Sample Category Title

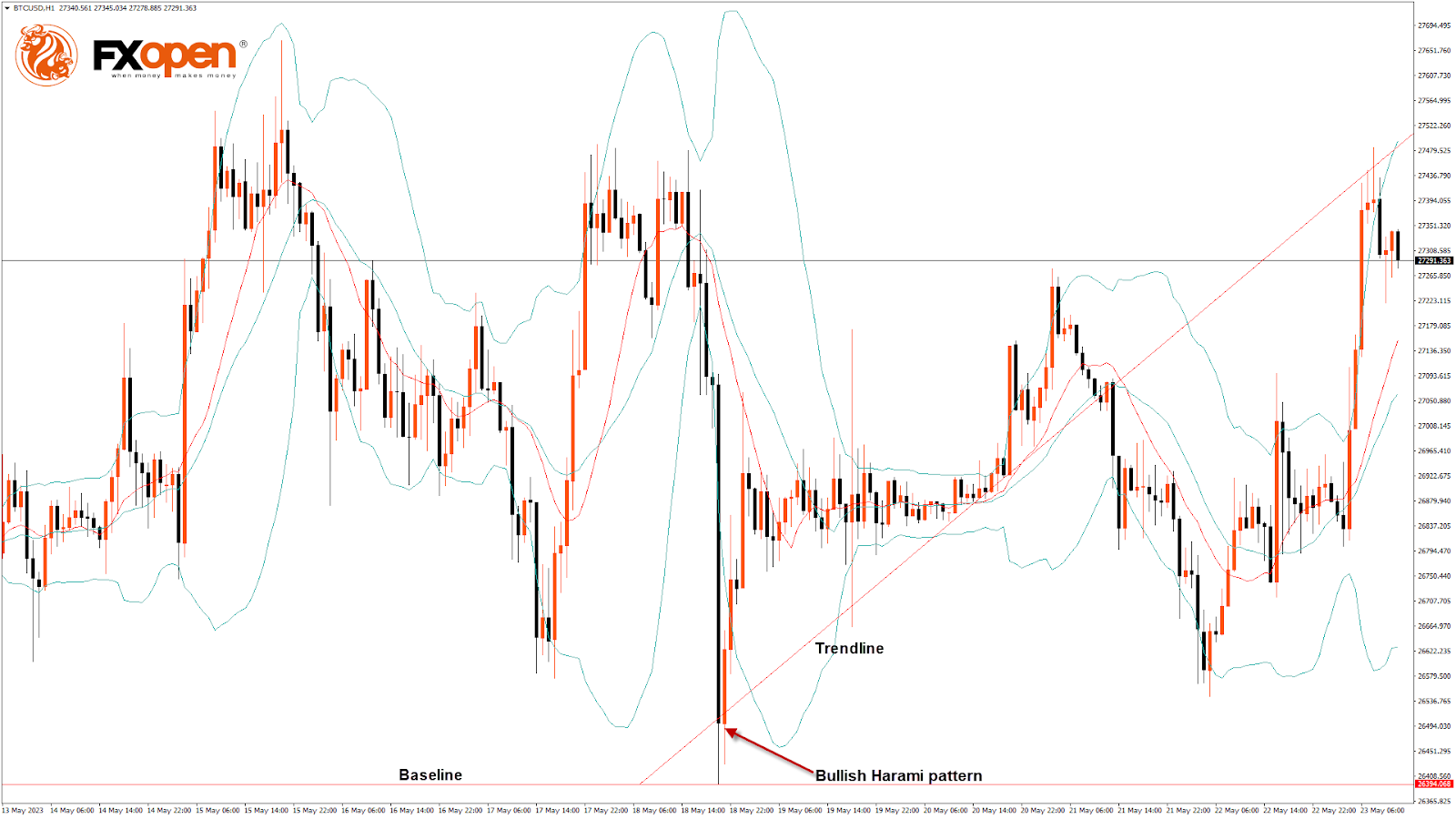

BTCUSD Analysis: Bullish Harami Pattern Above $26,394

Bitcoin’s price continues its bullish momentum from last week, and after touching a low of USD 26,394 on May 18, we can see a move towards a consolidation phase, after which we are expecting upsides in the range of USD 28500 and USD 29000.

On the hourly chart:

- We can clearly see a bullish Harami pattern above the USD 26,394 handle.

- Both the STOCH and Williams’s percent range indicate overbought levels, which means that in the immediate short term, a decline in the price is expected.

- The resistance of the channel is broken.

- The relative strength index is at 63.84, indicating a strong demand for Bitcoin and the continuation of the buying phase in the markets.

- Most of the major technical indicators are giving a bullish signal, which means that in the immediate short term, we are expecting targets of USD 28,000 and USD 28,500.

- Bitcoin’s price is now moving above its 100-hour simple moving average and its 100-hour exponential moving average.

- The average true range indicates low market volatility with mild bullish momentum.

