Sample Category Title

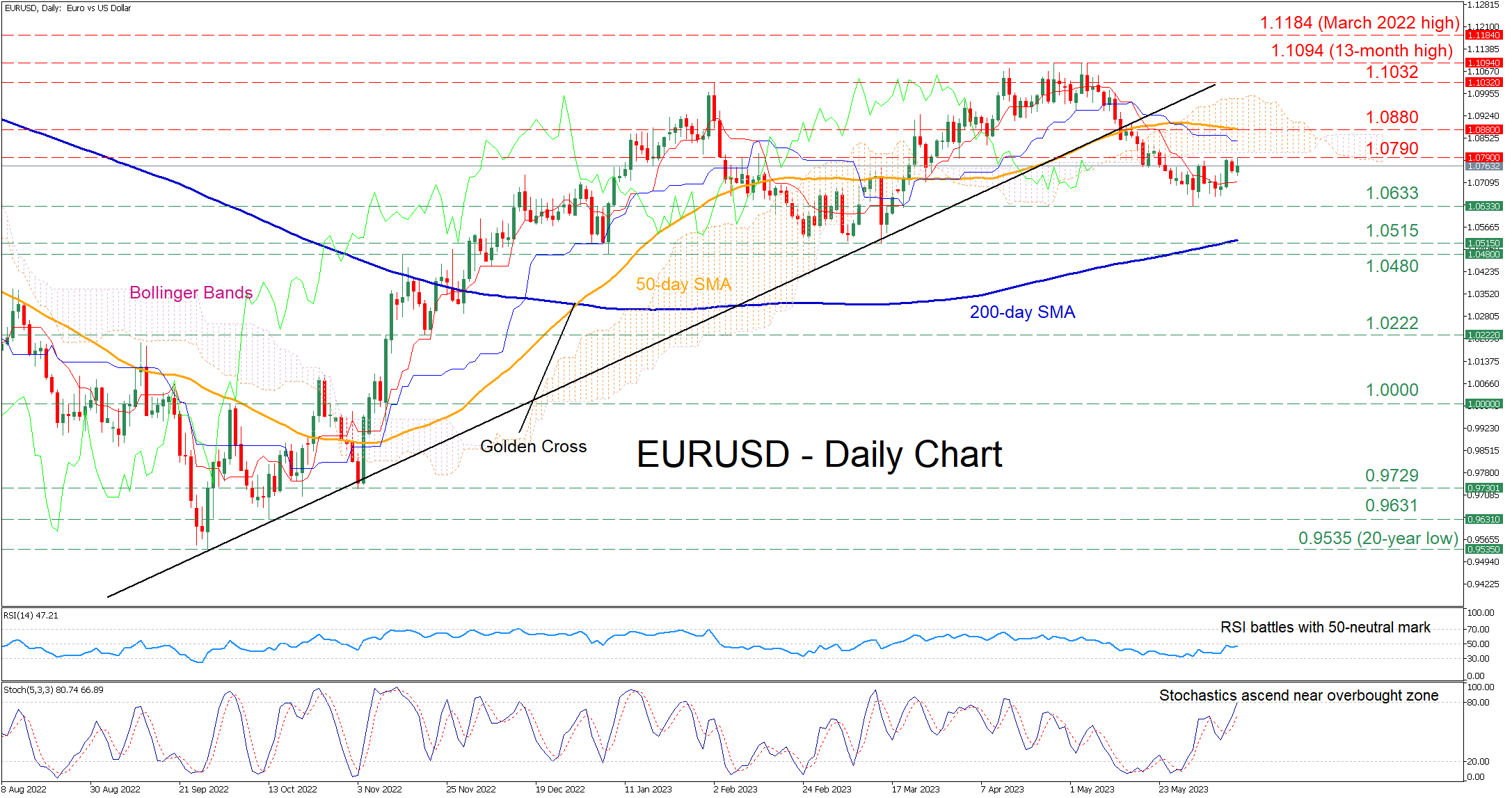

EURUSD Faces Tough Barrier Near 1.0800

EURUSD has been experiencing a downside correction after peaking at the 13-month high of 1.1094 in late April. In addition, the pair sliced through both its 50-day simple moving average (SMA) and the ascending trendline that connected its lows since September 2022, while its latest attempts for recovery have been repelled just shy of the 1.0800 region.

The momentum indicators are reflecting a cautiously bullish near-term bias. Specifically, the stochastic oscillator is ascending steeply near its 80-overbought zone, while the RSI is battling with its 50-neutral mark. Nevertheless, the price action remains below the Ichimoku cloud, endorsing a broader bearish short-term picture.

If the positive momentum intensifies further, the 1.0790 barrier could prove to be the first obstacle for buyers to clear. Surpassing that zone, the price could advance towards the 50-day SMA, currently at 1.0880. Even higher, the February peak of 1.1032 might fend off any upside moves before the 13-month high of 1.1094 gets tested.

