Sample Category Title

BoE Expected to Hike after CPI Figures

The consensus that the BoE will hike at the meeting on Thursday is pretty near unanimous. Where rates go after that is subject to intense debate, with the market and economists (and, potentially, the BoE) having different views. All of this could shake up the pound, especially if inflation is not in line with expectations tomorrow.

Where the disagreement lies

According to surveys by both Reuters and Bloomberg, the consensus among economists is that the BoE will reach a terminal rate of 5.0%. That means one hike at this meeting, and one more after that. The BoE would then hold rates steady for the rest of the year, according to this view.

The market, on the other hand, expects a terminal rate of 5.75%. It even got as high as 6.0% on Friday. This means 125bps of hiking over the course of the next few months. The BOE has been hesitant to do "double" hikes, so this could mean policy would continue to be tightened almost until the end of the year. Because the market is what rules the price of the pound, it's this view that's supporting the current strength in sterling. So, if something were to happen to bring the outlook more in line with what economists say, it could weaken the pound.

Why such disparate views?

The issue relates to inflation expectations, and in particular how the labor market is seen affecting prices. April saw the largest (nominal) increase in wages on record, at 7.2%. That means inflation has gone on to have "second-round" effects, something that BoE Governor Andrew Bailey warned about last May.

Second round of effects is when inflation causes employers to demand (and get) higher wages. Which means they have more cash to continue shopping, which in turn keeps prices higher. This is the incipient "wage price" spiral that worries many central bankers. The conventional wisdom is that it takes even higher rates to put an end to a wage-price spiral. It's likely that market participants are looking at the tightness in the labor market and betting that wages will keep rising. This will practically force the BoE to keep hiking, even if there is an economic downturn.

How the data could change things

Economists suggest that inflation in the summer could come down naturally, partially thanks to base effects. That's because inflation rose quickly last summer, driven by energy costs. If prices were to keep rising, but at a slower pace, it would bring inflation down. Other seasonal reasons for high inflation, such as the poor weather in Spain in spring, could also help bring grocer prices back to more normal levels.

A lot, therefore, hinges on the CPI figures that come out ahead of the BOE's meeting. If inflation shows that it's going strong, then it would imply the market is right, and boost the pound. The expectation is for a mere 3 decimal drop in inflation, so it wouldn't take much to even show inflation has actually increased. That would likely send shockwaves through the markets, and rase bets for rates even higher.

USD: When Will the Downtrend End?

The possibility of a US recession has ignited intense debates, especially as the labor market and consumer spending continue to demonstrate resilience despite aggressive interest rate hikes. However, hold on to your hats because Deutsche Bank is bringing a bold statement. They see a 100% probability of a US recession unfolding. The fed funds rate is currently at its highest level since 2006, but inflation still persists above the Fed's desired goal. Fed Chair Jerome Powell warned that more rate hikes may be necessary to tackle this stubborn inflation. However, here's where it gets interesting: David Folkerts-Landau, Deutsche Bank's chief economist, believes that while further rate increases may bring inflation down, the price we might have to pay is a full-blown recession. In fact, he suggests that the US is on the verge of experiencing its first policy-induced boom-bust cycle in decades, with the inflationary effects of expansive fiscal and monetary policies finally catching up. Buckle up, folks, because it would truly be a historical anomaly if we manage to avoid a hard landing. Stay vigilant, forex traders, as these dynamics unfold before our eyes.

