Sample Category Title

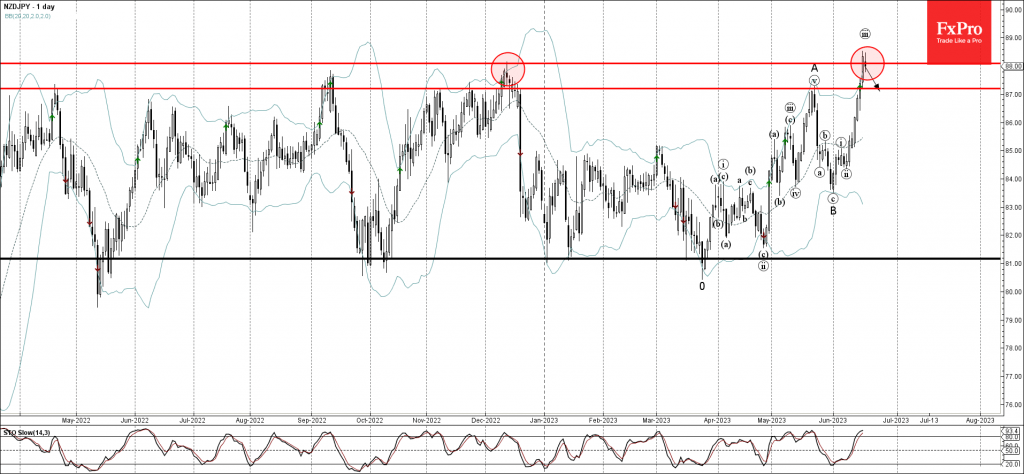

NZDJPY Wave Analysis

- NZDJPY reversed from resistance level 88.00

- Likely to fall to support level 87.20

NZDJPY currency pair recently reversed down after the pair failed to keep the ground above the key resistance level 88.00 (former multi-month high from last December).

The downward reversal from the resistance level 88.00 stopped the 2 of the earlier upward impulse waves – C and (iii).

Given the overbought daily Stochastic, NZDJPY can be expected to fall further toward the next support level 87.20 (former top of the previous impulse wave A).

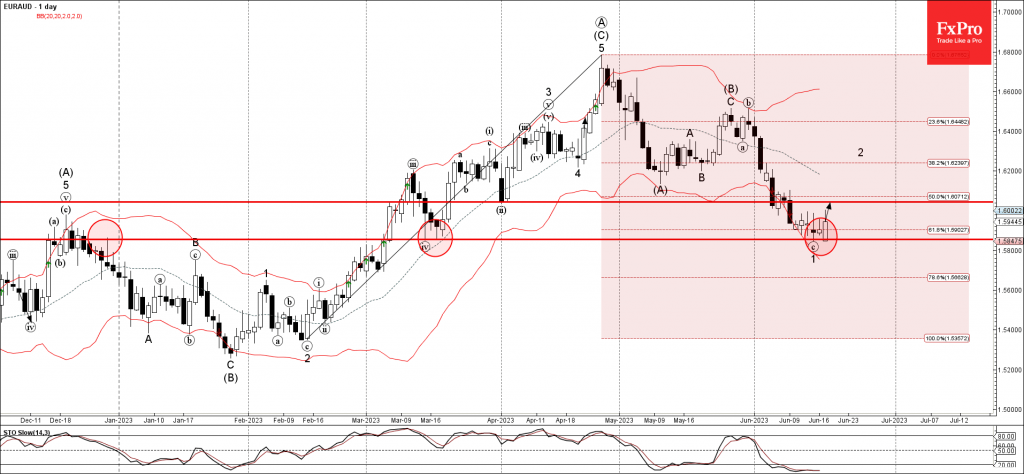

EURAUD Wave Analysis

- EURAUD reversed from support level 1.5855

- Likely to rise to resistance level 1.6045

EURAUD currency pair recently reversed up from the key support level 1.5855 (former support from March), strengthened by the lower daily Bollinger Band and by the 61.8% Fibonacci correction of the upward impulse from February.

The upward reversal from the support level 1.5855 started the active corrective wave 3.

Given the still oversold daily Stochastic, EURAUD can be expected to rise further toward the next resistance level 1.6045, former support from April.

Will the BoE Appear Hawkish Enough to Push the Pound Higher?

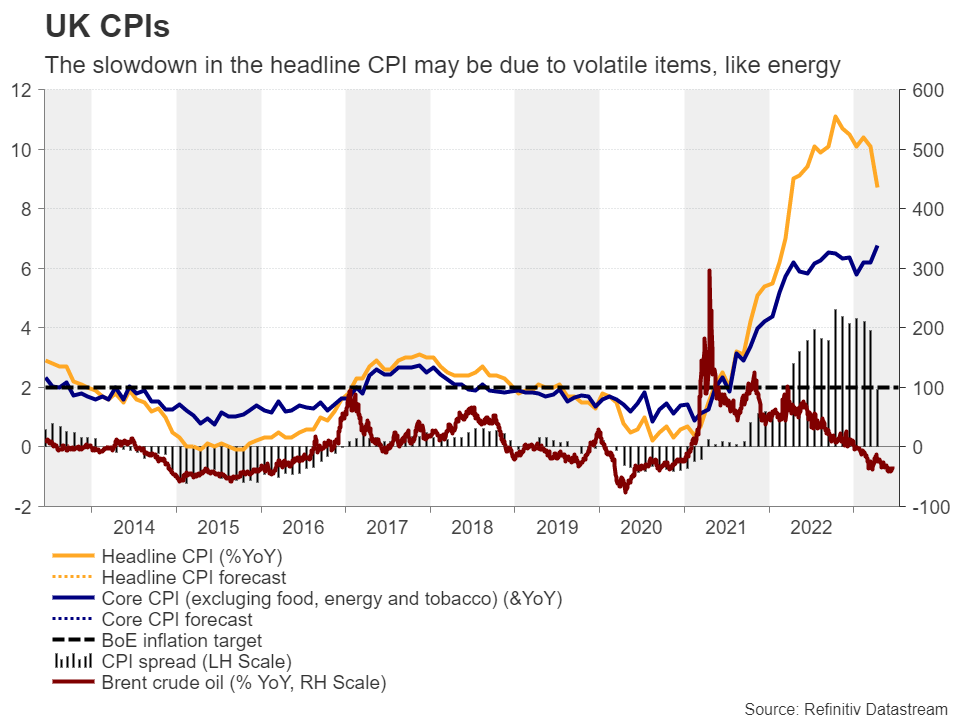

With the Bank of England (BoE) dropping calls that the UK is facing its longest recession since records began, investors are hoping, or even demanding, of more aggressive action. With that in mind, Thursday’s monetary policy decision at 11:00 GMT may attract special attention as traders may be eager to see whether Bailey and co will rise to the occasion. However, they will be already locked in front of their screens as just the day before, the UK CPIs for May are coming out.

