Sample Category Title

China’s CPI at 0.1% yoy in Apr, lowest since Feb 2021

China's CPI for April decelerated from the previous month's 0.7% yoy to a mere 0.1% yoy, well below market expectations of 0.3% yoy. This slowdown marks the lowest inflation rate since February 2021. Core CPI, which excludes food and energy prices, maintained its steady pace at 0.7% yoy.

A breakdown of CPI reveals that food prices, which had increased by 2.4% yoy in March, grew by a much slower 0.4% yoy in April. Non-food prices, on the other hand, edged up by just 0.1% yoy, down from 0.3% yoy.

Senior NBS statistician Dong Lijuan explained the latest CPI figures, saying, "In April, the market supply was generally adequate, and consumer demand gradually recovered, with the CPI falling by 0.1 per cent from a month earlier and rising by 0.1 per cent, year on year."

In a similar vein, PPI for April fell from -2.5% yoy to -3.6% yoy, again missing market predictions of -3.2% yoy. This marked the steepest fall in PPI since May 2020 and its seventh consecutive month in the negative territory.

Lijuan attributed the PPI plunge to several factors, stating, "In April, PPI fell by 0.5 per cent from a month earlier and by 3.6 per cent, year on year, due to fluctuations in international commodity prices; the overall weakness of the domestic and international market demand; and the higher base of comparison from the same period last year."

BoJ opinions: Current monetary easing should continue

In the Summary of Opinions at BoJ's monetary policy meeting on April 27/28, new governor Kazuo Ueda's debut, revealed the need to continue with current monetary easing despite improved view on inflation outlook.

One member said "attention is warranted for the time being on the possibility of continued high inflation" while another said "achievement of the price stability target of 2 percent is coming into sight". Meanwhile, "price projections have been raised somewhat".

Yet, it's generally agreed that the central bank "should continue with the current monetary easing," given that inflation is likely to decline ahead, in the background of heightened uncertainties in overseas economies.

Also it's reiterated that to achieve the inflation target in "sustainable manner", it needs to be "accompanied by wage increases". And it's "necessary" to continue to "firmly support the momentum for wage hikes through monetary easing ".

There was also cautions that "the risk of missing a chance to achieve the 2 percent target due to a hasty revision to monetary easing is much more significant than the risk of the inflation rate continuing to exceed 2 percent."

One member noted that there is no need to revise the conduct of yield curve control as "distortions on the yield curve are currently dissipating".

SNB Jordan signals readiness for further policy tightening amid inflation concerns

SNB Chairman, Thomas Jordan indicated yesterday that there might be a need to further tighten the monetary policy in Switzerland, signaling the bank's unwavering commitment to keeping inflation in check.

"Monetary policy is still not restrictive enough to anchor inflation in the area of price stability," Jordan said. "We cannot exclude that we have to further tighten monetary policy."

Jordan pointedly noted, "If the inflation forecast is significantly above the area of price stability, then monetary policy is too loose." This remark underscores the central bank's resolve to use monetary policy levers to ensure that inflation doesn't exceed the stability range.

The chairman's comments come on the heels of recent data showing that annual inflation in Switzerland edged down to 2.6% in April from 2.9% in March. While these figures are modest compared to many countries grappling with double-digit inflation rates, they still exceed SNB's traditional definition of price stability.