US DOLLAR - Daily Timeframe

At the moment, we’re seeing the likely onset of bullish price action from the US Dollar based on the candlestick formation within the demand zone. The confluences I have for this trade include;

Pivot zone from the weekly timeframe

Rally-base-rally demand zone, and

Trendline support

Analyst’s Expectations:

- Direction: Bullish

- Target: 102.218

- Invalidation: 103.0

EURUSD - Daily Timeframe

The bullish impulse is weakening, as we can see from the price action at the supply zone. Correlating this EURUSD price action with what we saw earlier on the US Dollar chart indicates, to a large degree, the likelihood of a bearish retracement. On this note, I expect to see the bearish movement slide toward the trendline support before we get to see a bullish continuation.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.08238

- Invalidation: 1.10092

GBPUSD - Daily Timeframe

GBPUSD has reached a crucial resistance level after commencing a solid rally from the 100-Day moving average, which on a regular day would imply a possibility of a bearish movement. The current price action indicates an attenuation that often symbolizes a rejection from a support or resistance area. The correlation of this price action with that on the daily timeframe of the US Dollar chart reinforces my bias.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.26657

- Invalidation: 1.28523

AUDUSD - Daily Timeframe

AUDUSD made a solid rejection from the convergence point of the two resistance trend lines and could be heading toward the 100-Day moving average for support.

The confluences for this position include;

The resistance trendline convergence

The rally-base-drop supply zone, and

The previous rejection from the supply zone

Analyst’s Expectations:

- Direction: Bearish

- Target: 0.67323

- Invalidation: 0.68483

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

BTCUSD Analysis: Positivity Has Returned to the Markets, But for How Long?

The price of bitcoin is rising to the highs of June after a sharp drop that happened due to SEC lawsuits against the Binance and Coinbase exchanges.

Fortunately for crypto investors, the situation did not go according to the worst-case scenario. The court did not freeze Binance.US funds, giving the regulator and exchanges the opportunity to find a compromise. But if it does, what kind of compromise will it find and when? It is not surprising that we will be able to witness the massive relocation of crypto companies from the US:

→ To the UK. This week, the House of Lords of England approved the FSMB cryptocurrency regulation project, which has been under consideration since June 2022. Now the document must be approved in Parliament and sent to the king for signature. This month, by the way, venture capital firm a16z announced plans to open its first office in London later this year, citing a more predictable business environment.

→ To the UAE. VARA, the world's first independent regulator of virtual assets, operates there. As of January 2023, there were over 500 cryptocurrency startups operating in Dubai.

→ To Hong Kong, where the Securities and Futures Commission (SFC) approved a loyal licensing regime for virtual asset trading platforms.

→ To Europe, where the principles of regulation of the cryptocurrency market are laid down in Markets in Crypto Assets (MiCA).

Meanwhile, the bitcoin chart shows that the market has formed a false breakout of the USD 25k psychological level. We wrote about this option on June 15th.

After the puncture, against the backdrop of a weakening dollar and news about crypto regulation, the price of bitcoin rose to USD 27k per coin. However, the upside momentum may fade as it approaches 27,800, where the 50% of the A→B decline lies. In addition, the activity of the bears can be facilitated by the upper border of the descending channel (shown in red).

