Sample Category Title

The Weekly Bottom Line: Canada – Getting Back Into the Game

U.S. Highlights

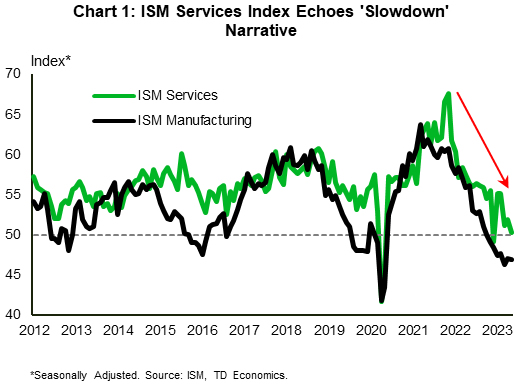

- The ISM Services index surprised on the downside, falling 1.6 points to 50.3 in May. The employment sub-index drifted below the 50-point contractionary threshold for the first time since December.

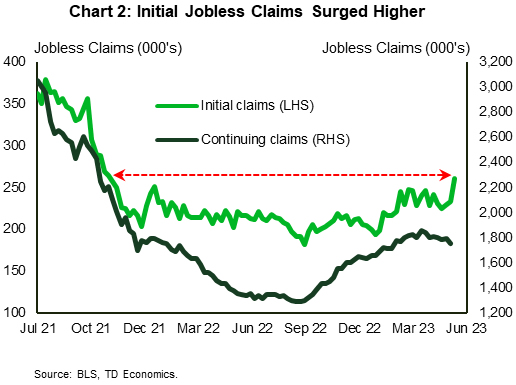

- Initial jobless claims rose by 28,000 in the week ending on June 3rd, lifting initial claims to 261,000 – the highest level in 20 months. However, this week included the Memorial Day holiday, which may have distorted the data.

- The U.S. trade deficit jumped by $14 billion or 23% in April to $74.6 billion – the widest level in six months. The widening of the trade deficit in April indicates that trade is likely to subtract from growth in the second quarter.

Canadian Highlights

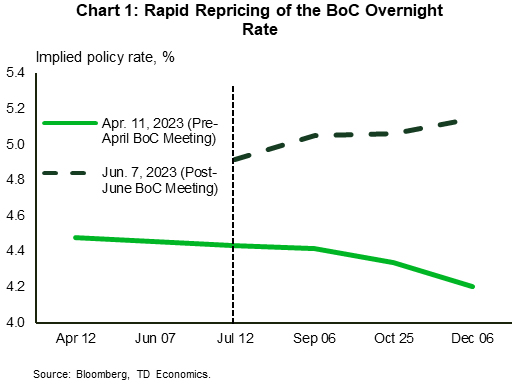

- The Bank of Canada (BoC) raised the overnight rate by 25 basis points to 4.75%, the highest level since early-2001. The BoC has left the door open to further interest rate hikes.

- The Canadian job market was set back -17.3k jobs in May, the first contraction in nine months. It is too early to tell if this crack will continue to grow in coming months.

- Next week’s national housing market data will be watched to see if home sales continued their rapid ascent in May.

U.S. – Mild Signs of a Slowdown Continue

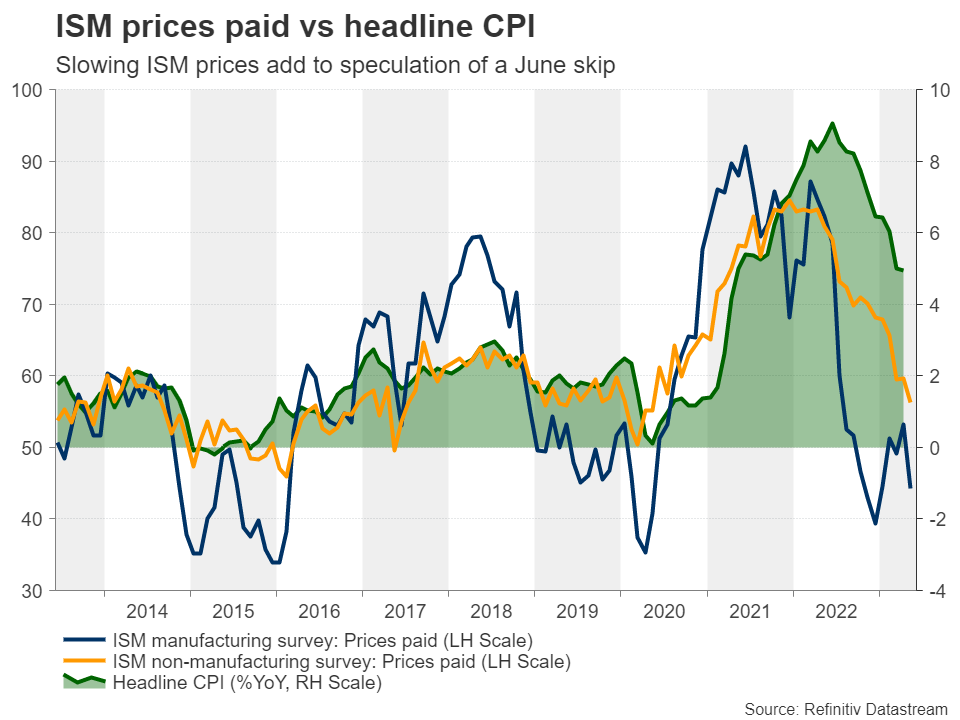

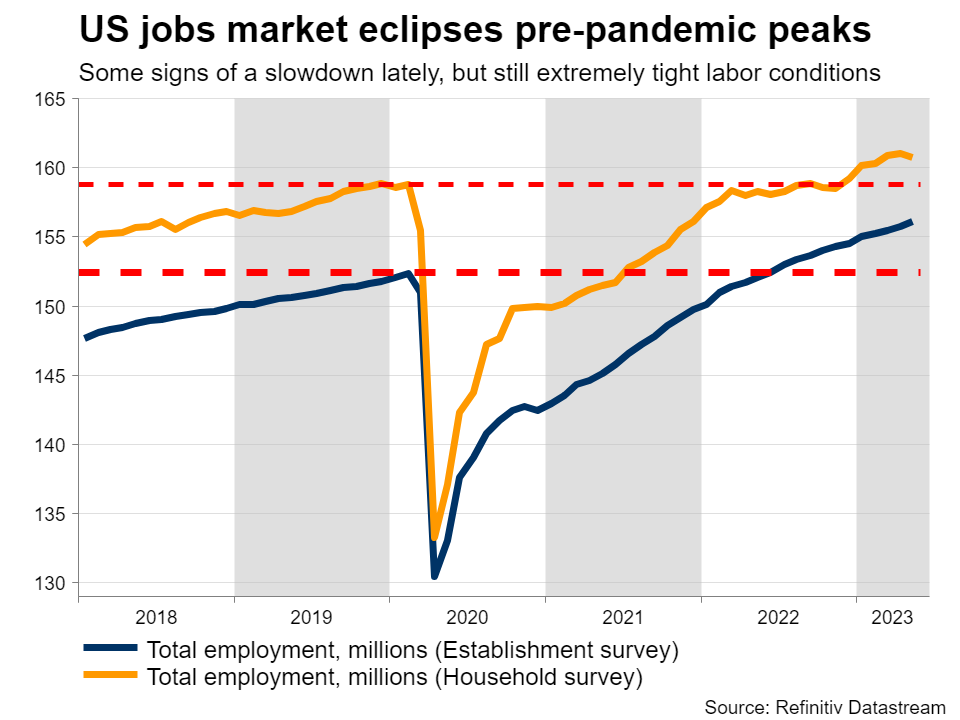

In the wake of last week’s debt ceiling deal, markets had the opportunity to catch their breath in a quiet week for data releases. The ISM Services report disappointed, with the headline index falling 1.6 points to 50.3 in May, instead of improving moderately to 52.4 as per market expectations. The recent downtrend reflects an economy that is gradually decelerating, echoing the ‘slowdown’ narrative advanced by its manufacturing counterpart (Chart 1). This theme was further supported by the report’s details, with all the main sub-indicators – including business activity, new orders, and employment – declining on the month. Of note, the employment index fell 1.6 points to 49.2, drifting below the 50-point contractionary threshold for the first time since December.

Continuing with signs for some potential softening in the labor market, initial jobless claims surged higher in the week ending on June 3rd, rising by 28,000 – much more than anticipated. This lifted initial claims to 261,000 – the highest level in 20 months (Chart 2). While the increase is substantial, for now we caution against reading too much into this. The weekly data can be noisy, and the week included the Memorial Day holiday, which may have also injected some volatility. Secondly, looking at seasonally unadjusted figures, the increase lacked breadth across states, as it was concentrated in Ohio, California, and Minnesota.