Bailey and co under pressure to tame inflation

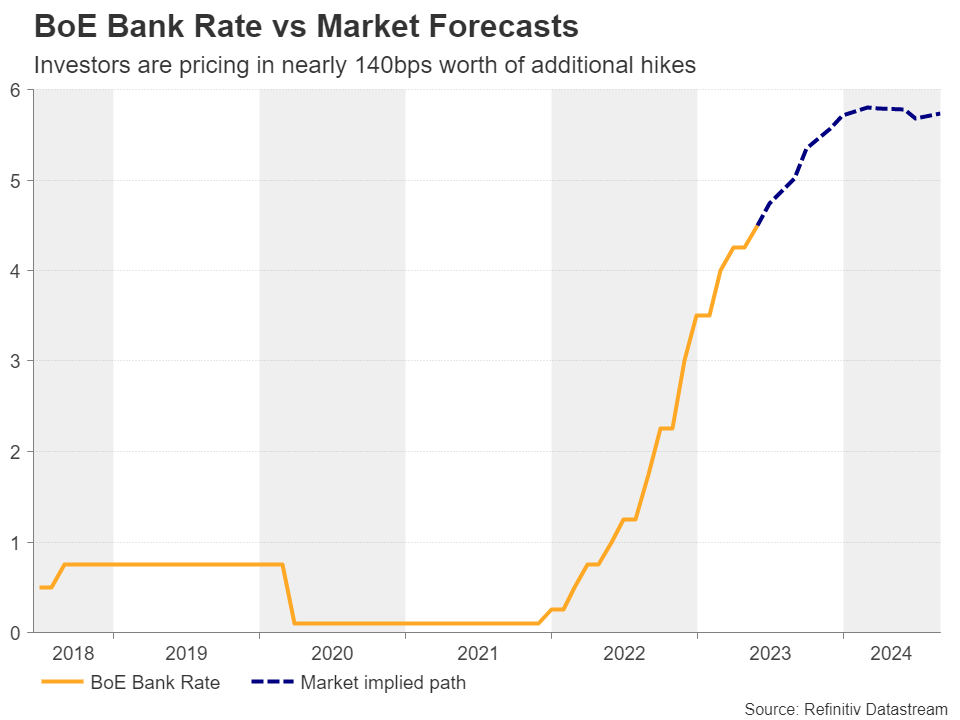

When they last met, BoE policymakers delivered their 12th successive rate hike, abandoning their recession calls and signaling that they will not hesitate to raise interest rates should inflation pressures persist.

Around two weeks after the decision, the inflation numbers for April revealed that the headline CPI slowed by less than expected, to 8.7% year-on-year from 10.1%, but what was much more worrisome was the unexpected acceleration in underlying inflation to 6.8% y/y from 6.2%. This suggested that price pressures are becoming more embedded in the broader economy, and that the decline in the headline rate was just the result of a slowdown in the prices of volatile items like energy.

So, after being criticized by politicians for his response to persistently high inflation, Governor Bailey is now under pressure to rise to the occasion and deliver not only another rate hike but also a message that is hawkish enough to satisfy everyone that’s been questioning the BoE’s ability to produce results.

Investors expect several more hikes

Market participants are also demanding more by the BoE. They are now pricing in around 140bps worth of additional rate increases, and that’s even after the PMIs for May disappointed. Perhaps, investors remained content with the fact that the composite index continued pointing to expansion, which enhances the view that the UK economy may have avoided a recession.

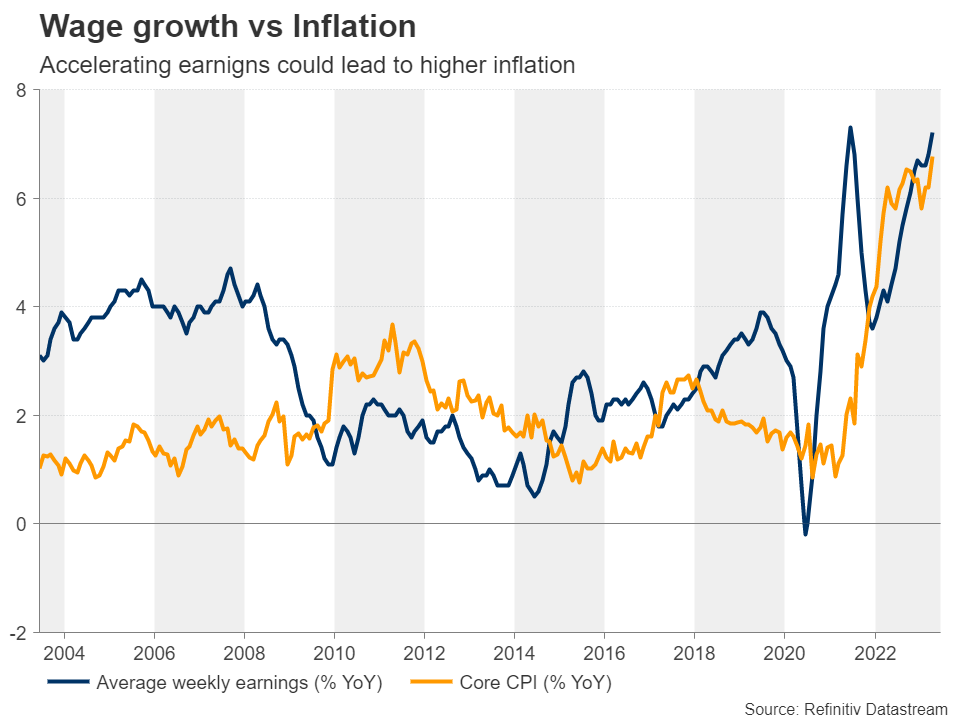

What may have also convinced them to maintain their hike bets is the employment report for April, which revealed a stronger-than-expected acceleration in wage growth and a small decline in the unemployment rate. Accelerating wages could translate into accelerating consumer demand and thereby higher inflation.