Alternatively, bearish actions could send the price to test the recent low of 1.0633. Diving lower, the pair may encounter support at the March double-bottom region of 1.0515. A violation of that territory could pave the way for the 2023 low of 1.0480 observed in January.

In brief, despite managing to halt its retreat, EURUSD seems to be struggling to recover some of its lost ground. For that to happen, the pair needs to decisively cross above its 50-day SMA.

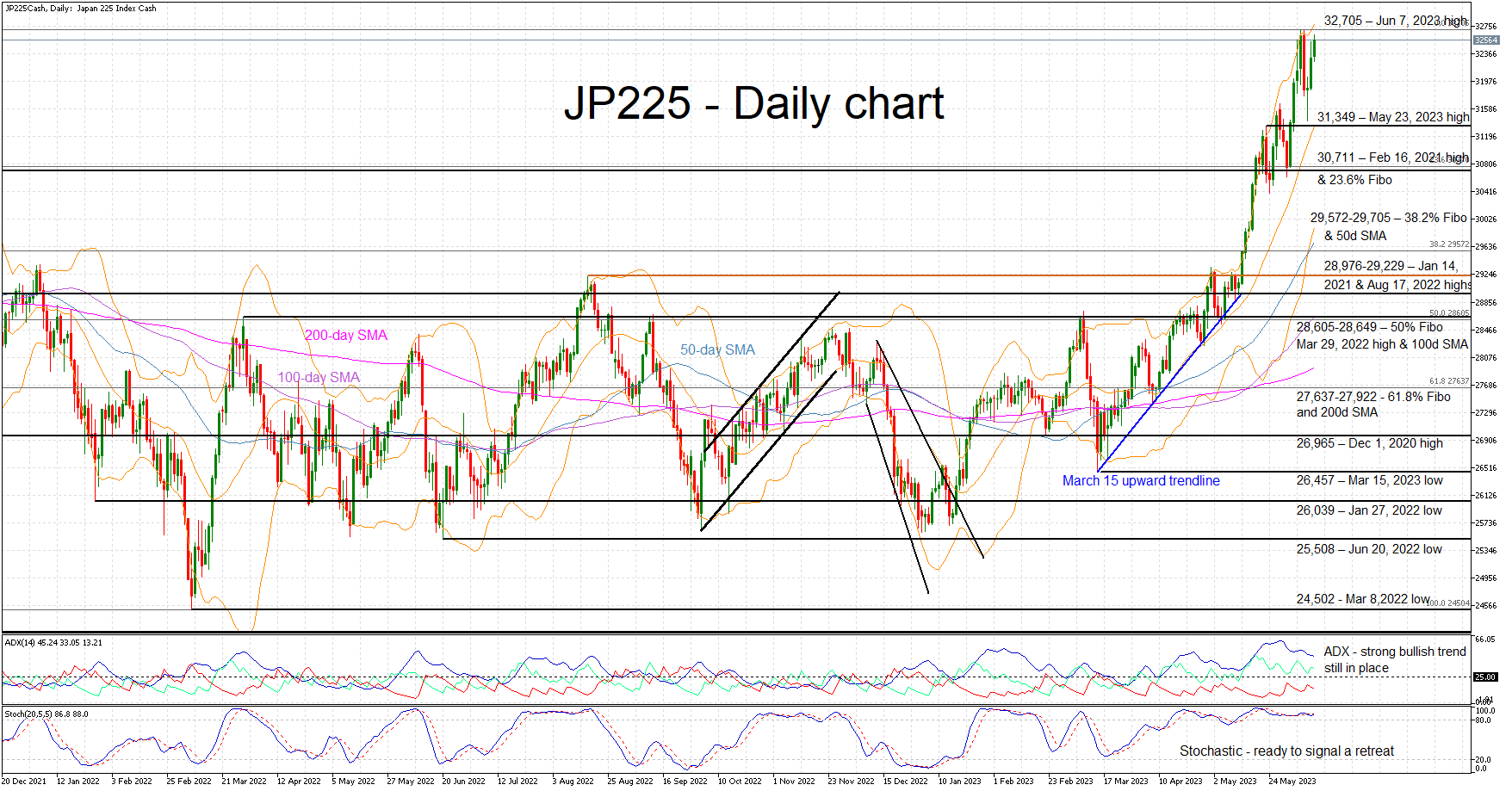

JP225 Cash Index Ready for Higher High But Overall Move Looks Overstretched

The JP225 cash index is hovering a tad below the all-time high of 32,705 as the bulls have successfully managed to limit the bearish pressure. It has been an explosive 32% rally from the March 15, 2023 low with almost no corrections taking place. The move appears to be overstretched and maybe a small pullback could be welcomed by both sides.

