Sample Category Title

AUD/USD Daily Report

Daily Pivots: (S1) 0.6734; (P) 0.6771; (R1) 0.6803; More...

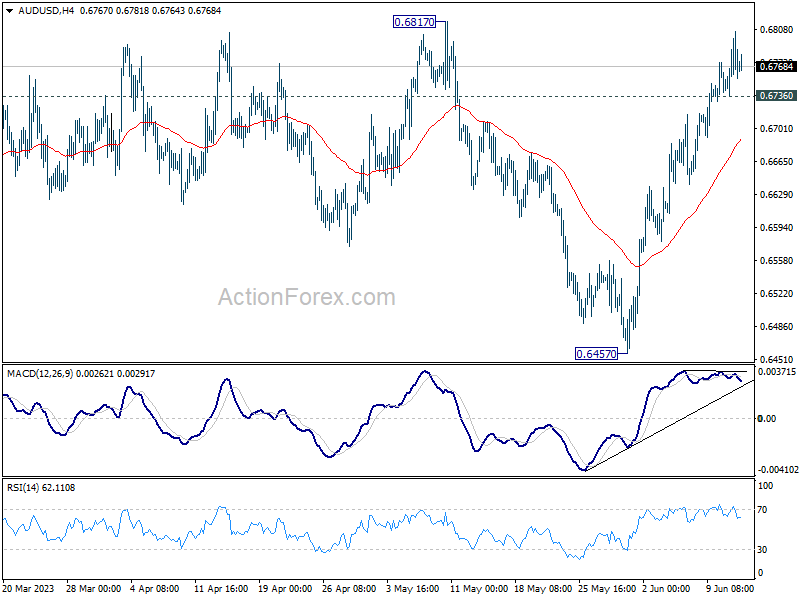

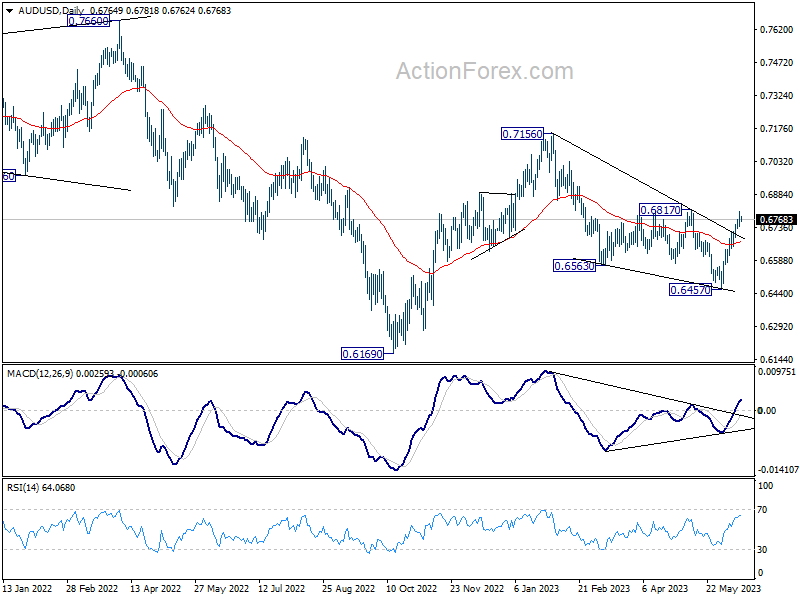

Intraday bias in AUD/USD remains on the upside as rise from 0.6457 is still in progress. Next target is 0.6817 structural resistance. Decisive break there should confirm near term bullish reversal, and pave the way to retest 0.7156 resistance next On the downside though, below 0.6736 minor support will turn intraday bias neutral first.

In the bigger picture, as long as 0.6817 resistance holds, the decline from 0.7156, as well as the down trend from 0.8006 (2021) are still in favor to continue through 0.6169 (2022 low) at a later stage. However, firm break of 0.6817 will indicate that fall from 0.7156 has completed in a three-wave corrective structure. Such development will argue that rise from 0.6169 is ready to resume through 0.7156, and add credence to the case that whole down trend from 0.8006 has completed already.

Risk-On Mood Prevails as Fed Decision Looms; EUR/GBP in Spotlight First

The financial markets remain firmly entrenched in a risk-on stance as signs increasingly point towards Fed "skipping" tightening at today's rate decision. As a result, Yen, Swiss Franc, and Dollar are this week's worst performers, exhibiting no clear indications of a resilient bounce. On the other end of the spectrum, Australian and New Zealand Dollar are emerging as the frontrunners, followed by Euro and Sterling.

This current wave of positive sentiment is expected to sustain in the near term. However, market participants should brace for a potential brief pullback once Fed's decision to hold rates steady materializes. Furthermore, the release of new economic projections may incite some market volatility.

