Sample Category Title

Dollar Extending Rebound in Quiet Markets, Central Bankers Triggered No Volatility

In today's Asian trading session, forex markets are experiencing a lull, with most of the major currency pairs and crosses moving within the boundaries set by yesterday's trading ranges. The anticipated volatility sparked by the robust remarks from the heads of the ECB, Fed, BoE, and BoJ during the ECB forum overnight failed to materialize. Their unified message underscored the ongoing fight against inflation amidst a landscape of uncertainties, yet the markets remain unresponsive. While major US indexes closed with mixed results, Asian markets seem to lack a clear common trajectory.

Taking stock of the week's movements thus far, Dollar leads as the strongest currency, displaying promising gains against commodity currencies. However, it would need to make further rally against Euro and Swiss Franc to substantiate its underlying strength. Euro trails as the second-strongest currency, followed the Swiss Franc, boosted partially by buying against the weakening Sterling. Australian and New Zealand Dollars sit at the bottom of the pack as the week's worst performers, while Japanese Yen remains mixed, digesting its recent losses.

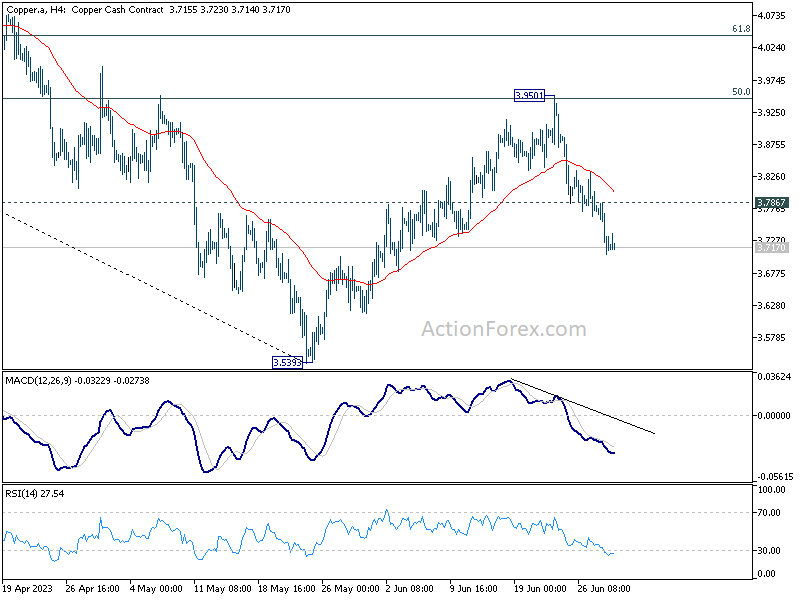

Technically, Copper's fall from 3.9051 is extending and the development reinforces the case that corrective rebound from 3.5393 has completed already. Further decline is now in favor as long as 3.7867 minor resistance holds, back to retest 3.5393 low. Any downside acceleration could drag AUD/USD further towards 0.6457 support.

In Asia, at the time of writing, Nikkei is up 0.37%. Hong Kong HSI is down -1.35%. China Shanghai SSE is down -0.18%. Singapore Strait Times is up 0.06%. Japan 10-year JGB yield is down -0.002 at 0.385. Overnight, DOW dropped -0.22%. S&P 500 dropped -0.04%. NASDAQ rose 0.27%. 10-year yield fell -0.058 to 3.710.

Japan retail sales rose 1.3% mom, 5.7% yoy, beat expectations

In the latest release from Japan, retail sales rose 1.3% mom, surpassing the anticipated increase of 0.8% mom. This growth also reflects a robust 5.7% yoy rise, again beating expectations of 5.2% year-on-year.

While inflation remaining above 3% mark could have been a contributing factor in boosting retail sales, there is evidence to suggest that return of overseas tourists is also playing a substantial role in stimulating economic activity.

Earlier reports from Japan National Tourism Organization highlighted that number of overseas visitors is nearing 70% of pre-pandemic levels as of May, indicating a resilient recovery of the tourism sector, and with it, potential for further economic growth.

In separate release, Consumer Confidence index nudged up from 36.0 to 36.2. This is the highest reading observed since January 2022, suggesting that households are more optimistic about the economy's trajectory. This could potentially translate into a higher propensity to spend, further bolstering retail sales and overall economic performance in the coming months.