The stochastic oscillator is confirming this overstretched nature as it continues to trade at its overbought (OB) territory, hovering around its moving average. A break below its OB area would clearly be seen as a bearish signal. In the meantime, the Average Directional Movement Index (ADX) is still pointing to a bullish but gradually weakening trend.

If the stochastic indicator delivers a bearish signal, the bears would quickly like to break the 31,349 level and target the busier 30,711 area set by the February 16, 2021 high and the 23.6% Fibonacci retracement level of the March 8, 2022 – June 7, 2023 uptrend. Even lower, the 29,572-29,705 range would probably be the first true test of the bears’ resolve.

If the bulls decide to ignore the mixed technical signs, they would aim at retesting the all-time high of 32,705. If successful, they would have the chance to record higher highs with 33,000 being the first step.

To sum up, the JP225 index bulls are preparing for a higher high. However, they seem to understand the need for a short-term correction following the aggressive rally since the March 15 low.

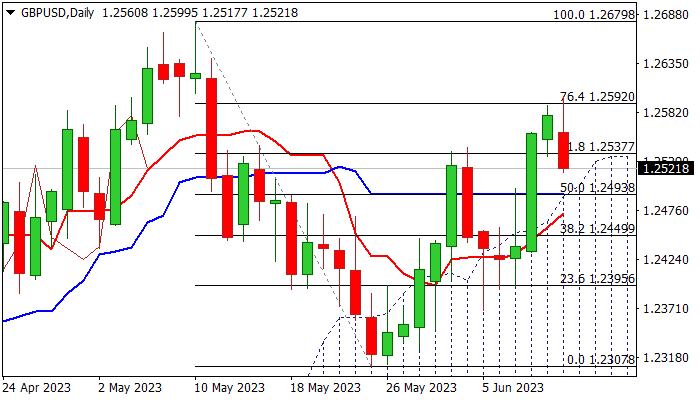

GBP/USD: Larger Bulls Pause Ahead of Key Economic Events

Cable pulled back from new one-month high on Monday, as traders collected profits from rally in past three days.

Overbought daily studies contributed to decision, though investors exited longs ahead of key events this week – UK jobs/earnings and US CPI data on Tuesday and Fed rate decision on Wednesday, which are expected to generate fresh direction signals.

Economists expect US annualized inflation to fall to 4.1% in May, from 4.9% in April, while core inflation is expected to drop to 5.3% in May from 5.5% previous month, which will add to broad expectations of the Fed staying on hold in June policy meeting.

This would add to scenario that current pullback is just positioning for fresh push higher on dovish Fed.

Fresh easing should ideally find ground around strong supports at 1.2493 (top of rising daily cloud / daily Kijun-sen / broken Fibo 50% of 1.2679/1.2307) to keep larger bulls intact.

Caution on penetration of thick daily cloud and violation of daily Tenkan-sen (1.2473) which would open way for deeper pullback.

Res: 1.2537; 1.2599; 1.2640; 1.2679.

Sup: 1.2493; 1.2473; 1.2450; 1.2395.

Sunset Market Commentary

Markets:

Markets took a guarded but constructive start to a week that might be key in shaping investors’ expectations on the Fed’s (and to a lesser extent the ECB’s) intentions during summer. At the same time, tomorrow’s May US CPI release might still complicate positioning in the run-up to Wednesday’s Fed decision. With especially the US 2-y yield only a whisker away from the key 4.63% resistance (end May top), some consolidation/cautiousness ahead of the Fed policy meeting is quite logical. In technical trade, US yields are changing less than 2 bps across the curve. This evening, the US will sell $40bn of 3-y notes and $32bn of 10-y bonds as the Treasury starts refilling its coffers after the removal of the debt ceiling. Markets will closely monitor investor appetite for the sale. German Bunds slightly outperform. The 2-y & 5-y yield are ceding 3 bps. The 30-y trades unchanged. The ECB on Thursday probably will reiterate that it still has work to do to bring (core) inflation sustainably to the 2% target. At the same time, we don’t expect any detailed guidance yet, especially not on what will happen after the July meeting. This is leaving markets comfortable with discounting a peak ECB rate near 3.75%. The debate on additional steps probably might resurface post summer, when the easy inflation gains due to lower energy prices have materialized, while core inflation at that time still might prove much more sticky. However, it is too early for markets already to make up their mind on the likelihood of such a scenario. Even as the Fed ‘skip scenario’ doesn’t intend to signal the end of the cycle, equity investors apparently still see it as indication of a balanced approach that won’t aggressively kill growth in the near term. The Eurostoxx 50 gains 0.70.%. The cycle top of 4412,88 is still only about 2% away. The S&P 500 (+0.3%) for now also continues its post-March uptrend and nears the August 2022 top. Oil still struggles with Brent ($72,85/b) not that far away from the 2023 lows just above $70/b).

