Sample Category Title

Crypto Attracts Buyer Interest, But Reversal Needs Proof

Market picture

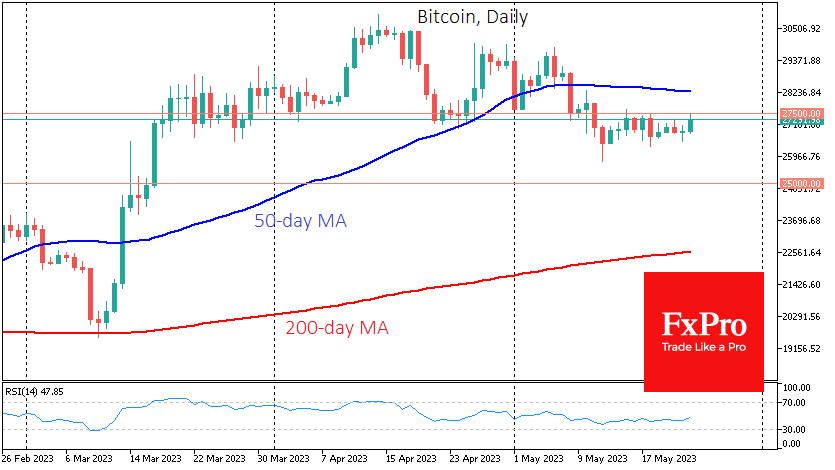

Crypto market capitalisation rose 1.4% over the last 24 hours to $1.138 trillion. After quiet trading on Monday, most gains came on Tuesday morning. The timing of the move is due to news on the US debt ceiling, where there is no deal yet, but Biden notes progress in negotiations. Ether is up 2.3% at $1856, with the top altcoins gaining between 0.3% (Solana) and 3% (Polygon).

Bitcoin is up 1.6% over the past day to $27.3K and earlier today climbed close to $27.5K, the upper end of the range since the 15th. Despite the positive momentum, the daily timeframes remain bearish, with Bitcoin trading below $27.5K.

According to CoinShares, investments in cryptocurrency funds fell for the fifth consecutive week to $32 million last week, with bitcoin investments down $33 million and Ethereum investments down $1 million. Investment in funds that allow shorts on Bitcoin fell by $1.3 million.

According to Santiment, the number of BTC and ETH on exchanges has fallen to its lowest level in several years, which is seen as a sign of an attitude towards long-term holding.

News background

Mott Capital Management founder Michael Kramer warned that Bitcoin could fall to $20K. According to him, BTC is a leading indicator for all risky assets, so its decline would be negative for the stock market.

Anthony Scaramucci, founder of hedge fund SkyBridge Capital, believes that the actual value of Bitcoin should now be $40K. According to him, we are now witnessing a global proliferation of BTCs, similar to what happened in the late 1990s with the rise of the internet.

Cryptocurrency platform Bakkt is considering expanding its business in Europe in light of the Crypto Asset Market Regulation Act (MiCA) passed in April. Bakkt currently only offers services in the US.

US lawmakers have drafted a bipartisan bill prohibiting the Fed from issuing the digital dollar (CBDC). Lawmakers cited Americans’ right to financial privacy.

