw a floor under any short-term selloff in crude oil. But the $70pb resistance remains strong, and more offers are waiting into the 50-DMA, a touch below the $72pb level. The chances are that we will see some back and forth between $67 and $72 range, until one side gives in.

All Eyes on Riksbank

Market movers today

Today we expect a 25bp hike from the Riksbank. We expect the Riksbank to conclude their hiking cycle with another 25bp hike in September putting the terminal policy rate at 4.0% like the ECB, see more in the Nordic section below.

Following a big decline in Italian inflation from 8.0 to 6.7% yesterday, more euro area countries, including Germany, will publish June inflation data.

We also have both Powell and Lagarde on the wires again today.

Overnight, China publishes official PMI data, where we look for a small lift to the manufacturing PMI and further moderation in the service PMI from still high levels.

The 60 second overview

Sintra: The policy panel with Lagarde, Powell, Bailey and Ueda brought few new signals on the monetary policy outlook. Powell struck a somewhat more hawkish tone than in his most recent speeches, highlighting that US monetary policy might not be restrictive enough and that moving back to consecutive hikes is not off the table. Furthermore, he underscored the asymmetric outlook, where the cost of bringing inflation down quickly will be lower than allowing inflation to prolong, even if it requires a modest recession.

Lagarde mostly reiterated her earlier messages, saying that the ECB is likely to hike again in July, but not commenting on the outlook for meetings beyond summer. On the macro data front, Italian June inflation data showed a clear decline in headline inflation from 8.0% to 6.7% y/y, with some easing in the core and services measures as well. Italy is the first major euro area economy to report monthly inflation data, followed by Germany and Spain today, and finally the euro area HICP tomorrow.

US bank stress tests: The Fed's annual stress tests showed that large US banks remain 'well positioned to continue lending' even in a scenario of a severe economic downturn. While large US lenders remain well capitalized for adverse events, the Fed's Barr cautioned that markets should remain humble about how risks can arise, referring to the turmoil seen last spring. For now, US banks' liquidity buffers remain above pre-pandemic levels, not least reflecting the gradual increase in the use of the Bank Term Funding Program introduced in March. The rebuild of US Treasury's cash balance has also not drained bank reserves as feared, even though the process is already more than halfway done. We discussed the latest USD liquidity developments in more detail yesterday in FX Strategy - USD liquidity unaffected by rebuild of cash balance, 28 June.

Equities: Global equities were a tad higher yesterday with big regional and sector differences. Japan almost 2% higher, US flat and Latin America down 1%. Same for sectors with cyclical part outperforming the defensives. We are only halfway through 2023 and sector returns go from -5% to plus 35% which no one (of course) expected going into the year. 2023 is not a big outlier; it happens every year, but strategists and investors are typically underestimating the low sector correlation and high realized return differences. However, this just tells us that one can make a lot of alpha even with limited sector bets.

In US yesterday, Dow -0.2%, S&P 500 -0.04%, Nasdaq +0.3% and Russell 2000 +0.5%. Asian markets with big differences again this morning, Japanese markets are higher while Hang Seng is down 1.5%. Many will end up concluding that Q2 2023 was the quarter of AI related outperformance but please take a look at Japan versus Hang Seng. Remarkable outperformance that no one is talking about and this is not an AI story.

FI: European yields fell through most of yesterday's session. German yields ended the day down by about 4-5bp across the curve, while BTP yields were close to unchanged. Market expectations for the peak ECB rate fell by approximately 5bp to 3.95% throughout the day. There was no single factor behind the declining pattern in yields, although both Italian CPI/PPI and Eurozone money supply data came in soft. Inflation forward swaps saw minor declines throughout the day.

FX: NOK and USD led the way yesterday, where GBP, AUD and NZD lost ground to the rest of G10. Majors largely ignored comments from key central bank heads speaking at Sintra as they did not offer any substantial news. Notably, SEK fell ahead of today's Riksbank meeting.

Credit: While primary market activity remained lively yesterday, the investor response for several of the new deals was rather disappointing. This was the case e.g. for Italian renewable energy company Alperia which priced its 5y green senior line with initial guidance at MS+250bp, while Commerzbank also seemed to struggle with its new 10.25NC5.25 EUR500m Tier 2. The spread on the latter was set at MS+370bp following IPTs of 370/375bp and the final book size was undisclosed. CDS indices were broadly unchanged with iTraxx Main closing at 77bp (-1bp) while Xover was 1bp tighter at 416bp.

