Sample Category Title

Week Ahead – Nonfarm Payrolls Eyed as Dollar Rides Fed Bets

With investors flirting with the idea of one final Fed rate increase this summer and the dollar making a comeback, there will be increased emphasis on the next round of US employment data on Friday. Debt ceiling negotiations will also be front and center as the clock ticks down to a US government shutdown, while in Europe, there’s a batch of inflation numbers to shape the euro’s fortunes.

Dollar looks to NFP for more juice

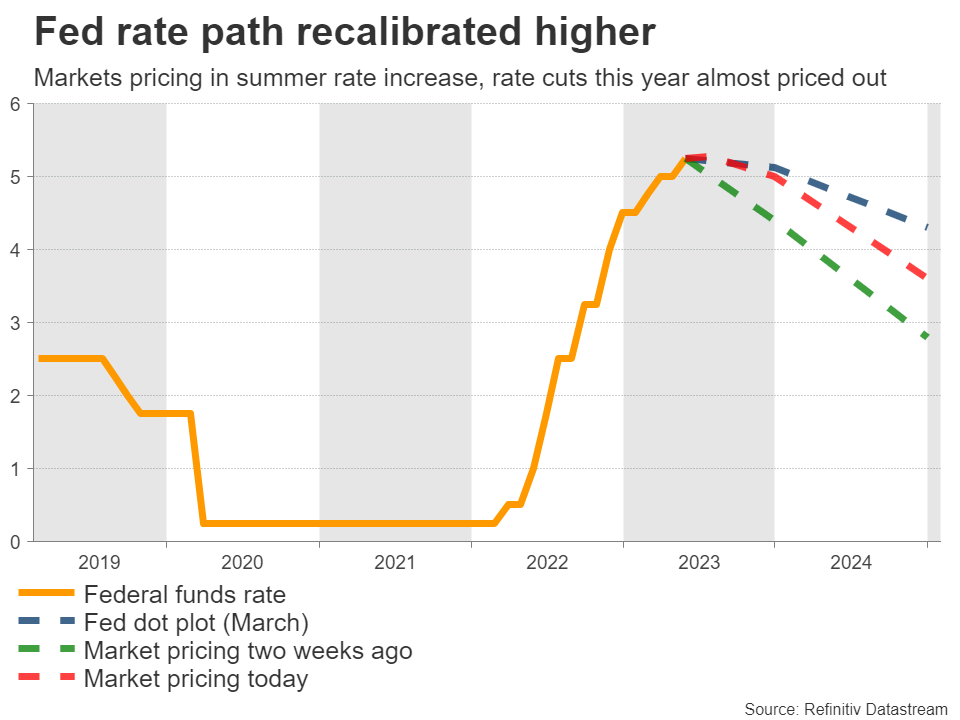

It’s been a fantastic month for the US dollar, which smoked the competition with a little help from interest rate differentials and safe-haven flows. With incoming business surveys highlighting the resilience of the American economy, investors have started to recalibrate the Fed’s rate trajectory higher.

Markets are currently pricing in a 40% probability for the Fed to raise rates in June, which increases to 85% when looking at the July meeting. Meanwhile, the rate cuts that were baked into the cake later in the year have been mostly priced out, as concerns of an imminent recession have melted away.

However, Fed officials are split on whether further tightening is needed. Some want to raise rates again, others would rather pause, but the majority is still on the fence, preferring to examine the next round of economic data before making any decisions.

As such, there will be increased attention on the latest employment report due Friday. Forecasts suggest nonfarm payrolls rose by 180k in May, less than the previous month but still a respectable number. The unemployment rate is set to tick up to 3.5%, while wage growth is projected to accelerate slightly in yearly terms.

Nonfarm payrolls have exceeded estimates 12 times in the last 13 months, so economists seem to consistently underestimate the strength of the labor market. This phenomenon might be repeated this time, as the latest business surveys from S&P Global pointed to the fastest increase in employment growth for ten months. They also highlighted rising salary pressures.

A surprisingly strong employment report could cement expectations for one final rate increase this summer, or lead investors to further unwind rate-cut bets, keeping the wind in the dollar’s sails.

Another factor that can boost the reserve currency is a selloff in stocks that fuels safe-haven demand. Paradoxically, the catalyst for such an event might be a debt ceiling deal. After a compromise is reached, the Treasury will scramble to raise its depleted cash levels by ramping up borrowing, unleashing a tsunami of bond issuance that can drain liquidity.

Other data releases include the JOLTS job survey on Wednesday, ahead of the ADP report and the ISM manufacturing index on Thursday. Note that several markets in the US and Europe will be closed on Monday for a bank holiday.

