Sample Category Title

XAU/USD: The Final Impulse Continues to Build in a Bullish Zigzag

In the long term, XAUUSD forms a primary double zigzag, it consists of three main sub-waves Ⓦ-Ⓧ-Ⓨ.

Apparently, the primary sub-waves Ⓦ-Ⓧ have already been formed, and the third sub-wave Ⓨ is under development.

It is assumed that Ⓨ will acquire a standard zigzag shape. Intermediate waves (A) and (B), impulse and correction, are finished. It is likely that in the near future the price will continue to rise in the intermediate impulse (C).

Gold may rise to 2154.06. At that level, primary wave Ⓨ will be at 100% of wave Ⓦ.

According to the alternative, the impulse wave (A) has recently ended, with a long minor correction 4 having a horizontal structure.

At the moment, we can expect a decline in the price and the development of an intermediate correction (B). It is still difficult to determine which correction model wave (B) will take.

However, it is possible to determine the approximate final of wave (B). At 1910.39, the correction (B) will be at 61.8% of impulse (A). Thus, we can expect a drop to the specified level.

Gold Holds Ground

AUD/USD seeks support

The Australian dollar inches higher over accelerating inflation expectations. The selling pressure has eased after the pair cleared the support-turned-resistance at 0.6720. Then a pop above the April high of 0.6800 has prompted more sellers to cover their positions. A close back above 0.6820 would send the pair to 0.6920. The base of the latest momentum at 0.6750 is a fresh support as the aussie consolidates its latest gains. 0.6700 along the 20 and 30-day SMAs is an important support to keep the momentum current intact.

XAU/USD tests resistance

Gold weakens as easing US inflation raises hopes for a pause in the Fed's rate hikes. On the daily chart, the price is seeking to consolidate its gains after a tentative close above August 2020’s peak of 2075. A shooting star pattern showed hesitation in keeping bids at the all-time high level. Zooming into the hourly chart, a drop below the first support of 2010 has dented the impetus, causing some short-term buyers to take profit. 1980 at the base of the recent rally is a critical floor. A close back above 2055 would resume the rally.

US Oil struggles to bounce

WTI crude slides as a surprise rise in US inventory raises concerns of soft demand. A bearish MA cross on the daily chart is a sign of strong selling interests as the price gave up its recent gains. A long candle wick below the daily support of 65.50 indicated a rejection of the downside after an oversold RSI triggered a ‘buy-the-dips’ behaviour. The supply zone around 75.50 is where the bears would sell into strength due to downward inertia. A fall below 71.00 would expose 65.50 once again, potentially extending losses to 60.00.

Bank of England to Raise Policy Rate by 25 bps to 4.5%

Markets

The April US CPI release was the key focus for global trading yesterday. However, as was often the case of late, the market reaction was influenced at least as much by the reigning market bias rather than the data. With headline and core inflation at 0.4% M/M-4.9% % Y/Y and 0.4% M/M-5.5% Y/Y respectively, the easing in inflation was negligeable. A core services measure stripping out energy and housing, eased to 0.1% as was seen as a pointer for a future decline in core inflation. Higher energy and goods prices were given less weight. Whatever the assessment on the details, markets (in our view prematurely) took report as supporting the view that a Fed pause might evolve toward the end of the tightening cycle and even lead to rate cuts in H2, even as Fed governors still dismiss this scenario. US yields declined between 11.2 (2-y) and 4.2 bps. The bond rally even accelerated going into a $35 bln 10-y auction, but momentum faded after the sale (awarded 3.448% vs 3.439% WI and close to average bid-cover of 2.45). German yields at a distance followed the US decline, but with no outspoken curve move (about 6.0 bps decline across the curve). Market rumours referring to people familiar with the debate were quoted that ECB officials are starting to accept a scenario were rate hikes might continue until the September meeting. Equities intraday rebounded immediately after the CPI release but price action remained choppy (EuroStoxx50 close -0.38%, S&P500 +0.45%, Nasdaq +1.04%). The dollar lost modestly but closed of the intra-day lows (DXY 101.48, EUR/USD 1.0982).

