Sample Category Title

EUR/USD: Bulls Crack Key Barrier, Awaiting US Inflation Data for Fresh Signals

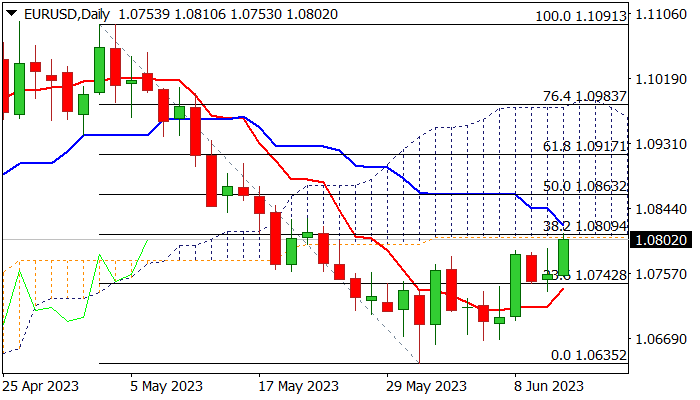

The Euro advanced nearly 0.5% in early Tuesday, driven by weaker dollar ahead of release of US May inflation data.

Fresh risk appetite on expectations that inflation will cool further in May and add to Fed’s plans to stay on hold in June policy meeting which starts today, as markets are currently pricing over 80% chance that the Fed will keep interest rates unchanged.

The Euro is expected to benefit from such scenario and extend recovery from 1.0635 (May 31 low).

Conversely, higher than expected US inflation in May would sour risk sentiment on negative signals to the Fed.

Fresh rally on Tuesday cracked key resistances at 1.0805/10 zone (base of thick daily cloud / Fibo 38.2% of 1.1091/1.0635 / 100DMA) but facing strong headwinds and is likely to stay around these levels and await fresh direction signals from US CPI data.

Firm break of 1.0805/10 zone would generate strong bullish signal for extension towards Fibo barriers at 1.0863 and 1.0917 (50% and 61.8% retracement respectively).

On the other hand, failure to break higher would generate initial signal of recovery stall and shift near-term risk to the downside, with dip below 10DMA (1.0734) to confirm upside rejection.

Res: 1.0810; 1.0863; 1.0917; 1.0980.

Sup: 1.0787; 1.0748; 1.0734; 1.0700.

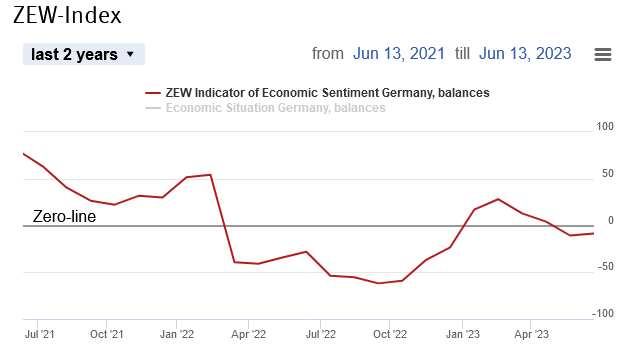

Germany ZEW economic sentiment rose to -8.5, but current situation tumbles very sharply

Germany ZEW Economic Sentiment rose slightly from -10.7 to -8.5 in May, above expectation of -14.7. Current Situation index, however, fell "very sharply" from -34.8 to -56.5, much worse than expectation of -40.

"The ZEW Indicator of Economic Sentiment shows a slight improvement, but it remains in negative territory. This means that experts do not anticipate an improvement in the economic situation during the second half of the year. Particularly, sectors focused on exports are likely to perform poorly due to a weak global economy. However, the current recession is generally not considered particularly alarming," comments ZEW President Achim Wambach.

Eurozone ZEW Economic Sentiment dropped from -9.4 to -10.0, above expectation of -13.1. Current Situation index dropped from -14.4 to -41.9.

Eurozone balance for short-term interest rates stands at 72.3, indicating anticipated rate hikes. On the other hand, balance for short-term interest rates for the US stands at 16.6, indicating no change in interest rates.