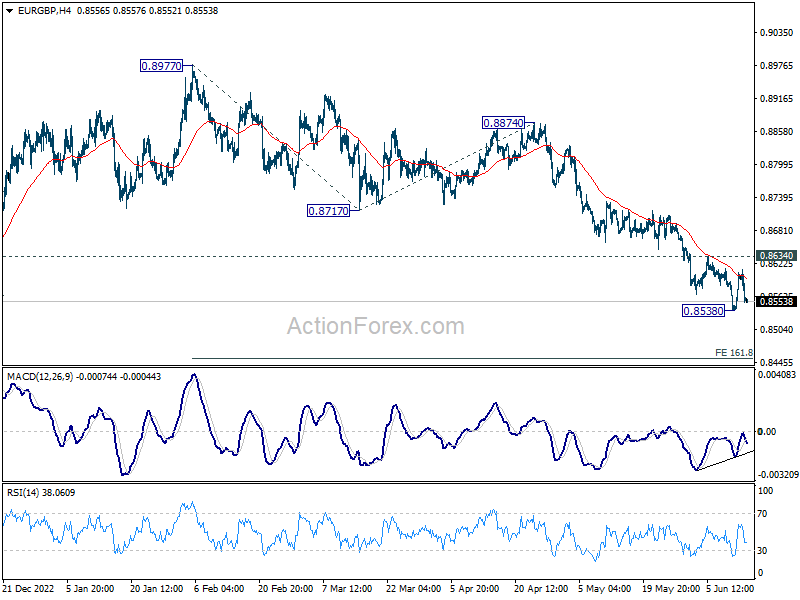

Technically, EUR/GBP is worth some attention in European session today. This week's recovery was rather brief, and capped well below 0.8634 near term resistance. Outlook stays bearish in the cross. Break of 0.8538 will resume the whole decline from 0.8997 to 161.8% projection of 0.8977 to 0.8717 from 0.8874 at 0.8453. Today's UK data might be a trigger for the move.

In Asia, at the time of writing, Nikkei is up 1.18%. Hong Kong HSI is down -0.05%. China Shanghai SSE is up 0.24%. Singapore Strait Times is up 0.70%. Japan 10-year JGB yield is up 0.0118 at 0.433. Overnight, DOW rose 0.43%. S&P 500 rose 0.69%. NASDAQ rose 0.83%. 10-year yield rose 0.074 to 3.839.

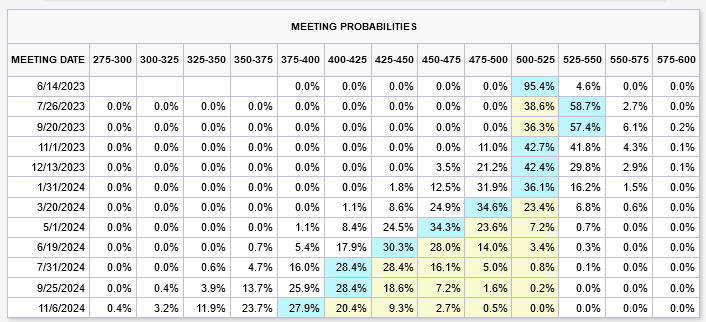

FOMC preview: 95% chance of a skip today, 60% chance of another hike in Jul

Yesterday's cooling US consumer inflation data in May provided further solid ground for Fed to bypass tightening at today's rate announcement. Fed funds futures now suggest a 95.4% probability of Fed maintaining status quo, holding rates steady at 5.00-5.25%. However, market sentiment leans towards the likelihood of another 25 bps to 5.25-5.50% in July, with over 60% chance.