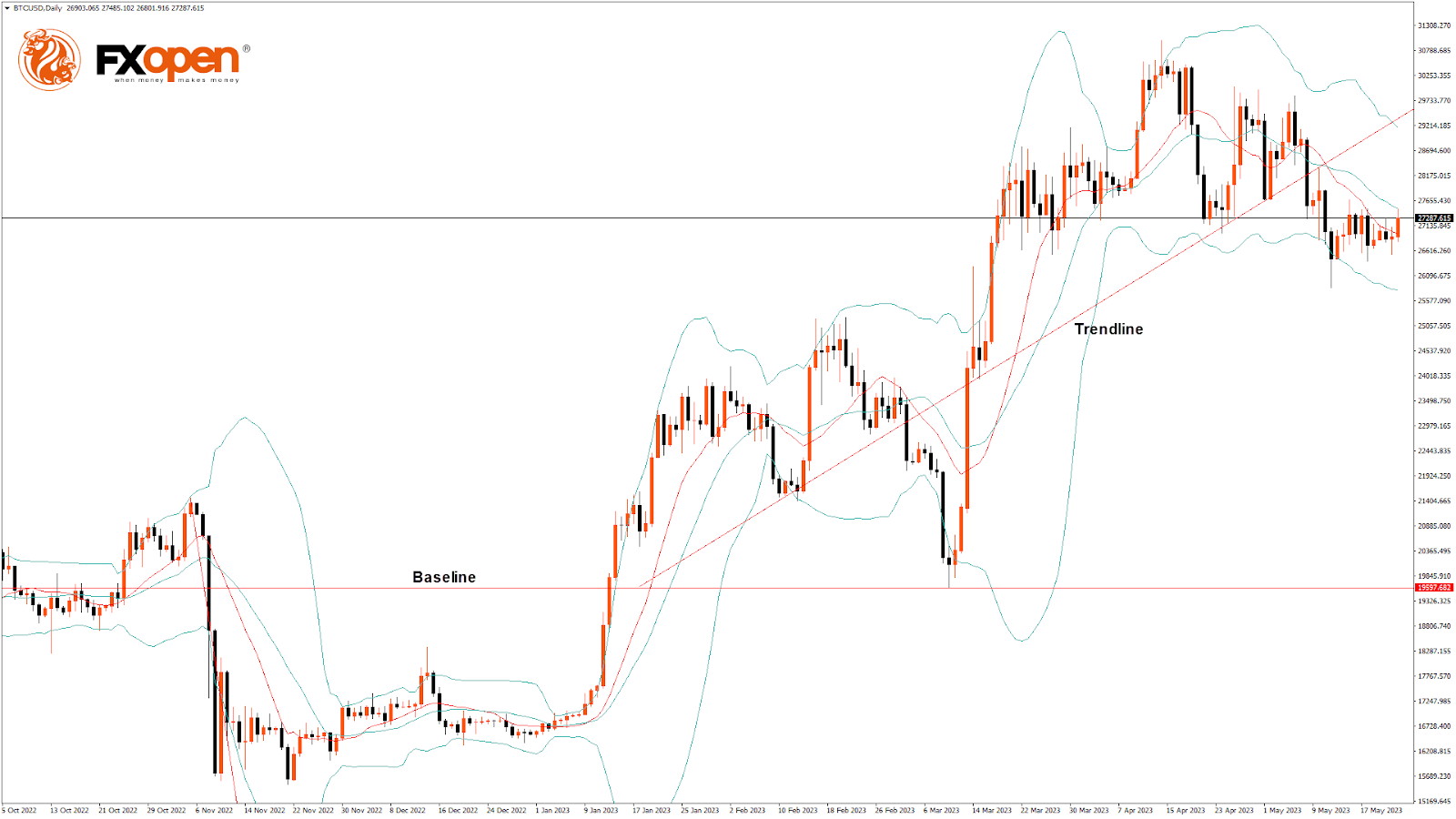

Bitcoin: Bullish Continuation Seen Above $26,394

The Bitcoin-to-USD exchange rate entered into a consolidation zone above the USD 26,000 handle after which we can see the start of the bullish moves.

On the daily chart:

- Bitcoin’s price bullish continuation is seen above USD 26,394.

- The RSI remains above 50, indicating a bullish market.

- The Bitcoin price is now trading below its pivot level of USD 27,337.

- The short-term range is mildly bullish.

- MACD crosses up its moving average.

A support zone is located at USD 25,881, which is a 1-month low, and at USD 26,624, which is a 38.2% retracement from 13-week high.

BTCUSD is now facing its classic resistance level of USD 27,383 and Fibonacci resistance level of USD 27406, breaking which the price will be able to move to USD 28,000.

The short-term outlook for Bitcoin is mildly bullish, the medium-term outlook has turned bullish, and the long-term outlook remains neutral under present market conditions.

The Week Ahead

We can see that the Bitcoin chart on D1 timeframe remains well supported above the USD 26,000 handle, and the medium term continuation pattern is seen, with the current support at USD 25,817, which is a pivot point 3rd support point.

The immediate expected target is USD 28,000, after which we may see some consolidation in the zone of the USD 28,500 level.

The monthly RSI is at 49.54, which indicates a neutral market and the shift towards the consolidation zone in the medium-term range.

We can see the formation of a bullish trend line from USD 26,394 to USD 27,489.

The BTCUSD is now facing resistance at USD 27,448, which is a 38.2% retracement from 4 week low, and at USD 27,879 at which the price crosses 9-day moving average stalls.

The weekly outlook for Bitcoin’s price is projected at USD 29,000 with a consolidation zone of USD 28,500.

