Sample Category Title

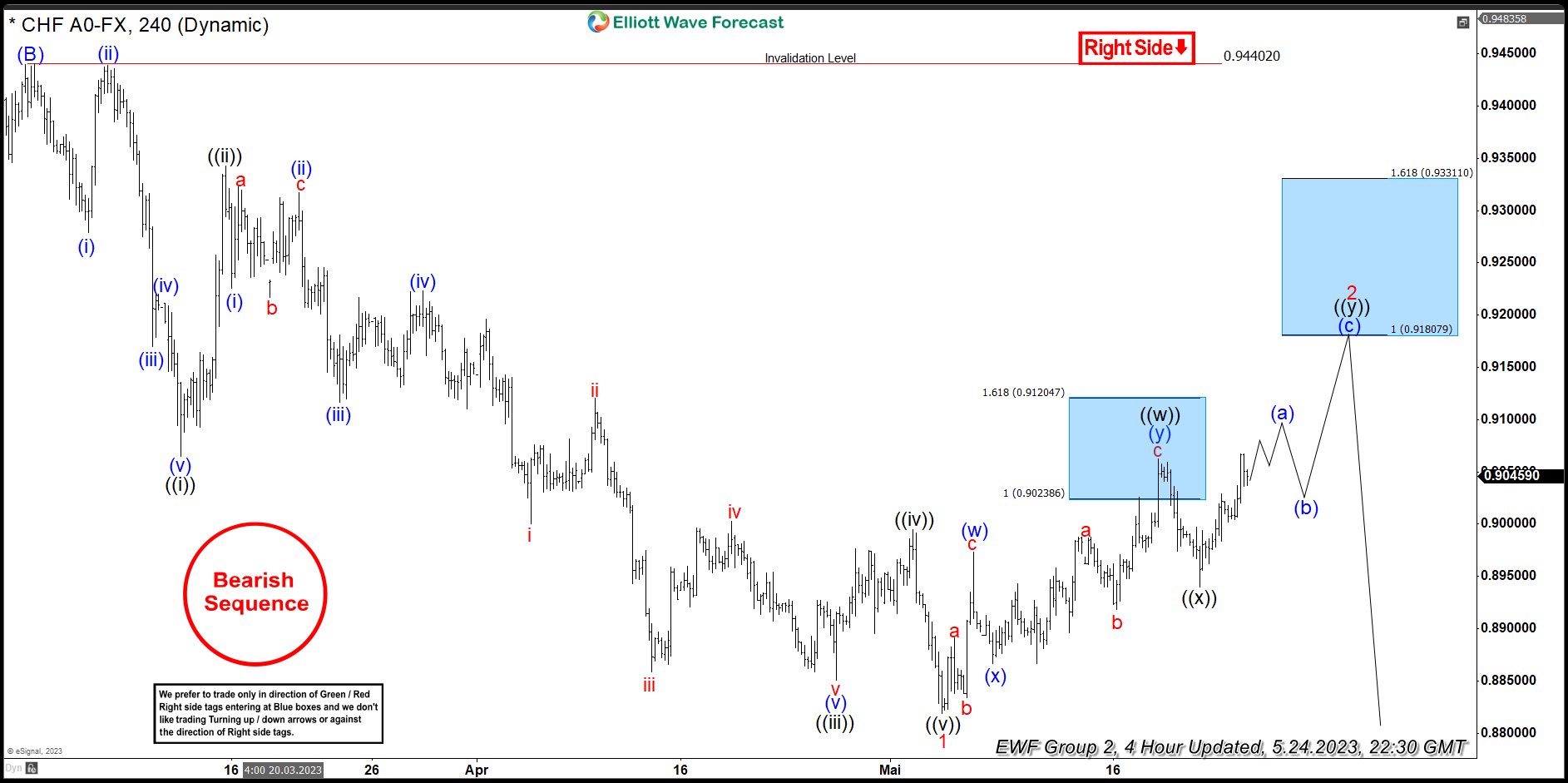

USDCHF Double Three Elliott Wave Advance and Next Blue Box Area

In our recent article about USDCHF, we explained incomplete bearish sequence in USDCHF since October 2022 and December 2016 highs and explained that bounces should fail in 3, 7 or 11 swings for extension lower. Pair found sellers after three waves in the first blue box area and reacted lower to allow any sellers to eliminate risk on their shorts. However, pair failed to break below 05.04.2023 low and has now broken above the previous peak within the blue box which was reached on 05.18.2023. Let’s take a look at the current structure and the next extreme in today’s article.