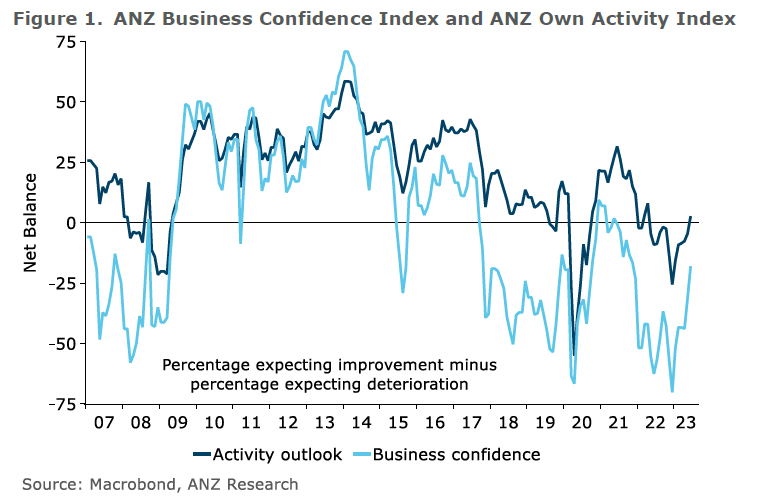

NZ ANZ business confidence rose to -18, subtle signs of easing inflation pressures

New Zealand ANZ Business Confidence Index improved notably from -31.1 to -18.0 in June, marking the highest level since November 2021. Furthermore, the outlook for their own activity rose from -4.5 to 2.7, turning positive for the first time in 14 months.

Digging into the details reveals a more nuanced picture. Despite the improved overall business sentiment, export intentions dipped from 2.0 to -1.8. However, there were more encouraging signs in other areas: investment intentions rose from -6.8 to -2.7, and employment intentions followed suit, moving from -5.7 to -3.5. Meanwhile, pricing intentions have shown a modest decline from 52.4 to 49.3.

On the inflation front, there are tentative signs that pressures might be easing slightly. Cost expectations dropped from 84.1 to 76.0, and inflation expectations decreased from 5.47% to 5.29%. There was also a slight improvement in profit expectations, which rose from -27.4 to -24.1.

Commenting on the results, ANZ noted, "for now, cautious optimism appears to be emerging that the worst could be past – but it's conditional on those inflation indicators continuing to fall."