Euro grinds lower ahead of inflation stats

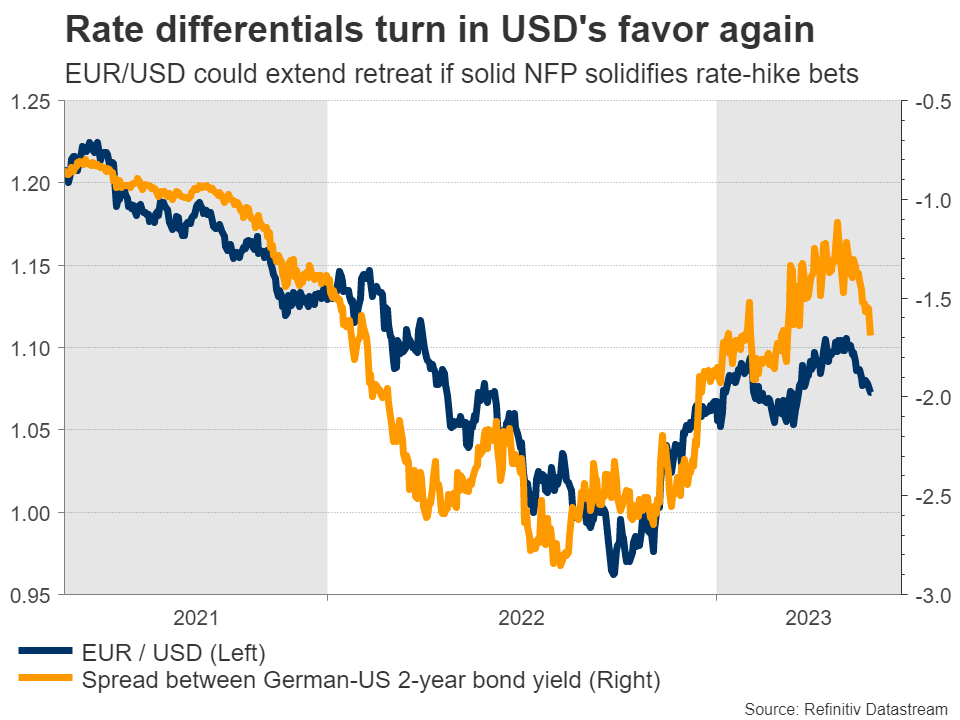

In euro land, the single currency has been under selling pressure for several weeks now. Some of that reflects the resurgent dollar, as the euro and the dollar are basically opposite sides of the same coin. However, there’s also an element of economic weakness creeping in.

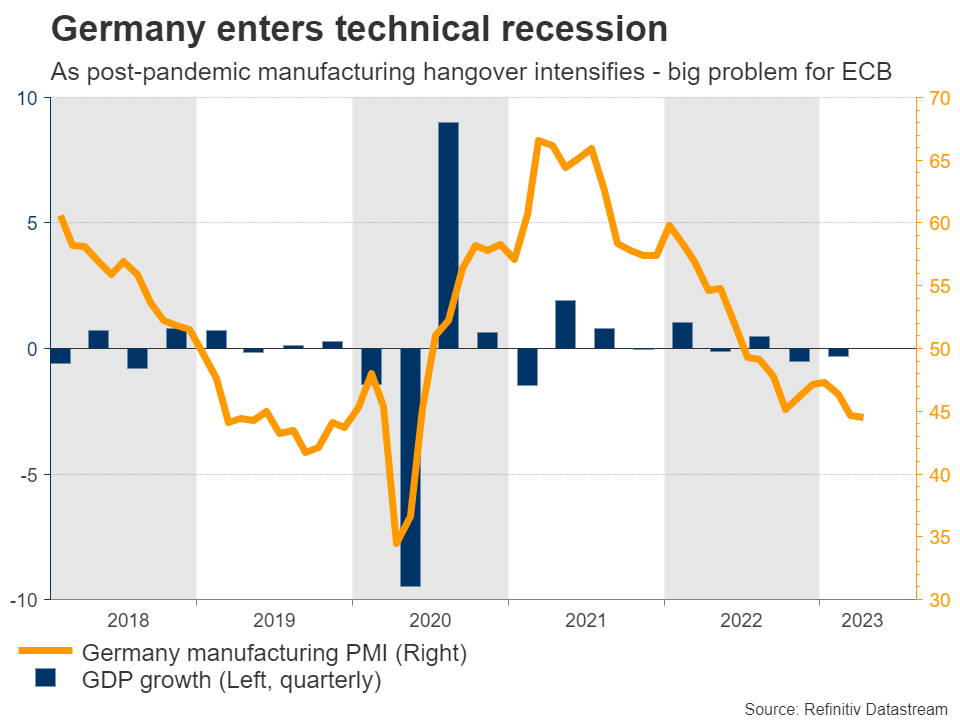

In particular, the slowdown in the manufacturing sector has intensified, dragging the bloc’s manufacturing powerhouse - Germany - into a technical recession. That’s a huge problem for the European Central Bank as economic growth seems to be rolling over but inflationary pressures remain scorching hot, leaving policymakers in a bind.

Markets are still pricing in another 60bps of ECB rate increases in the coming months, so the focus will be on incoming data, starting on Wednesday with Germany’s inflation and unemployment numbers for May. Then on Thursday, investors will get a glimpse at the same releases for the entire Eurozone, alongside the latest ECB minutes.

Forecasts point to a cooldown in inflation, something supported by business surveys where average selling prices for goods and services rose at the slowest pace in two years in May. If inflation cools significantly, some of those ECB rate-hike bets could be unwound, spelling more trouble for euro/dollar.