USDCHF 4 Hour Elliott Wave Chart – 05.24.2023

Chart above shows USDCHF cycle from 03.02.2023 ended as an impulsive Elliott wave structure and pair is now bouncing to correct the decline from 03.02.2023 peak at 0.94404. Pair completed a cycle from 05.04.2023 low (0.8819) at 05.18.2023 high (0.9062) and turned lower after sellers appeared in the blue box area between 0.9023 – 0.9120. Pair dropped from 0.9062 to 0.8940 (05.22.2023) which allowed sellers from blue box to eliminate risk on their shorts. However, it failed to get more downward momentum and didn’t manage to break below 05.04.2023 low. Instead the pair continue higher and it has now broken above 05.18.2023 (0.9062) high and has created yet another short-term incomplete sequence to the upside.

Near-term, expect some more upside toward 0.9087 – 0.9123 to complete the cycle from 05.22.2023 low i.e. black (( x )) before it pulls back to correct this cycle and turns higher again toward 0.9180 – 0.9331 to complete the larger double three structure since 05.04.2023 low. Area between 0.9180 – 0.9331 highlights the next extreme and the blue box area where we expect sellers to appear to resume the decline toward the double extreme area on the weekly chart between 0.8563 – 0.8189 or produce a reaction lower in three waves at least to allow sellers to get into a risk free position. like it did from the previous blue box area between 0.9023 – 0.9120.

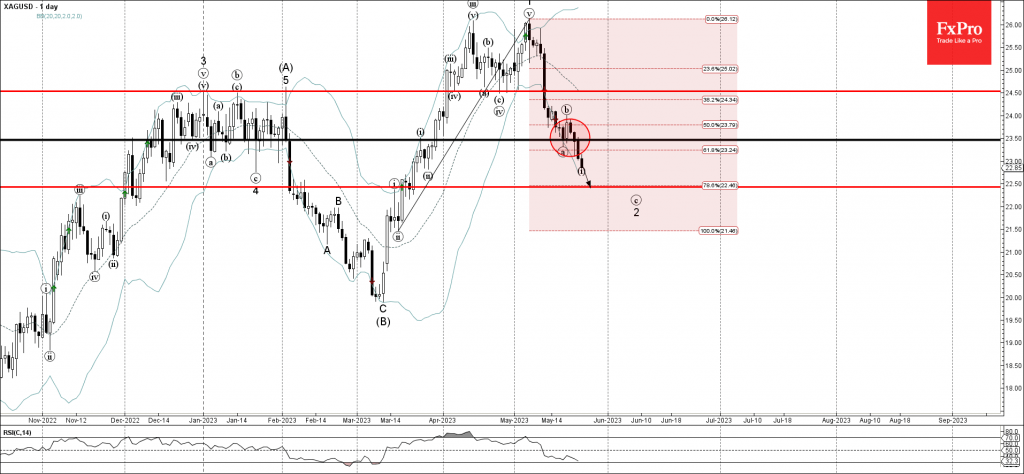

Silver Wave Analysis

- Silver broke support level 23.50

- Likely to fall to support level 22.50

Silver under the bearish pressure after the price broke the support level 23.50 (which stopped wave (a) earlier this month), nearly coinciding with the 61.8% Fibonacci correction of the previous sharp upward impulse from March.

The breakout of the support level 23.50 strengthened the bearish pressure on Silver – accelerating the active waves 2 and (c).

Silver can be expected to fall further toward the next support level 22.50 (target price for the completion of the active sharp downward ABC correction 2).