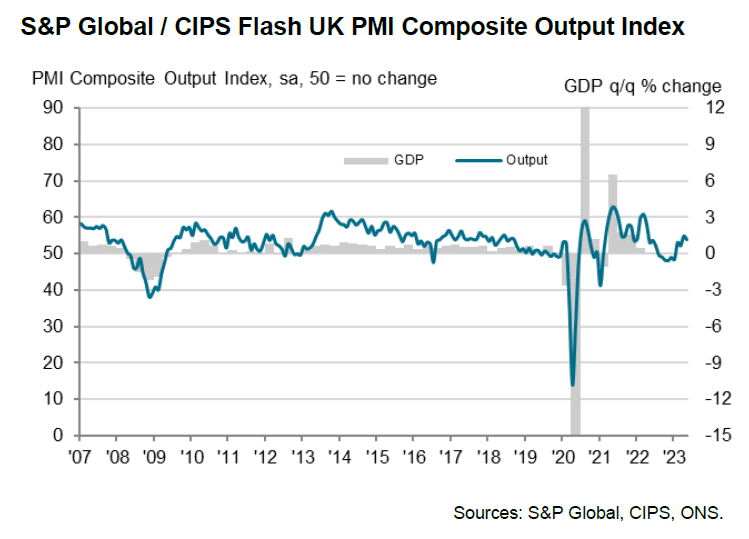

UK PMI composite dropped to 53.9, but BoE has more work to do

UK PMI Manufacturing dropped from 47.8 to 46.9 in May, a 5-month low. PMI Services dropped from 55.9 to 55.1. PMI Composite dropped from 54.9 to 53.9.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

"The UK economy enjoyed another month of strong growth in May, with the expansion continuing to be driven by surging post-pandemic demand in the service sector, notably from consumers and for financial services, with hospitality activities buoyed further by the Coronation. The surveys are consistent with GDP rising 0.4% in the second quarter after a 0.1% rise in the first quarter...

"The UK is therefore seeing a tale of two economies, with the divergence between manufacturing and services posing difficulties for policymakers. However, it's the far larger service sector that will typically dictate policy, meaning these survey results are nothing but hawkish in suggesting the Bank of England has more work to do to quash stubbornly high inflationary pressures in the services economy."

