Sample Category Title

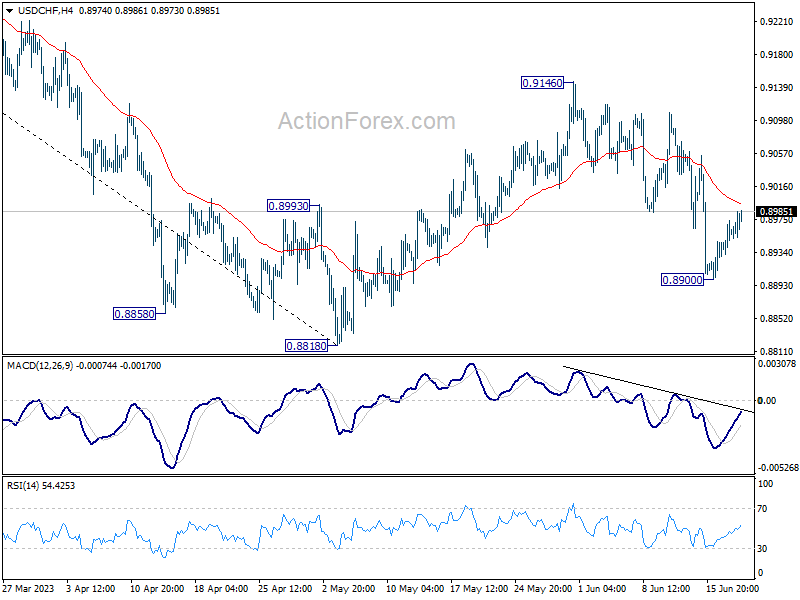

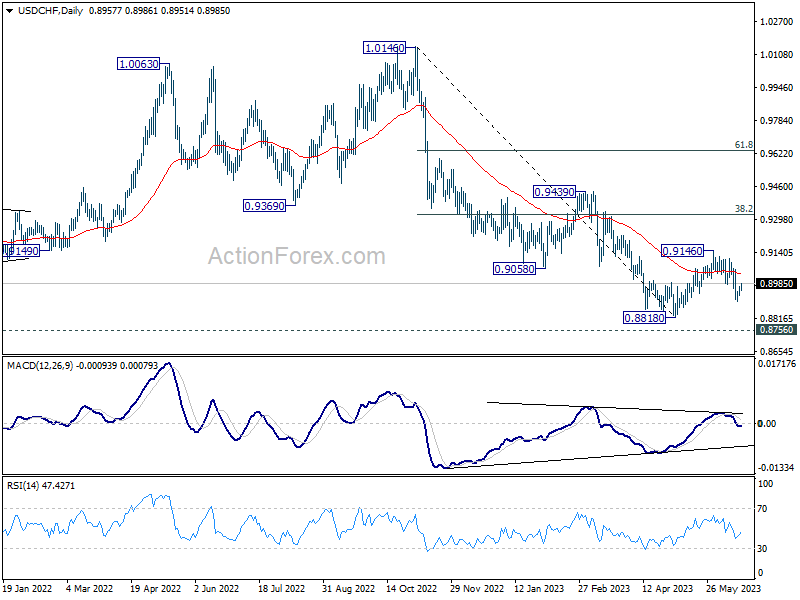

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8934; (P) 0.8954; (R1) 0.8978; More...

Intraday bias in USD/CHF remains neutral but risk also stays on the downside as long as 0.9146 resistance holds. Below 0.8900 will target 0.8818 and possibly below. But strong support is still expected from 0.8756 to bring reversal.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.61; (P) 141.83; (R1) 142.23; More...

Intraday bias in USD/JPY is turned neutral with current retreat and some consolidations should be seen. On the upside, sustained trading above 61.8% retracement of 151.93 to 127.20 at 142.48 will pave the way back to retest 151.93 high. However, rejection by 142.48, followed by break of 139.27 will indicate short term topping and turn bias back to the downside.

In the bigger picture, rise from 151.93 are seen as a corrective pattern to up trend from 102.58. The first leg has completed at 127.20. Rebound from there is seen as the second leg, and should be limited below 151.93. Sustained trading below 55 D EMA (now at 137.47) will argue that the third leg has started back to 127.20 and possibly below.