April’s international trade report did little to lift the mood. The U.S. trade deficit jumped by $14 billion or 23% in April to $74.6 billion – the widest level in six months. The most noticeable change was in the goods category. The U.S. goods deficit grew by close to 18%, as exports fell 5.3% and imports grew 2%, with the latter marking a rebound after two consecutive monthly declines. Trade made no contribution to economic growth in the first quarter of this year. The widening of the trade deficit in April indicates that it is likely to subtract from growth in the second quarter.

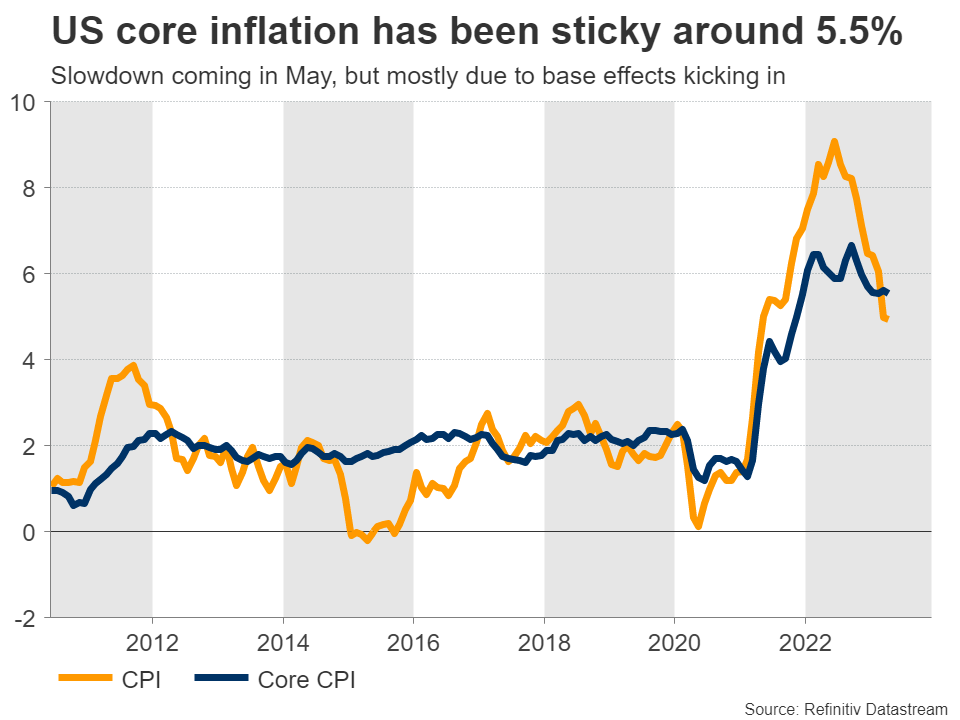

All told, the few reports that came out this week point to growth in the U.S. economy moderating. The Fed will take this information into account before it meets next week to set monetary policy. The last major piece of information on the docket before the Fed makes its decision is May’s CPI inflation report, which comes out one day ahead of the FOMC meeting. The market consensus forecast calls for core CPI to ease moderately to 5.3% year-on-year in May from 5.5% in April. Surprise rate hikes from the Reserve Bank of Australia and the Bank of Canada earlier this week serve as a reminder that amidst stubborn inflation there’s the potential for the Fed to opt for a hike too. That said, Fed officials have been vocal in signaling that they will forego a hike at next week’s meeting. Market odds are in tune with this view, attaching a 75% probability to a stand pat decision next week (as tracked by CME Group). However, markets still narrowly favor a hike at the next meeting in July (52% odds). In short, while next week is likely to be uneventful regarding policy changes, Fed communication may offer additional insight as to whether the FOMC sees the need for some further tightening over the near-term or not.

Canada – Getting Back Into the Game

The Bank of Canada (BoC) has made headlines once again. The Bank raised the overnight rate by 25 basis points (bps) to 4.75% as the conditions it had set to maintain a pause on interest rate hikes had been violated. The BoC will not step back to the sidelines, instead keeping the door open to further interest rate hikes should data reveal ongoing resiliency. Post-announcement, the Canadian two-year yield jumped by 20-bps to 4.58 (down to 4.50 by the end of the week) while the Canadian dollar rallied half a cent to 0.75 cents U.S. and has largely held at this level.

There has been plenty of justification for a rate hike on the data front so far in 2023. Notably inflation, especially core measures, proved stickier than expected in April. Labour markets wouldn't let up as monthly employment gains persistently surprised to the upside, contributing to resilient consumer spending. GDP for the first quarter clocked in at 3.1% quarter-on-quarter (q/q) annualized, above the 2.3% projected in the BoC's April Monetary Policy Rreport. The BoC also called out the recent pick up in spending on interest-sensitive goods and the housing market as evidence that "Excess demand… looks to be more persistent than anticipated".

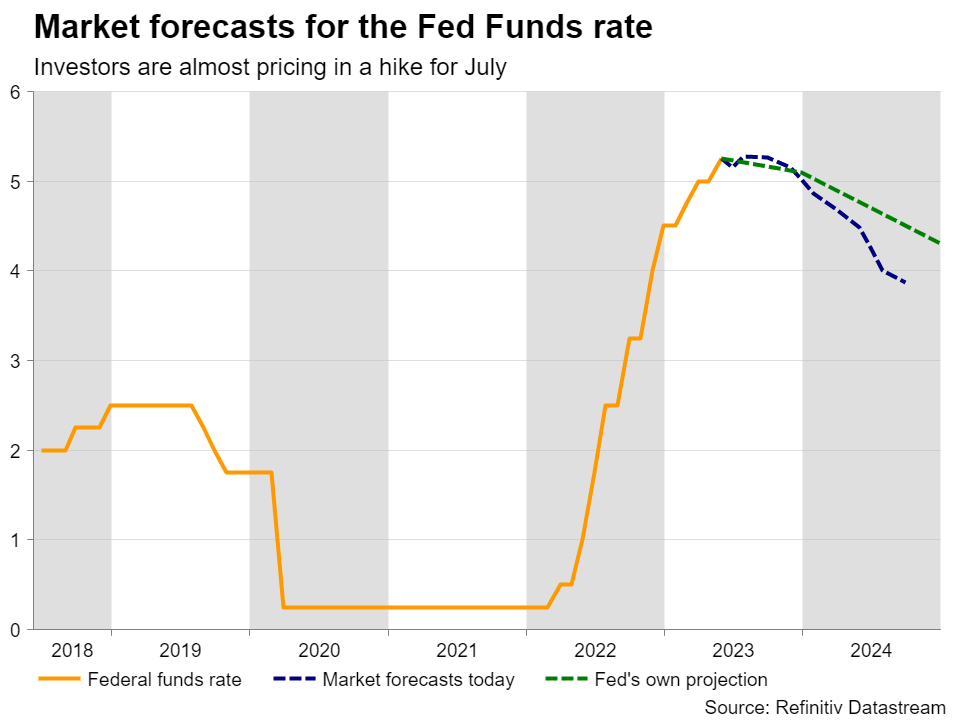

The question is where do they go from here? Chart 1 shows that prior to the April meeting, markets were anticipating the BoC to cut by 25–50 bps by the end of the year. Now, markets expect another 25-bps hike to come, with upside risk for 5.25%. We expect the BoC hike to 5.00% in July and hold at that level into 2024.

The policy rate announcement was delivered before Friday's labour market release for May, which saw Canada shed 17.3k jobs, ending the longest run of job gains since 2017. Full-time jobs contracted for a second straight month (-32.7k), while the unemployment rate ticked up two-tenths of a percent to 5.2%. Hours worked were down 0.4% month-on-month (m/m), potentially as a result of the Alberta wildfires, while wages clocked in at 5.1% year-on-year (y/y). At an industry level, Chart 2 shows that the breadth of employment change–measured on a three-month moving average basis–is coming back into balance. Productivity, measured as real output divided by hours worked, declined for a fourth straight quarter by 0.6%. Canada has been able to sustain a higher level of output through job creation even as productivity notoriously lags, but this trend is unsustainable as employment eventually moderates. All in all, it's too early to tell if May's jobs report signals the start of that trend, or if it is just a small chip on an otherwise super-tight labour market.

Next week features updates to May's housing data, where we expect home sales to continue their strong bounce back. We'll also get a pulse check on Canadian industrial activity via manufacturing and wholesale sales for the month of April.

Fed to ‘Skip’ June Interest Rate Hike Despite Higher Inflation

The U.S. Federal Reserve (Fed) looks likely to pass on raising interest rates next week—though policymakers are talking about a “skip” rather than a pause. The U.S. unemployment rate ticked higher in May, and job openings have continued to fall. But labour markets are still exceptionally tight and have been more resilient than expected despite higher interest rates. Still, it takes time for tighter monetary policy to impact the economy and there are signs that inflation pressures are easing, even if it’s happening more slowly than policymakers would like.