Therefore, pound traders will stay locked in front of their screens from the day before the meeting decision, when the UK CPI data for May are released. The headline rate is expected to have declined to 8.5% y/y from 8.7% and the core to have held steady at 6.8%, a combination that’s very unlikely to encourage market participants to scale back their hike bets.

Spotlight to fall on the accompanying statement

Putting all the aforesaid information into the same equation, a 25bps hike on its own on Thursday is unlikely to help the pound extend its latest gains. Actually, it could even trigger a small setback as traders assign a 25% probability for a bigger 50bps hike. With neither updated economic projections nor a news conference, the spotlight is likely to quickly turn to the accompanying statement.

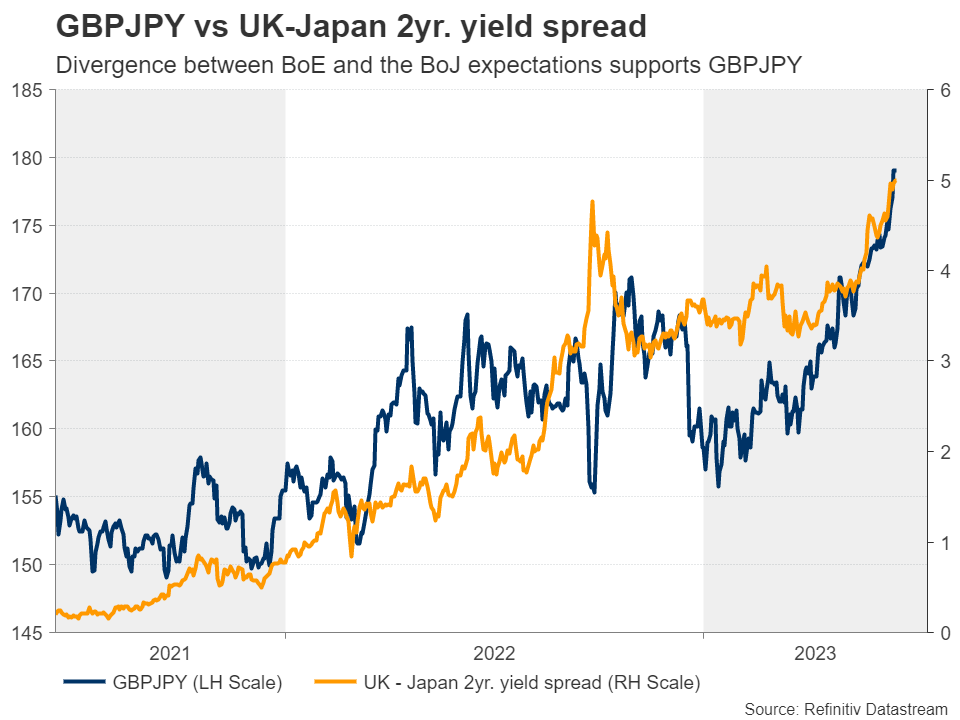

If officials turn more hawkish and say that they will continue raising rates until inflation is brought to heel, instead of noting that they will not hesitate to do so if price pressures persist, investors may feel comfortable adding to their long pound positions. The currency could gain the most against the wounded yen, which accelerated its tumble on Friday after the Bank of Japan kept its ultra-loose monetary policy untouched, maintaining its pledge to continue “patiently” with monetary policy easing.

