Sample Category Title

Last Week’s USD Setback/Euro Rally Taking a Breather

Markets

Even with no guidance from the US (markets close for Juneteenth) and no important data in Europe, the natural drift in European yields was to extend the recent uptrend. ECB speakers can’t but subscribe ECB’s Lagarde’s commitment to take a next 25 bps step at the July meeting. What happens later is subject to an internal debate. Hawks clearly indicate that the ECB has further to go at the September meeting as core inflation continues its higher for longer path. In this respect, ECB’s de Guindos said that the slowdown in core inflation might be more limited than the decline in the headline measure. More dovish oriented members (e.g. chief economist Lane) stress current data dependent ECB-modus which makes it too early to already guess on the appropriated policy action in September. Even so, German yields in a modest steepening move added between 3.7 bps (2-y) and 5.3 bps (30-y). At 3.16%, the 2-y closed at the highest levels since SVB/CS turbulence in March. The 10-y yield (2.52%) is closing in on the key 2.55% resistance area. Higher yields and a lack of guidance from the US prevented the EuroStoxx 50 to go for a test of the 4412 top (-0.74%). In technical trade, EUR/USD lost modest ground closing at 1.0921. The yen stabilized near recent low levels both against the dollar (USD/JPY 141.98) and the euro (EUR/JPY 155.09). UK bonds again hugely underperformed Bunds going into tomorrow’s UK CPI release annex Thursday’s BoE policy decision. In a sharp further curve inversion UK yields gained between 13.8 bps and 3.2 bps, with the 2-y easily surpassing the 5.0% barrier. EUR/GBP intraday touched a new ST low near 0.8520, but in the end EUR/GBP closed little changed (0.8537).

This morning, most Asian equity markets (except Australia, cf infra) are in a mild risk-off modus. Chinese banks eased the Prime Lending rate for 1-y and 5-y loans by 10 bps to respectively 3.55% and 4.20%. Some markets participants apparently hoped for more generous stimulus. The yuan weakens further (USD/CNY 7.177). The yen also stays in the defensive (USD/JPY 142.1) as US yields join the upside drift in Europe. Later today, the calendar mainly contains building permits and housing starts. Yesterday, NAHB homebuilders sentiment unexpectedly jumped from 50 to 55 (highest in 11 months). Is this a sign that interest rate sensitive parts of the economy stay resilient too? In US yields, the 2-y is again nearing the 4.80% resistance, the last hurdle before the 5.08% March top. The US 10-y (3.80%) meets similar resistance at 3.85%. Last week’s USD setback/euro rally are taking a breather. This process might continue short-term, especially if equities would fall prey to some profit taking after recent rebound. In CE, we also keep an eye a the rate decision of the Hungarian central bank (expected to ease the O/N deposit rate to 16%).

News and views

The Reserve Bank of Australia’s June policy meeting minutes showed the unexpected 25 bps rate hike to 4.10% was the result of “finely balanced” arguments. They considered inflation risks shifted to the upside. Some firms indexed prices to past inflation, making price pressures more persistent, especially against the backdrop of still little spare capacity and very low unemployment. The rate hike was based on inflation taking longer to hit the target and would boost confidence in the process. Arguments in favour for a pause, which was the analyst consensus then, included considerable uncertainty on household spending and the fact that past hikes will sharply slow the economy. Falling commodity prices and international shipping costs meanwhile pose downside inflation risks. All things considered, the case for a hike was stronger nevertheless and the RBA even kept the door open for further hikes if needed. Markets view the minutes as softer than the actual statement though. They were probably caught off guard by the RBA labeling it a finely balanced decision. Australian swap yields tumble between 2.7 and 8.9 bps with the front end of the curve outperforming. Money markets slightly pare their tightening bets, stopping short of pricing in two more 25 bps rate hikes by November. The Australian dollar slips, extending its recent loss streak into a third day. AUD/USD moves from 0.685 at the open to test the 0.68 big figure. RBA’s deputy governor Bullock in an interview later highlighted the central bank’s data dependence. The factors they are looking at are “inflation, particularly services prices, employment, consumption and what households are doing with their savings buffers, and the global economy, including China.” She also said the jobless rate may need to rise toward 4.5% from 3.6% today for inflation to return to target.

RBA Minutes Revealed ‘Fine Balance’ for This Month’s Surprise Hike

Asian stocks were moody, European indices traded lower, and US futures were under pressure on Monday. The rest of the week will likely prove to be challenging both in the US and elsewhere, as central bankers continue pressing economies like lemons, while signs of pain are just before their eyes.

It’s not because the stock markets are driven higher by the AI speculation that the underlying fundamentals are doing well. Average mortgage rates in the US are at the highest levels since the subprime crisis whereas mortgage rates in the UK are again above 6%. The last time we saw these levels was back during Liz Truss mini-budget crisis.

The UK 2-year yield spiked above 5% and has more to rally given the expectation of at least another 125bp hike from the Bank of England (BoE) before the end of this year, the first 25bp being due this Thursday.

What’s funny is that the Reserve Bank of Australia (RBA) minutes released earlier today showed that the RBA rate hike – which was the first hawkish shock in a series of hawkish central bank decisions this month – showed that the decision to hike rates by a surprise 25bp was ‘finely balanced’ and further decisions will depend on inflation outlook and home market. The minutes softened the RBA expectations but will likely undo the pledges of more policy action from the other central banks.