The calendar contains US PPI and jobless claims. We only expect them to be of intraday significance for trading, with the market still more sensitive to softer rather than stronger data. Plenty of ECB members are scheduled to speak. The US will sell $21 bln of 30-y bonds. For now, the ST upside in US yields probably remains limited. The picture for the US dollar remains unconvincing. Stubbornly high inflation, strong labour data and indications that the setback in the UK economy might be milder than previously expected will ‘force’ the Bank of England to raise its policy rate by 25 bps to 4.5%. We expect the Bank to keep its conditional guidance from the March statement (If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required). This still should be seen as a soft message given recent data evidence. Sterling recently succeeded a catch-up move with EUR/GBP breaking 0.8721 support. We look out whether the BoE communication will provide a trigger for a more neutral GBP positioning, maybe even some profit taking.

News and views

The Polish central bank kept rates steady at 6.75% for an eight meeting straight. Activity has slowed down with retail sales, industrial output and construction and assembly output all dropping in annual terms in March 2023. The labour market remains strong though and unemployment is low. Inflation has eased to 14.7% in April. But it remains well above target and is still affected by companies passing through earlier commodity and supply chain-driven cost rises. The NBP remains convinced that the current monetary policy stance, the weakening of external and internal activity and the easing of external supply shocks will support the ongoing, yet gradual disinflationary process. The central bank still welcomes a stronger zloty and retains a pledge to intervene in the FX market should the currency weaken to undesirably low levels. EUR/PLN averaged around 4.7 in the first quarter of this year before impressive zloty strengthening kicked in mid-April that ran all the way to 4.55 earlier this week. The pair broke below that technically important level going into yesterday’s policy meeting with significant follow-through losses (zloty gains). EUR/PLN eventually closed at 5.518 with next zloty-resistance already looming at 4.50.

Chinese inflation eased more than expected. Prices rose at a mere 0.1% y/y, down from 0.7% in March. It’s the slowest pace in two years and even less than the 0.3% expected. Core inflation (ex. food and energy) matched the March figure of 0.7%. While some base effects are at play (inflation shot up in April last year as the Shanghai lockdown triggered new supply chain disruptions and food stockpiling), it also suggests the Chinese economy is not yet going full steam ahead after zero-Covid was buried end last year. Similar evidence came from other data too, including trade figures earlier this week. Speculation is now building that the PBOC may offer additional monetary stimulus. USD/CNY ekes out a small gain this morning but the 200dMA is limiting the scope. The pair is currently trading around 6.93, testing the April highs.

BoE Could Hardly Close the Door for Further Rate Hikes

Inflation in the US came in slightly better than expected by analysts. The headline inflation slipped below the 5% psychological mark – to 4.9%. Core inflation eased to 5.5%, and the monthly headline figure jumped to 0.4% from 0.1% printed a month earlier, as expected.

The only surprise was the yearly headline figure that slipped to 4.9%.

Falling US inflation is feeding into higher demand in treasuries. The US 2-year yield slipped back below the 4% mark on expectations that the Federal Reserve's (Fed) latest rate hike was certainly the last.

Fed rate cut expectations jumped again. The consensus is that the Fed's latest rate hike was certainly its last for this cycle, and the Fed will cut the rates by 75bp before the year ends.

Is it reasonable? Yes and no.

No, because inflation is cooling but inflation is still more than twice compared to where the Fed wants it to be, and the downside potential from the actual levels is certainly lower, as most of the decline is due to the decent fall in energy prices, which have however mostly stabilized since a couple of months now. Therefore, if we consider the inflation fight alone, the Fed should continue hiking rates.

But we also know that the bank stress is tightening credit conditions and helping the Fed to do its job – restrict credit in a way to slow growth and ease inflation.

Today, the consensus is that the Fed’s latest rate hike was certainly its last for this cycle. And if that’s the case, looking at what happened over the past 40 years, five over the past six tightening cycles ended with the Fed immediately cutting the interest rates after a peak, except in 2018 where the rates remained at peak for 5 months before being pulled down again.

In this context, expecting a rate cut in the next few months is reasonable and the negative outlook for the USD makes sense, even more so when inflation numbers hint that the trend is in the right direction.

Though I can almost guarantee you that we won’t see US inflation back at 2% anytime this year, and any time before the Fed re-starts cutting rates. This is why, the price rallies in the USD remain interesting opportunities for topsellers for a further slide toward fresh ytd lows.