Technical considerations dominated trading in the major FX cross rates as well. EUR/USD extends its recent bottoming pattern. The 1.0790 area was again tested but upcoming event risk prevented a break (currently 1.077). The yen is going nowhere (USD/JPY 139.30) ahead of Friday’s BoJ policy decision. Sterling today fell prey to profit taking. EUR/GBP this morning extensively tested the 0.8547 area (December low), but rebounded to currently trade near 0.858. Tomorrow’s UK labour market data will be a next reality check on the 5.5% BoE policy rate peak markets currently are discounting.

News & Views

Czech inflation rose by 0.3% M/M in May, outpacing the consensus estimate of 0.1% M/M. The Y/Y-reading decreased slightly less than hoped, from 12.7% to 11.1%. The May inflation figure was 0.5 percentage point lower than expected in the CNB’s spring forecast though. This was due mainly to weaker-than-expected core inflation and, to a lesser extent, slower annual food price inflation (11.8% Y/Y) and a deeper decline in fuel prices (-21.1% Y/Y). Core inflation slowed to 8.6% Y/Y, reflecting a fading of foreign producer price inflation and a cooling of domestic demand. The latter is causing a gradual correction of the until recently increasing profit margins of producers, retailers and service providers. The CNB predicts inflation to fall to single digits in the summer months and to the 2% inflation target over the monetary policy horizon (Q2-Q3 2024). The Czech Koruna extended last week’s correction with EUR/CZK currently testing the May tops in the 23.75/80 area.

The Swedish SEB bank housing price indicator jumped by 18 points in June, to 11. The positive reading indicates that, for the first time in a year, more Swedes believe that home prices will rise rather than fall. The Swedish housing market was stabilizing over the past months after losing around 15% from peak levels early 2022. “A combination of the worst interest rate storm passing and a stable labor market is giving households wind in their sails for a more positive view of the housing market,” according to the SEB statement. The Swedish krone holds near (weakest) levels only seen during GFC early 2023 (EUR/SEK > 11.60)..

Markets Mixed ahead of Fed and ECB; Aussie Extending Rally With Eyes on Copper and China

The forex markets are relatively mixed with a near empty economic calendar today. Australian Dollar is extending last week's rally, while Euro and Yen are following as next strongest. On the other hand, Swiss Franc and Sterling are trading as the worst performers. Dollar is currently mixed in the middle, displaying no definitive directional trajectory.

Two monumental events this week will significantly sway the markets - Fed and ECB interest rate decisions. Simultaneously, BoJ will also meet, and the UK is set to release a slew of crucial economic data that could cause ripples in the market waters.

Notably, the softening of both oil and copper prices is also a crucial element in the global financial scene, deserving a significant mention. Specifically, for Australian Dollar, market sentiment and metal prices could be influenced heavily by China's economic data. Any disheartening figures from China have the potential to truncate Aussie's short-term rally.

In Europe, at the time of writing, FTSE is up 0.19%. DAX is up 0.78%. CAC is up 0.68%. Germany 10-year yield is down -0.0272 at 2.351. Earlier in Asia, Nikkei rose 0.52%. Hong Kong HSI rose 0.07%. China Shanghai SSE dropped -0.08%. Singapore Strait Times rose 0.29%. Japan 10-year JGB yield dropped -0.0059 to 0.429.