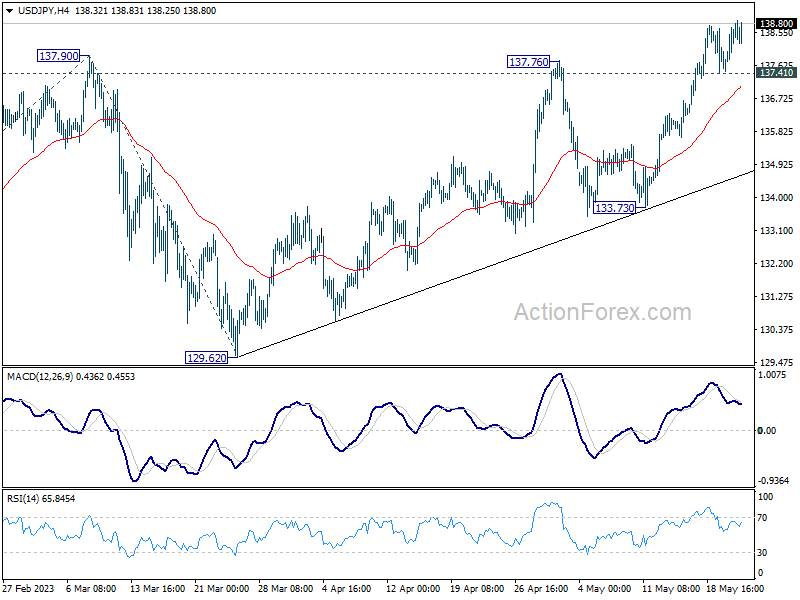

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 137.83; (P) 138.26; (R1) 139.02; More...

Intraday bias in USD/JPY stays on the upside despite some loss of upside momentum. Current rally from 127.20 should target 100% projection of 127.20 to 137.90 from 129.62 at 140.32. Break there will target 142.48 fibonacci level. On the downside, break of 137.41 minor support will turn intraday bias neutral again first, and bring more consolidation before staging another rise.

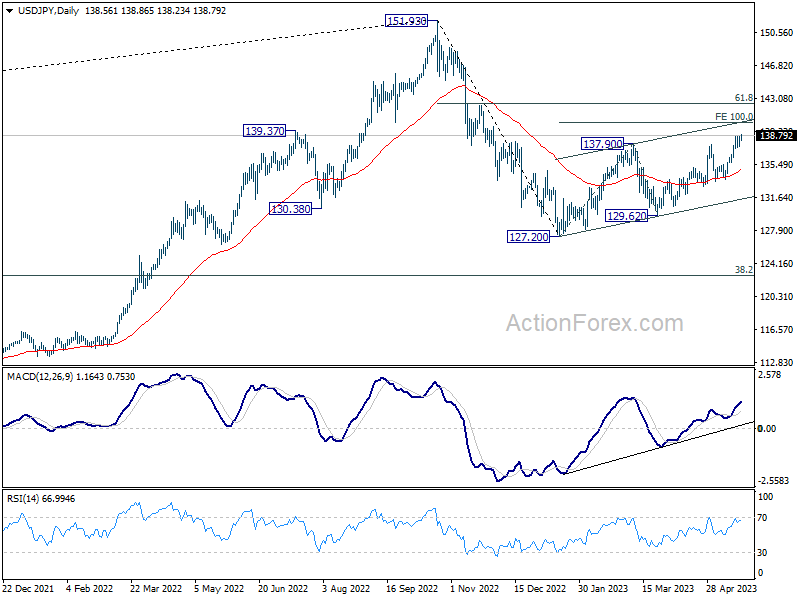

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 136.34. Sustained break there will pave the way back to retest 151.93. On the downside, however, break of 133.73 support will argue that the pattern could have started the third leg through 127.20 low.

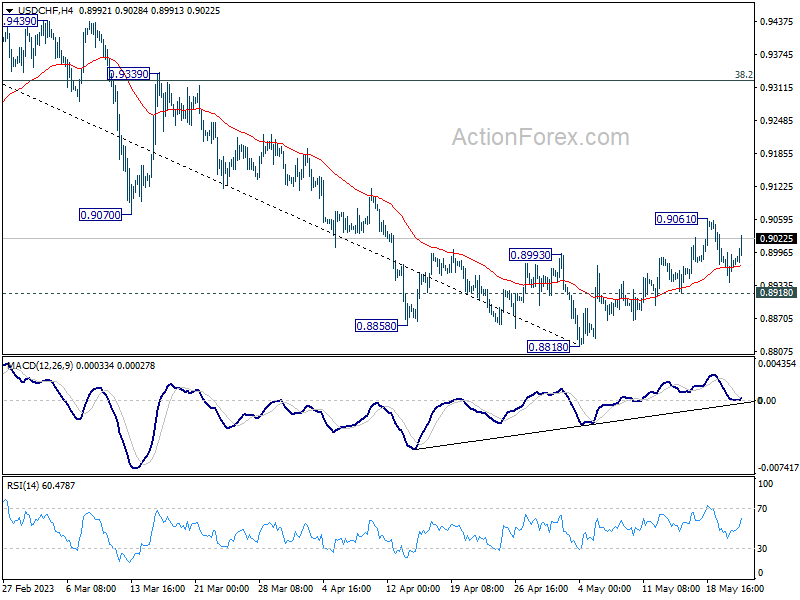

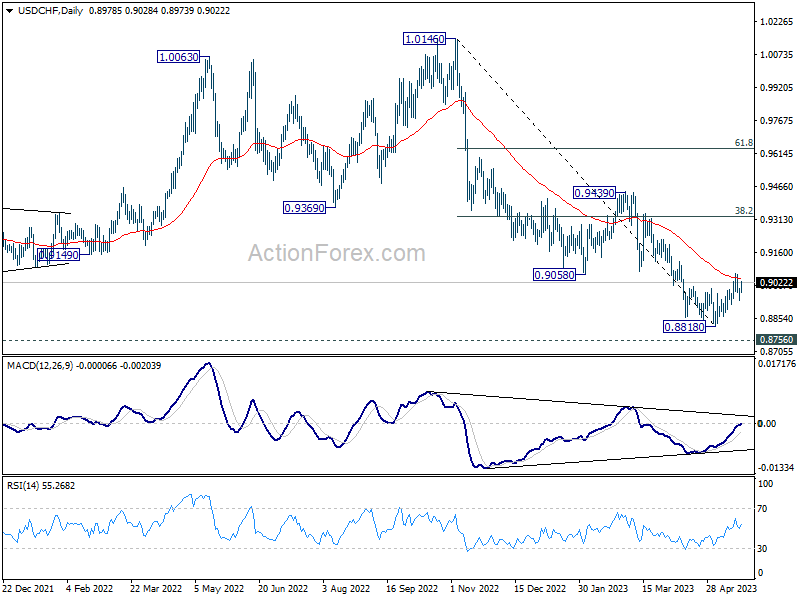

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8947; (P) 0.8972; (R1) 0.9004; More...