Chinese, Canadian, and Australian releases

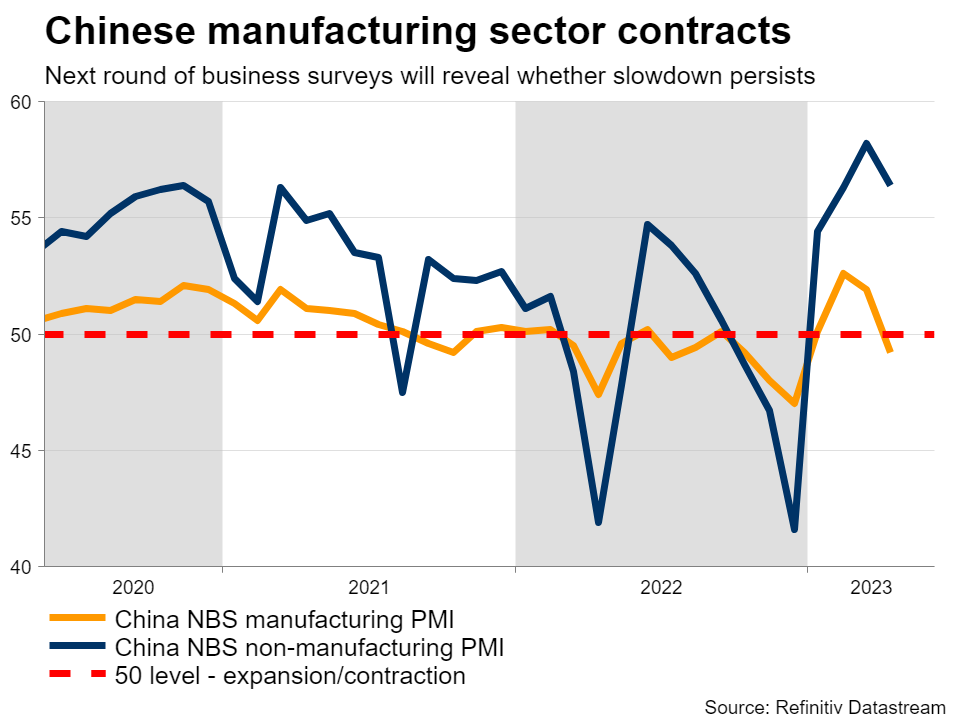

Over in China, the latest PMIs will be released Wednesday. The economy has lost steam lately as the reopening boom faded, so these surveys will reveal whether this worrisome trend persisted in May. If so, the currencies of nations that depend on Chinese demand to absorb their exports - such as Australia and New Zealand - could encounter further downside.

Speaking of Australia, monthly CPI data for April is out on Wednesday, ahead of Thursday’s capex data. In Canada, GDP growth numbers for Q1 will see the light on Wednesday.

Finally in Turkey, the second round of the presidential election will be held Sunday.

Weekly Focus – A Debt Ceiling Deal in the Vicinity?

Markets' focus has been on the debt ceiling negotiations, and while time is running short, the parties seem close to reaching a deal. While risk sentiment recovered towards the end of the week, equities have generally headed lower and yields higher while USD has gained especially vis-à-vis cyclical currencies. Based on the short-end of the US T-bill curve, default worries appear to be concentrated on the first two weeks of June. The first date when the treasury cash balance is expected to decline to dangerously low levels is next Thursday, 1 June, unless Congress can agree on raising the ceiling before then.

And while the negotiations could once again go down to the wire, ultimately we do think a deal will be struck in time to avoid a default. Following the debt ceiling raise, the treasury will soon start rebuilding its cash balance, which is set to tighten USD liquidity conditions towards the latter half of the year. Even so, we see room for the Fed to continue QT into 2024, read more from FX Strategy - Time to focus on QT and USD liquidity, 24 May.

On the macro data front, May flash PMIs continued to paint a relatively upbeat picture, although a two-speed one, of the economy. Both growth and inflation pressures are driven by the services sector, with US indices signalling even accelerating growth. That said, we still expect growth to weaken towards H2, which we are also increasingly seeing in our quantitative business cycle model MacroScope: recovery stalling, 25 May.

FOMC May minutes illustrated divided views among the participants. Fed's recent commentary has highlighted that the doves, and not least Powell, prefer a more cautious stance going forward, while the hawks found it 'crucial' to underscore that cuts would not be likely this year and that further hikes could not be ruled out. Markets have almost fully priced in one more 25bp Fed hike by the July meeting and while we do not expect it to materialize, we see no room for cuts this year either.

Over the weekend, the Turkish presidential election run-off will take place between the opposition candidate Kemal Kilicdaroglu and the incumbent president Recep Tayyip Erdogan, who stands out as a favourite after nearly clinching the victory on the first round (with 49.5% of votes). We discussed Turkey, the war in Ukraine as well as US-China relations in our monthly Geopolitical radar - Spring offensive starting in Ukraine, 22 May.

Next week, the main focus besides the debt ceiling will be on the euro area flash HICP data for May, where consensus is looking for a slight moderation in core inflation pressures. On Friday, we expect to see another relative upbeat US Jobs Report. So far the signals from leading data have pointed towards healthy employment growth, which could be further supported by a renewed uptick in labour force participation. We think non-farm payrolls grew by a solid 200 thousand, and besides employment, markets will closely follow if the April uptick in average hourly earnings growth has persisted into May.

Sunset Market Commentary

Markets

It was a waiting game for a series of US April data to be released today. They didn’t disappoint, in every sense of the word. Numbers were better or higher than expected across the board, starting with durable goods orders. The headline figure rose a monthly 1.1% compared to a 1% decline penciled in by analysts. Shipments, often seen as a proxy for capital investment in GDP calculations, rose 0.5% vs 0.1% expected. Personal income rose 0.4% m/m, matching expectations but spending (0.8% m/m), including the gauge correcting for inflation (0.5% m/m), easily leaped above the bar. Turning to the main dish, PCE deflators. Headline April PCE accelerated on a 0.4% m/m pace to 4.4% y/y. Core PCE inflation also rose a monthly 0.4% to be up 4.7% compared to the same month last year. The latter since the start of the year fluctuated between 4.6% and 4.7%, suggesting a lot of price stickiness and a very wobbly, drawn-out disinflationary process. All readings, both monthly and yearly, core and headline, topped expectations by a tenth of a percent. Marginal, but telling. Core bond yields in one swipe higher erased all previous losses to the tune of 4 bps to trade a few bps in the green again. The short end of the curve again underperforms as markets now more than fully priced in a 25 bps July rate hike. The 2-y yield briefly topped the 4.60% on a >7 bps gain before paring gains to about 4 bps at the time of writing. Another nice gain as they go into a long weekend (Memorial Day on Monday). German yields were caught in the slipstream higher, wiping out declines to trade >1 bp higher. UK gilt yields take a breather going into a long weekend after an outright impressive surge up to 40 bps over the past few days. The front end sheds 4.6 bps though the very long end (30-y) still adds 1.6 bps. Retail sales in April were stronger than expected, with 0.5% m/m for the headline figure and 0.8% in the core reading (excluding auto fuel). But since they follow up on a downwardly revised March print, the net surprise is negligible.