The central bank-induced stress has been well visible in the sovereign bond yields. Besides the sharp rise in UK yields, the US 2-year yield pushes decidedly toward the 5% mark, and the German 2-year yield tops at around 3.20%, the highest levels since the March banking stress. The Stoxx 600 fell more than 1% yesterday and slipped below the 50-DMA. It’s yet too early to call for a peak in equities, both in Europe and across the Atlantic, but there are all the reasons to believe that the rally could not carry on given the morose economic outlook and the aggressive central bank stances.

In China, the People’s Bank of China (PBoC) cut its one- and five-year LPR rates for the first time in ten months in hope to bolster economy, boost inflation and reverse the property crisis. But a targeted fiscal support is most probably needed because slashing rates when investment and consumption weaken due to a confidence crisis may not do much alone. Chinese stocks are under pressure since yesterday as investors were expecting stimulus measures last Friday, and they got nothing instead, as a proof that Xi remains against the Chinese kind of stimulus that we got used to. But that could be the only way to post the kind of Chinese growth numbers that we used to.

European Nat Gas prices are correct, but

The European nat gas prices fell nearly 15% on Monday, after they almost doubled since the start of the month on the back of hot weather and a series of outages. The beginning of this summer reminds us of last summer, when the water levels in European rivers and dams fell alarmingly, causing drought and risk of energy shortage.

Pricewise, we are at about a tenth of last summer’s peak levels, but the extreme weather conditions will likely keep the pressure to the upside, which in return keep inflation worries alive, the European Central Bank (ECB) hawks alert, and the euro bid.

We see the EURUSD’s positive momentum post the ECB meeting gently fade into the 1.10 mark, and we could see some more profit taking before Jerome Powell’s testimony this week, but the medium-term outlook remains positive for the EURUSD.

Improving US-China Relations

Market movers today

It should be another quiet day with mainly US housing data and a couple of Fed speakers on the agenda.

US housing looks like it is recovering as evidenced by the rise in the NAHB housing index yesterday. Today we get building permits and housing starts for May.

Fed's Bullard and Williams will both be speaking. Bullard is among the most hawkish members while Williams is more neutral.

The 60 second overview

Markets: European equity markets were off to a cautious start to the week with most indices in negative territory. US markets were closed due to the Juneteenth holiday. This morning, Asian equity markets are broadly mixed on the back of more monetary policy easing from China. The People's Bank of China cut two more key lending rates for the first time in 10 months to support growth in the world's second largest economy. The Chinese central bank cut the one-year loan prime rate by 10bp from 3.65% to 3.55%, and trimmed the five-year loan prime rate by 10bp from 4.3% to 4.2%. Equity futures point to a red opening in Europe and in the US later.

Blinken visit to China provides progress in US-China relations: It seems the visit by US Secretary of State Anthony Blinken to Beijing went as well as one could have hoped for. A key sign is that Blinken met Xi Jinping at the end of the visit. It was not a guarantee before the trip as it is not always custom due to their difference in ranks. But the fact that it happened suggests some real progress was made towards stabilizing the relations between US and China in Blinken's meetings with China's foreign minister Qin Gang and China's top diplomat Wang Yi. Before the meeting between Xi and Blinken started, Xi stated that "the two sides have also made progress and reached agreement on some specific issues. This is very good". Rare positive words on US-China talks.

New Nordic outlook: This morning, we published our new Nordic Outlook - Too soon to celebrate, 20 June. The news has mostly been good in recent months when it comes to inflation, employment and the near-term growth outlook in most major economies. However, we have yet to see the full effect of the monetary and fiscal tightening that has already happened, and inflation is still not sufficiently under control. We expect prolonged slowdown and moderately higher unemployment, with the risk of a deeper recession still present. This is also true in the Nordic countries, even though the outcome so far has surprised positively in Denmark and Sweden.

Continuing hawkish signals from the ECB: Schnabel's speech yesterday was filled with hawkish signals. She seems to favour one too many hikes than one too few, and she particularly warned against the risk of underestimating underlying inflation given its recent history. Notably Schnabel's hawkish inflation assessment sent yields higher, as she particularly said that they should 'err on the side of doing too much rather than too little' with uncertain inflation outlook. Lane's more cautious assessment did not seem to impact markets. The peak policy rate rose to 3.97%. The July ECB meeting is basically perceived as a 'done deal' by market pricing, yet the battle for September will be key, where markets currently price 18bp.

Equities: Equities saw some pushback on Monday, in thin volumes as US was closed for holidays. Stoxx 600 was down about -1% alike most Nordic markets. It was not a clear cut risk-off session though. An odd mix of banks and tech did relatively well, while it was partly defensives (health care, staples) that sold off, but also real estate and materials. Medical technology stocks were battered, driven by profit warnings from both Getinge and Sartorius. Asian markets are mostly lower too, despite another round of Chinese stimulus measures today. US futures are a notch lower this morning.

FI: Markets sold off through the day with the 10y point up around 5bp in core countries. After a remarkable spread tightening between Italy and Germany of more than 30bp this month, yesterday saw a 4bp reversal. The spread still remains tight at just 160bp. With the low realised volatility, the credit component in rates markets have performed. US was closed yesterday.

FX: EUR/SEK continued its move higher yesterday, trading close to the 14-year high of 11.78 fuelled by risk-off sentiment, periods of low liquidity and mere momentum trading. GBP took a breather from the past months' gains as markets await the May inflation data out Wednesday and Bank of England monetary policy meeting Thursday. EUR/USD declined steady throughout the session, trading firmly below the 1.10 mark.

