Sample Category Title

UK CPI unchanged at 8.7% yoy in May, core CPI rose to 7.1% yoy

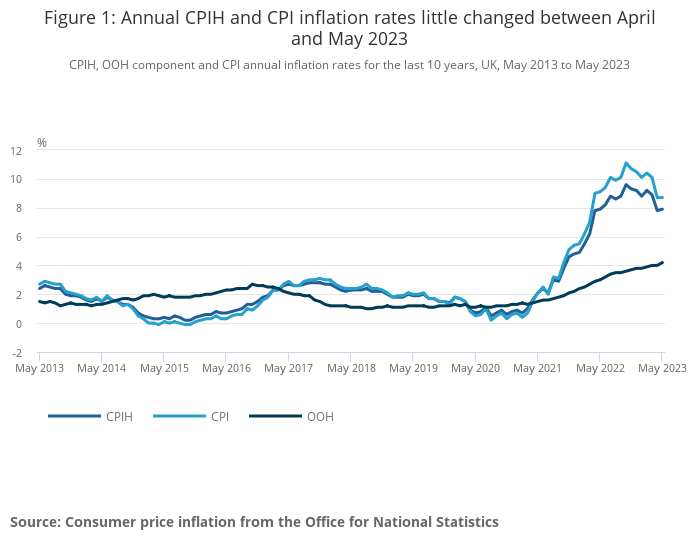

UK annual CPI was unchanged at 8.7% yoy in May, above expectation of 8.5% yoy. Core CPI (excluding energy, food, alcohol and tobacco) accelerated to 7.1% yoy, up from prior month's 6.8% yoy, and the highest rate since March 1992. CPI goods eased from 10.0% yoy to 9.7% yoy. But CPI services rose from 6.9% yoy to 7.4% yoy. For the month, CPI rose 0.7% mom, slowed from April's 1.2% mom, but was well above expectation of 0.4% mom.

Also released. RPI ticked down from 11.4% yoy to 11.3% yoy, above expectation of 11.1% yoy. PPI input came in at -1.5% mom, 0.5% yoy, versus expectation of -0.6% mom, 1.2% yoy. PPI output was at -0.5% mom, 2.9% yoy, versus expectation of -0.1% mom, 3.6% yoy. PPI output core was at -0.3% mom, 4.1% yoy, versus expectation of 0.1% mom, 4.7% yoy.

Australia’s Westpac leading index fell to -1.09%, weakness to extend into 2024

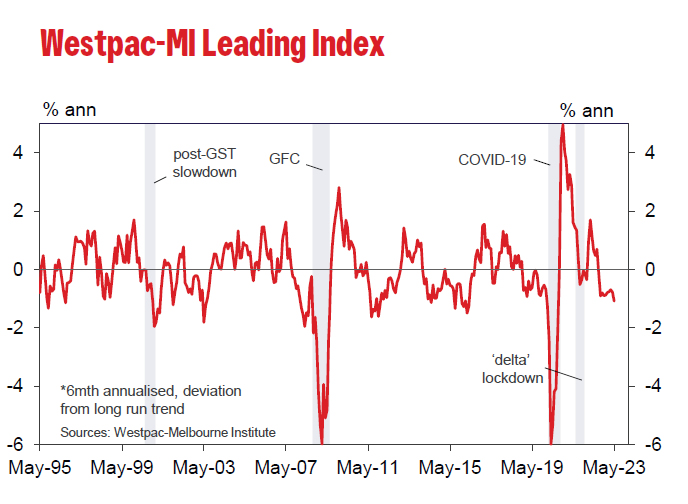

Australia Westpac Leading Index growth rate fell from -0.78% to -1.09% in May. This is the lowest read of the growth rate since the pandemic. The tenth consecutive negative print for the index. The negative Index growth rates point to below-trend economic growth.

Westpac expects the weakness to extend through 2023 and into 2024. Westpac recently revised down growth forecast 2023 and 2024, from 1% and 1.5% to 0.6% and 1.0% respectively. This weakness in the economy is centred around consumers but also reflects slowing global economy; downturn in dwelling construction; and progressive weakening in labour market.

Regarding RBA policy, Westpac expects the central bank to raise cash rate by a further 0.25% at July 4 meeting. "As we saw at the June Board meeting, we expect that the July meeting will see these considerations of inflation risks again overriding concerns about the poor growth outlook."

BoJ Adachi: Appropriate to continue monetary easing with YCC

BoJ board member Seiji Adachi voiced support for continued monetary easing amid a climate of significant uncertainty regarding price outlook. Adachi relayed these views during a discussion with business leaders in Kagoshima.

Adachi said, "My view is that it's appropriate to continue monetary easing with the yield curve control framework." He added, "The shape of the yield curve has become smooth overall and there is improvement in market functioning."

