Sample Category Title

BoE Bailey: We’ve got a very tight labour market in this country

BoE Governor Andrew Bailey expressed his concern regarding the tight labour market in the UK during a hearing at the House of Lords Economics Affairs Committee today. His comments followed the release of data showing stronger than expected wages growth.

Commenting on the situation, Bailey said, "As I'm afraid this morning's numbers illustrated, we've got a very tight labour market in this country." He also added, "We've had a fall in the supply of labour, which is showing signs of recovering, but very slowly, frankly."

On a similar note, MPC member Catherine Mann voiced her concerns, noting "wage increases of 4.0% would be a challenge to returning CPI to 2.0%." She also flagged services price inflation as a potential hindrance in achieving the 2% CPI target.

Mann stated, "Drop in inflation expectations was important for me to switch my vote to a 25 bps rate hike from 50 bps."

US Core Inflation Could Cause Fed’s Concern

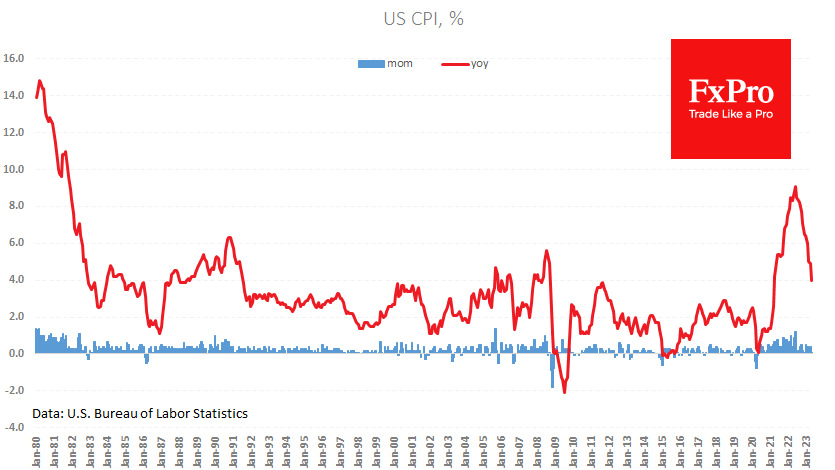

US consumer inflation slowed to 4.0% y/y in May from 4.9% y/y. The monthly gain was 0.1%. In both cases, the data was 0.1 percentage point weaker than expected, marking a slightly faster decline in the inflation problem than expected.

By and large, inflation has returned to normal due to energy and food, which are not only no longer contributing positively to price increases but are pulling them down.

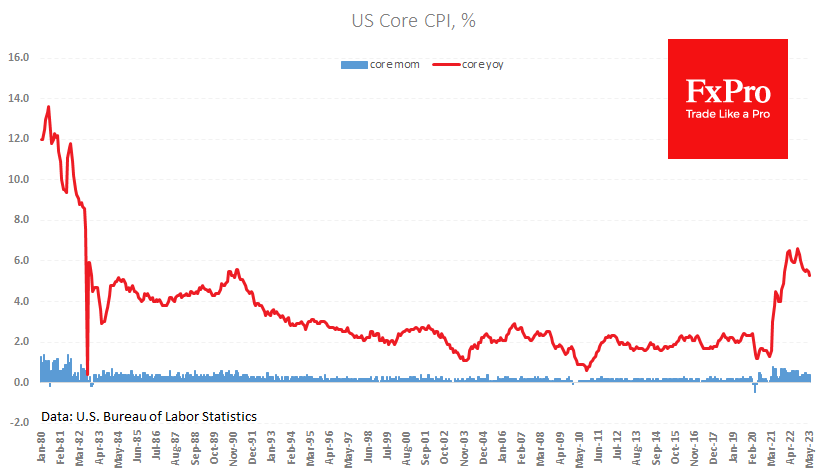

The core CPI (excluding food and energy) added 5.3% y/y against 5.5% y/y. However, there is an elevated pace of month-on-month price growth, which could soon be a stumbling block for the markets.