Pound/yen could extend steep rally

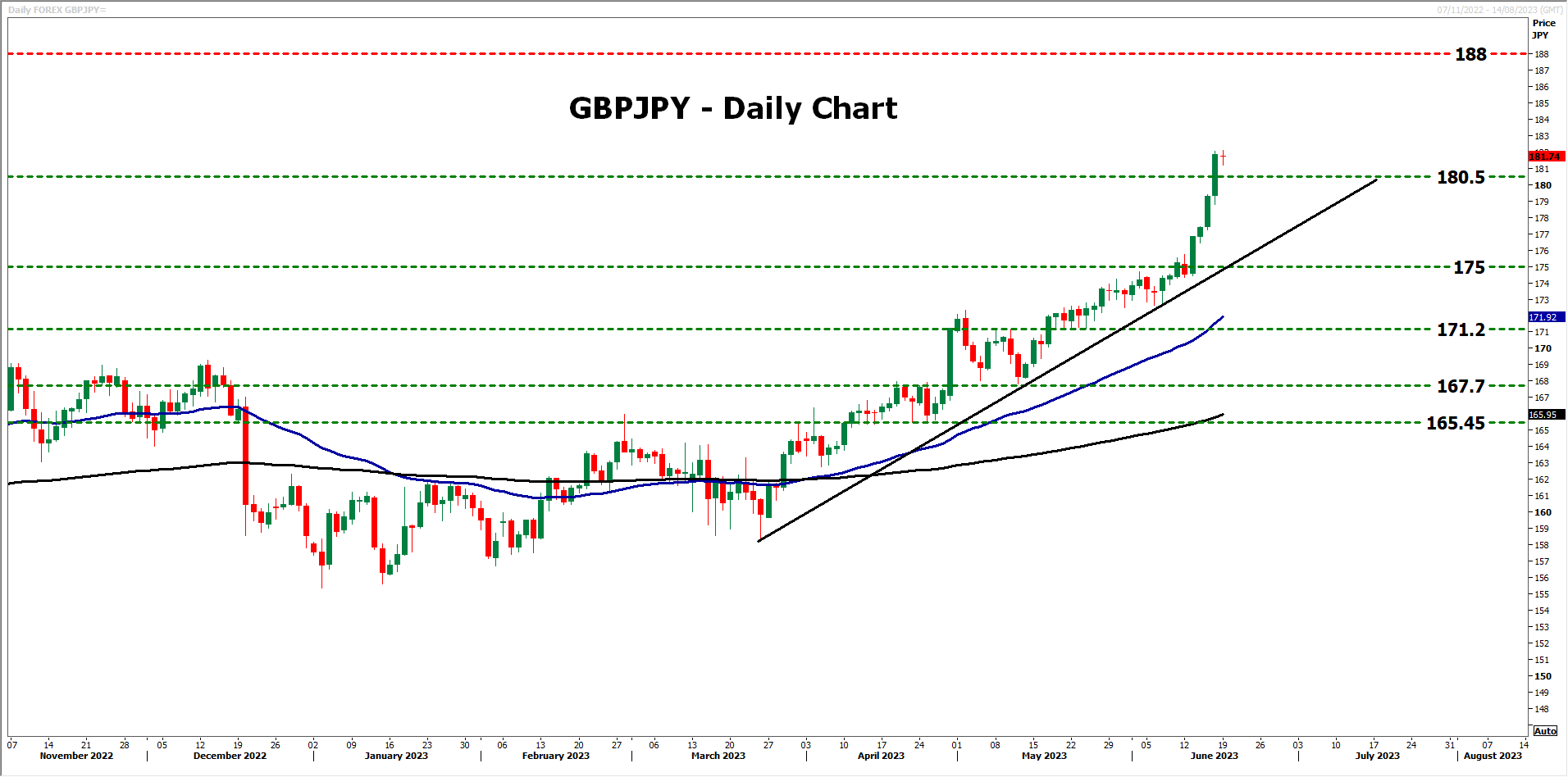

Pound/yen has been in a rally mode since last Tuesday and on Friday, it emerged above the 180.50 barrier, marked by the inside swing lows of September 7 and October 2, 2015. This, combined with the fact that the pair is trading above the steep uptrend line drawn from the low of March 24, paints an overly positive picture and a hawkish BoE may encourage traders to begin a journey towards the 188.00 zone, which acted as a ceiling back between August and November 2015.

Now, in the case of the Bank disappointing those expecting a more aggressive stance, the pair is likely to fall off the cliff and perhaps break the uptrend line. It could find initial support at around 175.00, but if the bulls are not willing to enter the action around there, the tumble may extend towards the 171.20 territory, which offered support between May 18 and 24.

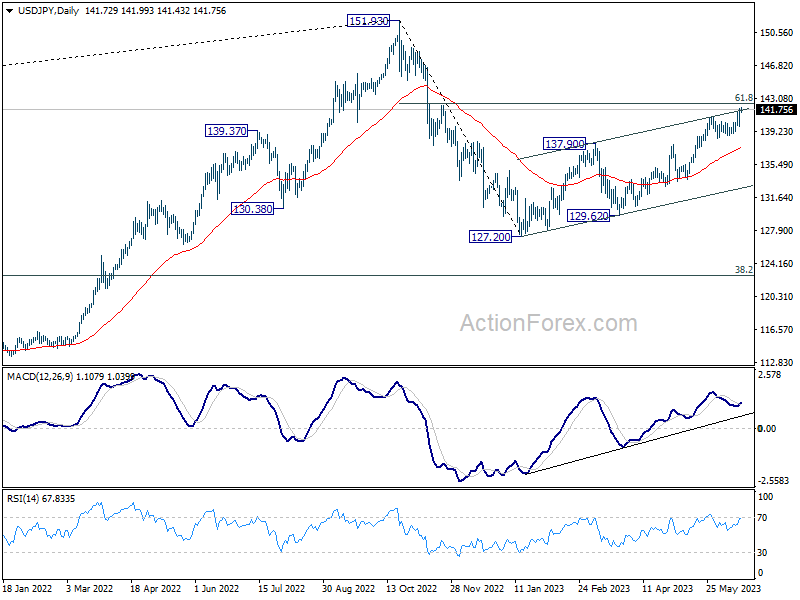

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 140.47; (P) 141.19; (R1) 142.54; More...

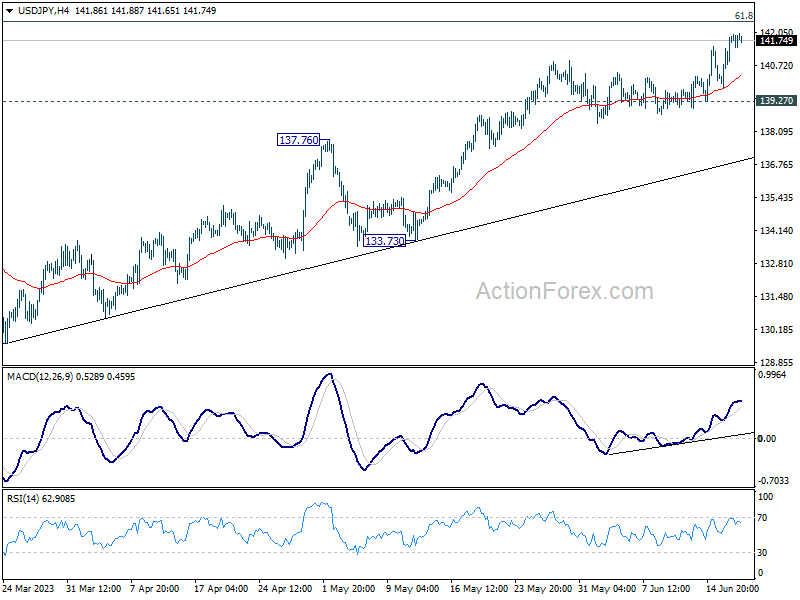

USD/JPY's rally is still in progress. Intraday bias remains on the upside for 61.8% retracement of 151.93 to 127.20 at 142.48 next. Sustained break there will pave the way back to retest 151.93 high. However, rejection by 142.48, followed by break of 139.27 will indicate short term topping and turn bias back to the downside.

In the bigger picture, rise from 151.93 are seen as a corrective pattern to up trend from 102.58. The first leg has completed at 127.20. Rebound from there is seen as the second leg, and should be limited below 151.93. Sustained trading below 55 D EMA (now at 137.47) will argue that the third leg has started back to 127.20 and possibly below.