"Amid huge uncertainty over the price outlook, there are upside and downside risks. In the long run, however, the downside risks appear to be larger," he warned. These risks, according to Adachi, must be carefully considered when deciding on changes to monetary policy.

Adachi also noted an interesting shift in public's perception of inflation, suggesting that Japan's long-standing deflationary mindset is starting to change. "We're seeing some changes in the public's deflationary mindset, or the perception that prices won't rise," he said.

"In a sense, we're moving closer to achieving our price target. But there's high uncertainty over our baseline inflation outlook, so it's premature to tweak monetary policy," Adachi concluded.

Fed nominees Jefferson, Cook and Kugler prioritize tackling inflation

Three nominees for key roles at Fed, including two sitting Fed Governors, have pledged to make tackling inflation their primary concern if their nominations are confirmed. This commitment was made in prepared remarks ahead of confirmation hearings before Senate Banking Committee on Wednesday.

Philip Jefferson, the nominee for vice chair, recognized the multifaceted challenges facing the economy including inflation, banking-sector stress, and geopolitical instability. Jefferson said, "The Federal Reserve must remain attentive to them all. Inflation has started to abate, and I remain focused on returning it to our 2 percent target."

Lisa Cook, who is nominated for a new 14-year term, echoed Jefferson's concerns about inflation. She stated, "The American economy is at a critical juncture, and it will be essential for the FOMC to act as needed to bring inflation back to our 2% inflation target."

Adriana Kugler, the nominee chosen by President Joe Biden to fill the vacancy left by Lael Brainard earlier this year, reiterated the same sentiment. Kugler emphasized, "If confirmed, I am deeply committed to setting monetary policy to reduce inflation and promote maximum employment, and to foster the resilience of the financial sector to support job creation and economic growth."

Can Fed Chair Powell Wake Up Dollar Bulls?

Despite the Fed’s updated dot plot last week signaling that two more rate hikes may be on the cards, market participants are finding it hard to believe it. Fed Chair Powell did not convince them either when he held the press conference following the decision. However, he is being given another opportunity to pass his message this week as he is testifying before Congress on Wednesday and Thursday at 14:00 GMT.

Investors don’t believe the Fed

At last week’s meeting, the Fed decided to hit the pause button, skipping a hike for the first time since March 2022. However, it was more than clear that this was not the end of the tightening crusade, rather than a small break to evaluate incoming data and how prior increases may have affected the world’s largest economy. After all, the updated ‘dot plot’ pointed to 50bps worth of additional rate hikes later this year before the end credits roll.

Having said that though, market participants remained unconvinced that this could be the case, continuing to price in only one more quarter-point hike and a series of rate cuts through next year, despite Fed Chair Powell saying at the press conference that any rate cuts are “a couple of years out.”

Powell gets a second chance to pass the message

This week, Chair Powell will have another opportunity to convince the financial community about the Committee’s intentions, on Wednesday and Thursday, when he is testifying before Congress. With the PMIs suggesting easing price pressures, the CPI slowing faster than expected, and wage growth softening as well, it may be hard for the Fed Chief to find convincing arguments regarding the need for two additional rate hikes. After all, the full effect of the prior increases is not fully felt by the economy yet.

