Sample Category Title

Dollar Dominates as Market Anticipates Another Fed Rate Hike in June

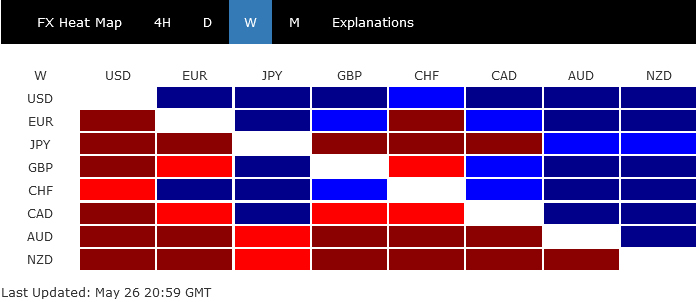

Last week saw the US Dollar dominating the currency markets, with a surprising rally buoyed by market sentiments flipping in favor of an imminent Fed rate hike in June. An atmosphere of growing optimism pervaded the scene, buoyed by increasing confidence in a forthcoming agreement on raising the US debt ceiling, thus staving off a looming government default.

The greenback's impressive stride was synchronized with an appreciable leap in treasury yields. An intriguing development was the apparent decoupling of Dollar's inverse performance from risk markets, as exemplified by NASDAQ's robust gains. It is now speculated that Dollar might maintain this trajectory of reduced sensitivity to risk sentiment in the near future.

Within the foreign exchange market, the New Zealand dollar trailed at the back of the pack. 'Kiwi' took a hit following what was perceived as a dovish rate hike by RBNZ. Australian Dollar, hampered perhaps by market pessimism over a waning Chinese recovery, was the second-worst performer. Yen also languished, buckling under the pressure of escalating global benchmark yields.

European majors, despite losing ground to the dollar, held their own against other currencies. Notably, the Swiss Franc and Euro managed to outpace the Sterling, if only just. These developments serve as a reminder of the capricious nature of the currency markets, where fortunes can shift rapidly based on global economic dynamics.

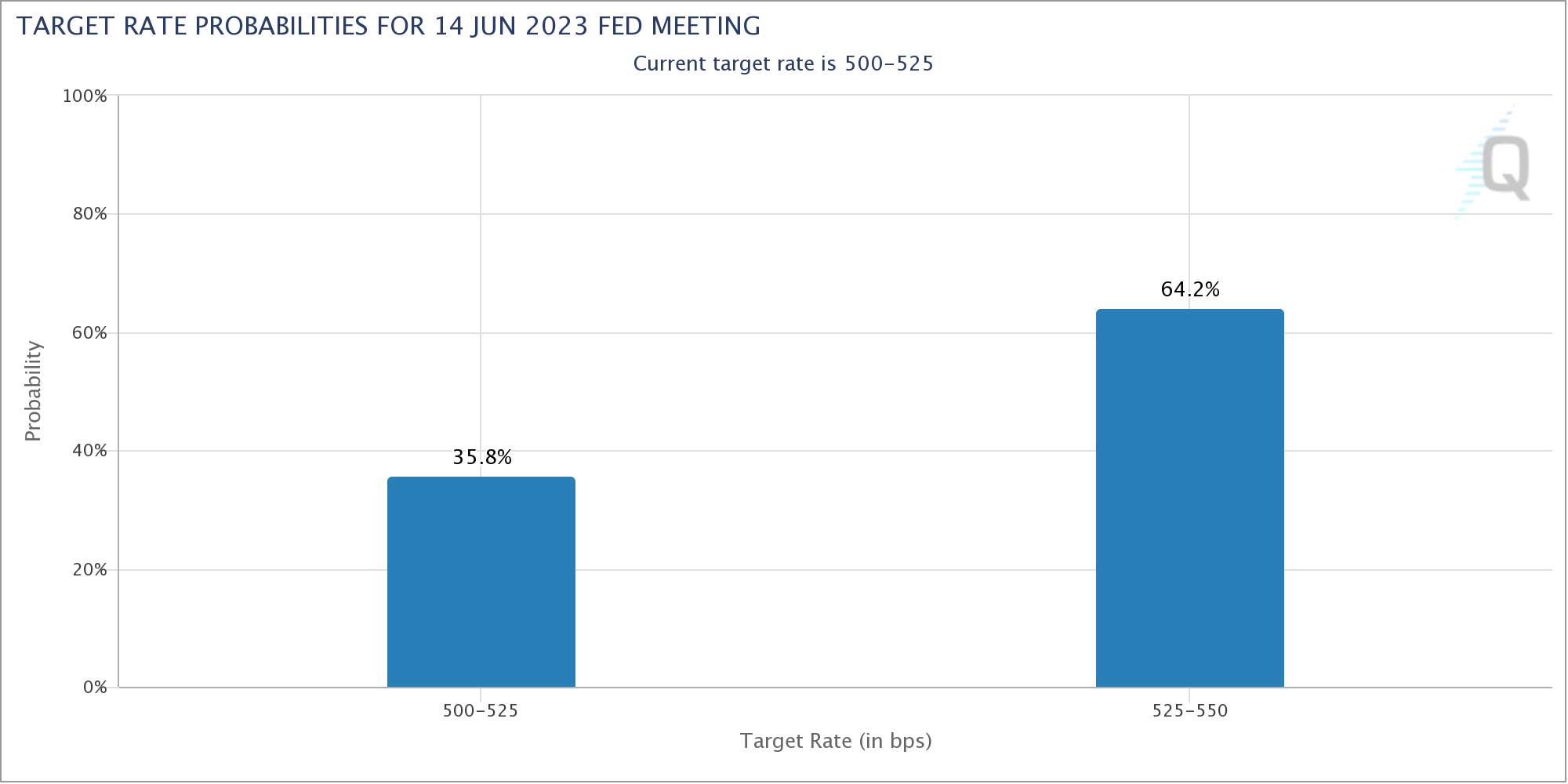

Markets now sees 64% chance of another Fed hike in Jun

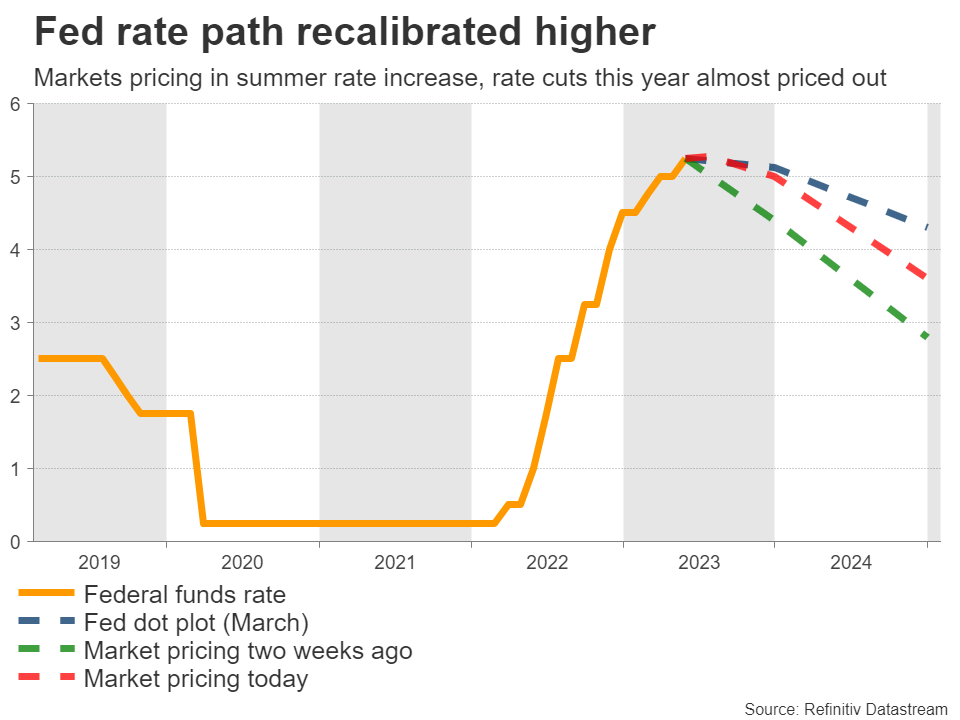

There was an unexpected and drastic U-turn in market expectations for Fed's June meeting. Fed funds futures are now pricing in 64.2% chance of another 25bps hike to 5.25-5.50% on June 14, with 35.8% chance of a odd. A week ago, there was just 17.4% chance of a hike with an overwhelming 82.6% chance of a hold.

The set of strong set release on Friday was a key driver of the change in sentiment. Both headline and core PCE inflation accelerated again in April, to 4.4% yoy and 4.7% yoy respectively. At the same, time, personal spending had robust growth of 0.8% mom, arguing that consumers might have well adapted themselves to the high inflation environment.

In the mean time, IMF also said in a statement: "To bring inflation firmly back to target will require an extended period of tight monetary policy, with the federal funds rate remaining at 5¼–5½ percent until late in 2024."

There are still more than two weeks to go before the next FOMC meeting. Theoretically, there is still lots of room for the picture to change. But markets reactions to upcoming US data, like non-farm payroll report on June 2 and CPI on June 13, could be asymmetric, and be more sensitive to the hawkish side.

Dollar index extending near term rise towards 106

Dollar index extended the rebound from 100.78 short term bottom as expected, to close at 104.20. The rally was driven by both Fed expectations and surging treasury yields. Meanwhile, the greenback has continued to engage in on-off inverse relationship with risk sentiment.

For now, further rally is expected as long as 55 D EMA (now at 102.73) holds, towards 105.88 resistance, and 38.2% retracement of 114.77 to 100.82 at 106.14. Based on current development this target zone could be reached within June.

However, it should be noted that DXY is still seen as in a three-wave corrective pattern from 100.82. Hence, strong resistance could emerge at 105.88/106.14) to complete the rebound. Or, sustained break of 106.14 will argue that it's already in a bullish trend reversal, which would set the tone for an up trend in H2.