The Swedish krone stands out on currency markets (see headline below). Taking stock of the kiwi dollar after the central bank over there unexpectedly formally finished its tightening cycle reveals a nasty 3% drop vs the USD. NZD/USD (0.606) dropped below the YtD lows yesterday and is unable to recover from that today. The US dollar recouped some of the losses it started the day with. EUR/USD ekes out a tiny gain to 1.073. The 1.0727/35 support zone is still very near. DXY hovers near but above 104(.1). Sterling is again attacking YtD closing highs around EUR/GBP 0.868 but it doesn’t look like a break is about to happen.

News & Views

Retail sales in Sweden rebounded 2.8% M/M in April, coming on the back two negative monthly readings registered in March and February. Sales in consumables increased by 1.8% M/M. Sales in durables gained 2.7%. During the February-April period sales still decreased 1.6% compared to the previous three-month period. Sales were also still 6.5% lower compared to April last year (was -10.8% in March). Yesterday, Swedish April unemployment data also were better than expected with the unemployment rate easing further from 7.7% to 7.5%. The data might be an indication that the Swedish economy is holding up better than expected. In its April monetary policy report, the Riksbank downwardly revised its forecast for 2023 household consumption from -0.6% to -1.2%. GDP growth was upwardly revised from -1.1% to a -0.7% contraction, but the was due to a better expected performance of next exports. At least for now, it is not sure whether the better April data will be enough for the Riksbank to take a more aggressive anti-inflation approach. The RB in March raised its policy rate by 0.5% to 3.50% and indicated a final 25 bps rate hike in June or September. The soft Riksbank policy approach recently weighed heavily on the Swedish currency. EUR/SEK yesterday traded at a historic low except for brief period in 2009. The currency regained some ground today with EUR/SEK declining from 11.60+ levels to currently near EUR/SEK 11.54. In this respect, Deputy governor Ana Breman this morning aired the idea of the Riksbank increasing the pace of sovereign bond sales if the koruna continues weakening. But is it a viable alternative for a (too) low policy rate?

Another Setback for Central Banks as Inflation Remains Stubborn and Spending Strong

Investors may have underestimated the pace of disinflation this year if economic data this week is anything to go by, with US figures today further enforcing the view that price pressures are stubborn and spending healthy.

The headline PCE price index brought the biggest surprise, jumping 0.4% on the month against expectations of zero increase, but the core reading also brought an upside surprise, as did spending which jumped 0.8%, double the consensus view.

Suddenly the jobs report next week looks like the last hope for the Fed pausing its tightening cycle next month and if recent data is anything to go by, no one can be feeling particularly optimistic. The economy is showing incredible resilience and if it is turning a corner, it's doing so painfully slowly. A soft landing is becoming harder to achieve and there's an increasing risk that central banks will have to go much further and accept the economic consequences.

How sustainable is the recent trend in UK household spending?

The cost-of-living crisis in the UK is not having the dampening effect on household spending that many anticipated and today's retail sales figures showed that once more. Bad weather depressed spending in March and by more than initially thought but it rebounded last month by 0.5%, maintaining the positive trend we've seen in recent months.

Resilience in household spending has been matched by an economy that has outperformed expectations and that positive feedback loop is probably encouraging consumers to keep going. The question now is how long that can last as higher interest rates continue to filter into the broader economy, and as markets price in much higher rates later this year as a result of better activity and higher inflation.

Lira hits new lows as Erdogan expected to coast to victory on Sunday

The lira rose above 20 against the dollar for the first time ever today, just 48 hours before the public goes back to the polls. The run-off between the incumbent, Tayyip Erdoğan, and Kemal Kilicdaroglu takes place on Sunday, and based on the first-round results, the current President looks like a firm favourite.

That is why the lira has crumbled again this past week, with investors forced to accept that an Erdogan victory means years more of experimentation with monetary policy and total disregard for the consequences. A surprise on Sunday, on the other hand, could see a quite dramatic reversal on the open next week.

Oil markets volatile ahead of OPEC+ meeting next weekend

Oil prices are recovering slightly after a volatile week amid conflicting commentary from key members of the OPEC+ alliance. From a "watch out" warning from the Saudi Energy Minister to a suggestion that the group will not cut output next weekend, traders have been left a little confused as to what we can expect.

It may be that Saudi Arabia wants to keep traders on their toes but to make these comments and not follow through could be perceived as weak and see prices drift lower again. Unilateral action may not pack the same punch as a group cut, although you wouldn't put it past them.

Gold hit by stronger US inflation numbers

Gold is paring losses at the end of the week but still looks vulnerable to further declines amid more unfavourable data. The US inflation, income, and spending data were another blow, indicating more resilience in the economy and stubbornness of price pressures. It's a common theme this week and a concerning one for policymakers that hoped they could ease off the brake after a gruelling tightening campaign.

The yellow metal broke below $1,960 on Thursday, a loss of key technical support, before trying and failing to break back above today in what could be viewed as confirmation of the initial move and a bearish signal. If it does continue to drift lower, $1,940 could be an interesting level of support, with $1,900 then being a notable psychological level.

Bitcoin correction continues, albeit slowly

Bitcoin is relatively flat going into the weekend and coming under some pressure in recent days. The cryptocurrency had been in consolidation after breaking lower earlier this month but retested recent lows around $26,000 yesterday, a level it remains above currently. A move below here could see attention shift back to $25,000 around the February peak, although even this would only represent a modest correction of the 2023 rally.

US: Spending Improves, Core Inflation Ticks up in April

Personal income grew 0.4% month-on-month (m/m) in April, in line with market expectations. This marked a slight acceleration from the prior month's gain of 0.3%. Gains were led by compensation to employees, which rose 0.5% in April – up from 0.3% in March.