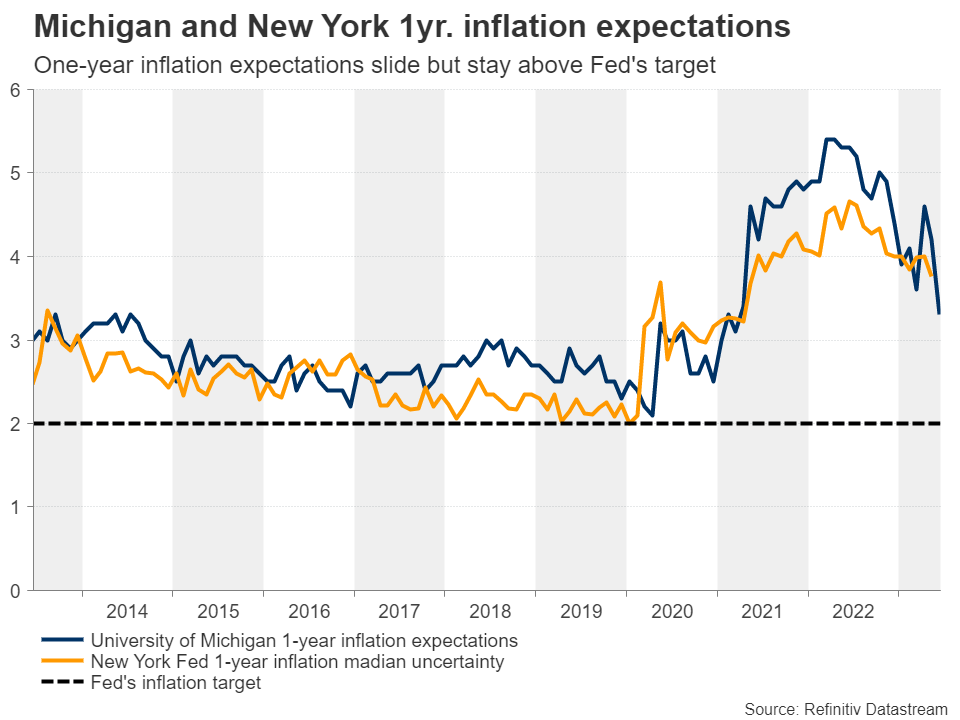

A relatively reasonable argument may be that, despite also sliding notably, inflation expectations suggest that in a year’s time, inflation will still be above the Fed’s 2% target. The University of Michigan is calculating a 3.3% y/y rate for next June, while the New York Fed model is pointing to a higher 3.76% rate. So, taking these rates as a given, it may be unwise for the Fed to start cutting rates massively next year.

Dollar could gain, but bullish reversal still premature

So, if Powell highlights the need for higher-for-longer rates because there is still a long way to go before the job is done, the dollar could gain and equities could correct lower. Nevertheless, with inflation expectations not being an accurate forecasting tool, but rather a comparison tool and a moving untouchable target, calling for a bullish trend in the dollar would still be premature.

Incoming data pointing to further cooling of price pressures could translate into further declines in inflation expectations and perhaps allow market participants to maintain their rate-cut bets for early next year. Currently, conditional upon a July or September hike, they even see more than 50bps worth of reductions by next May.

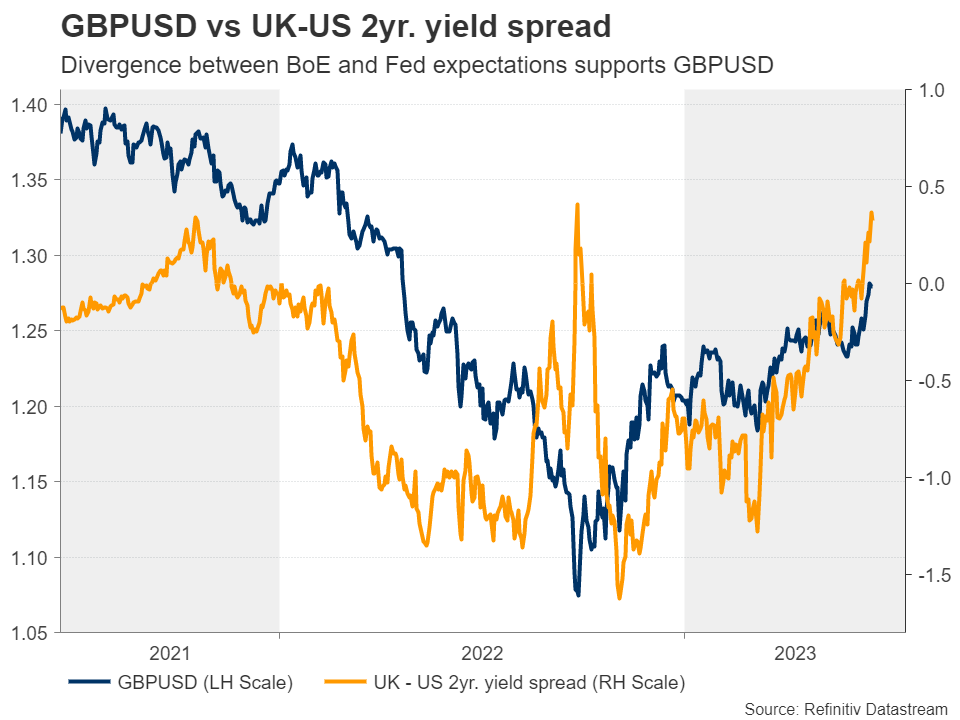

With the BoE expected to deliver 140bps worth of additional rate hikes, Fed cut bets are likely to keep pound/dollar in an uptrend for a while longer, especially if UK policymakers adopt a more aggressive stance when they meet on Thursday.

