Sample Category Title

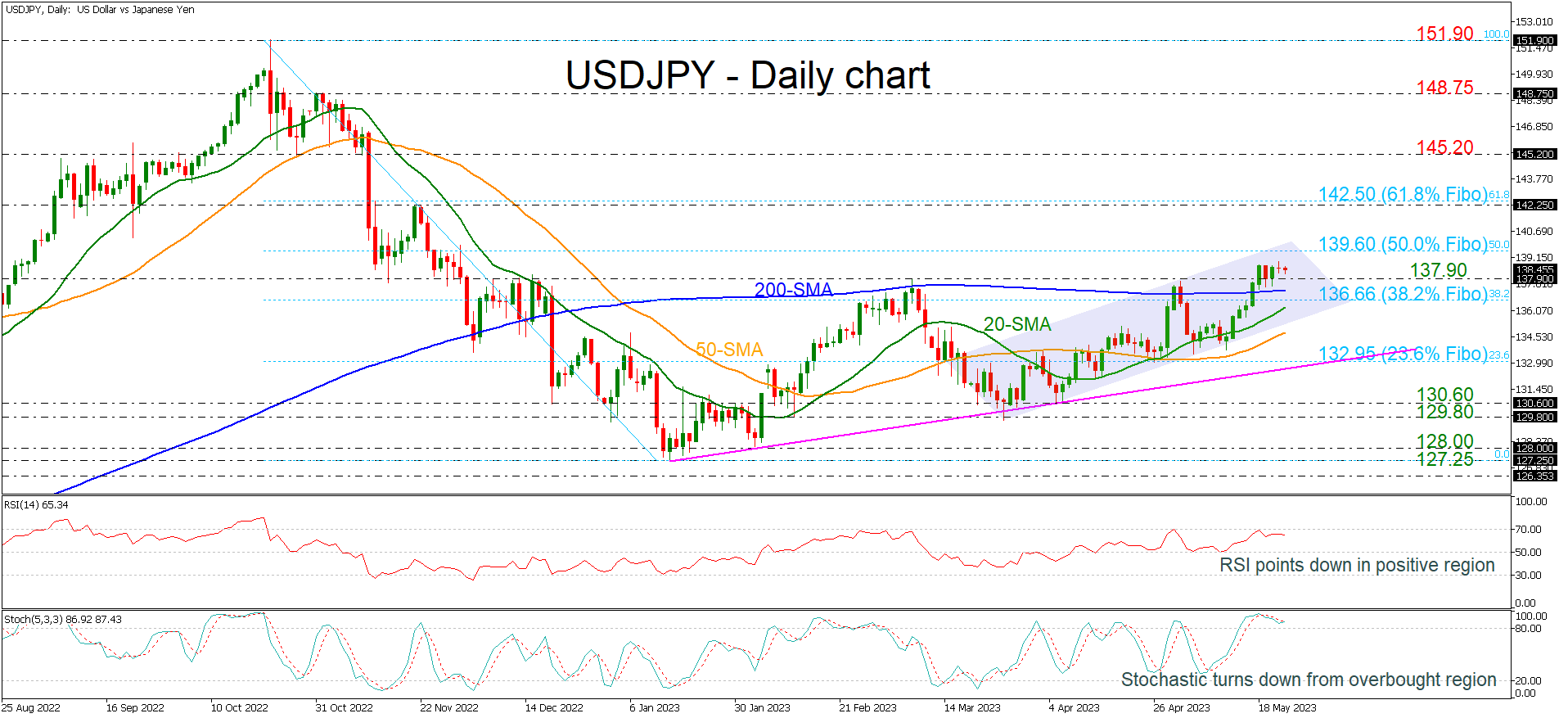

USDJPY Remains Above 200-SMA and Within Upward Channel

USDJPY is holding above the key 137.90 level and the 200-day simple moving average (SMA), suggesting that more bullish actions could come within the short-term upward sloping channel.

However, the technical oscillators are showing some weakness as the RSI is pointing down, failing to jump above the 70 level and the stochastic oscillator is flattening in the overbought region, indicating an overstretched market. In trend indicators, the bullish crossover within the 20- and the 50-day SMAs remains in place.

Should USDJPY make another run higher, it’s likely to meet resistance at the 50.0% Fibonacci retracement level of the downward wave from 151.90 to 127.25 at 139.60. A successful break above this resistance area would open the way for the 142.25 barrier and the 61.8% Fibonacci at 142.50.

If the soft positive momentum fails to hold and prices turn lower, the 137.90 level and the 200-day SMA at 137.20 are the nearest supports that could halt steeper declines. A potentially important support, though, is the 38.2% Fibonacci at 136.66 as well as the short-term SMAs at 136.20 and 134.85. If breached, it would shift the focus to the downside and prices would slip towards the 23.6% Fibonacci of 132.95.

In the bigger picture, USDJPY would need to make a sustained climb above the 50.0% Fibonacci of 139.60 in order for the outlook to become convincingly bullish.

Gold Tries to Bounce

USD/CHF bounces back

The US dollar finds support from recovering Treasury yields in the wake of hawkish Fed comments lately. Having seemingly bottomed out near January 2021’s lows at 0.8820, the pair could start to recover some lost ground. 0.8960 is the latest support and a bullish MA cross on the daily chart is an encouraging sign and could attract market participants who dread missing the rebound. After clearing the psychological level of 0.9000, 0.9060 would be the next hurdle where a subsequent breakout would lead to a runaway rally.