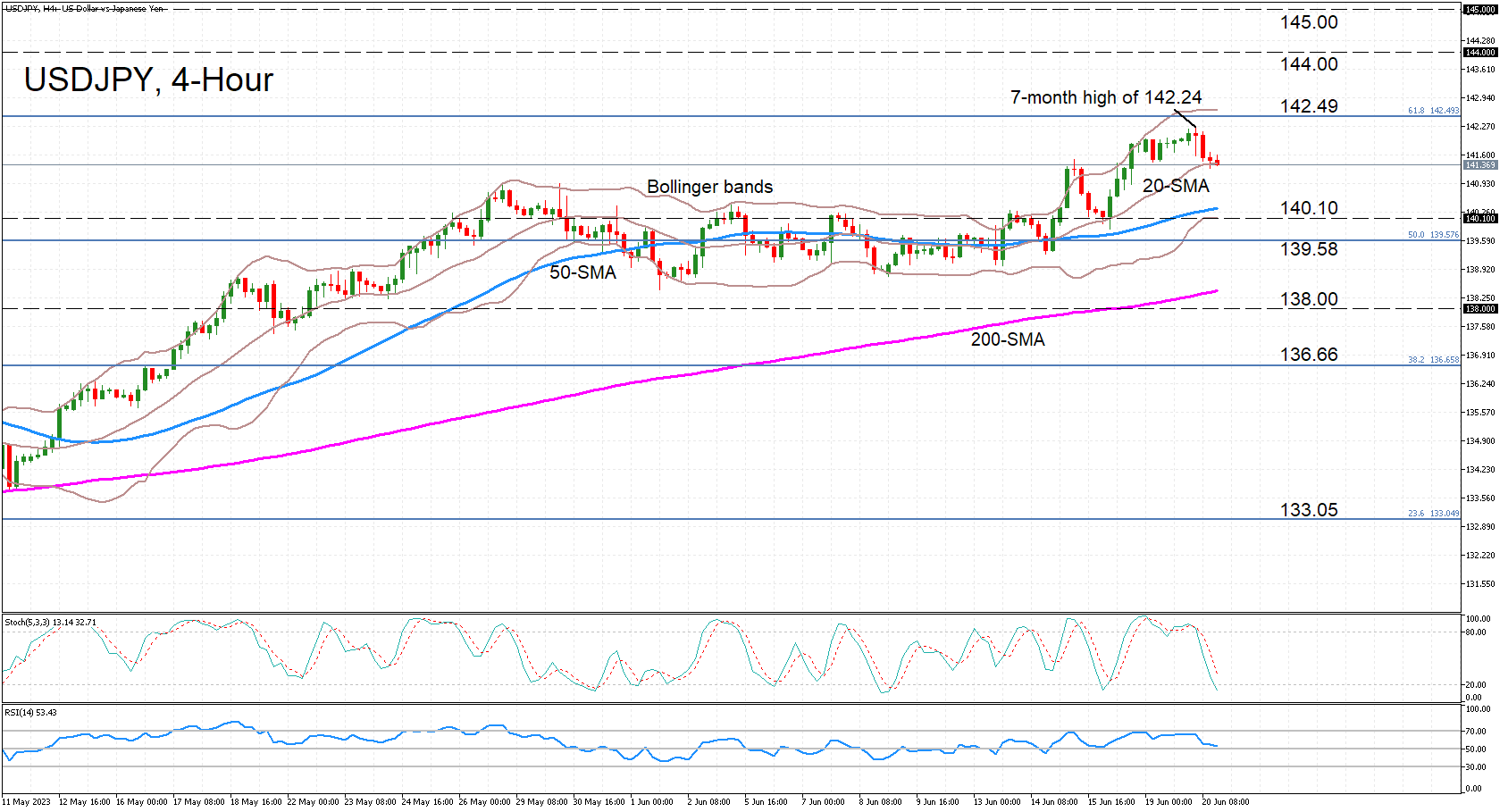

USDJPY Rally Stumbles But Finds Support at 20-Period SMA

USDJPY has come under selling pressure after hitting a seven-month high of 142.24 earlier today. Caution likely set in as the pair approached the 61.8% Fibonacci retracement level of the October 2022-January 2023 downtrend at 142.49.

But whilst the stochastic oscillator is indicating further losses in the short term as it has gone into a sharp downside reversal, heading for the oversold region below 20.0, the RSI is showing signs of stabilization just above the 50 neutral level.

The price action is underscoring the latter picture in the 4-hour chart as the 20-period simple moving average (SMA) has stepped in to defend the pair. Should it give way, the 50-period SMA is likely to be the next point of friction around 140.35. Slightly lower is an even more crucial support area around 140.10 where the lower Bollinger Band has flatlined and is where the upper Bollinger Band repeatedly capped prices during June. If the bears are able to penetrate this heavily fortified region, they will almost certainly aim for the 200-period SMA next.

However, if USDJPY manages to bounce off the 20-period SMA, it will probably have another attempt at cracking the 61.8% Fibo, which would then clear the way for the 144.00 and 145.00 levels.

Summing up, the negative bias in the very short term could be temporary if the 20-period SMA holds but breaching it would fuel the bearish forces, especially if the price also falls below 140.10. However, the bullish outlook in the medium term should stay intact as long as USDJPY trades above the 200-period SMA.