We expect year-over-year growth in the U.S. consumer price index (released a day ahead of the Fed’s rate decision) to slow substantially to 4.1% in May from 4.9% in April. Gas prices were 20% below year-ago levels in May. Oil prices are down after surging in the wake of Russia’s invasion of Ukraine. And soaring food inflation has cooled in recent months with back-to-back month-over-month declines in grocery prices over March and April. Slower food price growth should continue as supply chain pressures ease, and commodity and transport cost all move lower. Rent costs that drove core (ex-food & energy) price growth higher look to have turned a corner as an earlier decline in current market rent price growth ripples through to new leases. The share of goods and services with abnormally high inflation slowed over the spring. And the New York Fed’s inflation persistence index (based on PCE price deflators) also showed a significant deceleration in April. Still, progress has been slow and inflation pressures are still running well above the Fed’s 2% inflation target, making another rate hike in July look likely—even if the Fed takes a pass on a hike next week.

The impact of interest rate increases should be evident in next week’s Canadian National Balance Sheet Accounts data. The debt service ratio (the share of disposable household incomes eaten up by debt payments) almost certainly continued to rise in Q1 of this year—and we expect it to hit a record by the end of 2023. The Bank of Canada ended its conditional pause with a surprise 25 bp hike this week, citing a growing risk that inflation “could get stuck materially above the 2% target” amid persistent excess demand. But higher debt payments and prices are still likely to cut deeply enough into household purchasing power to slow consumer spending and ease inflation pressures over the second half of 2023.

Week ahead data watch

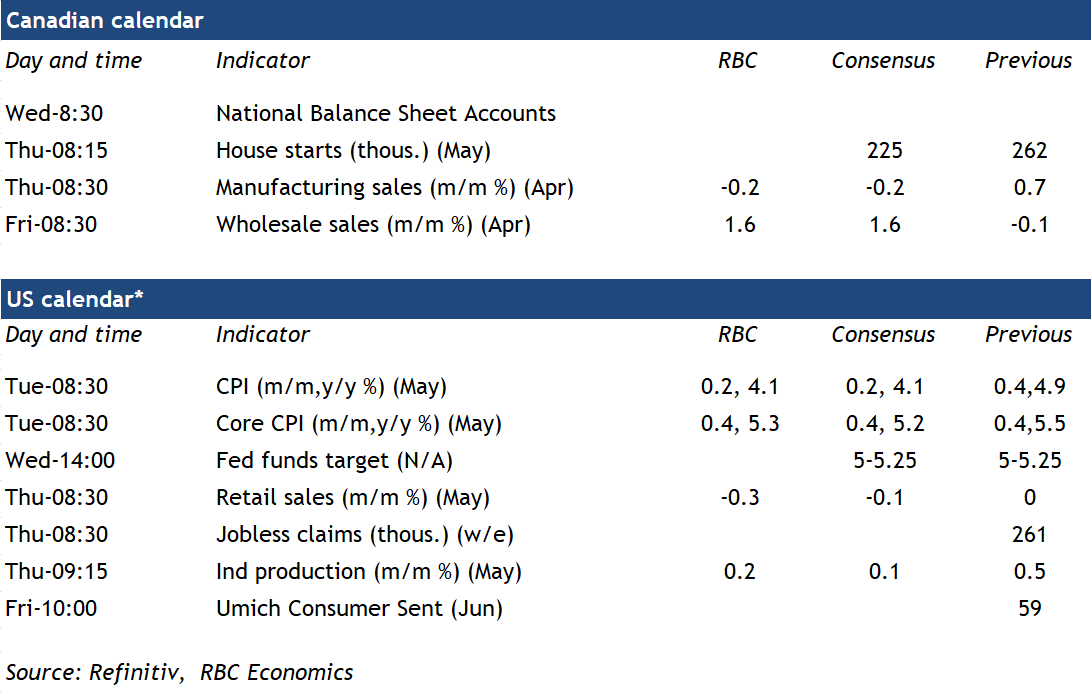

Manufacturing sales in Canada are expected to have declined by 0.2% in April despite strength in motor vehicle shipments, according to an advance estimate from Statistics Canada. That’s not the only soft spot in April. Oil production was flat on a seasonally adjusted basis month over month and the PSAC strike likely subtracted 0.3% from growth. We continue to expect a softer turnout for April GDP than the preliminary 0.2% growth reported by Statistics Canada.

U.S. retail sales likely edged lower in May on lower auto sales and a decline in gasoline prices. Industrial production likely edged higher in May on a weather-related increase in utilities output. Manufacturing hours worked were little-changed in May.

Week Ahead – Time for Fed But First, It’s US Inflation

US

The main event of the week is the FOMC decision, but before we get there, the May inflation report should show that inflation is cooling. Pricing pressures should ease as gasoline prices tumble and as demand destruction starts to become apparent in the data. The negative base effects start to help send the headline year-over-year inflation reading closer to 4.0%.

The Fed is expected to deliver a hawkish skip, but if inflation ends up being too hot, the Fed could opt to deliver a rate hike. This rate decision could be a close call and we should finally start to see some dissents. The US economy has been resilient for most of the year but signs are emerging that it is starting to weaken. If policymakers decide to hold off on another rate hike, there is a chance that this ‘skip’ could end up being a pause. While Wall Street seems confident that the end of tightening is near, sticky inflation in the fall could disrupt how this market has aggressively priced in rate cuts by the end of the year.

Eurozone

The ECB is expected to hike interest rates by another 25 basis points on Thursday is what is expected to be one of the final increases in the cycle. Markets are pricing one more in July but not fully, with the drop in inflation (including core) last month easing the pressure on the central bank to continue. I expect it will stress that there’s more to do and rate cuts are not even under consideration this year but they could indicate that a pause is now on the table.

UK

The biggest pre-BoE data release is the CPI the day before the 22 June meeting but next week offers of a host of other indicators that will attract plenty of attention. The most notable is the jobs data on Tuesday, with traders looking for any indication of slack appearing in the labor market and wage growth subsiding. Without it, the MPC will persevere with tightening. BoE Governor Andrew Bailey will appear before the House of Lords Economic Affairs Committee shortly after the release which could offer some fresh perspective on the data. GDP is also released on Wednesday.

Russia

Revised GDP data is the only noteworthy release next week. The CBR left interest rates unchanged on Friday at 7.5% but warned rate hikes remain on the table due to increased inflationary risks.

South Africa

Another quiet week with retail sales on Wednesday the only notable release. The country avoided recession in the first quarter, buoyed by resilient mining and manufacturing sectors. Rolling blackouts remain a massive constraint on the economy and company profits which will remain a huge headwind going forward.

Turkey

Now that President Erdogan has secured another term, it would seem he’s decided that more conventional fiscal and monetary policy measures may be in order. He’s ignored markets for as long as he could, burning through reserves in the process and now the job of clearing up the mess has been handed to new CBRT Governor, Hafize Gaye Erkan. The lira has sunk more than 10% to fresh lows in recent days so Erdogan’s new team has quite the job on their hands clearing up his mess. Jobs data the highlight of the economic calendar next week.

Switzerland

Very little on the calendar next week, with PPI the only notable highlight.

China

A key week ahead with a string of important economic data releases as well as a decision on the PBoC interest rate.

First up on Monday, we will have the release of several credit conditions data for May; new yuan loans, outstanding loan growth, and M2 money supply. Consensus estimates expect a contraction in credit growth where outstanding loan growth to dip to 11.6% year-on-year from 11.8% recorded in April in line with a reduction in M2 money supply to 12.1% year-on-year from 12.4% in April.

On Thursday, another set of key economic data to digest; retail sales, industrial production, and house price index for May. Industrial production is expected to slow down to 4.1% year-on-year from 5.6% in April, retail sales are also expected to grow at a slow pace of 13.9% year-on-year from 18.4% in April (its strongest pace since March 2021), and average new housing prices in China’s 70 major cities are being forecasted to increase slighted to 0.5% year-on-year from -0.2% in April.

Also on Thursday, the PBoC will announce its decision on its 1-year medium-term lending facility (MLF), the interest rate on loans that it lends to major financial institutions. It has been unchanged at 2.75% since its last cut on August 2022. Expectations have increased for a rate cut this time around due to a string of weak economic data and the recent deposit rate cut from China’s major state-owned banks by 15 basis points and 5 basis points on three-year and five-year term deposits, as per advice by PBoC.

India

A busy week ahead. On Monday, industrial production for April is expected to improve to 1.8% year-on-year from 1.1% printed in March, its lowest growth in industry activity since October 2022. Annual inflation growth for May is expected to slow for a second consecutive month to 4.42% year-on-year from 4.7% in April, its lowest since November 2021.