EUR/GBP struggles to bounce

The euro softened after May’s manufacturing PMI showed signs of easing across the bloc. The bulls have been trying to hold against the bears’ repeated attempts to push below 0.8660. A breakout would expose last December’s lows around 0.8560. 0.8720 on the 20-day SMA is a major ceiling and a shooting star in this supply zone indicates a lingering selling pressure. An invalidation of 0.8690 has forced short-term buyers to bail out and put sellers back on the driver’s seat instead, turning the level into a fresh resistance.

XAU/USD tests resistance

Gold rebounds amid a lack of breakthrough in the latest US debt ceiling talks. A fall below the daily support of 1980 has dented the bullish mood, prompting buyers to trim their exposure in fear of a deeper pullback. A bearish MA cross on the daily chart combined with a faded rebound at the demand-turned-supply zone around 1984 suggests that the path of least resistance could be down. A drop below 1950 would renew the selling pressure and make 1920 the next stop. 2012 is the ceiling to lift before the rally could resume.

Watch Out, You Bears

Debt ceiling talks in the US led to some progress, but no deal was reached yesterday. The two sides are apparently close in some areas – they both want to avoid a default – but the Republicans need ‘some movement or some fundamental change’ on the White House deck. Republicans want to slash spending over as long as possible, while Democrats offer little cuts over a couple of years. But the time is ticking louder as the US Treasury’s General Account goes south at a decent pace, and the US will soon run out of money to pay its bills.

And even though there is a strong belief that the US politicians are not foolish to trigger a self-induced economic crisis and that they will reach a deal just before time, appetite in risk assets looks weakened. Both the S&P 500 and Nasdaq lost more than 1% yesterday, while the US 2-year yield spiked to 4.40%, though it’s sharply lower this morning. Gold somehow struggles gathering positive momentum, and even the Swiss franc doesn’t benefit from safe haven inflows, as the US dollar is where investors seek refuge – as absurd as it sounds.

Watch out, you bears

Crude oil performed well on Tuesday despite the US debt ceiling shenanigans, as the Saudi Prince Abdulaziz bin Salman warned oil bears to watch out. The prince said speculators will be ouching ‘as they ouched in April’, that he doesn’t need to show his cards because he is not a poker player, but that he would just tell them to watch out.

In summary, bin Salman gave a clear hint that OPEC is preparing to announce another output cut when it meets at the beginning of June.

US crude jumped more than 2% yesterday after his warnings. There is a good chance that the oil bears will gently turn neutral into the OPEC announcement, and that we will see the price of a barrel test the 50 and 100-DMA to the upside.

But it’s important to note that any OPEC-induced boost to oil prices will likely remain short lived. The 200-DMA, which stands a touch below the $80pb level, will likely continue act as a solid resistance to any rally in the short run.

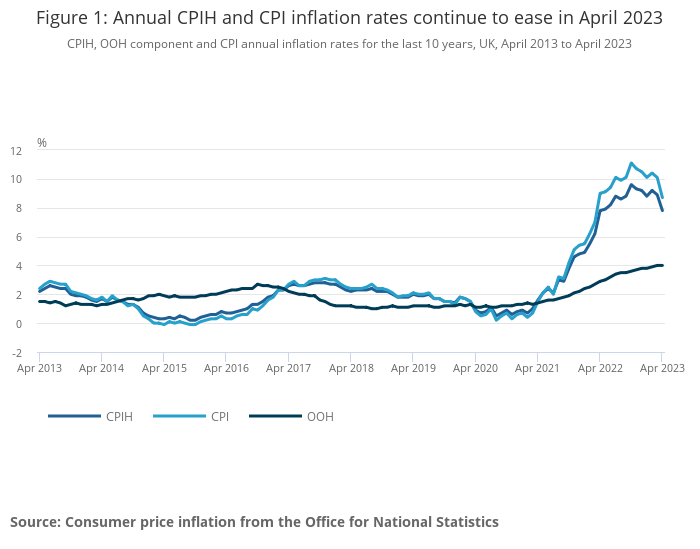

UK inflation slows, but less than expected

In May, both manufacturing and services PMI were lower than expected and lower than the previous readings in Britain. Yet, service-sector companies reported the fastest increase in cost pressures in 3 months.

Released this morning, the latest CPI fell less than expected by analysts while core inflation spiked to 6.8% unexpectedly, hinting that the Bank of England (BoE) will unlikely see inflation slump as fast as it expects in the second half of the year, and more rate hikes could be needed in the UK.

But maybe not in New Zealand. Even though the Reserve Bank of New Zealand raised interest rates to the highest levels in more than 14 years pointing at inflation that ‘remains too high’, the bank’s forecasts signaled that its tightening cycle has peaked amid an unexpected GDP contraction of 0.6% in Q4 of 2022 and a subdued near-term outlook for activity. The kiwi-dollar took a dive following the decision and is preparing to test the 200-DMA.

Debt Ceiling Anxiety Grows

Market movers today

Today we get IFO figures, which will shed some more light on the German growth momentum, after PMI figures yesterday further intensified the two-speed economy narrative.

In the FOMC minutes, focus will be on the banking sector turmoil and how it is seen affecting the monetary policy outlook, and any hints on the future policy rate outlook.

We will also keep an eye on UK April CPI inflation. Energy is set to drag headline inflation significantly lower. This is the first of two inflation prints ahead of the next BoE meeting where we expect a 25bps hike.

The 60 second overview

Macro: The release of US flash PMIs for May was a mixed bag. The manufacturing sector index fell below 50 again, while the service sector index rose to 55.1 - the highest level in a year.

US: Talks to solve the debt ceiling problem continued yesterday showing some progress, but no result. Meanwhile anxiety in the Treasury bills market grows with front-end bills briefly topping 6% yesterday. The market eyes 1 June as the potential X-date, when the US government risks running out of money. The yield on the Treasury bill maturing 1 June rose 2.5pp above the yield on the bill maturing 30 May yesterday.