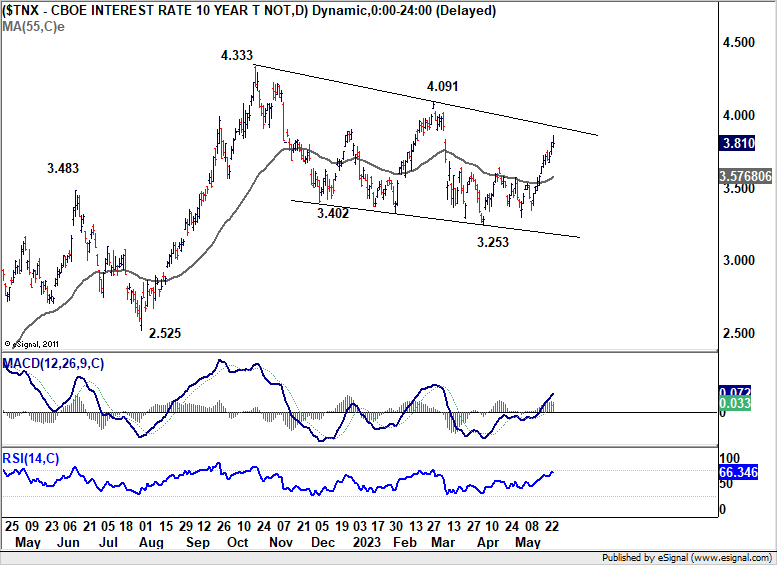

10-year yield in progress for 4.091 resistance next

10-year yield's rally from 3.253 extended higher to close at 3.810 last week. For the near term, further rise is expected as long as 55 D EMA (now at 3.576) holds. The primary question now is whether correction from 4.333 has completed in a three-wave pattern to 3.253. Firm break of 4.091 resistance would boost the bullish case, targeting 4.333.

It's too early to be confident about an upcoming bullish development. But TNX had drawn strong support from rising 55 W EMA (now at 3.312). Thus, the up trend from 0.398 is intact. Firm break of 4.333 would resume the up trend to 61.8% projection of 1.343 to 4.333 from 3.253 at 5.100.

Should this scenario unfold, it's likely that DXY could also break through the aforementioned 106 resistance level, confirming a bullish trend reversal.

NASDAQ surged again as AI rally continued

US stocks concluded the week on a high note as traders harbored hopes an agreement would be reached to raise US debt ceiling, thereby averting a potentially disastrous default. The strong rally towards the week's end suggests that investors were not unduly concerned by potential further interest rate hikes from Fed in June.

NASDAQ, the standout performer, registered its fifth consecutive weekly gain, rising by 2.5%, as the rally in AI continued unabated. The spotlight was undoubtedly on chipmaker Nvidia, which reported an extraordinary earnings performance and its leading position in AI technology. However, other tech giants such as Microsoft, Meta, and Alphabet also made their share of gains, each showcasing their individual contributions to the burgeoning AI narrative.

NASDAQ is now quickly approaching a key clusters resistance zone at 13150/81, 13181.08, 50% retracement of 16212.22 to 10088.82 at 13150.52, and 100% projection of 10088.82 to 12269.55 from 10982.80 at 13163.53.

Rejection by this resistance zone will keep the down trend from 16212.22 intact. However, sustained break there will suggest that the trend has already reversed. Next target is 161.8% projection at 14511.22.

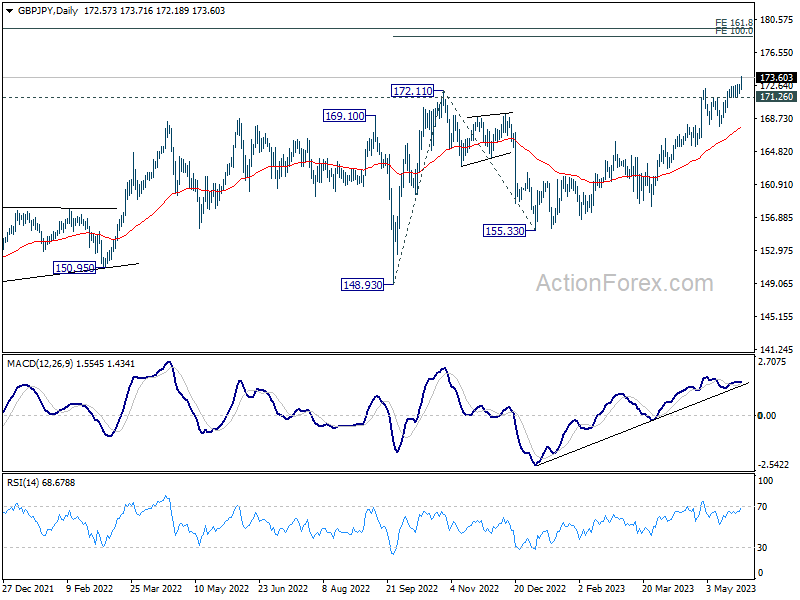

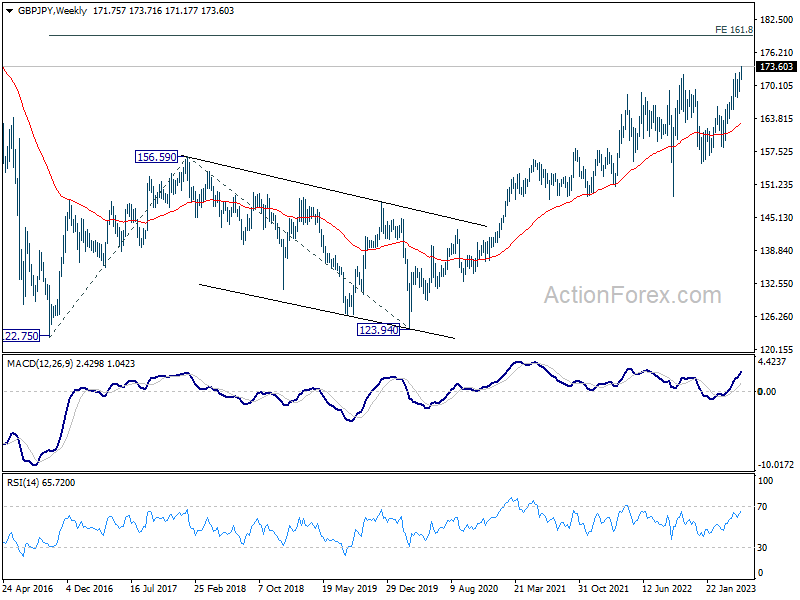

GBP/JPY extending up trend towards 178/180 zone

Yen's development is also a highlight for the near term in addition to Dollar. BoJ Governor Kazuo Ueda threw out the idea of tweaking YCC to target 5-year JGB yields. But that was largely ignored by the markets. After all, the central bank is still not expected to really exit its massive stimulus any time soon. Nikkei is also staying strong, which reinforces its trend with Yen's selloff.

GBP/JPY's up trend finally took off late last week, as UK CPI data suggested that BoE would likely have no change but to tighten again in June. From a near term point of view, further rally is expected as long as 171.26 support holds. Next target is 100% projection of 148.93 to 172.11 from 155.33 at 178.51.

From a medium term point of view, it's now extending the up trend from 123.94. Next target will be 161.8% projection of 122.75 (2016 low) to 156.59 (2018 high) from 123.94 at 178.69.

That is, there might be strong resistance around 178/180 to limit upside. But let's see if the cross could pick up momentum from now on.

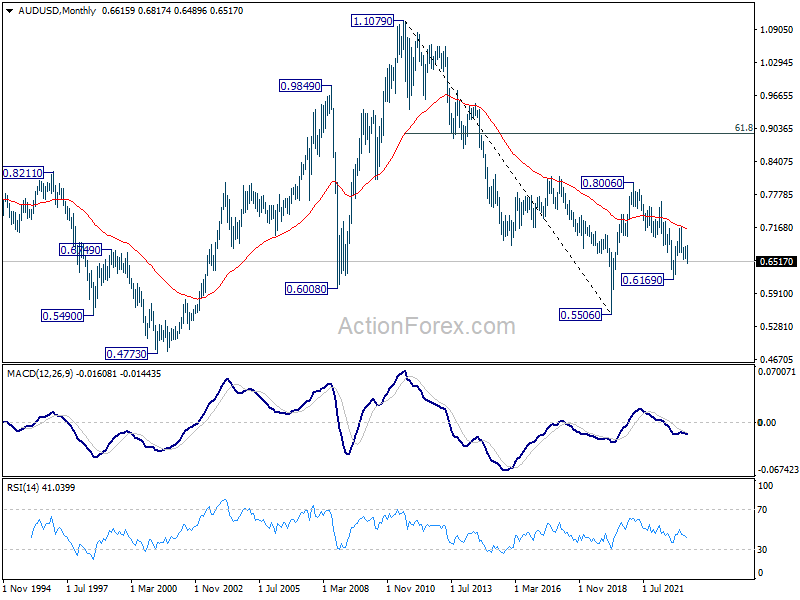

AUD/USD Weekly Report

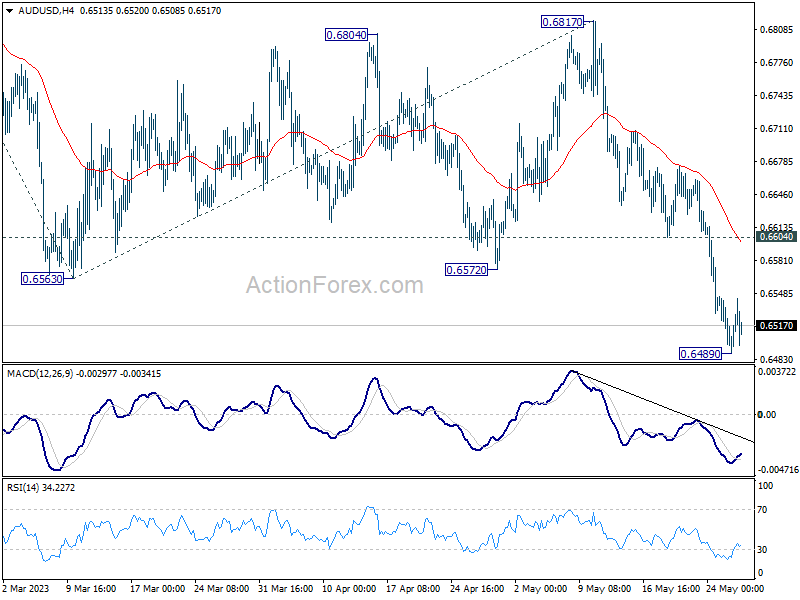

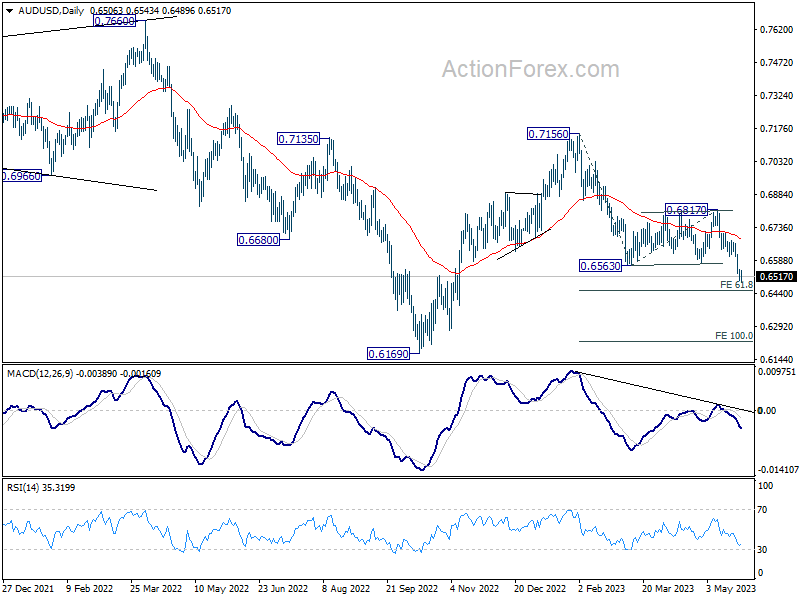

AUD/USD's decline from 0.7156 resumed by breaking through 0.6563 support last week. A temporary low was formed after falling to 0.6489. Initial bias is neutral this week for some consolidations first. Upside of recovery should be limited by 0.6604 support turned resistance to bring another decline. Break of 0.6489 will target 61.8% projection of 0.7156 to 0.6563 from 0.6817 at 0.6451. Firm break there will target 100% projection at 0.6224.