BoE will hardly close the door for further rate hikes

The Bank of England (BoE) is expected to raise its interest rate by 25bp when it meets today, but it will certainly leave the door open for further hikes.

Mr. Bailey and Mr. Sunak think and communicate that inflation in Britain will fall sharply in the second half of this year. But for now, nothing, in terms of hard data, points in that direction. Released yesterday, a report from Reed showed that average wages in the UK grew 10%, matching the rise in cost of living. While that’s good news for workers, a 10% rise in salaries means that inflation will likely be stickier and harder to combat and require further rate hikes.

On the currency front, the divergence between the Fed – which is getting concrete results on its inflation fight, and the BoE – which still deals with double-digit inflation, should support the medium term bullish outlook for Cable. The pair is about to break above a long-term down-trending channel top, if successful, we could see traders set their eyes back on the 1.30 mark.

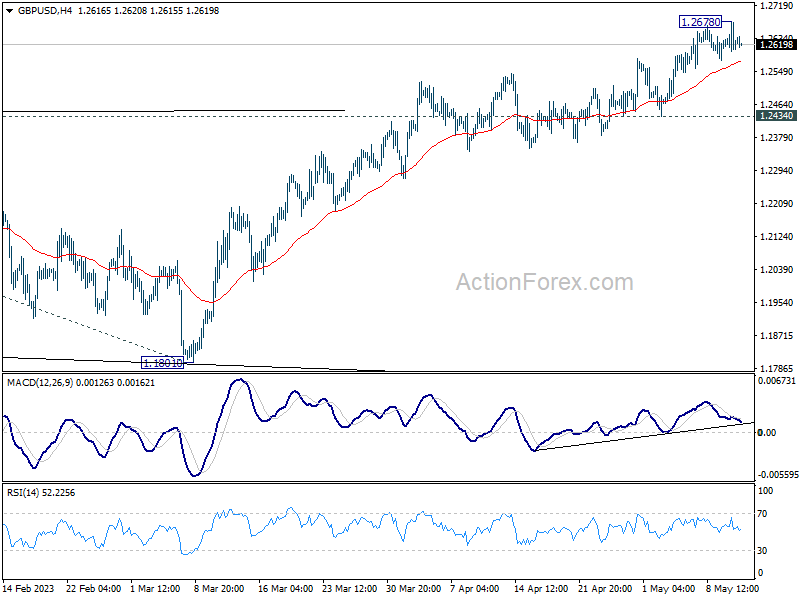

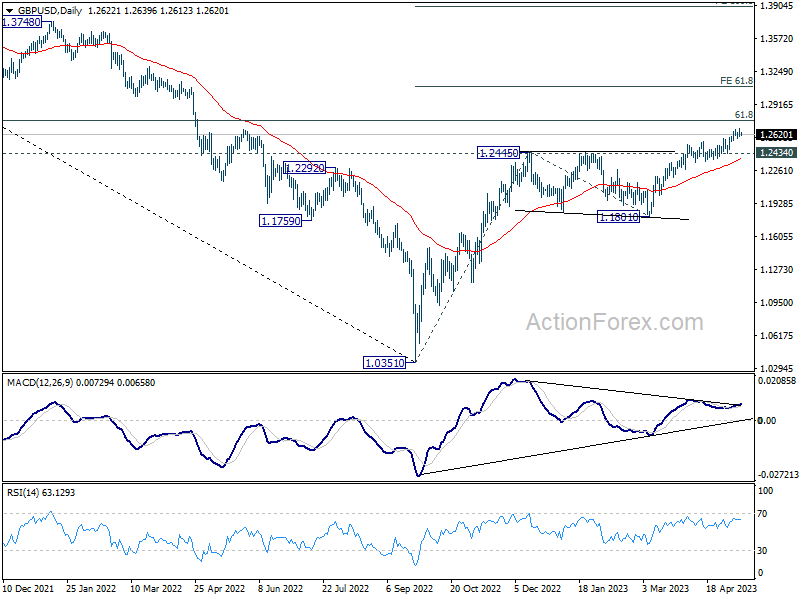

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2592; (P) 1.2636; (R1) 1.2669; More...