New Zealand: Another major central bank looks done raising interest rates. The Reserve Bank of New Zealand hiked its key policy rate 25bp to 5.5% overnight and signalled an end to monetary policy tightening.

Equities: Equities retreated on Tuesday, backed by weak data. The sell-off intensified in the US session, with S&P and Nasdaq closing south of -1%. Most sectors were lower and performance was tightly bunched. Almost all cyclicals a percent lower, while defensives (energy, utilities, staples) fared better together with regional banks. VIX rose to 18.5. Europe was a little different, as real estate stocks jumped 2% and banks continued its rebound. But in sum, a pretty harsh reaction to the numbers. Futures are a tad lower again.

FI: There have been modest movements in US Treasury yields. The US Treasury curve flattened a few bp from the long end as the uncertainty regarding a deal on the Debt Ceiling increased. There were only modest moves in the EGB markets that were dominated by issuance from Germany and Netherlands as well as the new 15Y Italian linker sold through syndication.

FX: The US dollar gained ahead IFO and FOMC Minutes and continued uncertainty about the debt ceiling, while diverging flash PMIs between the euro area and the US added fundamental support for EUR/USD moving lower, below the 1.08 mark. Also CNH loses ground vs the USD. GBP eyes today's inflation numbers. As for the Scandies there is no relief yet, with EUR/SEK in the mid-11.40s and EUR/NOK testing above 11.80.

Credit: Yesterday the credit markets were trading sideways exemplified by the iTraxx main tightening by 1bp to 82bp while the Xover index widened by 2bp to 433bp. All this happened under a continued flurry of new issues from both financials and non-financials. Noticeable deals included the Finnish nuclear operator TVO, which printed a 7-year EUR600m bond at MS+165bp corresponding to a yield of 4.8%.

Nordic macro

Denmark. The Danish government has raised its estimate for the structural budget balance by 0.4% of GDP for every year from now until at least 2030. This will allow it to increase spending or lower taxes by about DKK 12bn a year without violating its structural deficit targets. The change comes after many years of actual budget surpluses far above expectations, and in that light, the new estimate still looks cautious.

Sweden. Riksbank's deputy governor Jansson (hawk) will participate in a breakfast seminar and discuss the economic situation (CET 8:00). Yesterday's speech by governor Thedéen did not provide any new insights.

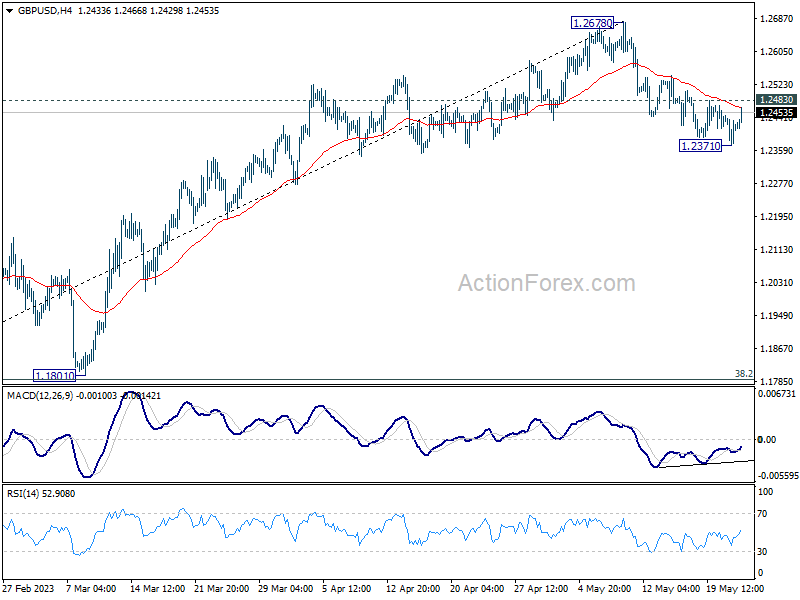

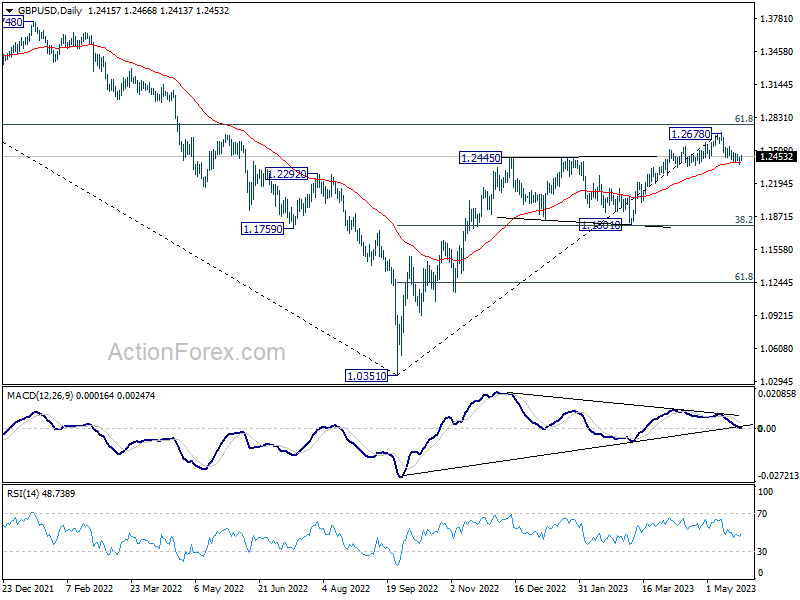

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2376; (P) 1.2412; (R1) 1.2450; More...