Credit: Credit markets were relatively calm on Monday despite a small leg lower in equities after soft markets in Asia. With the US market out for a public holiday, there were few signals from one of the key markets thus leading to relatively slow trading. Itrax main widened 0.9bp to close at 76.2bp, while Itrax Xover widened 5.5bp to close at 399.4bp. With the summer break nearing, primary markets were fairly active with both SSA's, Financials and HY corporates coming to the market. Among notable Nordic issuers in the market on Monday were European Energy tapping existing hybrid debt and SBAB which printed EUR500m in green SNP's.

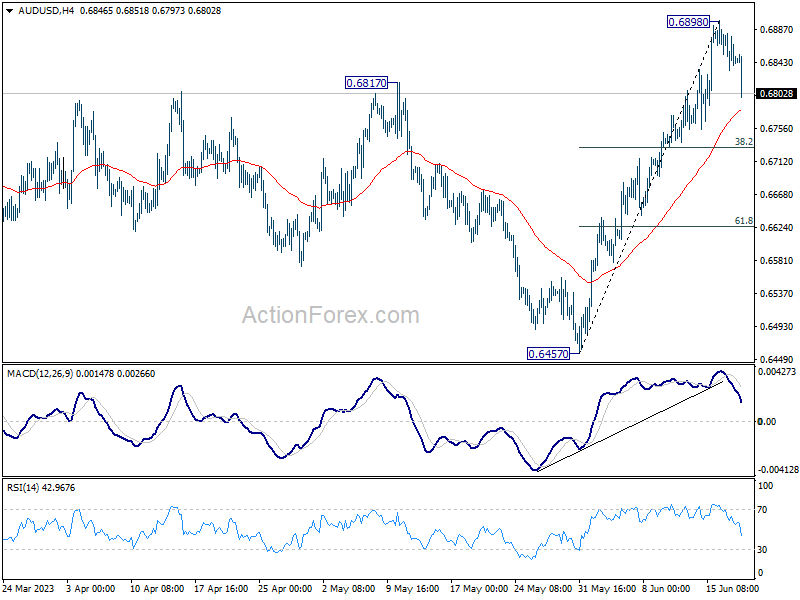

AUD/USD Daily Report

Daily Pivots: (S1) 0.6827; (P) 0.6857; (R1) 0.6880; More...

Intraday bias in AUD/USD remains neutral as consolidation from 0.6898 continues. Downside of retreat should be contained by 38.2% retracement of 0.6457 to 0.6898 at 0.6730 to bring another rally. As noted before, whole corrective decline from 0.7156 could have completed with three waves down to 0.6457 already. Above 0.6898 will resume the rise from 0.6457 to retest 0.7156 high next.

In the bigger picture, fall from 0.7156 could have completed in a three wave corrective structure at 0.6457. The development argues that rise from 0.6169 (2022 low) is still in progress. Firm break of 0.7156 will also add to the case that whole down trend from 0.8006 (2021 high) has finished and turn medium term outlook bullish. For now this will be the favored case as long as 55 D EMA (now at 0.6694) holds, even in case of deep pull back.

Aussie Down as RBA Minutes Raise Doubt Over July Hike

Australian Dollar is trading broadly lower today, reflecting uncertainties that emerged after release of minutes from RBA meeting earlier this month. The minutes revealed that a hold was considered at the meeting. Arguments were finely balanced even though it eventually decided to hike 25bps. These revelations have stirred market doubts about the continuity of monetary tightening in July, suggesting that the RBA might opt for a pause. Weighing down Aussie further is a slight pullback in Asian stocks, despite China's expected rate cut.

Elsewhere in the currency markets, New Zealand Dollar is trailing Aussie as the second weakest so far for the day, with Swiss Franc and Canadian Dollar following. Japanese Yen and Dollar are making mild gains as their corrective recoveries proceed. However, momentum of both currencies remains relatively weak. Euro and Sterling are showing mixed dynamics at the moment.

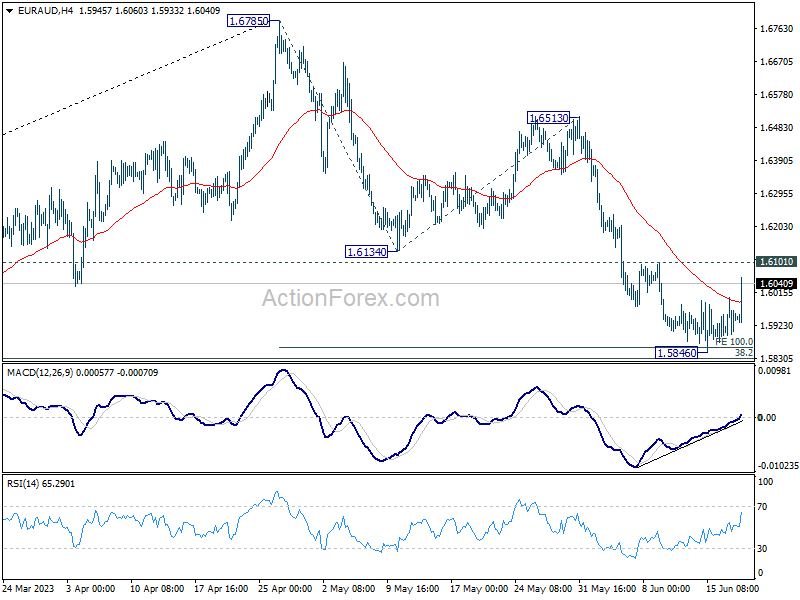

Technically, with the rebound in Asian session, EUR/AUD is now targeting 1.6101 resistance. Decisive break there should add to the case that whole corrective fall from 1.6785 has completed with three waves down to 1.5846, after hitting 100% projection of 1.6785 to 1.6134 from 1.6513 at 1.5862, slightly above 38.2% retracement of 1.4281 to 1.6785 at 1.5828. Stronger rally would be seen back to 1.6513 resistance next. If realized, the development would likely be accompanied by deeper pull back in AUD/USD and stronger rally in EUR/USD.