So far, rate rises have not caused enough of a cooling of the economy and labour market that this would reduce domestic price pressures. The current monthly rate of increase of the core index has been observed in the second half of the 1980s, bringing the overall inflation rate to around 4%, which is half the peak but twice the target.

On the other hand, given the lag effect in monetary policy, the Fed may still announce a “monetary regime change”, i.e., a signal that rates have peaked, and easing will follow a pause, the duration of which will be determined by economic data.

On the balance sheet, we have a contradictory inflation report, and it will be up to the Fed to determine the further direction of the stock indices and the dollar at tomorrow’s meeting.

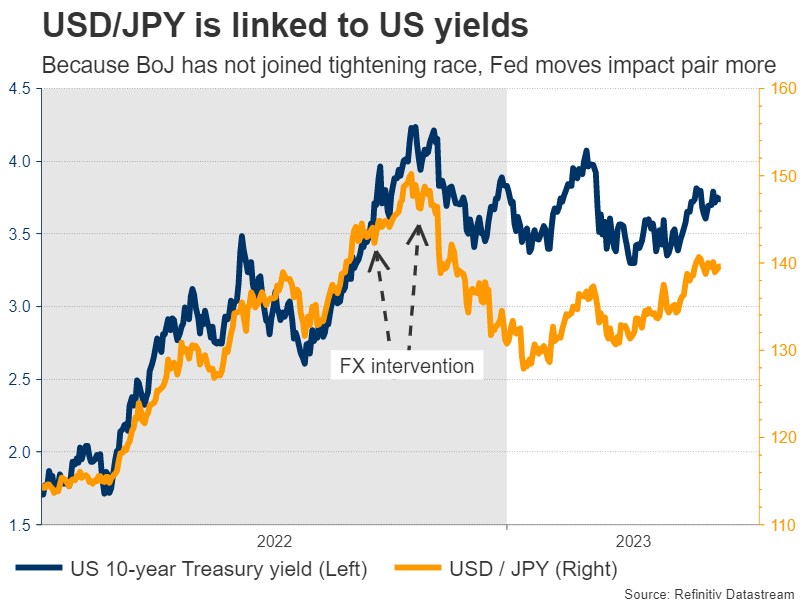

BoJ Unlikely to Tighten Policy, Yen Braces for Another Hit

Brighter outlook

Economic activity in Japan has picked up steam. Revised figures showed the economy grew by 2.7% in annualized terms in the first quarter of this year, and leading indicators such as business surveys suggest this momentum is likely to persist for some time.

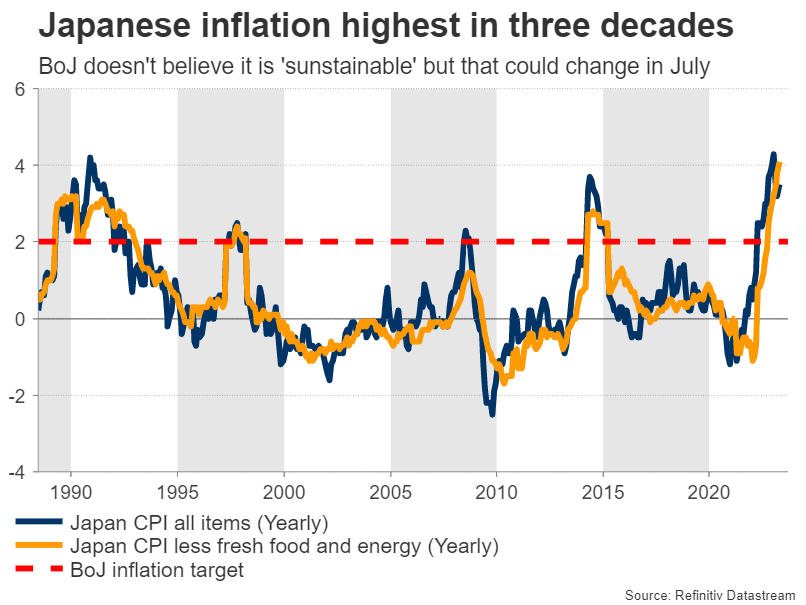

On the inflation front, the situation seems even more promising. Inflation is running near its fastest pace in three decades and the spring wage negotiations resulted in serious pay rises for workers, helping to fuel optimism that inflationary forces are becoming more entrenched.