Intraday bias in USD/CHF stays neutral for the moment. Rebound from 0.8818 short term bottom is expected to continue as long as 0.8918 minor support holds. On the upside, sustained trading above 55 D EMA (now at 0.9039) should confirm that current rally is at least correcting whole down trend from 1.0146. Further rise should then be seen to 38.2% retracement of 1.0146 to 0.8818 at 0.9325. On the downside, though, break of 0.8918 will bring retest of 0.8818 low instead.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

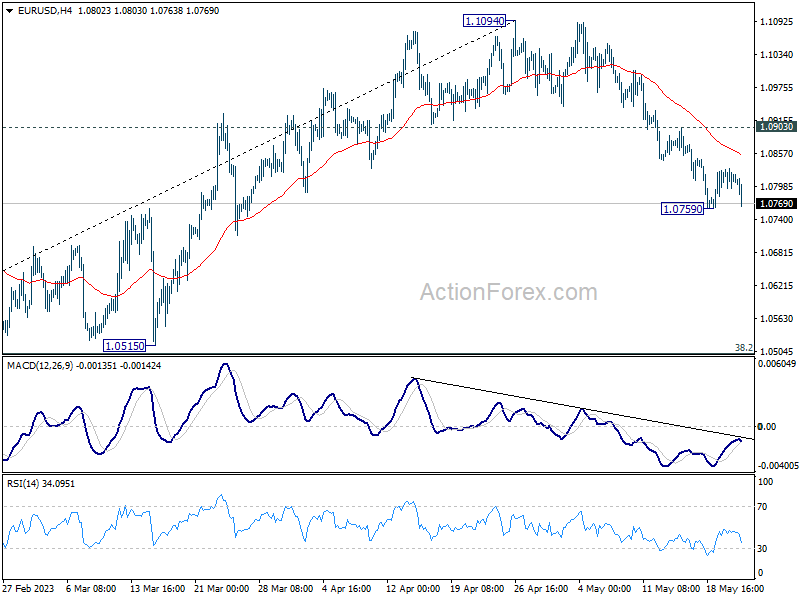

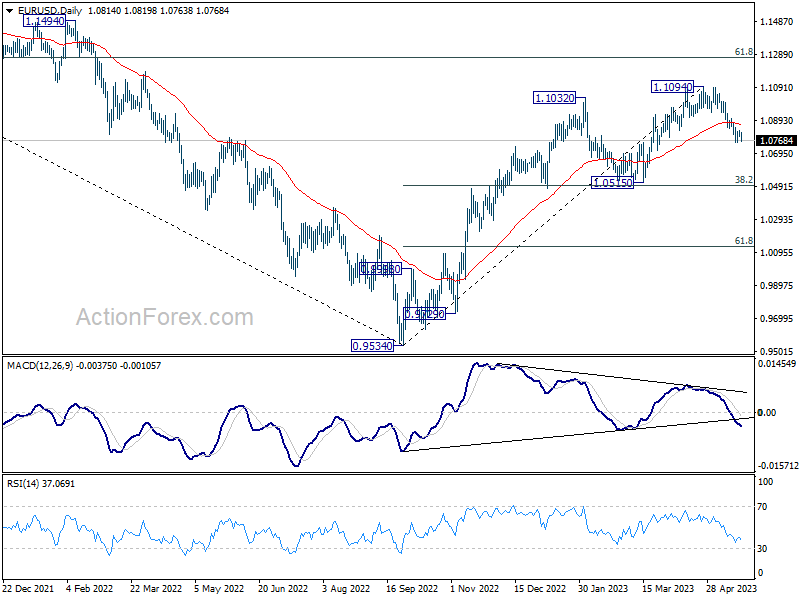

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0768; (P) 1.0798; (R1) 1.0837; More...

Intraday bias in EUR/USD stays neutral and outlook is unchanged. Deeper decline is expected as long as 1.0903 resistance holds. Fall from 1.1094 is seen as correcting whole up trend from 0.9534. Below 1.0759 will target 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, though, firm break of 1.0903 will bring stronger rebound back to retest 1.1094 high instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