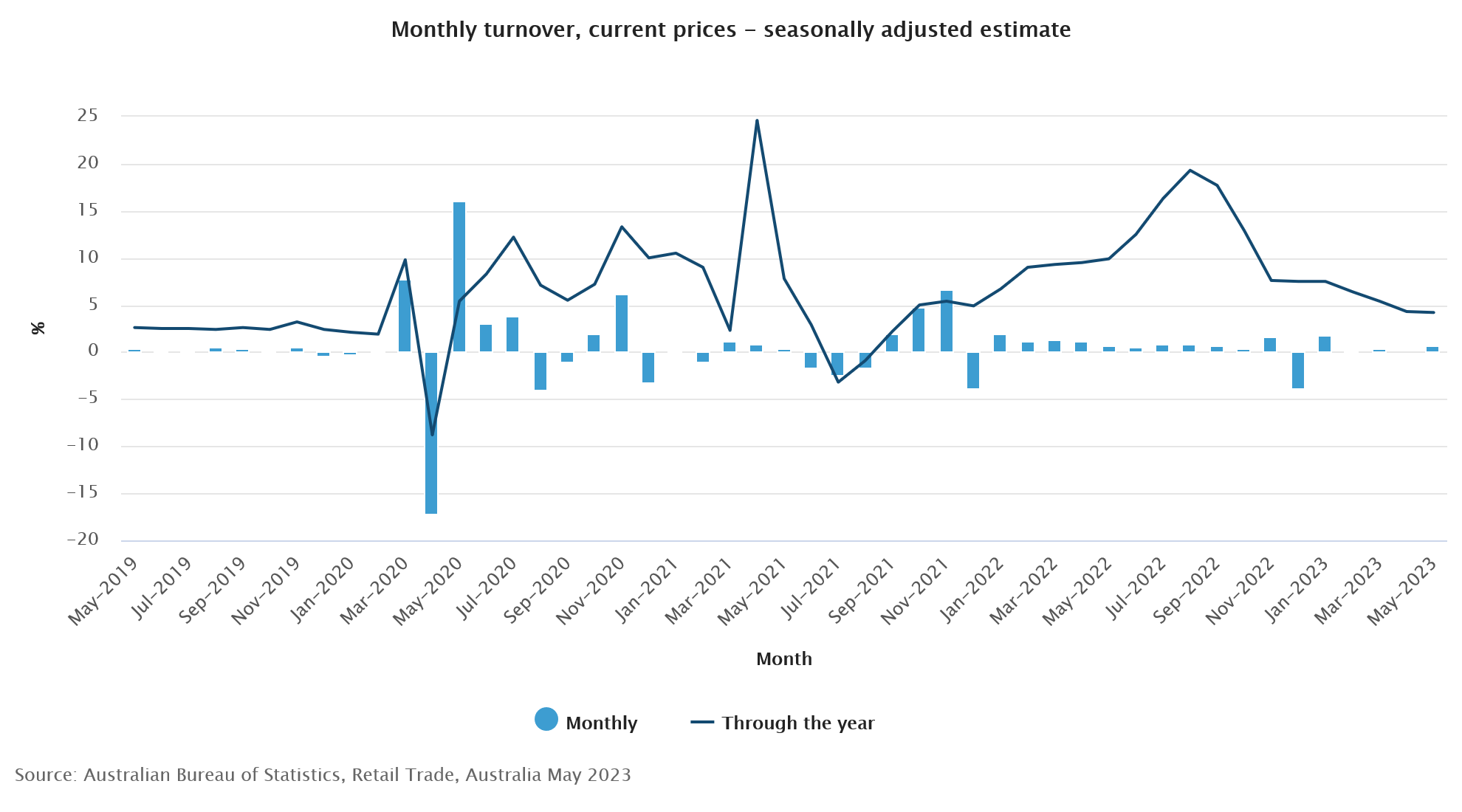

Australia retail sales rose 0.7% mom, boosted by sales events

Australia retail sales turnover rose 0.7% mom to AUD 35.52B in May, well above expectation of 0.1% mom. Through the year, sales turnover was up 4.2% yoy.

Ben Dorber, ABS head of retail statistics, said: "Retail turnover was supported by a rise in spending on food and eating out, combined with a boost in spending on discretionary goods.

"This latest rise reflected some resilience in spending with consumers taking advantage of larger than usual promotional activity and sales events for May."

Looking ahead

Eurozone economic sentiment, Germany CPI flash, UK M4 money supply and mortgage approvals will be released in European session. ECB will also publish monthly economic bulletin. Later in the day, US will release jobless claims, pending home sales and Q1 GDP final.