Yet, BoJ officials are not convinced. Haunted by decades of deflation and mistaken decisions to tighten policy prematurely in previous cycles, the BoJ has committed to 'play it slow' this time. The Bank's forecasts suggest inflation is going to cool off later this year and Governor Ueda has warned the recent victories on the wage front might not be sustained.

In addition, the BoJ is concerned about a global slowdown that inflicts collateral damage on Japan's export-heavy economy. As a result, the central bank has made it crystal clear that it won't tighten policy until it is convinced inflation will remain sustainably above 2%.

On hold, for now

With the likelihood of an immediate policy shift appearing low and this being a meeting without updated economic forecasts, the focus will be mostly on any changes in the language. Specifically, will the BoJ strike a more optimistic tone on inflation, setting the stage for an upgrade of its inflation forecasts at the next meeting in July?

Forecasts are extremely important for the central bank. The way that BoJ officials will ultimately determine whether inflation will remain 'sustainably' above 2% is by whether their inflation forecasts for the next 2-3 years say it will.

We are pretty close to this stage. All that remains is for the 2025 forecasts to be revised higher, which could very well happen in July. That would be the signal that further policy tightening is imminent, elevating the importance of the July meeting.

Yen outlook

In the markets, in case the BoJ does nothing once again, that would argue for a minor negative reaction in the yen as those looking for immediate tightening are left disappointed. Taking a technical look at dollar/yen, the first barrier to the upside might be the latest local high near 141.00.

On the flipside, a surprisingly hawkish tone that refuels market bets for near-term tightening could breathe some life back into the devastated currency. In this case, the focus would shift towards the 138.00 zone in dollar/yen, which roughly encompasses the 200-day moving average too, currently at 137.30.

Aside from BoJ policy, the other two elements that will influence the yen's trajectory moving forward are the actions of other major central banks and global risk sentiment. With the Fed and the ECB likely to hit the 'pause' button this summer just as the BoJ considers tighter policy, the environment seems favorable for the yen.

If such a shift in central bank policies coincides with a selloff in stock markets that fuels safe-haven demand for the Japanese currency, that could mark the beginning of a healthy recovery in the yen. Alas, this is probably a story for July or beyond.

Sunset Market Commentary

Markets:

Trading today was supposed to be a long-drawn countdown to the US CPI release. However, Asian investors got a first surprise impulse as the PBOC unexpectedly cut its 7-day reverse repo rate by 0.1% to 1.90%. Chinese inflation remains low (CPI 0.2% Y/Y, PPI -4.6% Y/Y in May) suggesting a sluggish post-pandemic recovery. The prospect of further stimulus supported risk sentiment in the region. Spill-overs to the likes of Europe were temporary and limited. Copper and oil gained, but especially oil (Brent $73,5/b) is still holding relatively close to the YTD lows. The yuan extended its recent decline. At USD/CNY 7.16, the yuan touched the weakest level since November.

UK labour data also delivered quite a huge surprise. UK job growth in the three months to April jumped 250k (3M/3M). The unemployment rate eased from 3.9% to 3.8%. Last but not least, wage growth (ex-bonus) accelerated sharply from 6.8% 3M/Y/Y to 7.2%. There is no one-on-one link between the labour data and the UK May inflation to be published next Wednesday. Even so, they evidently more than fulfill the condition from the BoE monetary policy statement ‘The MPC will continue to monitor closely indications of persistent inflationary pressures, including the tightness of labour market conditions and the behaviour of wage growth and services price inflation. If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required’. UK bond yields jumped between 20 bps (2-y) and 4 bp(30-y). The UK 2-y yield now surpasses the top during the Truss-Kwarteng fiscal/financial stability crisis in September, reaching the highest level since the GFC in 2008. Money markets now see the peak BoE policy rate well north of 5.5% in Q4. Still, a 50 bps rate hike next week is seen as unlikely (25%). Strangely, sterling hardly profits from a favourable interest rate differential. At EUR/GBP 0.8580, it stays relatively far away from the key 0.8540 area tested yesterday. FX traders apparently err to the side that at current levels enough interest rate support should be discounted for sterling and/or that a too slow BoE reaction function only clouds already weak UK growth prospects further down the road.