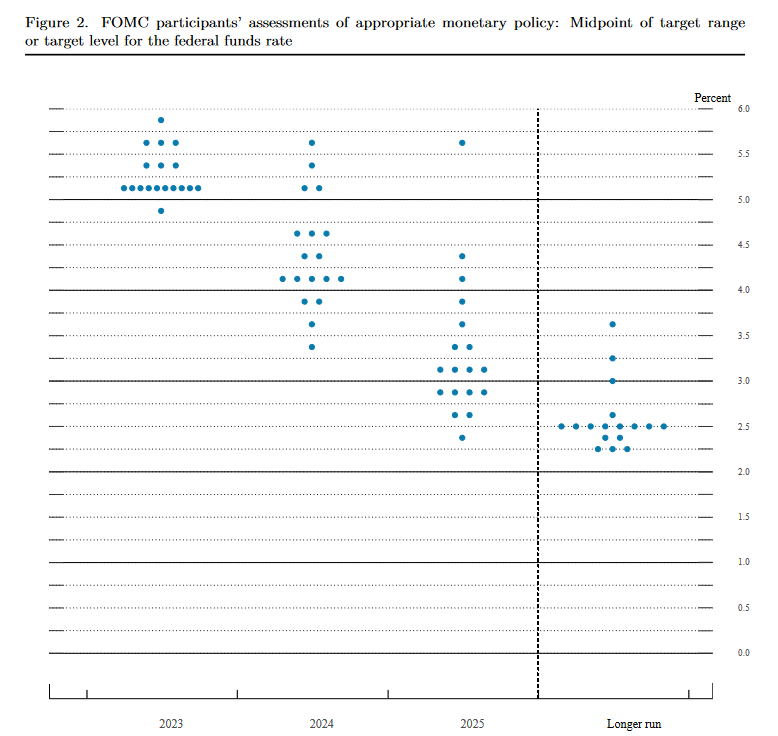

Yet, these market expectations are not set in stone and could see adjustments based on Fed's new economic projections. Rewinding to March, the median interest rate stood at 5.1% for 2023. A perusal of the dot plot reveals that only one policymaker anticipated no additional rate hikes from the current level. In contrast, 10 policymakers forecast one more hike, while seven projected two or more. Changes in this balance could provide insights on whether the interest rate will peak at 5.25-5.50%, as currently predicted by the market.

Furthermore, median interest rate is expected to decline to 4.3% in 2024 and then to 3.1% in 2025. Any deviations from these projections could hint at the duration for which the interest rate will remain at its peak and potentially even suggest a timeline for the initial rate cut.

Some readings on Fed:

- Will Fed Pause After 10 Straight Hikes?

- Fed Preview: On Hold

- June Flashlight for the FOMC Blackout Period

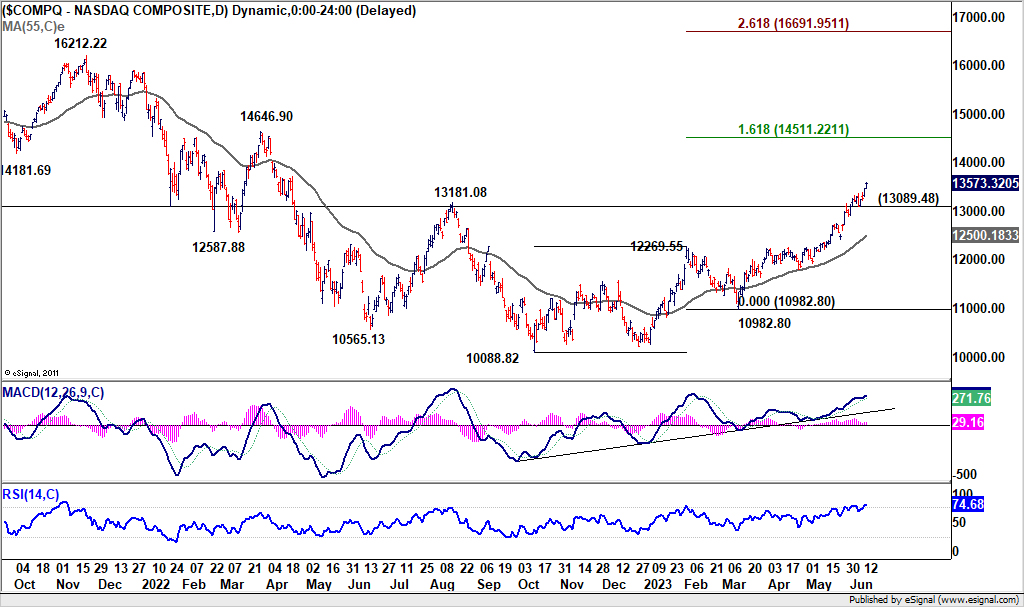

NASDAQ closed at 13-mth high, DOW broke resistance

US stocks surged broadly overnight as inflation data solidified a pause at today's FOMC rate decision. NASDAQ extended its near term up trend to close at the highest level in 13 months. For now, near term outlook will stay bullish as long as 13089.48 support holds. Next target is 161.8% projection of 1088.82 to 12269.55 from 10982.80 at 14511.22.

DOW also made notable progress by breaking 34257.83 resistance, even though it could close above the level yet. Near term outlook will stay bullish as long as 55 D EMA (now at 33419.74) holds. Next target is 61.8% projection of 28660.94 to 34712.28 from 314289.82 at 35169.54. Sustained break there could prompt upside acceleration to retest 36952.65 record high.

Looking ahead

UK GDP, production and trade balance are the main feature in European session. Eurozone will also publish industrial production. Later in the day, US PPI will be released before FOMC rate decision and press conference.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6734; (P) 0.6771; (R1) 0.6803; More...

Intraday bias in AUD/USD remains on the upside as rise from 0.6457 is still in progress. Next target is 0.6817 structural resistance. Decisive break there should confirm near term bullish reversal, and pave the way to retest 0.7156 resistance next On the downside though, below 0.6736 minor support will turn intraday bias neutral first.