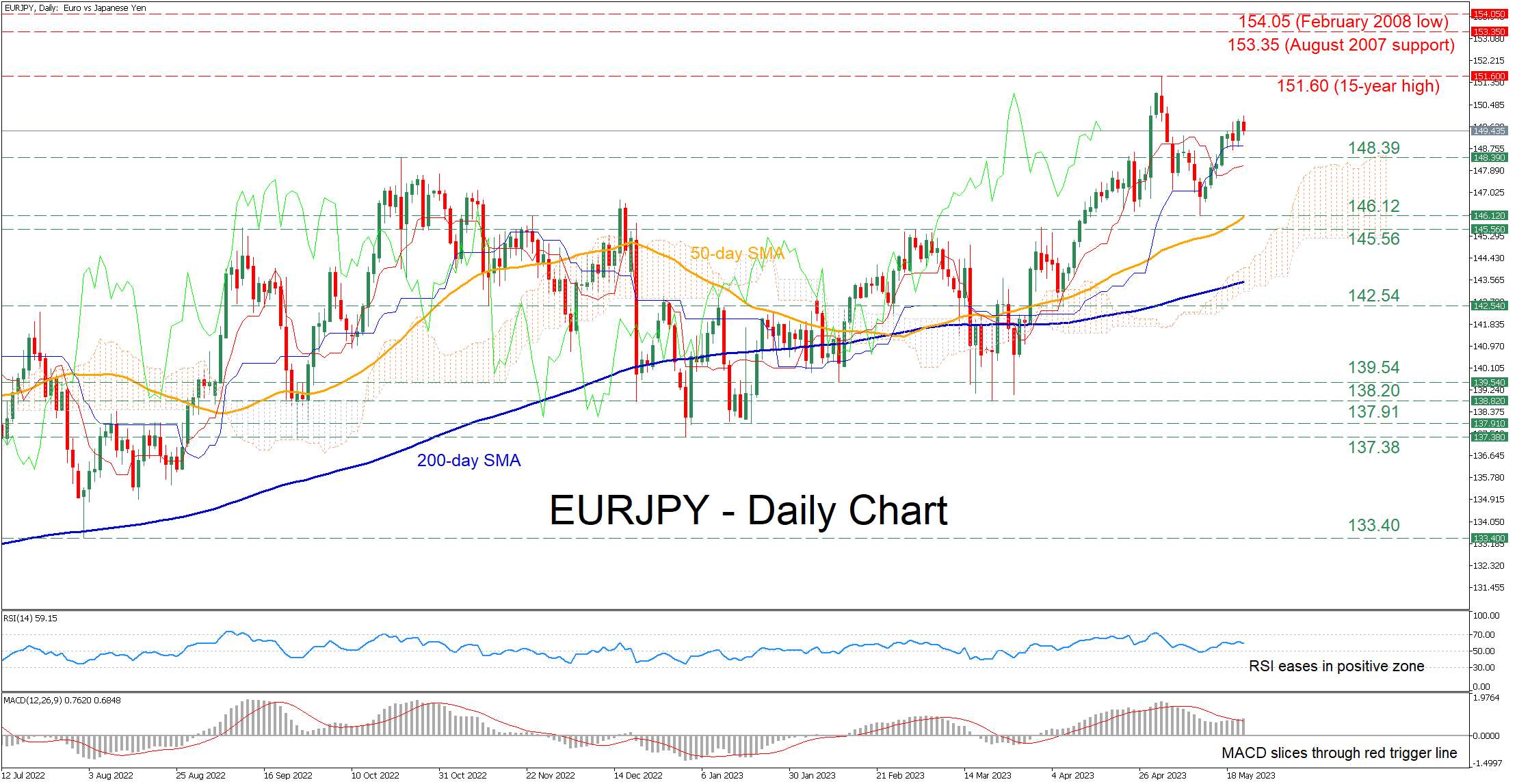

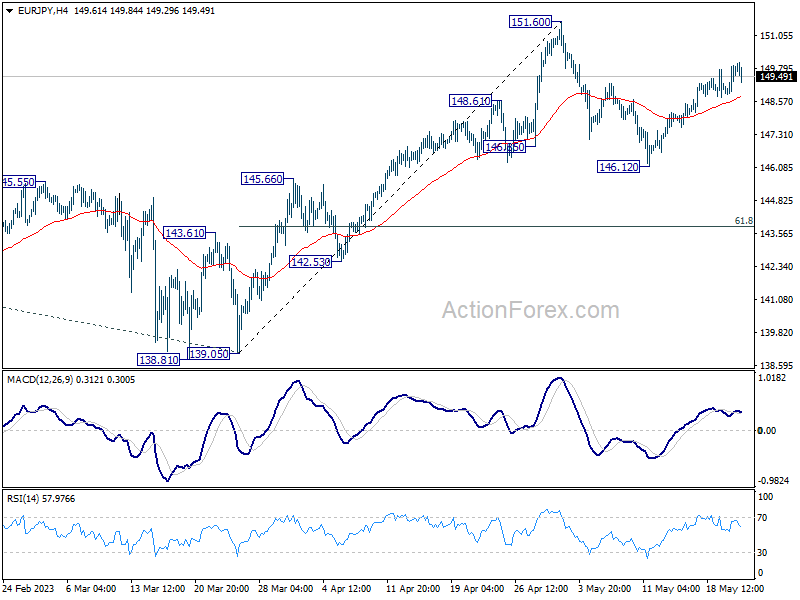

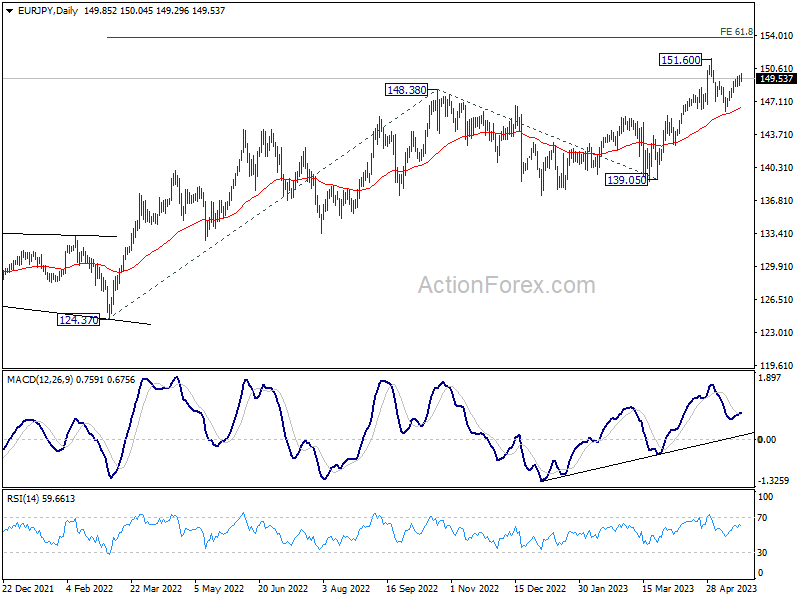

EURJPY Regains Traction, Eyeing Multi-Year Highs

EURJPY had been in a prolonged uptrend, which ceased at a fresh 15-year high of 151.60 in early May. Even though the pair experienced a mild pullback from its recent peak, it quickly found its feet and stormed back higher in an effort to extend its bullish medium-term structure.

The momentum indicators are endorsing this latest advance, with the RSI flatlining way above its 50-neutral mark and the MACD crossing above its red signal line in the positive region.

If the recent upside trajectory resumes, the bulls could attack the 15-year peak of 151.60. Breaking above that zone, the pair might ascend to form fresh multi-year highs, where the August 2007 support of 153.35 may provide upside protection. A violation of that territory could set the stage for the February 2008 low of 154.05.

Alternatively, a potential downside correction could come to a halt at the October 2022 high of 148.39, which could serve as support in the future. Diving beneath that region, the pair could challenge the 146.12 congested region that includes the May low and the 50-day simple moving average (SMA). Should that barricade fail, the 145.56 obstacle could prove to be a tough one for the bears to overcome.