GBP/USD Lower Ahead of UK Inflation

- UK inflation expected to fall to 8.4% on Wednesday

- BoE likely to raise rates on Thursday

- Fed Chair Powell to testify before House committee on Wednesday

The British pound is lower on Tuesday. In the European session, GBP/USD is trading at 1.2739, down 0.41%.

UK inflation expected to ease

The UK releases the May inflation report on Wednesday and BoE policy makers will be hoping that inflation continues to trend lower. Inflation dropped in April to 8.7%, decelerating for a second straight month. The consensus stands at 8.4%, and the good news is that those awful readings above 10% appear to be over. On a monthly basis, inflation is expected to fall to 0.5% in May, down from 1.2% in April.

Inflation appears to have peaked and is heading lower, but nobody at the Bank of England is smiling. The UK is expected to have one of the highest inflation rates in the G-20 this year at 6.9% and the BoE’s 2% target is miles away. Finance Minister Sunak has set a goal of lowering inflation to 5% by the end of the year, which seems feasible if inflation continues to downtrend in the coming months.

The BoE will be in the spotlight on Thursday when it makes its rate announcement. The markets have priced in a 25-basis point hike at 70%, with a 30% chance of an oversize 50-bp increase. If inflation falls as expected to 8.4% or lower, the MPC should be able to proceed with the 25-bp hike, although central banks have a tendency of surprising the money markets.

In the US, it’s an unusually light data calendar this week. There are no tier-1 releases on Tuesday, and the markets are looking ahead to Wednesday, with Jerome Powell testifying before the House Financial Services Committee. Powell will have to clarify to lawmakers the Fed’s interest rate path, as the Fed paused last week after ten straight hikes but expects to renew hiking in July.

GBP/USD Technical

- 1.2719 is under pressure in support. Next, there is support at 1.2589

- There is resistance at 1.2848 and 1.2950

New Zealand Dollar Slides as Consumer Confidence Stays Weak

- NZD/USD is down 1.3% this week

- New Zealand consumer confidence rises

- Powell to testify before a House Committee on Wednesday

The New Zealand dollar is sharply lower for a second straight day. In the North American session, NZD/USD is trading at 0.6148, down 0.83%.

New Zealand consumer confidence rises

New Zealand Westpac consumer confidence accelerated to 83.1 in May, up from 77.7 in April and above the consensus of 76.2 points. Still, this is a low level as consumers remain pessimistic about economic conditions. The Westpac survey found that even though household incomes were higher due to strong wage growth, household finances were squeezed for two reasons. First, the cost-of-living crisis has hurt households, with inflation climbing 6.7% over the past year. Second, high interest rates have impacted on many households as mortgage rates have shot up.

Weak consumer confidence, which could well translate into a drop in consumer spending, would not be bad news at all for the Reserve Bank of New Zealand, which needs the economy to slow in order to pause interest rate hikes. The benchmark rate currently stands at 5.50% and the RBNZ meets next on July 12th. Last week’s GDP report for the first quarter showed growth contracted by 0.1%, which means that technically New Zealand is in a recession, with two consecutive quarters of negative growth.

In the US, this week’s data calendar is very light. There are no tier-1 releases on Tuesday and the markets are looking ahead to Wednesday, with Jerome Powell testifying before the House Financial Services Committee. Powell will likely be grilled by lawmakers on the Fed’s unconventional interest rate path, as the Fed paused last week after ten straight hikes but has signalled that it plans to renew hiking at next month’s meeting.