In the bigger picture, as long as 0.6817 resistance holds, the decline from 0.7156, as well as the down trend from 0.8006 (2021) are still in favor to continue through 0.6169 (2022 low) at a later stage. However, firm break of 0.6817 will indicate that fall from 0.7156 has completed in a three-wave corrective structure. Such development will argue that rise from 0.6169 is ready to resume through 0.7156, and add credence to the case that whole down trend from 0.8006 has completed already.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account Q1 | -5.22B | -6.95B | -9.46B | |

| 06:00 | GBP | GDP M/M Apr | 0.20% | -0.30% | ||

| 06:00 | GBP | Industrial Production M/M Apr | -0.10% | 0.70% | ||

| 06:00 | GBP | Industrial Production Y/Y Apr | -2.60% | -2.00% | ||

| 06:00 | GBP | Manufacturing Production M/M Apr | -0.10% | 0.70% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Apr | -1.80% | -1.30% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Apr | -16.5B | -16.4B | ||

| 09:00 | EUR | Eurozone Industrial Production M/M Apr | 1.20% | -4.10% | ||

| 12:30 | USD | PPI M/M May | 0.20% | 0.20% | ||

| 12:30 | USD | PPI Y/Y May | 1.10% | 2.30% | ||

| 12:30 | USD | PPI Core M/M May | 0.20% | 0.20% | ||

| 12:30 | USD | PPI Core Y/Y May | 0.50% | 3.20% | ||

| 14:30 | USD | Crude Oil Inventories | -1.3M | -0.5M | ||

| 18:00 | USD | Fed Interest Rate Decision | 5.25% | 5.25% | ||

| 18:30 | USD | FOMC Press Conference |

NASDAQ closed at 13-mth high, DOW broke resistance

US stocks surged broadly overnight as inflation data solidified a pause at today's FOMC rate decision. NASDAQ extended its near term up trend to close at the highest level in 13 months. For now, near term outlook will stay bullish as long as 13089.48 support holds. Next target is 161.8% projection of 1088.82 to 12269.55 from 10982.80 at 14511.22.

DOW also made notable progress by breaking 34257.83 resistance, even though it could close above the level yet. Near term outlook will stay bullish as long as 55 D EMA (now at 33419.74) holds. Next target is 61.8% projection of 28660.94 to 34712.28 from 314289.82 at 35169.54. Sustained break there could prompt upside acceleration to retest 36952.65 record high.

FOMC preview: 95% chance of a skip today, 60% chance of another hike in Jul

Yesterday's cooling US consumer inflation data in May provided further solid ground for Fed to bypass tightening at today's rate announcement. Fed funds futures now suggest a 95.4% probability of Fed maintaining status quo, holding rates steady at 5.00-5.25%. However, market sentiment leans towards the likelihood of another 25 bps to 5.25-5.50% in July, with over 60% chance.

Yet, these market expectations are not set in stone and could see adjustments based on Fed's new economic projections. Rewinding to March, the median interest rate stood at 5.1% for 2023. A perusal of the dot plot reveals that only one policymaker anticipated no additional rate hikes from the current level. In contrast, 10 policymakers forecast one more hike, while seven projected two or more. Changes in this balance could provide insights on whether the interest rate will peak at 5.25-5.50%, as currently predicted by the market.

Furthermore, median interest rate is expected to decline to 4.3% in 2024 and then to 3.1% in 2025. Any deviations from these projections could hint at the duration for which the interest rate will remain at its peak and potentially even suggest a timeline for the initial rate cut.

Some readings on Fed:

ECB Policy Meeting: More Rate Hikes to Come

An inflation peak is not enough for central banks to stop raising interest rates. The Reserve Bank of Australia and the Bank of Canada resumed their rate hike strategy unexpectedly last week for the sake of their inflation target, having previously pledged a pause. The European Central bank (ECB) could follow suit on Thursday at 12:15 GMT, but the announcement might not surprise investors, with guidance on future rate increases likely attracting the most attention.