Overall, EURJPY has staged a massive comeback following the recent retreat from its multi-year peaks. However, a failure to create a fresh higher high may open the door for a moderate downside correction.

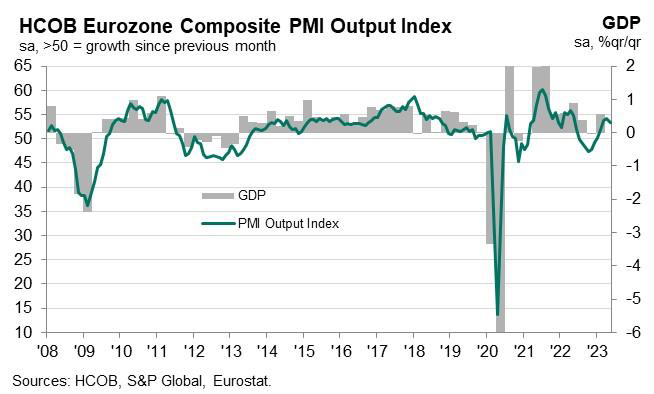

Eurozone PMI manufacturing fell to 36-mth low, services dipped

Eurozone PMI Manufacturing fell from 45.8 to 44.6 in May, a 36-month low. PMI Services fell from 56.2 to 55.9. PMI Composite decreased from 54.1 to 53.3.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank said: Eurozone GDP is likely to have grown in the second quarter thanks to the healthy state of the services sector. However, the manufacturing sector is a powerful drag on the momentum of the economy as a whole.

He added that ECB will have a "headache" with the PMI price data, as "selling prices in the services sector actually rose more than in the previous month".

Full Eurozone PMI release here.

Also released, Germany PMI manufacturing dropped from 44.5 to 42.9 in May, a 36-month low. PMI Services rose from 56.0 to 57.8, a 21-month high. PMI Composite rose from 54.2 to 54.3, a 13-month high.