Intraday bias in GBP/USD is turned neutral with current recovery. Another fall is expected as long as 1.2483 resistance holds. Break of 1.2371, and sustained trading below 55 D EMA (now at 1.2397) will confirm that it's in correction to whole up trend from 1.0351. Deeper fall should then be seen to 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789). On the upside, however, break of 1.2483 resistance will bring stronger rebound back to retest 1.2678 high instead.

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

GBP Bounces on CPI, NZD Down after RBNZ

New Zealand Dollar falls broadly today as the markets considered the RBNZ rate hike as a dovish one, probably with interest rate already peaked. The development also takes Aussie lower too. Meanwhile, Sterling is attempting a bounce after strong core CPI reading, as well as services prices. But buyers of the Pound appear to be hesitating for now. Euro is also slightly firmer but there is no apparent momentum except versus commodity currencies. Dollar and Yen are mixed, awaiting further guidance from overall risk sentiment.

Technically, one focus for the rest of the day would be on whether Sterling could extend its rebound attempt. EUR/GBP has already breached 0.8660 temporary low too, and it's on track to resume the decline from 0.8977. Levels to watch include 1.2483 minor resistance in GBP/USD, and 172.60 temporary top in GBP/JPY. Break of these levels would mark a stronger come back in the Pound.

In Asia, Nikkei closed down -0.89%. Hong Kong HSI is down -1.17%. China Shanghai SSE is down -0.89%. Singapore Strait Times is down -0.30%. Japan 10-year JGB yield is up 0.0089 at 0.413. Overnight, DOW dropped -0.69%. S&P 500 dropped -1.12%. NASDAQ drooped -1.26%.

UK CPI slowed to 8.7%, CPI core rose to highest since 1992

UK CPI slowed from 10.1% yoy to 8.7% yoy in April, above expectation of 8.2% yoy. On a monthly basis, CPI rose by 1.2% mom, above expectation of 0.8% mom.

CPI core (excluding energy, food, alcohol and tobacco) rose from 6.2% yoy to 6.8% yoy, above expectation of 6.2% yoy. That's the highest level since March 1992.

CPI goods annual rate eased from 12.8% yoy to 10.0% yoy, while the CPI services annual rate rose from 6.6% yoy to 6.9% yoy.

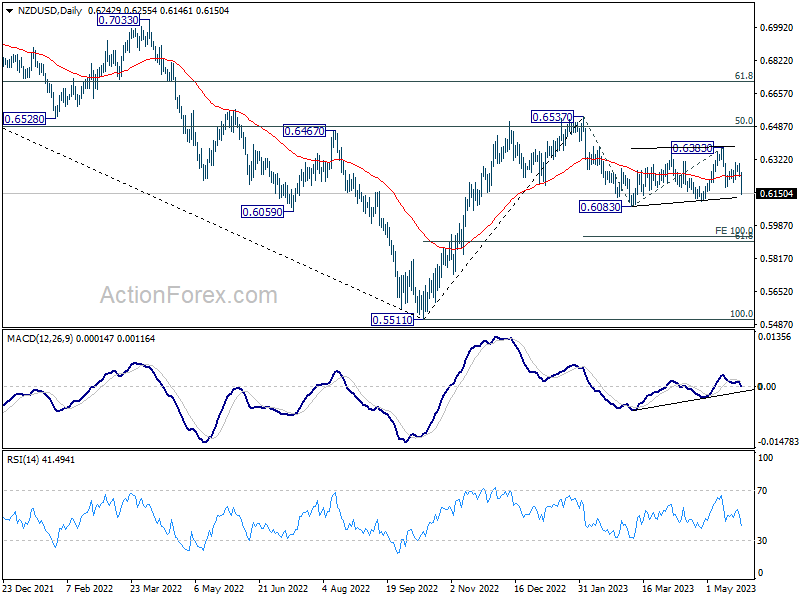

NZD/USD dives after dovish RBNZ hike

RBNZ raised OCR by 25bps to 5.50% today, reaching the projected peak interest rate. The decision was made by a 5-2 vote, with two committee members voted for no change. The central bank noted that "The OCR will need to remain at a restrictive level for the foreseeable future, to ensure that consumer price inflation returns to the 1% to 3% annual target range, while supporting maximum sustainable employment."

The overall announce was seen as being dovish by the markets, sending New Zealand Dollar broadly lower. NZD/USD's break of 0.6181 support confirms resumption of the decline from 0.6383 for retesting 0.6083/0.6110 support zone.

More importantly, the development is inline with the view that corrective pattern from 0.6083 has completed with three waves up to 0.6383. That is, the decline from 0.6537 might be ready to resume too. Firm break of 0.6083 will target 100% projection of 0.6537 to 0.6083 from 0.6383 at 0.5929.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2376; (P) 1.2412; (R1) 1.2450; More...

Intraday bias in GBP/USD is turned neutral with current recovery. Another fall is expected as long as 1.2483 resistance holds. Break of 1.2371, and sustained trading below 55 D EMA (now at 1.2397) will confirm that it's in correction to whole up trend from 1.0351. Deeper fall should then be seen to 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789). On the upside, however, break of 1.2483 resistance will bring stronger rebound back to retest 1.2678 high instead.

