Sample Category Title

Sunset Market Commentary

Markets

US core bond yields recovered from what we consider an outsized market reaction to yesterday’s disappointing US weekly jobless claims. In a technical trading session stripped of any important data, US yields rise between 1.9 and 4.9 bps with the front underperforming, the Canadian payrolls (see below) only temporarily interrupting the move higher. German Bunds outperform US Treasuries though they did miss out partially on the core bond rally yesterday. Yields add 0.5-1.7 bps at the front while shedding 1.2-2.4 bps further out. Equity sentiment is fragile with the EuroStoxx50 shedding 0.2% after touching the upper bound of the downward sloping short-term trend channel. Wall Street opens with minor gains. The Norwegian crown on currency markets ends the week on a strong note following above-consensus inflation numbers (cf. infra). Its bigger brother, the SEK, could sure use some relief as well with EUR/SEK hovering near a 14-year low. Next week’s Swedish inflation numbers may perhaps do the (same) trick. The Canadian loonie forfeited earlier gains after the job numbers but manages to eke out a tiny gain still. Other majors including the US dollar and euro trade directionless. The Japanese yen is feeling some selling pressure. USD/JPY trades in the mid 139-area and EUR/JPY is testing the 150 barrier. Bloomberg cited officials as saying there’s little need to adjust the yield curve programme at the meeting next week. They recognize inflation is running stronger than expected but aren’t confident enough to say the 2% target is in sight. It does raise chances for some tweaks at the July meeting, when the BoJ is to deliver new quarterly forecasts. Other key events next week obviously include the ECB and Fed meeting. Both will bring updated projections. The former is sure to raise rates further, to strongly hint at another move in July while keeping a data-dependent approach for moves further out (including September). The Fed will probably skip hiking but we expect its updated dot plot to show higher policy rates than the current 5-5.25%. Reasons to do so include ongoing tightness on the labour market, economic resilience, an already bottoming out housing market and (core) inflation stalling at elevated levels. Regarding the latter, the Fed at day one of its two-day meeting gets the May CPI figure served.

News & Views

Consumer prices in Norway in May again printed substantially higher than expected. Headline inflation rose 0.5% M/M and 6.7% Y/Y (6.4% in April). Core CPI-ATE (adjusted for tax changes and ex. energy) jumped 0.7% M/M, raising the Y/Y measure to 6.7%, the highest on record. The rise was broad-based across sub-categories of the basket, with biggest monthly increases registered for food and non-alcoholic beverages (2.3%), clothing and footwear (2.1%), hotels and restaurants (0.9%) and health (0.5%). The May CPI also widely surpassed expectations of the Norges Bank (NB). In its latest monetary policy report (March) the NB saw May CPI-ATE inflation at 6.0%. Early May, the NB raised its policy rate by 25 bps to 3.25%. It flagged another step at the June meeting with according to the projections in the March report could be the cycle top (3.5%). However, NB in May already mentioned the risk that further tightening might be needed if, amongst others, the krone remains weak. Today’s data suggest that the policy rate might be raised to or even beyond 4%. The NB will published new forecasts at the June 22 meeting. The krone anticipates additional interest support rebounding from the EUR/NOK 11.76 area to 11.61 currently.