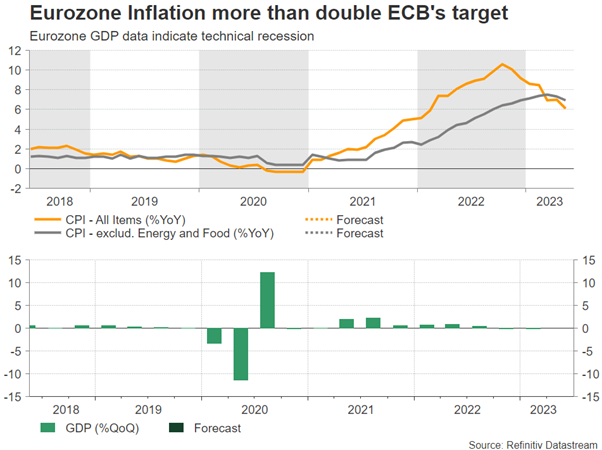

Pause not in sight as inflation remains elevated

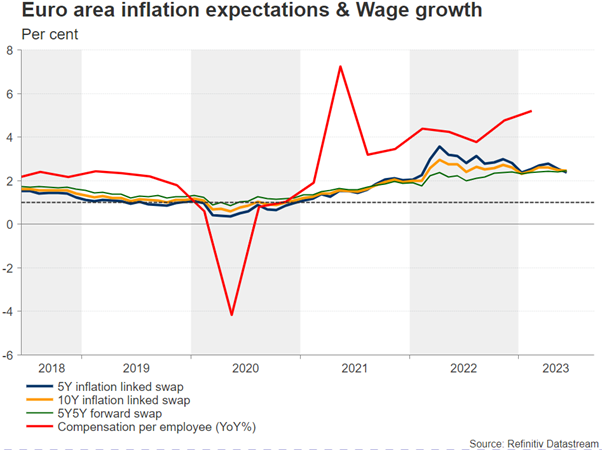

It's hard to argue that the fight against inflation is over. Even though the CPI inflation figures are past their 2022 peaks in developed economies, they are still more than double the central banks’ targets. Many focus on the falling headline CPI, but the core measure, which is a better proxy of the inflation trend, has barely eased from its April peak of 5.7% y/y in the eurozone, flagging a permanent inflation risk that the ECB might struggle to overcome. Notably, the core measure, which excludes food, energy, and tobacco, has barely eased, arriving at 6.9% y/y recently.

Hence, ECB policymakers are reasonably sustaining a hawkish communication, with President Lagarde recently stressing the need to raise rates to levels sufficiently restrictive and keep them at those levels as long as necessary. She also highlighted the impact of some businesses profiting from high inflation by raising prices more than they have to and urged competition authorities to investigate.

Guidance important for euro

Another quarter percentage rate hike to 3.5% is currently looking like a done deal, and there is a negligible group of investors who are even thinking that the rate discussion may expand to a bolder 50bps rate hike. That suggests there is a lot of hawkishness priced in already, which could consequently leave little room for improvement for the euro.

Commentary on future policy actions, however, could still help euro/dollar extend its positive momentum and run towards the 1.0900 territory. Policymakers have clearly restated that the costs of doing too little is still greater than the costs of doing too much. Therefore, the negative GDP growth figures, which put the bloc in a technical recession, may raise some caution within the board but are not expected to prevent additional rate hikes in the coming months.

Investors anticipate an equal 25bps rate hike in July with a probability of 62% before a period of steady rates kicks in. Apparently, a repetition of the aggressive rate increases that took place over the past year could find little backing given the worsening economic picture and the falling household inflation expectations. Yet, policymakers may judge that acting now rather than later could be a safer option, especially as long as the labor market remains tight and wage growth trends higher. New economic projections, and specifically updated inflation forecasts, could provide more evidence on the central bank’s thinking.