In the bigger picture, rejection by 55 W EMA (now at 0.6822) keeps medium term outlook bearish. Current development suggests that down trend from 0.8006 (2021 high) is possibly still in progress. Retest of 0.6169 (2022 low) should be seen next. Firm break there will confirm down trend resumption. For now, this will remain the favored case as long as 0.6817 resistance holds.

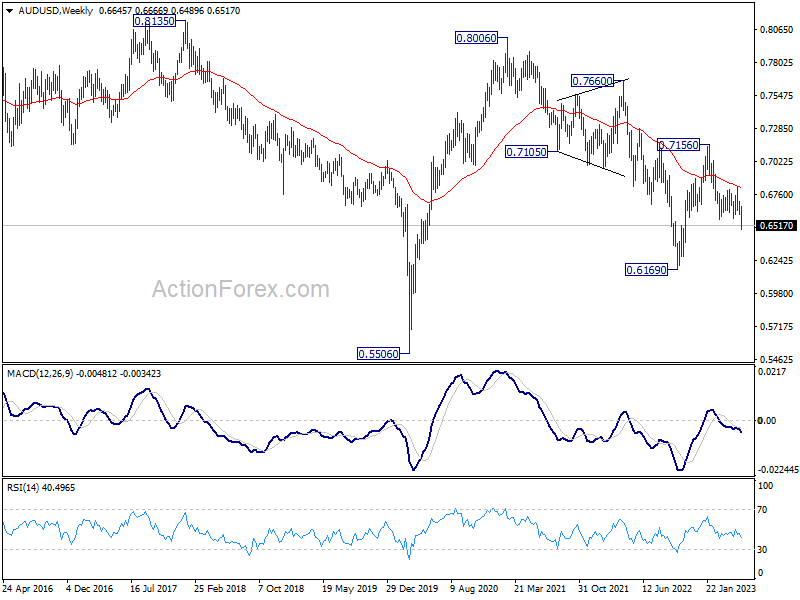

In the long term picture, initial rejection by 55 M EMA (now at 0.7119) retains long term bearishness. That is, down trend from 1.1079 (2011 high) could still resume through 0.5506 (2020 low) on resumption.

BOJ Shifting Tone on YCC?

The USDJPY bumped against the technically important 140.00 handle, and the Japanese government took notice. Both BOJ Governor Ueda and Finance Minister Suzuki addressed the yen, and it has retraced a bit. Does this mean the BOJ could be looking at a policy change?

What happened?

Japan policy makers have had both good and bad news recently. The Nikkei blue chip stock index has returned to highs not seen since 1990 thanks to better results from Japanese firms. Exporters in particular were doing well, as the weaker yen since last year has boosted competitiveness. This increased activity helped boost the country's GDP, which led to hopes that Japan could finally be getting out of its multi-decade slump of lethargic growth and low inflation.

In that context, the BOJ has been hesitant to step away from its ultra-easing policy. Inflation has risen dramatically in the country, doubling the central bank's target. But, that was seen primarily driven by the weaker yen, raising costs for imported goods. In particular, food and energy. The BOJ wants so-called "dynamic" inflation, driven by increased economic activity, which still hasn't consolidated.

You get what you ask for

BOJ governor Ueda's insistence on sticking to the ultra low policy has contributed to the yen weakening against other currencies. Carry trading (selling yen to buy commodity currencies, for example) has returned to increased popularity as other central banks raise rates. The yen had strengthened late last year on speculation that the BOJ could start tightening. Under former ultra-dove Kuroda, it widened the YCC, which in practice caused some tightening. There was rampant speculation that the new governor meant that tightening would be back on the table.

But, as time has gone on, Ueda's insistence on not revising YCC - the first step towards tightening - has progressively convinced more traders that he actually means it. There would not be more tightening, so bets have come back on a weaker yen. Last year, the yen went all the way to 150 before the Ministry of Finance stepped in to do something about it.

Now what?

With the pair hitting 140, it appears that the Ministry of Finance has taken notice, and Minister Suzuki yesterday said he would be watching the exchange rate. That doesn't mean action is imminent, but it clearly was meant to send a message to the markets that the government wouldn't be allowing another depreciation run like last year.

Since a weak yen has monetary policy implications, Ueda finally weighed in. Without making reference to the exchange rate, he said that tweaks could be made to YCC. Previously he had been insistent that nothing would change until the review was over. He went on to clarify that this didn't mean any change would happen, refusing to comment on how likely it was. But it was a clear change in tone, suggesting that while the BOJ is happy to keep easing to support the economy, it won't tolerate another bout of weakness in the yen. 140 might be consolidated as something of a policy floor.

The question now is how committed will the BOJ be in defending the yen, so yen traders might want to pay extra attention to how much bond buying the BOJ does in the coming days.

Summary 5/29 – 6/2

Monday, May 29, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Apr | 7.00% | |

| 23:30 | JPY | Unemployment Rate Apr | 2.70% | 2.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Apr | |

| Forecast: | Previous: 7.00% | ||

| 23:30 | JPY | Unemployment Rate Apr | |

| Forecast: 2.70% | Previous: 2.80% | ||

Tuesday, May 30, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Building Permits M/M Apr | 2.30% | -0.10% |

| 07:00 | CHF | KOF Leading Indicator May | 95.3 | 96.4 |

| 07:00 | CHF | GDP Q/Q Q1 | 0.10% | 0.00% |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Apr | 2.10% | 2.50% |

| 09:00 | EUR | Eurozone Economic Sentiment May | 99 | 99.3 |

| 09:00 | EUR | Eurozone Industrial Confidence May | -4 | -2.6 |

| 09:00 | EUR | Eurozone Services Sentiment May | 10 | 10.5 |

| 09:00 | EUR | Eurozone Consumer Confidence May F | -17.4 | -17.4 |

| 12:30 | CAD | Current Account (CAD) Q1 | -9.9B | -10.6B |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Mar | -1.70% | 0.40% |

| 13:00 | USD | Housing Price Index M/M Mar | 0.30% | 0.50% |

| 14:00 | USD | Consumer Confidence May | 99.1 | 101.3 |

| 23:50 | JPY | Industrial Production M/M Apr P | 1.40% | 1.10% |

| 23:50 | JPY | Retail Trade Y/Y Apr | 7.10% | 7.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Building Permits M/M Apr | |

| Forecast: 2.30% | Previous: -0.10% | ||

| 07:00 | CHF | KOF Leading Indicator May | |

| Forecast: 95.3 | Previous: 96.4 | ||

| 07:00 | CHF | GDP Q/Q Q1 | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Apr | |

| Forecast: 2.10% | Previous: 2.50% | ||

| 09:00 | EUR | Eurozone Economic Sentiment May | |

| Forecast: 99 | Previous: 99.3 | ||

| 09:00 | EUR | Eurozone Industrial Confidence May | |

| Forecast: -4 | Previous: -2.6 | ||

| 09:00 | EUR | Eurozone Services Sentiment May | |

| Forecast: 10 | Previous: 10.5 | ||

| 09:00 | EUR | Eurozone Consumer Confidence May F | |

| Forecast: -17.4 | Previous: -17.4 | ||

| 12:30 | CAD | Current Account (CAD) Q1 | |

| Forecast: -9.9B | Previous: -10.6B | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Mar | |

| Forecast: -1.70% | Previous: 0.40% | ||

| 13:00 | USD | Housing Price Index M/M Mar | |

| Forecast: 0.30% | Previous: 0.50% | ||

| 14:00 | USD | Consumer Confidence May | |

| Forecast: 99.1 | Previous: 101.3 | ||

| 23:50 | JPY | Industrial Production M/M Apr P | |

| Forecast: 1.40% | Previous: 1.10% | ||

| 23:50 | JPY | Retail Trade Y/Y Apr | |

| Forecast: 7.10% | Previous: 7.20% | ||

Wednesday, May 31, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence May | -43.8 | |

| 01:30 | AUD | Private Sector Credit M/M Apr | 0.30% | 0.30% |

| 01:30 | AUD | Construction Work Done Q1 | 0.60% | -0.40% |

| 01:30 | AUD | Monthly CPI Y/Y Apr | 6.40% | 6.30% |

| 01:30 | CNY | NBS Manufacturing PMI May | 49.4 | 49.2 |

| 01:30 | CNY | Non-Manufacturing PMI May | 54.9 | 56.4 |

| 05:00 | JPY | Housing Starts Y/Y Apr | -0.90% | -3.20% |

| 05:00 | JPY | Consumer Confidence Index May | 36.1 | 35.4 |

| 06:00 | EUR | Germany Import Price Index M/M Apr | -0.60% | -1.10% |

| 06:30 | CHF | Real Retail Sales Y/Y Apr | -1.40% | -1.90% |

| 06:45 | EUR | France Consumer Spending M/M Apr | 0.30% | -1.30% |

| 06:45 | EUR | France GDP Q/Q Q1 | 0.20% | 0.20% |

| 07:55 | EUR | Germany Unemployment Change Apr | 15K | 24K |

| 07:55 | EUR | Germany Unemployment Rate Apr | 5.60% | 5.60% |

| 08:00 | CHF | Credit Suisse Economic Expectations May | -33.3 | |

| 12:00 | EUR | Germany CPI M/M May P | 0.30% | 0.40% |

| 12:00 | EUR | Germany CPI Y/Y May P | 6.50% | 7.20% |

| 12:30 | CAD | GDP M/M Mar | -0.10% | 0.10% |

| 13:45 | USD | Chicago PMI May | 47.1 | 48.6 |

| 18:00 | USD | Fed's Beige Book | ||

| 23:50 | JPY | Capital Spending Q1 | 5.50% | 7.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence May | |

| Forecast: | Previous: -43.8 | ||

| 01:30 | AUD | Private Sector Credit M/M Apr | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 01:30 | AUD | Construction Work Done Q1 | |