On Wednesday, we will have another set of inflation data; the wholesale prices, food Index and fuel for May. Consensus estimates for wholesale prices are pegged at -2.35% year-on-year, a deeper contraction from -0.92% in April. If it comes out as expected, it will be a second consecutive month of deflation for wholesale prices.

On Thursday, balance trade data for May is forecasted to show a wider deficit of US$17.4 billion from US$15.24 billion reported in April.

Lastly, June data on foreign exchange reserves and bank loan growth will be released on Friday.

Australia

Two key data to take note of. Firstly, Westpac’s consumer confidence Index on Tuesday where an improvement is forecasted to come in at 3.2% from a significant decline of -7.9% recorded in May.

On Thursday, the focus will be on the jobs market; employment change for May is expected to show an improvement with a gain of 20,000 jobs added after a surprise decline of 4,300 in April. The unemployment rate is expected to hold steady at 3.7%.

New Zealand

On Wednesday, Q1 current account data and food inflation for May will be released. Food prices is being forecasted to increase slightly to 12.9% year-on-year from 12.5% in April. If it turns out as expected, it will be the fourth consecutive month of growth acceleration in food prices.

On Thursday, first-quarter growth is expected to be 2.6% year-on-year, an improvement from the fourth quarter print of 2.2%.

Japan

The balance of trade data for May will be released on Thursday where a wider deficit of JPY1331.9 billion is expected from -JPY432.4 billion recorded in April. A contraction of 0.8% year-on-year in export growth is expected, that’s a significant swing from a growth of 2.6% recorded in April, its softest pace since a fall in February 2021.

On Friday, BoJ will announce the outcome of its monetary policy meeting. Given the recent mixed guidance from Governor Ueda on the future path of inflationary growth in Japan, the consensus is no change in its ultra-loose policy.

Singapore

One key data release to focus on is the balance of trade for May which will be released on Friday. A reduction in its surplus to S$4.2 billion is being forecasted versus a surplus of S$4.71 billion recorded in April.

Economic Calendar

Monday, June 12

Economic Data/Events

- India CPI, industrial production

- Japan PPI

- Turkey current account

- Denmark inflation

- Gas transits to resume for Hungary as maintenance expected to be completed for TurkStream pipeline

- BOE’s Mann speaks in a webinar hosted by Signum

- Asia New Vision Forum expected to host more than 300 business leaders, policymakers, industry practitioners, and opinion leaders

- NATO Secretary General Stoltenberg visits Washington to meet President Biden

Tuesday, June 13

Economic Data/Events

- US May CPI M/M: 0.2%e v 0.4% prior; Y/Y: 4.1%e v 4.9% prior; CPI ex-food and energy M/M: 0.4%e v 0.4% prior; Y/Y: 5.3%e v 5.5% prior

- Fed begins two-day policy meeting

- Australia consumer confidence

- Germany CPI, ZEW survey expectations

- Mexico international reserves

- Spain CPI

- UK jobless claims, unemployment

- BOE Gov Bailey testifies to the House of Lords economic affairs committee.

Wednesday, June 14

Economic Data/Events

- US FOMC rate decision: Expected to keep rates steady, along with updated economic forecasts and Fed Chair Powell’s press conference

- US PPI

- Eurozone industrial production

- India wholesale prices

- New Zealand food prices

- South Africa retail sales

- Sweden CPI

- UK monthly GDP, industrial production, trade

- Monthly IEA oil market report

- Swedish landlord SBBl holds an extraordinary general meeting to approve emergency cash-savings measures

Thursday, June 15

Economic Data/Events

- PBOC meeting to decide on one-year policy loan rate; 1-year Medium-term lending facilities volume could rise from 125B to 225B

- US initial jobless claims, retail sales, empire manufacturing, business inventories, industrial production

- Australia unemployment

- Canada housing starts, existing home sales

- China property prices, retail sales, industrial production

- Eurozone ECB rate decision: Expected to raise Main Refinancing Rate by 25bps to 4.00%, President Lagarde holds a press conference

- France CPI

- India trade

- Japan machinery orders, tertiary index, trade

- New Zealand GDP

- Poland CPI

- Russia GDP

- Spain trade

- NATO defense ministers meet in Brussels

- Fed’s Bullard to speak at Norges Bank, the International Monetary Fund, and the IMF Economic Review hold a joint conference on “The Future of Macroeconomic Policy” in Oslo

- BOE’s Cunliffe speaks at Politico Global Tech Summit — London Tech Week — on ‘Central banks and the future of payments’

Friday, June 16

Economic Data/Events

- BOJ rate decision: No changes expected with monetary policy

- US University of Michigan consumer sentiment

- Eurozone CPI

- Italy CPI, trade

- New Zealand PMI

- Singapore trade

- UK Bank of England inflation expectations survey

- ECB’s Holzmann speaks at the Austrian National Bank’s presentation of updated economic forecasts

- ECB’s Villeroy speaks at a tech conference in Paris

- UK BOE inflation attitudes survey

Sovereign Rating Updates

- Luxembourg (Fitch)

- Norway (Fitch)

- Turkey (Moody’s)

What BOC Surprise Could Mean For Fed

The BOC really shocked markets back on Wednesday when it hiked rates by 25bps. Pretty much everyone was expecting it to be a non-event. Given Canada's unique position, the move impacted how many analysts viewed central banks around the world. The number of traders expecting a "skip" at the next Fed meeting dropped dramatically (though it's still a majority).

What happened?

The BOC was the first G20 country to start pausing rates, all the way back in February. Canada had a spike in inflation like most major world economies, but it was starting to come down at the start of this year. That made Governor Macklem and his Board sufficiently confident to announce that there would be a pause to rate hikes. The bank did make it clear that more rate hikes were still on the table if necessary.

Since then, inflation did come down, in recent months it had started to creep back up. Particularly the core with relation to "second level" effects. That is, when inflation increases, it causes employees to demand higher wages. With relatively low unemployment, businesses are forced to raise wages to retain workers. This is a "secondary" effect of higher prices, and is generally a worrisome trend for central bankers, because it can mean the start of inflation potential spiraling out of control.

The reaction around the world.

The BOE has already acknowledged that inflation has spread to secondary effects, and just yesterday the SNB said it had moved to third level effects in Switzerland. That is when prolonged high interest rates start to slow economic growth. All of this leads to the increasing feeling that central banks are running out of time to get inflation under control. Pausing or "skipping" along the way might be counterproductive.

The rise in inflation in Canada made the BOC also the first of the G20 central banks to "restart" rate hikes. The idea is that they let up the pressure on inflation too soon, and as a consequence it started to rise again. This is something that former US Treasury Secretary Larry Summers has warned about the Fed's upcoming meeting. If there is a "skip", he said, then the Fed might have to hike by "double" at the next meeting to keep inflation under wraps.

Pause vs skip

With governments in high levels of debt and economic growth remaining sluggish, central banks are under increasing pressure to ease up on the tightening as soon as possible. The fear among those central bankers is that if they do, they will lose "credibility" in the fight against inflation. Letting up too soon means inflation can come back, and then monetary policy would have to be even more aggressive. The UK stands as a warning, going months with double-digit inflation despite being the first to start hiking. The slow rate of hikes apparently wasn't enough to suppress inflation and turn it around as fast as more aggressive central banks, like the BOC and Fed.

The BOC going from one of the more aggressive central banks to being the first to pause, and then having to restart hiking has left many investors a little concerned. The Fed might err on the side of "caution" and opt to forego the "skip" at the next meeting. It will likely all come down to the CPI data to be released the day before the FOMC meeting.

Pound Eyes UK GDP and Jobs Data for Clues on BoE Rate Path

The Bank of England doesn’t meet for another couple of weeks and there is quite a bit of data for traders to sift through until then, including employment and GDP numbers for April. The employment report is out on Tuesday followed by the GDP estimate on Wednesday, both due at 06:00 GMT. With inflation still running hot, the choice for the BoE isn’t so much between a hike and a pause but rather, between a small rate increase and a larger one. Stronger-than-expected readings could boost the odds for the latter, lifting the pound.