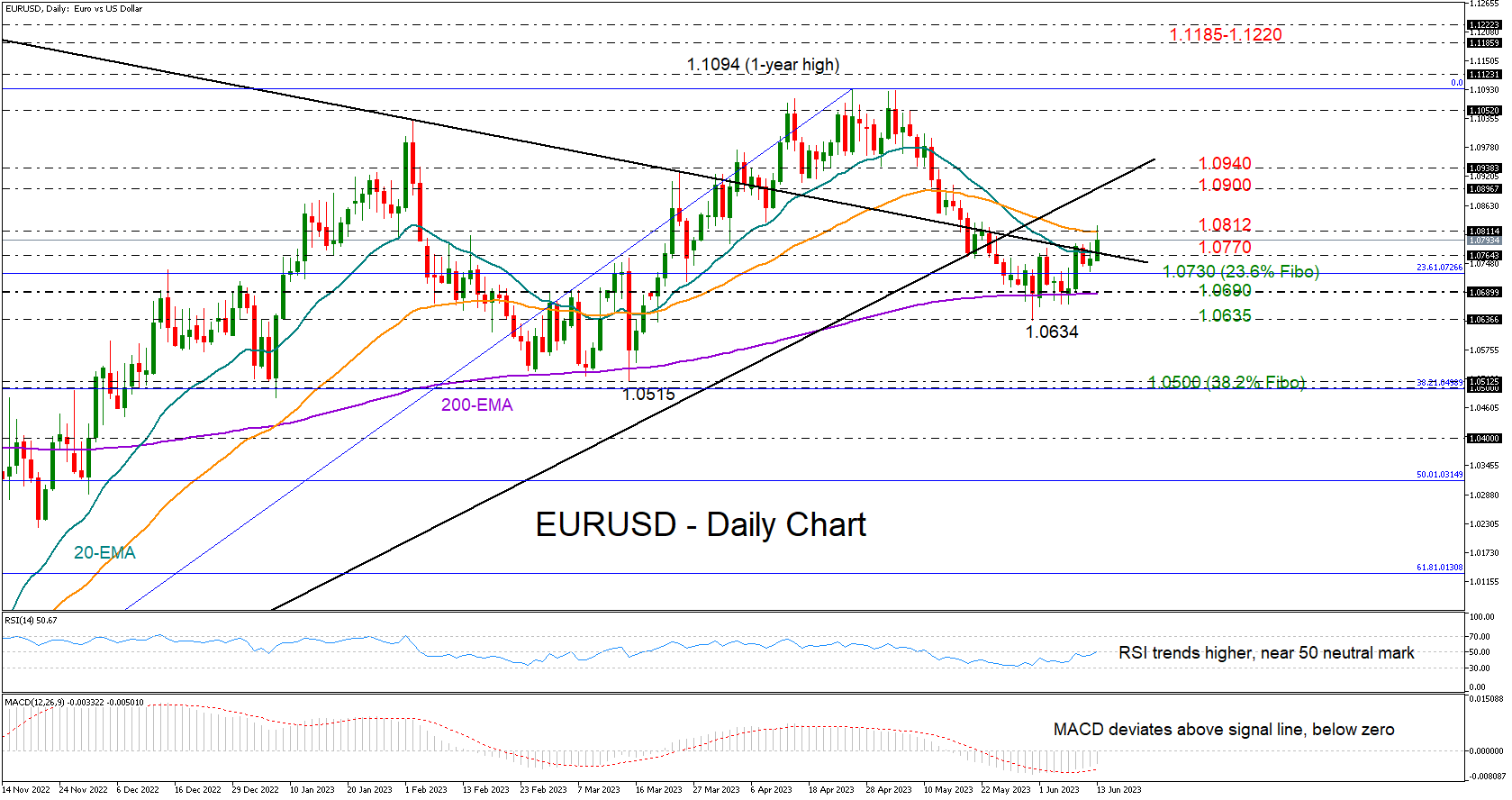

Should the central bank lower its inflation estimates, signaling that a rate peak is closer than analysts believe, euro/dollar could erase its latest pickup to test its flattening 200-day exponential moving average (EMA) at 1.0690 ahead of May’s low of 1.0635. A decisive close lower could intensify selling pressures towards the 1.0500 floor.

Quantitative tightening

In other interesting topics, balance sheet talks could also come under the limelight. The ECB has been struggling to reduce the size of its huge balance sheet after the pandemic boost, leaving excess liquidity in money markets and making its monetary tightening less effective. It promised to accelerate quantitative tightening by reducing reinvestment from maturing securities at a faster pace of 25 billion euros in July compared to 15 billion euros before. Therefore, any extra details on the matter could make headlines, although that might be a story for the next policy meeting.