France PMI Manufacturing rose from 45.6 to 46.1. PMI Services dropped from 54.6 to 52.8. PMI Composite dropped from 52.4 to 51.4.

USD Continues to Bounce

EUR/USD struggles for bids

The US dollar inched higher after the St. Louis Fed president called for another half-point hike. A bearish MA cross on the daily chart indicates waning buying pressure as the euro strives to preserve its gains from the past two months. A break below 1.0850 may have prompted more buyers to bail and sit on the sidelines, turning it into a fresh resistance. The RSI’s oversold situation attracted some bottom buyers with 1.0760 as an immediate support, its breach may trigger a new round of sell-off, sending the exchange rate to 1.0700.

US Oil awaits breakout

WTI crude rebounds as supply tightens with the OPEC+ production cuts going into effect this month. The bulls are still trying to keep the latest bounce off 66.00 valid and the sideways action is a sign of hesitation as both sides look to regain control. 73.40 on the 20-day SMA is the first resistance and a bullish breakout would lead to a test of 76.00 which coincides with the 30-day SMA, foreshadowing a potential recovery. On the downside, a slip below 70.00 would flush out buyers and expose the recent bottom at 66.00.

US 30 attempts to rebound

The Dow Jones 30 weakened after a slew of hawkish comments from Fed officials. The index is struggling to secure a solid footing after bouncing off the psychological level of 33000. While successive breaks above 33450 and 33600 had led short-term sellers to cover and eased the downward pressure, the failure to lift offers around the triple-tested 33750 is a sign of weakness as only its breach would signal a turnaround. A tentative break below 33220 would cause a retest of 30000, potentially triggering a deeper correction.

Markets Gripped by US Debt Ceiling Talks

Asian markets gave up earlier gains on Tuesday as investors adopted a cautious stance after US debt ceiling negotiations ended "productive talks" without a deal. However, President Joe Biden and House Speaker Kevin McCarthy both expressed optimism about reaching a breakthrough to avoid a default. European futures are pointing to a positive open ahead of the preliminary PMI figures for the eurozone in May. Wall Street closed mixed and remains influenced by the US debt ceiling developments. In the currency space, the dollar crept higher drawing strength from hawkish Federal officials while gold fell for a second day amid hints of progress towards avoiding a US default.

Big week for USD

The dollar could be injected with fresh volatility this week due to the US debt limit negotiations, Fed minutes, and top-tier US economic data.

Dollar bulls were able to draw support in the previous session from the productive US debt limit talks and hawkish comments from Fed officials. Midweek, all eyes will be on the minutes from the May FOMC meeting which could offer more clues about the central bank's next move. After proceeding with a 25-basis point hike in May, the Fed signalled a potential pause. It will be interesting to see what the minutes show in regard to the thinking of policymakers and how united they were around the idea of 5.25% being the peak level of rates. Of course, we have heard from a slew of Fed officials since the meeting which could make the minutes relatively stale.

On the data front, much focus will be on the Fed’s preferred inflation gauge, the Core Personal Consumption Expenditure (PCE) scheduled to be released on Friday. The April PCE report is forecast to show headline prices rising 0.3% month-over-month after March’s 0.1% increase, while the core PCE deflator is projected to rise 0.3%, the same as March. The core personal consumption expenditures price index is seen rising 4.6% year-over-year, the same as seen in March. Any further evidence of cooling inflationary pressures may reinforce the argument around the Fed pausing and eventually cutting interest rates later in 2023.

Currency spotlight – GBP/USD

GBPUSD could see more weakness if the pending UK inflation data on Wednesday shows signs of cooling inflationary pressures. Markets forecast inflation cooling to 8.2% in April, down from the 10.1% in March. If expectations match reality, this would be the sharpest decline in more than 30 years, bringing an end to seven consecutive months of double-digit inflation. Looking at the technical picture, GBPUSD may slip towards 1.2370 on expectations around the BoE potentially pausing rate hikes. A solid breakdown below 1.2370 could signal a further selloff towards 1.2280. If prices push back above 1.2450, bulls may target 1.2550.