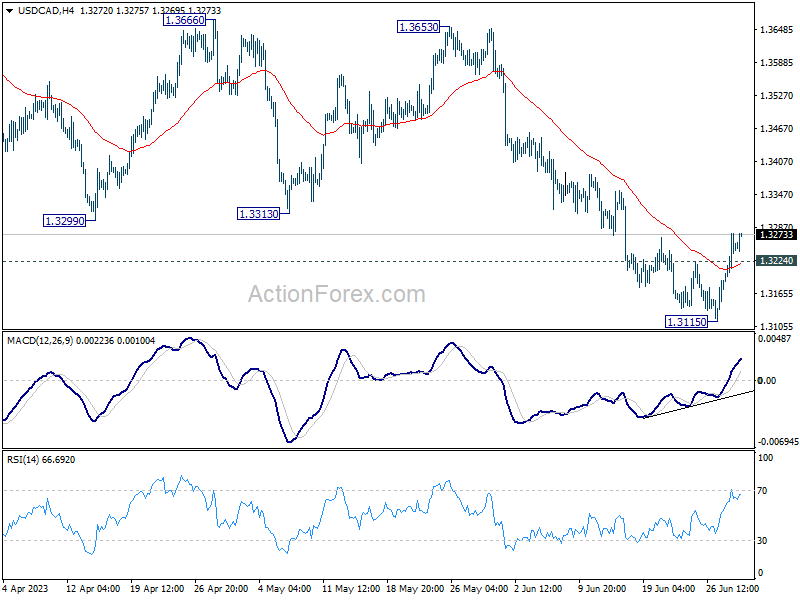

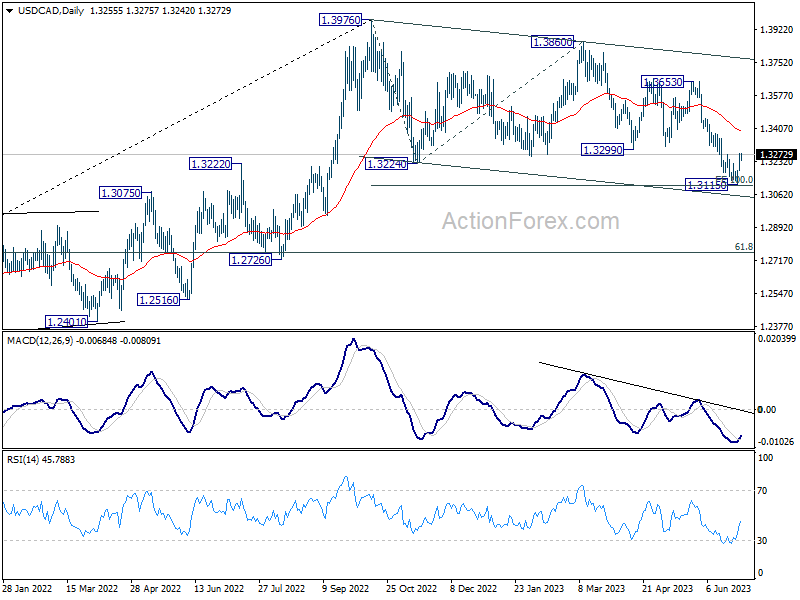

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3207; (P) 1.3242; (R1) 1.3294; More....

USD/CAD's break of 1.3224 minor resistance should confirm short term bottoming at 1.3115, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for 1.3229 support turned resistance. Firm break there will extend the rebound to 55 D EMA (now at 1.3389). On the downside, break of 1.3115 is needed to confirm resumption of recent decline. Otherwise, more consolidative trading should be seen first, in case of retreat.

In the bigger picture, price actions from 1.3976 are still viewed as a correction to up trend from 1.2005 (2021 low), but chance of trend reversal is increasing with current decline. In either case, risk will stay on the downside as long as 1.3299 support turned resistance holds, even in case of strong rebound. Next target is 61.8% retracement of 1.2005 to 1.3976 at 1.2758. Sustained trading above 1.3229 will raise the chance that the correction has completed and turn focus back to 1.3653 resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y May | 5.70% | 5.20% | 5.00% | 5.10% |

| 01:00 | NZD | ANZ Business Confidence Jun | -18 | -31.1 | ||

| 01:30 | AUD | Retail Sales M/M May | 0.70% | 0.10% | 0.00% | |

| 05:00 | JPY | Consumer Confidence Jun | 36.2 | 36.2 | 36 | |

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 08:30 | GBP | Mortgage Approvals May | 50K | 49K | ||

| 08:30 | GBP | M4 Money Supply M/M May | -0.10% | 0.00% | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jun | 96 | 96.5 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Jun | -5.5 | -5.2 | ||

| 09:00 | EUR | Eurozone Services Sentiment Jun | 5.5 | 7 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Jun F | -16.1 | -16.1 | ||

| 12:00 | EUR | Germany CPI M/M Jun P | 0.20% | -0.10% | ||

| 12:00 | EUR | Germany CPI Y/Y Jun P | 6.30% | 6.10% | ||

| 12:30 | USD | Initial Jobless Claims (Jun 23) | 265K | 264K | ||

| 12:30 | USD | GDP Annualized Q1 F | 1.30% | 1.30% | ||

| 12:30 | USD | GDP Price Index Q1 F | 4.20% | 4.20% | ||

| 14:00 | USD | Pending Home Sales M/M May | -0.30% | 0.00% | ||

| 14:30 | USD | Natural Gas Storage | 83B | 95B |

Japan retail sales rose 1.3% mom, 5.7% yoy, beat expectations

In the latest release from Japan, retail sales rose 1.3% mom, surpassing the anticipated increase of 0.8% mom. This growth also reflects a robust 5.7% yoy rise, again beating expectations of 5.2% year-on-year.

While inflation remaining above 3% mark could have been a contributing factor in boosting retail sales, there is evidence to suggest that return of overseas tourists is also playing a substantial role in stimulating economic activity.

Earlier reports from Japan National Tourism Organization highlighted that number of overseas visitors is nearing 70% of pre-pandemic levels as of May, indicating a resilient recovery of the tourism sector, and with it, potential for further economic growth.

In separate release, Consumer Confidence index nudged up from 36.0 to 36.2. This is the highest reading observed since January 2022, suggesting that households are more optimistic about the economy's trajectory. This could potentially translate into a higher propensity to spend, further bolstering retail sales and overall economic performance in the coming months.