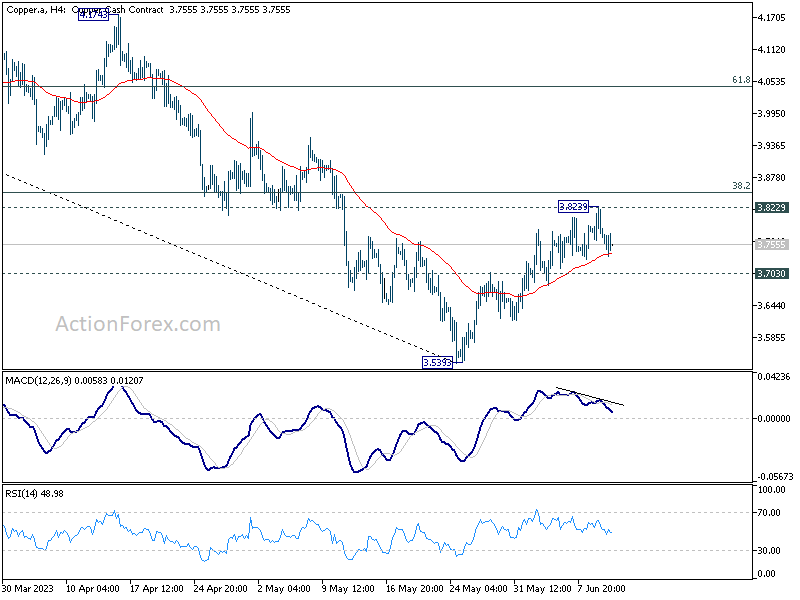

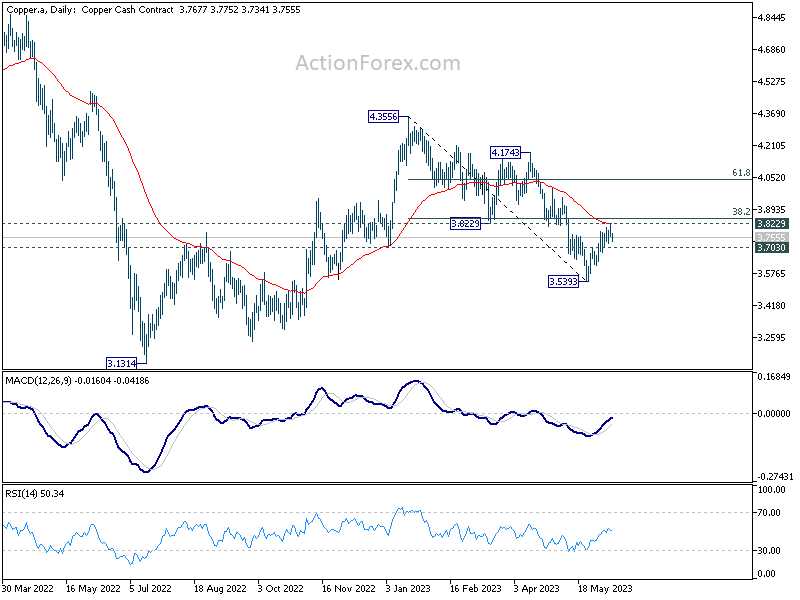

Copper dips after hitting strong cluster resistance

Copper prices dip notably today as metal traders appeared to be turning cautious ahead of FOMC rate decision. In addition, the market needs to seek direction from Chinese data including investment and production to gauge the outlook of demand.

Technically, Copper is facing a key cluster resistance zone at around 3.8229 support turned resistance, 55 D EMA (now at 3.8200), as well as 38.2% retracement of 4.3556 to 3.5393 at 3.8511. Rejection by this resistance zone, followed by 3.703 near term support will bring deeper fall back to 3.5393 low, with prospect of resuming the whole down trend from 4.3556. Given the correction between Australian Dollar and Copper, this bearish scenario could push AUD/USD back towards 0.6457 low.

On the other hand, sustained break of 3.8229/8511 will argue that whole fall from 4.3556 has completed with three waves down, and turn outlook bullish for 61.8% retracement at 4.0438 and above. This bullish development could help push AUD/USD through structural resistance at 0.6817 decisively.

WTI crude oil eyes 67 support as selling intensifies

Oil prices trade deeply lower today as the impact of Russian supply recovery was more than enough to offset Saudi Arabia production cut. Indeed, Goldman Sachs has lowered its WTI forecast for December from 89 to 81 (above current level at around 68 though).

Technically speaking, WTI crude oil was clearly rejected by falling 55 D EMA repeatedly, keeping outlook bearish. Immediate focus is now on 67.05 support. Firm break there could prompt downside acceleration through 63.67 low to 61.8% projection of 83.46 to 63.67 from 74.38 at 62.14. Also,l outlook will stay bearish as long as 74.38 resistance holds, in case of another recovery.

BoE's Haskel: Important to lean against risks of inflation momentum

In an article penned for The Scotsman newspaper, BoE Monetary Policy Committee member Jonathan Haskel signaled the potential for further increases in interest rates, citing persistent inflation concerns.

Haskel highlighted an improvement in UK's inflation outlook, observing, "Things look better than a few months ago. Since October last year, inflation has fallen from 11.1 per cent to 8.7 per cent, and we expect it to be around 5 per cent by the end of this year."

However, he expressed concern that "inflation remains much too high," reaffirming the MPC's commitment to achieving its 2% target. "Our tool for doing this is interest rates," he added.

"My own view is that it's important we continue to lean against the risks of inflation momentum, and therefore that further increases in interest rates cannot be ruled out," he said.

Haskel addressed the often-asked question of how increasing interest rates can help when inflation is driven by the prices of essential goods like energy and food, largely determined at a global level.

He clarified, "The aim of higher interest rates is not to affect the prices of these goods directly. Instead, it is to ensure the resulting inflation does not become embedded in the economy and prices do not continue to increase at the rates we've seen recently."

Markets brace for Fed, ECB and BoJ, as well as UK data

As June unfolds, global financial markets brace for a cavalcade of central bank decisions following last week's unexpected moves by RBA and BoC. Both banks sent shockwaves through the market with their surprise rate hikes. As we gear up for a busy week ahead, market participants will have a keen eye on Fed, ECB and BoJ, anticipating their monetary policy decisions amid an intricate economic landscape.