Pound/dollar uptrend may be destined to continue

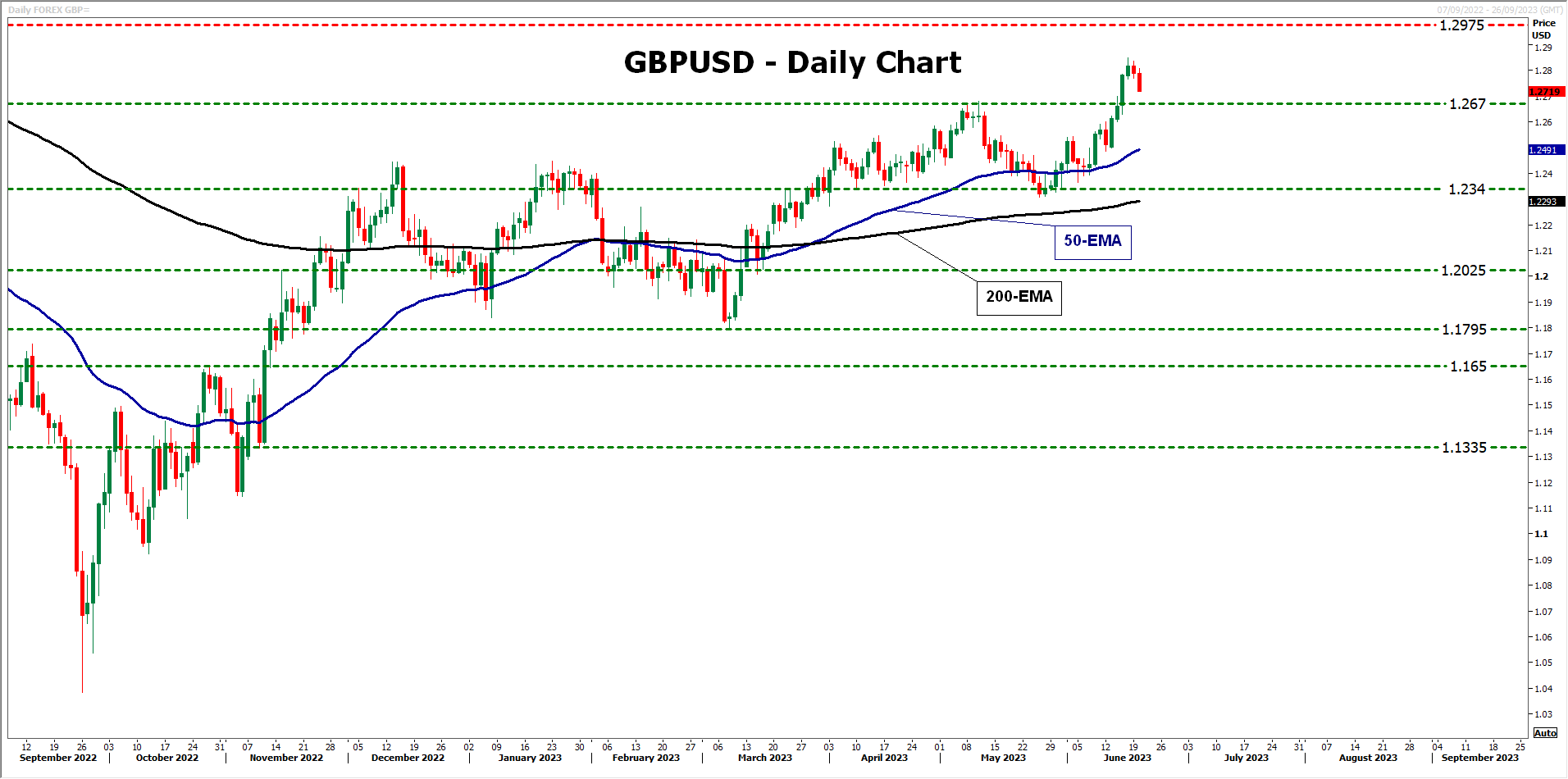

Just last Thursday, Cable emerged above the 1.2670 barrier, which offered resistance on May 10 this year and back on May 27, 2022, confirming a higher high on the daily chart and signaling the continuation of the prevailing medium-term uptrend.

The pair is currently in a sliding mode, but even if it continues for a while longer due to Powell appearing in his hawkish suit, the bulls could recharge from above the key 1.2340 zone and push the pair up again. A potential catalyst for the rebound may be a hawkish BoE on Thursday. The rebound could take the price back above 1.2670 and perhaps aim for the 1.2975 zone, which acted as key support between March and April 2022.

Now, if pound/dollar falls below 1.2340, it will enter its flat zone and thus, the outlook may be considered neutral. For the picture to turn bearish, a break below 1.1795 may be required. Such a dip could initially target the 1.1650 level, the break of which could see scope for declines towards the low of November 9 at 1.1335.