Some cracks are forming in the labour market

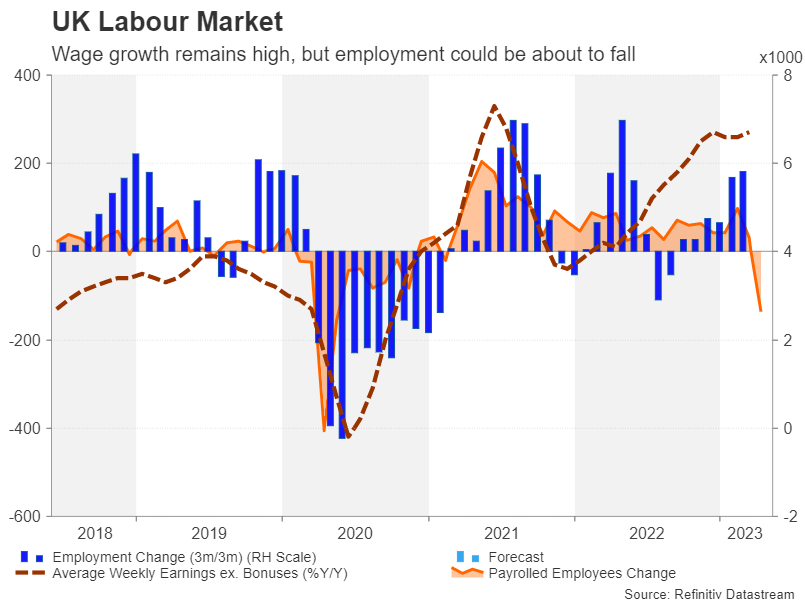

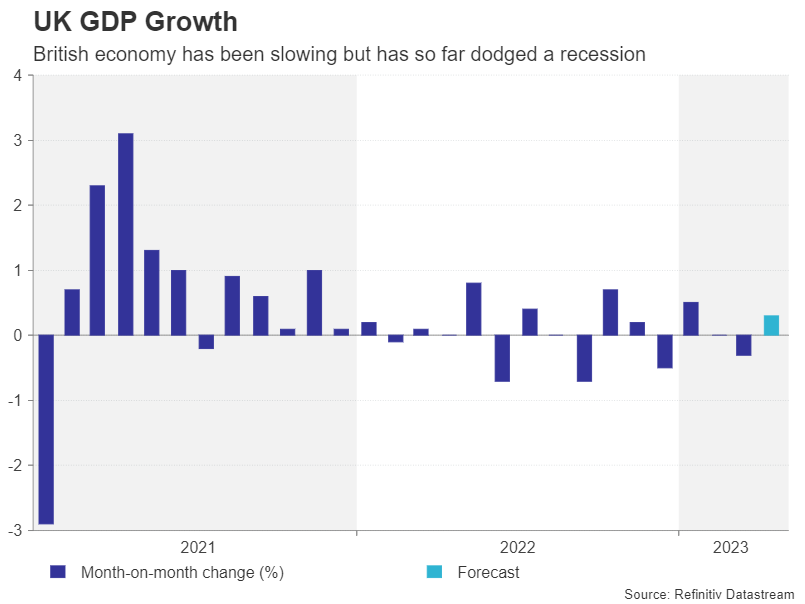

The UK economy has so far avoided a technical recession but nevertheless it ended the first quarter on a weak note. The April stats will therefore be vital to see whether economic output bounced back after the March dip, as despite defying the odds of a recession, the risk of one hasn’t entirely dissipated and even the labour market is showing some signs of a crack.

The unemployment rate has been edging higher since September and could reach 4.0% in the April quarter, having risen to 3.9% in the three months to March. Unusually, total employment has also been growing during this period and was up an impressive 182k in March. However, the more up-to-date payrolls estimate, which is based on data of payrolled employees collected from the UK tax office, points to a sharp deterioration.

BoE wants to see lower wage growth

Payrolled employees fell by 135k in April, suggesting that the official employment figure for the same period will also be weaker. A slowdown in jobs growth would be good news for policymakers, however, as a tight labour market has kept wage growth running around 6% since last August.

When excluding bonuses, average weekly earnings growth has been even stronger and is forecast to hit 6.9% y/y in the three months to April. Without a substantial deceleration in pay growth, the Bank of England will feel pressured to keep hiking rates amid a stubbornly high inflation rate.

A resilient economy

The expectation that UK interest rates will have to rise a lot higher than in other advanced economies has had a mixed effect on sterling as a recession might be the only eventual outcome should inflation not come down fast enough. The Bank of England has been trying to strike a careful balance to not completely choke off growth as it fights high inflation. But the longer sticky inflation remains a problem, the less accommodative monetary policy needs to become.

On the other hand, if the economy continues to withstand everything that is being thrown at it, the farther the BoE will be willing to go with its tightening campaign.

GDP likely expanded by a decent 0.3% month-on-month at the start of Q2 after shrinking by 0.3% in March. Separate figures on industrial and manufacturing production will also be released. If the economy fails to rebound in April, the probability of a 50-bps hike by the BoE on June 22, which currently stands at less than 10%, could evaporate, weighing on the British currency.

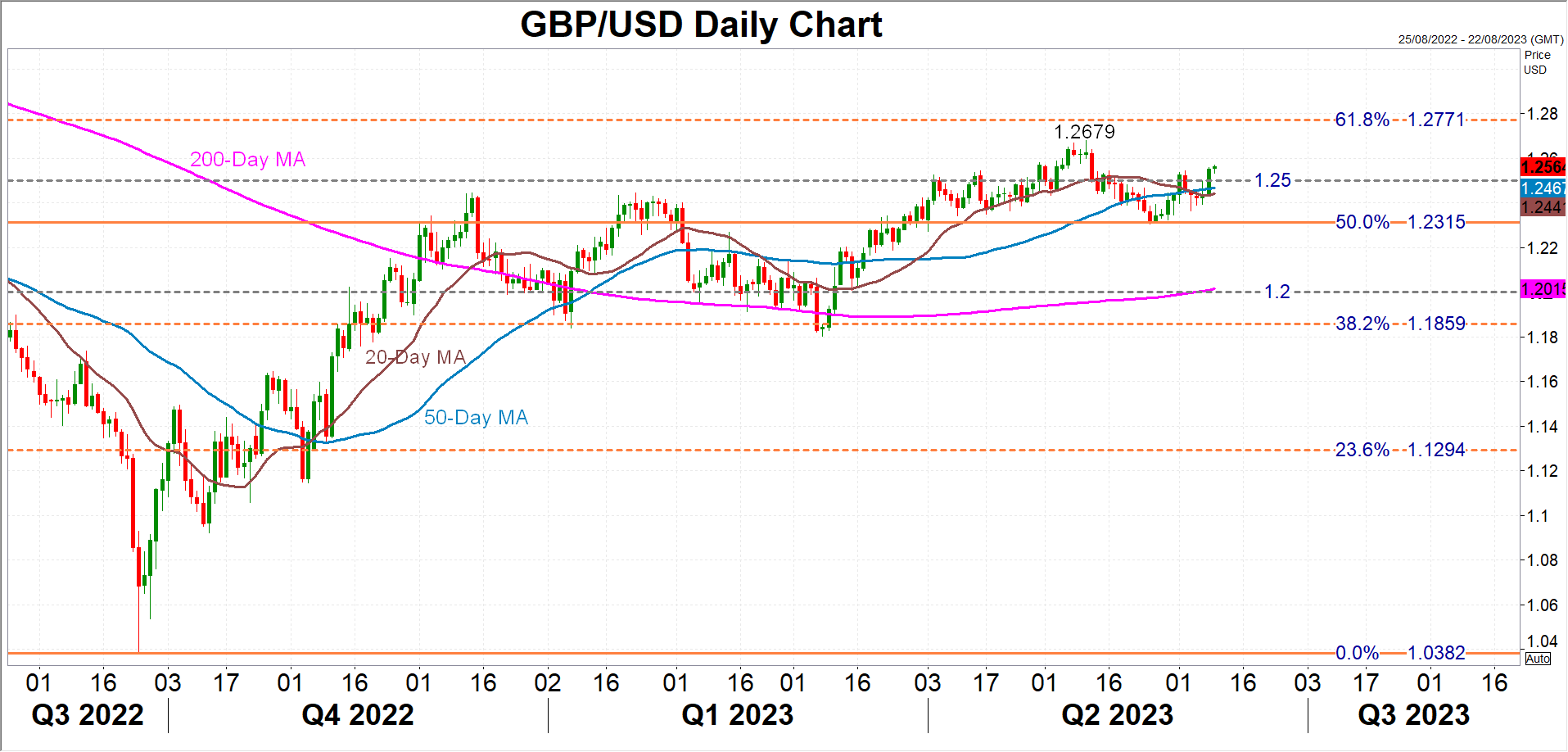

Higher rates not a guarantee for pound uptrend

The pound is consolidating at the moment after touching a one-year peak of $1.2679 on May 10. The 50% Fibonacci retracement of the June 2021-September 2022 downleg at $1.2315 managed to halt the correction at the end of May and could again prevent a steep selloff induced by disappointing numbers. Below that, the 200-day moving average in the $1.2000 region would be an obvious target for the bears.

In the event, however, that the data exceeds expectations, bolstering the ‘higher for longer’ case for the Bank of England, the pound could re-challenge the May top and aim for the 61.8% Fibonacci of $1.2771.