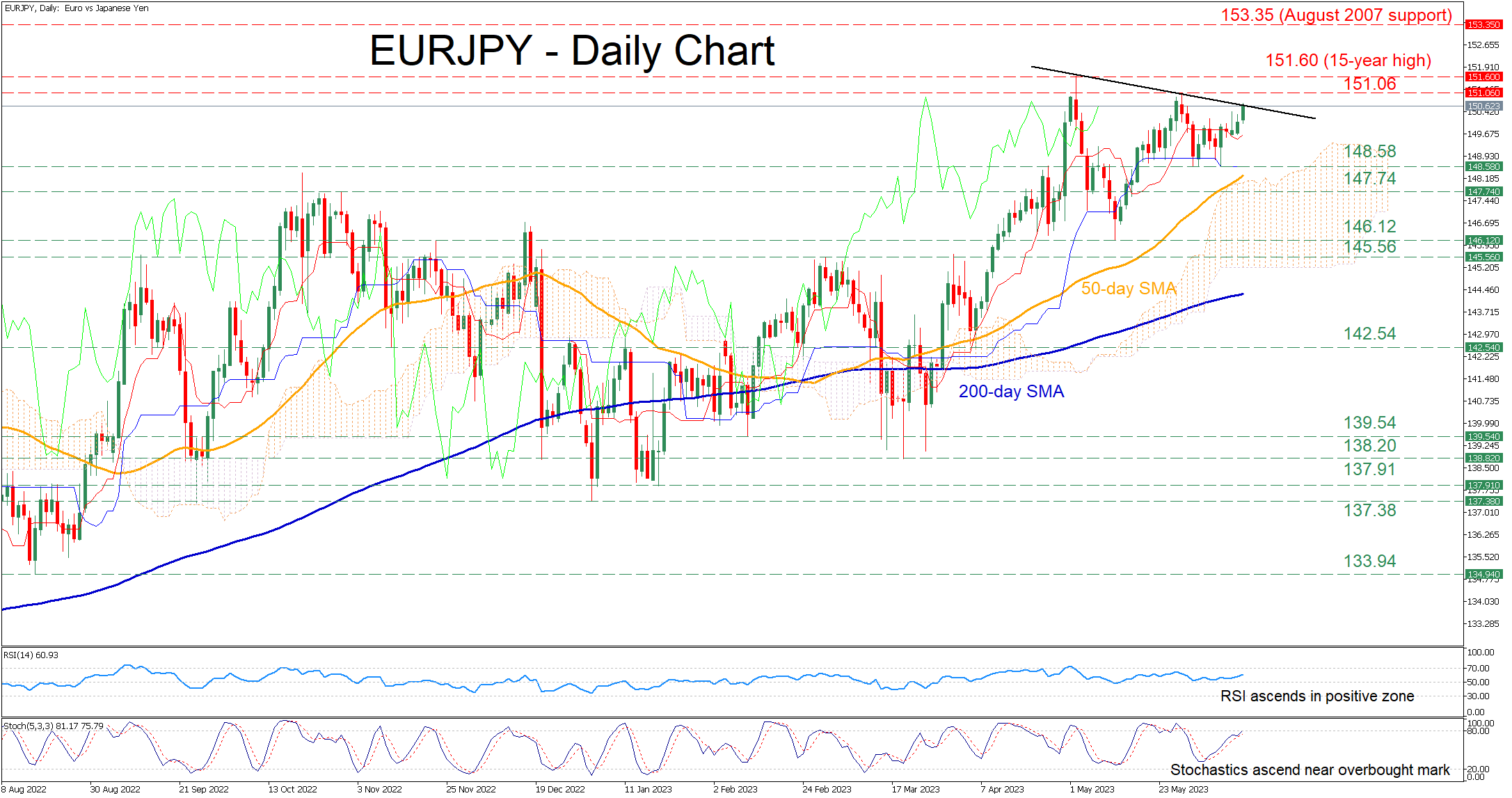

EURJPY Tests Restrictive Trendline Near 15-Year Peaks

EURJPY had been in a strong uptrend, which ceased at a fresh 15-year high of 151.60 in early May before the pair corrected lower. Although it quickly found its feet and attempted a rebound, the price failed to revisit its recent multi-year peak, potentially forming a structure of lower highs but also higher lows.

The momentum indicators currently suggest that bullish forces are strengthening. Specifically, the RSI is ascending above its 50-neutral mark, while the stochastic oscillator is approaching its 80-overbought zone.