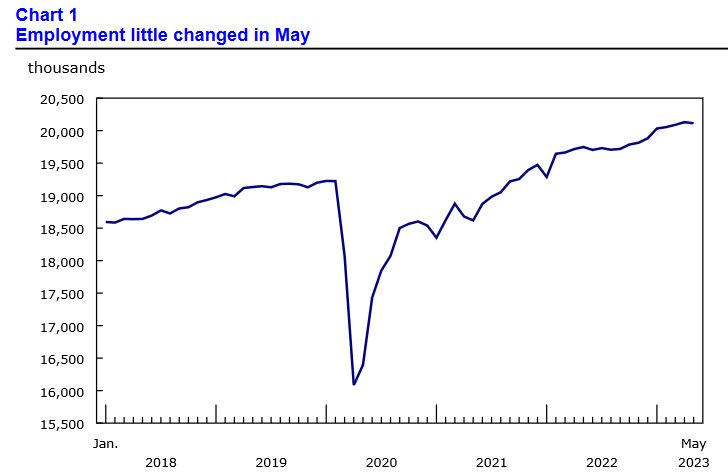

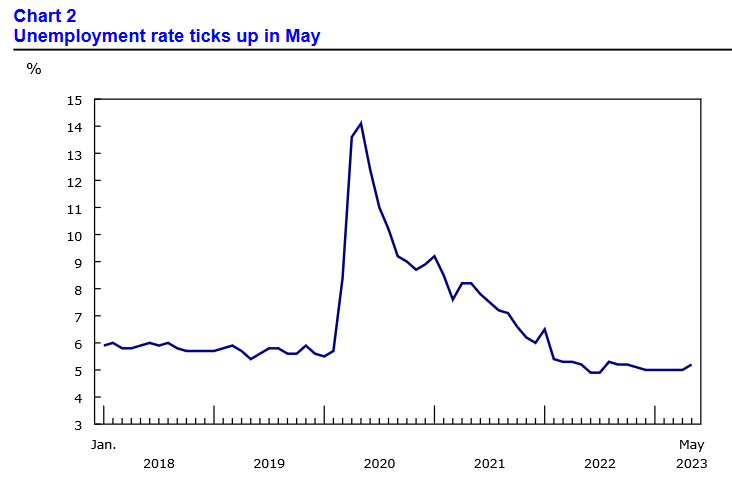

The May Canada Labour Market report was softer than expected. Net employment growth turned negative (-17.3K) to be compared with 41.4k jobs created in April. The decline was due to a loss in the services sector (-40.1k). Employment in goods producing sectors grew by 22.8k. It was the first negative job growth figure in 9 months. The number of unemployed rose by 34.8k. The unemployment rate rose from 5.0.% to 5.2%. The participation rate eased from 65.6% to 65.5%. Average hourly wage growth of permanent workers slowed to 5.1% from 5.2%. The softer data come in the wake of the Bank of Canada this week restarting its hiking cycle (+ 25 bps to 4.75%) on stronger than expected growth, a tight labour market and persist (core) price pressures. Canadian bonds outperform after the data with the 2-ycurrently ceding 4.0 bps. The report also slightly eased market expectations on further BoC rate hikes. However an additional 25 bps tightening is still discounted for the September meeting. The loonie is losing modest ground with CAD/USD rising from 1.332 to 1.335. This compared to a close of 1.3425 end last week.

Canada’s Labour Market Sheds Jobs in May

The Canadian labour market shed 17.3k positions in May, with full-time employment down 32.7k and part-time employment up 15.5k.

The unemployment rate rose 0.2 percentage points to 5.2% and the participation rate dropped 0.1 percentage point to 65.5%.

Employment declined in business, building and other support services (-31k) and in professional, scientific and technical services (-13k). On the positive side, employment rose in manufacturing (+13k), other services (+11k), and utilities (+4k).

Lastly, total hours worked were down 0.4% month-on-month and wages were up 5.1% year-on-year (vs 5.2% in April).

Key Implications

Today's negative print ends a streak of eight months of job gains. While most of the job losses were concentrated in the younger age cohort (15-24 year-olds), the drop in full-time jobs and reduction in hours worked point to weakness under the hood. The question is now: Is this a one off or the start of a trend? The labour market had been defying gravity for months and was bound for some giveback. Our forecast implies that the massive job gains of prior months are behind us, causing the unemployment rate to rise towards 6% by the end of this year.

The Bank of Canada couldn't have seen this coming when it decided to surprise markets with a 25 basis point rate hike on Wednesday. It decided to hike because economic/labour market growth was exhibiting stronger momentum than the Bank was anticipating. While one weak labour market report doesn't make a trend, the BoC will be closely watching to see if other cracks start to form.