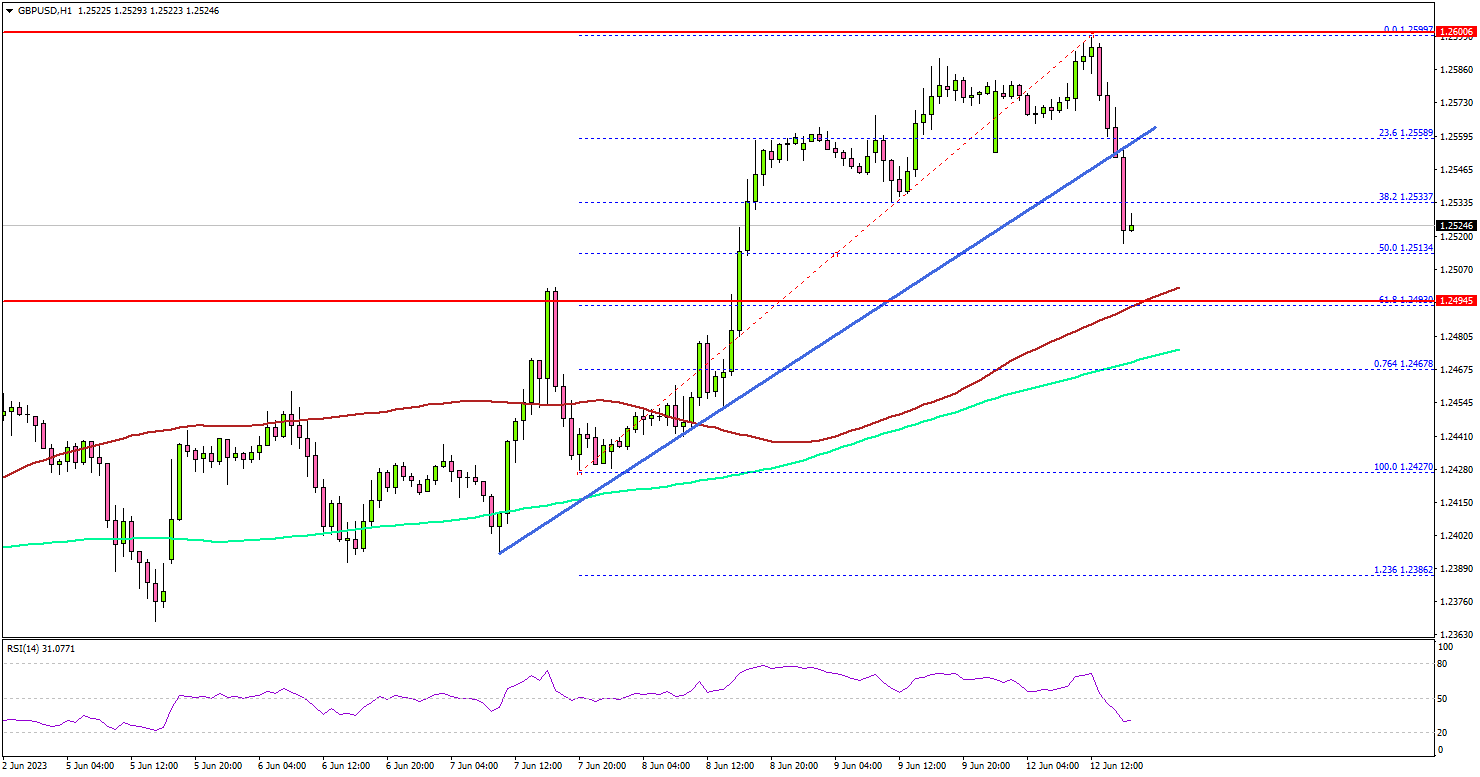

GBP/USD Starts Correction, US CPI Report Next

Key Highlights

- GBP/USD started a downside correction from the 1.2600 zone.

- It traded below a key bullish trend line with support near 1.2550 on the 4-hour chart.

- EUR/USD is still holding the 1.0710 support zone.

- The US Consumer Price Index could decline from 4.9% to 4.1% in May 2023 (YoY).

GBP/USD Technical Analysis

The British Pound gained pace for a move above 1.2500 against the US Dollar. GBP/USD even broke the 1.2550 resistance before the bears appeared.

Looking at the 4-hour chart, the pair tested the 1.2600 zone. It recently started a downside correction below the 1.2550 level. The pair traded below a key bullish trend line with support near 1.2550.

It even traded below the 38.2% Fib retracement level of the upward move from the 1.2427 swing low to the 1.2599 high. Immediate support is near the 1.2500 level and the 100 simple moving average (red, 4 hours).

The 61.8% Fib retracement level of the upward move from the 1.2427 swing low to the 1.2599 high is also near 1.2500. The next major support is near the 1.2460 level and the 200 simple moving average (green, 4 hours).

If there is a downside break below the 1.2460 support, the pair could decline toward the 1.2400 support. Any more losses might send EUR/USD toward 1.2320.

If there is a fresh increase, the pair could face resistance near 1.2550. The first major resistance is near the 1.2600 level. If there is a move above the 1.2600 resistance, the pair could drift toward 1.2740.

Looking at EUR/USD, the pair is attempting a recovery wave but the pair could face resistance near the 1.0850 zone.

Economic Releases

- UK Claimant Count Change for May 2023 – Forecast -9.6K, versus 46.7K previous.

- UK ILO Unemployment Rate for April 2023 (3M) – Forecast 4.0%, versus 3.9% previous.

- US Consumer Price Index for May 2023 (MoM) – Forecast +0.2%, versus +0.4% previous.

- US Consumer Price Index for May 2023 (YoY) – Forecast +4.1%, versus +4.9% previous.

- US Consumer Price Index Ex Food & Energy for May 2023 (YoY) – Forecast +5.3%, versus +5.5% previous.

Must BoE Now Consider Larger Rate Hikes? Fed on Course to Pause? Oil Bounces Back

A truly devastating jobs report for BoE policymakers

It's not often that you would refer to a jobs report that delivers a drop in unemployment, record employment and a rise in wages as horrible, but that is exactly what the Bank of England will be feeling today.

The central bank has raised interest rates for the last 12 meetings in a row and yet the economy is showing the kind of resilience that few would have anticipated. This creates an enormous headache for the MPC as it desperately wants to avoid crashing the economy in order to weaken the labour market and get wages and inflation down to more sustainable levels but that's looking increasingly possible at these levels.

A rate hike at the next meeting is now unavoidable – assuming it wasn't already – but a 50 basis point increase could suggest the BoE is throwing in the towel in trying to deliver 2% inflation and a soft landing for the economy. And the withdrawal of any votes for a pause will be equally important as the scale of the hike – we've seen two for four consecutive meetings – and would be another strong sign that the BoE is very concerned.