Should the price jump above the restrictive trendline taken from the pair’s recent highs, immediate resistance could be found at 151.06. A violation of that territory could set the stage for the 15-year high of 151.60. Piercing through that wall, the pair might ascend to form fresh multi-year highs, where the August 2007 support of 153.35 may cap the upside.

Alternatively, if the price bounces off the trendline and reverses lower, the recent support of 148.58 could act as the first line of defense. Trespassing that area, the October resistance of 146.74 might serve as support in the future. Should that barricade fail, the May low of 146.12 could prove to be a tough one for the bears to overcome.

Overall, EURJPY’s latest advance is currently in a critical stage as a failure to cross above the restrictive trendline could lead to a significant pullback. Nevertheless, a break above that crucial zone could open the door for the pair to test its recent multi-year highs.

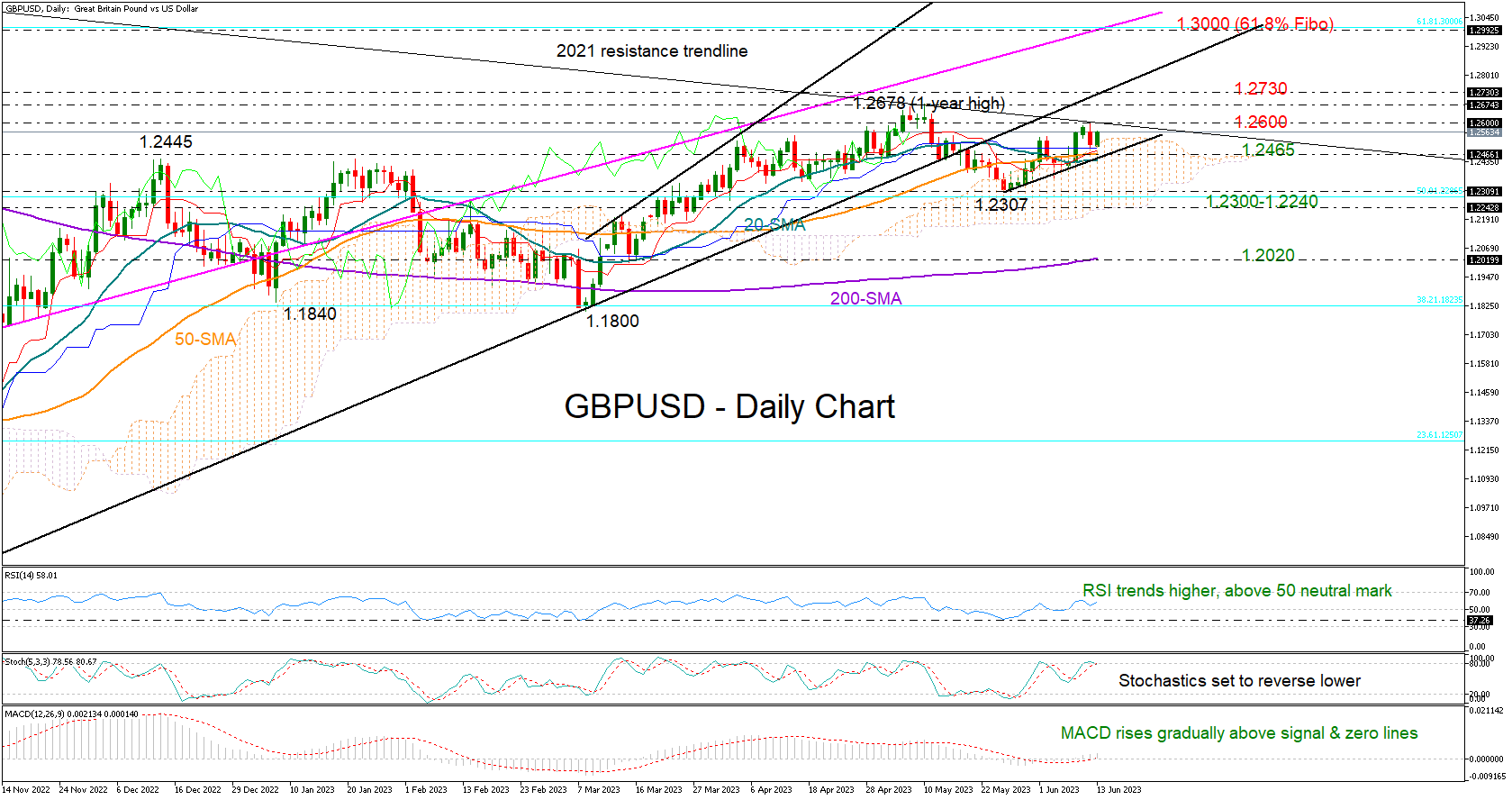

GBPUSD Gets Trendline Rejection, But Bulls Still in Play

GBPUSD turned red on Monday after marking a one-month high of 1.2598 near the long-term resistance trendline, which has been capping bullish actions since the June 2021 high.