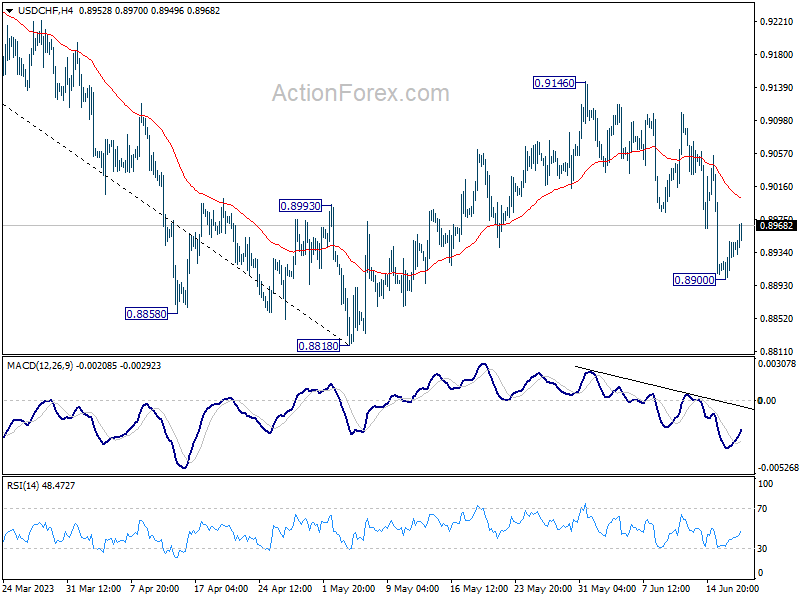

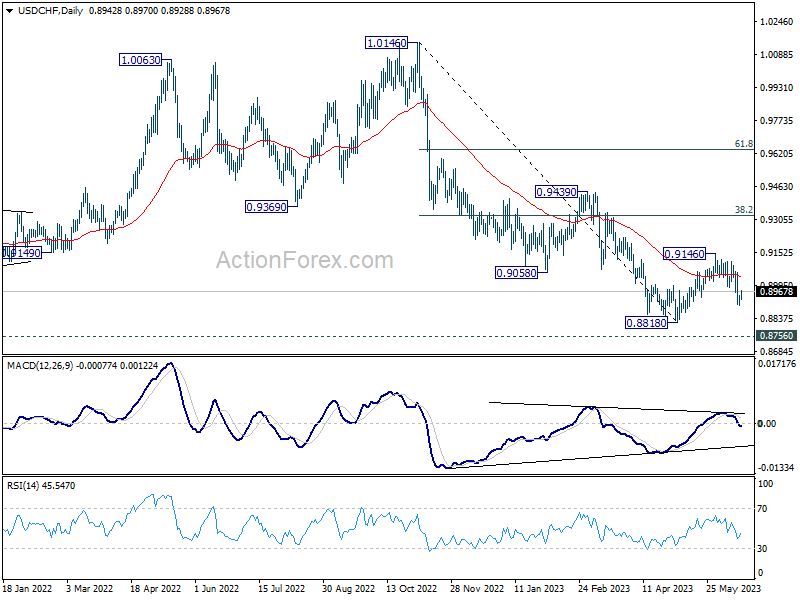

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8912; (P) 0.8930; (R1) 0.8959; More...

Intraday bias in USD/CHF is turned neutral with current recovery. But risk will stay on the downside as long as 0.9146 resistance holds. Below 0.8900 will target 0.8818 and possibly below. But strong support is still expected from 0.8756 to bring reversal.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming.

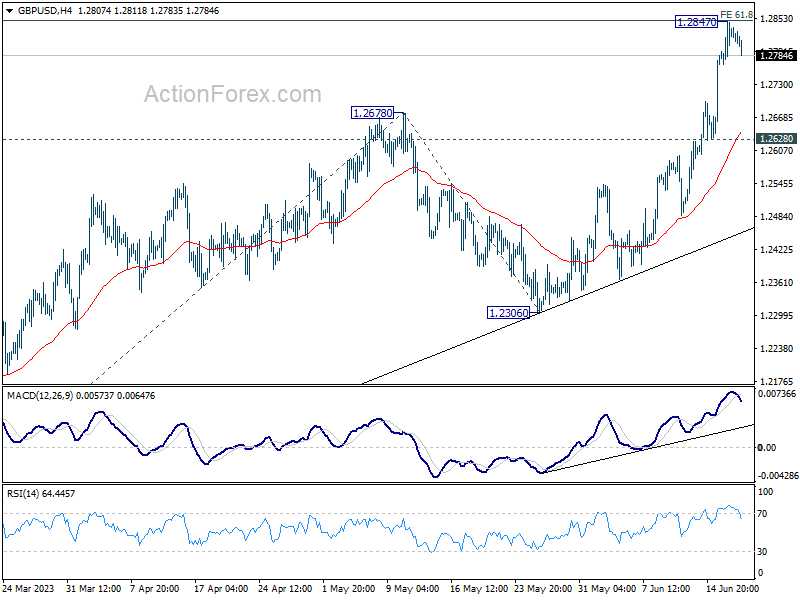

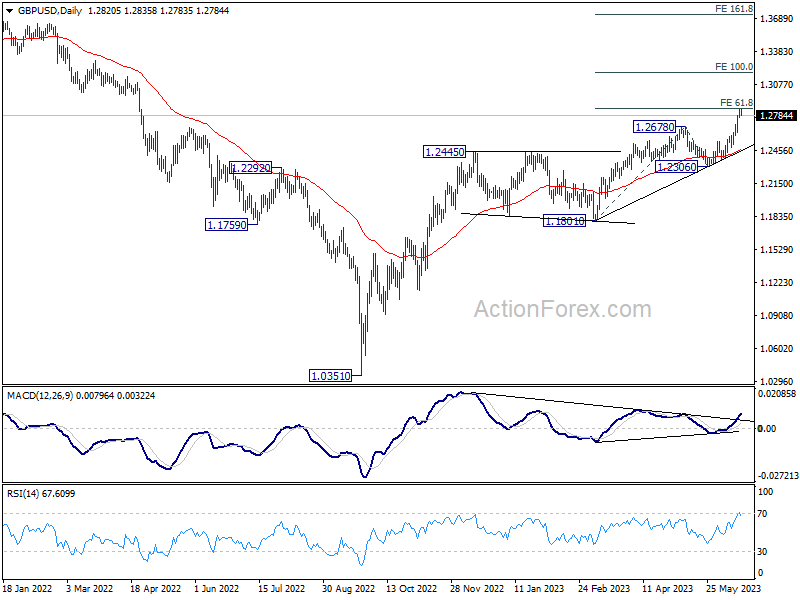

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2777; (P) 1.2812; (R1) 1.2857; More...