| Forecast: 0.60% | Previous: -0.40% | ||

| 01:30 | AUD | Monthly CPI Y/Y Apr | |

| Forecast: 6.40% | Previous: 6.30% | ||

| 01:30 | CNY | NBS Manufacturing PMI May | |

| Forecast: 49.4 | Previous: 49.2 | ||

| 01:30 | CNY | Non-Manufacturing PMI May | |

| Forecast: 54.9 | Previous: 56.4 | ||

| 05:00 | JPY | Housing Starts Y/Y Apr | |

| Forecast: -0.90% | Previous: -3.20% | ||

| 05:00 | JPY | Consumer Confidence Index May | |

| Forecast: 36.1 | Previous: 35.4 | ||

| 06:00 | EUR | Germany Import Price Index M/M Apr | |

| Forecast: -0.60% | Previous: -1.10% | ||

| 06:30 | CHF | Real Retail Sales Y/Y Apr | |

| Forecast: -1.40% | Previous: -1.90% | ||

| 06:45 | EUR | France Consumer Spending M/M Apr | |

| Forecast: 0.30% | Previous: -1.30% | ||

| 06:45 | EUR | France GDP Q/Q Q1 | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 07:55 | EUR | Germany Unemployment Change Apr | |

| Forecast: 15K | Previous: 24K | ||

| 07:55 | EUR | Germany Unemployment Rate Apr | |

| Forecast: 5.60% | Previous: 5.60% | ||

| 08:00 | CHF | Credit Suisse Economic Expectations May | |

| Forecast: | Previous: -33.3 | ||

| 12:00 | EUR | Germany CPI M/M May P | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 12:00 | EUR | Germany CPI Y/Y May P | |

| Forecast: 6.50% | Previous: 7.20% | ||

| 12:30 | CAD | GDP M/M Mar | |

| Forecast: -0.10% | Previous: 0.10% | ||

| 13:45 | USD | Chicago PMI May | |

| Forecast: 47.1 | Previous: 48.6 | ||

| 18:00 | USD | Fed's Beige Book | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Capital Spending Q1 | |

| Forecast: 5.50% | Previous: 7.70% | ||

Thursday, Jun 1, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI May F | 50.8 | 50.8 |

| 01:30 | AUD | Private Capital Expenditure Q1 | 1.10% | 2.20% |

| 01:45 | CNY | Caixin Manufacturing PMI May | 49.5 | |

| 06:00 | CHF | Trade Balance (CHF) Apr | 3.73B | 4.53B |

| 06:00 | EUR | Germany Retail Sales M/M Apr | 0.90% | -2.40% |

| 07:30 | CHF | Manufacturing PMI May | 44.5 | 45.3 |

| 07:45 | EUR | Italy Manufacturing PMI May | 45.8 | 46.8 |

| 07:50 | EUR | France Manufacturing PMI May F | 46.1 | 46.1 |

| 07:55 | EUR | Germany Manufacturing PMI May F | 42.9 | 42.9 |

| 08:00 | EUR | Eurozone Manufacturing PMI May F | 44.6 | 44.6 |

| 08:30 | GBP | Mortgage Approvals Apr | 54K | 52K |

| 08:30 | GBP | Manufacturing PMI May F | 46.9 | 46.9 |

| 08:30 | GBP | M4 Money Supply M/M Apr | -0.20% | -0.60% |

| 09:00 | EUR | Eurozone Unemployment Rate Apr | 6.50% | 6.50% |

| 09:00 | EUR | Eurozone CPI Y/Y May P | 6.30% | 7.00% |

| 09:00 | EUR | Eurozone CPI Core May P | 5.50% | 5.60% |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||

| 11:30 | USD | Challenger Job Cuts May | 175.90% | |

| 12:15 | USD | ADP Employment Change May | 167K | 296K |

| 12:30 | USD | Initial Jobless Claims (May 26) | 236K | 229K |

| 12:30 | USD | Nonfarm Productivity Q1 | -2.70% | -2.70% |

| 12:30 | USD | Unit Labor Costs Q1 | 6.30% | 6.30% |

| 13:30 | CAD | Manufacturing PMI May | 50.2 | |

| 13:45 | USD | Manufacturing PMI May F | 48.5 | 48.5 |

| 14:00 | USD | ISM Manufacturing PMI May | 47 | 47.1 |

| 14:00 | USD | ISM Manufacturing Prices Paid May | 52.5 | 53.2 |

| 14:00 | USD | ISM Manufacturing Employment Index May | 50.2 | |

| 14:00 | USD | Construction Spending M/M Apr | 0.10% | 0.30% |

| 14:30 | USD | Natural Gas Storage | 96B | |

| 15:00 | USD | Crude Oil Inventories | -12.5M | |

| 22:45 | NZD | Terms of Trade Index Q1 | -1.10% | 1.80% |

| 23:50 | JPY | Monetary Base Y/Y May | -1.40% | -1.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI May F | |

| Forecast: 50.8 | Previous: 50.8 | ||

| 01:30 | AUD | Private Capital Expenditure Q1 | |

| Forecast: 1.10% | Previous: 2.20% | ||

| 01:45 | CNY | Caixin Manufacturing PMI May | |

| Forecast: | Previous: 49.5 | ||

| 06:00 | CHF | Trade Balance (CHF) Apr | |

| Forecast: 3.73B | Previous: 4.53B | ||

| 06:00 | EUR | Germany Retail Sales M/M Apr | |

| Forecast: 0.90% | Previous: -2.40% | ||

| 07:30 | CHF | Manufacturing PMI May | |

| Forecast: 44.5 | Previous: 45.3 | ||

| 07:45 | EUR | Italy Manufacturing PMI May | |

| Forecast: 45.8 | Previous: 46.8 | ||

| 07:50 | EUR | France Manufacturing PMI May F | |

| Forecast: 46.1 | Previous: 46.1 | ||

| 07:55 | EUR | Germany Manufacturing PMI May F | |

| Forecast: 42.9 | Previous: 42.9 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI May F | |

| Forecast: 44.6 | Previous: 44.6 | ||

| 08:30 | GBP | Mortgage Approvals Apr | |

| Forecast: 54K | Previous: 52K | ||

| 08:30 | GBP | Manufacturing PMI May F | |

| Forecast: 46.9 | Previous: 46.9 | ||

| 08:30 | GBP | M4 Money Supply M/M Apr | |

| Forecast: -0.20% | Previous: -0.60% | ||

| 09:00 | EUR | Eurozone Unemployment Rate Apr | |

| Forecast: 6.50% | Previous: 6.50% | ||

| 09:00 | EUR | Eurozone CPI Y/Y May P | |

| Forecast: 6.30% | Previous: 7.00% | ||

| 09:00 | EUR | Eurozone CPI Core May P | |

| Forecast: 5.50% | Previous: 5.60% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | |

| Forecast: | Previous: | ||

| 11:30 | USD | Challenger Job Cuts May | |

| Forecast: | Previous: 175.90% | ||

| 12:15 | USD | ADP Employment Change May | |

| Forecast: 167K | Previous: 296K | ||

| 12:30 | USD | Initial Jobless Claims (May 26) | |

| Forecast: 236K | Previous: 229K | ||

| 12:30 | USD | Nonfarm Productivity Q1 | |

| Forecast: -2.70% | Previous: -2.70% | ||

| 12:30 | USD | Unit Labor Costs Q1 | |

| Forecast: 6.30% | Previous: 6.30% | ||

| 13:30 | CAD | Manufacturing PMI May | |

| Forecast: | Previous: 50.2 | ||

| 13:45 | USD | Manufacturing PMI May F | |

| Forecast: 48.5 | Previous: 48.5 | ||

| 14:00 | USD | ISM Manufacturing PMI May | |

| Forecast: 47 | Previous: 47.1 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid May | |

| Forecast: 52.5 | Previous: 53.2 | ||

| 14:00 | USD | ISM Manufacturing Employment Index May | |

| Forecast: | Previous: 50.2 | ||

| 14:00 | USD | Construction Spending M/M Apr | |

| Forecast: 0.10% | Previous: 0.30% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 96B | ||

| 15:00 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -12.5M | ||

| 22:45 | NZD | Terms of Trade Index Q1 | |

| Forecast: -1.10% | Previous: 1.80% | ||

| 23:50 | JPY | Monetary Base Y/Y May | |

| Forecast: -1.40% | Previous: -1.70% | ||

Friday, Jun 2, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:45 | EUR | France Industrial Output M/M Apr | 0.30% | -1.10% |

| 12:30 | USD | Nonfarm Payrolls May | 180K | 253K |

| 12:30 | USD | Unemployment Rate May | 3.50% | 3.40% |

| 12:30 | USD | Average Hourly Earnings M/M May | 0.30% | 0.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:45 | EUR | France Industrial Output M/M Apr | |

| Forecast: 0.30% | Previous: -1.10% | ||

| 12:30 | USD | Nonfarm Payrolls May | |

| Forecast: 180K | Previous: 253K | ||

| 12:30 | USD | Unemployment Rate May | |

| Forecast: 3.50% | Previous: 3.40% | ||

| 12:30 | USD | Average Hourly Earnings M/M May | |

| Forecast: 0.30% | Previous: 0.50% | ||

Weekly Economic & Financial Commentary: Long Holiday Weekend Clouded by Debt Ceiling

Summary

United States: Long Holiday Weekend Clouded by Debt Ceiling

- With a deal on the debt ceiling hanging in the balance, the near-term economic outlook remains uncertain. Data released this week suggest the real economy is showing resilience, as new home sales and durable goods orders stabilized, while real personal spending surprised to the upside.

- Next week: Consumer Confidence (Tue), ISM Manufacturing (Wed), Nonfarm Payrolls (Fri)

International: Inflation to Force the Bank of England's Hand

- The U.K. April consumer price index was an unpleasant surprise for Bank of England policymakers. Headline inflation slowed and energy prices receded, albeit by much less than expected. As a result, we now expect the Bank of England to raise its policy rate at both its June 22 and August 3 announcements. We have adjusted up our global growth outlook slightly on the back of improving economic activity, which continues to flow in; however, growth prospects for the global economy this year may be starting to plateau.

- Next week: China PMIs (Tuesday), India GDP (Wednesday), Brazil GDP (Thursday)

Interest Rate Watch: Star Gazing Once Again

- As the FOMC tries to determine what level of interest rates will be sufficient to tame inflation, oneguidepost is the natural rate of interest, or r-star. Estimations resumed this month after being temporarily halted due to the volatility surrounding the pandemic, and suggest the era of a low natural rate of interest remains intact.

Topic of the Week: Is Demography Still Destiny?

- The 2020 Census Demographic and Housing Characteristics (DHC) data were published this week and The population of the United States is not getting any younger. The median age in most states rose between 2010 and 2020 as falling birth rates and domestic migration drove demographic shifts.