Still, big moves are not very likely from next week’s releases as most traders will be putting more weight on the May CPI report due on June 21. Core CPI shot up to 6.8% y/y in April, in a massive setback for the BoE. Unless this trend reverses quickly in the coming months, UK rates are seen peaking well above 5%. Yet, for the pound to be able to stay on an upward path against the US dollar, the growth side of the story additionally has to hold up.

Will Fed Pause After 10 Straight Hikes?

The FOMC will announce its interest rate decision on Wednesday at 18:00 GMT, with most market participants anticipating the Committee to hit the brakes on rate increases for the first time since March 2022. Having said that, market expectations could very well change just the day before the decision, when the US CPIs for May are due out, thereby impacting the way the dollar may react to the outcome of the meeting. So, what could officials decide and how may the US dollar perform post this gathering?

Investors convinced the Fed will skip a hike

The last time Fed officials met, they delivered the broadly anticipated 25bps hike, but they removed from the statement the part saying that some additional policy firming may be appropriate and instead turned data dependent. As such, market participants started to raise bets that policymakers could take their hands off the hike button as soon as at the next gathering.

After the meeting though, strong economic data and hawkish remarks by Fed officials have encouraged investors to price in a hike either in June or July, with expectations of massive rate cuts by the end of the year being scaled back.

This allowed the dollar to stage a comeback against all its major peers. However, that recovery stalled the last couple of weeks as data pointing to slowing wage growth and subdued prices charged in the manufacturing and service sectors convinced traders that the Fed will skip hiking in June and perhaps do so in July. Specifically, investors are now assigning a 75% probability of no change on Wednesday, while they are penciling in 20bps worth of a hike for July.

As for thereafter, conditional upon a summer hike materializing, market participants foresee nearly two quarter-point cuts by January. Thus, apart from focusing on whether the Committee will press the hike button now, the financial community may also pay attention to the updated macroeconomic projections and especially the new dot plot.

Inflation data to reshape bets just a day before

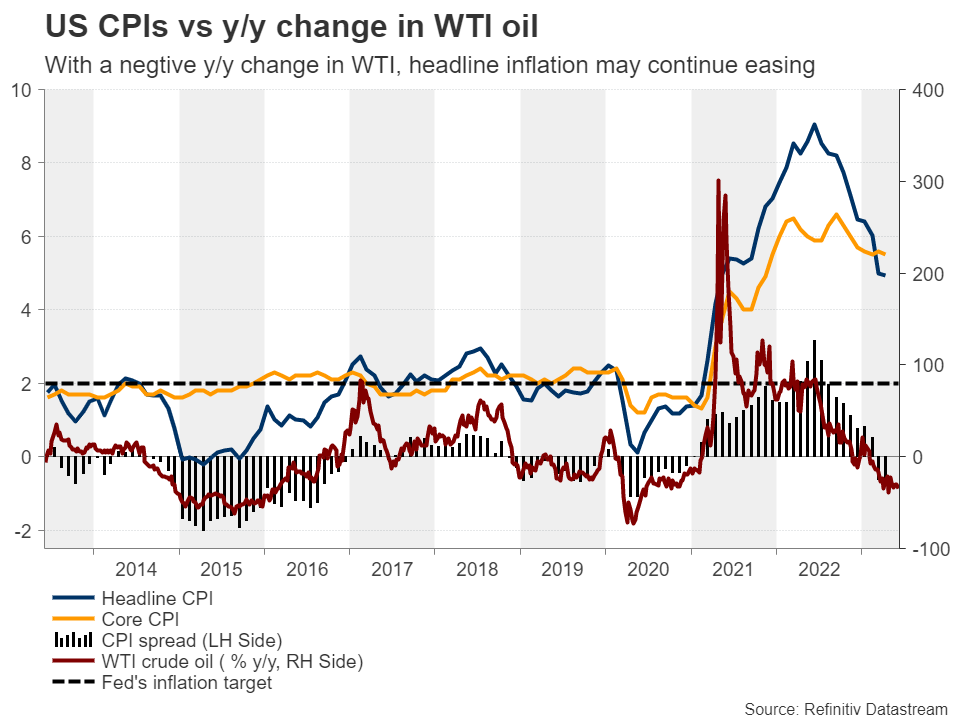

Having said all that though, how the dollar will react to any outcome will depend on the market expectations heading into the meeting, and those expectations could very well be altered the day before the decision, when the US CPIs for May are released. No forecasts are available for the year-on-year rates yet, but with the y/y change in WTI crude oil staying in negative territory, it seems that the limelight is likely to fall on the core rate once again.

A slowdown in underlying price pressures could further diminish the probability of a rate hike on Wednesday and may also lessen the likelihood of that happening in July. The opposite may be true if the core CPI rate accelerates.

Dollar dependent on a combination of outcomes

Therefore, if inflation slows, the Fed will be more tempted to stay sidelined. However, if the updated dot plot shows a higher median rate for this year, the dollar is still likely to rally despite skipping a hike this month, as this will mean a hike in July and no cuts this year. Now, conditional upon inflation accelerating, the only decision that could support the dollar may be a rate increase, as a skip could disappoint those adding to their hike bets just the day before. For the greenback to come under strong selling interest no matter what the results of the inflation report are, the Fed may need to stay sidelined and indicate that no more hikes are needed, which appears to be the least likely scenario at the moment.