In Asia, at the time of writing, Nikkei is down -0.31%. Hong Kong HSI is down -1.53%. China Shanghai SSE is down -0.18%. Singapore Strait Times is down -0.46%. Japan 10-year JGB yield is down -0.0038 at 0.391.

RBA minutes: Finely balanced arguments for hold and hike

Minutes from RBA's June 6 monetary policy meeting reveal an active debate over whether to hold or raise the cash rate by 25bps.

As stated in the minutes, "Members recognised the strength of both sets of arguments, concluding that the arguments were finely balanced." However, they ultimately determined that a rate increase was the stronger course of action at this meeting.

Recent data indicating that inflation risks had begun tilting to the upside were a key influence on the board's decision. As they noted, "Given this shift and the already drawn-out return of inflation to target, the Board judged that a further increase in interest rates was warranted."

Such a move would bolster confidence that inflation would indeed return to the target range "over the period ahead", they reasoned.

At the meeting, RBA raised cash rate target by 25bps to 4.10%.

RBA Bullock: Economy needs to grow at a below trend pace for a while

In a speech, RBA Deputy Governor Michele Bullock noted the economy needs to "grow at a below trend pace for a while" to bring demand and supply into better balance. Only that will give "the greatest chance of securing sustainable full employment into the future."

Bullock explained, "For monetary policy... We think of full employment as the point at which there is a balance between demand and supply in the labour market (and in the markets for goods and services) with inflation at the inflation target."

"In recent months, the balance between labour demand and supply has improved somewhat," she noted. "Nevertheless, the labour market remains tight."

Also, "for the first time in decades, firms' demand for labour exceeds the amount of labour that people are willing and able to

"At the same time, with demand for goods and services high relative to the economy's capacity to supply those things, inflation is well above the 2–3 per cent target range."

PBoC cuts two key lending rates

China's PBoC executed cuts to two of its pivotal lending rates today, marking the first time such adjustments have been made in 10 months since last August.

The Chinese central bank opted to reduce one-year loan prime rate by -10 bps, taking it down from 3.65% to 3.55%. Concurrently, it also implemented a -10 bps cut to five-year loan prime rate, adjusting it from 4.3% to 4.2%.

These measures follow other recent actions aimed at easing monetary policy. Only last Thursday, PBOC made its first cut to one-year medium-term loan facility in 10 months. Furthermore, the bank reduced its seven-day reverse repurchase rate on the preceding Monday.

Looking ahead

Swiss trade balance, Germany PPI and Eurozone current account will be released in European session. Later in the day, US will release housing starts and building permits.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6827; (P) 0.6857; (R1) 0.6880; More...

Intraday bias in AUD/USD remains neutral as consolidation from 0.6898 continues. Downside of retreat should be contained by 38.2% retracement of 0.6457 to 0.6898 at 0.6730 to bring another rally. As noted before, whole corrective decline from 0.7156 could have completed with three waves down to 0.6457 already. Above 0.6898 will resume the rise from 0.6457 to retest 0.7156 high next.

In the bigger picture, fall from 0.7156 could have completed in a three wave corrective structure at 0.6457. The development argues that rise from 0.6169 (2022 low) is still in progress. Firm break of 0.7156 will also add to the case that whole down trend from 0.8006 (2021 high) has finished and turn medium term outlook bullish. For now this will be the favored case as long as 55 D EMA (now at 0.6694) holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Minutes | ||||

| 04:30 | JPY | Industrial Production M/M Apr F | 0.70% | -0.40% | -0.40% | |

| 06:00 | CHF | Trade Balance (CHF) May | 3.45B | 2.60B | ||

| 06:00 | EUR | Germany PPI M/M May | -0.70% | 0.30% | ||

| 06:00 | EUR | Germany PPI Y/Y May | 1.70% | 4.10% | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Apr | 27.3B | 31.2B | ||

| 12:30 | USD | Housing Starts May | 1.40M | 1.40M | ||

| 12:30 | USD | Building Permits May | 1.43M | 1.42M |

RBA Bullock: Economy needs to grow at a below trend pace for a while

In a speech, RBA Deputy Governor Michele Bullock noted the economy needs to "grow at a below trend pace for a while" to bring demand and supply into better balance. Only that will give "the greatest chance of securing sustainable full employment into the future."

Bullock explained, "For monetary policy... We think of full employment as the point at which there is a balance between demand and supply in the labour market (and in the markets for goods and services) with inflation at the inflation target."

"In recent months, the balance between labour demand and supply has improved somewhat," she noted. "Nevertheless, the labour market remains tight."

Also, "for the first time in decades, firms' demand for labour exceeds the amount of labour that people are willing and able to

"At the same time, with demand for goods and services high relative to the economy's capacity to supply those things, inflation is well above the 2–3 per cent target range."

PBoC cuts two key lending rates

China's PBoC executed cuts to two of its pivotal lending rates today, marking the first time such adjustments have been made in 10 months since last August.

The Chinese central bank opted to reduce one-year loan prime rate by -10 bps, taking it down from 3.65% to 3.55%. Concurrently, it also implemented a -10 bps cut to five-year loan prime rate, adjusting it from 4.3% to 4.2%.