The Weekly Bottom Line: “Discretion” Is the Better Part of Valor in Washington

U.S. Highlights

- Negotiators appeared close to a deal to raise the debt ceiling and set spending levels. However, the deal does not address Washington’s medium-term fiscal challenges, which were part of the reason Fitch put the U.S. on a negative watch.

- Consumers continued to spend at a healthy clip in April, contributing to sustained inflation pressures. We continue to expect spending to cool as the year goes on, helping to ease inflation, eventually.

- In the meantime, the Fed is in a tough spot. It will need courage to pause and wait for the full impact of its past tightening to show up.

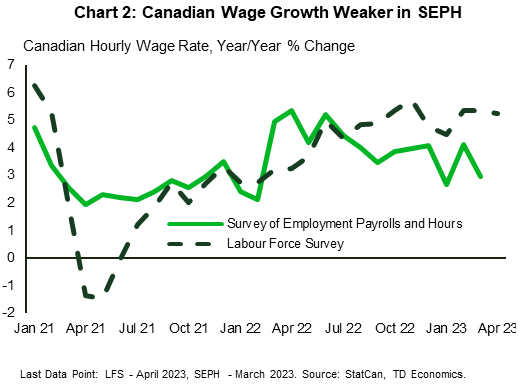

Canadian Highlights

- According to the Survey of Employment Payrolls and Hours (SEPH) March’s employment fell 10k with both goods and services sectors posting declines.

- The number of job vacancies continued to fall with more sectors reporting fewer postings. This improvement, however, made no mark on the measure of labour market tightness, which remained unchanged from February.

- The SEPH also showed a continued deceleration in year-on-year estimates of wage growth but it is partially attributed to base effects and may reverse. All said, this week’s data doesn’t make a strong case for the BoC to come off the sidelines just yet.

U.S. - “Discretion” Is the Better Part of Valor in Washington

Thankfully, negotiators appeared close to a deal to raise the debt ceiling as of Friday morning. It looks like the two-year deal would cap discretionary spending and raise the debt ceiling through the 2024 election, avoiding the worst-case scenarios. However, ratings agency Fitch had cited the “failure of the U.S. authorities to meaningfully tackle medium-term fiscal challenges” as a reason for putting the U.S. on a negative watch, and this deal does not change that.

Congress has taken the Shakespearean proverb “discretion is the better part of valor” literally. The Bard’s original intention was a criticism of a lack of honour and courage in focusing on discretion. The debt ceiling deal only tinkers around the edges of the larger issue of a structural deficit on the order of 6% of GDP.

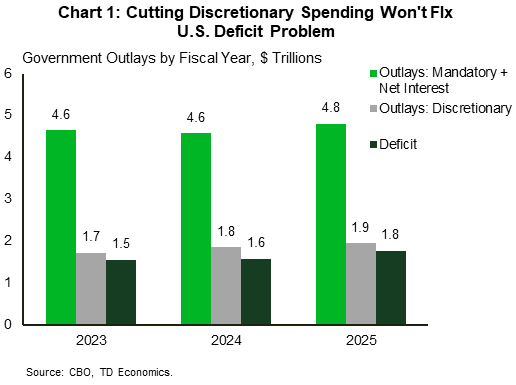

Discretionary spending accounts for only 27% of total federal government outlays, and the federal deficit is estimated to be $1.5 trillion in 2023. As shown in Chart 1, Congress would need to cut discretionary spending nearly to zero to balance the books if they only address discretionary spending. To seriously address the deficit, it needs to take the more courageous steps and look at mandatory spending – namely entitlements like social security and Medicare. Or, it needs to find a way to grow revenues at the same pace as population aging. Alas, courage seems in short supply in Congress these days.

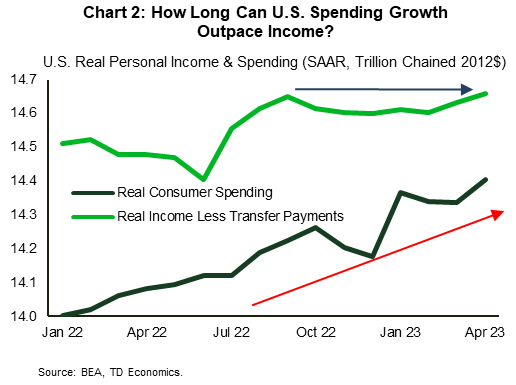

Speaking of discretion in spending, real consumer spending was up a healthy 0.5% month-on-month in April. Spending was driven by robust gains in outlays on both goods and services. Monthly spending data has been very choppy over the past six months but comparing it to real income less transfer payments (which is a key recession indicator used by the NBER), you see that the upward trend in spending is outpacing real income growth (Chart 2).

Thanks to a strong labor market, real income gains have held up. Added to the cushion of excess savings built up during the pandemic, the consumer has been able to keep spending in the face of very high inflation, in turn contributing to demand-driven inflation pressures. Chart 2 suggests that spending is set to slow – even if the labor market doesn’t cool. About 60% of the excess savings cushion has been spent, and spending cannot outgrow income indefinitely before consumers will need to tighten their belts.

We expect that belt tightening to be in greater evidence as the year goes on. After consumer spending grew by 3.8% annualized in Q1, it is tracking a more modest 2% in Q2. We expect it to fall below 1% in the second half of the year, which will help to dampen inflationary pressures. Until then, the Fed is on the horns of a dilemma.

Its preferred inflation gauge, the core PCE deflator, remained around where it has been all year at 4.7% year/year in April. Markets are judging this could mean the Fed should push a bit harder on rates, with market odds tilting slightly in favor of another hike in June. We believe that the Fed will need to hold its courage and pause and assess the impact of the significant monetary policy tightening that has not yet had its full impact on economic growth.

Canada – SEPH Adds Brushstrokes to Labour Landscape

Second quarter bank earnings and investor sentiment around the U.S. debt-ceiling negotiations were the two factors moving equity markets this week, with the TSX tracking 2% lower at the time of writing. Meanwhile, economic data was in short supply. The most important release was the Survey of Employment Payrolls and Hours (SEPH) for the month of March. Relative to the household survey, SEPH is less timely as it provides employment measures with a two-month lag and captures only payroll employees, excluding self-employed. Still, the survey is closely watched as it provides additional insights into earnings and industry-level payrolls, as well as measures of labour demand.

According to the SEPH, employment fell 10k in March, led by declines in the goods producing sector, with construction and manufacturing reporting the largest losses which were only partially offset by gains in utilities – the only industry with an increase in hiring. This is comparable with estimates reported by the household survey for the month of March. However, within the services sector, payrolls declined by 17k, while households reported growth of 35k.

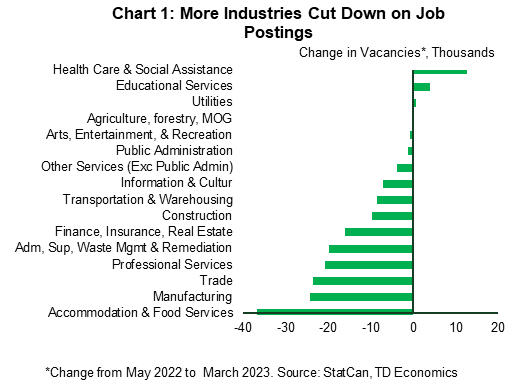

The demand side of the labour market showed marginal easing in March. The number of job vacancies was down by 17k, resulting in a cumulative contraction of 56k since the beginning of the year and 188k relative to May 2022 (when job vacancies reached their peak). Since then, the number of unfilled positions declined by more than 20k in accommodation & food services, manufacturing, trade and professional services – industries that jointly accounted for more than half of the change in labor demand (Chart 1).

The improvement in March, made no mark on the measure of labour market tightness. The ratio of jobs points to unemployed remained at 0.8 – unchanged from February. This is still much higher than an average of 0.5 vacancies per unemployed observed in 2019. Based on the current level of employment, we would need to vacancies to fall by roughly another 300k in order to restore better balance in the labour market and help normalize wage pressures.

Speaking of wages, the SEPH showed a continued deceleration in year-on-year estimates of average hourly earnings to 3.0% in March (from 4.1% in February). However, the loss in momentum is partially attributed to base effects as it's measured against a sizeable spike in March of last year, which could reverse in the following months. In addition, the more recent measure of wage growth as reported by the Labour Force Survey remains elevated at 5% – a significant divergence from the SEPH estimate (Chart 2). Evidently, the path to normalization in the job market won't feel like a downhill journey.

It sure doesn’t for small business owners. According to May's small business barometer, wage costs remain the biggest concern, with 68% of them reporting elevated labour costs as the biggest headwind businesses are facing today. With that, average wage increase plans for the next year were softer at 3.2%. All told, this week's data provides additional information on the labour market situation, but doesn't make a strong case for the BoC to come off the sidelines just yet, even if markets have started to price another 25 basis point hike next month.