Bitcoin Price Rallies After Crucial Bullish Breakout

Key Highlights

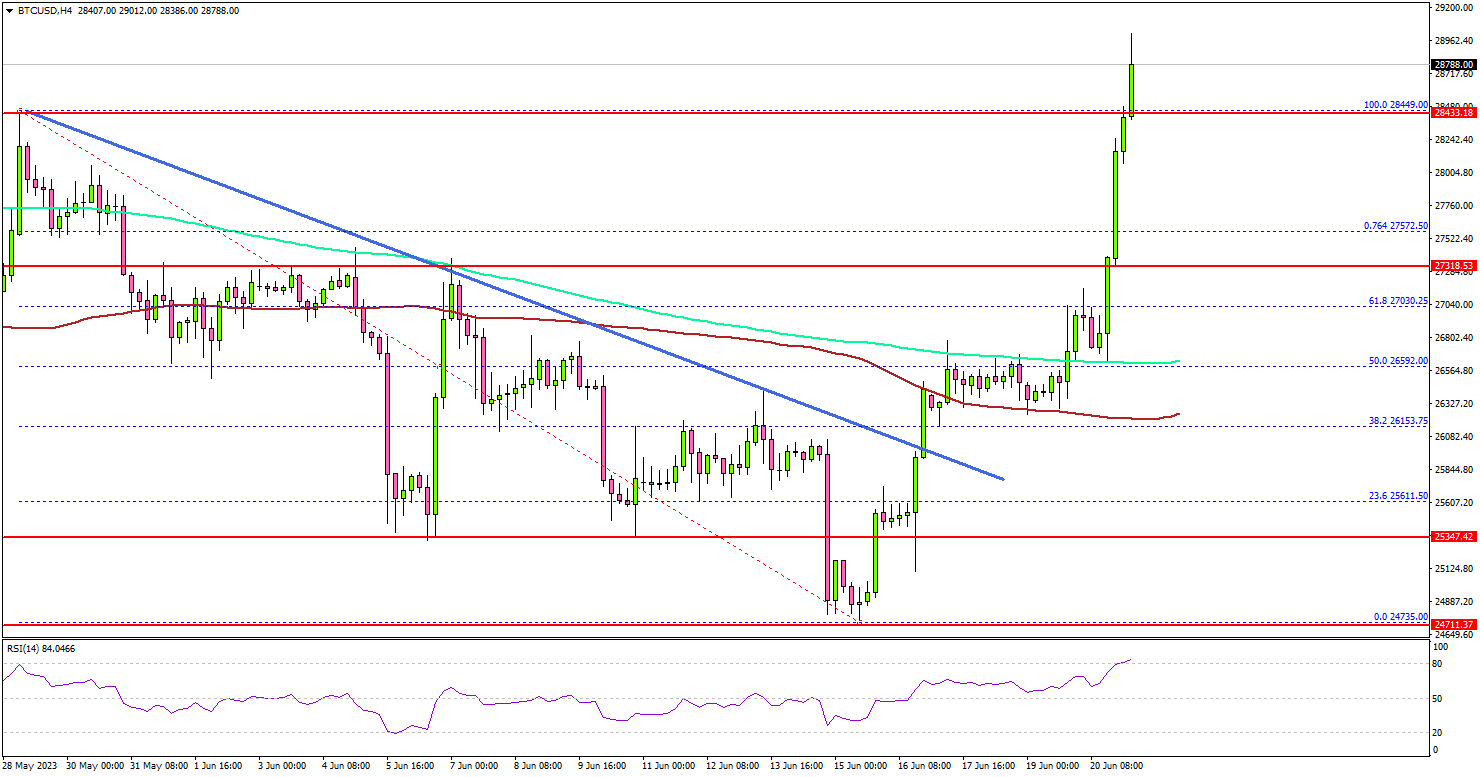

- Bitcoin price is gaining pace above $27,500.

- BTC broke a major bearish trend line with resistance at $25,900 on the 4-hour chart.

- EUR/USD is consolidating gains above the 1.0880 support.

- The UK Consumer Price Index could decline from 8.7% to 8.4% in May 2023 (YoY).

Bitcoin Price Technical Analysis

Bitcoin price started a recovery wave from the $24,750 zone. BTC/USD climbed higher above the $26,500 and $27,000 resistance levels.

Looking at the 4-hour chart, the price was able to surpass the $26,500 resistance zone and a major bearish trend line with resistance at $25,900.

There was a clear move above the 61.8% Fib retracement level of the downward move from the $28,449 swing high to the $24,735 low. It is now trading above the 100 simple moving average (red, 4 hours) and the 200 simple moving average (green, 4 hours).

On the upside, the price is facing resistance near the $29,000 level. The first major resistance is near the $29,200 level (a multi-touch zone).

A successful close above the $29,200 level might spark another bullish wave. In the stated case, the price may perhaps rise toward the $30,000 level.

If not, Bitcoin might decline again and trade below the $27,500 support. The next major support is near the $27,200 level. If there is a downside break and a close below $27,200, Bitcoin might revisit the $26,000 zone in the coming days.

Economic Releases

- UK Consumer Price Index for May 2023 (YoY) – Forecast +8.4%, versus +8.7% previous.