The pair switched back to recovery mode early on Tuesday, with the technical indicators reflecting appetite for a bullish breakout. The RSI is trending higher and is above its 50 neutral mark, while the MACD is gradually strengthening within the positive region and above its red signal line. The fact that the price has avoided a drop inside the Ichimoku cloud is also making additional gains possible.

Yet, only a clear extension above the resistance trendline and the 1.2600 round level could activate fresh buying orders. If that proves to be the case, the bulls may drive the pair straight up to May's high of 1.2678 and then towards the broken support trendline from the September 2022 low at 1.2730. A continuation higher could pick up pace towards the 1.3000 zone, where the 61.8% Fibonacci retracement of the 1.4248-1.0324 downtrend is placed.

Alternatively, the pair could seek support somewhere between its 20- and 50-day simple moving averages (SMAs) at 1.2465. Failure to rebound there may press the price into the 1.2300-1.2240 territory, where May’s bearish wave bottomed out. The 50% Fibonacci mark and the cloud’s lower boundary are also positioned in the same region. Therefore, a decisive close lower could spark a notable decline towards the 200-day SMA at 1.2020.

All in all, GBPUSD seems to have some extra bullish power in the tank despite a discouraging start to the week. An advance above 1.2600 could extend the uptrend to new highs.

Nasdaq 100 Technical: Squeezed Up Ahead of CPI and FOMC

Nasdaq 100 Technical: Squeezed Up Ahead of CPI and FOMC

- The mega-cap tech Nasdaq 100 resumed its daily outperformance over the S&P 500, DJIA, and Russell 2000.

- It closed at a 15-month high.

- 14,540 is the key short-term support to watch.

Fig 1: US Nas 100 medium-term trend as of 13 Jun 2023 (Source: TradingView, click to enlarge chart)

Fig 2: US Nas 100 short-term trend as of 13 Jun 2023 (Source: TradingView, click to enlarge chart)

Once again, the bullish tone of the Nasdaq 100 which is heavily concentrated in the mega-cap technology-related stocks such as Microsoft, Apple, Amazon, and NVIDIA resumed its outperformance yesterday, 12 June with a daily gain of +1.76% over the rest of the US benchmark indices; S&P 500 (+0.93%), Dow Jones Industrial Average (+0.56%), and Russell 2000 (+0.40%).

From a technical analysis perspective, momentum remains positive at least in the short-term.

Squeezed up and ended yesterday’s session with a daily bullish “Marubozu”

Price actions of the US Nas 100 (a proxy for the Nasdaq 100 futures) have managed to stage a breakout above the upper boundary of an impending “Ascending Wedge” that now turns into a near-term pull-back support at 14,540. Ended yesterday’s session, (12 June) with a daily bullish “Marubozu” candlestick pattern which suggests that the bullish camp controlled the price of the Index from the opening to the close of the day.

Short-term momentum remains positive

In the shorter-term horizon, as depicted on the 1-hour chart, the price actions of the Index have evolved within a minor ascending channel since the 24 May 2023 low of 13,526. In addition, the 1-hour RSI oscillator has just inched up into its overbought zone (above 70%) yesterday but without any bearish divergence signal yet. These observations suggest that short-term upside momentum remains intact.

14,540 key short-term pivotal support to maintain the bullish tone with next intermediate resistances coming in at 15,100 and 15,270; defined by a confluence of elements (the medium swing high areas of 2 February/29 March 2022, the upper boundary of the minor ascending channel & a Fibonacci retracement/extension cluster).

On the flip side, failure to hold above 14,540 exposes the next support at 14,220 (also the 20-day moving average).