Commodity spotlight – Gold

Gold prices got no love on Tuesday morning, shedding 0.5% as optimism over the US debt ceiling developments dampened its allure. This promises to be another volatile week for the precious metal thanks to the cocktail of risk events and economic releases. If US debt talks continue to head in the right direction and hopes continue to rise over a deal reached, this could drag prices lower as risk appetite returns. Expect gold to also be influenced by the Fed minutes and key US data including the inflation report on Friday. Focusing on the technicals, sustained weakness below $1970 may open a path toward $1945 and $1900 respectively. Bulls need to claw their way back above $2000 to get back into the game.

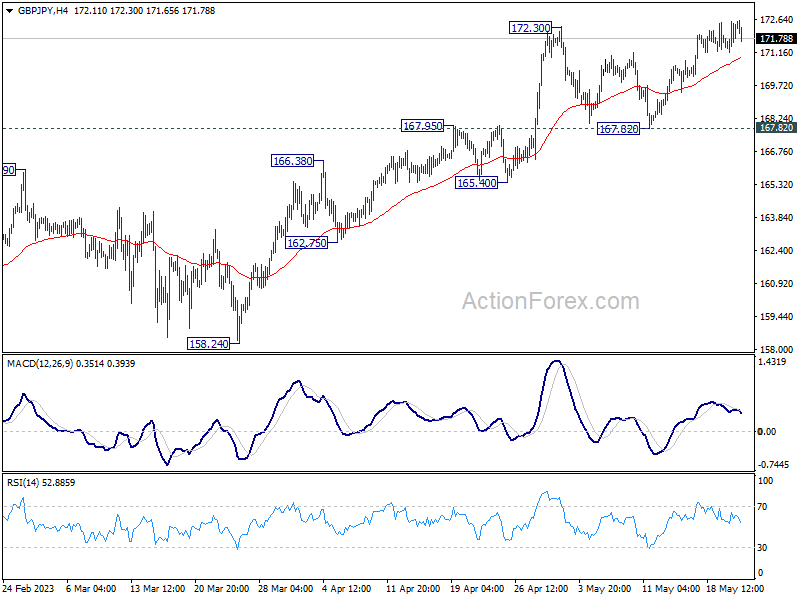

GBP/JPY Daily Outlook

Daily Pivots: (S1) 171.52; (P) 172.05; (R1) 172.90; More...

GBP/JPY's rally is still in progress, as part of the larger up trend, and should target 100% projection of 148.93 to 172.11 from 155.33 at 178.51. Nevertheless, firm break of 167.82 support should confirm short term topping, and turn bias back to the downside for deeper pull back to 165.40 support and possible below instead.

In the bigger picture, focus stays on 172.11 resistance (2022 high). Decisive break there will resume whole up trend from 123.94 (2020 low). Next target will be 161.8% projection of 122.75 (2016 low) to 156.59 (2018 high) from 123.94 at 178.69. Nevertheless, firm break of 165.40 support will indicate rejection by 172.11 and extend the corrective pattern from there with another falling leg.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 149.15; (P) 149.54; (R1) 150.23; More....

EUR/JPY's rebound from 146.12 is still in progress. Further rise could be seen for retesting 151.60 high. Decisive break there will resume larger up trend. On the downside, however, break of 146.12 will resume the fall to 61.8% retracement of 139.05 to 151.60 at 143.84.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64. Sustained break there will pave the way to 100% projection at 162.82. For now, medium term outlook will remain bullish as long as 139.05 support holds, even in case of deep pull back.