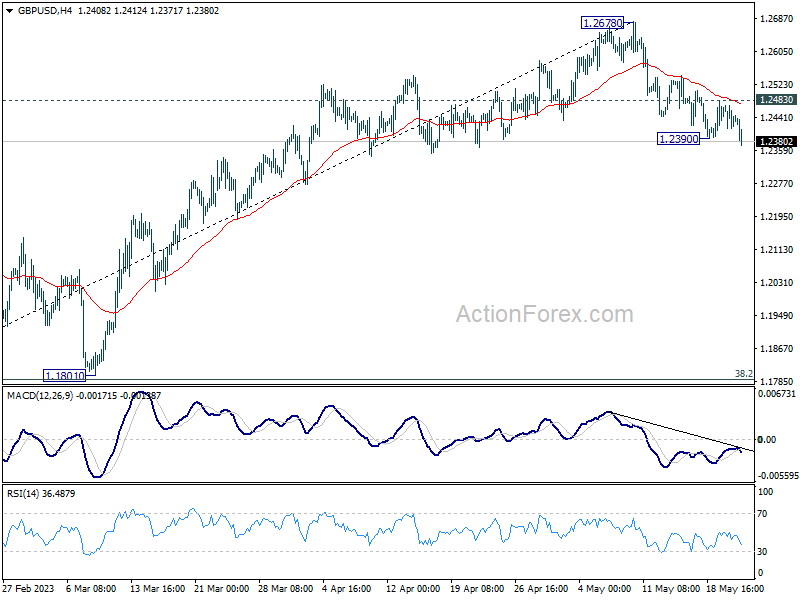

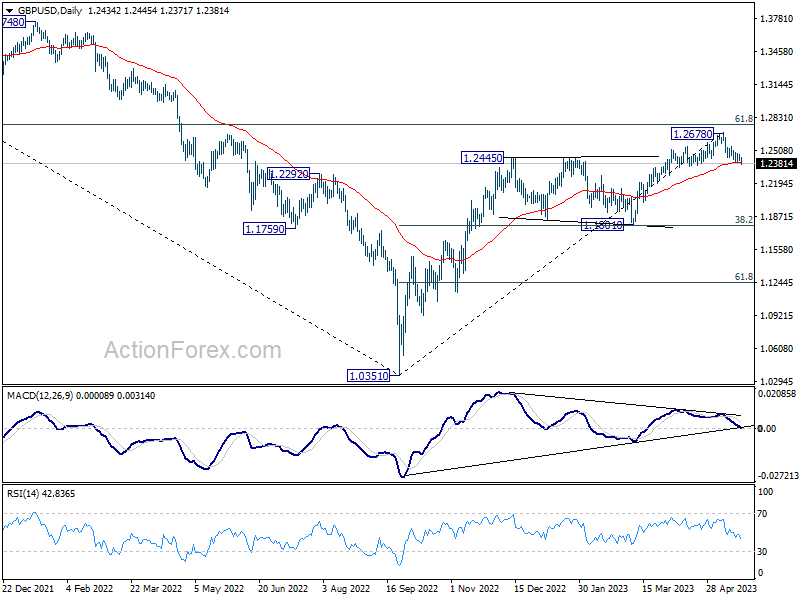

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2410; (P) 1.2441; (R1) 1.2469; More...

GBP/USD's decline from 1.2678 resumed by taking out 1.2390 temporary low and intraday bias is back on the downside. Current fall is seen as a correction to whole up trend form 1.0351. Deeper fall should then be seen to 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789). On the upside, however, break of 1.2483 resistance will bring stronger rebound back to retest 1.2678 high instead.

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

Forex Markets Turn Risk-Averse, Sterling Lower after PMI

Forex markets have turned noticeably risk-off today, with Aussie and Kiwi showing broad-based declines. Despite Loonie holding strong, it is being outperformed by both Dollar and Yen. Meanwhile, European majors present a mixed picture, with Sterling lagging behind Euro and Swiss Franc.

Today's PMI data illustrated a 'two-track' economy in Europe, marked by robust services and weak manufacturing. Despite the resilience of services sector helping to stave off recession, questions linger about the longevity of this support given the prevailing high inflation. Furthermore, in countries like UK where services sector is a large portion of the economy, it is likely that BoE will be compelled to persist with tightening measures in order to suppress demand.

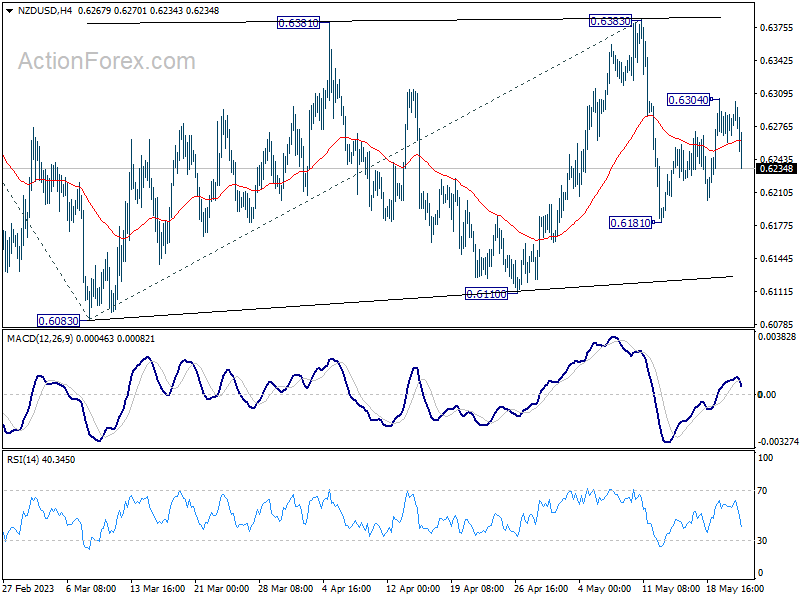

Attention now turns to the upcoming Asian session featuring an anticipated rate hike by RBNZ, placing NZD/USD in the spotlight. Recovery of NZD/USD from 0.6181 appears to be corrective so far, suggesting potential for further downside. Break below 0.6181 could trigger a rapid descent towards 0.6083 low. While a break above the 0.6304 resistance would extend the recovery, near-term outlook will continue to be bearish as long as 0.6383 resistance holds, just that downside breakout is delayed.

In Europe, at the time of writing, FTSE is up 0.31%. DAX is down -0.33%. CAC is down -0.97%, Germany 10-year yield is up 0.0328 at 2.492. Earlier in Asia, Nikkei dropped -0.42%. Hong Kong HSI dropped -1.25%. China Shanghai SSE dropped -1.52%. Singapore Strait Times rose 0.22%. Japan 10-year JGB yield rose 0.0167 to 0.404.