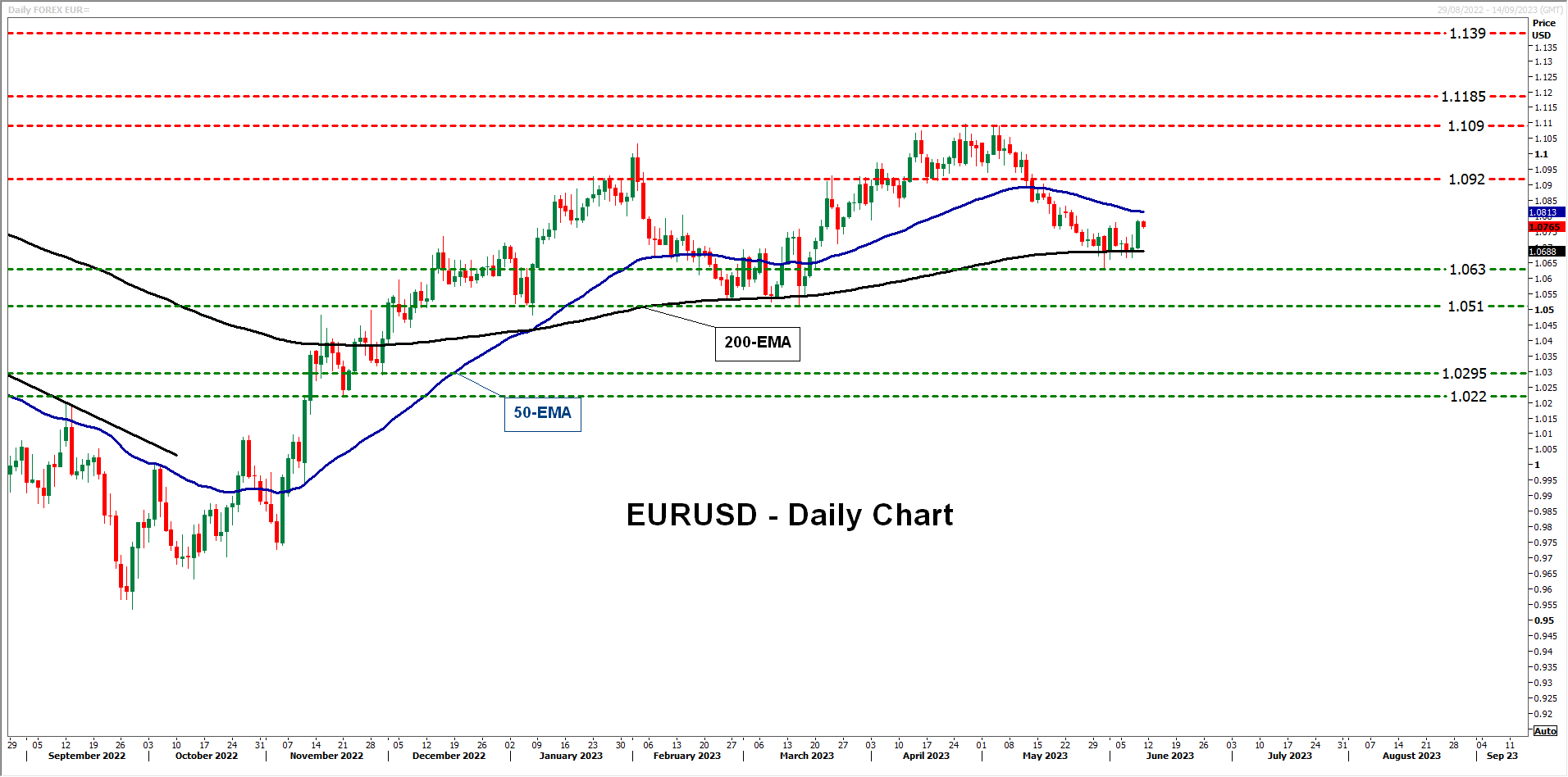

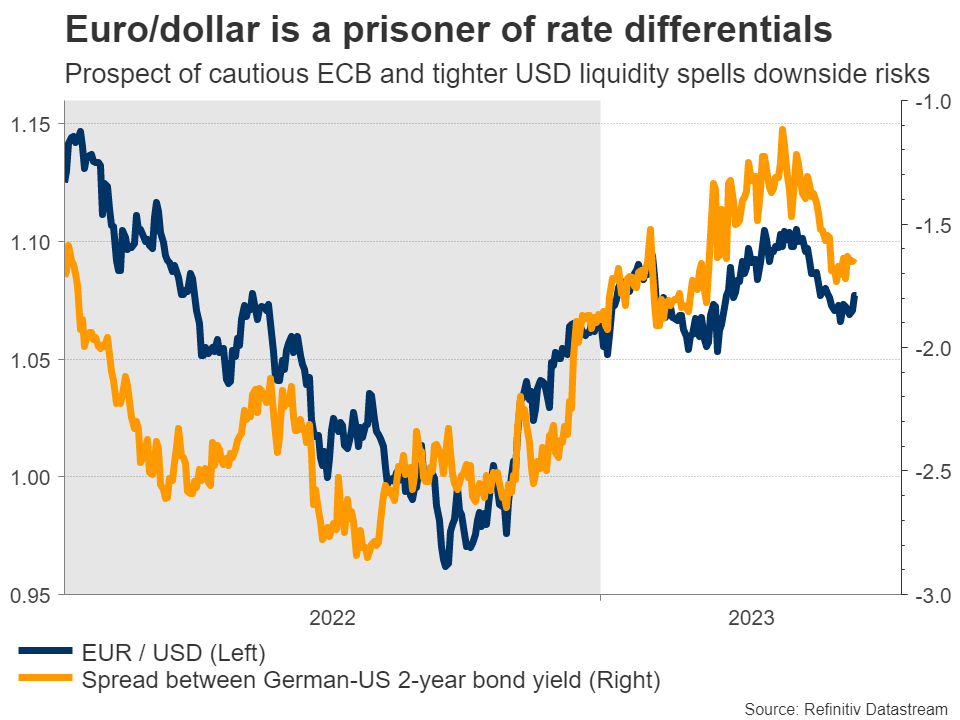

So, with the forthcoming direction of the US dollar dependent on many variables and several combinations of outcomes, the outlook doesn’t seem crystal clear now. The greenback’s comeback has stalled the last couple of weeks, with the currency coming under selling interest on Thursday after initial jobless claims spiked to a 20-month high. This makes the retreat in euro/dollar look like a correction for now.

For a bearish reversal to start being examined, the pair may need to fall below the key zone of 1.0510, which offered strong support between January and March. Something like that could set the stage for declines all the way down to the 1.0295 area, marked by the low of November 30.

On the other hand, a dovish decision could result in advances, but for the picture to be painted with bullish colors, euro/dollar may need to overcome the key resistance zone of 1.1090. If at some point in the not-too-distant future this happens, the bulls may challenge the 1.1185 area, the break of which could carry extensions towards the high of February 21, 2022, at 1.1390.

Week Ahead – Fed, ECB, and BoJ Meet after US Inflation Report

A bombshell week is coming up, featuring rate decisions in the United States, Eurozone, and Japan. The Fed is likely to ‘pause’ according to market pricing, but the decision might ultimately depend on the inflation stats that will be released the previous day, fueling volatility in the dollar. By contrast, there isn’t much scope for surprises in Europe or Japan, leaving those currencies mostly in the hands of other forces.

Split Fed decision?

It will be a difficult decision for Fed officials on Wednesday. By most indications, the US economy is in good shape. The labor market is firing on all cylinders, economic growth is on track to hit 2% this quarter, the housing sector has staged a recovery, and the resilience in demand means that core inflation continues to burn hot.

Hence, the economic data pulse argues for another rate increase next week, although some Fed officials have expressed caution. Led by Chairman Powell, there is a large group within the FOMC that favors “skipping” a rate increase this month, effectively postponing the decision until July.

One of the main elements behind this ‘take it slow’ approach is that the Fed has already raised rates by 5% since last year. The full impact of all this tightening hasn’t been felt yet, and unleashing even more could inflict unnecessary damage on the US economy. Hence, several Fed officials would like some extra time to examine incoming data.

The sharp slowdown in the manufacturing sector has amplified these concerns. Manufacturing is usually seen as a leading recession indicator, so this is worrisome. But in this case, the manufacturing weakness might reflect a hangover following the pandemic boom, as consumption globally switches from goods towards services. As such, it doesn’t seem too scary.

Markets currently assign a 25% probability for a rate increase next week, which increases to 80% for the July meeting. What might influence these percentages though, and the Fed decision itself, is the CPI inflation report on Tuesday.

Both headline and core inflation are likely to have cooled in May on a yearly basis. Yet, that’s mostly mechanical, as some very hot prints from last year will be dropping out of the 12-month calculation. In other words, this is probably a story of base effects, not an ‘organic’ cooldown in inflationary pressures.

As for the Fed decision, it might be a split affair, with a few officials voting for a rate increase but most of them voting for no action. The camp that favors a ‘pause’ is larger and more influential, so that’s the most likely endgame.

Such an outcome might hurt the dollar initially, although whether any weakness persists will depend on the rate projections in the new ‘dot plot’ and Powell’s commentary. If he keeps the door wide open for July, the dollar could bounce back quickly.

In other releases, producer prices for May are due out Wednesday ahead of the Fed decision, while retail sales for the same month are out Thursday.

ECB set to hike despite technical recession

Over in the euro area, the main event will be the European Central Bank meeting on Thursday, where markets have fully priced in a 25bps rate increase. Therefore, the euro’s reaction will depend mostly on any messages about future moves, not the rate hike itself.

The Eurozone economy has fallen into a technical recession according to the latest revised GDP figures, as the troubles in the manufacturing sector left their marks on Germany. Meanwhile, inflation finally seems to be cooling, something reflected in the latest CPI data.

With economic growth rolling over and inflation moderating, it’s likely that the ECB will preach caution and patience. The economy is already contracting and the last thing the central bank wants is to pour gasoline on the recessionary fire.

Market pricing suggests another rate hike is in the pipeline for July, but under these circumstances, the ECB is unlikely to validate that. Officials probably want to keep their options open, and if they signal that they could ‘take a break’ next month, that might come as a disappointment for the euro.

BoJ to bide its time

Wrapping up the week will be the Bank of Japan on Friday. Looking at economic data alone, it’s tempting to speculate that some tightening is warranted. Economic growth turned positive in Q1, inflation is near its highest levels in three decades, and the outlook for wage growth has brightened after the results of the spring wage negotiations.

However, the BoJ is not convinced this is sustainable. Governor Ueda has warned that inflation would likely cool off later this year and that it’s doubtful whether the victories on the wage front will persist. Additionally, the BoJ is concerned about a global slowdown that inflicts collateral damage on Japan.

It’s essentially a game of patience. The BoJ wants credible evidence that inflation will remain sustainably above 2% before it phases out its massive stimulus, so any policy tweaks might take some time. Simply waiting until July would allow policymakers to access new economic forecasts, which makes that meeting a more realistic candidate for any tightening decisions.

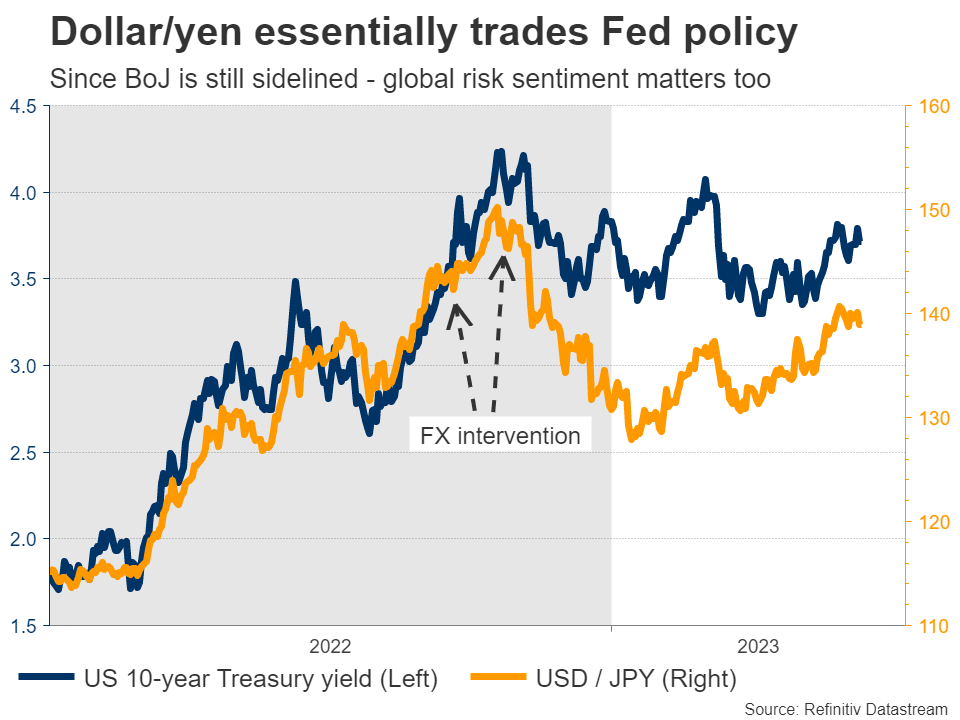

This means that for now, the yen is mostly at the mercy of external forces, namely how foreign central banks act and how global risk sentiment evolves, given its status as a safe haven.