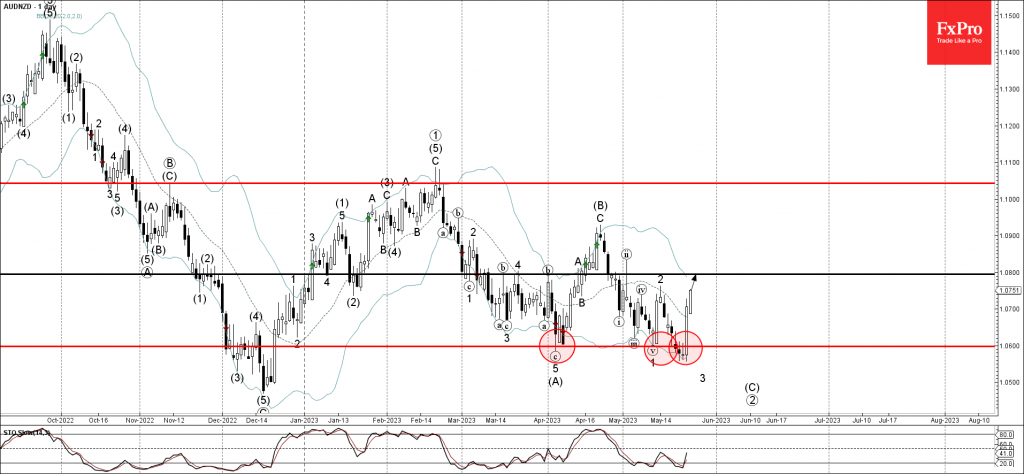

AUDNZD Wave Analysis

- AUDNZD reversed from key support level 1.0600

- Likely to rise to resistance level 1.0800

AUDNZD continues to rise after the earlier sharp upward reversal from the key support level 1.0600 (former low of wave (A) from the start of April), intersecting with the lower daily Bollinger Band.

The upward reversal from the support level 1.0600 stopped the previous impulse waves 3 and (C).

Given the strongly bearish NZD sentiment seen today, AUDNZD can be expected to rise further toward the next resistance level 1.0800.

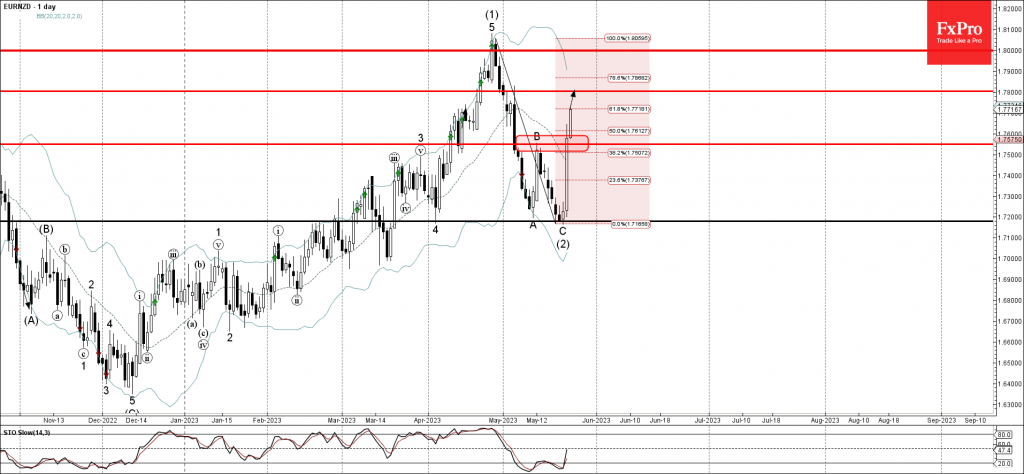

EURNZD Wave Analysis

- EURNZD broke resistance level 1.7550

- Likely to rise to resistance level 1.7800

EURNZD continues to rise after the earlier breakout of the resistance level 1.7550 (top of the previous correction B), intersecting with the 38.2% Fibonacci correction of the ABC correction (2) from April).

The breakout of the resistance level l 1.7550 accelerated the active intermediate impulse wave (3).

Given the overriding daily uptrend, EURNZD can be expected to rise further toward the next resistance level 1.7800.