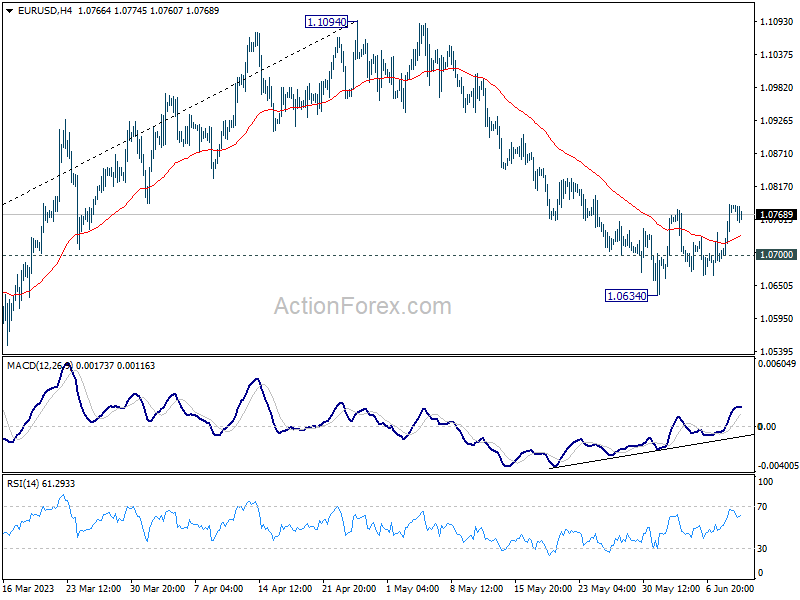

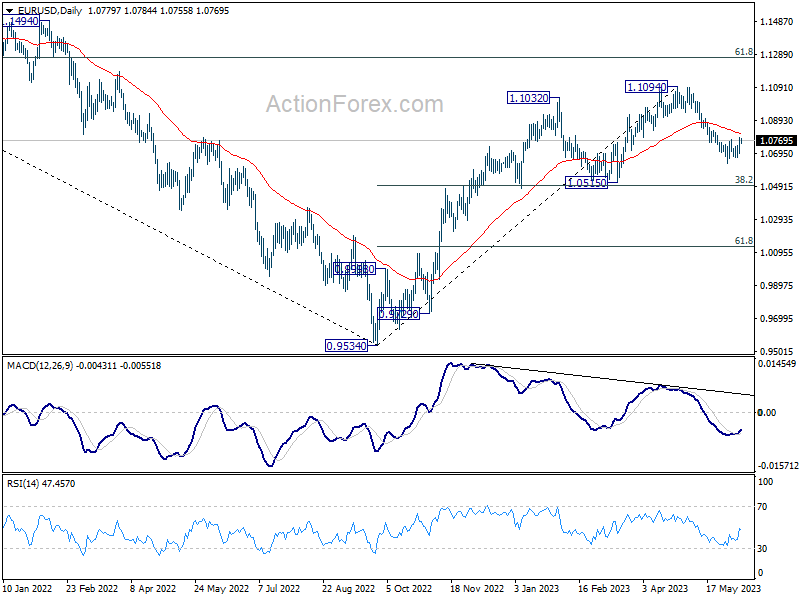

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0724; (P) 1.0755; (R1) 1.0815; More...

Intraday bias in EUR/USD remains mildly on the upside at this point. Rebound from 1.0634 is in progress. Sustained trading above 55 EMA (now at 1.0813) will pave the way back to retest 1.1094 high. Nevertheless, break of 1.0700 minor support should resume the fall from 1.1094 through 1.0634 support.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