Copper (HG) Low Likely in Place with 5 Waves Rally

Short Term Elliott Wave in Copper (HG) suggests the metal ended wave ((2)) pullback at 3.54. The metal has turned higher in wave ((3)). Rally from wave ((2)) low is unfolding as a 5 waves impulse Elliott Wave structure. Up from wave ((2)), wave (i) ended at 3.618 and pullback in wave (ii) ended at 3.578. The metal extends higher in wave (iii) towards 3.694 and pullback in wave (iv) ended at 3.667. Copper then extends higher again in wave (v) towards 3.711 which completes wave ((i)).

The metal then corrected in wave ((ii)) towards 3.622 with internal subdivision as a zigzag. Down from wave ((i)), wave (a) ended at 3.627, wave (b) ended at 3.694, and wave (c) lower ended at 3.622. This completed wave ((ii)) in higher degree. The metal then extends higher in wave ((iii)). Up from wave ((ii)), wave (i) ended at 3.656 and pullback in wave (ii) ended at 3.624. The metal rallies higher in wave (iii) towards 3.7315 and pullback in wave (iv) ended at 3.676. The metal extends higher again in wave (v) towards 3.789 which completed wave ((iii)). Pullback in wave ((iv)) ended at 3.686. Wave ((v)) higher unfolded as a diagonal and ended at 3.833. This completed wave 1 in higher degree. Wave 2 pullback is in progress now as a zigzag structure. Down from wave 1, wave ((a)) ended at 3.735. While rally in wave ((b)) fails below 3.833, expect the metal to turn lower in wave ((c)) to complete wave 2. As far as pivot at 3.54 low stays intact, expect pullback to find support in 3, 7, or 11 swing for further upside.

Copper (HG) 1 Hour Elliott Wave Chart

HG Elliott Wave Video

https://www.youtube.com/watch?v=pQSsZc6Dfeg

Markets Rise ahead of US CPI, Fed in Focus

Asian markets traded higher on Tuesday, following the positive cues from Wall Street overnight after the S&P 500 rallied to its highest level in more than a year. Market sentiment has been lifted by hopes around the Federal Reserve pausing its tightening cycle with the People’s Bank of China’s decision to lower short-term lending rates stimulating risk appetite. The next few days promise to be incredibly eventful for global financial markets thanks to a long list of high-risk events ranging from key central bank decisions to top-tier data from major economies.

European futures are pointing to a positive open as focus falls on the pending Euro area and Germany ZEW economic sentiment reports. Looking at currencies, the dollar has edged lower ahead of the key U.S inflation data due later today. In the commodity space, oil prices are trading near their lowest level in almost three months thanks to ongoing concerns around the demand outlook while gold remains on standby.

US CPI and Fed meeting in focus

All eyes will be on the latest US inflation report which is expected to have slowed again in May after slightly easing in April. The headline CPI is forecast to rise 0.1% month-on-month after the 0.4% increase in April while the annual headline is seen cooling to 4.1% from 4.9%. However, focus will be on the core CPI reading which is projected to rise 0.4% in May while the annual reading is seen easing to 5.2% from 5.5% in April. Ultimately, signs of lower inflationary pressures may boost expectations around the Fed’s hiking quest coming to an end. Alternatively, a sticky reading could boost bets around US rates remaining higher for longer.

On Wednesday, the main focus will be the Fed decision which is expected to keep interest rates unchanged. Traders are currently pricing in a 28% probability of a 25bps hike, according to Fed funds futures. However, expectations may be influenced by Tuesday’s inflation data, especially if it prints hotter than expected. The updated dot plots and Fed Chair Jerome Powell’s press conference will be closely watched for fresh clues on the Fed’s next move. A hawkish hold seems to be the widely expected outcome of this meeting. Should the central bank surprise markets with a rate hike, this could boost the dollar and rattle markets.

Currency spotlight – EUR/USD

A major breakout could be on the horizon for EURUSD as the currency pair braces for a week jam-packed with key risk events including the European Central Bank meeting on Thursday. Policymakers are expected to raise interest rates by 25 basis points, bringing the deposit rate to 3.50% from 3.25%. However, the key question is whether the central bank hiking cycle is nearing an end, especially after the eurozone entered into a technical recession at the start of the year. Over the past few weeks, EURUSD has been trapped within a range with support at 1.0686 and resistance at 1.0811. Should the pair break above 1.0811, this may open a path toward 1.0845 and 1.0900. A decline back towards 1.0686 may see prices test 1.0635.