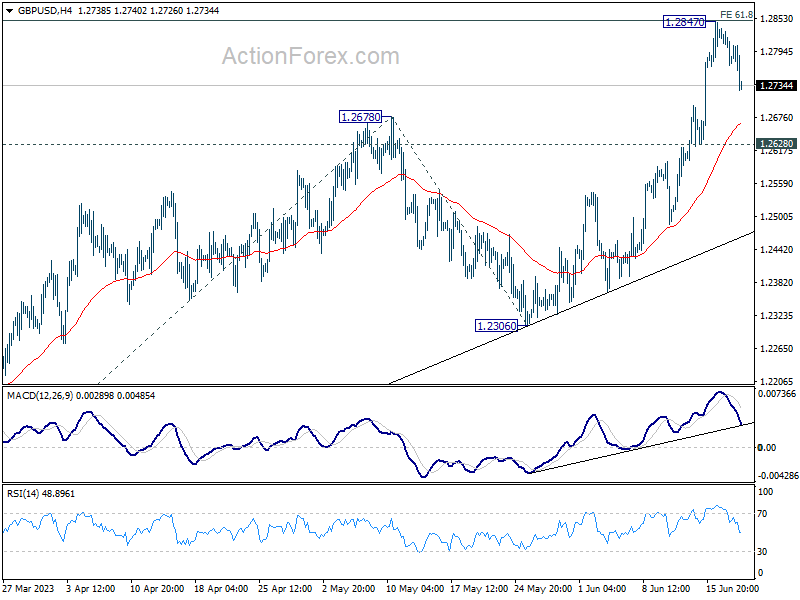

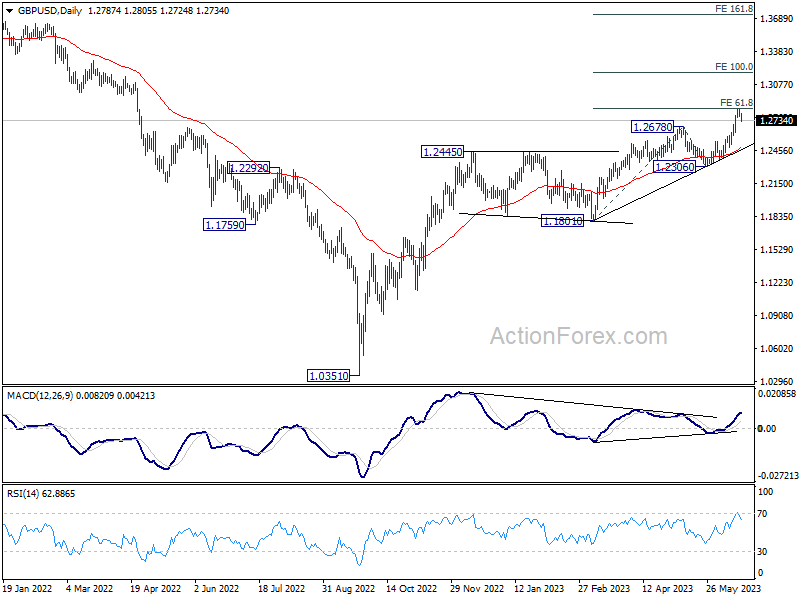

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2764; (P) 1.2801; (R1) 1.2830; More...

GBP/USD's retreat from 1.2847 extends lower today but stays well above 1.2628 support. Intraday bias remains neutral first and further rally is expected. On the upside, firm break of 1.2847 will resume larger up trend and target 100% projection of 1.1801 to 1.2678 from 1.2306 at 1.3183 next.

In the bigger picture, the strong support from 55 W EMA (now at 1.2345) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

Dollar and Yen Rebound Gains A Little Momentum in Listless Markets

As US trading session commences, rebounds of Dollar and Yen seem to be gathering a bit more some steam. The broader financial market appears to be rather listless today, with major European indices roughly flat and US futures slightly down. There's also no unified movement in the U.S. and European benchmark treasury yields. Investors appear to be holding their bets ahead of key events tomorrow, namely UK CPI data and Fed Jerome Powell's testimony, then BoE and SNB rate decisions the day after.

For now, Yen, Euro and Dollar are the stronger ones for the day. Australian Dollar is the worst performer after RBA minutes raised some doubts on July rate hike. Aussie is followed by Kiwi and then Sterling, in a mild risk aversion environment. Swiss Franc and Canadian Dollar are mixed.