Canada’s Widespread Economic Resilience Likely Slipped in March

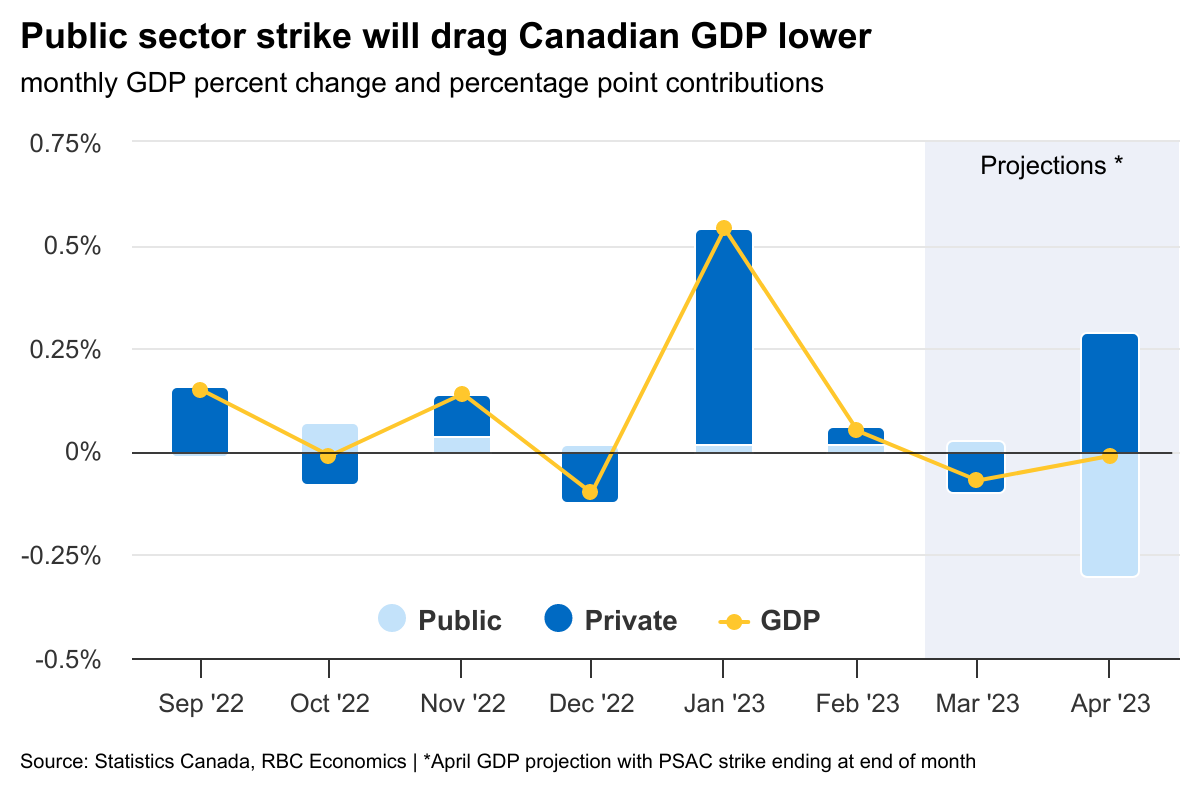

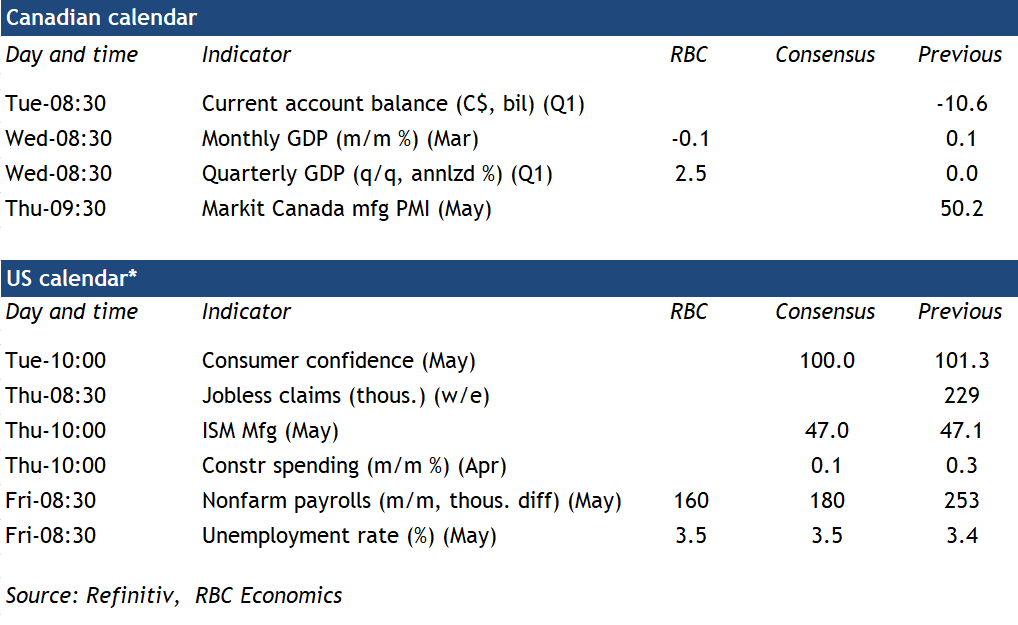

We expect next week’s Q1 GDP report to show a strong start to 2023—with real output up 2.5% on an annualized basis. Aside from a significant add from exports (thanks to a rebound in motor vehicle and parts), domestic demand was probably on the softer side. And rate-sensitive sectors continue to be squeezed by tighter monetary policy. This has had the most notable impact on residential investment, which we expect to post another significant decline. Business investment is also expected to have slowed and our own RBC cardholder data signaled softening discretionary goods-sector spending throughout the quarter. Resilience gave way in March. Monthly GDP data is likely to be broadly in line with Statistics Canada’s initial flash estimate for a 0.1% decline in March. Weakness in wholesale and retail trade and residential investment was enough to offset strength in manufacturing sales.

We anticipate another small monthly decline in April. The strike by workers with the Public Service Alliance of Canada (PSAC) is expected to shave 0.3 percentage points from April GDP. But aside from public sector weakness, activity was likely largely flat. The impact of the Bank of Canada’s aggressive rate hikes will continue to be felt with a lag as household debt servicing ratios become more burdensome. Demand is expected to weaken into Q2 as Canada enters a mild recession.

Next week’s monthly GDP release will be the final reading before the Bank of Canada’s June rate decision. An increase in headline CPI in April and four months of exceptionally strong labour market data have increased the risk of an additional hike. However, softening monthly GDP may help solidify the Bank of Canada’s present stance of staying on the sidelines (for now).

Week ahead data watch

U.S. employment numbers will likely come in weaker in May. The unemployment rate is expected to tick slightly higher but remain at historic lows. While U.S. labour markets remain exceptionally strong, early signs of a slowdown are emerging. U.S. job openings and quits are trending lower as wage growth slows.

Week Ahead – Turkey Decides, Crucial US Jobs Report, X-Date Fast Approaching

US

Wall Street is starting to get nervous as we near the X-date. A US default seemed unimaginable a couple of weeks ago and despite a lot of positive comments from both sides, negotiations will go down to the wire and that means the risk that it falls apart is growing. Treasury Secretary Yellen will soon provide an update on the X-date and that could show talks might have an extra week from the current June 1st deadline to get a deal done.

Economic data for the week will focus on the labor market, consumer confidence, and ISM manufacturing report. The US economy is expected to show job growth softened from 230K to 180K in May. Consumer confidence is expected to decline from 101.3 to 99.8 and manufacturing activity is expected to remain in contraction territory.

This week contains a handful of Fed appearances, with Barkin talking about monetary policy on Tuesday, Collins and Bowman attending a Fed Listens event on Wednesday, and Harker speaks twice, once on macroeconomic conditions, and the other time about the economic outlook. The Fed will also release its Beige Book Wednesday. A steady dose of hawkish speak along with solid job growth could make the June FOMC meeting a live one.

Eurozone

Monday is a bank holiday for some countries including Germany and France but the rest of it is filled with economic data and central bank speakers. The standouts on the economic calendar are the flash HICP data on Thursday – which follows individual country inflation numbers earlier in the week – and accounts from the last ECB meeting on the same day. Also on that day, we’ll hear from ECB President Christine Lagarde, which will arguably be more insightful, particularly in light of recent data from the US and UK which showed the economies to be resilient and inflation stubborn. Is that a concern for the ECB and are investors being too optimistic on rates?

UK

The week starts with a bank holiday and it doesn’t really pick up from there. BoE policymakers have been everywhere the last couple of weeks and it seems most are planning a week out of the spotlight which may be no bad thing. The economic data has not delivered what they wanted forcing investors to reluctantly price in four more hikes over the rest of the year. There’s no data of value next week, with the final manufacturing PMI arguably the highlight.

Russia

Unemployment is expected to tick higher to 3.6% on Wednesday, up from multi-decade lows of 3.5% and perhaps a sign of a slightly weakening labor market. The manufacturing PMI on Thursday is the only other notable release.

South Africa

A quiet week following the SARB decision on Thursday to hike rates by 50 basis points, taking the repo rate to 8.25%. This came after data on Wednesday showed inflation cooling to 6.8%, just above the 3-6% target range but the central bank warned that the risks remain to the upside.

Turkey

The run-off Presidential election on Sunday is undoubtedly the highlight of the next week. The lira hit a record low against the dollar on Friday ahead of the vote, with President Erdogan widely expected to emerge victorious after almost clinching 50% of the vote in the first round. The lira could suffer more if the result is confirmed as it means the monetary policy experiment will likely continue. A surprise victory for Kemal Kilicdaroglu could be very interesting on the open, as a potential return to normal policymaking could have a huge impact on the currency. And it would also occur in thin markets with so many countries enjoying the bank holiday break.

Switzerland

An appearance from SNB Chair, Thomas Jordan, on Wednesday will be the highlight next week but we’ll also get GDP data on Tuesday, retail sales on Wednesday and the manufacturing PMI on Thursday. An unusually busy week.

China

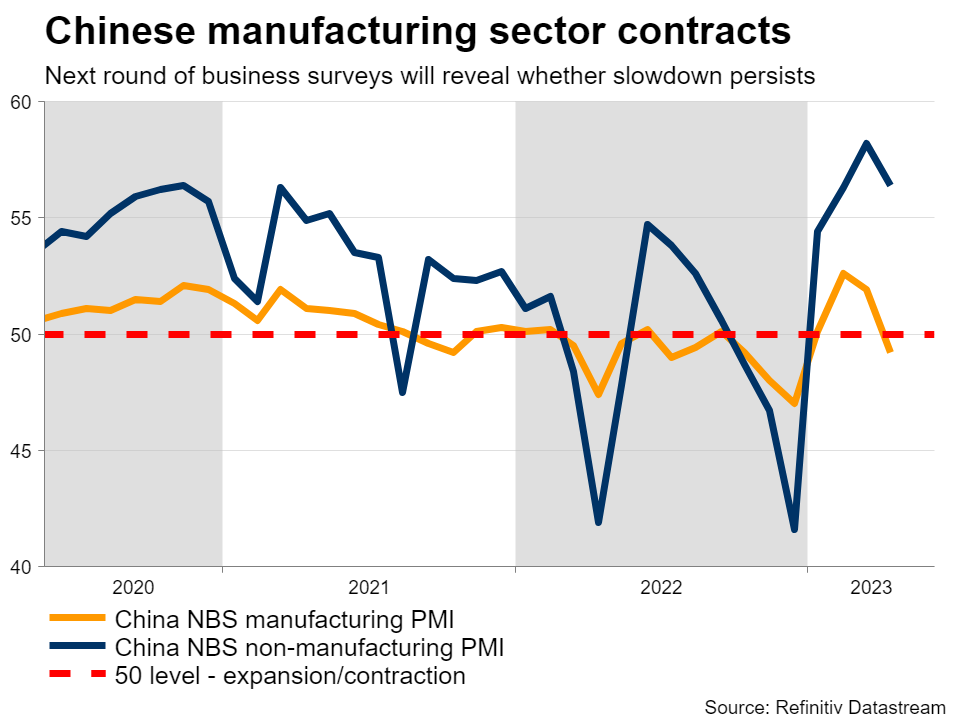

It will be a key PMI week in which the NBS manufacturing and non-manufacturing PMIs for May will be released on Wednesday. Another month of contraction is expected for manufacturing to 49.4, a slight improvement from 49.2 in April. As for services, a dip to 55 is expected from 56.4 in April.