NZD/USD Technical

- NZD/USD is putting strong pressure on support at 0.6147. Below, there is support at 0.6056

- 0.6198 and 0.6276 are the next resistance lines

Sunset Market Commentary

Markets

The sense of disappointment following the Chinese 10 bps rate cut found its way through European markets as well. Stocks at some point ceded about 0.6% before paring losses to just 0.1% (EuroStoxx 50). Wall Street opens 0.1-0.5% lower. US yields eked out a few bps at the reopen after a long weekend (Juneteenth) but gains evaporated throughout the European session and in early US dealings even turned into losses of 2.3-4.6 bps. Strong US housing data suggesting the rate-sensitive sector stands its ground pretty well but were unable to prevent declines from happening. Building permits in May rose 5.2% m/m vs 0.6% expected, bringing the amount to 1491k (vs 1425). The series is considered a leading indicator as it marks the first step in the home building process. Shovel-in-the-ground housing starts seared a whopping 21.7% whereas expectations were for a minor 0.1% contraction. The total amount stood at 1631k, the highest in a year. The data follow up on yesterday’s bigger than expected rebound in the NAHB housing market index. German yields gapped lower at the open with lower-than-expected PPI numbers (-1.4% m/m vs -0.7% expected) explaining the move. Losses deepened from there on out into net daily changes ranging between -3.6 bps (2-y) to -11.6 bps (30-y). Rehn from Finland was the latest ECB policymaker to note the underlying inflation’s disappointing decline over the past months. Governing council member Muller later expressed worry over fast rising wages, which may get inflation firmly anchored to 2% over the medium term more complicated. His comments failed to deliver any market response though. Gilts outperform global peers after doing the exact opposite yesterday. Yields tank 12.6-15.7 bps across the curve compared to the 3.1-14 bps gains in a move that deepened the inversion on Monday. The amount of volatility underscores the important week UK assets are facing, kicking off with UK CPI numbers tomorrow.

The Japanese yen outperforms on currency markets today. USD/JPY eases towards 141.51 while EUR/JPY dips back below 155. Especially the latter combination is still trading at strong levels though. On the other side of the spectrum we have the Aussie dollar, trading heavily after what were perceived as dovish meeting minutes. The unexpected rate hike turned out to be the result of “finely balanced” arguments rather than an outright hawkish assessment. The euro and the dollar trade on equal footing. The pair holds a tight balance north of 1.09. The trade-weighted dollar (DXY) ekes out a slight gain to 102.60. Sterling declines in a profit-taking move going into the first checkpoint. EUR/GBP rebounds towards 0.8571, up from 0.8537 at the open.

News & Views

Turkish labour minister Vedat Isikhan said that the minimum wage will rise by 34% to TRY 11 402. It’s the second hike this year, bringing the minimum compensation 107% higher than end 2022. Of course, we need to keep in mind that Turkish inflation is still running at 40% Y/Y (85% peak in October of last year). The head of Turkey’s labour unions confederation hoped that authorities (both fiscal & monetary) will step up efforts to slow inflation down or wage hikes risk becoming meaningless. The Turkish central bank meets a first time on Thursday under new governor Hafize Gaye Erkan who got the job in the wake of a broad reshuffle after Turkey presidential elections earlier this year. The earlier decision by the new economic minister to stop FX interventions to synthetically prop up the currency (EUR/TRY 26 from 22 ahead of decision) is expected to get the backing of a significant rate hike from the current 8.5%. The consensus estimate stands at 20% but it’s actually anyone’s guess with prognosis ranging between 14% and 40%.

The Hungarian central bank (MNB) cut its overnight deposit rate by 100 bps for a second meeting running. It now stands at 16% and will be further reduced towards the base rate of 13% if risks continue to recede. The former was introduced to stem unwarranted selling pressure on the forint while the latter should be sufficient to tame inflation. The MNB sees CPI this year in a 16.5%-18.5% range before dropping steeply to 3.5%-5.5% next year. GDP prognosis are 0%-1.5% and 3.5%-4.5% for respectively this year and next. The forint stomachs this second, anticipated, rate cut again well with EUR/HUF broadly unchanged around 372 and keeping the 370-support area (YTD lows) well in sight. HUF swap yields lose 10 bps (2-yr) to 6 bps (30-yr).