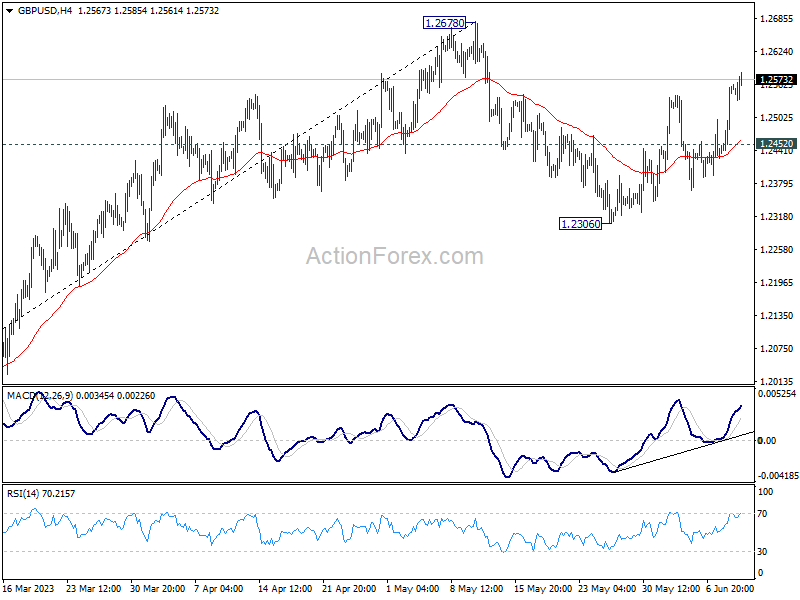

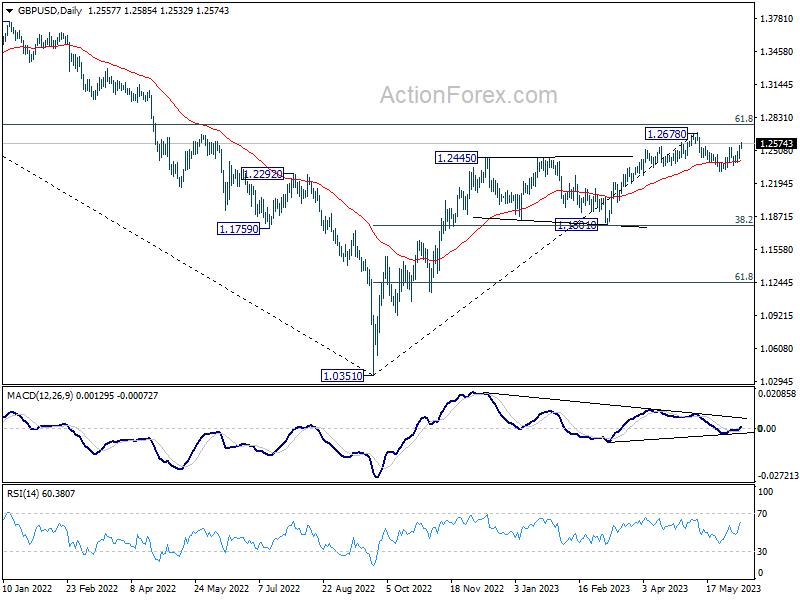

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2475; (P) 1.2518; (R1) 1.2603; More...

Intraday bias in GBP/USD remains mildly on the upside for the moment. Rebound from 1.2306 is in progress for retesting 1.2678 high. However, break of 1.2452 minor support will turn bias back to the downside, to extend the pattern from 1.2678 with another falling leg through 1.2306 support.