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Q/Q Q1 | -1.40% | 0.20% | -0.60% | -1.00% |

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q1 | -1.10% | -1.00% | -1.30% | -1.60% |

| 00:30 | AUD | Westpac Leading Index M/M Apr | 0.00% | 0.00% | ||

| 02:00 | NZD | RBNZ Rate Decision | 5.50% | 5.50% | 5.25% | |

| 03:00 | NZD | RBNZ Press Conference | ||||

| 06:00 | GBP | CPI M/M Apr | 1.20% | 0.80% | 0.80% | |

| 06:00 | GBP | CPI Y/Y Apr | 8.70% | 8.20% | 10.10% | |

| 06:00 | GBP | Core CPI Y/Y Apr | 6.80% | 6.20% | 6.20% | |

| 06:00 | GBP | RPI M/M Apr | 1.50% | 1.70% | 0.70% | |

| 06:00 | GBP | RPI Y/Y Apr | 11.40% | 11.20% | 13.50% | |

| 06:00 | GBP | PPI Input M/M Apr | -0.30% | -0.50% | 0.20% | |

| 06:00 | GBP | PPI Input Y/Y Apr | 3.90% | 3.80% | 7.60% | 7.30% |

| 06:00 | GBP | PPI Output M/M Apr | 0.00% | -0.10% | 0.10% | 0.00% |

| 06:00 | GBP | PPI Output Y/Y Apr | 5.40% | 7.40% | 8.70% | 8.50% |

| 06:00 | GBP | PPI Core Output M/M Apr | 0.00% | 0.10% | 0.30% | |

| 06:00 | GBP | PPI Core Output Y/Y Apr | 6.00% | 7.30% | 8.50% | 8.30% |

| 08:00 | EUR | Germany IFO Business Climate May | 93.4 | 93.6 | ||

| 08:00 | EUR | Germany IFO Current Assessment May | 95.2 | 95 | ||

| 08:00 | EUR | Germany IFO Expectations May | 91.7 | 92.2 | ||

| 14:30 | USD | Crude Oil Inventories | 1.5M | 5.0M | ||

| 18:00 | USD | FOMC Minutes |

UK CPI slowed to 8.7%, CPI core rose to highest since 1992

UK CPI slowed from 10.1% yoy to 8.7% yoy in April, above expectation of 8.2% yoy. On a monthly basis, CPI rose by 1.2% mom, above expectation of 0.8% mom.

CPI core (excluding energy, food, alcohol and tobacco) rose from 6.2% yoy to 6.8% yoy, above expectation of 6.2% yoy. That's the highest level since March 1992.

CPI goods annual rate eased from 12.8% yoy to 10.0% yoy, while the CPI services annual rate rose from 6.6% yoy to 6.9% yoy.

NZD/USD dives after dovish RBNZ hike

RBNZ raised OCR by 25bps to 5.50% today, reaching the projected peak interest rate. The decision was made by a 5-2 vote, with two committee members voted for no change. The central bank noted that "The OCR will need to remain at a restrictive level for the foreseeable future, to ensure that consumer price inflation returns to the 1% to 3% annual target range, while supporting maximum sustainable employment."

The overall announce was seen as being dovish by the markets, sending New Zealand Dollar broadly lower. NZD/USD's break of 0.6181 support confirms resumption of the decline from 0.6383 for retesting 0.6083/0.6110 support zone.

More importantly, the development is inline with the view that corrective pattern from 0.6083 has completed with three waves up to 0.6383. That is, the decline from 0.6537 might be ready to resume too. Firm break of 0.6083 will target 100% projection of 0.6537 to 0.6083 from 0.6383 at 0.5929.

(RBNZ) Official Cash Rate (OCR) set to remain restrictive

The Monetary Policy Committee today voted to raise the Official Cash Rate (OCR) from 5.25% to 5.50%.

The Committee agreed the level of interest rates are constraining spending and inflation pressure. The OCR will need to remain at a restrictive level for the foreseeable future, to ensure that consumer price inflation returns to the 1% to 3% annual target range, while supporting maximum sustainable employment.

Global economic growth remains weak and inflation pressures are easing. This follows a period of significant monetary policy tightening by central banks internationally. International supply chain constraints have also eased following a period of disruption, and shipping costs have declined. The weaker global growth has led to lower export prices for New Zealand's goods.

In New Zealand, inflation is expected to continue to decline from its peak and with it measures of inflation expectations. However, core inflation pressures will remain until capacity constraints ease further. While employment is above its maximum sustainable level, there are now signs of labour shortages easing and vacancies declining.

Consumer spending growth has eased and residential construction activity has declined, while house prices have returned to more sustainable levels. More generally, businesses are reporting slower demand for their goods and services, and weak investment intentions. Businesses report that a lack of demand, rather than labour shortages, is now the main constraint on activity.

There has been a return of net inward migration since international borders reopened. The Committee expects the pace of immigration to ease back toward pre-COVID-19 trend levels over coming quarters. While immigration has assisted to ease labour shortages, its net impact on overall spending is uncertain. The recent recovery in tourism spending, to around three-quarters of its pre-COVID-19 trend level, is also supporting demand.

The repair and rebuild facing significant regions of the North Island — due to the recent severe weather events — will support economic activity, in particular the horizontal construction sector. The timing of this predominantly government investment will be spread over several years. Broader government spending is anticipated to decline in inflation-adjusted terms and in proportion to GDP. The Committee is confident that with interest rates remaining at a restrictive level for some time, consumer price inflation will return to within its target range of 1% to 3% per annum, while supporting maximum sustainable employment.

Read the May 2023 Monetary Policy Statement

Media contact

James Weir

Senior Advisor, External Stakeholders

Phone:021 103 1622

Email: james.weir@rbnz.govt.nz

Summary record of meeting

The Committee discussed recent developments in the New Zealand economy. The Committee agreed that monetary conditions are restricting spending and reducing inflationary pressure. However, current inflation remains high and spending will have to continue to slow to better match the supply capacity of the economy, so that consumer price inflation returns to its target range. While employment indicators reflect easing capacity pressures, they remain elevated.