As market forecasts a 70% chance of maintaining status quo, Fed is likely to hold the line on tightening during this week's FOMC meeting, leaving interest rates untouched at 5.00-5.25%. However, in the wake of last week's unexpected moves by RBA and BoC, nothing can be definitively ruled out. Regardless of the decision, the focus will be on Fed's new economic projections and dot plot, revealing policymakers' terminal rate expectations and potential timing for rate cuts. The release of key economic data including CPI, PPI, retail sales, and U of Michigan consumer sentiment will also potentially stir the markets.

Meanwhile, ECB is anticipated to raise the main refinancing rate by 25bps to 4.00%. While continued tightening bias is expected, ECB President Christine Lagarde will likely emphasize the data-dependency and meeting-by-meeting approach of future decisions. Given recent unexpected dips in inflation data, inflation outlook detailed in the new economic projections will be crucial. Other noteworthy data from Eurozone include German ZEW economic sentiment.

In contrast, BoJ is expected to keep monetary policy unchanged, holding the short-term interest rate at -0.10% and capping 10-year JGB yield at 0.50%. Governor Kazuo Ueda is likely to reiterate that expected slowing in inflation rate in the second half of the year necessitates continuation the current ultra-loose monetary policy. Lack of violent fluctuations in 10-year JGB yields recently suggest that market participants not speculating on any changes. A clearer picture of BoJ's next steps might not emerge until release of July's updated Outlook for Economic Activity and Prices.

In the UK, employment and wage growth data, along with GDP and production figures, will play a crucial role in solidifying another rate hike by BoE next week. Other significant data releases to monitor include China's industrial production, retail sales, and fixed asset investment, as well as Australia's employment figures.

Here are some highlights for the week:

- Tuesday: Japan BSI manufacturing; Australia Westpac consumer sentiment, NAB business confidence; UK employment; Germany CPI final, ZEW economic sentiment; US CPI.

- Wednesday: New Zealand current account; UK GDP, production, trade balance; US PPI, FOMC rate decision.

- Thursday: New Zealand GDP; Australia employment; Japan machine orders, trade balance, tertiary industry activity; China industrial production, retail sales, fixed asset investment; Swiss PPI, SECO economic forecasts; Eurozone trade balance, ECB rate decision.; Canada manufacturing sales; US retail sales, Empire state manufacturing, Philly Fed survey, jobless claims, import prices, industrial production, business inventories.

- Friday: New Zealand BusinessNZ manufacturing; BoJ rate decision; Eurozone CPI final; wholesale sales; US U of Michigan sentiment.