- UK Core Consumer Price Index for May 2023 (YoY) – Forecast +6.8%, versus +6.8% previous.

- Federal Reserve Chair Jerome Powell testifies before Congress.

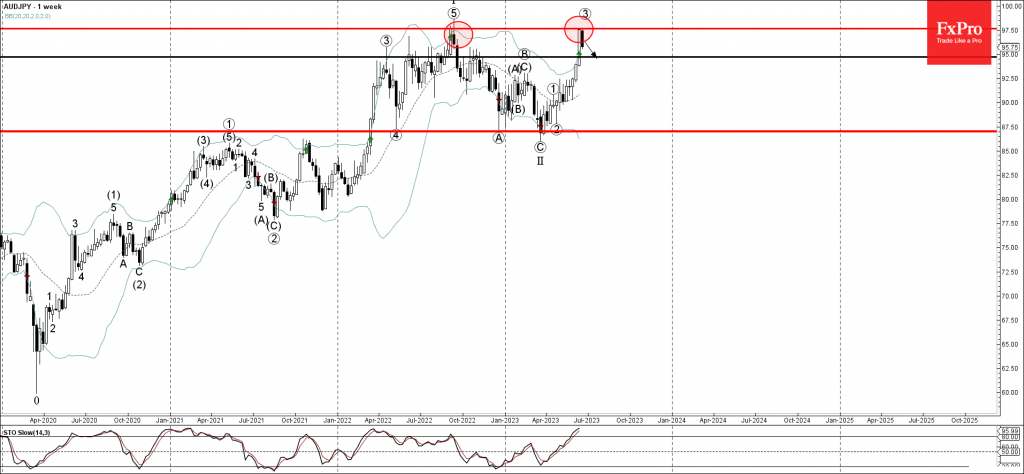

AUDJPY Wave Analysis

- AUDJPY reversed from resistance level 97.50

- Likely to fall to support level 95.00

AUDJPY currency pair recently reversed down from the resistance level 97.50, which stopped the weekly uptrend in the middle of last year.

The downward reversal from the resistance level 97.50 stopped the previous weekly upward impulse sequence from March .

Given the strength of the resistance level 97.50 and the overbought weekly Stochastic, AUDJPY can be expected to correct down further to the next string support level 95.00.

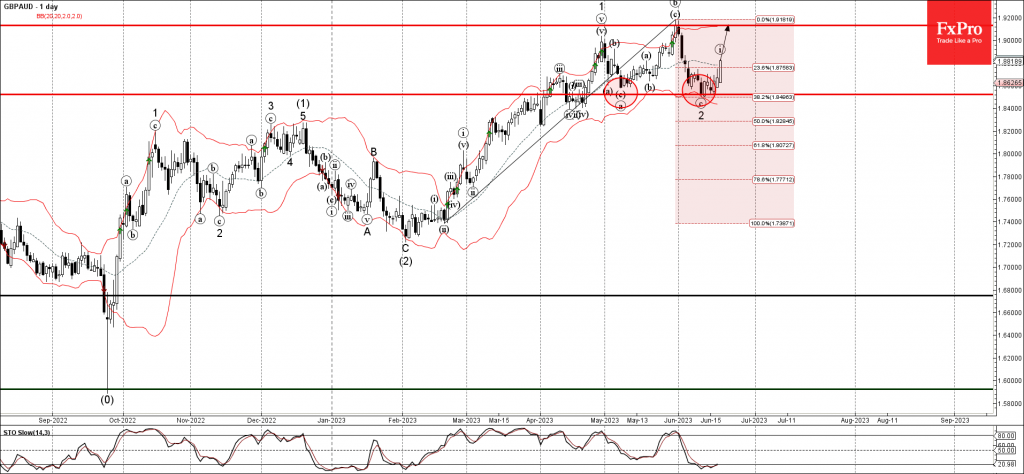

GBPAUD Wave Analysis

- GBPAUD rising inside impulse wave 3

- Likely to reach resistance level 1.9130

GBPAUD currency pair continues to rise inside the minor impulse wave 3, which started earlier with the daily Bullish Engulfing from the support level 1.8525.

The active minor impulse wave 3 belongs to the intermediate impulse sequence (3) from February.

Given the prevailing uptrend, GBPAUD can be expected to rise further toward the next resistance level 1.9130 (which stopped the previous impulse wave (c) at the end of last month).

SNB to Raise Rates, But Will It Be Enough to Lift the Franc?

The Swiss National Bank (SNB) is widely expected to raise interest rates at 07:30 GMT Thursday, although markets are divided about the size of the move. With inflation grinding lower, the risks seem tilted towards a smaller rate increase that could briefly hurt the Swiss franc, although its overall path will also depend on global risk appetite and FX interventions.