Global economic growth has slowed below trend for most of our key trading partners. The Committee noted this weakness has been reflected in slowing demand for our goods exports, as seen in lower dairy and meat prices. For a number of years, COVID-19 and the war in Ukraine have constrained global production, disrupted supply chains, and increased shipping costs. These global supply bottlenecks have eased and commodity prices – in particular oil prices – have remained below their peaks in early 2022. Overall, headline inflation is continuing to decline amongst our key trading partners. Nevertheless, core inflation remains elevated in most of our trading partner economies.

Members discussed developments in global financial markets. Recent banking stress in the United States and Europe has been contained by regulators so far but has added to financial market volatility, tighter credit conditions, and uncertainty regarding the global economic outlook. The impacts from these events on domestic financial conditions have been limited to date, and the New Zealand banking system is sound.

The Committee discussed domestic economic developments. Economic activity in New Zealand contracted by 0.6% in the December 2022 quarter. This contraction was unexpected. Business and residential investment and overall government spending contracted in the December 2022 quarter, and domestic spending remained flat. The near-term outlook for activity remains subdued.

In addition, annual CPI inflation was lower than assumed in the February Statement, easing to 6.7% in the March 2023 quarter. Short-term price pressure from recent severe weather events appears to have been less than initially assumed. Both annual non-tradables and tradables inflation were lower than expected, with a reduction in tradables inflation accounting for a larger share of the overall decline in inflation.

Members discussed the evidence that demand is slowing in those parts of the economy that are most sensitive to higher interest rates. The constraining impact of higher interest rates has been most visible in spending and economic activity related to housing. Residential investment has started to ease and falling consent numbers suggest it will continue to slow. Feedback from the industry suggests the pipeline of future building activity is subdued. The rebuild work following the recent floods is assumed to provide a small offset to this decline.

Members also discussed the impact interest rate increases were having on the housing market and household spending. House prices have continued to decline, while first home buyers were accounting for a larger share of new home purchases. Overall, current monetary policy is supporting a moderation in house prices to more sustainable levels. The wealth effects from this decline in house prices have contributed to slowing spending on durable goods since early 2022. In addition, the rate of credit growth for households has declined.

The Committee discussed evidence that elevated interest rates were constraining business activity. Businesses are reporting a general slowing in demand, a weaker outlook for investment, and business credit growth has declined. Businesses are also reporting that orders are now the main constraint on activity – after a period of it being labour availability.

The Committee noted that while the total number of international visitors remains below pre-COVID-19 levels, its recovery since the border was reopened has supported aggregate demand.

Members discussed the recent increase in net inward migration. The projections incorporate a stronger starting point for net inward migration. The Committee discussed what this stronger starting point for migration means for the economy. Overall, it suggests that spending and activity have been subdued, even in an environment of strong population growth. The increase in net inward migration is providing some relief in a very tight labour market, but the net impact on demand – including for housing – is uncertain, as is the impact on inflationary pressure.

Members noted this increase in migration is assumed to be temporary. Migration is assumed to fall back towards the average inflows seen in the years preceding COVID, and settle at an inflow of around 36,000 working age people per year. While the recent increase may partly reflect some pent-up demand to migrate to New Zealand, immigration rules have also been eased to alleviate acute labour shortages in some sectors. The Government recently made it temporarily possible for some migrants on work visas who had already been living in New Zealand for a period to apply for a special resident class visa. Given these new residents would have already been participating in the economy and the housing market as renters, it is expected this change will add only modest pressure to housing demand.

The Committee discussed likely economic impacts of recent severe weather events. Public infrastructure was significantly damaged. Clean-up, repair and rebuild work continues. While estimates are uncertain, the Committee assumes the recovery from these events will add about 1.5 percent to GDP spread out over a number of years.

Members discussed the impact of Budget 2023. Fiscal policy is projected to add to demand over the 2023/24 fiscal year, then dampen demand in subsequent years. Overall, fiscal policy will be contractionary on demand over the projection horizon. This reflects that government consumption, which is the larger share of government spending, is expected to fall as a share of GDP in coming years. Government investment is expected to continue to grow, in part due to the repair and rebuild work in the aftermath of the weather events. Fiscal policy is projected to be less contractionary than the Committee had assumed in February.

The Committee also discussed the functioning of the New Zealand Government bond market. This was particularly in the context of an expansion to the New Zealand Treasury's bond issuance programme, and ongoing sales of bonds in the Large Scale Asset Purchase Programme portfolio. Overall, the market continues to function in line with historic norms. Notably spreads between government bond and swap rates have remained relatively stable.

The Committee discussed the New Zealand labour market. Employment is above its maximum sustainable level. The unemployment rate was 3.4% in the March 2023 quarter, still near record lows. However, same-job wage inflation was weaker than expected. The majority of maximum sustainable employment measures are now pointing to less labour market capacity pressure relative to March last year. Firms are reporting that labour is now less of a constraint to production. In addition, measures of skilled and unskilled labour shortages have eased.

Members discussed inflation expectations. Measures of the inflation expectations of businesses have eased, while household inflation expectations moved higher. It was noted that there was increasing evidence that New Zealand households were putting greater weight on recent past inflation outturns when setting their inflation expectations. This has likely contributed to persistence in domestic inflationary pressure as inflation has risen.

The Committee discussed evidence that monetary conditions are having a contractionary effect on the economy. Members were confident that the interest rates faced by firms and households have constrained spending and investment for some time. This reflects the significant increase in the Official Cash Rate (OCR) that has occurred since late 2021.