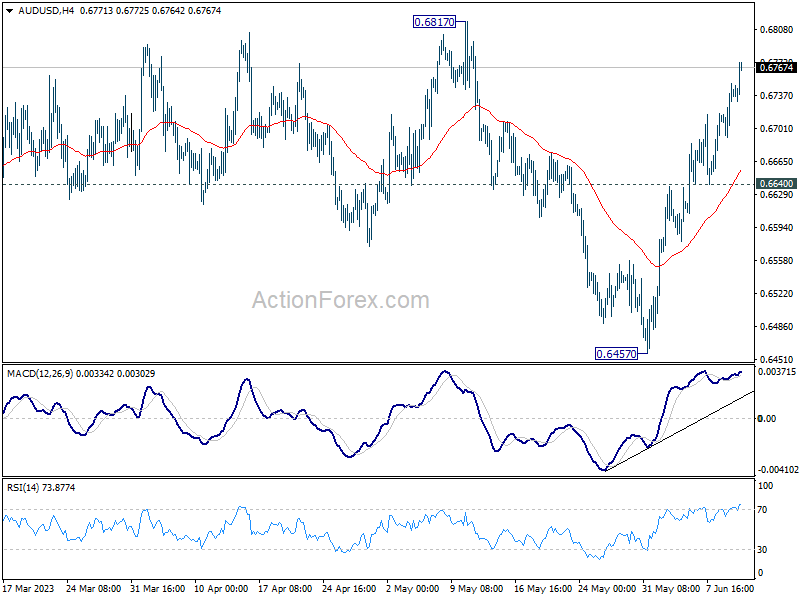

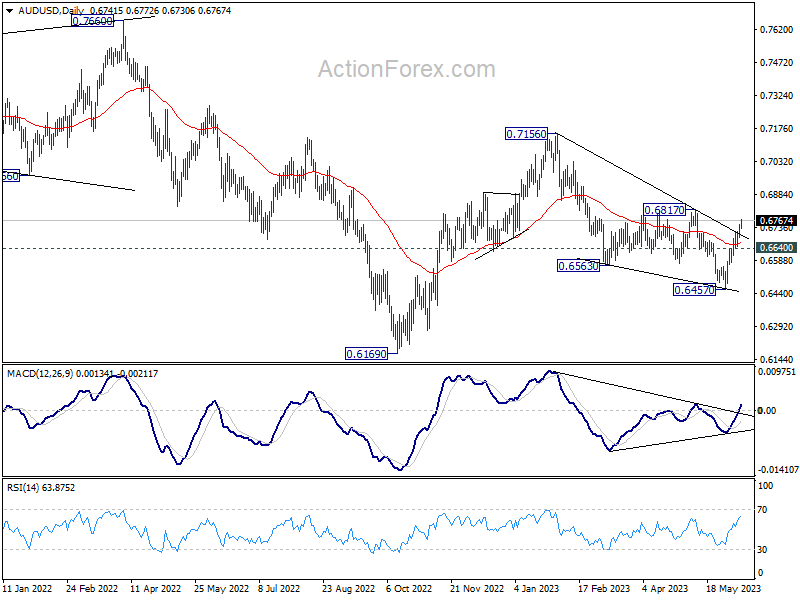

AUD/USD Daily Report

Daily Pivots: (S1) 0.6708; (P) 0.6729; (R1) 0.6766; More...

Intraday bias in AUD/USD remains on the upside for 0.6817 structural resistance. Decisive break there will carry larger bullish implications. On the downside, however, break of 0.6640 minor support will turn bias back to the downside for retesting 0.6457 low again.

In the bigger picture, fall from 0.7156 is still in favor to continue as long as 0.6817 resistance holds. Prior rejection by 55 W EMA (now at 0.6801) keeps medium term outlook bearish. Break of 0.6457 will target 0.6169 key support (2022 low). Nevertheless, firm break of 0.6817 will indicate that fall from 0.7156 has completed in a three-wave corrective structure. Rise from 0.6169 would then be ready to resume through 0.7156.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y May | 5.10% | 5.50% | 5.80% | 5.90% |

| 06:00 | JPY | Machine Tool Orders Y/Y May F | -22.20% | -14.40% |

Copper dips after hitting strong cluster resistance

Copper prices dip notably today as metal traders appeared to be turning cautious ahead of FOMC rate decision. In addition, the market needs to seek direction from Chinese data including investment and production to gauge the outlook of demand.

Technically, Copper is facing a key cluster resistance zone at around 3.8229 support turned resistance, 55 D EMA (now at 3.8200), as well as 38.2% retracement of 4.3556 to 3.5393 at 3.8511. Rejection by this resistance zone, followed by 3.703 near term support will bring deeper fall back to 3.5393 low, with prospect of resuming the whole down trend from 4.3556. Given the correction between Australian Dollar and Copper, this bearish scenario could push AUD/USD back towards 0.6457 low.

On the other hand, sustained break of 3.8229/8511 will argue that whole fall from 4.3556 has completed with three waves down, and turn outlook bullish for 61.8% retracement at 4.0438 and above. This bullish development could help push AUD/USD through structural resistance at 0.6817 decisively.

WTI crude oil eyes 67 support as selling intensifies

Oil prices trade deeply lower today as the impact of Russian supply recovery was more than enough to offset Saudi Arabia production cut. Indeed, Goldman Sachs has lowered its WTI forecast for December from 89 to 81 (above current level at around 68 though).

Technically speaking, WTI crude oil was clearly rejected by falling 55 D EMA repeatedly, keeping outlook bearish. Immediate focus is now on 67.05 support. Firm break there could prompt downside acceleration through 63.67 low to 61.8% projection of 83.46 to 63.67 from 74.38 at 62.14. Also,l outlook will stay bearish as long as 74.38 resistance holds, in case of another recovery.

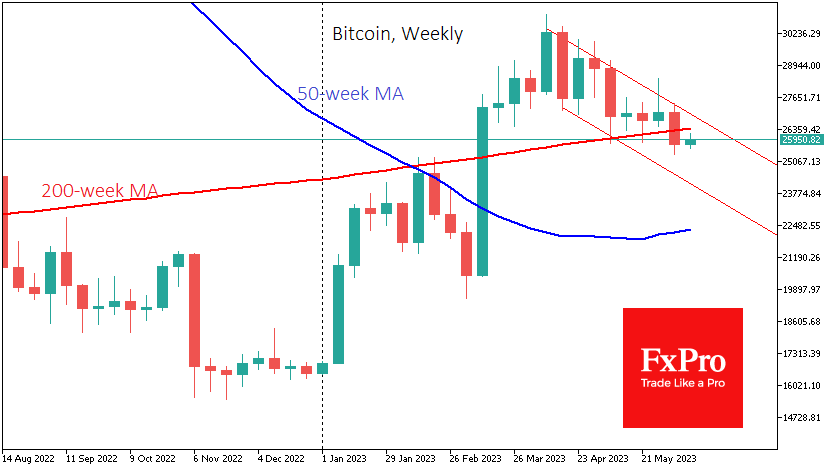

Bitcoin Remains in a Downtrend

Market picture

According to CoinMarketCap, the total capitalisation of the crypto market fell 7.6% over the week to $1.06 trillion, close to lows not seen since almost mid-March. Adding to the market’s nervousness was a sharp sell-off in altcoins in light of the SEC’s ongoing crusade against the crypto business.