These measures follow other recent actions aimed at easing monetary policy. Only last Thursday, PBOC made its first cut to one-year medium-term loan facility in 10 months. Furthermore, the bank reduced its seven-day reverse repurchase rate on the preceding Monday.

RBA minutes: Finely balanced arguments for hold and hike

Minutes from RBA's June 6 monetary policy meeting reveal an active debate over whether to hold or raise the cash rate by 25bps.

As stated in the minutes, "Members recognised the strength of both sets of arguments, concluding that the arguments were finely balanced." However, they ultimately determined that a rate increase was the stronger course of action at this meeting.

Recent data indicating that inflation risks had begun tilting to the upside were a key influence on the board's decision. As they noted, "Given this shift and the already drawn-out return of inflation to target, the Board judged that a further increase in interest rates was warranted."

Such a move would bolster confidence that inflation would indeed return to the target range "over the period ahead", they reasoned.

At the meeting, RBA raised cash rate target by 25bps to 4.10%.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Sydney – 6 June 2023

Members present

Philip Lowe (Governor and Chair), Michele Bullock (Deputy Governor), Mark Barnaba AM, Ian Harper AO, Carolyn Hewson AO, Steven Kennedy PSM, Iain Ross AO, Carol Schwartz AO

Members granted leave of absence to Alison Watkins AM in accordance with section 18A of the Reserve Bank Act 1959.

Others present

Luci Ellis (Assistant Governor, Economic), Christopher Kent (Assistant Governor, Financial Markets)

Anthony Dickman (Secretary), David Norman (Acting Deputy Secretary)

Penelope Smith (Head, International Department), Carl Schwartz (Acting Head, Domestic Markets Department), Meredith Beechey Osterholm (Deputy Head, Economic Research Department)

International economic developments

Members commenced their discussion of the global economy by noting that inflation in many economies remained well above central banks' targets. Although headline inflation had continued to decline as energy prices fell and food price inflation eased, members noted that core inflation had remained sticky and shown little sign of easing. Services inflation, which had become the primary source of inflationary pressures across advanced economies, had continued at a high rate. This partly reflected strong wages growth, which remained above rates consistent with inflation targets in many economies. This, in combination with subdued growth in labour productivity, had resulted in a rapid rise in unit labour costs over the preceding year. Members acknowledged the implications of this for Australia, given the high degree of commonality in inflation experience globally since the pandemic. While central banks in advanced economies expected inflation to return to target, most do not see this as likely to occur in the coming year.

Members noted that economic growth in advanced economies was slowing gradually as contractionary monetary policy settings took effect. GDP in major advanced economies had risen only slightly in the March quarter and had declined in some euro area countries. Consumption growth had been subdued in the March quarter and indications were that this had continued into the June quarter. Business investment was yet to surpass pre-pandemic levels in most advanced economies. Other indicators of economic activity had been more resilient in recent months. Housing prices appeared to have stabilised in several countries, following significant declines over 2022, and survey measures of business conditions pointed to services sector activity having increased further in May.

In China, the growth momentum had waned in April after a strong bounce-back following the end of pandemic restrictions and the reopening of the international border in late 2022. As a result, the strength of the economic recovery had become more uncertain than a month earlier. Retail sales and industrial production had declined markedly in April and conditions in the property market had deteriorated.

Members noted that the price of iron ore had been broadly stable over the prior month, despite the soft run of Chinese data. More broadly, the soft outlook for global growth had led to falls in a range of commodity prices since the start of the year. Bulk commodity prices had declined and were now close to pre-pandemic levels. Prices of energy commodities had declined the most, with thermal coal and spot prices for liquified natural gas falling in response to relatively high levels of inventories and broader concerns about the outlook for growth. Oil prices had also fallen. If sustained, these declines would further dampen consumer price inflation globally over the second half of the year.

Domestic economic conditions

Members noted that growth in economic activity in Australia had slowed since mid-2022, as the post-pandemic recovery in spending faded and the substantial tightening in monetary policy worked its way through the economy. The national accounts, to be released the day after the meeting, were expected to show only modest growth. Members noted that the new policies announced in the Australian Government Budget had not had a material effect on the staff forecasts for economic activity and inflation.

There was growing evidence that household consumption growth had been subdued in the first half of 2023. Retail volumes had declined in the March quarter, despite strong population growth, and liaison with retailers suggested that conditions had softened further in the June quarter. Growth in spending on consumer services, including cafes and restaurants, had generally slowed but by less than other forms of consumption. Members discussed the significant financial pressure facing many households and the effect of this on communities and the economy as a whole. They also discussed the unevenness in household spending, noting that some households had drawn on the substantial additional savings built up during the pandemic, while other households were facing considerable budget constraints.

National housing prices had increased in recent months and households' expectations for future rises in housing prices had strengthened. Members noted that, if sustained, this would imply less of a drag on consumption in the year ahead than had previously been envisaged. The increase had been broadly based across capital cities in May and was consistent with developments in a number of other countries. Members discussed the reasons for the unexpected strength in housing prices. They noted that strong population growth had supported demand for housing and that this was largely affecting the established housing market. Expectations that the interest rate cycle was near its peak might also have played a role. Orders for newly constructed housing remained weak and residential construction firms continued to report that high materials costs and shortages of skilled tradespeople were contributing to low margins and delays in work being completed.

Members noted that the labour market remained very tight. Nonetheless, conditions had eased slightly, alongside slower growth in economic activity. Employment growth over the prior six months had been a little less than growth in the working-age population over that period. Firms in the Bank's liaison program had reported some improvement in labour availability. Acknowledging that the monthly data are volatile, members noted that the unemployment rate had ticked up to 3.7 per cent in April and the number of people employed had been little changed.