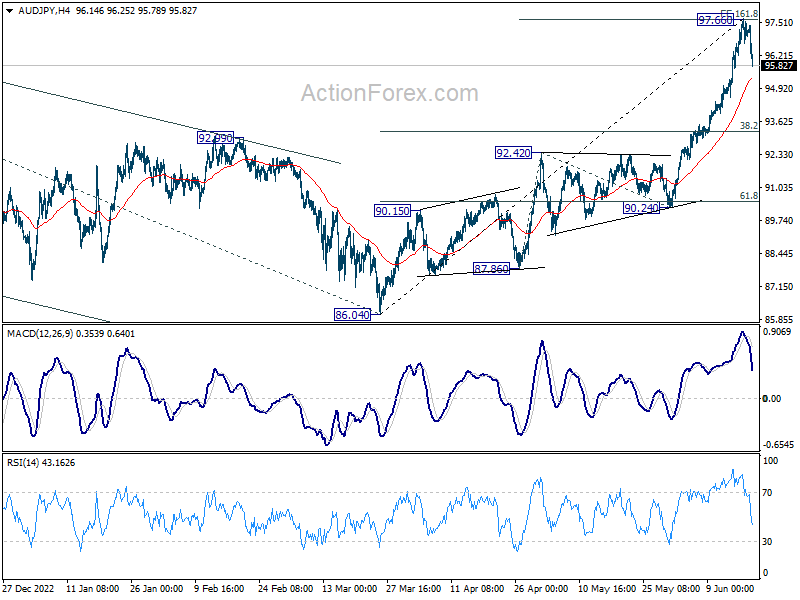

Technically, AUD/JPY should have now turn into a corrective phase with today's pull back. The question is on whether it's correcting the whole rise from 86.04. It's possible that such rally has completed a five-wave sequence after meeting 161.8% projection of 87.86 to 92.42 from 90.24 at 97.61. If that's the case, AUD/JPY could easily dive through 55 4H EMA (now at 95.27) to 38.2% retracement of 86.04 to 97.66 at 93.22. Let's see how AUD/JPY reacts to the EMA and we'll know quickly.

In Europe, at the time of writing, FTSE is up 0.14%. DAX is down -0.16%. CAC is up 0.11%. Germany 10-year yield is down -0.0771 at 2.442. Earlier in Asia, Nikkei rose 0.06%. Hong Kong HSI dropped -1.54%. China Shanghai SSE fell -0.47%. Singapore Strait Times lost -0.65%. Japan 10-year JGB yield declined -0.0052 to 0.390.

ECB Rehn: Inflation excluding energy and food is falling only gradually

ECB Governing Council member Olli Rehn has underscored the significance of core inflation in guiding the bank's monetary-policy decisions. His comments comes at a time when consumer prices in eurozone are reportedly slowing, but not at the desired pace.

Rehn stated, "The rise in consumer prices in the euro area is slowing, but not to the extent desired," further adding, "Inflation excluding energy and food is falling only gradually."

Highlighting the primacy of core inflation – which excludes the volatile sectors of energy and food – in policy considerations, Rehn remarked, "I consider core inflation a very important, essential yardstick in the overall judgment of monetary-policy making."

Rehn emphasized ECB's commitment to bringing inflation back to its target, saying, "We will bring interest rates to levels sufficiently restrictive to achieve a timely return of inflation to the 2% medium-term target and keep them there as long as necessary."

RBA minutes: Finely balanced arguments for hold and hike

Minutes from RBA's June 6 monetary policy meeting reveal an active debate over whether to hold or raise the cash rate by 25bps.

As stated in the minutes, "Members recognised the strength of both sets of arguments, concluding that the arguments were finely balanced." However, they ultimately determined that a rate increase was the stronger course of action at this meeting.

Recent data indicating that inflation risks had begun tilting to the upside were a key influence on the board's decision. As they noted, "Given this shift and the already drawn-out return of inflation to target, the Board judged that a further increase in interest rates was warranted."

Such a move would bolster confidence that inflation would indeed return to the target range "over the period ahead", they reasoned.

At the meeting, RBA raised cash rate target by 25bps to 4.10%.

RBA Bullock: Economy needs to grow at a below trend pace for a while

In a speech, RBA Deputy Governor Michele Bullock noted the economy needs to "grow at a below trend pace for a while" to bring demand and supply into better balance. Only that will give "the greatest chance of securing sustainable full employment into the future."