Sunset Market Commentary

Markets

UK gilt yields one again caught the attention today. They initially add another 6.5-10 bps following yesterday’s ugly CPI surprise which will almost certainly force the Bank of England into additional tightening. This time though, the long end of the curve joined the short end, which could mean markets have taken a less pessimistic view on the growth implications of a tighter monetary policy. Tomorrow’s UK retail sales are to give a glimpse on the resilience of the UK consumer. Is this the trigger sterling is waiting for to push beyond the current YtD highs (EUR/GBP today down to 0.868, near recent lows)? The whole curve in any case is now close to the levels seen in the aftermath of Truss & Kwarteng’s disastrous minibudget September last year. Another slew of central bank governors hit the wires. ECB VP de Guindos said wages and profits pose upside inflation risks. Nagel put it bluntly and said more tightening is needed to overcome high inflation. French governor Villeroy, typically holding a more centrist view, said policy rates should peak in the next three meetings. Assuming action on all three, that implies a 4% rate. He also noted that it may take monetary policy longer to hit the economy than we were used to in the past. Said otherwise: rates need to be restrictive for a long enough period. Despite the overall hawkish tone, the speeches failed to really inspire German yields (+2 bps at the front). US rates fluctuated within a tight range before a series of better-than-expected data shook things up. We’re talking about the Chicago Fed Activity Index, weekly and continuing jobless claims and the second reading of US Q1 GDP. Very much second-tier indeed and that makes the sharp yield jump so telling. The curve inversion deepens with the short end surging 8.5 bps after trading 2 bps or so in the red earlier. The 2y briefly ventured north of 4.5% before paring gains a bit. Markets are more and more convinced the Fed will have to hike a bit more (at one point a July hike was fully discounted) while further pushing back the timing of rate cuts. The dollar embraces the juicy interest rate support but a solid equity performance caps its gains (Nasdaq up 1.3%). DXY extends gains to 104.16, extensively testing the 104.089 resistance (23.6% recovery of the DXY 2022-2023 decline). EUR/USD currently loses the critical 1.0727 (23.6% retracement of the 2022-2023 rally) - 1.0735 (December 2022 interim high) support. In other US news, rating agency DBRS Morningstar followed Fitch in putting its triple A US-rating on review for a downgrade.

News & Views

The Central Bank of Turkey (CBRT) as expected kept its policy rate unchanged at 8.5%. It said that economic activity in the earthquake zone has been recovering faster than expected and that it will not have a permanent impact in the medium term. The CBRT sees a stronger than expected positive contribution of tourism supporting the current account balance, even as an ongoing increase in domestic demand, high energy prices and weaker external activity remain risks to the external balance. Still a sustainable current account balance remains important for price stability. The MPC will continue to use tools supporting the effectiveness of monetary policy, with Liraization strategy an important part of this policy. The MPC will continue to prioritize the creation of supportive financial conditions in order to minimize the effects of the disaster and support the necessary recovery. The CBRT takes notice of recent improvement in the trend of inflation and still aims to reach the 5% inflation target over the medium term. The implementation of the Liraization strategy (including reversal in currency substitution and an uptrend in FX reserves) are also important to reach this goal. Still inflation and core inflation were 43.68% and 45.48% respectively in April. The lira today remained in the defensive against the dollar with the EUR/TRY cross rate nearing the 20 mark (currently 19.93) as markets are counting down to the second round of the presidential election.

The monthly index of report sales in retailing from the Confederation of British industry indicated a decline in retail sales in May. The index declined from + 5 in April to -10 in May. The orders placed index also declined from 1 to -30. Sales for the time of the year also deteriorated from 21 to -18. However, the indicator for expected sales improved slightly from -7 to 0. According to CBI a future improvement might be supported by an improvement in consumer confidence and a decline in energy prices. According to the May quarterly survey, reported selling prices remain elevated (77 from 80) while both reported (-48 from -12) and expected employment (-49 from -16) in retailing declined sharply. Tomorrow morning, the official ONS April UK retail sales will be published.

GBP/USD Edges Lower, Markets Eye UK Retail Sales

- UK retail sales expected to fall sharply

- US debt ceiling impasse continues

- FOMC minutes show Fed divided over rate policy

GBP/USD continues its downswing. The pound is trading at 1.2340, down 0.20% and is at a one-month low against the US dollar.

The UK releases retail sales for April on Friday. On an annualized basis, the headline and core readings are expected to decline by 2.8% in April, which would indicate that UK consumers continue to hold tight onto the purse strings. Consumers are having a tough time with the cost of living crisis, with inflation at 8.3% and a weak reading could weigh on the pound.

US debt ceiling still unresolved

The US debt ceiling impasse remains unresolved, with the White House warning that the US could default on its debt on June 1st if no deal is reached in Congress. The markets are jittery and US 10-year Treasury yields have jumped to 3.75, up 1.1% today. The US dollar has also benefited from the debt ceiling crisis as investors have snapped up safe-haven assets. On Wednesday, Fitch Ratings put the top-ranked United States sovereign credit rating on “rating watch negative” due to the danger of a US debt ceiling default and we can expect market risk sentiment to continue falling as we move closer to June without a deal in place.

Fed uncertain about rate outlook

The FOMC minutes indicated that the Fed remains unclear over future rate policy. At the May meeting, some members said there was a need for further increases as inflation was not falling fast enough. Other members argued that the economy was cooling and there was no need for more tightening. All the members agreed that inflation remains too high and the vote to raise rates by 25 basis points at the May meeting was unanimous.