A range of measures suggested that wages growth had been in the 3½ to 4 per cent range. The pace of increase in the Wage Price Index (WPI) had risen to 3.7 per cent over the year to the March quarter, broadly in line with earlier expectations. The average size of wage changes in the private sector for those who received an increase had remained at around 4 per cent for the third consecutive quarter. In the public sector, wages growth had picked up to 3 per cent and a further increase was expected. Information from the Bank's liaison program was also signalling that firms' expectations were for wages growth to remain stable at around current levels over the year ahead.

The recent Annual Wage Review decision of the Fair Work Commission (FWC) had increased award wages by 5.75 per cent. This was higher than the expectation embedded in staff forecasts and would add directly to WPI growth in the September quarter, relative to the prior forecasts. In addition to this, a range of public sector enterprise agreements were being negotiated and it appeared likely that some of these would contain wage rises of at least 4 per cent for the first year, followed by smaller increases in subsequent years. Members observed that the FWC decision would support wages growth for around 30 per cent of workers (but a significantly smaller share of the total wage bill) whose wages are either directly or indirectly affected by award rates. Recently struck enterprise bargaining agreements would similarly see wages growth for those on enterprise bargaining agreements rise from current levels. Members observed that it was understandable that the lowest paid workers would be compensated for high inflation, but that it would be concerning if wages across a broad range of jobs were to become implicitly indexed to high inflation.

Timely indicators pointed to a gradual easing in inflation in the June quarter. The monthly CPI indicator for headline inflation had increased to 6.8 per cent over the year to April, a little higher than had been expected. However, this was partly due to the timing of price changes for volatile items, and growth in the indicator excluding volatile items and holiday travel had slowed, particularly in six-month-annualised terms. The easing in global upstream cost pressures and the more recent declines in commodity prices and shipping rates could be expected to lower firms' costs, but the easing in consumer goods price inflation had been limited. Members acknowledged that additional information on the momentum of services prices inflation would become available over subsequent months.

Members noted that there were various other considerations that created upside risk for inflation. Retail electricity prices had risen over the preceding year, but – unlike in other countries – there would be an even larger increase in the year ahead. Rent inflation had been high in April, reflecting very tight rental market conditions across the capital cities, and appeared to be drifting up further. There had also not been as clear a moderation in goods price inflation in Australia as there had been in some other countries. In considering the outlook for inflation, members discussed the importance of productivity growth, noting that output per hour worked had not increased over the preceding three years.

International financial markets

Members commenced their discussion of international financial conditions by observing that the US Federal Reserve, the European Central Bank, the Bank of England, Norges Bank and the Reserve Bank of New Zealand (RBNZ) had increased policy rates further over the prior month to address high and persistent core inflation. Some central banks, including the RBNZ, had communicated that policy rates were now likely to be sufficiently restrictive or close to sufficiently restrictive. However, central banks had also emphasised that policy rates were unlikely to decline over coming months, in contrast to market-implied expectations.

Market expectations for the path of central bank policy rates had shifted higher over the prior month in response to stronger-than-expected inflation and labour market data. The suspension of the US debt ceiling and easing of concerns about stress in some parts of the US banking system had also contributed to these moves.

Government bond yields in advanced economies had also increased over the prior month. Members noted that the increase in nominal yields mostly reflected higher real yields, while market measures of longer term inflation expectations remained anchored in most economies. This implied that markets expected central banks to raise policy rates sufficiently to return inflation to target.

Private sector financial conditions had been little changed. US funding markets had stabilised after the banking stress in March and deposit outflows from banks had slowed. Members noted that US banks' funding costs were likely to remain under pressure for some time, particularly for smaller banks.

In China, financial conditions had remained accommodative, with bond yields having declined a little in response to concerns around the strength of the economic recovery and expectations of further policy easing. Credit growth had eased alongside a slump in property sales and many highly leveraged property developers continued to face considerable financial stress.

The Australian dollar had ended the month little changed on a trade-weighted basis. Members observed that there had been two countervailing forces on the exchange rate over preceding months. Interest rate differentials between Australia and major advanced economies had generally been supportive, and members noted that the Australian dollar had appreciated noticeably in response to the decision to raise the cash rate in May. Meanwhile, the decline in commodity prices and concerns about the strength of China's economic recovery had weighed on the value of the Australian dollar.

Domestic financial markets

Members noted that increases in the cash rate continued to be passed through to higher lending rates. Scheduled mortgage payments had increased further and equated to around 9 per cent of household disposable income in April. The increase in average variable mortgage lending rates over the tightening phase had been less than the rise in the cash rate, reflecting competition in the banking sector. There were, however, some signs that competition for borrowers had started to ease. The continuing rollover of low fixed-rate loans into higher rate loans would contribute to a further increase in scheduled payments over the months ahead. Members noted that, based on increases in the cash rate to date, payments were projected to rise to the equivalent of around 10 per cent of household disposable income by the end of 2024.

Net flows into borrowers' offset and redraw accounts remained positive to April, although extra mortgage payments were well below the highs seen during the pandemic. Increases in scheduled mortgage payments would reduce some borrowers' ability to make these extra payments, but higher rates were also creating an incentive to hold savings in these accounts. The value of non-performing housing loans had risen a little but from a very low level. Measures of personal insolvencies also remained at low levels.