Australia retail sales rose 0.7% mom, boosted by sales events

Australia retail sales turnover rose 0.7% mom to AUD 35.52B in May, well above expectation of 0.1% mom. Through the year, sales turnover was up 4.2% yoy.

Ben Dorber, ABS head of retail statistics, said: "Retail turnover was supported by a rise in spending on food and eating out, combined with a boost in spending on discretionary goods.

"This latest rise reflected some resilience in spending with consumers taking advantage of larger than usual promotional activity and sales events for May."

NZ ANZ business confidence rose to -18, subtle signs of easing inflation pressures

New Zealand ANZ Business Confidence Index improved notably from -31.1 to -18.0 in June, marking the highest level since November 2021. Furthermore, the outlook for their own activity rose from -4.5 to 2.7, turning positive for the first time in 14 months.

Digging into the details reveals a more nuanced picture. Despite the improved overall business sentiment, export intentions dipped from 2.0 to -1.8. However, there were more encouraging signs in other areas: investment intentions rose from -6.8 to -2.7, and employment intentions followed suit, moving from -5.7 to -3.5. Meanwhile, pricing intentions have shown a modest decline from 52.4 to 49.3.

On the inflation front, there are tentative signs that pressures might be easing slightly. Cost expectations dropped from 84.1 to 76.0, and inflation expectations decreased from 5.47% to 5.29%. There was also a slight improvement in profit expectations, which rose from -27.4 to -24.1.

Commenting on the results, ANZ noted, "for now, cautious optimism appears to be emerging that the worst could be past – but it's conditional on those inflation indicators continuing to fall."