Commodity Spotlight – Gold

Gold edged higher ahead of today’s US inflation report and the Federal Reserve policy decision on Wednesday. The precious metal may display sensitivity to the latest US CPI report and is likely to weaken if the Fed moves ahead with a hawkish pause. A surprise rate hike has the potential to trigger an aggressive selloff towards levels not touched since mid-March at $1900. In the meantime, prices remain trapped within a range with support at $1935 and resistance at $1983.

USD Attempts to Rebound

USD/CHF breaks resistance

The Swiss franc weakened across the board as risk appetite picks up. The pair had met stiff selling pressure in the former daily demand zone around 0.9140 and a subsequent fall below 0.9020 pushed out the weak hands. However, the 30-day SMA (0.8980) has proved to be a solid backbone with an oversold RSI attracting renewed buying interests. A surge above 0.9100 might have kept the bulls in the game by prompting sellers to reconsider. 0.9040 is a fresh support and a close above the ceiling of 0.9140 would resume the rebound.

EUR/JPY bounces higher

The euro advances as the ECB will stretch the rate differential at the upcoming policy meeting. On the daily chart, sentiment remains upbeat as the price grinds its way along the 30-day SMA. The single currency has consolidated its gains after clearing the psychological level of 150.00 with 149.60 as a key support to keep the current momentum going. The double top next to 151.00 is a major ceiling ahead and its breach would flush out the last sellers and pave the way for a bullish continuation in the medium-term.

DAX 40 to test recent peak

The Dax 40 pops higher as investors expect a modest 25bp hike from the ECB this week. A surge above the psychological level of 16000 has helped the index break free of the recent consolidation range. After the RSI shot into the overbought area a brief pullback saw follow-through interests over the former resistance, keeping the bullish momentum intact as a deeper retracement would send the price to 15730. On the upside, the recent peak of 16300 is the last obstacle before the uptrend could resume.

China Cuts Rates

Market movers today

US CPI for May is out ahead of the monetary policy decision announced tomorrow. Consensus looks for unchanged m/m core inflation of 0.4% but we see a better change that it will decline to 0.3%, not least because used car prices took a big jump in April which should not repeat in May. Headline inflation should decline to 0.2% m/m so close to be consistent with 2% annual inflation, driven by cheaper energy.

German ZEW measures analysts' assessment of the economy and is not always the best indicator, but it can trigger market reactions from time to time. Consensus is for a slight worsening in June. We also get the more detailed final inflation data for May in Germany and Spain.

The UK labour market report is expected to show slightly higher inflation but also slightly higher wage growth in April, so could be a mixed bag for the rate outlook.

We get Norwegian GDP for April which we expect to show a contraction, but for assessing the Norwegian economy, the Regional Network report on Thursday is more important.

The 60 second overview

Risk appetite improves: Market sentiment got off to a good start this week as investors eye a pause in the Fed's hiking cycle and inflation releases have generally surprised to the downside lately. It provides some optimism that today's US CPI will confirm that inflation pressures are easing.

China cuts rates: The People's Bank of China (PBOC) overnight cut the repo rate by 10bp from 1.9% to 2.0. The CNH weakened in response and Chinese equities and metals prices saw a small lift adding to gains seen over the past two weeks. While monetary easing has been expected, the repo rate cut came slightly earlier than most expected as repo rate changes normally coincide with changes in the rate on the Medium Lending Facility, which will be set on Thursday. It sends a clear signal policy makers are now ready to step in to add stimulus to underpin the economy after recent data has disappointed. We are likely to see other stimulus measures soon but we expect the overall amount of new stimulus to be moderate and mostly aimed at avoiding a new downturn rather than giving a big boost to the economy.

Oil prices fall: Oil prices slipped yesterday towards recent lows around USD72 (Brent spot) even as risk sentiment was on the positive side. It seems fair to conclude by now that the decision by Saudi Arabia to slash another 1mb/d of its oil production in July has failed to stabilise the market. Instead, continued selling of strategic reserves may be what is depressing oil prices currently. There has also been speculation about a US-Iran nuclear deal drawing closer although officials on both sides have denied this. European natural gas prices on the other hand have started to rise again, albeit only modestly. The European natural gas price was normalised in real terms this year, so a small rise should not cause panic. In particular since natural gas storages are more than 70% full already. Still the natural gas market remains fragile as imports are much lower now and demand increasingly dependent on the weather due to the volatility of renewable energy production; hence, it might not take a lot for the market to start tightening again.