Subtracting inflation and taxes, real personal disposable income held flat on the month, decelerating from 0.2% in March. In year-over-year terms, real disposable income was up 3.4% in April, an acceleration from 3.3% in March.

Personal consumption rose 0.8% m/m, accelerating from the 0.1% gain in each of the two months' prior. April's gain came in above market expectations for a 0.5% reading. Goods spending rose by 1.1% m/m, while services spending rose by 0.7% m/m.

Adjusting for inflation, real spending was up 0.5% from March, coming in above the consensus estimate of 0.3%. Goods spending rose 0.8% m/m, while services were up 0.3%.

The personal consumption expenditure (PCE) price deflator rose 0.4% m/m, and 4.4% on a year-on-year (y/y) basis – slightly above the market consensus forecast (4.3% y/y) and the 4.2% y/y reading in March.

The Fed's preferred measure of inflation – core PCE – rose 0.4% m/m, which was slightly above the consensus forecast and the March reading (both at 0.3%). Our calculations of "supercore" inflation show that it was up 0.5% - an acceleration from the 0.3% gain in March. On an annual basis, core PCE inflation accelerated to 4.7% y/y from 4.6% y/y the month prior. The measure has held in the 4.6-4.7% range since December 2022.

The personal saving rate was 4.1% in April, which was 0.4%-pts below the downwardly revised 4.5% reading in March.

Key Implications

Real consumer spending grew slightly above market expectations in April, leaving behind the sluggish performance of the two months prior and starting the second quarter off on a decent note. That said, consumer sentiment has continued to trend lower in recent months, while household credit standards have also been tightening (albeit at a moderate clip). These factors are in tune with our expectations for a more moderate spending growth profile this quarter. With April's data now in the books, our tracking is for consumption growth to slow from 3.8% (annualized) at the start of the year to around 2% this quarter.

The acceleration in core PCE inflation is not what policymakers are hoping to see. While the continued persistence in inflationary pressures alongside ongoing strength in the labor market suggest the Fed should push a bit harder on rates, uncertainties surrounding the regional banking crisis and the ongoing debt ceiling negotiations are clouding the path for monetary policy. We believe that holding rates steady and assessing the impact of past rate hikes remains the most likely path forward for the Fed. That said, the probability of another hike has increased recently, with market odds as of this morning tilting slightly in favor of another 25-basis point rate hike at the Fed's next meeting in June.

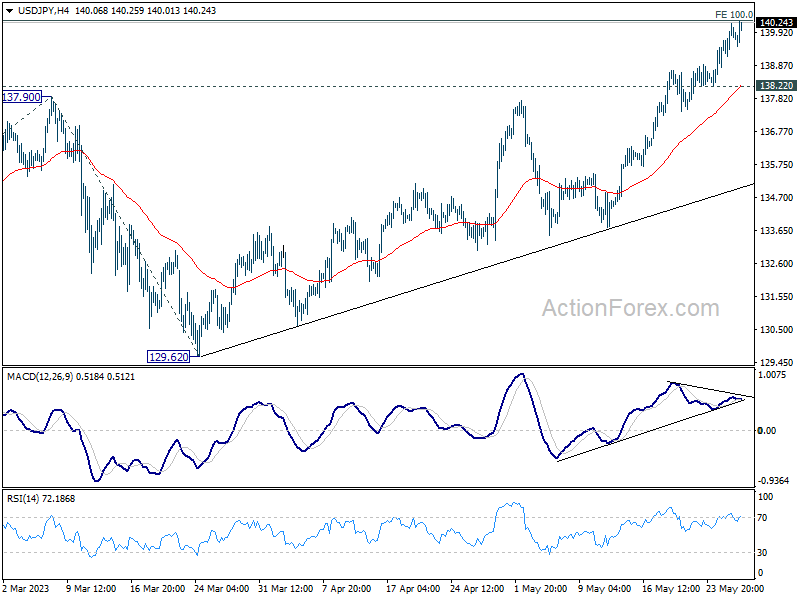

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 139.18; (P) 139.70; (R1) 140.57; More...

Focus is back on 100% projection of 127.20 to 137.90 from 129.62 at 140.32 in USD/JPY. Firm break there will extend the whole rise from 127.20 to 142.48 fibonacci level. Nevertheless, on the downside, break of 138.22 support will indicate short term topping, and turn bias back to the downside for 55 D EMA (now at 135.39).

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 136.34. Sustained break there will pave the way back to retest 151.93. On the downside, however, break of 133.73 support will argue that the pattern could have started the third leg through 127.20 low.

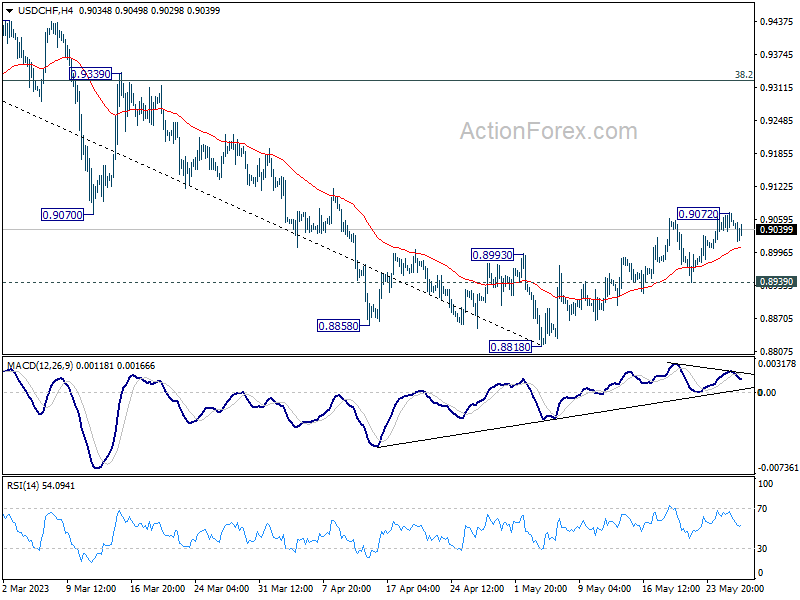

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9040; (P) 0.9056; (R1) 0.9075; More...