Inflation cools

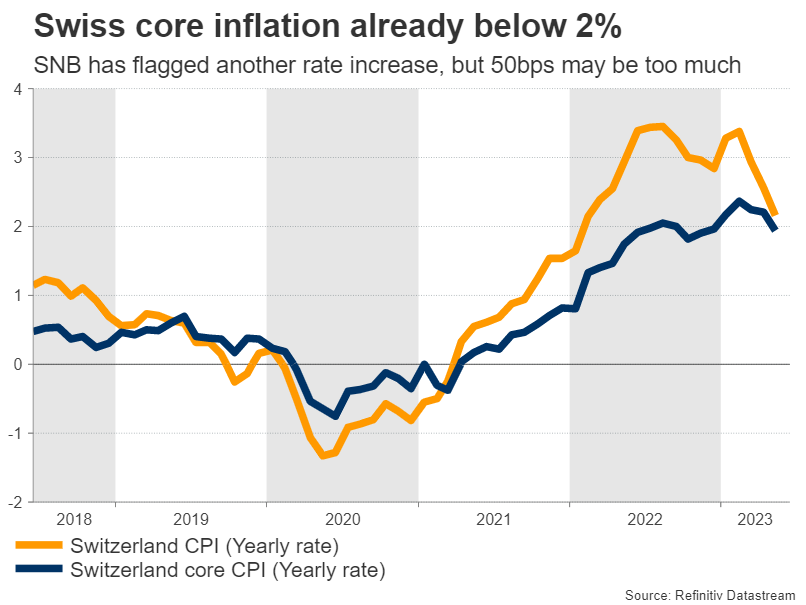

Switzerland's economy has been flashing some encouraging signals lately. Economic growth was surprisingly strong in the first quarter of the year, the unemployment rate is near its lowest levels in two decades, and inflation has been falling steadily to reach just 2.2% in May.

The SNB aims to keep inflation positive but below 2%, so it would seem the mission has almost been accomplished. Nonetheless, the latest comments from SNB officials suggest otherwise. Speaking last week, Chairman Thomas Jordan stressed that more rate increases might be required to tackle 'stubborn' inflation.

One concern is that inflation could heat up again later this year, as rent prices play catch-up with previous increases in house prices. Another risk is that the longer inflation remains above 2%, the more likely that the inflationary mindset becomes entrenched in consumer and business decisions.

By raising rates further, the SNB can address these threats and equip itself with more 'ammunition' to fight the next downturn, as it would have more scope to cut rates and help the economy if it runs into trouble.

Single or double move?

The problem is that raising rates too much can also inflict damage on economic growth, making it a double-edged sword. There are already signs that economic momentum has started to slow as Switzerland's manufacturing sector is in contraction, and the Credit Suisse episode certainly did not help.

Hence, markets are split on the size of the upcoming rate hike, pricing in a 60% probability for a 50bps rate increase and a 40% chance for a smaller 25bps move. Since the SNB gathers only four times per year, there's a sense it might 'frontload' the rate increases and deliver a larger move.

It's a close call, but considering the progress on inflation lately, it seems more prudent from a risk-management perspective for the SNB to go for the smaller hike of 25bps, especially following a similar downshift from the European Central Bank last week.