So what’s next? The Fed meets on June 14th and appears to be leaning towards a pause in rate increases. The odds of a pause are currently 62%, versus 37% for a 25-bp hike, according to CME’s FedWatch. Just a month ago, the probabilities were 70% for a pause, 8% for a 25-bp hike and 22% chance for a rate cut of 25 basis points. A hawkish Fed and solid US data have put to rest market speculation of a rate cut next month.

Speaking of solid economic data, US Preliminary GDP rose 1.3% y/y in the first quarter, up from 1.3% in Q4 2020, which was also the estimate. On a quarterly basis, GDP climbed 4.2%, above the estimate of 4.0% and after a Q4 gain of 4.0%. Unemployment claims rose to 229,000, following a previous reading of 225,000, which was downwardly revised from 242,000. This easily beat the estimate of 245,000. The Fed will not be thrilled with these numbers, as it needs the economy to cool in order to wrap up the current rate-tightening cycle.

GBP/USD Technical

- GBP/USD tested support at 1.2375 in the European session. Below, there is support at 1.2307

- 1.2461 and 1.2529 are the next resistance levels

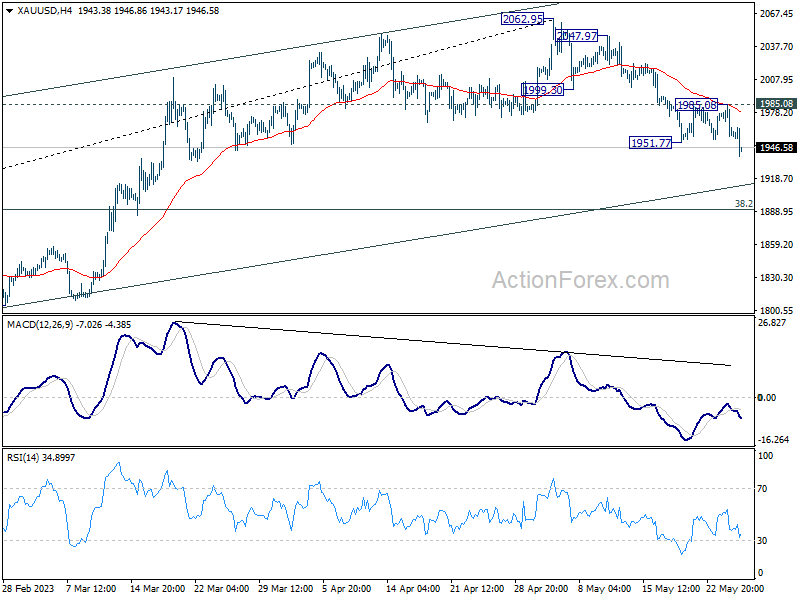

Dollar Power Continues, Gold Resumes Near Term Fall

Dollar continues to be the strongest one for the week and sees fresh buying in early US session. Republican House Speaker Kevin McCarthy noted the debt ceiling negotiations have made some progress. But that was largely ignored by stock investors, even through treasury yields are on the rise. As for today, Canadian Dollar and Swiss France are currently the next strongest, just because they're facing less selling pressure. Kiwi, Aussie and Euro are the worst together with Euro.