GBP/USD retreated quickly after rising to 1.2678 and intraday bias is turned neutral again. for now, further rally is expected as long as 1.2434 support holds. Break of 1.2678 will resume larger up trend to 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. However, decisive break of 1.2434 will confirm short term topping, and turn bias back to the downside for deeper fall.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

Sterling Soft Ahead of BoE Rate Hike, Euro Staying Pressured

As the market holds its breath for today's BoE rate decision and economic projections, Sterling is trading on a softer note, barring against Euro. Overnight attempts to resume the recent rally against Dollar were short-lived, with the Pound returning swiftly to its familiar range. The potential for hawkish and dovish surprises, or simultaneously both, at today's meeting promises a volatile session for the British currency.

Elsewhere in the currency markets, Australian and New Zealand Dollars, along with Japanese Yen, stand as the week's strongest performers. Risk sentiment is playing a minor role as stock markets continue to show lackluster performance. However, weakness in US and European yields seems to be providing some support for these currencies. Euro emerges as the current underperformer, followed by Canadian Dollar and US Dollar.

From a technical perspective, EUR/GBP appears to be losing some of its downside momentum, as reflected in 4H MACD. Yet, as long as 0.8745 resistance level holds, further decline is anticipated. Next target is 100% projection of 0.8977 to 0.8717 from 0.8874 at 0.8614. Decisive break of this level could trigger further downside acceleration. Conversely, in case of recovery, failure to regain 0.8745 could limit Euro's strength elsewhere.

In Asia, at the time of writing, Nikkei is down -0.02%. Hong Kong HSI is down -0.34%. China Shanghai SSE is down -0.20%. Singapore Strait Times is down -0.41%. Overnight, DOW dropped -0.09%. S&P 500 rose 0.45%. NASDAQ rose 1.04%. 10-year yield dropped -0.082 to 3.439.

SNB Jordan signals readiness for further policy tightening amid inflation concerns

SNB Chairman, Thomas Jordan indicated yesterday that there might be a need to further tighten the monetary policy in Switzerland, signaling the bank's unwavering commitment to keeping inflation in check.

"Monetary policy is still not restrictive enough to anchor inflation in the area of price stability," Jordan said. "We cannot exclude that we have to further tighten monetary policy."

Jordan pointedly noted, "If the inflation forecast is significantly above the area of price stability, then monetary policy is too loose." This remark underscores the central bank's resolve to use monetary policy levers to ensure that inflation doesn't exceed the stability range.

The chairman's comments come on the heels of recent data showing that annual inflation in Switzerland edged down to 2.6% in April from 2.9% in March. While these figures are modest compared to many countries grappling with double-digit inflation rates, they still exceed SNB's traditional definition of price stability.

BoJ opinions: Current monetary easing should continue

In the Summary of Opinions at BoJ's monetary policy meeting on April 27/28, new governor Kazuo Ueda's debut, revealed the need to continue with current monetary easing despite improved view on inflation outlook.

One member said "attention is warranted for the time being on the possibility of continued high inflation" while another said "achievement of the price stability target of 2 percent is coming into sight". Meanwhile, "price projections have been raised somewhat".

Yet, it's generally agreed that the central bank "should continue with the current monetary easing," given that inflation is likely to decline ahead, in the background of heightened uncertainties in overseas economies.

Also it's reiterated that to achieve the inflation target in "sustainable manner", it needs to be "accompanied by wage increases". And it's "necessary" to continue to "firmly support the momentum for wage hikes through monetary easing ".

There was also cautions that "the risk of missing a chance to achieve the 2 percent target due to a hasty revision to monetary easing is much more significant than the risk of the inflation rate continuing to exceed 2 percent."

One member noted that there is no need to revise the conduct of yield curve control as "distortions on the yield curve are currently dissipating".

China's CPI at 0.1% yoy in Apr, lowest since Feb 2021

China CPI slowed from 0.7% yoy to 0.1% yoy in April, below expectation of 0.3% yoy. That's the lowest level since February 2021. Core CPI, excluding food and energy, was unchanged a 0.7% yoy.

Within the CPI, food prices in China rose by 0.4 per cent from a year earlier in April, compared with a rise of 2.4 per cent in March, while non-food prices rose by 0.1 per cent last month, year on year, down from an increase of 0.3 per cent in March.