Intraday bias in USD/CHF remains neutral for the moment. Further rally is in favor as long as 0.8939 support holds. On the upside, sustained trading above 55 D EMA (now at 0.9039) should confirm that current rally is at least correcting whole down trend from 1.0146. Further rise should then be seen to 38.2% retracement of 1.0146 to 0.8818 at 0.9325. On the downside, though, break of 0.8939 will bring retest of 0.8818 low instead.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

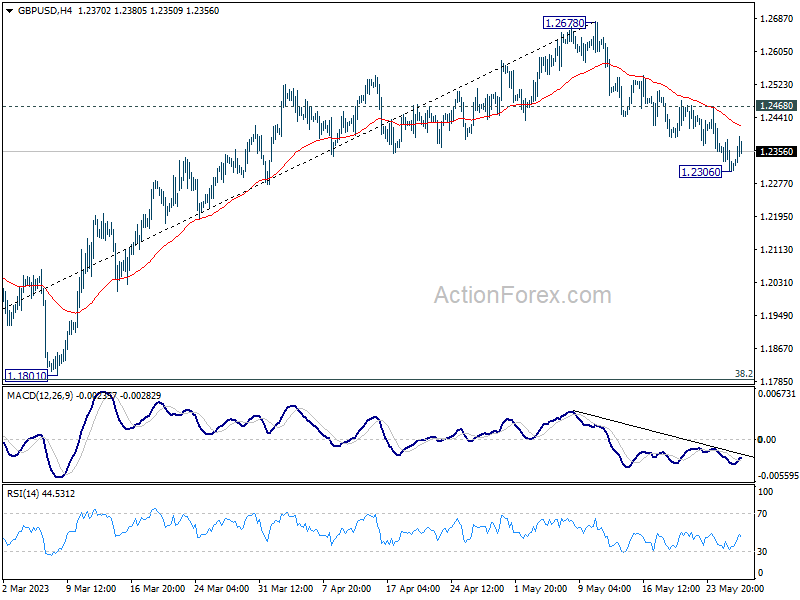

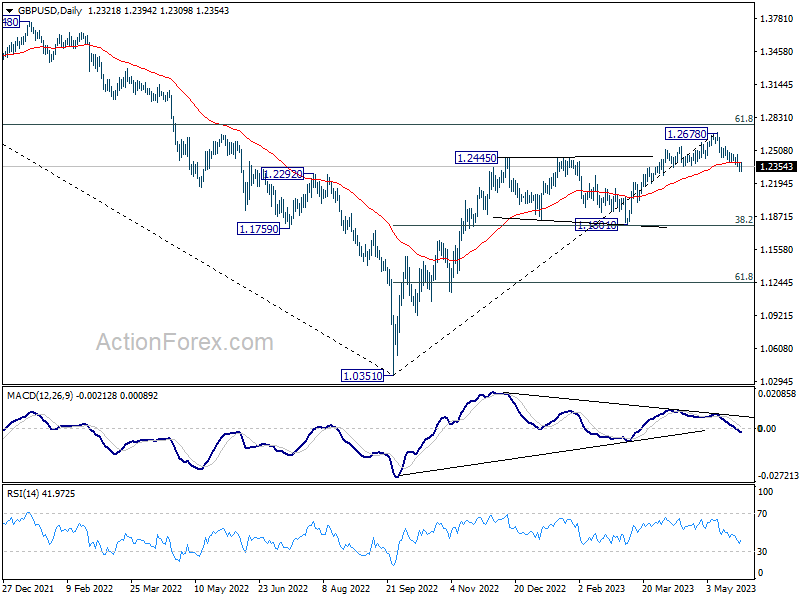

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2291; (P) 1.2339; (R1) 1.2370; More...

Intraday bias in GBP/USD is turned neutral first with current recovery. But further fall is expected as long as 1.2468 resistance holds. Decline from 1.2678 is seen as correcting whole up trend from 1.0351. Break of 1.2306 will target 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789). On the upside, above 1.2468 minor resistance will turn bias back to the upside for stronger rebound.

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

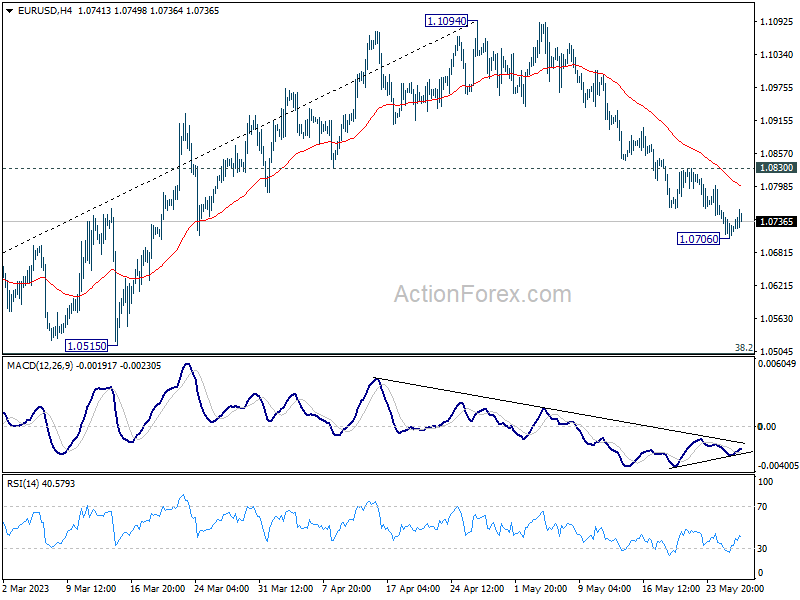

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0703; (P) 1.0730; (R1) 1.0752; More...