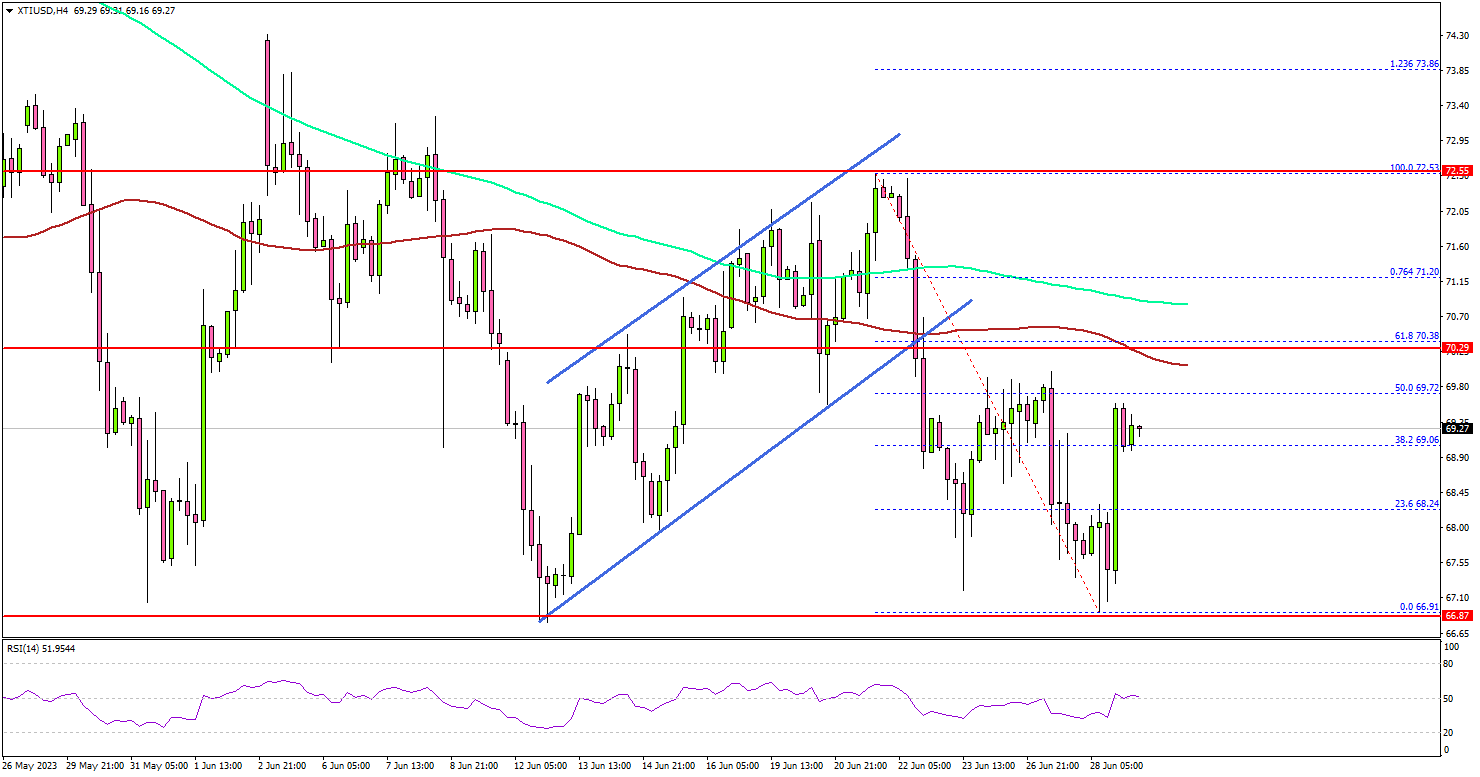

Crude Oil Price Stuck In Crucial Range Below $72

Key Highlights

- Crude oil price retested the key $66.90 support zone.

- A crucial resistance is forming near $70.40 and $71.00 on the 4-hour chart.

- EUR/USD is again struggling to clear the 1.1000 resistance.

- Gold price is slowly moving lower toward $1,880.

Crude Oil Price Technical Analysis

Crude oil price failed to clear the $72 range resistance against the US Dollar. The price started a fresh decline and traded below the $70.40 support.

Looking at the 4-hour chart of XTI/USD, the price settled below the $70.00 level, the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

It retested the $66.90 support zone. The price is now attempting a fresh increase above the $68.00 level. There was a move above the 23.6% Fib retracement level of the recent decline from the $72.53 swing high to the $66.91 low.

On the upside, the first major resistance is near the $70.40 level and the 100 simple moving average (red, 4-hour). It is close to the 50% Fib retracement level of the recent decline from the $72.53 swing high to the $66.91 low, above which the price may perhaps accelerate higher.

On the downside, initial support is near the $68.00 level. The next major support sits near the $66.90 level. Any more losses might call for a test of the $65.00 support zone in the coming days.

Looking at Gold price, the bears are still in action and there are chances of a move toward the $1,880 support zone in the coming sessions.

Economic Releases to Watch Today

- US Initial Jobless Claims - Forecast 265K, versus 264K previous.

- US Gross Domestic Product for Q1 2023 (Preliminary) – Forecast 1.3% versus previous 1.3%.

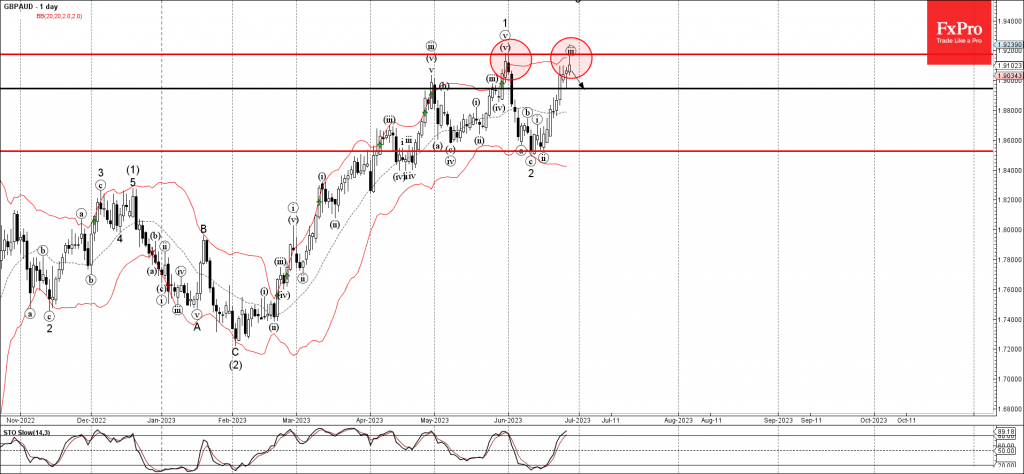

GBPAUD Wave Analysis

- GBPAUD reversed from resistance level 1.9175

- Likely to fall to support level 1.8945

GBPAUD currency pair recently reversed down from the pivotal resistance level 1.9175 (top of the previous impulse wave 1 from the end of May) standing near the upper daily Bollinger Band.

The downward reversal from the resistance level 1.9175 created the daily Japanese candlesticks reversal pattern Shooting Star, which stopped the previous short-term impulse wave 3.