Bullock explained, "For monetary policy... We think of full employment as the point at which there is a balance between demand and supply in the labour market (and in the markets for goods and services) with inflation at the inflation target."

"In recent months, the balance between labour demand and supply has improved somewhat," she noted. "Nevertheless, the labour market remains tight."

Also, "for the first time in decades, firms' demand for labour exceeds the amount of labour that people are willing and able to

"At the same time, with demand for goods and services high relative to the economy's capacity to supply those things, inflation is well above the 2–3 per cent target range."

PBoC cuts two key lending rates

China's PBoC executed cuts to two of its pivotal lending rates today, marking the first time such adjustments have been made in 10 months since last August.

The Chinese central bank opted to reduce one-year loan prime rate by -10 bps, taking it down from 3.65% to 3.55%. Concurrently, it also implemented a -10 bps cut to five-year loan prime rate, adjusting it from 4.3% to 4.2%.

These measures follow other recent actions aimed at easing monetary policy. Only last Thursday, PBOC made its first cut to one-year medium-term loan facility in 10 months. Furthermore, the bank reduced its seven-day reverse repurchase rate on the preceding Monday.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2764; (P) 1.2801; (R1) 1.2830; More...

GBP/USD's retreat from 1.2847 extends lower today but stays well above 1.2628 support. Intraday bias remains neutral first and further rally is expected. On the upside, firm break of 1.2847 will resume larger up trend and target 100% projection of 1.1801 to 1.2678 from 1.2306 at 1.3183 next.

In the bigger picture, the strong support from 55 W EMA (now at 1.2345) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Minutes | ||||

| 04:30 | JPY | Industrial Production M/M Apr F | 0.70% | -0.40% | -0.40% | |

| 06:00 | CHF | Trade Balance (CHF) May | 5.48B | 3.45B | 2.60B | 2.56B |

| 06:00 | EUR | Germany PPI M/M May | -1.40% | -0.70% | 0.30% | |

| 06:00 | EUR | Germany PPI Y/Y May | 1.00% | 1.70% | 4.10% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Apr | 4B | 27.3B | 31.2B | |

| 12:30 | USD | Housing Starts May | 1.63M | 1.40M | 1.40M | 1.34M |

| 12:30 | USD | Building Permits May | 1.49M | 1.43M | 1.42M |

ECB Rehn: Inflation excluding energy and food is falling only gradually

ECB Governing Council member Olli Rehn has underscored the significance of core inflation in guiding the bank's monetary-policy decisions. His comments comes at a time when consumer prices in eurozone are reportedly slowing, but not at the desired pace.

Rehn stated, "The rise in consumer prices in the euro area is slowing, but not to the extent desired," further adding, "Inflation excluding energy and food is falling only gradually."

Highlighting the primacy of core inflation – which excludes the volatile sectors of energy and food – in policy considerations, Rehn remarked, "I consider core inflation a very important, essential yardstick in the overall judgment of monetary-policy making."

Rehn emphasized ECB's commitment to bringing inflation back to its target, saying, "We will bring interest rates to levels sufficiently restrictive to achieve a timely return of inflation to the 2% medium-term target and keep them there as long as necessary."

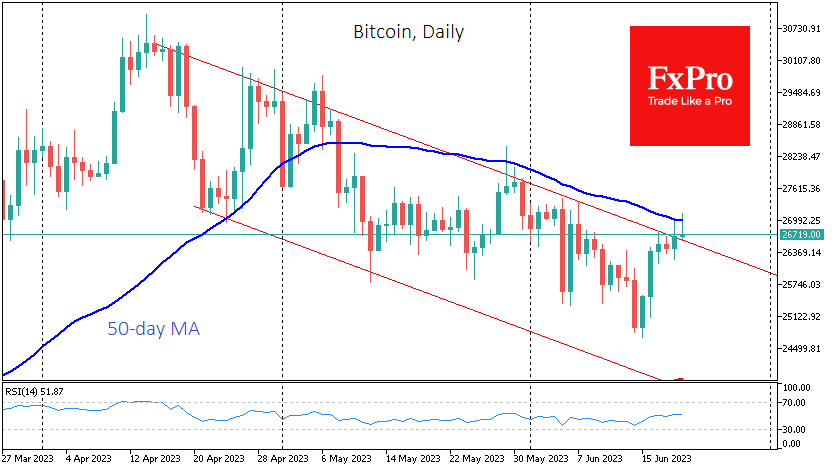

Bitcoin Testing a Downtrend

Market picture

Crypto market capitalisation rose 0.8% to $1.073 trillion, close to its level of 10 days ago. Bitcoin was a major contributor to the rally, rising 1.6% to $28.8K, while Ethereum gained just 0.4% to $1730. Among the top altcoins, Solana (+3.5%) stands out, with other altcoins ranging from -1.2% (XRP) to +1.6% (Polygon).