Intraday bias in EUR/USD is turned neutral first with current recovery, and some consolidations could be seen. But further decline is expected as long as 1.0830 resistance holds. Current fall from 1.1094 is seen as correcting whole up trend from 0.9534. Below 1.0706 will target 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, however, above 1.0830 minor resistance will turn bias to the upside for stronger rebound.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Dollar Buying Emerges Again after Inflation Data, Yen Extending Fall

While Dollar engaged in retreat for most of the day, some buying appears to emerge again in early US session. A surprising rise in both headline and core PCE inflation is considered to be a key factor driving this resurgence. While it's unsure whether that could result in sustainable rally, the sentiment should stabilize the greenback at least.

Meanwhile, selloff in Yen is taking off again, following rally in US and European benchmark yields, with US 10-year yield breaking 3.8% level in pre-market. The current tone in the markets will likely keep the greenback as the best performer for the week. New Zealand and Australian Dollars will end as the worst, with Yen a distant third. Euro, Sterling, and Swiss Franc are basically still bounded in range against each other.

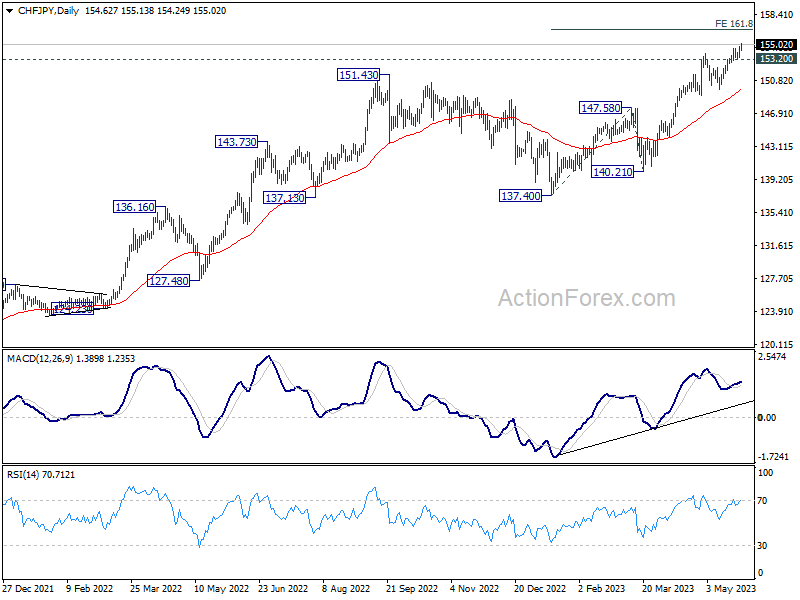

Technically, CHF/JPY's rally resumes today and hits as high as 155.13 so far. Near term outlook will stay bullish as long as 153.20 support holds. Next target is 161.8% projection of 137.40 to 147.58 from 140.21 at 156.68. GBP/JPY is also extending recent up trend and breaks above 173 handle. It's a question now whether the development is enough to take EUR/JPY through 151.60 resistance.

In Europe, at the time of writing, FTSE is up 0.24%. DAX is up 0.33%. CAC is up 0.44%. Germany 10-year yield is up 0.005 at 2.529. Earlier in Asia, Nikkei rose 0.37%. Hong Kong HSI dropped -1.93%. China Shanghai SSE rose 0.35%. Singapore Strait Times dropped -0.01%. Japan 10-year JGB yield dropped -0.0078 to 0.422.

US PCE rose to 4.4% yoy, core PCE up to 4.7% yoy

US personal income rose 0.4% mom or USD 80.1B in April, matched expectations. Personal spending rose 0.8% mom or USD 151.7B, above expectation of 0.4% mom.

For the month, PCE price index rose 0.4% mom. Core PCE price index (excluding food and energy) rose 0.4% mom. Goods prices increased 0.3% mom while services prices increased 0.4% mom. Food prices decreased less than -0.1% mom. Energy prices rose 0.7% mom.

From the same month one year ago, headline PCE price index rose from 4.2% yoy to 4.4% yoy, above expectation of 3.9% yoy. Core PCE price index also ticked up from 4.6% yoy to 4.7% yoy, above expectation of 4.6% yoy. Prices for goods were up 2.1% yoy and prices for services were up 5.5% yoy. Foods prices increased 6.9% yoy. Energy prices decreased -6.3% yoy.

Also released, durable goods orders rose 1.1% mom in April versus expectation of -0.9% mom. Ex-transport orders dropped -0.2% mom versus expectation of 0.0%. Goods trade deficit widened to USD -96.8B, versus expectation of USD -85.6B.

ECB Lane: Reversal of energy prices will feed into lower core

ECB Chief Economist Philip Lane has asserted that falling energy prices could lead to lower core inflation due to reduced living costs and, consequently, restrained wage increases. However, he stressed the timeline and extent of this effect remain uncertain.

Speaking at a conference in Dubrovnik, Lane said, "I don't think it's symmetric... but when energy prices fall, core inflation does follow, because there is less pressure from an energy cost, there's less pressure on the cost of living, therefore on nominal wage increases

"So, we do think this spectacular reversal of energy prices will feed into lower core, but the timeline for that and the scale of it is uncertain," he added.

Lane further observed that wage growth is generally progressing at a moderate pace, with many people still bound to older contracts. "The latest deals are coming in at above 5%, but (this is in the) ballpark of what we expect," he noted.