Given the overbought daily Stochastic, GBPAUD currency pair can be expected to fall further toward the next support level 1.8945.

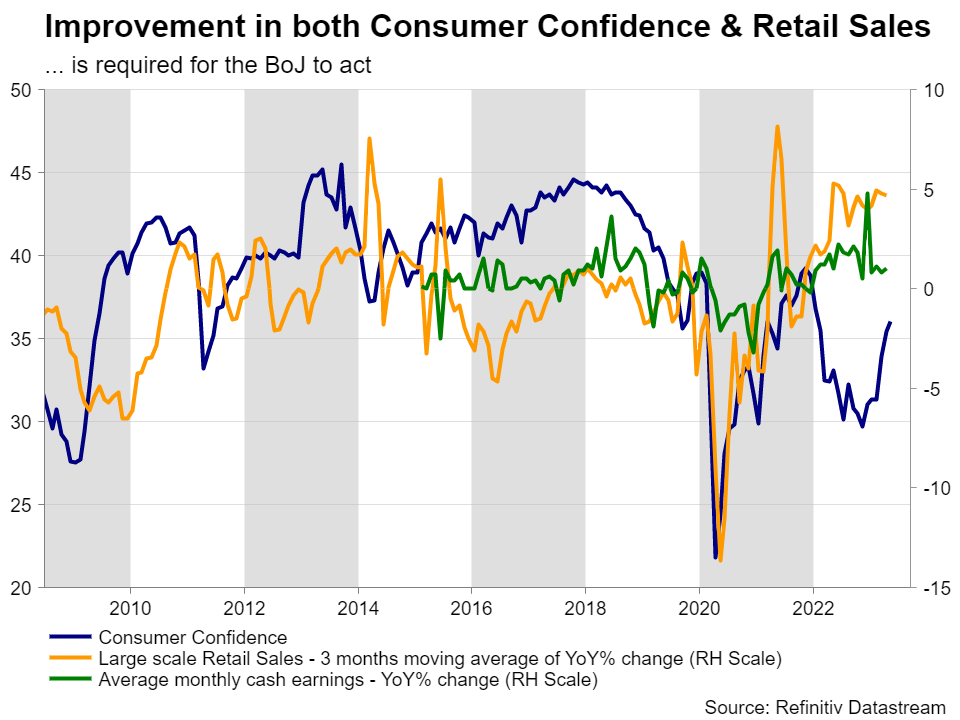

Key Japanese Data This Week But Market’s Mind Already on Next BoJ Meeting

Despite the quiet start of Governor Ueda’s term, there are some expectations being built up for the BoJ’s July meeting. This week’s data prints could, on the margin, tip the balance in favour of some sort of policy announcement at the next meeting. Will these developments, though, allow the yen to finally record some gains against the pound?

What has been happening lately?

The continued underperformance of the yen against major currencies is getting increased airtime. With the outright levels close to multi-year highs, the pace of the recent price action is flashing red. After years of strong cooperation between the then PM Abe and Governor Kuroda, the current situation is clearly a test of the developing relationship of the new leadership at the BoJ and the Japanese finance ministry. While the latter is performing the actual intervention, it is known that the BoJ has an active role in the discussion.

Despite the negative implications on the business environment, the weaker yen is helping the BoJ in its inflation-creation challenge. Imported inflation has helped the national CPI to remain above 3% for the past 10 months. BoJ members have repeatedly commented on the nature of current inflation – i.e. supply side pressures – and the need for inflation to become a demand issue. Until this happens though, they are happy to accept the higher CPI prints and hope that these elevated inflation figures become imprinted on the public’s mind.

The BoJ would clearly love to start scaling back its ample monetary policy stance by curtailing its yield curve framework, and eventually announcing a rate increase. This is also an alternative way of supporting the ailing currency and avoiding a costly intervention. In addition, currency interventions are strongly criticized by other G20 members although Japan, amidst its decade-long fight against deflation, is usually not scolded. However, the BoJ needs sufficient evidence to support a policy announcement. The recent Summary of Opinions opened the door to a likely announcement at the July meeting, but data prints and the inflation outlook will eventually dictate BoJ’s reaction.

Retail sales and consumer confidence in the spotlight

On Thursday morning, we will get two important consumer sector indicators. Looking at the details of the stellar GDP print for Q1, private consumption was again lagging behind other sectors, despite the recent positive run of both the retail sales figures and consumer confidence. Another strong set of data this week would probably cement the recent strength in consumer spending, and create hopes for a long-lasting positive trend in this sector after the stronger wage agreements in April 2023.