For the fifth day out of the last six, Bitcoin has breached the upper boundary of its bearish range and tested the 50-day moving average near $27K. Although the price has now breached the channel’s upper boundary, a break of the downtrend cannot be declared until a close above $27.2K, the previous local high, is achieved. A reversal from current levels offers a downside of more than 10% with the potential for a drop to the 200-day moving average.

According to CoinShares, investment in crypto funds fell by a paltry $5 million last week, but net outflows continued for the ninth consecutive week. Retail traders helped push Bitcoin above $26K, according to Glassnode, which noted an increase in activity from addresses controlling between 0.1 and 1 BTC.

News background

MicroStrategy founder Michael Saylor said that recent SEC actions against crypto have made it clear to the industry that it is doomed to be bitcoin-centric. According to him, BTC is the only institutional-level asset.

US crypto payments company Wyre announced it was shutting down after a decade of operation due to difficult bear market conditions. After fintech company Bolt terminated a $1.5bn acquisition agreement in September 2022, the platform was on the brink of bankruptcy.

Ethereum developers discussed details of a future update to the Deneb consensus level during a conference call that will be part of Dencun hard fork. The minimum balance for ETH network validators is proposed to be increased from 32 ETH to 2048 ETH, attempting to improve blockchain efficiency.

The International Monetary Fund (IMF) is working on a global infrastructure for central bank digital currencies (CBDCs) and legislation to control the movement of funds in CBDCs, said IMF chief Kristalina Georgieva.