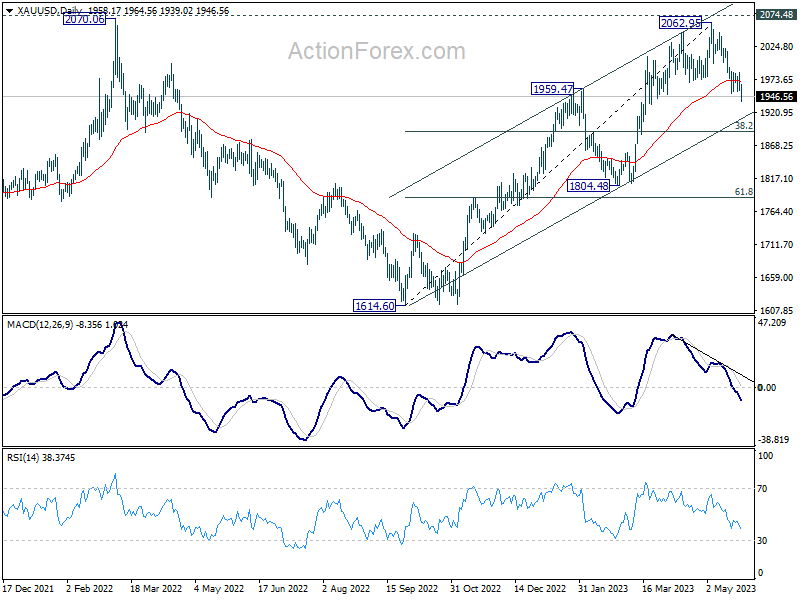

Technically, Gold's decline from 2062.95 resumed by breaking through 1951.77 support today. Further fall is now expected as long as 1985.08 resistance holds. There might be some support between 38.2% retracement of 1614.60 to 2062.95 at 1891.68, and channel support at around 1913 to contain downside. That is, 1900 is a key hurdle for the down trend to overcome. However, firm break of this support zone could easily push gold towards 1800 handle.

In Europe, at the time of writing, FTSE is down -0.17%. DAX is up 0.05%. CAC is down -0.05%. Germany 10-year yield is up 0.007 at 2.480. Earlier in Asia, Nikkei rose 0.39%. Hong Kong HSI dropped -1.93%. China Shanghai SSE dropped -0.11%. Singapore Strait Times dropped -0.20%. Japan 10-year JGB yield rose 0.0215 to 0.430.

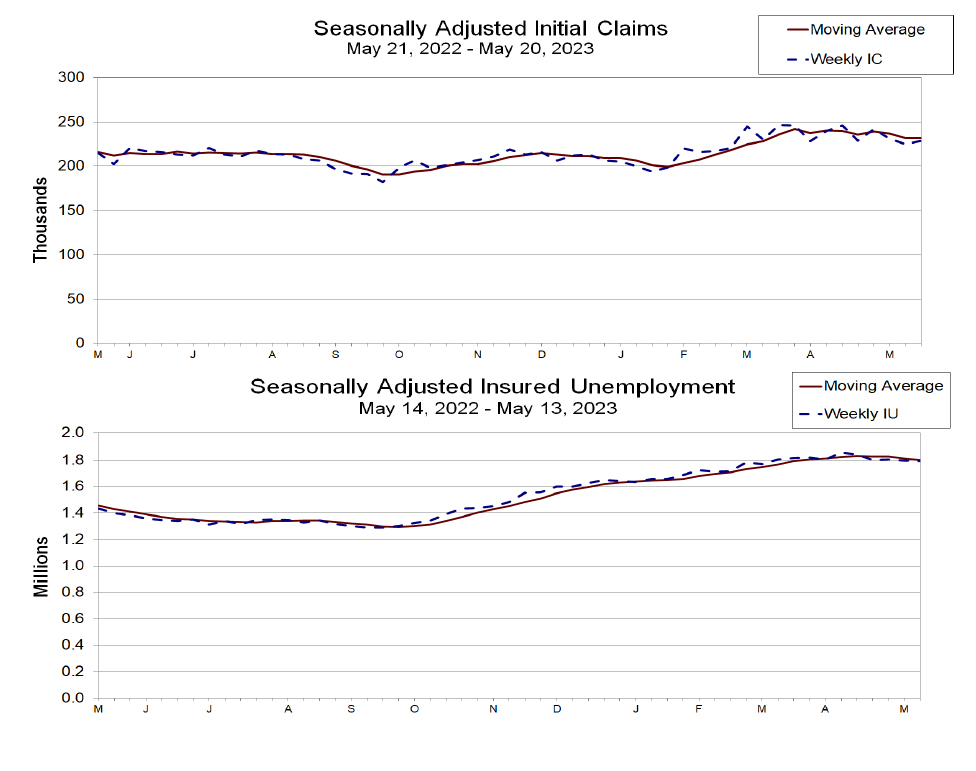

US initial jobless claims rose 2k to 229k

US initial jobless claims rose 4k to 229k in the week ending May 20, below expectation of 253k. Four-week moving average of initial claims was unchanged at 232k.

Continuing claims dropped -5k to 1794k in the week ending May 13. Four-week moving average of continuing claims dropped -12k to 1800k.

BoJ Ueda: No premature exit, but YCC tweak an option

BoJ Governor Kazuo Ueda stressed the importance of not prematurely tightening monetary policy to ensure that Japan can sustainably achieve its 2% inflation target. However, Ueda also suggested potential adjustments to the Yield Curve Control (YCC) if the policy's benefits and costs shift.