"In April, the market supply was generally adequate, and consumer demand gradually recovered, with the CPI falling by 0.1 per cent from a month earlier and rising by 0.1 per cent, year on year," said senior NBS statistician Dong Lijuan."Core CPI, excluding food and energy prices, rose by 0.1 per cent from a month earlier to 0.7 per cent, year on year, up at the same rate as in the previous month."

PPI dropped from -2.5% yoy to -3.6% yoy, below expectation of -3.2% yoy. PPI fell at the fastest rate since May 2020 and was down for a seventh consecutive month

"In April, PPI fell by 0.5 per cent from a month earlier and by 3.6 per cent, year on year, due to fluctuations in international commodity prices; the overall weakness of the domestic and international market demand; and the higher base of comparison from the same period last year," Dong added.

BoE to hike 25bps, will there be hint on pause?

Today marks BoE's much-anticipated "Super Thursday," with markets bracing for a 25 bps increase that brings interest rate to 4.50%. While some speculate that BoE may hit the pause button post today's rate hike, opinions are far from unanimous. Notably, Goldman Sachs anticipates interest rate to reach a terminal rate of 5.00% by August, implying two more rate hikes in the pipeline.

Attention will be focused on voting too. Known doves Silvana Tenreyro and Swati Dhingra are anticipated to vote against any change. However, given that inflation remained in double digits at 10.1% in March, any dissent from the remaining seven MPC members could be viewed as a dovish surprise. Conversely, hawkish surprises could arise if any members vote for a more aggressive 50bps hike today.

Further intrigue lies in the new economic projections, which will be closely examined for hints of the future rate path. Outlook for inflation remains shrouded in uncertainty. A report released today by NIESR suggests that inflation will remain "persistently elevated," decreasing only to 5.4% by the end of 2023. This forecast markedly exceeds prediction by the Office for Budget Responsibility, which anticipated inflation to drop to 2.9%.

Here are some previews on BoE:

- BoE Expected to Hike, Then What?

- Will Bank of England Once Again Fail to Address the Inflation Problem?

- Bank of England Preview – 25 and Priming the Markets for a Pause

Elsewhere

US PPI and jobless claims will also be featured today.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2592; (P) 1.2636; (R1) 1.2669; More...

GBP/USD retreated quickly after rising to 1.2678 and intraday bias is turned neutral again. for now, further rally is expected as long as 1.2434 support holds. Break of 1.2678 will resume larger up trend to 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. However, decisive break of 1.2434 will confirm short term topping, and turn bias back to the downside for deeper fall.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance Apr | -39% | -38% | -43% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Bank Lending Y/Y Apr | 3.20% | 2.90% | 3.00% | |

| 23:50 | JPY | Current Account (JPY) Mar | 1.01T | 1.32T | 1.09T | 1.23T |

| 01:00 | AUD | Consumer Inflation Expectations May | 5.00% | 4.60% | ||

| 01:30 | CNY | CPI Y/Y Apr | 0.10% | 0.30% | 0.70% | |

| 01:30 | CNY | PPI Y/Y Apr | -3.60% | -3.20% | -2.50% | |

| 05:00 | JPY | Eco Watchers Survey: Current Apr | 54.6 | 54.1 | 53.3 | |

| 11:00 | GBP | BoE Interest Rate Decision | 4.50% | 4.25% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | 7--0--2 | 7--0--2 | ||

| 12:30 | USD | PPI M/M Apr | 0.30% | -0.50% | ||

| 12:30 | USD | PPI Y/Y Apr | 1.40% | 2.70% | ||

| 12:30 | USD | PPI Core M/M Apr | 0.30% | -0.10% | ||

| 12:30 | USD | PPI Core Y/Y Apr | 2.70% | 3.40% | ||

| 12:30 | USD | Initial Jobless Claims (May 5) | 245K | 242K | ||

| 14:30 | USD | Natural Gas Storage | 78B | 54B |

BoE to hike 25bps, will there be hint on pause?