On Thursday, we will have the release of the Caixin manufacturing PMI for May which consists of the coverage of small and medium enterprises. Another month of contraction is expected, slipping to 49.3 from 49.5 in April. If manufacturing and services are lackluster, it will provide further evidence that the growth spurt from China’s re-opening is likely to have disappeared.

India

A couple of key data to watch. Firstly, Q1 GDP on Wednesday where a 5% year-on-year growth rate is expected, above the 4.4% y/y recorded in Q4 2022.

Next up on Thursday, we will have manufacturing PMI for May, a dip in expansion is expected to 55.8 from 57.2 printed in April. If it turns out as expected, it will be the first growth slowdown after three consecutive months of growth expansion. Lastly, on Friday, bank loan growth for May will be released.

Australia

A few data releases to focus on. On Tuesday, building permits for April, 2% month-on-month growth is expected, up from -0.1% in March.

On Wednesday, we will have the monthly CPI indicator for April, which is expected at 6.3%, unchanged from March. On the same day, private sector credit growth for April will be released, with a slight dip to 6.4% from 6.8% in March, expected. If it turns out as forecasted, it will be the sixth consecutive month of a growth slowdown.

On Thursday, retail sales data for April is expected to show zero growth month-on-month from 0.4% in March.

New Zealand

Two key data releases to watch next week. Firstly, ANZ business confidence for May on Wednesday where the consensus forecast is -42 from -43.8 in April. If it turns out as forecasted, it will mark the 23rd consecutive month of negative readings.

Lastly, Q1 terms of trade, export prices, and import prices on Friday. A contraction of 1.8% quarter-on-quarter from 1.8% in Q4 2022 is expected. Export prices are expected to decline further to -2.7% quarter-on-quarter from -0.6% while a slower pace of decline is expected for import prices at -1.3% month-on-month from -2.1%.

Japan

On Monday, the unemployment rate for April is expected to improve slightly to 2.7% from 2.8% in March while April’s jobs/applications ratio is expected to hold steady at 1.32.

After an upbeat flash manufacturing and services PMI data for May, the attention for this week will be on retail sales and industrial production data for April, released on Wednesday. Retail sales are expected to record a slight dip to 7% year-on-year from 7.2% in March, while industrial production is expected to increase at a faster rate of 1.5% month-on-month, from 1.1% in March.

On Wednesday, we will have consumer confidence and housing starts. Consumer confidence for May is forecasted to improve to 36 from 35.4 in April. If it turns out as expected, it will be the 4th consecutive of improvement in consumer sentiment. Housing starts for April are expected to improve to -0.9% year-on-year from -3.2% printed in March.

Given that the Nikkei 225 has just hit a 33-year high, it will be paramount to see the amount of stock investment by foreigners and data for the week ending 27 May will be released on Thursday.

Singapore

Two key data to focus on. Firstly, the PPI for April released on Monday where is forecasted to contract further to -12% year-on-year from -11.3% in March. If it turns out as forecasted, it will mark the fourth consecutive month of contraction.

On Friday, the manufacturing PMI for May is forecasted to improve slightly to 49.9 from 49.7 in April.

Economic Calendar

Saturday, May 27

Economic Events

- The US could announce an Indo-Pacific Economic Framework, or IPEF, if trade talks are successful with Japan, India, and South Korea

Sunday, May 28

Economic Events

- Turkish presidential runoff election between incumbent Recep Tayyip Erdogan and Kemal Kilicdaroglu

- Regional and municipal elections in Spain

Monday, May 29

Economic Events

- US Memorial Day holiday. Markets and federal offices closed

- Major European markets also closed for holidays: the UK observes Summer Bank Holiday, Switzerland and Germany closed for Whit Monday

Tuesday, May 30

Economic Data/Events

- US consumer confidence

- Australia building approvals

- Czech Republic GDP

- Eurozone economic confidence, consumer confidence

- Japan unemployment

- Mexico international reserves

- New Zealand building permits

- Spain CPI

- Sweden GDP

- Switzerland GDP

- Fed’s Barkin interviewed by NABE VP/Morgan Stanley chief US economist Zentner as part of NABE monetary policy webinar series

- ECB’s Holzmann speaks at a meeting of the Austrian National Bank and the European Investment Bank

- EU-US Trade and Technology Council meets in Sweden

- Panama Canal draft limit becomes effective and will impact the travel of large ships

Wednesday, May 31

Economic Data/Events

- US job openings, Fed’s Beige Book

- Canada GDP

- China manufacturing PMI, non-manufacturing PMI

- Finland GDP

- France GDP, CPI

- Germany CPI, unemployment

- India GDP

- Italy GDP, CPI

- Japan industrial production, retail sales

- Poland CPI

- Russia unemployment, industrial production

- South Africa trade balance

- Thailand rate decision: BOT expected to raise rates by 25bps to 2.00%

- Turkey GDP

- NATO foreign ministers start a two-day meeting in Oslo

- Fed’s Harker has a fireside chat on the global macroeconomy and monetary conditions at the Official Monetary and Financial Institutions Forum in Philadelphia

- Fed’s Collins and Bowman give opening remarks at the “Fed Listens” event hosted by Boston Fed

- ECB issues financial stability review

- ECB’s Visco presents the bank’s annual report for 2022

- SNB President Jordan speaks at a monetary policy conference in Lugano, Italy

- BOE’s Mann speaks at the Pictet Family Forum “Central banks, inflation, monetary policy” in Zurich

- Hearing on Riksbank monetary policy in Swedish parliament

Thursday, June 1

Economic Data/Events

- US construction spending, initial jobless claims, ISM Manufacturing, light vehicle sales

- Tentative X-date (when the US gov’t could run out of cash to pay bills)

- China Caixin manufacturing PMI

- ECB Minutes for May 3-4th meeting

- Eurozone HCOB Eurozone manufacturing PMI, CPI, unemployment

- France HCOB France manufacturing PMI

- Germany HCOB Germany manufacturing PMI

- Hungary GDP

- India manufacturing PMI

- Italy unemployment

- Japan capital spending

- UK S&P Global / CIPS UK manufacturing PMI

- ECB President Lagarde and German Finance Minister Lindner speak at German savings banks conference

- European leaders gather at the second European Political Community meeting in Moldova

- Fed’s Harker speaks on the economic outlook at NABE’s virtual monetary policy & outlook webinar

- Sweden’s Riksbank issues report on financial stability

- BRICS foreign ministers meet in Cape Town

- DOE crude oil inventories report

Friday, June 2

Economic Data/Events

- US May Jobs Report: 180Ke v 253K prior; Unemployment Rate: 3.5%e v 3.4% prior; Average hourly earnings M/M: 0.3%e v 0.5% prior

- France industrial production

- Mexico unemployment

- Spain unemployment

- Possible UK rail strike

Sovereign Rating Updates

- United Kingdom (Fitch)

- France (S&P)

- Finland (Moody’s)

- Germany (DBRS)

- United Kingdom (Fitch)

Week Ahead – Nonfarm Payrolls Eyed as Dollar Rides Fed Bets

With investors flirting with the idea of one final Fed rate increase this summer and the dollar making a comeback, there will be increased emphasis on the next round of US employment data on Friday. Debt ceiling negotiations will also be front and center as the clock ticks down to a US government shutdown, while in Europe, there’s a batch of inflation numbers to shape the euro’s fortunes.

Dollar looks to NFP for more juice

It’s been a fantastic month for the US dollar, which smoked the competition with a little help from interest rate differentials and safe-haven flows. With incoming business surveys highlighting the resilience of the American economy, investors have started to recalibrate the Fed’s rate trajectory higher.

Markets are currently pricing in a 40% probability for the Fed to raise rates in June, which increases to 85% when looking at the July meeting. Meanwhile, the rate cuts that were baked into the cake later in the year have been mostly priced out, as concerns of an imminent recession have melted away.

However, Fed officials are split on whether further tightening is needed. Some want to raise rates again, others would rather pause, but the majority is still on the fence, preferring to examine the next round of economic data before making any decisions.

As such, there will be increased attention on the latest employment report due Friday. Forecasts suggest nonfarm payrolls rose by 180k in May, less than the previous month but still a respectable number. The unemployment rate is set to tick up to 3.5%, while wage growth is projected to accelerate slightly in yearly terms.

Nonfarm payrolls have exceeded estimates 12 times in the last 13 months, so economists seem to consistently underestimate the strength of the labor market. This phenomenon might be repeated this time, as the latest business surveys from S&P Global pointed to the fastest increase in employment growth for ten months. They also highlighted rising salary pressures.

A surprisingly strong employment report could cement expectations for one final rate increase this summer, or lead investors to further unwind rate-cut bets, keeping the wind in the dollar’s sails.

Another factor that can boost the reserve currency is a selloff in stocks that fuels safe-haven demand. Paradoxically, the catalyst for such an event might be a debt ceiling deal. After a compromise is reached, the Treasury will scramble to raise its depleted cash levels by ramping up borrowing, unleashing a tsunami of bond issuance that can drain liquidity.

Other data releases include the JOLTS job survey on Wednesday, ahead of the ADP report and the ISM manufacturing index on Thursday. Note that several markets in the US and Europe will be closed on Monday for a bank holiday.

Euro grinds lower ahead of inflation stats

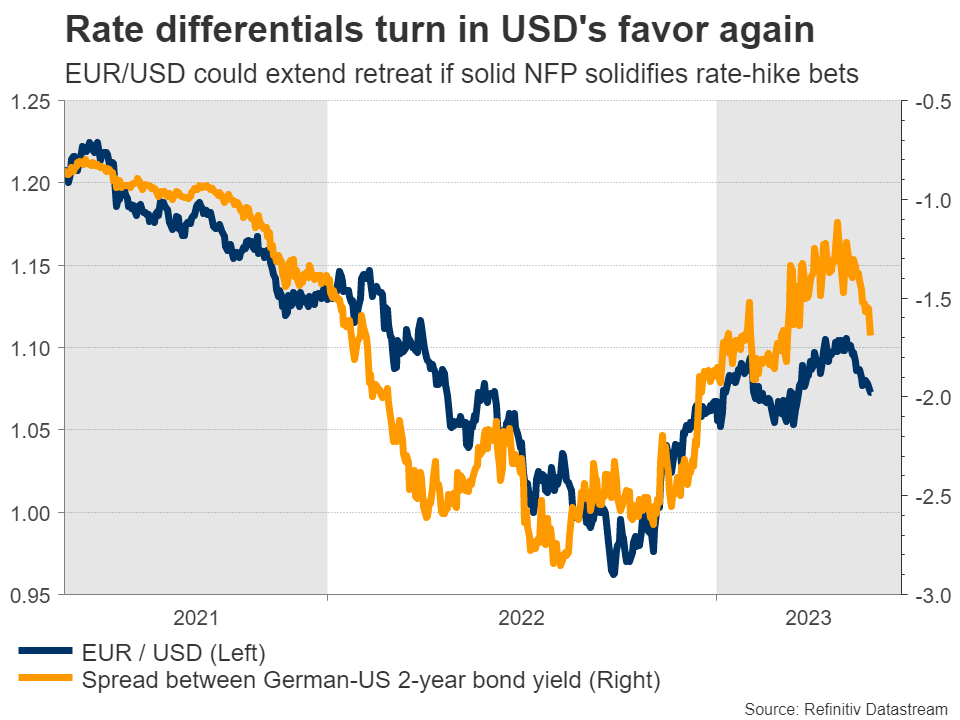

In euro land, the single currency has been under selling pressure for several weeks now. Some of that reflects the resurgent dollar, as the euro and the dollar are basically opposite sides of the same coin. However, there’s also an element of economic weakness creeping in.