The PBOC interest rate cut and/or the UK labour data had limited impact on EMU/US bonds. US and German yields traded almost unchanged (< 2bps) going into the US CPI release. The US CPI was close to expectations with the headline at 0.1% M/M and 4% Y/Y (from 4.9) and core at 0.4% M/M and 5.3% Y/Y (from 5.5%). However, in an understandable asymmetric reaction, US yields declined temporary (2-y -8 bps) as some market participants apparently still feared that a stronger than expected figure could question the Fed ‘skip ‘ scenario. This option is now scrapped. Even so US yields currently again trade little changed (2-y -2.5bps, 30-y +2 bps). German bunds underperform (2-y +4 bps; 30-y 0.5 bp). (European) equities couldn’t keep PBOC-driven gains at the open, but regained some ground after the US CPI (EuroStoxx +0.6%, S&P 500 +0.6%). The combination of softer US yields and a constructive risk context triggers further USD profit taking. DXY nears the 103 area. EUR/USD regained the 1.0775 resistance area, but still struggles to move above the 1.08 barrier in a sustainable way. USD/JPY extends its short-term consolidation pattern between 139/140

News & Views:

Hungarian business newspaper Vilaggazdasag reported that PM Orban’s government may pass a decree to overwrite private contracts between SME’s and utility providers (especially fixed-price electricity contracts struck during the height of the energy crisis) to lower their costs and help slow inflation which still runs at a Y/Y-pace over 20%. The head of the Hungarian Chamber of Industry and Commerce said that the change could be approved within a week. The Hungarian forint loses ground today. In hindsight, the forint may also face selling pressure as comments by Economic Development Minister and previous central bank governor Nagy yesterday get a bigger platform. He suggested that a higher inflation goal may help lower real interest rates, making borrowing more accessible, incentivizing investment and economic expansion. Nagy is part of the wing who believes that inflation won’t return to target due to structural factors like energy, demographics and cost of capital. Acknowledging a higher inflation target implies, all else equal, faster scope to introduce policy rate cuts. The MNB last month started lowering its emergency deposit rate (17% from 18%) towards the normal policy rate (13%). EUR/HUF rises from 369 to 371. From a technical point of view, the extensive test of EUR/HUF 368 support is rejected.

GBP/USD Rebounds on Strong UK Job Numbers, US Inflation Drops

- UK job numbers shine

- US inflation falls to 4%

- Fed widely expected to pause rates

The British pound has pushed higher today, courtesy of a strong employment report. In the North American session, GBP/USD is trading at 1.2592, up 0.64%.

UK job market flexes muscles

The UK labour market remains robust, and today’s employment numbers were higher than expected. The economy created 250,000 jobs, up from 182,000 crushing the consensus of 162,000. The unemployment rate dipped to 3.8%, down from 4.0% and below the consensus of 4.0%. As well, average earnings including bonuses jumped to 6.5%, above 6.1%, which was also the consensus.

The hot numbers will be a major disappointment for the Bank of England, which was expecting the labour market to show signs of cooling off after 12 straight rate hikes. The jump in wages may pose the biggest concern for the BoE, as high wage growth is a key driver of inflation, which remains very high at 8.7%. Governor Bailey testifies today before the House of Lords Economic Affairs Committee, and the committee members are likely to grill Bailey on the latest job data.

US inflation has been heading lower and the trend continued today. Headline CPI for May fell from 4.9% to 4.0%, just beating the consensus of 4.1%. The core rate dipped from 5.5% to 5.3%, as expected. The Fed’s tightening policy has succeeded in pushing inflation lower, but the question is whether the Fed feels that inflation is dropping fast enough.