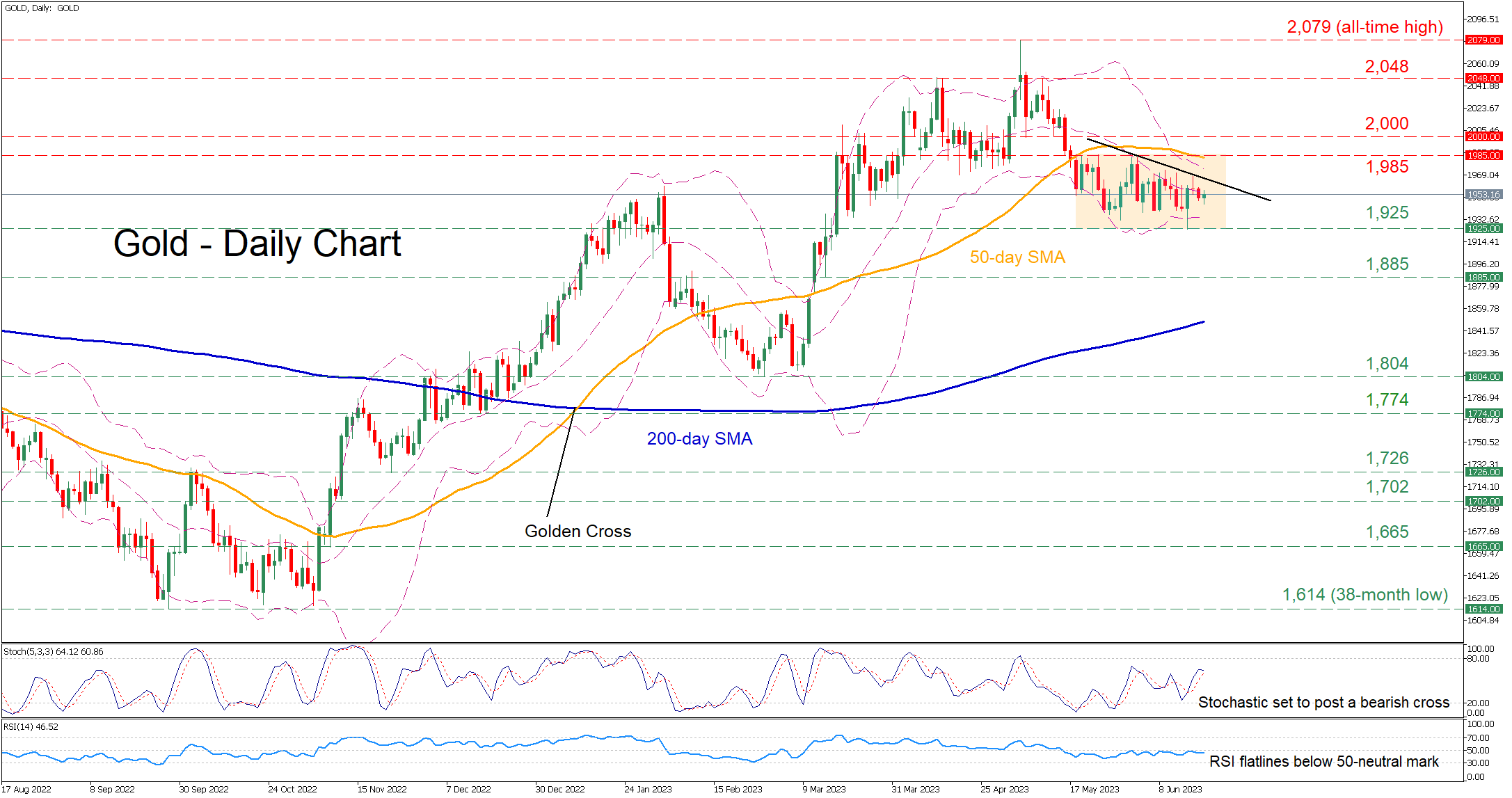

Gold Stuck in Range, Downside Risks Rise

Gold experienced a pullback after peaking at the all-time high of 2,079 in early May, falling beneath its 2,000 psychological mark and the 50-day simple moving average (SMA). Although bullion has been stuck within a tight range for the past month, the formation of a structure of lower highs is hinting at a deteriorating technical picture.

The momentum indicators currently suggest that near-term risks are tilted to the downside. Specifically, the stochastic oscillator is set to post a bearish cross, while the RSI has flatlined beneath its 50-neutral mark.

Should the bearish near-term structure extend, the price could initially challenge the recent three-month low of 1,925. If that floor collapses, the spotlight could turn to 1,885 before the 2023 bottom of 1,804 gets tested. Even lower, the 1,774 hurdle may provide downside protection.

Alternatively, if the price manages to break above the restrictive trendline that connects the recent lower highs, initial resistance could be found at 1,985, which overlaps with the 50-day SMA. Conquering this barricade, the bulls could aim at the crucial 2,000 psychological mark before 2,048 comes under examination. Piercing through the latter, the price could revisit its record high of 2,079.

Overall, gold has been directionless in the past month, but the short-term oscillators are slowly tilting towards the bearish side. Therefore, a failure to break through the descending trendline might trigger a significant retreat.

Hang Seng Index Technical: Minor Uptrend Intact

- Hang Seng Index has dropped by -2.4% since last Friday’s high ex-post interest rate cuts by PBoC.

- Short-term uptrend from 31 May 2023 low remains intact as it still trades above the 200-day moving average.

- Key support to watch will be at 19,090.

This is a following-up analysis of our earlier publication, “Hang Seng Index Technical: Potential breakout from channel resistance” dated on 9 June 2023 .

The Hong Kong 33 Index (a proxy for the Hang Seng Index futures) has staged the expected bullish breakout and almost met the first resistance of 20,300 as it rallied by +5% from 9 June to an intraday high of 20,205 last Friday, 16 June in light of a shift in the China central bank, PBoC conservative targeted monetary policy stance to a more accommodating approach as it cut 3 key interest rates within two weeks; 7-day reverse repos, 1-year medium-term lending facility, and the 1-year & 5-year loan prime rates today, 20 June that are being used to price corporates/consumer loans and mortgages respectively.

Since Monday, 19 June, the Index has tumbled by -2.4% which seems to have fallen victim to the “buy the rumours, sell on the actual news release” mantra as today’s cut on the loan prime rates have been almost fully priced in.

Fig 1: Hong Kong 33 minor short-term trend as of 20 Jun 2023 (Source: TradingView, click to enlarge chart)

The current drop in price actions is now coming close to a key pull-back support area

The Index is now hovering right above the former descending channel resistance and now turns pull-back support at 19,440 and the 200-day moving average coming in as support at around 19,090.