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

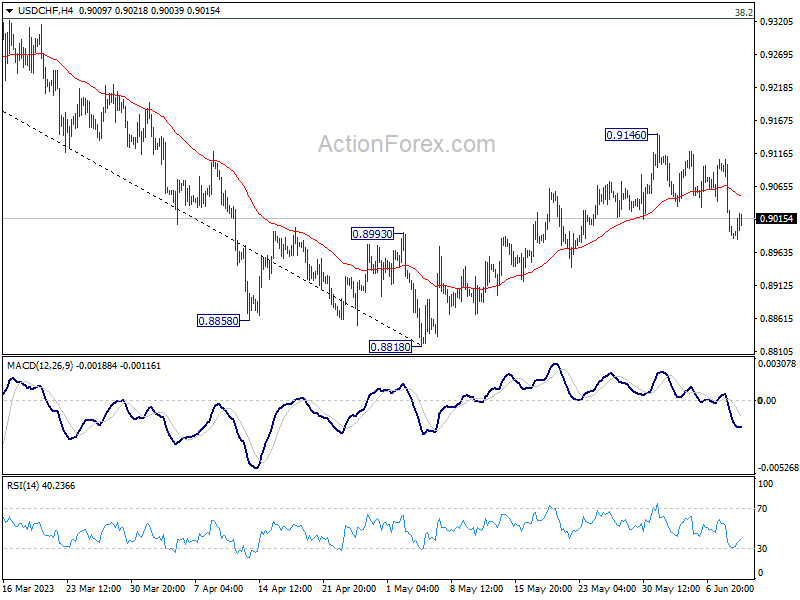

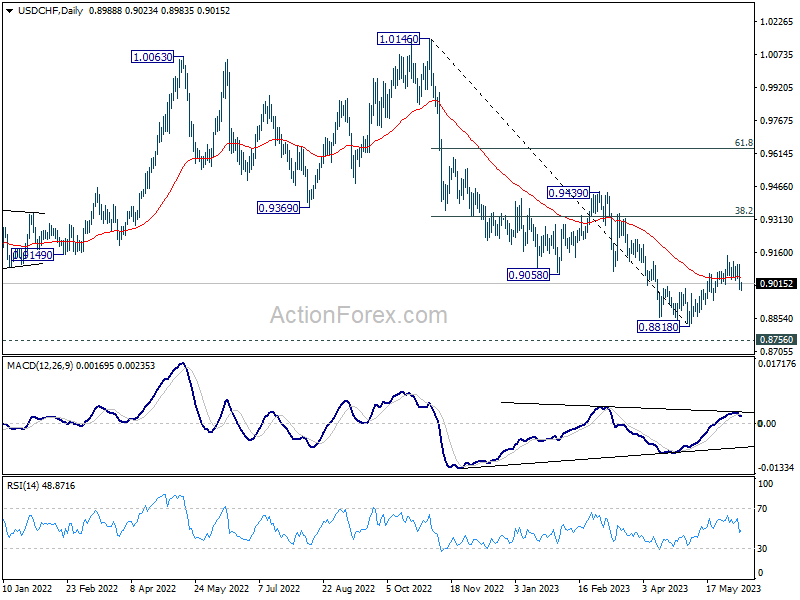

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8951; (P) 0.9029; (R1) 0.9070; More...

Intraday bias in USD/CHF stays mildly on the downside for the moment. Corrective recovery from 0.8818 could have completed at 0.9146 already. Deeper fall would be seen back to 0.8818 and possibly below. But strong support is still needed at around 0.8756 long term support to bring another rebound. Nevertheless, for now, risk still stay on the downside as long as 0.9146 resistance holds, in case of recovery.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming. Further break of 0.9439 resistance will confirm bullish trend reversal.