Today’s inflation data has the markets buying all into a pause at Wednesday’s Fed meeting. The probability of a pause has soared to 99% according to CME’s FedWatch, compared to 75% prior to the inflation release. There are Fed members who favour more rate hikes and the expected non-move on Wednesday could be a “hawkish skip” in which the Fed signals that it is taking a breather but more rate hikes are coming.

GBP/USD Technical

- There is resistance at 1.2657 and 1.2734

- 1.2513 and 1.2436 are providing support

US: Inflation Continues to Ease in May, But Lingering Price Gains Will Keep FOMC Vigilant

The Consumer Price Index (CPI) increased 0.1% month-on-month (m/m) in May, a tick below the consensus forecast (+0.2% m/m). The 12-month change slipped to 4.0% – down from 4.9% in April`.

Energy prices fell 3.6% m/m, as prices at the pump (-5.6% m/m) were down in May, as were energy services (-1.4% m/m). Food prices ticked up by 0.2% m/m and remain 6.7% above year-ago levels.

Core inflation (excludes food & energy) rose 0.4% m/m – meeting the consensus forecast and matching both March and April's monthly gain. The annualized 1-month (+5.4%), 3-month (+5.0%), 6-month (+5.1%) and 12-month (+5.3%) change on core inflation all remained above 5% in May.

Price growth across services rose 0.4% m/m. Shelter was again a meaningful contributor, with rent of primary residence and owners' equivalent rent both notching a gain of 0.5%.

- Non-housing services rose 0.3% m/m – accelerating from April's flat reading – with gains concentrated in lodging away from home (+1.8% m/m), transportation (+0.8% m/m) and other personal services (+0.8% m/m). Airfares (-3%) were the one standout, where prices fell for a second consecutive month, and are now down 13.4% on a year-over-year basis.

Core goods prices increased by 0.6% m/m – matching April's gain. Much like April, gains were narrowly concentrated in used vehicle prices, which were up 4.4% m/m.

Key Implications

May's inflation reading largely met expectations, with both the headline and core measure easing to 4.0% and 5.3%, respectively. That said, non-housing service inflation heated up in May, with price gains led across those spending categories most closely tied to discretionary spending. Goods prices were also higher, though this was largely driven by another sharp gain in used vehicle prices. After stripping out its effects, price growth across all other goods were flat. This is an encouraging sign, as wholesale used vehicle prices have turned lower in recent months, suggesting goods prices will (again) soon become a source of deflation.

We will hear from the Fed tomorrow, where markets are widely expecting policymakers to move to the sidelines. However, a pause doesn't guarantee that the Fed's work is done. Since Chair Powell's remarks on May 19th where he referred to having 'time on their side to watch the data', the pace of hiring has accelerated, job openings have ticked higher, while inflation has remained intolerably high. Unless we see a clear softening in the economic data between now and the Fed's next meeting in July, another rate hike remains in play.