Nordic macro

Sweden: Today's main event is undoubtedly the Riksbank policy decision at 09.30 CET. Our call entails a 25bp hike, increased QT volumes (+50%, from SEK3.5bn to SEK5.25bn) and a repo rate path indicating an additional 10-15bp worth of hikes for the September meeting. Market pricing going into the meeting implies a (roughly) 40% probability of a 50bp hike which cannot be completely ruled out, especially in light of the continued weakening of the SEK. However, as recent inflation developments have been in line with Riksbank projections, we see 25bp as the most likely outcome today, which is also consensus. Increased QT volumes is also consensus amongst banks, and we deem an increase of 50% as reasonable. As for the rate path we believe that the Riksbank opts to keep the door open for further hikes, and thus signal a non-zero probability of further hikes in coming meetings, just as they did back in February.

In the Riksbank's shadow, we also get data on retail sales and NIER's Economic Tendecy Survey. Both these variables have shown signs of near-term stabilization as Swedish consumers are concerned, and as such the new prints will be important input for whether this continues or not, with potentially strong implications for broader Swedish economic developments as well.

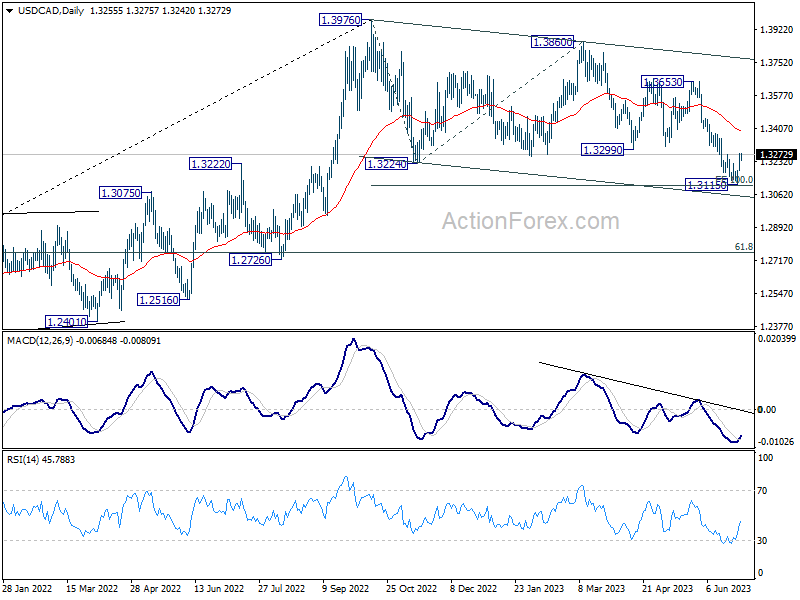

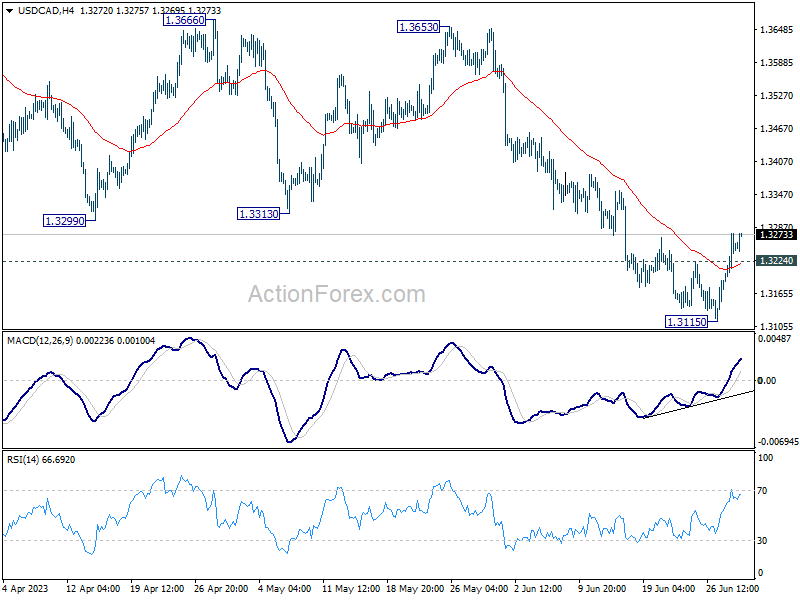

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3207; (P) 1.3242; (R1) 1.3294; More....

USD/CAD's break of 1.3224 minor resistance should confirm short term bottoming at 1.3115, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for 1.3229 support turned resistance. Firm break there will extend the rebound to 55 D EMA (now at 1.3389). On the downside, break of 1.3115 is needed to confirm resumption of recent decline. Otherwise, more consolidative trading should be seen first, in case of retreat.

In the bigger picture, price actions from 1.3976 are still viewed as a correction to up trend from 1.2005 (2021 low), but chance of trend reversal is increasing with current decline. In either case, risk will stay on the downside as long as 1.3299 support turned resistance holds, even in case of strong rebound. Next target is 61.8% retracement of 1.2005 to 1.3976 at 1.2758. Sustained trading above 1.3229 will raise the chance that the correction has completed and turn focus back to 1.3653 resistance.