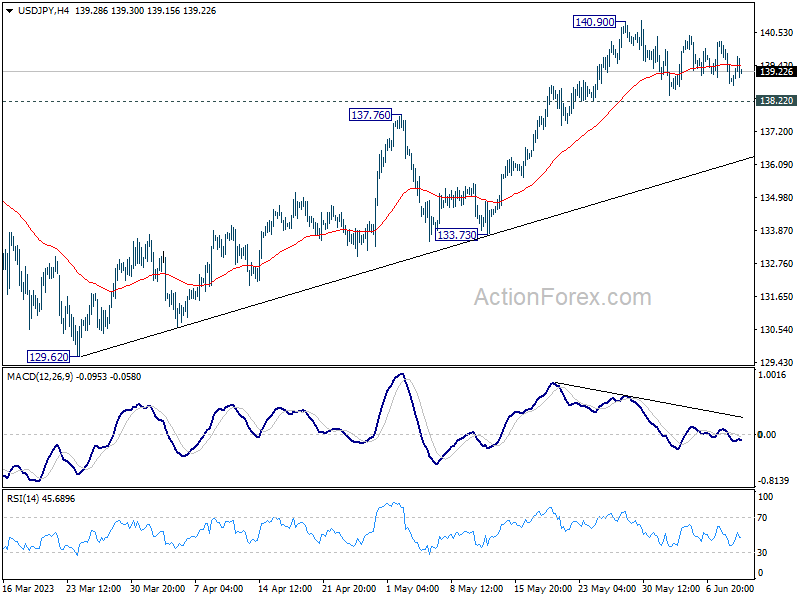

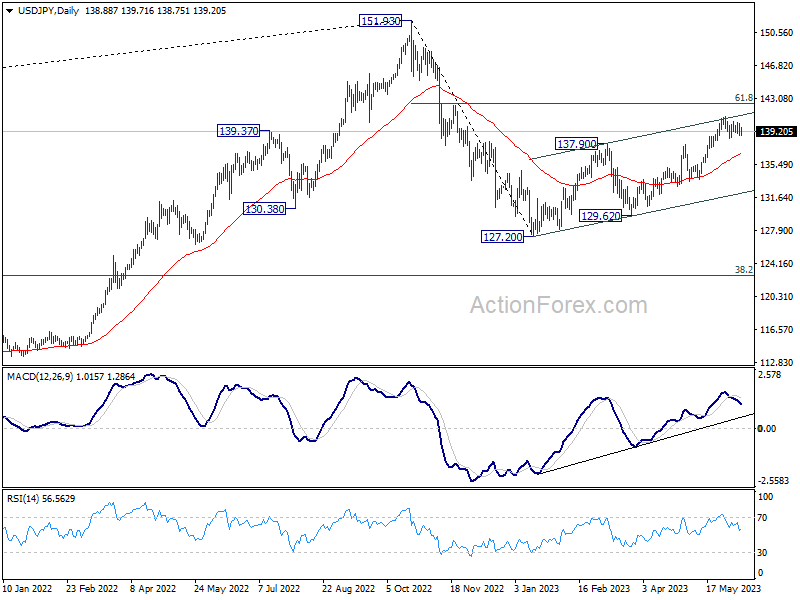

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 138.41; (P) 139.32; (R1) 139.82; More...

Sideway trading continues in USD/JPY and intraday bias remains neutral at this point. With 138.22 minor support intact, further rally is expected. On the upside, break of 140.90 will resume larger rise from 127.20 to 142.48 fibonacci level. However, considering bearish divergence condition in 4 hour MACD, break of 138.22 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 136.70).

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 136.34. Sustained break there will pave the way back to retest 151.93. On the downside, however, break of 133.73 support will argue that the pattern could have started the third leg through 127.20 low.

Yen Staying Generally Weak, Canadian Shrugs Poor Job Data

Yen remains the worst performer for the day, but selloff appears to have slowed somewhat. Meanwhile, Euro and Swiss Franc are also softening, thanks to selling against Sterling. Canadian Dollar is mixed for now, with muted reaction to worse than expected job data from Canada. While the data doesn't add to the case for another rate hike by BoC in July, the eventual outcome will still very much depend on the next around of economic projections. Meanwhile, Australian and New Zealand Dollars are the better performers today. US Dollar turned mixed digesting some of this week's losses.

Technically, EUR/GBP is finally resuming recent decline from 0.8977. Next target is 0.8545 support and then 161.8% projection of 0.8977 to 0.8717 from 0.8874 at 0.8453. The question is whether the selloff in EUR/GBP would spread to other Euro pairs. In particular, attention would be on whether EUR/CHF could break through 0.9670 support to resume larger decline.

In Europe, at the time of writing, FTSE is down -0.51%. DAX is down -0.16%. CAC is down -0.29%. Germany 10-year yield is down -0.026 at 2.379. Earlier in Asia, Nikkei rose 1.97%. Hong Kong HSI rose 0.47%. China Shanghai SSE rose 0.55%. Singapore Strait Times rose 0.01%. Japan 10-year JGB yield dropped -0.0070 to 0.435.

Canada employment down -17.3k in May, unemployment rate rose to 5.2%

Canada employment dropped -17.3k, or -0.1% mom in May, worse than expectation of 21.2k growth. That compared to average 33k monthly growth from February to April. Employment was down -30k in the services-producing sector, and up 23k in the goods-producing sector.

Employment rate dropped -0.3% to 62.1%, reflecting strong population growth of 83k in the month.

Unemployment rate rose from 5.0% to 5.2%, above expectation of 5.1%. That's the first monthly increase since August 2022.

BoJ to persist with monetary easing amid inflation uncertainty, says Ueda

BoJ is committed to maintaining its monetary easing policy as it seeks to sustainably achieve its 2% inflation target, stated BOJ Governor Kazuo Ueda in a parliamentary address.

He acknowledged, "There's still some distance to sustainably and stably achieve our 2% inflation target. As such, we will patiently maintain our monetary easing policy."

Ueda explained that the central bank's strategy is to initiate a positive cycle in which inflation-adjusted wages will start to rise.

However, he also indicated that BOJ anticipates core consumer inflation to dip below 2% target in the latter half of the fiscal year. Despite this projection, Ueda expressed that there remains a substantial degree of uncertainty surrounding the inflation outlook.