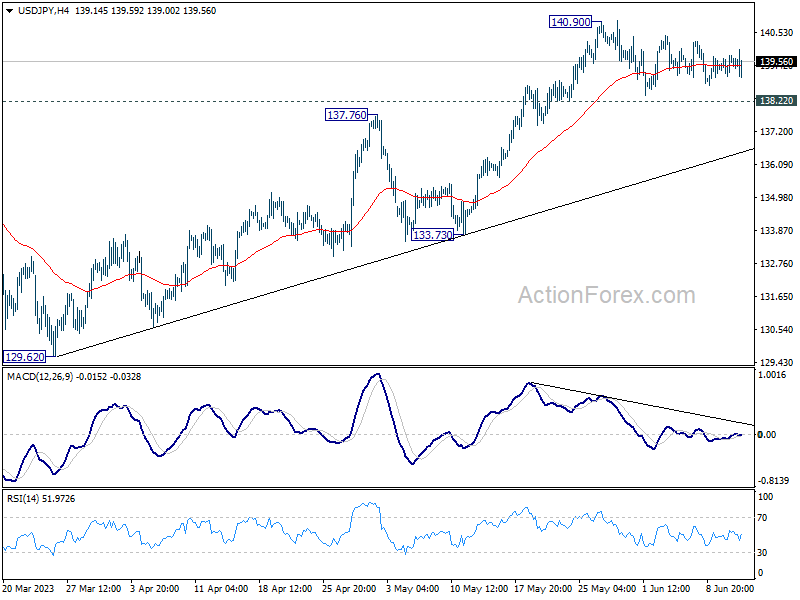

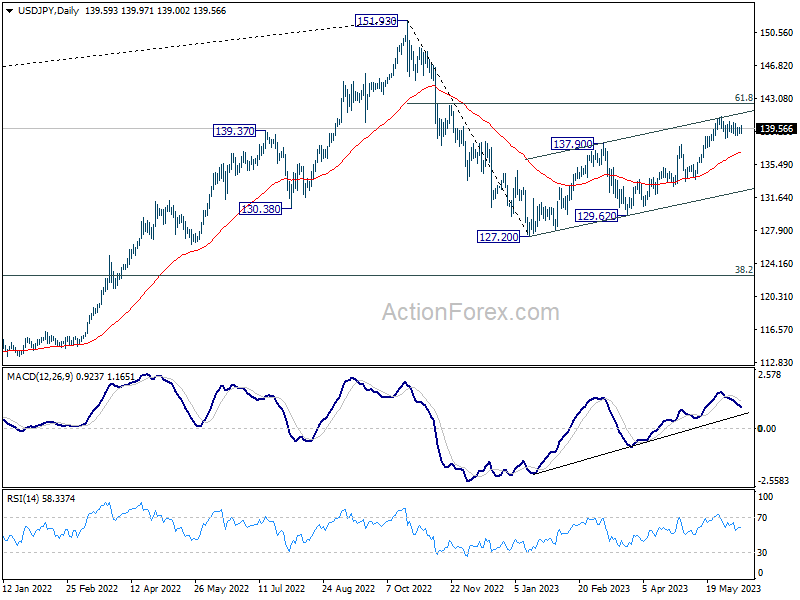

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 139.20; (P) 139.48; (R1) 139.90; More...

Intraday bias in USD/JPY remains neutral as range trading continues. Further rally is expected as long as 138.22 minor support holds. On the upside, break of 140.90 will resume larger rise from 127.20 to 142.48 fibonacci level. However, considering bearish divergence condition in 4 hour MACD, break of 138.22 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 136.77).

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 136.34. Sustained break there will pave the way back to retest 151.93. On the downside, however, break of 133.73 support will argue that the pattern could have started the third leg through 127.20 low.

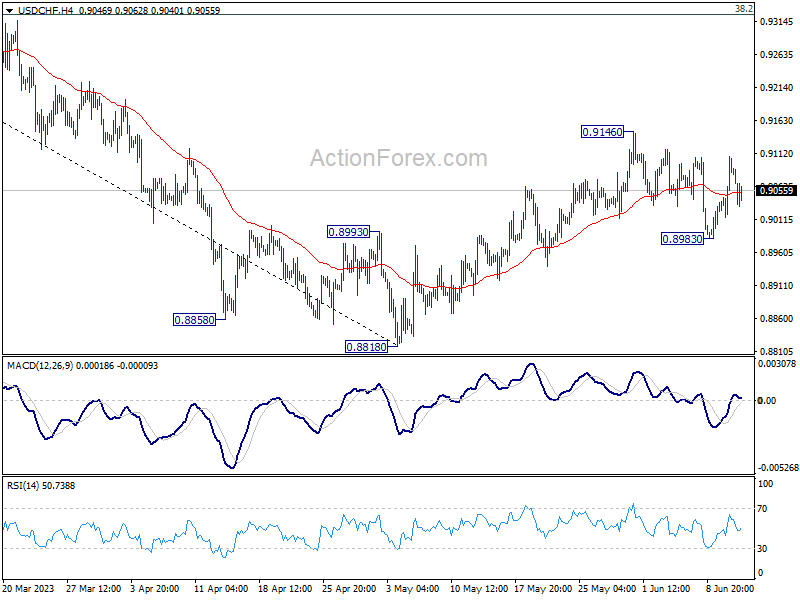

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9034; (P) 0.9072; (R1) 0.9127; More...