Members observed that new housing loan commitments had stabilised over preceding months, following declines of around 30 per cent from the peak in early 2022. Commitments had steadied among both owner-occupiers and investors, and across states. This pattern was consistent with housing prices having steadied after prior declines. Housing credit growth was also showing signs of levelling out after a period of deceleration.

Members noted that the decision to increase the cash rate in May had been unexpected by many market participants and contributed to bond yields in Australia rising by around 30 basis points over the prior month. For the June meeting, markets were pricing in about a 50 per cent chance of an increase in the cash rate and a little less than half of market economists expected an increase. These expectations had increased over the prior week, following the release of the monthly CPI and the FWC's decision. Further ahead, around half of economists surveyed expected 50 basis points of tightening by August, which was broadly in line with the probability implied by market pricing.

Considerations for monetary policy

In turning to the policy decision, members noted that inflation had passed its peak but remained well above target and was forecast to return to the top of the target range only by mid-2025. There was little spare capacity in the economy, with the unemployment rate very low. At the same time, members noted that consumer spending had softened significantly, with both higher interest rates and high inflation weighing on household purchasing power. Members observed that the economy still looked to be traversing a narrow path on which inflation comes back to target while the unemployment rate rises but remains low. They noted that there were significant risks and uncertainties to staying on this path.

Members discussed two options: increasing the cash rate by 25 basis points; or holding the cash rate unchanged.

The case for raising the cash rate by a further 25 basis points focused on the increased risk that inflation would take longer to return to target than had been expected. Members observed that inflation was already projected to be above target for a number of years and was expected to take somewhat longer to return to target in Australia than in some other countries. This extended timeframe reflected the Board's desire to bring inflation down while, at the same time, preserving as many of the gains in employment as possible. While this remained the Board's objective, members noted that a more prolonged period of above-target inflation would increase the risk that firms' and households' expectations for inflation rise. If this occurred, high inflation would become more persistent with the result that interest rates would need to be higher for longer. This would increase the risk of a sharp rise in unemployment.

In discussing the risks to the inflation outlook, members observed that the monthly indicator of headline inflation had surprised on the upside in April and that the decline in goods price inflation had been less than observed in other countries. In addition, services price inflation had not yet shown signs of moderating and the evidence from abroad suggested that it may prove to be persistent.

Members noted that wages growth was still consistent with the inflation target, provided productivity growth picked up to around the average pace that had been recorded before the pandemic. While future trends in productivity were uncertain, the outcomes over recent times had been disappointing. Members discussed the possibility of implicit indexation of wages to past high inflation and the potential for this to become widespread. Similarly, members observed that some firms were indexing their prices, either implicitly or directly, to past inflation. These developments created an increased risk that high inflation would be persistent, which would make it more difficult to keep the economy on the narrow path.

Members observed that the resumption of growth in housing prices would – if sustained – imply less drag on consumer spending in the coming year than had been envisaged. Members also noted that the stabilisation in housing loan approvals suggested that financial conditions may not have been as tight as they had previously judged. The downside risks to global growth had also abated a little as conditions in the US banking sector had stabilised.

Members concluded that these developments had shifted the balance of risks on inflation to the upside compared with a month earlier, although they also noted that there were some downside risks to inflation, including from developments in global markets and the slowdown in household spending in Australia.

The case for holding the cash rate unchanged at this meeting rested on the slowing in the economy and the possibility that the significant increases in interest rates to date would lead to the economy slowing more sharply than expected. Members noted that consumption growth was already quite weak, especially in per capita terms. Real disposable incomes were falling, especially for home loan borrowers, and many renters were experiencing difficult financial conditions. Members also noted that the scale of increase in the cash rate over the preceding year, lags in the transmission of monetary policy through the economy and the large number of fixed-rate loans scheduled to expire over coming months would see financial conditions tighten further. Given these developments, there was a risk of the economy slowing and unemployment rising by more than expected.

Members also discussed some of the downside risks to inflation. They observed that commodity prices had fallen quite significantly over preceding months, as had the price of international shipping, which could be expected to reduce pressure on consumer prices over time. Members noted that medium-term inflation expectations in financial markets had been little changed to date and that the moderation occurring in headline inflation could mitigate the risk of inflation expectations rising. They also observed that the staff forecasts had overestimated wages growth for a prolonged period prior to the pandemic and that productivity could prove stronger than expected.

In light of these considerations, members discussed the possibility of holding the cash rate unchanged at this meeting and then reconsidering at subsequent meetings, with the benefit of additional data.

Members recognised the strength of both sets of arguments, concluding that the arguments were finely balanced. They judged, though, that the case to raise the cash rate at this meeting was the stronger one.

The Board affirmed that its priority is to return inflation to target within a reasonable timeframe. The recent data suggested that inflation risks had shifted somewhat to the upside. Given this shift and the already drawn-out return of inflation to target, the Board judged that a further increase in interest rates was warranted. This increase would provide greater confidence that inflation would return to target over the period ahead. An extended period of high inflation would distort the economy and exacerbate cost-of-living pressures, hurting those on low incomes the most. Sustained high inflation would also lead to even higher interest rates in the future and a worse outlook for the labour market.

In taking the decision to increase interest rates again, members acknowledged the considerable uncertainty regarding the outlook for household spending and the financial stresses facing some households. Given this, they agreed to continue to monitor trends in household spending closely and consider the implications for the inflation outlook, as well as developments in the global economy and the domestic labour market. Members reaffirmed their determination to return inflation to target and their willingness to do what is necessary to achieve that.

Members agreed that the Governor's speech the following day would provide an opportunity to explain the decision in more detail.