Equities: Global equities higher yesterday in a strong growth, quality, and cyclical lead rally. No major news out justifying the magnitude of this risk-on mode but the absence of bad news fostering renewed risk taking and investors giving up on their underweight position. The pain trade has been up this year and risk is that it will continue until we get much weaker job data, or a new tail risk threat arises. Bears should not count on inflation or central banks. Inflation is heading lower and central banks are getting closer to pausing, both supporting equity risk taking. In US yesterday, Dow +0.6%, S&P 500 +0.9%, Nasdaq +1.5% and Russell 2000 +0.4%. Rally continues this morning in Asian with Japanese markets once again leading the region higher. Futures in Europe are in solid green while US futures are higher not to the same extent as in Europe.

FI: There was a modest decline in global bond yields yesterday as well as another spread tightening between the periphery and core-EU. The 10Y spread between Italy and Germany has tightened to 165bp and is now at the tightest level since the start of the year. This is despite the expected reduction in the TLTROs, higher funding rates, QT and the possibility of a hawkish ECB on Thursday.

FX: It has been a fairly slow start to the week in FX markets with the drop in oil taking centre stage. This has put notable pressure on the NOK with EUR/NOK back above 11.60 whilst also CHF and GBP have had a weak start to the weak. EUR/USD remains little changed heading into the next couple of important sessions with US CPI today and both Fed (Wednesday) and ECB meetings (Thursday) later in the week.

Credit: The primary market activity slowed down somewhat during the start of the week as investors await decisions from the Fed and ECB on interest rates. The secondary market saw relatively limited news and credit spreads barely moved on Monday where iTraxx Main widened 1bp to 78bp while iTraxx Xover widened 2bp to 410bp.

Nordic macro

Norwegian GDP for April is the main Nordic release today. We expect it to show a contraction, but the Regional Network report on Thursday will be more important to assess the state of the Norwegian economy.

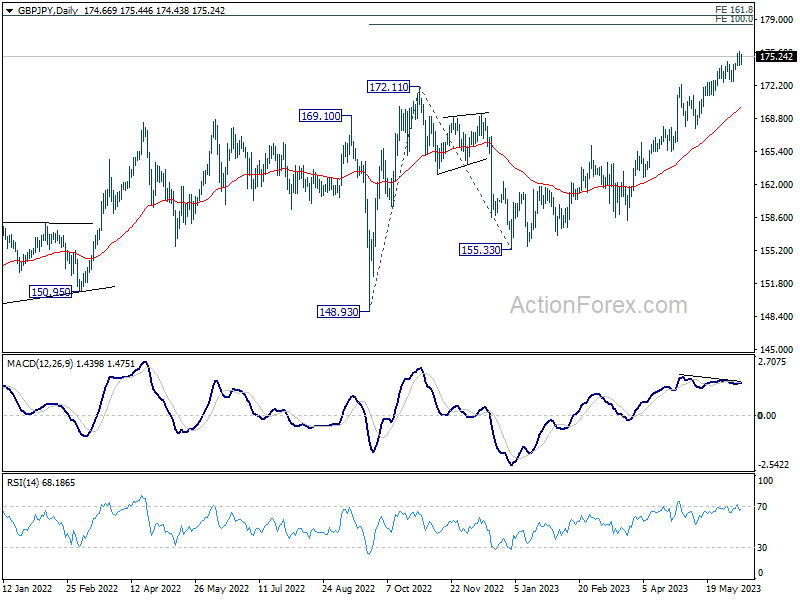

GBP/JPY Daily Outlook

Daily Pivots: (S1) 174.11; (P) 174.94; (R1) 175.52; More...

Further rise is expected in GBP/JPY with 172.64 support intact, despite current retreat. Further rise should be seen to 100% projection of 148.93 to 172.11 from 155.33 at 178.51 next. Strong resistance could be seen from there to bring pull back, at least on first attempt. But break of 172.64 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, up trend from 123.94 (2020 low) is extending. Next target will be 161.8% projection of 122.75 (2016 low) to 156.59 (2018 high) from 123.94 at 178.69. For now, medium term outlook will remain bullish as long as 167.82 support holds, even in case of deep pull back.