Today marks BoE's much-anticipated "Super Thursday," with markets bracing for a 25 bps increase that brings interest rate to 4.50%. While some speculate that BoE may hit the pause button post today's rate hike, opinions are far from unanimous. Notably, Goldman Sachs anticipates interest rate to reach a terminal rate of 5.00% by August, implying two more rate hikes in the pipeline.

Attention will be focused on voting too. Known doves Silvana Tenreyro and Swati Dhingra are anticipated to vote against any change. However, given that inflation remained in double digits at 10.1% in March, any dissent from the remaining seven MPC members could be viewed as a dovish surprise. Conversely, hawkish surprises could arise if any members vote for a more aggressive 50bps hike today.

Further intrigue lies in the new economic projections, which will be closely examined for hints of the future rate path. Outlook for inflation remains shrouded in uncertainty. A report released today by NIESR suggests that inflation will remain "persistently elevated," decreasing only to 5.4% by the end of 2023. This forecast markedly exceeds prediction by the Office for Budget Responsibility, which anticipated inflation to drop to 2.9%.

Here are some previews on BoE:

China’s CPI at 0.1% yoy in Apr, lowest since Feb 2021

China's CPI for April decelerated from the previous month's 0.7% yoy to a mere 0.1% yoy, well below market expectations of 0.3% yoy. This slowdown marks the lowest inflation rate since February 2021. Core CPI, which excludes food and energy prices, maintained its steady pace at 0.7% yoy.

A breakdown of CPI reveals that food prices, which had increased by 2.4% yoy in March, grew by a much slower 0.4% yoy in April. Non-food prices, on the other hand, edged up by just 0.1% yoy, down from 0.3% yoy.

Senior NBS statistician Dong Lijuan explained the latest CPI figures, saying, "In April, the market supply was generally adequate, and consumer demand gradually recovered, with the CPI falling by 0.1 per cent from a month earlier and rising by 0.1 per cent, year on year."

In a similar vein, PPI for April fell from -2.5% yoy to -3.6% yoy, again missing market predictions of -3.2% yoy. This marked the steepest fall in PPI since May 2020 and its seventh consecutive month in the negative territory.

Lijuan attributed the PPI plunge to several factors, stating, "In April, PPI fell by 0.5 per cent from a month earlier and by 3.6 per cent, year on year, due to fluctuations in international commodity prices; the overall weakness of the domestic and international market demand; and the higher base of comparison from the same period last year."

BoJ opinions: Current monetary easing should continue

In the Summary of Opinions at BoJ's monetary policy meeting on April 27/28, new governor Kazuo Ueda's debut, revealed the need to continue with current monetary easing despite improved view on inflation outlook.

One member said "attention is warranted for the time being on the possibility of continued high inflation" while another said "achievement of the price stability target of 2 percent is coming into sight". Meanwhile, "price projections have been raised somewhat".

Yet, it's generally agreed that the central bank "should continue with the current monetary easing," given that inflation is likely to decline ahead, in the background of heightened uncertainties in overseas economies.

Also it's reiterated that to achieve the inflation target in "sustainable manner", it needs to be "accompanied by wage increases". And it's "necessary" to continue to "firmly support the momentum for wage hikes through monetary easing ".

There was also cautions that "the risk of missing a chance to achieve the 2 percent target due to a hasty revision to monetary easing is much more significant than the risk of the inflation rate continuing to exceed 2 percent."

One member noted that there is no need to revise the conduct of yield curve control as "distortions on the yield curve are currently dissipating".

SNB Jordan signals readiness for further policy tightening amid inflation concerns

SNB Chairman, Thomas Jordan indicated yesterday that there might be a need to further tighten the monetary policy in Switzerland, signaling the bank's unwavering commitment to keeping inflation in check.

"Monetary policy is still not restrictive enough to anchor inflation in the area of price stability," Jordan said. "We cannot exclude that we have to further tighten monetary policy."

Jordan pointedly noted, "If the inflation forecast is significantly above the area of price stability, then monetary policy is too loose." This remark underscores the central bank's resolve to use monetary policy levers to ensure that inflation doesn't exceed the stability range.

The chairman's comments come on the heels of recent data showing that annual inflation in Switzerland edged down to 2.6% in April from 2.9% in March. While these figures are modest compared to many countries grappling with double-digit inflation rates, they still exceed SNB's traditional definition of price stability.