The Committee then discussed if monetary conditions were contractionary enough to get inflation back to the 1-3% target in a suitable timeframe. Overall, current mortgage rates and business lending rates were restrictive, supporting a further moderation in inflation. A normalisation in bank funding costs, including increases in retail term deposit rates, is expected to support the maintenance of current mortgage rates. Some households would further limit their spending as they rolled onto higher fixed mortgage rates. Debt servicing costs for households have risen from historically low levels during the pandemic, and are projected to rise further. In addition, the usual lags of monetary policy transmission mean that the full effects of past OCR increases will still take some time to occur.

Members discussed the key economic developments they would need to see in coming quarters to remain confident that lending rates around current levels remained sufficiently contractionary. The Committee noted that the projections incorporate a moderation in inflation and inflation expectations, a continued slowing in household spending growth, and a continued moderation in global inflationary pressure.

Members discussed the key risks to the outlook for activity and inflation. Views on the outlook for the inflationary impact of migration were mixed. Some members saw the risk that strong migration inflows could persist for longer than assumed in current projections and boost spending and inflation. Other members saw the risks as more balanced. In particular, there were not yet obvious signs that high rates of migration were affecting house prices and spending – and there were reasons to believe that current strength reflects pent up demand, and will prove temporary. In addition, migration could further alleviate labour shortages. There has also been a recent change in policy settings in Australia that eases the pathway to citizenship for emigrating New Zealanders. The effect of this on both the quantity and composition of net migration has yet to be seen.

Some members saw upside risk to tourism activity. New Zealand has already experienced a strong recovery in tourism. This has occurred at a time when the arrival of tourists from China has remained weak. A recovery in tourist arrivals from China would add demand in an already supply constrained sector.

The Committee discussed risks around the outlook for inflation expectations, notably the implications of evidence that New Zealand households were putting greater weight on recent past inflation outturns when setting their inflation expectations. Some members noted this could mean inflation expectations fall faster than in past cycles, as headline inflation declines. Others noted this behaviour could be asymmetric on the downside, and core inflation could prove stickier than currently assumed.

Members also discussed risks around the pass-through of past OCR increases to activity and inflation. Some members saw the risk of stronger than expected pass-through. Most notably, a large number of households are still facing the prospect of rolling onto higher fixed rate mortgages. This could constrain spending more than currently projected.

The Committee discussed the reaction to the April monetary policy review decision. The Committee's view in April was that inflationary pressures were still elevated, with little risk of fallout from global bank failures. In addition, the Committee was of the view that rebuild activity following recent weather events would necessitate a rise in government investment. A 50 basis point OCR increase was seen as necessary to support retail interest rates, especially given the fall in wholesale rates that had occurred at the time.

The Committee discussed the stance of policy to be confirmed at this meeting and the outlook for the OCR. The Committee was comfortable with the projected forward path for the OCR. The Committee discussed the suitability of keeping the OCR on hold at 5.25% or increasing it to 5.50%. The Committee agreed that neither decision would cause unnecessary instability in output, interest rates, or the exchange rate.

Raising the OCR to 5.50% is consistent with the projections. This reflects the view that while monetary policy is having a moderating effect on demand at this point in time, a 25 basis point increase in the OCR will increase confidence that inflation falls back to the midpoint of the target band.

The case for keeping the OCR at 5.25% with the same forward projections rested on the recognition that monetary policy is having a sufficiently moderating effect on demand and inflation, and that we are yet to see the full effects of past tightening on the economy. A pause would also allow more time to assess the impact of the significant tightening, and the timing of any further increase that might be needed.

On Wednesday 24 May, the Committee took the decision to vote on the two options. By a majority of five votes to two, the Committee agreed to increase the OCR by 25 basis points from 5.25% to 5.50%.

The Monetary Policy Committee reached a consensus that interest rates will need to remain at a restrictive level for the foreseeable future, to ensure consumer price inflation returns to the 1 to 3% target range while supporting maximum sustainable employment.

Attendees:

Reserve Bank members of MPC: Adrian Orr, Christian Hawkesby, Karen Silk, and Paul Conway.

External MPC members: Bob Buckle, Peter Harris, Caroline Saunders.

Treasury Observer: Dominick Stephens.

MPC Secretary: Adam Richardson.

NZD/USD: RBNZ Less Hawkish Tilt Reinforces USD Bulls

- RBNZ hiked its official cash rate as expected by 25 bps to 5.50%

- It is the first time RB NZ’s monetary policy-setting committee went to a vote today.

- Split vote of 5 to 2 has indicated a high probability 5.50% is the terminal rate after today’s hike.

- USD bulls are playing catch-up against prior NZD’s outperformance.

The New Zealand dollar, NZD is the weakest currency against the US dollar in today’s Asian session as it tumbled by -1.10% at this time of the writing reinforced by post-RBNZ, the New Zealand central bank’s monetary policy decision to hike as expected by 25 basis points (bps) to bring the official cash rate to 5.50%, the highest level since December 2008.

Why did the NZD fall so much since the 25-bps hike by RBNZ is already priced in?

It’s all about positioning and forward guidance. Firstly, today’s monetary policy decision after the prior surprise hawkish vibe, a 50-bps hike in April 2023 has been accompanied by a split vote of 5 to 2 in RBNZ’s monetary policy committee; the first time the committee went to a vote over its decision which has signalled that official cash rate of 5.50% after today’s hike is likely the terminal rate for its current interest rate hiking cycle.

Also, the latest RBNZ’s forecasts show that the probable path of an interest rate cut cycle will only start at the beginning of Q3 2024 which indicates that monetary policy will remain restrictive for the rest of 2023 in New Zealand.