A temporary top is in place at 1.2847 in GBP/USD with current retreat, and intraday bias is turned neutral first. Some consolidations would be seen first, but downside should be contained above 1.2628 support to bring rise resumption. On the upside, firm break of 1.2847 will resume larger up trend and target 100% projection of 1.1801 to 1.2678 from 1.2306 at 1.3183 next.

In the bigger picture, the strong support from 55 W EMA (now at 1.2345) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

Sunset Market Commentary

Markets

ECB members filled today’s dull trading hours awaiting possible fireworks later this week. Comments coming from Frankfurt since last week’s 25 bps rate hike all point to the same scenario: firm backing to continue hiking in July, but more hesitance on the September outcome. Lack of unanimity on how to proceed from there logically explains why ECB President Lagarde kept all options last week during the Q&A session. Data-dependence it is with the September Monetary Policy Report providing new GDP & CPI forecasts. Belgian ECB governor Wunsch kicked off in fashion last week by saying that rate hikes may have to be continued beyond September as the central bank needs to see a sustainable drop in core inflation. So far that’s not the case, with big upward revisions to core CPI forecast in last week’s policy report as a consequence: 5.1% for this year (from 4.6%), 3% for next year (from 2.5%) and 2.3% (from 2.2%) for 2025. Other hawks, like ECB Holzmann or Vasle sounded more conditional: “if trends continue post-summer ECB move may be needed”. ECB Villeroy is in a more neutral camp; saying that interest rates are clearly in restrictive territory and that the ECB has covered most of the ground. His suggestion that the ECB will meet the inflation goal in 2 years doesn’t stroke with official forecasts though. ECB Kazimir today added that he is open for a September move by pointing out that fiscal policies aren’t helping in bringing inflation down. ECB Simkus believes that we’re close the end of the rate cycle, but doesn’t want to rush the September assessment. ECB Schnabel had a close look at hawkish rate hikes by the RBA and by the BoC last week and concluded that the ECB needs to keep raising rates and to err on the side of doing too much given upside risks to the inflation outlook. Both the RBA and BoC had to restart tightening campaigns after pausing too fast. Finally, chief economist Lane kept a very balance tone whereas in the past, he often erred on the dovish side of the aisle. Now he simply states that September is so far away so let’s see then whether there’s room for pause or not.

Traded volumes were low today. The absence of eco data, of US traders (Juneteenth holiday) and this week’s backloaded eco agenda explain a lot. European stock markets failed to build on last week’s momentum with EuroStoxx50 failing to take out this year’s cycle tops around 4400. Main indices lose around 0.5% today. Core bonds face some more selling pressure. German yields add 2.6 bps (2-yr) to 5.5 bps (30-yr). EUR/USD is going nowhere around 1.0925 with EUR/GBP still near key support just below 0.8550. All eyes are on UK CPI data (Wednesday) and the Bank of England verdict (Thursday) later. Will the BoE live up to hawkish market expectations or live up to its nickname of unreliable boyfriend?

News & Views

EU energy ministers balked at Poland’s requested and then secured subsidy extension for coal power plants until 2028. Sweden, which is currently chairing the EU presidency, has allowed the exemption considering Poland’s high reliance on coal currently (+/- 70% of its energy mix) and the need for a steady flow of energy when other (eg. renewable) forms were not available because of lack of stable storage and capacity in general. The extension should buy Poland more time to make the necessary investments. Germany, where coal provides about a quarter of the energy needed still, said that coal plants should run in times of need but giving them an extra subsidy is going too far.

Belgium successfully tapped three existing OLOs for a combined amount of €3.502bn. It sold €1.14bn of its OLO91 series (0% coupon, maturing October 2027) at a 2.878% yield. OLO97 (3%, June 2033) was tapped for €1.357bn with a yield of 3.089% while €1bn of OLO98 (3.3%, June 2054) bonds were sold at 3.518%. Investor interest was decent with bid-to-covers ranging between 1.98 and 2.23. The Belgian Debt Agency projected some €45bn of OLO issuance for 2023. Today’s auctions bring the total amount raised to date at €30.015bn, or 66.70%.