UK PMI composite dropped to 53.9, but BoE has more work to do

UK PMI Manufacturing dropped from 47.8 to 46.9 in May, a 5-month low. PMI Services dropped from 55.9 to 55.1. PMI Composite dropped from 54.9 to 53.9.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

"The UK economy enjoyed another month of strong growth in May, with the expansion continuing to be driven by surging post-pandemic demand in the service sector, notably from consumers and for financial services, with hospitality activities buoyed further by the Coronation. The surveys are consistent with GDP rising 0.4% in the second quarter after a 0.1% rise in the first quarter...

"The UK is therefore seeing a tale of two economies, with the divergence between manufacturing and services posing difficulties for policymakers. However, it's the far larger service sector that will typically dictate policy, meaning these survey results are nothing but hawkish in suggesting the Bank of England has more work to do to quash stubbornly high inflationary pressures in the services economy."

Eurozone PMI manufacturing fell to 36-mth low, services dipped

Eurozone PMI Manufacturing fell from 45.8 to 44.6 in May, a 36-month low. PMI Services fell from 56.2 to 55.9. PMI Composite decreased from 54.1 to 53.3.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank said: Eurozone GDP is likely to have grown in the second quarter thanks to the healthy state of the services sector. However, the manufacturing sector is a powerful drag on the momentum of the economy as a whole.

He added that ECB will have a "headache" with the PMI price data, as "selling prices in the services sector actually rose more than in the previous month".

Also released, Germany PMI manufacturing dropped from 44.5 to 42.9 in May, a 36-month low. PMI Services rose from 56.0 to 57.8, a 21-month high. PMI Composite rose from 54.2 to 54.3, a 13-month high.

France PMI Manufacturing rose from 45.6 to 46.1. PMI Services dropped from 54.6 to 52.8. PMI Composite dropped from 52.4 to 51.4.

Australia PMI composite dropped to 51.2, still early to call an end to RBA tightening

Australia's PMI Manufacturing index stayed put at 48.0 in May, marking the joint-lowest reading since May 2020. On the other hand, PMI Services fell from 53.7 to 51.8, causing Composite PMI to decrease from 53.0 to 51.2.

Warren Hogan, Chief Economic Advisor at Judo Bank, said, "The May Flash result shows a small retracement from the strong April outcome reinforcing the view that overall economic activity in Australia is holding up well as we enter the winter months."

Despite the manufacturing sector's continuous slowdown, Hogan emphasized that this does not signal a recession. In contrast to manufacturing, the services sector has shown recent strength, and was "far from the risk of recession:.

However, he warned of the implications of better economic conditions in terms of inflation. "The RBA is trying to engineer a soft landing to rid the economy of inflation. But if they don't lean hard enough on monetary policy, we could see a more stubborn inflation emerge which will ultimately require a bigger lift in interest rates," Hogan cautioned.

Highlighting the strong correlation between the pick-up in the services PMI, housing market, rising population growth, and job advertising, he concluded, "Last week's labour market data on employment and wages have bought the RBA some time, but the Flash PMIs highlight that it is still too early to call an end to the monetary policy tightening cycle."

Japan PMI manufacturing rose to 50.8, services rose to 56.3

Japan PMI Manufacturing rose from 49.5 to 50.8 in April, signalling the first improvement in operating conditions since October 2022. PMI Manufacturing Output rose from 47.9 to 51.9. PMI Services rose from 55.4 to 56.3. PMI Composite Output rose from 52.9 to 54.9.

Usamah Bhatti, Economist at S&P Global Market Intelligence, said:

"The Japanese private sector economy continued on an upward trajectory, as signalled by a further expansion in May. The rate of growth quickened from April to reach the strongest since October 2013 and the second-strongest in the survey history (since September 2007).

"Service providers continued to report strong growth momentum with a renewed record increase in business activity, while manufacturers indicated an improvement in operating conditions for the first time in seven months, with output and new orders returning to expansion territory for the first time since last June."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2410; (P) 1.2441; (R1) 1.2469; More...

GBP/USD's decline from 1.2678 resumed by taking out 1.2390 temporary low and intraday bias is back on the downside. Current fall is seen as a correction to whole up trend form 1.0351. Deeper fall should then be seen to 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789). On the upside, however, break of 1.2483 resistance will bring stronger rebound back to retest 1.2678 high instead.

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI May P | 48 | 48 | ||

| 23:00 | AUD | Services PMI May P | 51.8 | 53.7 | ||

| 00:30 | JPY | Manufacturing PMI May P | 50.8 | 49.5 | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Apr | 24.7B | 17.5B | 20.7B | 20.0B |

| 07:15 | EUR | France Manufacturing PMI May P | 46.1 | 46.1 | 45.6 | |

| 07:15 | EUR | France Services PMI May P | 52.8 | 54.3 | 54.6 | |

| 07:30 | EUR | Germany Manufacturing PMI May P | 42.9 | 45.2 | 44.5 | |

| 07:30 | EUR | Germany Services PMI May P | 57.8 | 55.5 | 56 | |

| 08:00 | EUR | Eurozone Manufacturing PMI May P | 44.6 | 46.2 | 45.8 | |

| 08:00 | EUR | Eurozone Services PMI May P | 55.9 | 55.6 | 56.2 | |

| 08:00 | EUR | Current Account (EUR) Mar | 31.2B | 20.2B | 24.3B | |

| 08:30 | GBP | Manufacturing PMI May P | 46.9 | 48.2 | 47.8 | |

| 08:30 | GBP | Services PMI May P | 55.1 | 55.5 | 55.9 | |

| 12:30 | CAD | Industrial Product Price M/M Apr | -0.20% | 0.20% | 0.10% | |

| 12:30 | CAD | Raw Material Price Index Apr | 2.90% | 0.70% | -1.70% | |

| 13:45 | USD | Manufacturing PMI May P | 50 | 50.2 | ||

| 13:45 | USD | Services PMI May P | 53.6 | 53.6 | ||

| 14:00 | USD | New Home Sales Apr | 665K | 683K |

UK CPI to Drop, But Will It Change BoE?