As for Japan's inflation forecast, Ueda expects consumer inflation to slow down as global fuel and raw material prices have begun to decline. Despite this projection, he did not entirely dismiss the possibility of needing to revise this outlook. "We can't completely rule out the possibility that this projection could prove wrong," Ueda said, adding, "If that's the case and if we see the need to revise our forecast, we'd like to act swiftly."

Ueda elaborated on possible modifications to the YCC policy. "If the BOJ were to modify YCC in the future, there are various ways of doing so," he stated. One potential approach he mentioned was targeting bond yields in the five-year zone, rather than the current 10-year zone.

"But I won't comment on whether we would definitely do so, how likely this could happen, or under what conditions the BOJ would see this option as desirable," Ueda said.

ECB de Guindos: Will continue tightening path to overcome high inflation

ECB Vice President Luis de Guindos told lawmakers in Brussels today, "Our future decisions will ensure that the policy rates will be brought to levels sufficiently restrictive to achieve a timely return of inflation to our 2% medium-term target." Then, interest rates will be "kept at those levels for as long as necessary," he said.

"Within less than a year we have raised the key interest rate by 375 basis points so far, stopped net purchases of bonds, and will probably stop reinvesting via the APP program from July," he said. "And the ECB Governing Council will continue on this monetary tightening path to overcome high inflation."

"As the energy crisis fades, governments should roll back the related support measures promptly and in a concerted manner to avoid driving up medium-term inflationary pressures, which would call for a stronger monetary policy response," de Guindos added.

Separately, Governing Council member, Bostjan Vasle, said "Further interest-rate increases will be needed."

"But they'll be smaller than they were in the past. We're approaching the level of rates that's restrictive enough to bring inflation back toward 2%. Fiscal — including wage policy — and monetary policies will have to be linked to a greater extent than in the past," Vasle noted.

Germany Gfk consumer sentiment rose to -24.2, not showing a clear up trend

Germany Gfk consumer sentiment for June rose slightly from -25.8 to -24.2, above expectation of -24.5. In May, economic expectations dropped from 14.3 to 12.3. Income expectations rose from -10.7 to -8.2. Propensity to buy dropped from -13.1 to -16.1.

"Consumer sentiment is not showing a clear upward trend at present. As a result, the rise in consumer climate index has slowed again somewhat," explains Rolf Bürkl, GfK consumer expert.

"A lower propensity to save has prevented the recovery in consumer sentiment from stagnating this month. However, it is still below the low level of spring 2020 during the first Covid-19 lockdown."

RBNZ Orr sees potential for rate cut after early next year

In his address to the parliament's finance and expenditure committee, RBNZ Governor Adrian Orr noted that the country's interest rates are already significantly above neutral, thereby suppressing spending and investment.

"They (interest rates) are well above what we would consider neutral, are constraining spending and investment," Orr said. He further stated, "The committee is confident monetary policy is restrictive and doing its job."

Orr characterized yesterday's 25bps rate hike as "an extra bit of insurance." The RBNZ committee voted five to two in favor of raising the OCR with two dissenting votes advocating for holding. Orr was quick to downplay any notion of discord within the committee. "On the division in the committee, the voting, there is no division. It's a committee decision," he told the parliamentary committee.

Looking forward, Orr hinted that the RBNZ might start easing interest rates in early next year. "The committee expects the OCR to remain steady until early next year. At that point, we may be able to start easing interest rates," he noted.