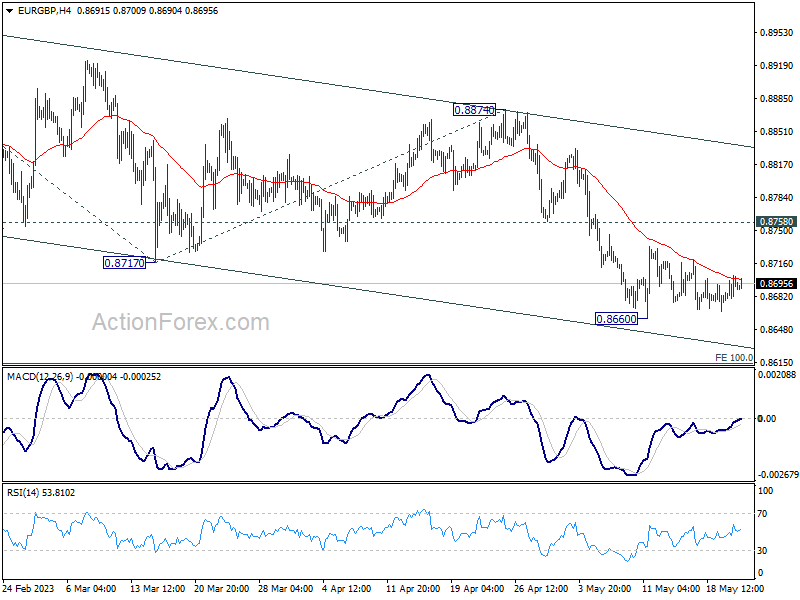

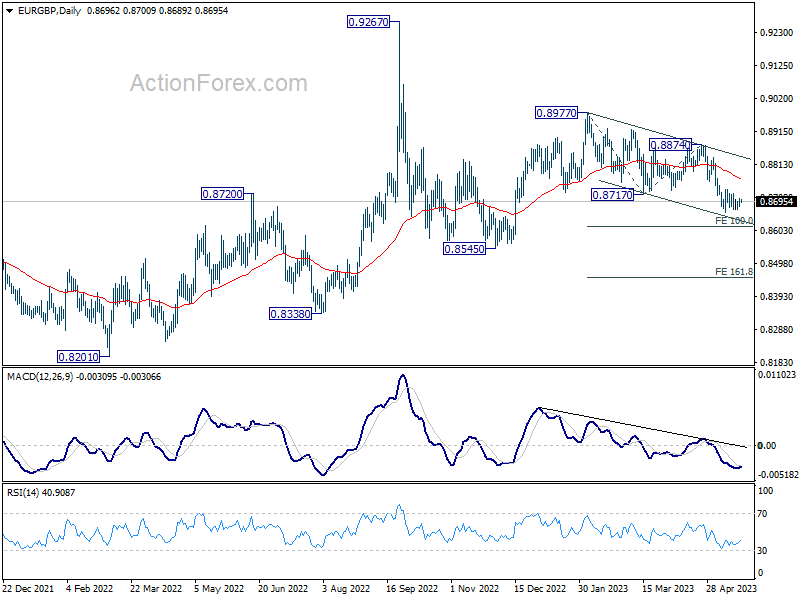

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8681; (P) 0.8692; (R1) 0.8706; More...

EUR/GBP is staying in consolidation from 0.8660 and intraday bias remains neutral. Further decline is expected as long as 0.8758 resistance holds. On the downside, break of 0.8660 will resume recent decline from 0.8977 to 100% projection of 0.8977 to 0.8717 from 0.8874 at 0.8614. Nevertheless, break of 0.8758 minor resistance will turn bias back to the upside for stronger rebound.

In the bigger picture, current development argues that whole decline from 0.9267 (2022 high) is still in progress. This is part of the long term range pattern from 0.9499 (2020 high). Deeper fall would be seen through 0.8545 support. This will now remain the favored case as long as 0.8874 resistance holds.