British and Chinese data releases

Elsewhere, it will be a busy week in terms of economic data, starting with monthly GDP data from the UK on Wednesday. Then on Thursday, there will be a deluge of releases from China that include retail sales and industrial production.

Amid signs that the Chinese economy is losing steam as the manufacturing downturn deepens, these figures will be closely watched and could impact commodity-linked currencies like the Australian and New Zealand dollars.

Those economies will also be on the receiving end of crucial data, with Australia’s monthly jobs report and New Zealand’s quarterly GDP numbers both hitting the markets on Thursday as well.

Weekly Focus – ECB Hike Coming Up, What About the Fed?

We are entering a big central bank week, with rate decisions from the US Federal Reserve, the European Central Bank and the Bank of Japan. It seems highly likely that the ECB will deliver another 25bp rate hike, but the Fed outlook is a bit more uncertain. We expect that this will be the first FOMC meeting since January 2022 where there is no rate hike, but market pricing is not ruling out a hike on Wednesday.

Central banks in both Australia and Canada hiked rates in the past week, with Canada's hike being especially surprising. It was the first increase in the country's overnight rate since January, taking it to its highest level in 22 years and sending market rates higher also in the US and Europe.

In the US, the job report for May was clearly stronger than expected in terms of payroll growth, but also showed increasing slack in the labour market from an increasing work force and slowing wage growth. Also, jobless claims were higher than expected this week. In our view, the Fed can afford to pause rate hikes now. Just before the decision next week, we will get the CPI for June, where we can see monthly inflation decline to just 0.2%, also reducing the need for further hikes. Apart from the rate decision, we will also get projections from FOMC members, and there is chance that they will point towards a hike in July.

The ECB has quite clearly signalled that there will be a 25bp rate hike on Thursday which is also fully priced by markets, and an end to APP reinvestment from July. We will get new staff projections and policy signals at the meeting. With the current market mood focusing on signs of decreasing inflation, the market could react strongly on dovish signals from the ECB, while hawkish tones are more likely to be ignored. In the hawkish direction, though, new data show a 5.2% y/y increase in wages in Q1 measured as compensation per employee, the ECB's preferred measure.

We expect the Bank of Japan to tweak the yield curve control at one of the upcoming meetings. Widening of the yield curve control band to e.g. +/-100bps can be explained as a move to improve market functioning, but will essentially be tightening. We still deem it most likely that the BoJ will stay put at the Friday meeting, though.

In China, producer prices declined 4.6% y/y, the biggest decline since 2016. This puts further downwards pressure on consumer prices, which are barely increasing in China and it is possible that we will get more central bank easing. Credit data will be out during the coming week and could be key to watch.

The Turkish lira weakened significantly this week as local banks stopped intervening. Hopes are building up that Erdogan's newly appointed economic team would soon take steps towards normalizing policies. This week's move in the lira can perhaps be seen as an 'intentional devaluation' as opposed to a full loosening of controls. In the absence of interventions, we think there is still room for significant lira depreciation until the central bank credibility is restored and we see interest rate hikes.

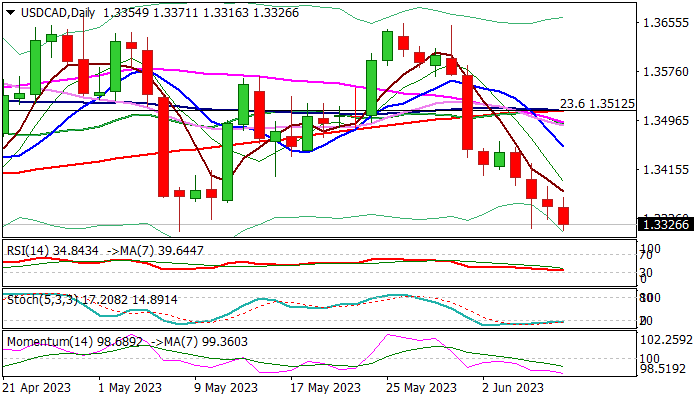

USD/CAD: Canadian Dollar Keeps Firm Tone Despite Downbeat Canada’s Labor Data

The USDCAD continues to trend lower and on track for the second straight big weekly loss, as Canadian dollar received fresh boost from unexpected BOC rate hike earlier this week and renewed hawkish stance, which suggests that further tightening is likely, as the central bank estimates that recent measures were not enough efficient to curb high inflation.

Bears were interrupted by negative Canada’s May labor report, released today and showing higher than expected rise in a number of jobless, while employment slumped by 17.3K in May after adding 41.4K new jobs previous month and strongly missed expectations for 23.2K rise.

However, downbeat labor data so far showed limited negative impact on CAD and likely to be insufficient to stronger counter very positive signals from BOC, as policymakers expected inflation to remain elevated and well above 2%, which will likely require further action from the central bank, as markets fully price for another 25 basis points hike in July.

Daily studies show strong rise in negative momentum and MA’s in bearish setup fueling bears, though a number of solid supports within 1.3315/1.3225 zone is expected to produce headwinds, along with oversold daily studies and probably slow bears in coming sessions.

Larger bears are expected to remain in play as long as upticks stay capped under 1.3440 zone.

Next week’s key events (US inflation/Fed rate decision) are expected to provide fresh signals.

Res: 1.3371; 1.3396; 1.3445; 1.3484.

Sup: 1.3320; 1.3301; 1.3262; 1.3225.

USD/CAD – Canadian Dollar Extends Gains Despite Weak Job Data

- Canada’s economy sheds 17K jobs, unemployment rate climbs

- US dollar under pressure after unemployment claims jump

- Canadian dollar rallies for a third straight day

The Canadian dollar continues to rally. USD/CAD is trading at 1.3328 in the North American session, down 0.22% on the day.

Canada’s labour market softens

The week wrapped up with Canada’s May employment report, which usually is released at the same time as the US job data, but had the spotlight to itself today. The data was a disappointment. Canada’s economy shed 17,300 jobs, all of which were full-time positions. This followed an increase of 41,400 in April and missed the consensus of a gain of 23,200. The unemployment rate rose from 5.0% to 5.2%, the first rise since August 2022.

The weak job numbers could signal softness in the labour market, which would have major ramifications for the Bank of Canada’s rate path. The Canadian dollar lost 40 points in the aftermath of the release but quickly recovered these losses. We could see more movement from USD/CAD on Monday as the markets digest these numbers.

US dollar beats a retreat after jobless claims rise

The US labour market has shown resilience, as we saw last week with a red-hot nonfarm payroll report. Still, some cracks have appeared, such as the jump in the unemployment rate and a low participation rate. The markets are looking for signs that the labour market is cooling off and jumped all over unemployment claims, which surprised on the upside at 261,000, up from 233,000 a week earlier. A spike in one weekly report isn’t all that significant, but the timing of the release close to the Fed meeting may make a Fed pause more likely, and that has sent the US dollar lower against its major rivals.

Bank of Canada delivers a rate hike

Central banks continue to wrestle with high inflation, which has remained stubbornly high despite aggressive rate tightening. This week alone, the Reserve Bank of Australia and the Bank of Canada raised rates by 0.25%, surprising the markets which had expected a pause. The BoC has made clear that its “conditional pause” stance would be data-dependent and perhaps the markets should have paid more attention to the uptick in April inflation and strong GDP growth in the first quarter. The BoC highlighted both of these indicators in its rate statement as factors in its decision to hike rates, and the central bank will be keeping a close eye on economic growth and inflation ahead of the July meeting.

USD/CAD Technical

- USD/CAD is testing support at 1.3339. Below, there is support at 1.3250

- 1.3496 and 1.3585 are the next resistance lines