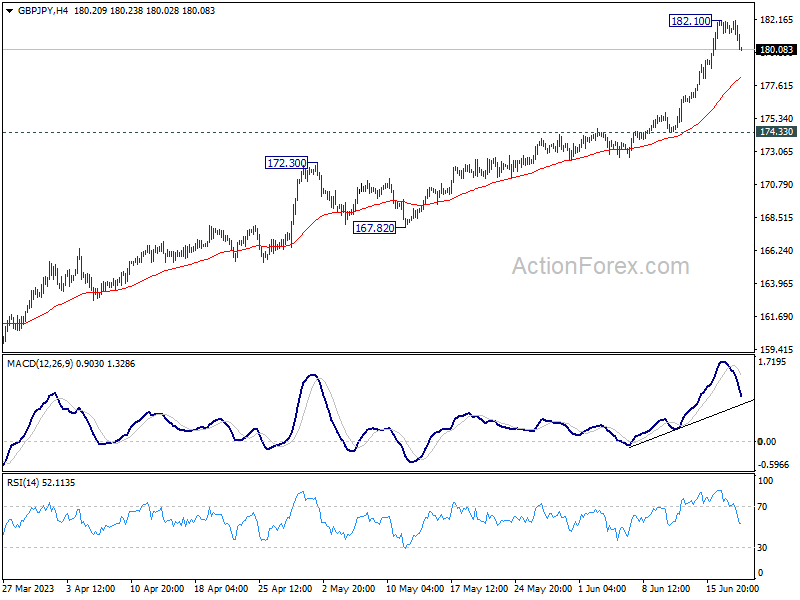

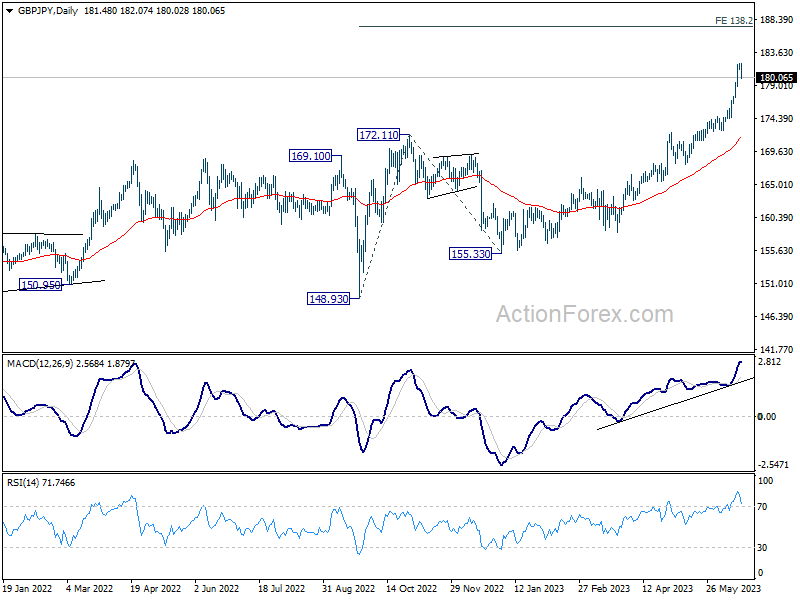

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 181.20; (P) 181.68; (R1) 182.13; More...

Intraday bias in GBP/JPY is turned neutral as retreat from 182.10 is extending lower. Downside of retreat should be contained above 174.33 to bring another rally. Break of 182.10 will resume larger up trend to 138.2% projection of 148.93 to 172.11 from 155.33 at 187.36.

In the bigger picture, up trend from 123.94 (2020 low) is extending. Next target is 195.86 (2015 high). For now, medium term outlook will remain bullish as long as 172.11 resistance turned support holds, even in case of deep pull back.

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.68; (P) 155.05; (R1) 155.44; More....