Tokyo CPI ready to leapfrog

More importantly, on Friday we will get the June Tokyo headline and core CPI figures, an early preview of the current national inflation pressures. The market is looking for a sizeable increase in both indicators with the core index, excluding food and energy, seen jumping for the first time above 4%. Confirmation of these forecasts will most likely have a ripple effect across the market and give a significant boost to BoJ expectations.

Pound/yen at 7.5-year high

The unexpected strength of the pound during 2023, despite the BoE’s muted monetary policy response, and the continued yen weakness seen across the board has pushed the pound/yen pair to a 7.5-year high. The overall technical picture is not positive for the yen, but there are some early rally-exhaustion signs in the momentum indicators. Naturally, a stronger set of data this week has the potential to cause a small correction in this pair, which could gain further traction if the April 9, 2001 high of 181.42 is easily broken.

Central bank leaders signal continued inflation battle

In an engaging dialogue at ECB forum, central bank leaders from across the globe hinted at the ongoing struggle against inflation, with an emphasis on the need for continued restrictive monetary policy.

Christine Lagarde, President of ECB, highlighted the necessity of sustained effort in the face of inflation, saying, "We still have more ground to cover." She underlined the lack of "tangible evidence" that domestic prices, a key indicator of underlying inflation, were stabilizing and starting to fall.

Meanwhile, Fed Chair Jerome Powell echoed this sentiment, asserting that, despite the current restrictive stance, monetary policy "may not be restrictive enough and it has not been restrictive for long enough." Leaving the door open for consecutive rate hikes, he said, "I wouldn't take moving in consecutive meetings off the table at all."

Andrew Bailey, Governor of BoE, justified last week's significant 50 basis point rate hike, attributing it to the persistence of inflation and labor market pressures. He stated, "The cumulative data... caused us to conclude that we had to make really quite a strong move."

On the other hand, Kazuo Ueda, Governor of BoJ, projected a temporary slowdown in inflation due to diminishing effects of past import price increases. However, he forecasted an inflation uptick into 2024, albeit admitting less confidence about this second phase. Ueda mentioned that confirmation of this second inflationary surge could be a "good reason to shift policy."

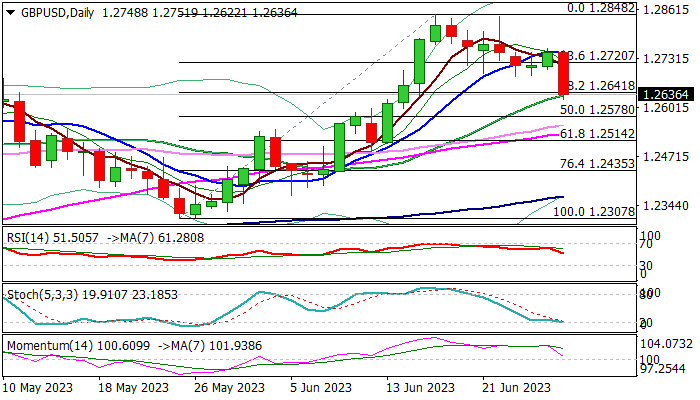

GBP/USD: Cable Loses Ground and Dips Nearly 1%

Cable was sharply down on Wednesday, losing 0.9% until early US session, as pound was weaker against all major counterparts.

Fresh bears broke below the floor of the recent range (1.2684) and cracked key near-term supports at 1.2641/34 (Fibo 38.2% of 1.2307/1.2848 / rising 20DMA).

Firm break of these levels would generate bearish signal for deeper pullback from new 2023 high (1.2848), left after larger bulls stalled under strong barriers, provided by 200WMA and monthly Ichimoku cloud base.

Sharp loss of bullish momentum weakens the structure on daily chart, increasing risk of deeper pullback, which could be triggered on firm break of 1.2641/34 pivots.

Daily Kijun-sen and 50% retracement of 1.2307/1.2848, mark next significant support at 1.2578, followed by Fibo 61.8% (1.2514) and top of thinning daily cloud at 1.2485.

Broken range floor (1.2684) reverted to resistance which should limit upticks and keep near-term bias with bears.

Res: 1.2684; 1.2720; 1.2735; 1.2759.

Sup: 1.2600; 1.2578; 1.2530; 1.2514.