The biggest demand in such a market is for USDT, as issuer Tether decided to print an additional 1 billion stablecoins.

Bitcoin once again briefly acted as a safe haven, temporarily enjoying an influx of buyers as one of the most liquid assets in the sector. At the same time, the technical picture remains bearish. Bitcoin closed the week below its 200-week moving average, which last time out resulted in a 20-week downtrend. On the daily timeframe, there is little to cheer about as the decline remains within the bearish corridor. However, the final victory of the bears can only be seen in the case of a fix below $25,000, from which BTCUSD bounced over the weekend.

Ethereum lost 6.5% to $1750. Other leading altcoins from the top 10 changed from 3% (XRP) to -28% (Solana) and 22% (BNB).

News background

The US authority’s crackdown on the Binance and Coinbase exchanges has hit the entire crypto industry. Altcoins, which the SEC classifies as securities, have been particularly hard hit.

Former SEC official John Reed Stark believes that owners of cryptocurrency assets should abandon their investments because the storm in the US crypto industry has only just begun. Crypto exchanges have no reason to comply with laws and regulations prohibiting manipulation, insider trading and other fraudulent activities. A former SEC official says they operate without oversight and offer poor customer protection and risk identification.

Binance is prepared to spend $1 billion to fight the SEC, Bitboy Crypto’s YouTube blogger reported, citing the company’s lawyer.

According to Bloomberg strategist Mike McGlone, the likelihood of a negative stock market recession in the US and a gold hoarding trend coupled with Fed policy tightening could harm crypto investor sentiment. As a result of the pressure, the riskiest assets could be pushed out of investment portfolios.

During a conference call, Ethereum developers approved details of a future update to the network, called Dencun (Cancun-Deneb), expected later this year.

Ethereum co-founder Vitalik Buterin published a roadmap outlining critical areas for the sustainable development of the world’s second-largest cryptocurrency.

GBP/USD Drifting, Markets Eye UK Employment and US CPI Data

- There are no UK of US tier-1 releases on Monday

- On Tuesday, UK releases jobs data and BoE’s Bailey testifies before House of Lords committee

- US releases inflation data on Tuesday, with Fed rate announcement on Wednesday

The British pound is trading quietly on Monday at 1.2566, up 0.11%. The pound took advantage of a broadly weak US dollar last week, gaining 1%.

There are no tier-1 releases out of the US or the UK, so it should be a calm day for the pound. Tuesday could be the polar opposite, with key releases on both sides of the pond. The UK releases May employment data and Bank of England Governor Bailey testifies before a House of Lords Committee. In the US, the markets are anxiously awaiting Tuesday’s inflation report, which comes just one day before the Fed rate announcement.

UK jobs numbers could point in different directions

The UK labour market has proven resilient to the BoE’s aggressive tightening cycle. Perhaps too much of a good thing, as inflation remains sticky, although it did fall to 8.7% in May, down from 10.1% in April. The good news for the BoE is that the labour market appears to be cooling, and that should help reduce inflation.

The markets are expecting mixed numbers in May. The unemployment rate is expected to rise from 3.9% to 4.0% and employment change is projected to fall from 182,000 to 150,000. At the same time, wage growth including bonuses is expected to rise from 5.8% to 6.1% and unemployment claims are expected to drop. If the data turns out to be a mixed bag, it will be interesting to see Governor Bailey’s take when he testifies before the House of Lords committee.

Inflation is expected to continue to ease in May. Headline inflation is expected to fall from 4.9% to 4.1%, and the core rate is projected to ease from 5.5% to 5.3%. Market rate pricing is swinging, with the probability of a pause rising from 70% on Friday to 77% today, according to the CME’s FedWatch. A rate hike remains unlikely, barring a sharp spike in inflation.

If the Fed stays on the sidelines, the markets will be looking for clues as to what happens next. The Fed may decide to skip raising rates on Wednesday but leave the door wide open for further rate hikes, as early as in July. There seems to be some support amongst Fed members for more tightening, and a pause tomorrow may turn out to be a short skip ahead of more rate increases.

GBP/USD Technical

- There is resistance at 1.2645 and 1.2734

- 1.2513 and 1.2436 are providing support