One key factor he highlighted is corporate price-setting behaviour, which he stated was "somewhat overshooting expectations."

China CPI ticked up to 0.2% yoy in May, but PPI down -4.6% yoy

China CPI ticked up slightly from 0.1% yoy to 0.2% yoy in May, above expectation of 0.1% yoy. Core CPI, which excludes volatile food and energy prices, slowed from 0.7% yoy to 0.6% yoy.

Food price rose 1.0% yoy, up from prior month's 0.4% yoy. However, price for industrial consumer products dropped -1.7% yoy, worse than April's -1.5% yoy. On a month-on-month basis CPI dropped -0.2% mom, deeper than April's -0.1% mom.

PPI dropped from -3.60% yoy to -4.6% yoy, below expectation of -3.9% yoy. That's also the steepest decline in seven years since May 2016.

Dong Lijuan, an NBS statistician, said the consumer inflation picked up marginally with the gradual recovery in consumer demand, while the fall in factory-gate prices was affected by declining international commodity prices, weak demand for industrial products at both home and abroad, as well as a high comparison base in the previous year.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 138.41; (P) 139.32; (R1) 139.82; More...

Sideway trading continues in USD/JPY and intraday bias remains neutral at this point. With 138.22 minor support intact, further rally is expected. On the upside, break of 140.90 will resume larger rise from 127.20 to 142.48 fibonacci level. However, considering bearish divergence condition in 4 hour MACD, break of 138.22 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 136.70).

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 136.34. Sustained break there will pave the way back to retest 151.93. On the downside, however, break of 133.73 support will argue that the pattern could have started the third leg through 127.20 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y May | 2.70% | 2.50% | 2.50% | 2.60% |

| 01:30 | CNY | CPI Y/Y May | 0.20% | 0.10% | 0.10% | |

| 01:30 | CNY | PPI Y/Y May | -4.60% | -3.90% | -3.60% | |

| 08:00 | EUR | Italy Industrial Output M/M Apr | -1.90% | 0.10% | -0.60% | |

| 12:30 | CAD | Capacity Utilization Q1 | 81.90% | 82.20% | 81.70% | |

| 12:30 | CAD | Net Change in Employment May | -17.3K | 21.2K | 41.4K | |

| 12:30 | CAD | Unemployment Rate May | 5.20% | 5.10% | 5.00% |

Gold Loses Pace Near Key Barrier

Gold got stuck around the resistance trendline that has been blocking bullish actions over the past month at 1,963 following another strong bounce near the 1,938 floor.

The technical indicators in the four-hour chart provide no clear direction. Hence, traders may wisely wait for the price to close above the trendline and the 23.6% Fibonacci retracement level of the latest downfall near 1,965 before they target the 200-period simple moving average (SMA) at 1,985. A greater rally could challenge the 2,000 psychological mark.

If the bears retake control below the 20- and 50-period SMAs at 1,960, the door will open again for the 1,938 base. Failure to bounce there could prompt a fast decline towards the 1,910 restrictive zone, while slightly lower, the 1,895-1,887 region might be another key spot to watch given its constraining role in the first quarter, and the presence of two restrictive lines in the neighborhood.

Overall, caution is necessary as gold is trading near a key resistance territory. A move above 1,965 could provide fresh impetus to the precious metal, though only an advance above 1,985 would boost the price out of the short-term range.