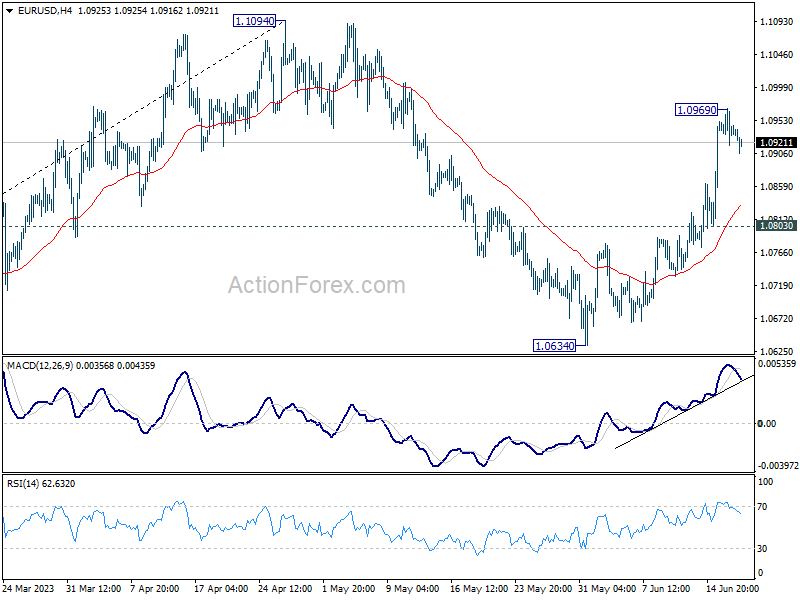

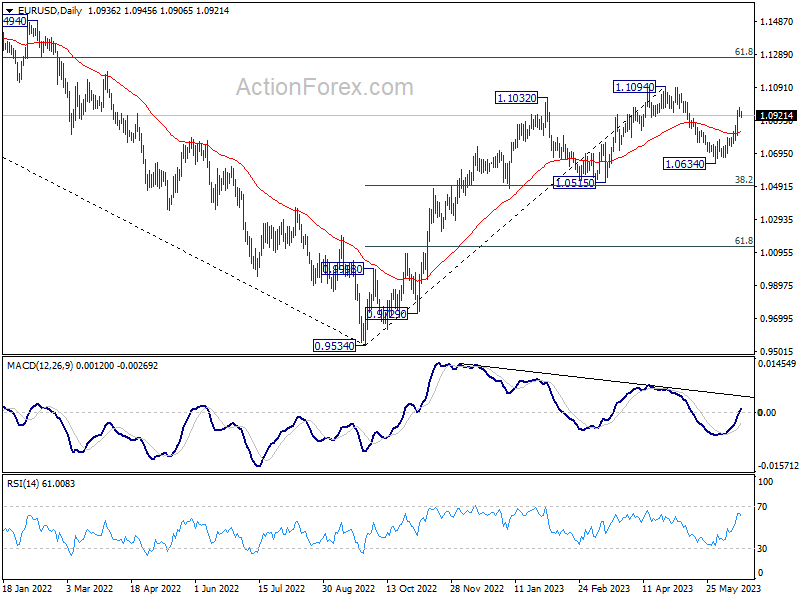

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0916; (P) 1.0944; (R1) 1.0969; More...

A temporary top is in place at 1.0969 with current retreat and intraday bias in EUR/USD is turned neutral first. Some consolidations could be seen. But further rally is expected as long as 1.0803 support holds. On the upside, above 1.0969 will resume the rise from 1.0634 to retest 1.1094 high. Decisive break there will confirm resumption of whole up trend from 0.9534. However, firm break of 1.0803 will extend the corrective pattern from 1.1094 with another falling leg, targeting 1.0634 and below.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Euro Ignores Hawkish ECB Comments, Markets Continue Consolidations

The forex markets are holding steady in a consolidative pattern today. Notably, Euro has remained largely unaffected by continued hawkish messages emanating from top ECB officials, who have merely echoed President Christine Lagarde's suggestion that an interest rate hike is likely in July, while situation in September remains uncertain.

Euro is the third weakest in trading today so far, trailing behind Aussie and Kiwi. Both of these are consolidating alongside other risk markets. Sterling and Swiss Franc are showing mixed performance as markets await rate decisions from the BoE and SNB later in the week. Dollar and Yen, meanwhile, are demonstrating signs of a modest recovery, while Canadian Dollar edges slightly ahead.

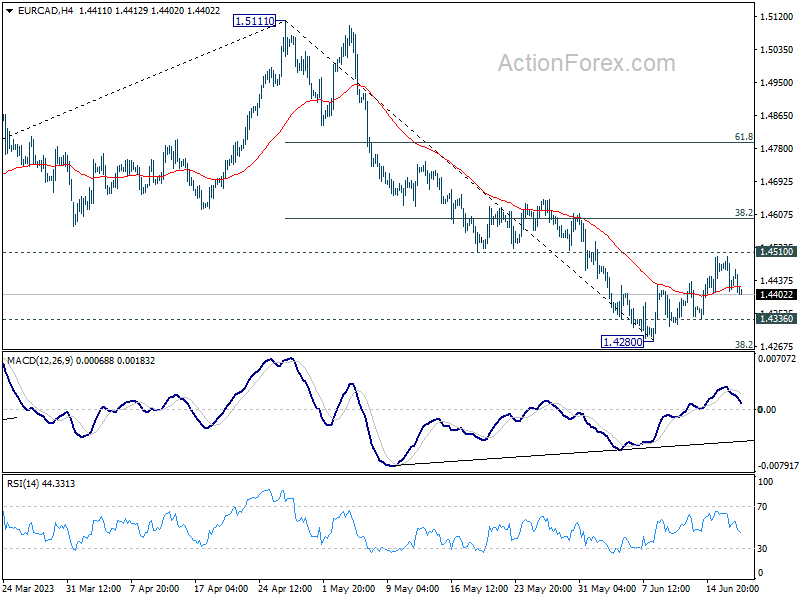

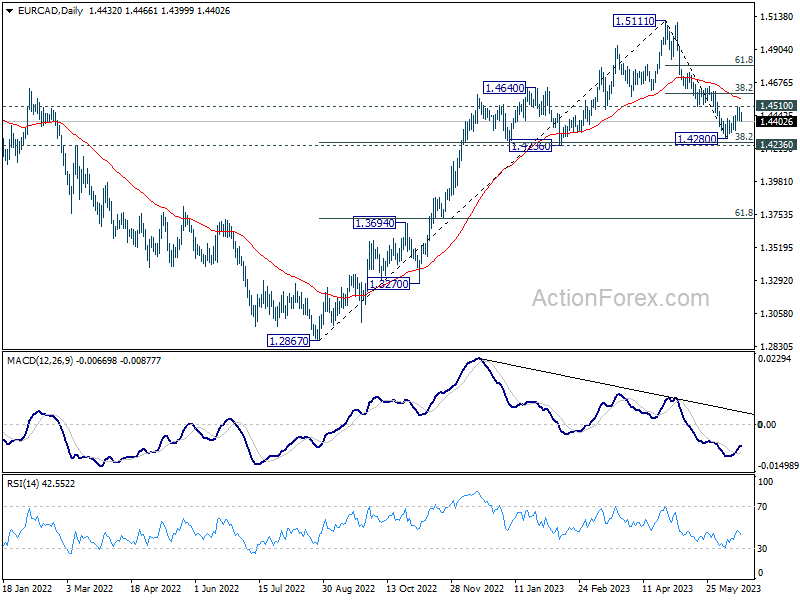

From a technical standpoint, the conditions appear ripe for a EUR/CAD rebound, with bullish convergence condition evident in 4H MACD. The 1.4280 mark is perilously close to 1.4236 cluster support (38.2% retracement of 1.2867 to 1.5111 at 1.4254). However, the current recovery momentum from 1.4280 is less than inspiring.