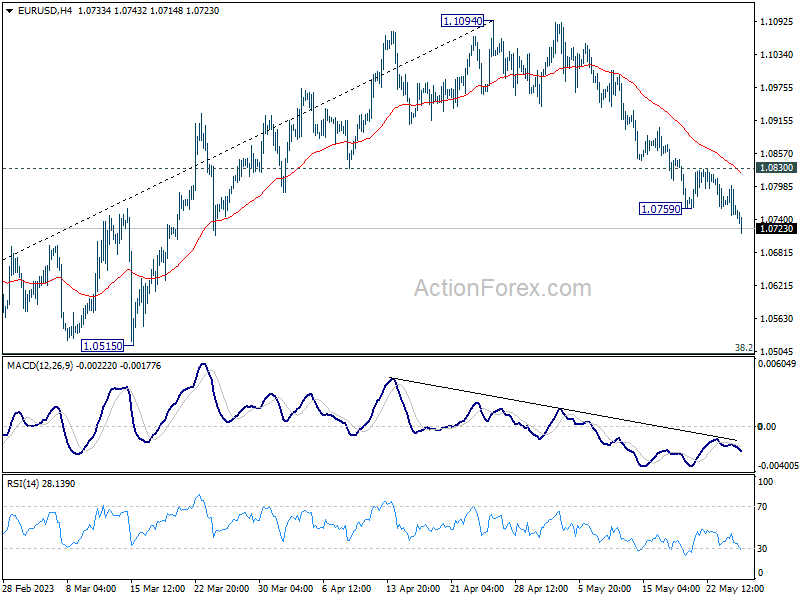

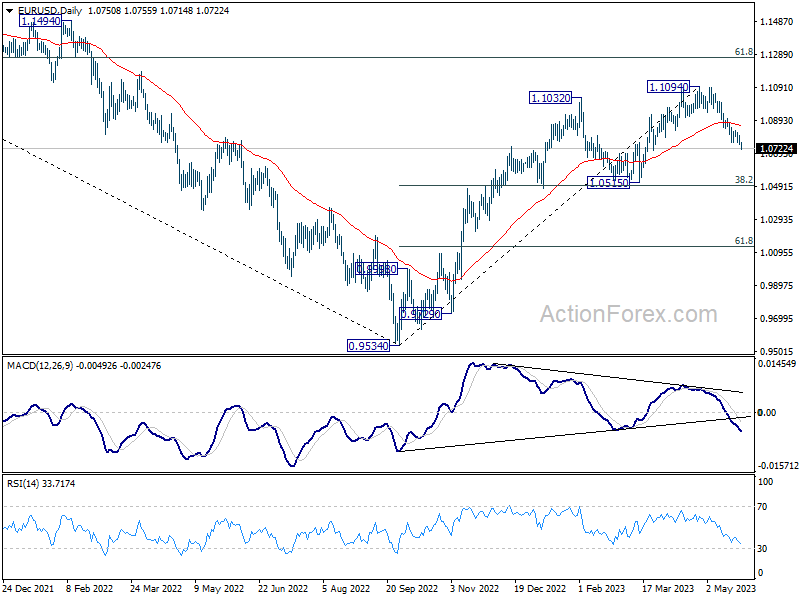

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0731; (P) 1.0766; (R1) 1.0784; More...

Intraday bias in EUR/USD is back on the downside as fall from 1.1094 resumes by breaking 1.0759. Current fall is seen as correcting whole up trend from 0.9534. Deeper decline should be seen to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, above 1.0830 minor resistance will turn intraday bias neutral first.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | Germany Gfk Consumer Confidence Jun | -24.2 | -24.5 | -25.7 | -25.8 |

| 06:00 | EUR | Germany GDP Q/Q Q1 F | -0.30% | 0.00% | 0.00% | |

| 12:30 | USD | Initial Jobless Claims (May 19) | 229K | 253K | 242K | 225K |

| 12:30 | USD | GDP Price Index Q1 P | 4.20% | 4.00% | 4.00% | |

| 12:30 | USD | GDP Annualized Q1 P | 1.30% | 1.10% | 1.10% | |

| 14:00 | USD | Pending Home Sales M/M Apr | 1.20% | -5.20% | ||

| 14:30 | USD | Natural Gas Storage | 100B | 99B |

BoJ Ueda: No premature exit, but YCC tweak an option

BoJ Governor Kazuo Ueda stressed the importance of not prematurely tightening monetary policy to ensure that Japan can sustainably achieve its 2% inflation target. However, Ueda also suggested potential adjustments to the Yield Curve Control (YCC) if the policy's benefits and costs shift.

As for Japan's inflation forecast, Ueda expects consumer inflation to slow down as global fuel and raw material prices have begun to decline. Despite this projection, he did not entirely dismiss the possibility of needing to revise this outlook. "We can't completely rule out the possibility that this projection could prove wrong," Ueda said, adding, "If that's the case and if we see the need to revise our forecast, we'd like to act swiftly."

Ueda elaborated on possible modifications to the YCC policy. "If the BOJ were to modify YCC in the future, there are various ways of doing so," he stated. One potential approach he mentioned was targeting bond yields in the five-year zone, rather than the current 10-year zone.

"But I won't comment on whether we would definitely do so, how likely this could happen, or under what conditions the BOJ would see this option as desirable," Ueda said.

US initial jobless claims rose 2k to 229k

US initial jobless claims rose 4k to 229k in the week ending May 20, below expectation of 253k. Four-week moving average of initial claims was unchanged at 232k.

Continuing claims dropped -5k to 1794k in the week ending May 13. Four-week moving average of continuing claims dropped -12k to 1800k.