Range trading continues in USD/CHF and intraday bias stays neutral. On the downside, break of 0.8983 will revive the case that corrective rebound from 0.8818 has completed at 0.9146. Intraday bias will be back to the downside for deeper fall back to retest 0.8818 low. On the upside, however, break of 0.9146 will resume the rebound from 0.8818 instead.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming. Further break of 0.9439 resistance will confirm bullish trend reversal.

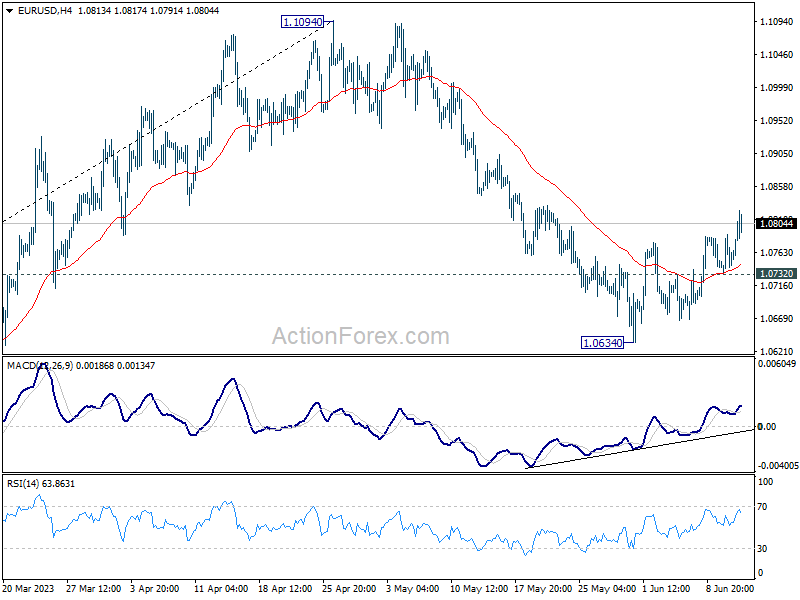

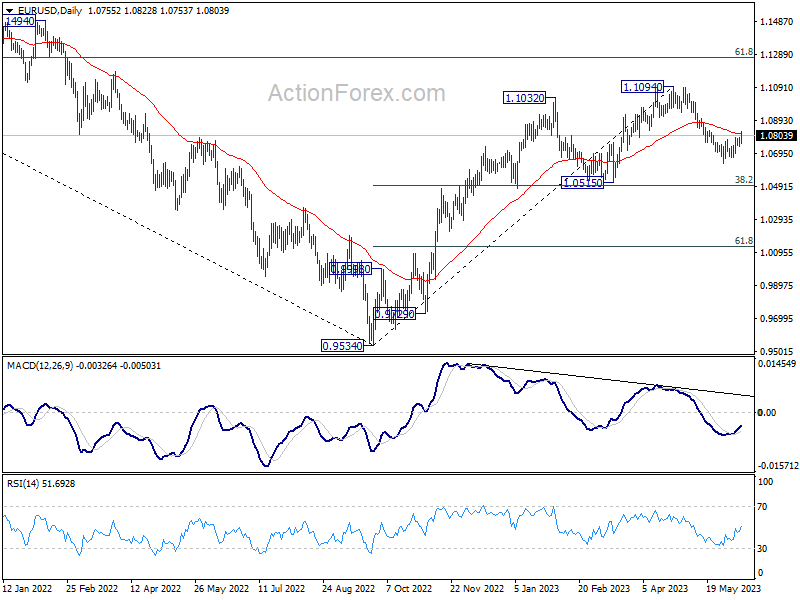

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0731; (P) 1.0760; (R1) 1.0788; More...