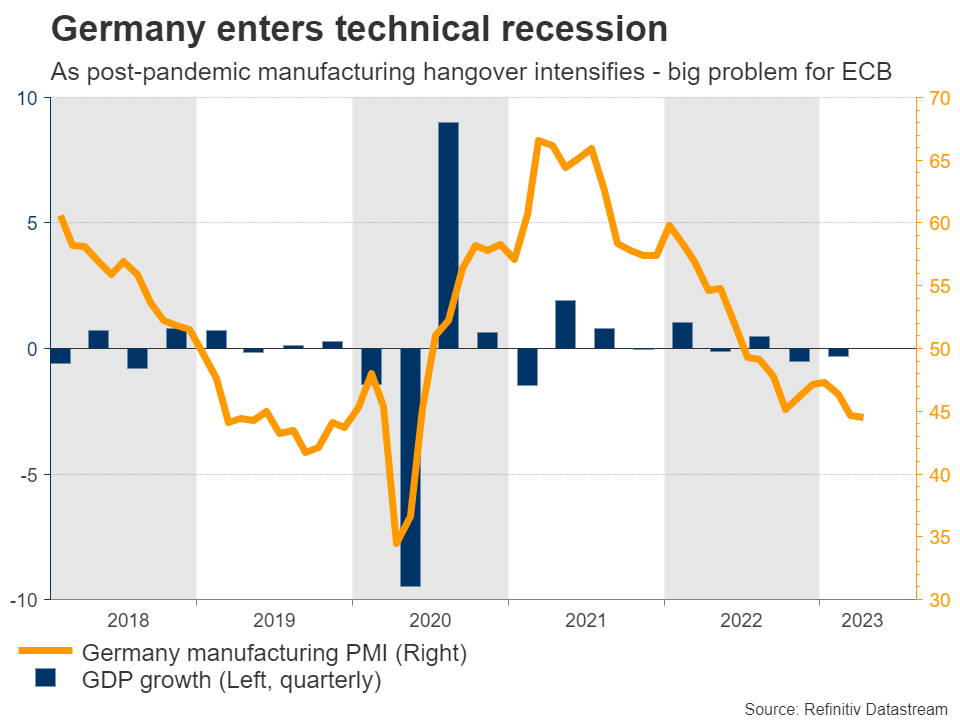

In particular, the slowdown in the manufacturing sector has intensified, dragging the bloc’s manufacturing powerhouse - Germany - into a technical recession. That’s a huge problem for the European Central Bank as economic growth seems to be rolling over but inflationary pressures remain scorching hot, leaving policymakers in a bind.

Markets are still pricing in another 60bps of ECB rate increases in the coming months, so the focus will be on incoming data, starting on Wednesday with Germany’s inflation and unemployment numbers for May. Then on Thursday, investors will get a glimpse at the same releases for the entire Eurozone, alongside the latest ECB minutes.

Forecasts point to a cooldown in inflation, something supported by business surveys where average selling prices for goods and services rose at the slowest pace in two years in May. If inflation cools significantly, some of those ECB rate-hike bets could be unwound, spelling more trouble for euro/dollar.

Chinese, Canadian, and Australian releases

Over in China, the latest PMIs will be released Wednesday. The economy has lost steam lately as the reopening boom faded, so these surveys will reveal whether this worrisome trend persisted in May. If so, the currencies of nations that depend on Chinese demand to absorb their exports - such as Australia and New Zealand - could encounter further downside.

Speaking of Australia, monthly CPI data for April is out on Wednesday, ahead of Thursday’s capex data. In Canada, GDP growth numbers for Q1 will see the light on Wednesday.

Finally in Turkey, the second round of the presidential election will be held Sunday.

Weekly Focus – A Debt Ceiling Deal in the Vicinity?

Markets' focus has been on the debt ceiling negotiations, and while time is running short, the parties seem close to reaching a deal. While risk sentiment recovered towards the end of the week, equities have generally headed lower and yields higher while USD has gained especially vis-à-vis cyclical currencies. Based on the short-end of the US T-bill curve, default worries appear to be concentrated on the first two weeks of June. The first date when the treasury cash balance is expected to decline to dangerously low levels is next Thursday, 1 June, unless Congress can agree on raising the ceiling before then.

And while the negotiations could once again go down to the wire, ultimately we do think a deal will be struck in time to avoid a default. Following the debt ceiling raise, the treasury will soon start rebuilding its cash balance, which is set to tighten USD liquidity conditions towards the latter half of the year. Even so, we see room for the Fed to continue QT into 2024, read more from FX Strategy - Time to focus on QT and USD liquidity, 24 May.

On the macro data front, May flash PMIs continued to paint a relatively upbeat picture, although a two-speed one, of the economy. Both growth and inflation pressures are driven by the services sector, with US indices signalling even accelerating growth. That said, we still expect growth to weaken towards H2, which we are also increasingly seeing in our quantitative business cycle model MacroScope: recovery stalling, 25 May.

FOMC May minutes illustrated divided views among the participants. Fed's recent commentary has highlighted that the doves, and not least Powell, prefer a more cautious stance going forward, while the hawks found it 'crucial' to underscore that cuts would not be likely this year and that further hikes could not be ruled out. Markets have almost fully priced in one more 25bp Fed hike by the July meeting and while we do not expect it to materialize, we see no room for cuts this year either.

Over the weekend, the Turkish presidential election run-off will take place between the opposition candidate Kemal Kilicdaroglu and the incumbent president Recep Tayyip Erdogan, who stands out as a favourite after nearly clinching the victory on the first round (with 49.5% of votes). We discussed Turkey, the war in Ukraine as well as US-China relations in our monthly Geopolitical radar - Spring offensive starting in Ukraine, 22 May.

Next week, the main focus besides the debt ceiling will be on the euro area flash HICP data for May, where consensus is looking for a slight moderation in core inflation pressures. On Friday, we expect to see another relative upbeat US Jobs Report. So far the signals from leading data have pointed towards healthy employment growth, which could be further supported by a renewed uptick in labour force participation. We think non-farm payrolls grew by a solid 200 thousand, and besides employment, markets will closely follow if the April uptick in average hourly earnings growth has persisted into May.

Sunset Market Commentary

Markets

It was a waiting game for a series of US April data to be released today. They didn’t disappoint, in every sense of the word. Numbers were better or higher than expected across the board, starting with durable goods orders. The headline figure rose a monthly 1.1% compared to a 1% decline penciled in by analysts. Shipments, often seen as a proxy for capital investment in GDP calculations, rose 0.5% vs 0.1% expected. Personal income rose 0.4% m/m, matching expectations but spending (0.8% m/m), including the gauge correcting for inflation (0.5% m/m), easily leaped above the bar. Turning to the main dish, PCE deflators. Headline April PCE accelerated on a 0.4% m/m pace to 4.4% y/y. Core PCE inflation also rose a monthly 0.4% to be up 4.7% compared to the same month last year. The latter since the start of the year fluctuated between 4.6% and 4.7%, suggesting a lot of price stickiness and a very wobbly, drawn-out disinflationary process. All readings, both monthly and yearly, core and headline, topped expectations by a tenth of a percent. Marginal, but telling. Core bond yields in one swipe higher erased all previous losses to the tune of 4 bps to trade a few bps in the green again. The short end of the curve again underperforms as markets now more than fully priced in a 25 bps July rate hike. The 2-y yield briefly topped the 4.60% on a >7 bps gain before paring gains to about 4 bps at the time of writing. Another nice gain as they go into a long weekend (Memorial Day on Monday). German yields were caught in the slipstream higher, wiping out declines to trade >1 bp higher. UK gilt yields take a breather going into a long weekend after an outright impressive surge up to 40 bps over the past few days. The front end sheds 4.6 bps though the very long end (30-y) still adds 1.6 bps. Retail sales in April were stronger than expected, with 0.5% m/m for the headline figure and 0.8% in the core reading (excluding auto fuel). But since they follow up on a downwardly revised March print, the net surprise is negligible.

The Swedish krone stands out on currency markets (see headline below). Taking stock of the kiwi dollar after the central bank over there unexpectedly formally finished its tightening cycle reveals a nasty 3% drop vs the USD. NZD/USD (0.606) dropped below the YtD lows yesterday and is unable to recover from that today. The US dollar recouped some of the losses it started the day with. EUR/USD ekes out a tiny gain to 1.073. The 1.0727/35 support zone is still very near. DXY hovers near but above 104(.1). Sterling is again attacking YtD closing highs around EUR/GBP 0.868 but it doesn’t look like a break is about to happen.

News & Views

Retail sales in Sweden rebounded 2.8% M/M in April, coming on the back two negative monthly readings registered in March and February. Sales in consumables increased by 1.8% M/M. Sales in durables gained 2.7%. During the February-April period sales still decreased 1.6% compared to the previous three-month period. Sales were also still 6.5% lower compared to April last year (was -10.8% in March). Yesterday, Swedish April unemployment data also were better than expected with the unemployment rate easing further from 7.7% to 7.5%. The data might be an indication that the Swedish economy is holding up better than expected. In its April monetary policy report, the Riksbank downwardly revised its forecast for 2023 household consumption from -0.6% to -1.2%. GDP growth was upwardly revised from -1.1% to a -0.7% contraction, but the was due to a better expected performance of next exports. At least for now, it is not sure whether the better April data will be enough for the Riksbank to take a more aggressive anti-inflation approach. The RB in March raised its policy rate by 0.5% to 3.50% and indicated a final 25 bps rate hike in June or September. The soft Riksbank policy approach recently weighed heavily on the Swedish currency. EUR/SEK yesterday traded at a historic low except for brief period in 2009. The currency regained some ground today with EUR/SEK declining from 11.60+ levels to currently near EUR/SEK 11.54. In this respect, Deputy governor Ana Breman this morning aired the idea of the Riksbank increasing the pace of sovereign bond sales if the koruna continues weakening. But is it a viable alternative for a (too) low policy rate?