Despite this, he expects nominal wage growth to peak this year and suggested it would take real wages until 2025 to recover back to their 2019 level.

UK retail sales volume up 0.5% mom in Apr, value up 1.1% mom

UK retail sales volumes rose 0.5% mom in April, well above expectation of 0.0% mom. Excluding automotive fuel, sales volume rose 0.8% mom. Sales value rose 1.1% mom in the month, with ex-automotive fuel sales value up 1.7% mom.

In the three months to April, sales volumes rose 0.8% 3mo3m, the highest rates since August 2021, which was at 1.3% 3mo3m.

RBNZ Silk warns against premature rate cut expectations

RBNZ Assistant Governor Karen Silk advised caution against pricing in rate cuts too prematurely. In her comments, Silk stressed that RBNZ has reached a juncture where it can "take a pause and watch how this evolves," ensuring that "you don't overdo things."

However, Silk emphasized that it's core inflation that the central bank is focused on bringing down, and this will require maintaining the current rate levels for an extended period. "We've said we need to hold for an extended period of time to ensure core inflation comes down; it's core inflation that we need to get down," she stated.

She explained the bank's holistic approach to assessing economic conditions, saying, "We look at economic data, but we also look at transmission," Silk explained. "If at a wholesale level and most importantly at a retail level we start to see those things come off faster, then that's one of the things we take into account when we think about where we set the OCR."

In terms of the inflationary impact of Cyclone Gabrielle, Silk indicated that its effect has been less severe than initially anticipated. RBNZ had initially projected the storm would add 0.3% to inflation in both the first and second quarters. Still, it has since revised this down to just 0.1%, citing that while the storm led to increased food costs, it didn't inflate the prices of other goods such as used cars.

Australia retail sales flat in Apr, cost-of-living pressures and rising interest rates

Australia retail sales turnover was flat at 0% mom in April, and up 4.2% yoy.

"Retail turnover has plateaued over the last six months as consumers spent less on discretionary goods in response to cost-of-living pressures and rising interest rates. Spending was again soft in April but was boosted by increased spending on winter clothing in response to cooler and wetter than average weather across the country," Ben Dorber, ABS head of retail statistics said.

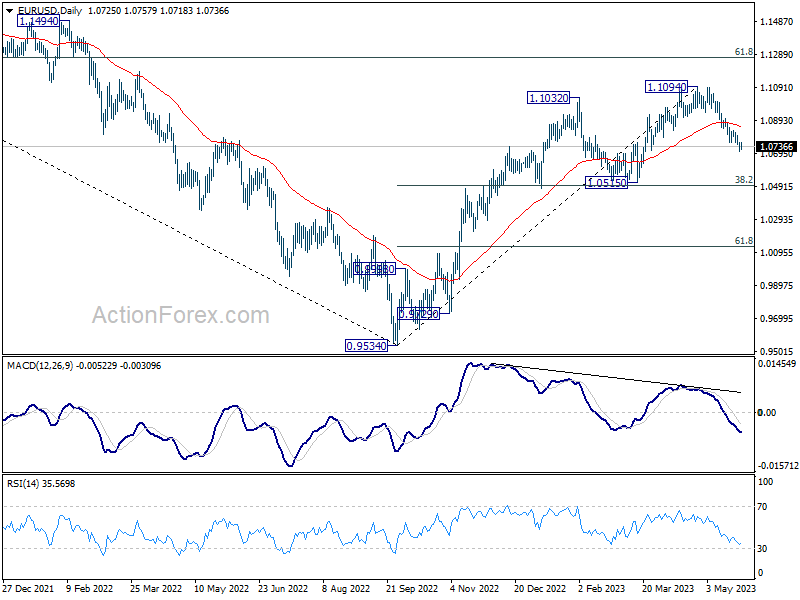

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0703; (P) 1.0730; (R1) 1.0752; More...

Intraday bias in EUR/USD is turned neutral first with current recovery, and some consolidations could be seen. But further decline is expected as long as 1.0830 resistance holds. Current fall from 1.1094 is seen as correcting whole up trend from 0.9534. Below 1.0706 will target 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, however, above 1.0830 minor resistance will turn bias to the upside for stronger rebound.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y May | 3.20% | 3.40% | 3.50% | |

| 23:50 | JPY | Corporate Service Price Index Y/Y Apr | 1.60% | 1.40% | 1.60% | 1.70% |

| 01:30 | AUD | Retail Sales M/M Apr | 0.00% | 0.30% | 0.40% | |

| 06:00 | GBP | Retail Sales M/M Apr | 0.50% | 0.00% | -0.90% | |

| 12:30 | USD | Durable Goods Orders Apr | 1.10% | -0.90% | 3.20% | 3.30% |

| 12:30 | USD | Durable Goods Orders ex Transportation Apr | -0.20% | 0.00% | 0.20% | |

| 12:30 | USD | Personal Income M/M Apr | 0.40% | 0.40% | 0.30% | |

| 12:30 | USD | Personal Spending M/M Apr | 0.80% | 0.40% | 0.00% | 0.10% |

| 12:30 | USD | PCE Price Index M/M Apr | 0.40% | 0.40% | 0.10% | |

| 12:30 | USD | PCE Price Index Y/Y Apr | 4.40% | 3.90% | 4.20% | |

| 12:30 | USD | Core PCE Price Index M/M Apr | 0.40% | 0.40% | 0.30% | |

| 12:30 | USD | Core PCE Price Index Y/Y Apr | 4.70% | 4.60% | 4.60% | |

| 12:30 | USD | Goods Trade Balance (USD) Apr P | -96.8B | -85.6B | -84.6B | -82.7B |

| 12:30 | USD | Wholesale Inventories Apr P | -0.20% | 0.10% | 0.00% | |

| 14:00 | USD | Michigan Consumer Sentiment Index May F | 58.2 | 57.7 |