UK CPI will finally fall below double digits when the April report is issued tomorrow. Unless there is an unprecedented catastrophe, that is. While policymakers and politicians might cheer the results, the components are likely to keep the BOE on track to hike at the next meeting.

Why will UK inflation drop?

Usually, analysts are cautious about making forecasts for economic data, because surprises are very common. But this time around, the math is pretty certain. What isn't certain, as usual, is the market reaction. So, let's first address the math.

Back in April of 2022, between March and April, inflation jumped a whopping 2.5%. That was due to an adjustment in energy prices made by Ofgem, as gas and crude prices spiked following the imposition of sanctions on Russia over the war in Ukraine. That's the highest monthly increase recorded, ever. It is, therefore, very, very unlikely to be repeated.

Accounting for the base effect

For the inflation rate to come in in the double digits this month, it would have to have a similar monthly increase as April of last year. Over the last few months, the median monthly inflation change has been around 0.5%. In order for annual inflation to stay at or above 10%, then monthly inflation would have to have jumped by five times the median. March inflation was 0.8%, which means that for inflation to come in at 10% (to maintain double digits), April 2023 monthly inflation would have to be 1.8%. It is currently forecast to be 0.8%. Analysts would have to be wrong by more than double in order for inflation to stay in the double digits.

But, how far below double digits is still an open question. The current average of economists' forecasts is 8.5% for annual headline inflation, compared to 10.1% reported for last March. In other words, inflation is expected to remain quite high. The drop is thanks to technical reasons, which would likely not change monetary policy outlook.

The market movers

What the market is mostly focused on now is how the BOE will react, and it is more interested in the core inflation rate. Excluding the volatile elements of energy and food, UK inflation is expected to tick down just slightly to 6.1% compared to 6.2% prior. Over triple the BOE's target. A one decimal decline is very unlikely to change the view of the 7 MPC members who voted last time to hike.

Meanwhile, inflation might be getting out of the BOE's hands. In a recent presentation before the British Chamber of Commerce, BOE Governor Bailey said that core inflation was now due to "secondary effects". Translated into English, this means that in his estimation, there are signs of the dreaded wage-price spiral that could signal inflation will remain high for a long time. That, at least in the market's estimation, implies that even more tightening will be needed.

But, the pound might not gain so much strength, because the division in the BOE's MPC leaves many market participants with doubts that the BOE is sufficiently committed to bring inflation down. The IMF's new report says that the UK is likely to avoid a recession this year, which could allow room for more hiking. But whether the BOE will deliver is still an open question.

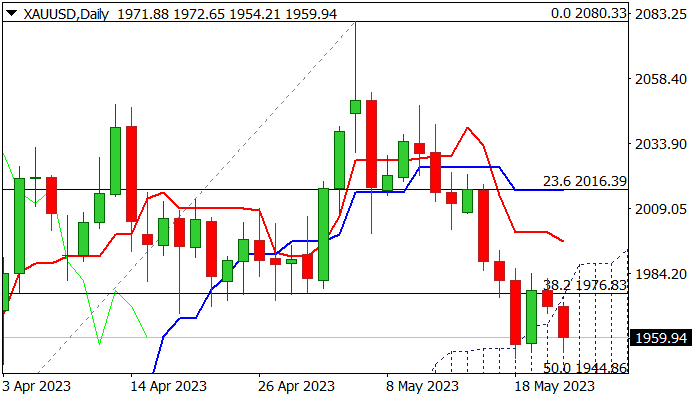

XAU/USD: Gold Comes Under Renewed Pressure on Hawkish Fed/Debt Ceiling Deal Hopes

Gold dips further on Tuesday, as renewed hawkish stance from Fed and optimism about debt ceiling deal improve risk sentiment and inflate dollar.

Fresh weakness eyes pivotal $1950 zone (lows of last Thu/Fri) and Fibo support at $1944 (50% retracement of $1809/$2080 rally), violation of which would add to reversal signals risk deeper fall towards targets at $1931 (100DMA) and $1926 (daily cloud base).

Weakening daily studies (rising negative momentum / daily Tenkan/Kijun-sen bear-cross) maintain near-term bearish outlook.

The price penetrated thick rising daily Ichimoku cloud and needs close within the cloud to confirm signal.

Strong resistance at $1975 (daily cloud top / former higher base) should cap upticks to keep bears in play.

Res: 1975; 1986; 1990; 2000.

Sup: 1951; 1944; 1931; 1926.

USD/JPY Hits 6-mth High as BoJ Core CPI Accelerates

- BoJ Core CPI rises to 3.0%

- USD/JPY hits 6-mth high

USD/JPY climbed as high as 138.87 earlier on Tuesday, its highest level since May 28th. The yen has edged lower and is trading at 138.43 in the European session, down 0.17%.

BoJ Core CPI surprises to the upside

Japan released BoJ Core CPI earlier in the day. The March reading rose to 3.0%, up from 2.9% in February and above the estimate of 2.8%. This is the BoJ’s preferred inflation gauge and is another indication that inflation remains sticky and above the Bank’s target of 2%.