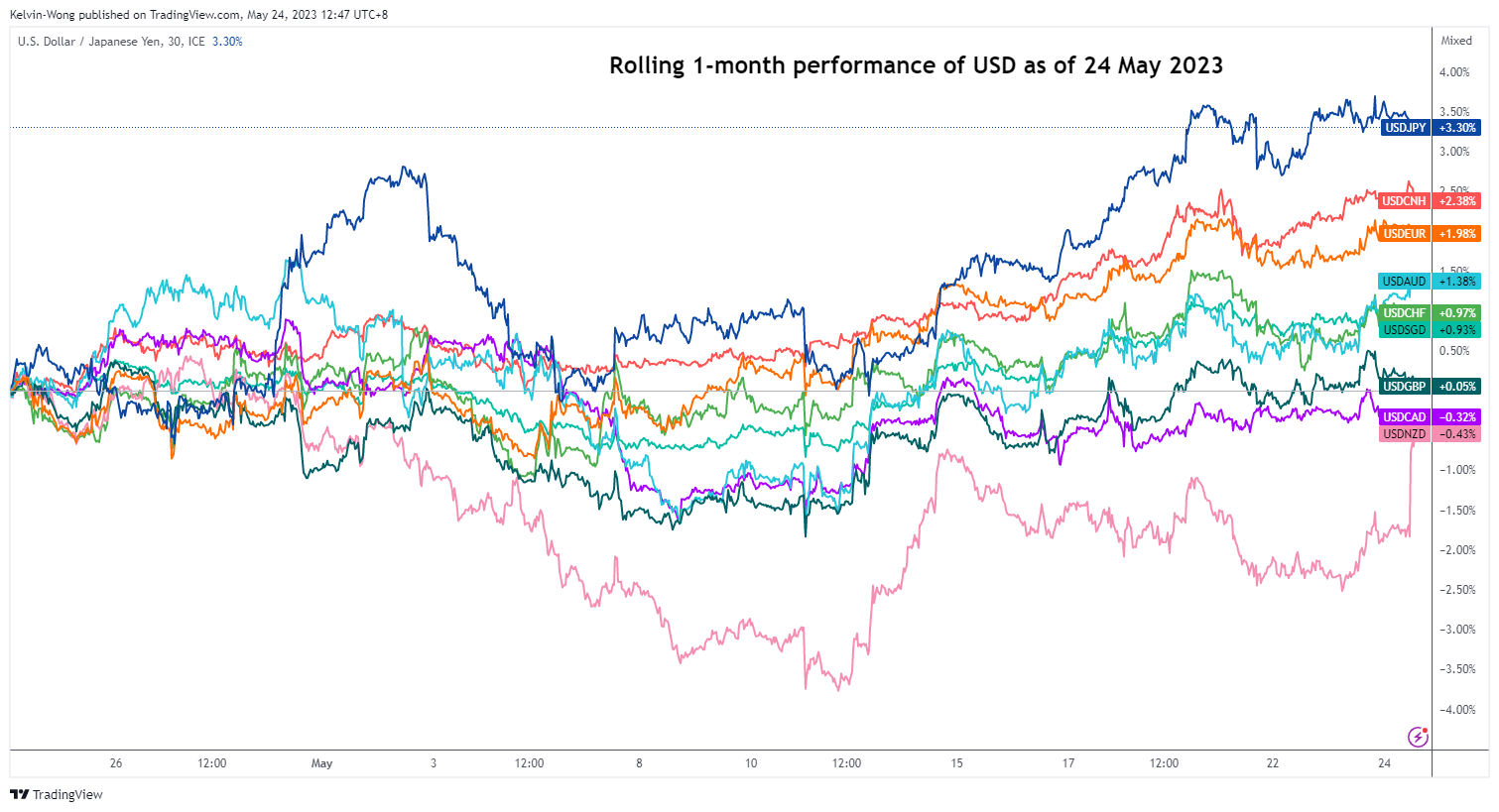

In the recent two weeks, the US dollar strength has started to creep back into the foreign exchange market where the US Dollar Index recorded its best weekly gain of +1.4% since 19 September 2022 for the week of 8 May 2023. However, the NZD was the strongest against the USD versus other major currencies in the past two weeks as seen in the rolling one-month performance cahrt below.

Thus, the sentiment that has driven the prior NZD’s outperformance has been altered easily after today RBNZ’s less hawkish surprise tilt on its forward guidance which led to a possible US dollar bullish momentum trend following systematic trading strategies to target the laggard, NZD that explains its steep movement in today’s Asian session.

NZD is now playing catch-up to the recent US dollar strength renewal

Fig 1: US dollar rolling 1-month performance against other currencies as of 24 May 2023 (Source: TradingView, click to enlarge chart)

NZD/USD Technical Analysis – Risk of a bounce within minor downtrend phase

Fig 2: NZD/USD trend as of 24 May 2023 (Source: TradingView, click to enlarge chart)

The medium-term trend of the NZD/USD as highlighted on the daily chart is trapped within a complex range configuration since its 2 February 2023 high of 0.6538 after a failure to stage a breakout above a major descending trendline resistance from its 21 October 2021 swing high of 0.7218 on 11 May 2023. The medium-term range support and resistance are at 0.6095 and 0.6315 respectively.

In the shorter term as depicted on the hourly chart, its price actions have evolved into a minor downtrend (descending channel) from its 11 May 2023 minor swing high of 0.6385. Today’s Asian session’s steep decline post RBNZ’s monetary policy outcome has led the hourly RSI oscillator to hit an extremely oversold level at 15% which suggests an overextended slide where a minor bounce cannot be ruled out at this juncture.

The key short-term pivotal resistance to watch will be at 0.6235 to maintain the minor downtrend phase with the next intermediate support at 0.6115/6095. However, a clearance above 0.6235 negates the bearish tone to see the next resistance coming in at 0.6315.