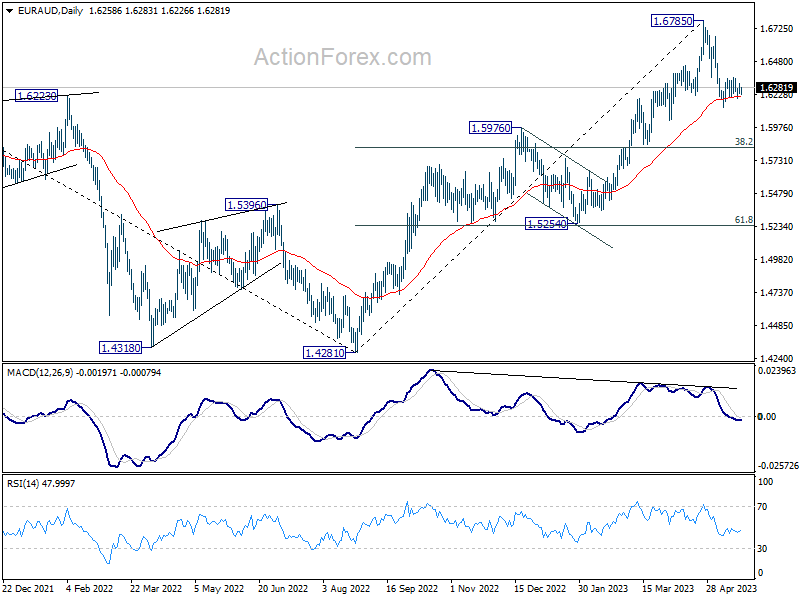

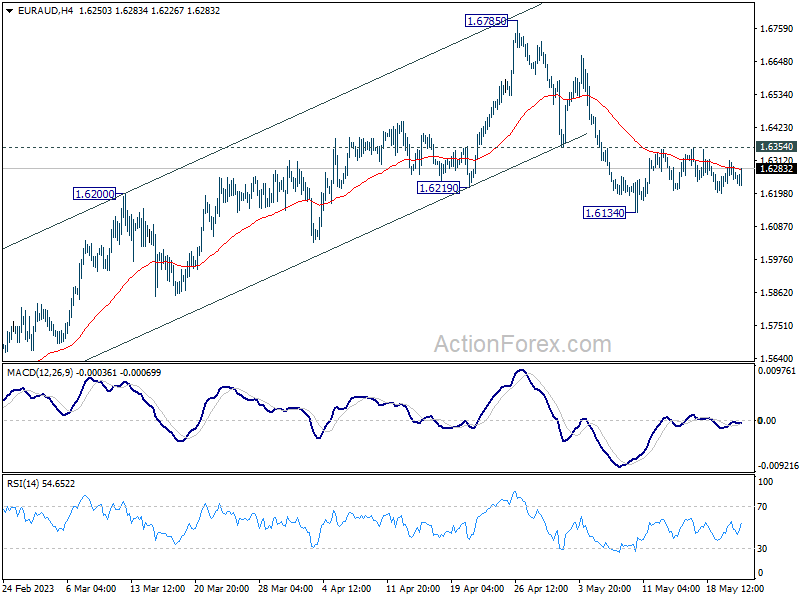

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6224; (P) 1.6268; (R1) 1.6299; More...

Range trading continues in EUR/AUD and intraday bias remains neutral. Fall from 1.6785 might be a correction to whole up trend from 1.4281. Break of 1.6134 will target 38.2 retracement of 1.4281 to 1.6785 at 1.5828, which is inside 1.5254/5976 support zone. Nevertheless, sustained break of 1.6354 minor resistance will turn bias back to the upside for retesting 1.6785 high instead.

In the bigger picture, whole down trend from 1.9799 (2020 high) should have completed at 1.4281 (2022 low). Further rise should be seen to 61.8% retracement of 1.9799 to 1.4281 at 1.7691 next. For now, outlook will stay bullish as long as 1.5976 resistance turned support holds, even in case of deep pull back.