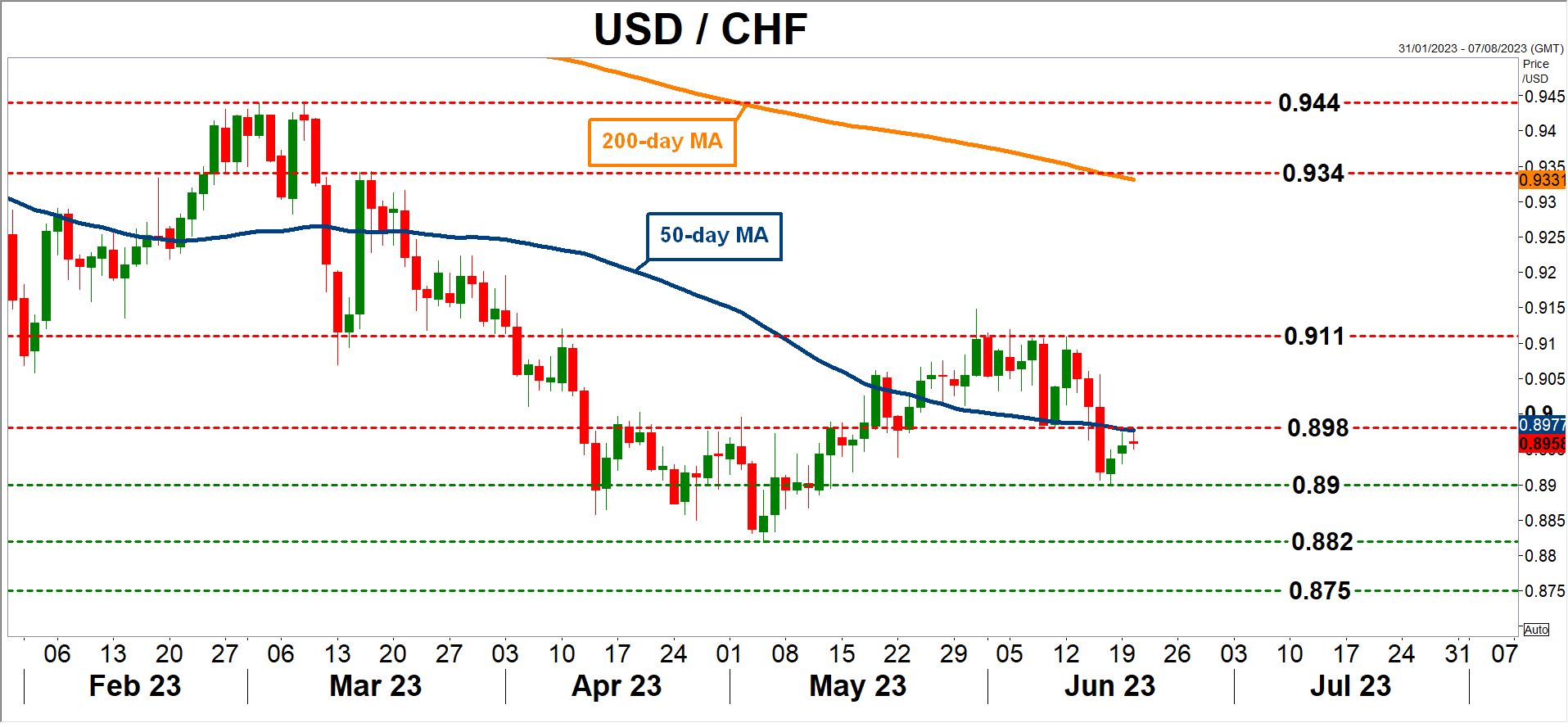

Such a decision could spell bad news for the Swiss franc, at least initially. Turning to the dollar/franc chart, a potential move higher might encounter immediate resistance near 0.8980, which is where the 50-day moving average has converged. A break higher would open the door towards the 0.9110 region.

On the flipside, a 50bps rate hike could trigger the opposite response, sending dollar/franc lower for another test of the 0.8900 zone. If violated, the spotlight would turn to the May low of 0.8820.

The big picture

Looking beyond this rate decision, the broader outlook for the Swiss franc seems rather bright. Even though the SNB has not raised rates as much as other central banks, at least the franc is not haunted by negative rates anymore.

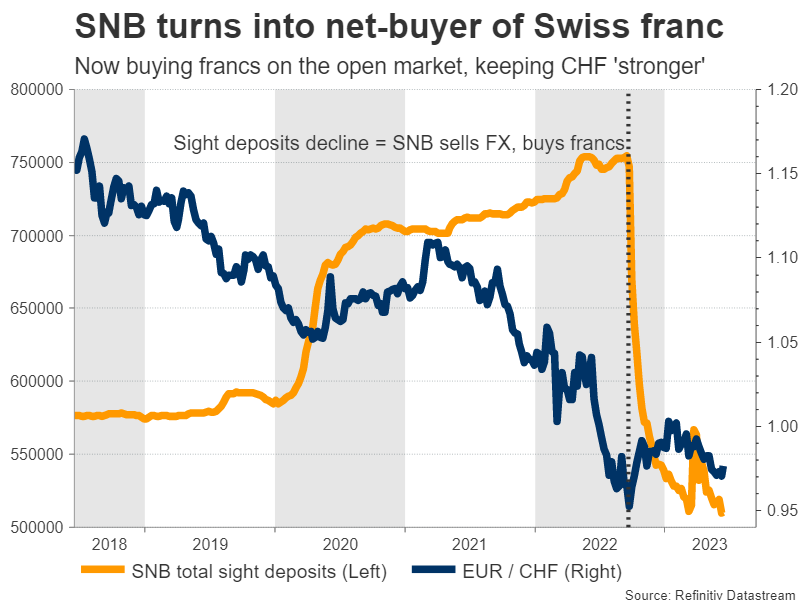

Even more importantly, the SNB has flipped from a net-seller of the franc to a net-buyer. The latest data on sight deposits suggest the SNB still intervenes in the FX market, but it is now actively buying francs and selling foreign currencies. The goal is to keep the currency 'strong' and in the process, keep imported inflation under control.

Finally, there's global risk sentiment to consider, as the franc is a safe haven instrument. If the recent euphoria in riskier assets calms down and concerns about a global economic slowdown resurface later this year, that could be another beneficial force for the defensive currency.