Intraday bias in EUR/USD remains on the upside. Rebound from 1.0634 short term bottom is in progress. Sustained trading above 55 EMA (now at 1.0810) will pave the way back to retest 1.1094 high. Nevertheless, break of 1.0732 minor support should resume the fall from 1.1094 through 1.0634 support.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

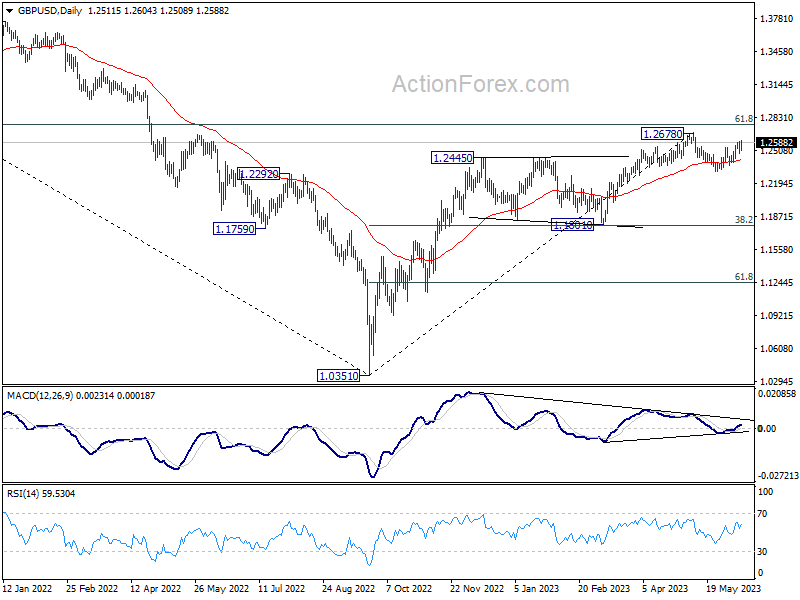

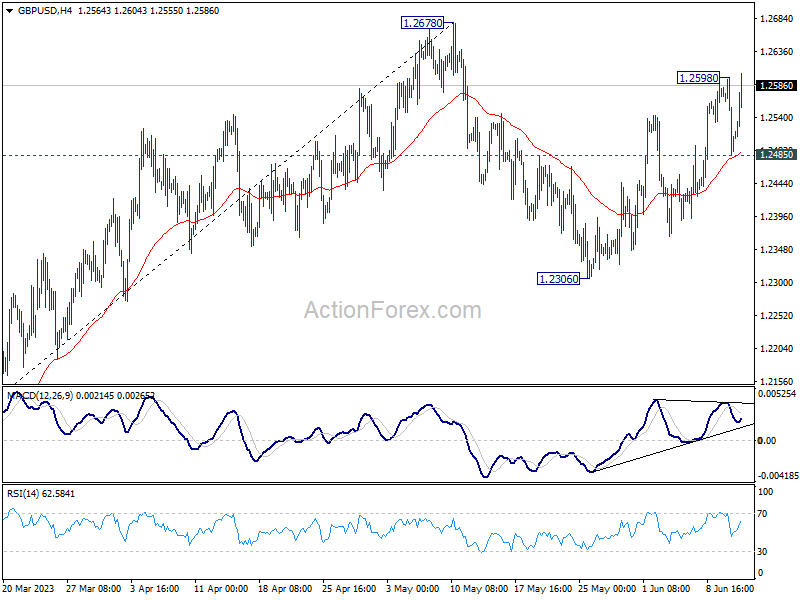

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2466; (P) 1.2533; (R1) 1.2578; More...

Intraday bias in GBP/USD is back on the upside as rebound from 1.2306 resumed after brief retreat. Further rally should be seen to retest 1.2678 high. Based on current momentum, upside could be limited there, to bring another fall to extend the corrective pattern from 1.2678. On the downside, break of 1.2485 support will turn bias back to the downside for 1.2306 support instead.

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.