There is a widespread feeling in the markets that change is coming to the Bank of Japan, after years of deflation and an ultra-loose policy. The new Governor, Kazuo Ueda has kept a fairly low profile, perhaps to keep market volatility at a minimum during a sensitive time for the central bank. Ueda has indicated that he would consider tightening policy if it was evident that inflation was sustainable at 2%. The BoJ insists that inflation is still temporary but this argument will start to ring hollow if inflation indicators continue to point to inflation hovering around 3%.

If the BoJ were to tighten, it would likely adjust or phase out its yield control curve policy, rather than raise interest rates. The BoJ widened the target band for 10-year Japanese government bonds in December, which sent the yen sharply higher. Another widening of the target band would likely send the yen higher, and speculators are betting that the Ueda will eventually shift policy which will boost the yen.

We’ll get another inflation reading on Thursday, with Tokyo Core CPI expected to ease to 3.3% in May, following a 3.5% gain in April.

USD/JPY Technical

- USD/JPY tested support at 138.37 earlier in the day. Below, there is support at 137.45

- There is resistance at 139.25 and 140.55

Will GBP Recover Now?

The Bank of England (BoE) has dramatically shifted its economic forecasts. They no longer expect a recession in the UK and have upgraded their growth projections. This year, the BoE predicts GDP growth of +0.25%, a significant improvement from previous expectations. Next year's forecast is even more optimistic, with a projected growth of 0.75%. However, let's not get too carried away—the outlook remains subdued, with growth below 1% until 2025. The UK economy is still fragile, as evidenced by lackluster performance in the first quarter of 2023. On the inflation front, the BoE expects a decline over the year but at a slower pace than previously anticipated. Inflation is now projected to be around 5% by the end of this year and is not expected to fall below the 2% target until 2025. The recent interest rate hike suggests that further tightening may be on the horizon, especially considering the upgraded growth and inflation forecasts. So, keep your eyes peeled for potential developments in monetary policy.

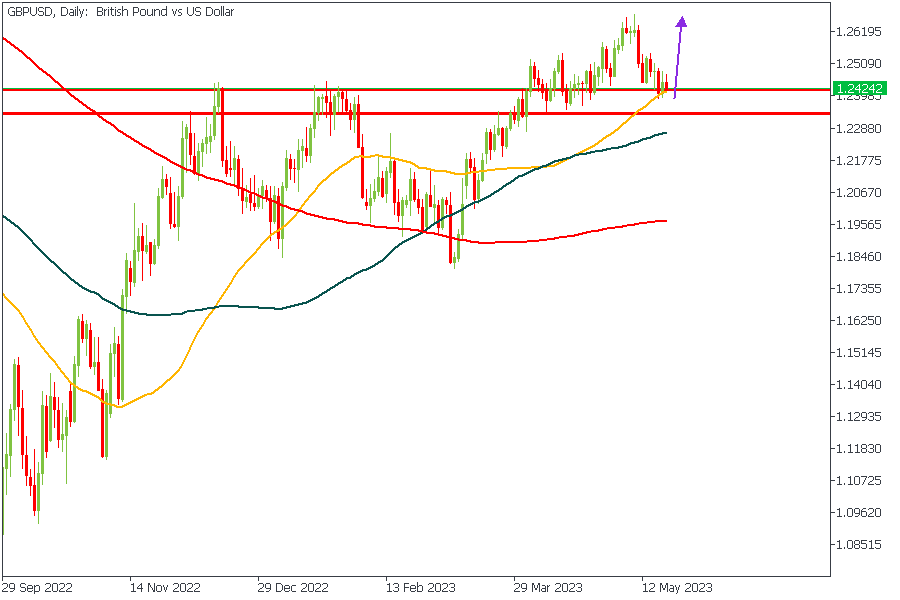

GBPUSD - Daily Timeframe

From the chart above, it is clear that the price is at a key level - a pivot zone. Considering the break above the previous high, the support from the 50-Day moving average, and the arrangement of the moving averages in increasing order, I will maintain a bullish sentiment on this commodity until the price breaks below the pivot zone.

Analyst’s Expectations:

- Direction: Bullish

- Target: 1.25873

- Invalidation: 1.23420

GBPAUD - H4 Timeframe

GBPAUD presents a very tricky case. We see price trading within the consolidation channel while pulling a dance between the 50-period and 100-period moving averages. We haven’t seen a touch of the resistance trendline of the channel. Hence, my argument is in favor of bullish price action. Combine that with the confluence from the trendline support and the 200-period moving average, and you will see why I expect a bullish price action.

Analyst’s Expectations:

- Direction: Bullish

- Target: 1.87952

- Invalidation: 1.86353

GBPNZD - H4 Timeframe

The moving averages on GBPNZD signal an overall bearish market, but it is good to scalp a few bullish pips in between. My bullish sentiment is based on the confluence of the trendline support and the pivot zone - maybe not be a strong argument, but I will be watching for a clear reaction from the pivot zone as my entry cue.

Analyst’s Expectations:

- Direction: Bullish

- Target: 1.99571

- Invalidation: 1.97104

GBPJPY - Daily Timeframe

This pivot zone on GBPJPY can be traced to the Monthly timeframe. The zone has also been retested a few times - serving as an area of liquidity grab from the previous high. In this scenario, as in the case of GBPNZD, the confluences seem scanty - making it a daring trade. That is why my entry will be timed to follow a notable reversal candlestick pattern, without which I wouldn’t bother taking a trade on GBPJPY at all!

Analyst’s Expectations:

- Direction: Bearish

- Target: 169.349

- Invalidation: 174.048

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.