The decision

The Board decided to increase the cash rate target by 25 basis points to 4.1 per cent and to increase the interest rate on Exchange Settlement balances by 25 basis points to 4 per cent.

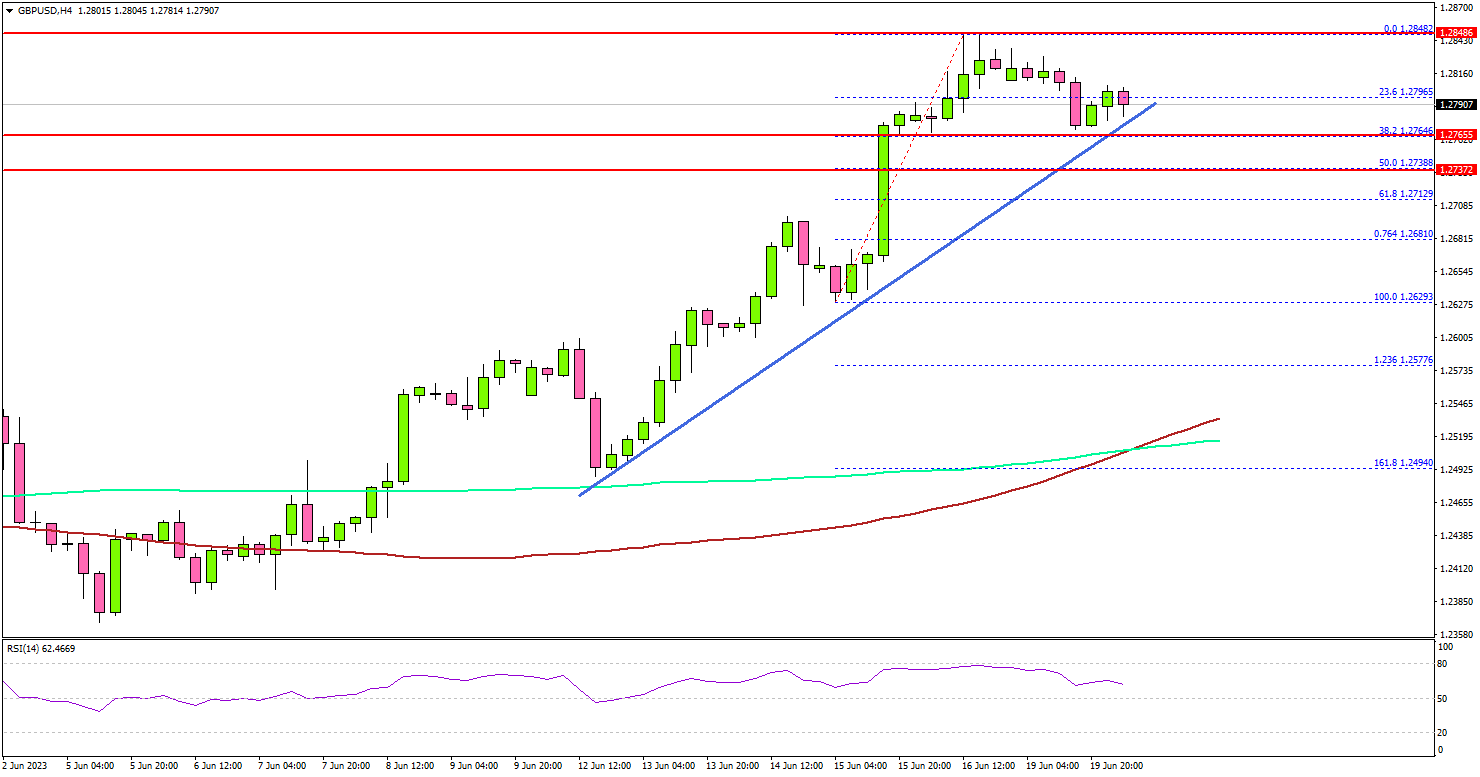

GBP/USD: Dips Turn Attractive In Near-Term

Key Highlights

- GBP/USD climbed above the 1.2750 and 1.2800 resistance levels.

- A major bullish trend line is forming with support near 1.2765 on the 4-hour chart.

- EUR/USD started a downside correction from the 1.0970 zone.

- Gold price is facing heavy resistance near the $1,965 level.

GBP/USD Technical Analysis

The British Pound started a major increase above the 1.2720 resistance against the US Dollar. GBP/USD settled above 1.2700 to move into a bullish zone.

Looking at the 4-hour chart, the pair gained pace above the 1.2800 resistance. It traded as high as 1.2848 and settled well above the 100 simple moving average (red, 4 hours) and the 200 simple moving average (green, 4 hours).

Recently, there was a minor downside correction below 1.2800. The pair dipped below the 23.6% Fib retracement level of the upward move from the 1.2629 swing low to the 1.2848 high.

Immediate support is near the 1.2770 level. There is also a major bullish trend line forming with support near 1.2765 on the same chart. It is close to the 38.2% Fib retracement level of the upward move from the 1.2629 swing low to the 1.2848 high.

The next major support is near the 1.2715 level. If there is a downside break below the 1.2715 support, the pair could decline toward the 1.2650 support.

Any more losses might send GBP/USD toward 1.2600. If there is a fresh increase, the pair could face resistance near 1.2850. The first major resistance is near the 1.2920 level. If there is a move above the 1.2920 resistance, the pair could rise toward 1.3000.

Looking at EUR/USD, the pair rallied above the 1.0900 resistance zone and recently started a short-term downside correction.

Economic Releases

- Euro Zone Current Account for April 2023 - Forecast €30.1B versus €31.6B previous.