Should we witness a firm break above 1.4510 resistance, this would confirm short-term bottoming, leading to a stronger rise to 38.2% retracement of 1.5111 to 1.4280 at 1.4597 and above. Conversely, break below 1.4336 would suggest higher likelihood of an extended fall from 1.5111, pushing through 1.4236 cluster support.

In Europe, at the time of writing, FTSE is down -0.51%. DAX is down -0.77%. CAC is down -0.71%. Germany 10-year yield is up 0.0397 at 2.514. Earlier in Asia, Nikkei dropped -1.00%. Hong Kong HSI dropped -0.64%. China Shanghai SSE dropped -0.34%. Singapore Strait Times dropped -0.58%. Japan 10-year JGB yield fell -0.0090 to 0.395, below 0.4 handle.

ECB Lane: September is so far away, let's see

ECB Chief Economist Philip Lane emphasized the central bank's data-driven approach in managing inflation. Speaking today he suggested that another interest rate hike is likely in July, provided there are no significant changes in the economic outlook.

"At this point, we are surely data-driven," Lane stated, reflecting ECB's commitment to making policy decisions based on economic indicators and trends. "July is not so far away, we can say unless there's a material change another hike (is likely)."

Regarding further in September, however, Lane was more reserved. "But to me, September is so far away; let's see in September," he added.

Despite rising inflation, Lane remains optimistic about the medium-term outlook. "Inflation will come down fairly quickly in the next couple of years to ECB's 2% target," he predicted.

ECB Schnabel: We need to err on the side of doing too much

ECB Executive Board member Isabel Schnabel stressed the necessity of maintaining a proactive approach to monetary policy amid persistent inflation risks. In a speech today, she noted that "risks to the inflation outlook are tilted to the upside, reflecting both supply- and demand-side factors."

Referencing IMF's recent guidance, Schnabel noted, "The IMF has recently issued a clear recommendation: if inflation persistence is uncertain, risk management considerations speak in favour of a tighter monetary policy stance."

She further explained the rationale behind this approach. "First, the costs of protecting the economy from upside risks to inflation are comparatively small, as the policy rate can be brought back to neutral levels faster than if policymakers acted under the assumption of low inflation persistence," Schnabel said.

The second reason revolves around the high costs of reactive policies. Schnabel pointed out, "it is very costly to react only after upside risks to inflation have materialized, as this could destabilise inflation expectations and thus require a sharper contraction in output to restore price stability."

Overall, Schnabel emphasized the need for data-dependent decisions that lean towards more action rather than less. "We need to remain highly data-dependent and err on the side of doing too much rather than too little," she asserted.

She insisted, "We thus need to keep raising interest rates until we see convincing evidence that developments in underlying inflation are consistent with a return of headline inflation to our 2% medium-term target in a sustained and timely manner."

ECB Kazimir: We need to deliver another rate hike in July

ECB Governing Council member Peter Kazimir stressed today the necessity for continued monetary policy tightening to address prevailing inflationary pressures. he specifically highlighted the need for another rate hike in July to move further into a restrictive policy stance.

"We need to deliver another rate hike in July and move further into restrictive territory," Kazimir stated. He underscored that a continuation of monetary policy tightening is "the only reasonable way ahead."

Looking ahead to September, Kazimir cautioned that an updated analysis would be required to assess the impact of ECB's rate hike cycle before proceeding with further tightening measures. However, he emphasized that halting rate hikes prematurely presents a "much more significant" risk than overtightening.

Kazimir drew attention to several factors contributing to inflation risks, asserting, "Upward inflation risks are still substantial, linked to the labour market situation, food prices and, last but not least, profit margins."

NZ BNZ services jumped back to 53.3, economy still on a broader slowing trajectory

New Zealand's BusinessNZ Performance of Services Index climbed from 50.1 in April to 53.3 in May, revealing a slight uptick in the services sector. However, it's worth noting that this figure remains marginally under long-term average of 53.6. A closer look at the numbers shows activity/sales leaping from 45.4 to 52.0, employment increasing from 50.5 to 52.6, and new orders/business ascending from 50.1 to 55.4. Stocks inventories slightly declined from 57.1 to 56.8, while supplier deliveries edged up from 50.6 to 51.1.

BusinessNZ's Chief Executive Kirk Hope shared his insights, stating, "The lift in expansion for May also saw a pickup in the proportion of positive comments, which rose from 39.8% in April to 50.6% for the current month." He further added that while there weren't any defining themes, the overall positive comments were "either industry-specific or very general around increased activity."

Nonetheless, the economy appears to be on a deceleration trajectory, which, according to BNZ Senior Economist Craig Ebert, is necessary to deflate the inflationary pressures.

"The bounce back in the PSI in May arguably helped calm a lot of nerves – after it sagged to 50.1 in April, and after the services component of Q1 GDP declined 0.6%. Still, this doesn't deny the economy is on a broadly slowing trajectory, which is what's required to take the inflationary heat out of it," Ebert explained.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0916; (P) 1.0944; (R1) 1.0969; More...

A temporary top is in place at 1.0969 with current retreat and intraday bias in EUR/USD is turned neutral first. Some consolidations could be seen. But further rally is expected as long as 1.0803 support holds. On the upside, above 1.0969 will resume the rise from 1.0634 to retest 1.1094 high. Decisive break there will confirm resumption of whole up trend from 0.9534. However, firm break of 1.0803 will extend the corrective pattern from 1.1094 with another falling leg, targeting 1.0634 and below.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI May | 53.3 | 49.8 | 50.1 | |

| 12:30 | CAD | Industrial Product Price M/M May | -1.00% | 0.20% | -0.20% | -0.60% |

| 12:30 | CAD | Raw Material Price Index M/M May | -4.90% | 2.40% | 2.90% | 1.80% |

| 14:00 | USD | NAHB Housing Market Index Jun | 50 | 50 |