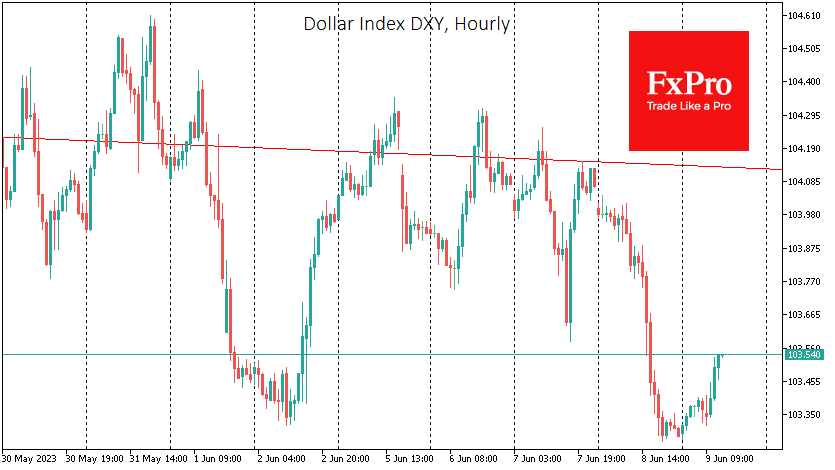

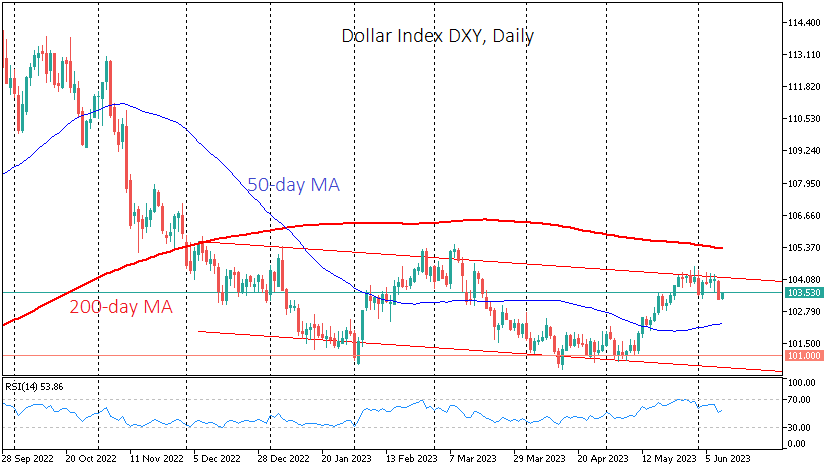

Dollar Index: Bearish Tech Picture vs Bullish Fundamentals

The dollar index lost about 0.7% on Thursday, briefly bouncing back under 103.3. The dollar’s rise against a basket of major currencies stalled late last month and has been trending lower since early June. A situation has developed in which fundamentals are bullish for the dollar, while technical analysis of the medium-term trend favours a decline.

The resolution of the debt ceiling problem forces the US Treasury to return to debt markets with placements. Such actions drain liquidity from the financial system and often cause the dollar to strengthen, as investors prefer US government debt to stocks and bonds of many other governments. And the latest announcements from Treasury Secretary Yellen are setting up near-record placements. What makes the situation unprecedented is that the monetary policy has been stimulative in previous episodes of large auctions: a sharp contrast with the 5% key rate and the Fed selling funds off the balance sheet.

Since the beginning of June, the US Treasury has raised a net capital of $139bn. This is a lot, but because of the accumulated pent-up demand and the buffer built up, we have not seen a noticeable pull into the dollar or a significant sell-off in equity markets. But demand will be saturated, and available liquidity will be depleted, which should work to the dollar’s advantage and is a headwind for equity and commodity markets.

At the same time, the chart picture is still against the dollar. The DXY has been forming a sequence of declining local highs and lows over the past two weeks. It is also easy to see a series of lower peaks on the daily timeframes. Globally, this trend has been in force since last September but has been in the form of a downward channel since December.

In this latest trend, the DXY, having reversed from the upper boundary at the end of May, is now heading towards support below 100.5.

Also in favour of a further decline in the dollar over the next couple of weeks is the return of the RSI from overbought territory, often accompanied by a more substantial pullback.

A bearish “technical” scenario looks quite realistic if the US Treasury does not rush to test the financial system by vacuuming up market liquidity but rather gently probes the ground. There is room for manoeuvre for the US government, as taxes will flow into the Treasury accounts in the coming weeks.

Canada employment down -17.3k in May, unemployment rate rose to 5.2%

Canada employment dropped -17.3k, or -0.1% mom in May, worse than expectation of 21.2k growth. That compared to average 33k monthly growth from February to April. Employment was down -30k in the services-producing sector, and up 23k in the goods-producing sector.

Employment rate dropped -0.3% to 62.1%, reflecting strong population growth of 83k in the month.

Unemployment rate rose from 5.0% to 5.2%, above expectation of 5.1%. That's the first monthly increase since August 2022.