Also, the 19,440/19,090 support area confluences with 38.2% and 50% Fibonacci retracement of the minor short-term uptrend phase from the 31 May 2023 low to the 16 June 2023 high.

The momentum indicator is also at a parallel/corresponding support

The 4-hour RSI oscillator, a momentum indicator has exited from its overbought area, and it has now reached a corresponding support zone of 42%/36% which may lead to a potential positive reversal in price actions.

19.090 key short-term pivotal support to maintain the minor short-term uptrend phase with intermediate resistances coming in at 20,300 and 20,900.

On the other hand, a break below 19,090 negates the bullish tone to expose the 18,130/17,630 key medium-term support.

USD/JPY at the High of the Year

This morning, the Japanese currency weakened to 142.25 yen per US dollar for the first time since November 2022.

This is a consequence of the difference in the monetary policies of the two countries. Last week, the Fed, although it paused in raising the rate, said that it could be raised before the end of the year. On the other hand, the Bank of Japan on Friday maintained its commitment to ultra-soft monetary policy.

The USD/JPY chart shows that the rate is moving within a long-term ascending channel (shown in blue), and today it is near its median line — it can serve as resistance, which can at least slow down the growth of the rate. Or even promote a pullback within the channel shown in yellow.

However, the series of higher lows that has been going on since March 2023 suggests that bulls are dominating the USD/JPY market and may be trying to break the median line.

US Return Could Boost Activity, Focus Remains on BoE and UK Inflation

Stock markets remain slightly in the red on Tuesday but activity should pick up with the return of Wall Street from the long bank holiday weekend.

The focus this week remains on the central banks and whether we are as close to the end of the tightening cycle as everyone wants to believe. While there is the temptation to take what the Fed and others say with a small pinch of salt given their record over the last couple of years and the fact that any pivot was always likely to come late, they have been proven more accurate recently on their assertion that rates need to keep rising.

Markets have been overly optimistic this year and there may be an element of luck on the central bank side - keen to not underestimate inflation again, they were always going to remain hawkish as long as feasibly possible - but the data simply hasn't justified changing course yet.

That may change over the next couple of months but so far, especially in the UK, the turnaround in inflation has been more akin to a container ship performing a U-turn than a speedboat as many hoped. That may not dramatically increase the terminal rate but it may ensure it remains there much longer. Rate cuts this year look more fantasy than reality now.

The BoE will be hoping for some good news from the UK inflation data tomorrow but I'm guessing policymakers are approaching it with a sense of dread rather than hope. We're not likely to see any significant progress from the May data but avoiding another nasty surprise may be viewed as a win, allowing the MPC to proceed with 25 basis points rather than 50 which markets are pricing in a 30% chance of at this stage.

Oil remains choppy but flat and in lower range

Oil prices are relatively flat today, mirroring yesterday's session which was broadly choppy but ultimately directionless. Crude has rebounded strongly since falling toward its 2023 lows early last week but remains in its lower range, roughly between $70-$80 per barrel and it's showing little sign of breaking that in the short term.

While some believe the market will be in deficit later in the year, aided by the Saudi-driven OPEC+ cuts, which could support prices closer to what we saw late last year and early this, the economy remains one significant downside risk to this amid an adjustment in the markets toward higher rates for longer.

Gold drifting as we await more data

Gold has started the week slightly softer but very little has changed, in that it remains in the $1,940-$1,980 range that it has spent the vast majority of the last month. It was a very quiet start to the week which is why gold has basically continued to drift and that may continue until we see a significant change in the data.

The Fed last week made it perfectly clear that it doesn't believe it's done and its commentary this week, including Chair Powell's appearing in Congress on Wednesday, isn't likely to change in any significant way from that. It will be interesting to see if we get any response to UK inflation data as a potential signal of stickiness more broadly but then, there's every chance it could be viewed as a UK issue, rather than an indication of something more, considering how much more the country has struggled until now.

Bitcoin's recent trend remains against it despite recovery

Bitcoin drifted a little higher at the start of the week and is continuing to do so today. The move back toward $25,000 may have worried some but it's recovered relatively well since then. The recent trend remains against it and until it breaks the pattern of lower highs - recovery rallies that fall short of recent peaks before falling again - it will continue to look vulnerable. A break below $25,000 could be another blow although gains this year would still remain extremely healthy.