Is a Fed pause as locked in as markets think?

What the BoE would give to now be in the Fed's position. Inflation is falling and has been for almost a year, while core inflation is also on the decline even if it stands above 5% which is still too high. But progress is clear and there is plenty of optimism that the trend will continue, enabling the Fed to perhaps not just pause tomorrow – which markets are heavily pricing in – but maybe even bring an end to the tightening cycle altogether.

Not that they'll be ready to acknowledge that yet but a pause will certainly be a step in the right direction. The BoE will be wondering where they've gone so wrong. Having been one of the first out of the traps, they may be the last to cross the finish line.

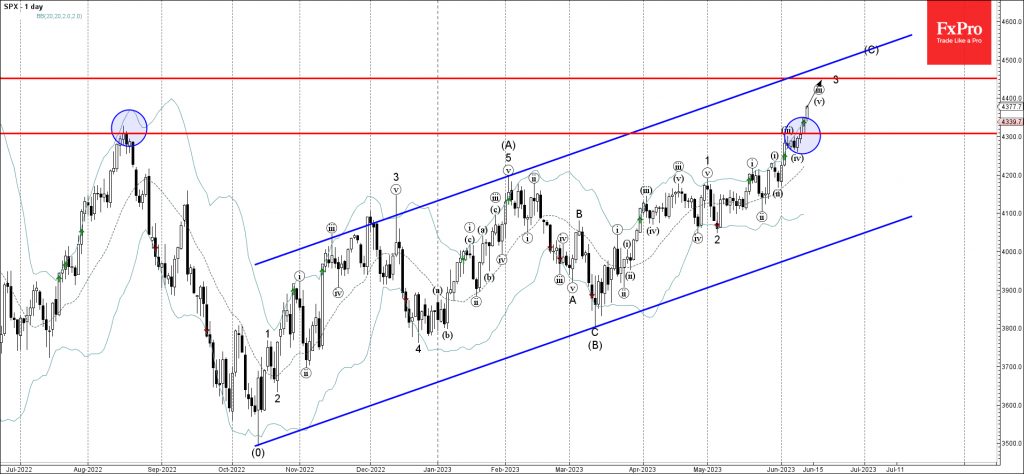

S&P 500 Wave Analysis

- S&P 500 broke key resistance level 4310.00

- Likely to rise to resistance level 4450.00

S&P 500 index recently broke sharply above the key resistance level 4310.00 (former multi-month high from August).

The breakout of the resistance level 4310.00 accelerated the active minor impulse wave 3 of the intermediate impulse wave (C) from the start of March.

Given the strong multi-month uptrend, S&P 500 index can be expected to rise further toward the next resistance level 4450.00 (target for the completion of the active impulse wave 3).

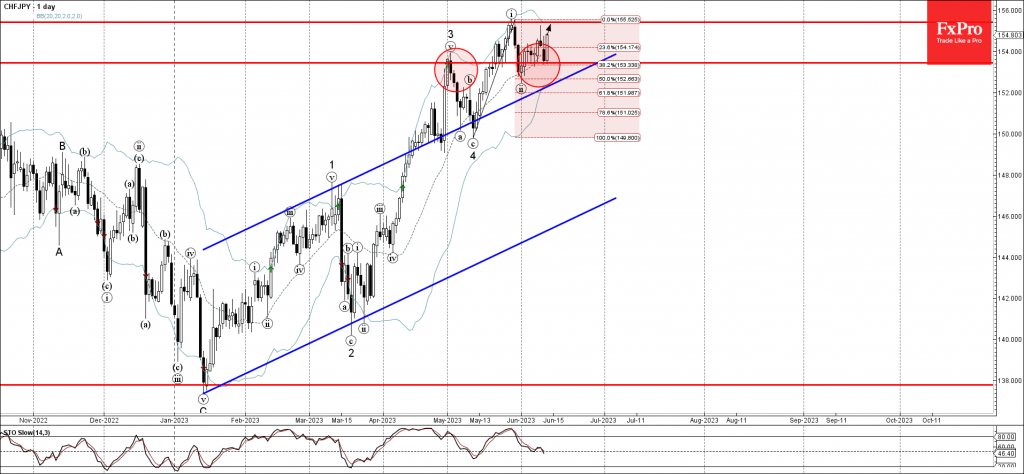

CHFJPY Wave Analysis

- CHFJPY reversed from support level 153.45

- Likely to rise to resistance level 155.400

CHFJPY currency pair recently reversed up from the pivotal support level 153.45 (former strong resistance from the start of May).

The support level 153.45 was strengthened by the 20-day moving average and by the 38.2% Fibonacci correction of the previous sharp upward impulse wave (i).

Given the clear daily uptrend, CHFJPY can be expected to rise further toward the next resistance level 155.400 (top of the previous impulse wave (i)).