Intraday bias in EUR/JPY is turned neutral as retreat from 155.37 is set to extend lower. But downside should be contained above 151.60 resistance turned support to bring another rally. Break of 155.37 will resume larger up trend to 100% projection of 139.05 to 151.60 from 146.12 at 158.67.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. For now, medium term outlook will remain bullish as long as 148.38 resistance turned support holds, even in case of deep pull back.

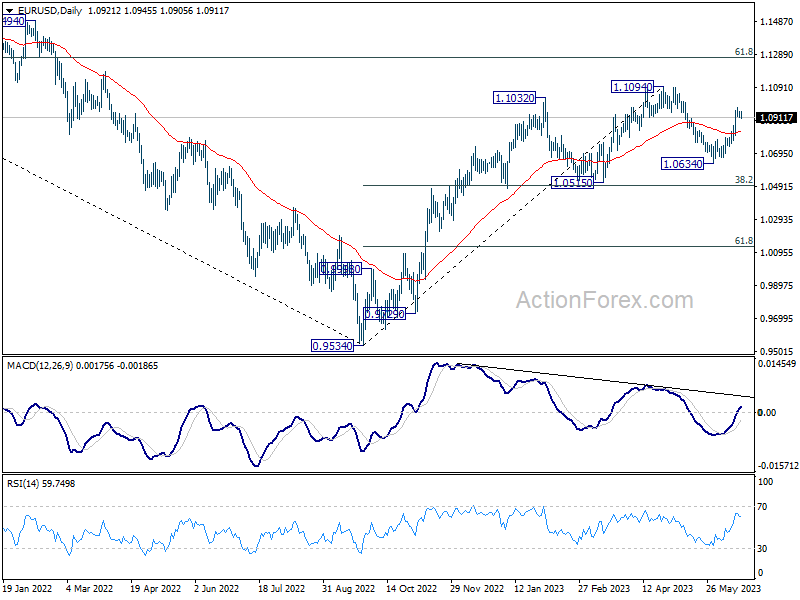

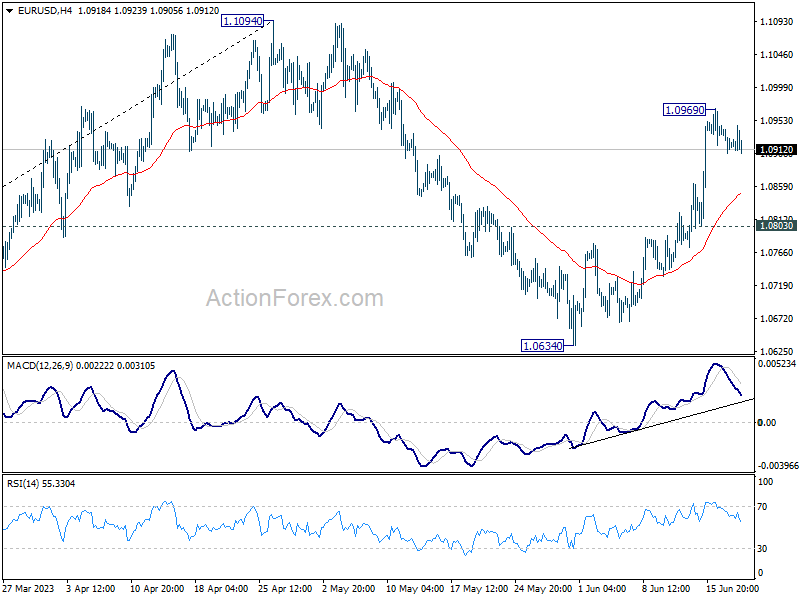

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0903; (P) 1.0925; (R1) 1.0942; More...

EUR/USD is staying in consolidation from 1.0969 and intraday bias remains neutral. Further rally is expected as long as 1.0803 support holds. On the upside, above 1.0969 will resume the rise from 1.0634 to retest 1.1094 high. Decisive break there will confirm resumption of whole up trend from 0.9534. However, firm break of 1.0803 will extend the corrective pattern from 1.1094 with another falling leg, targeting 1.0634 and below.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).