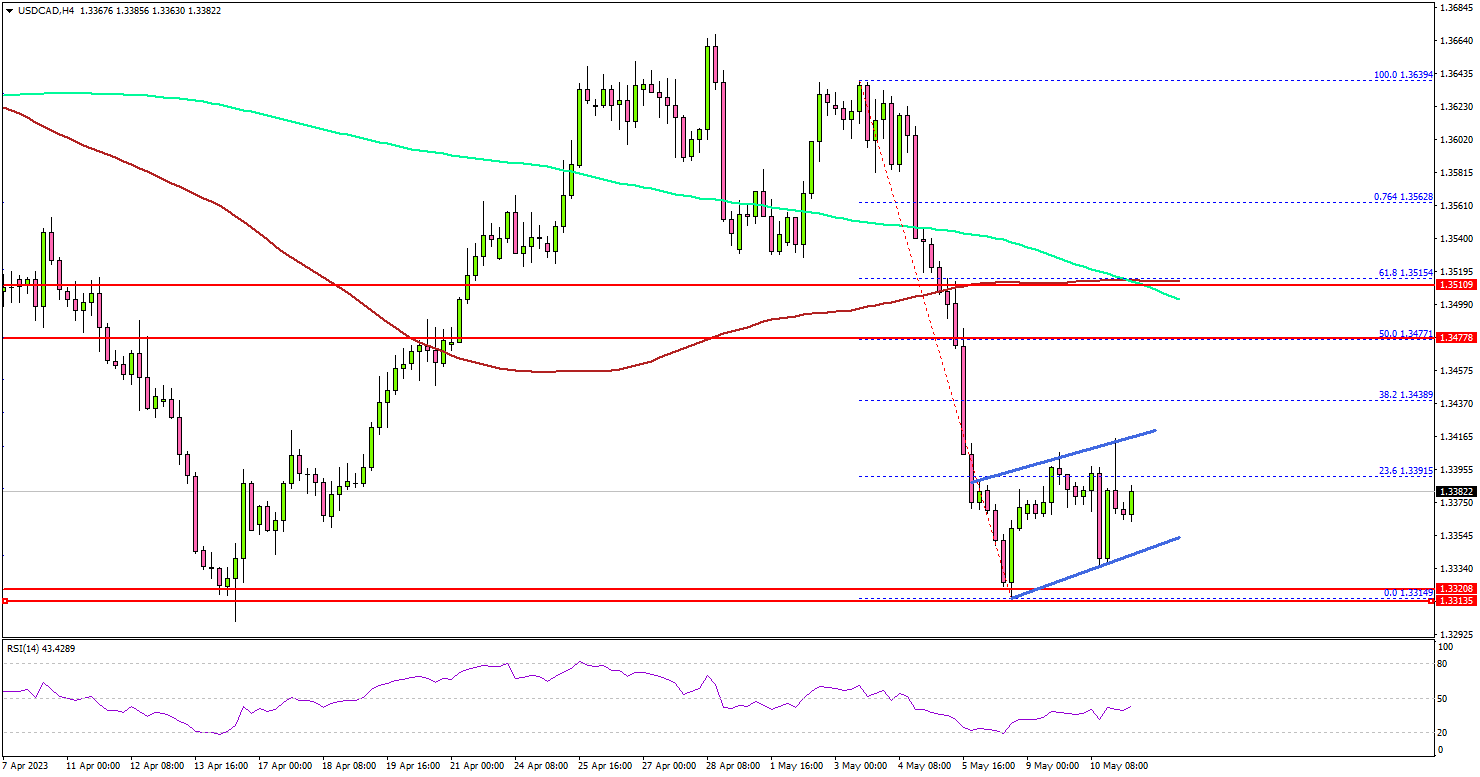

USD/CAD Holds Support But Can It Recover?

Key Highlights

- USD/CAD declined heavily and tested the 1.3330 support.

- A key rising channel is forming with support near 1.3350 on the 4-hour chart.

- EUR/USD is trading above the 1.0950 support and might climb higher.

- The BoE interest rate decision is scheduled today (forecast 4.5%, versus 4.25% previous).

USD/CAD Technical Analysis

The US Dollar started a strong decline from the 1.3640 zone against the Canadian Dollar. USD/CAD traded below the 1.3480 level to move into a bearish zone.

Looking at the 4-hour chart, the pair settled below the 1.3400 level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

Finally, the bulls took a stand near the 1.3330 support. A low is formed near 1.3314 and the pair is now consolidating losses. There is also a key rising channel forming with support near 1.3350 on the same chart.

Immediate resistance on the upside is near the 1.3420 level. The next key resistance is near the 1.3450 level. The main resistance sits near 1.3480 and the 100 simple moving average (red, 4 hours).

A clear upside break and close above the 1.3480 resistance might start another steady increase. The next key resistance is near the 1.3550 zone. Any more gains might send the pair toward 1.3640.

On the downside, the pair might find bids near 1.3340. The next major support is near the 1.3320 level. If there is a downside break below the 1.3420, the pair could test the 1.3250 level.

Looking at EUR/USD, the pair is still trading in a positive zone above 1.0950 and might attempt a fresh increase in the near term.

Economic Releases

- BoE Interest Rate Decision - Forecast 4.5%, versus 4.25% previous.

- US Initial Jobless Claims - Forecast 245K, versus 242K previous.

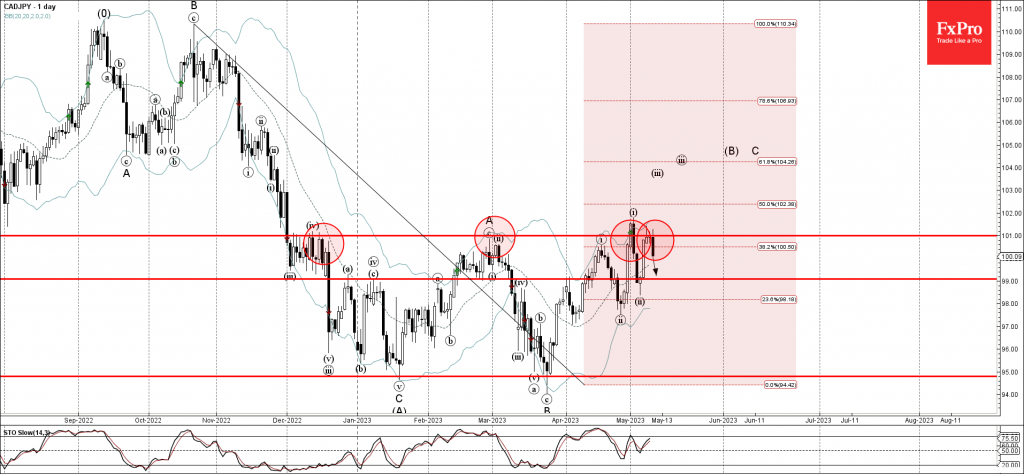

CADJPY Wave Analysis

- CADJPY reversed from pivotal resistance level 101.00

- Likely to fall to support level 99,00

CADJPY earlier reversed down once again from the pivotal resistance level 101.00 (which has reversed the pair multiple times from December), strengthened by the upper daily Bollinger Band.

The downward reversal from the resistance level 101.00 stopped the previous impulse wave C.

Given the bearish divergence on the daily Stochastic, CADJPY can be expected to fall further toward the next support level 99,00.

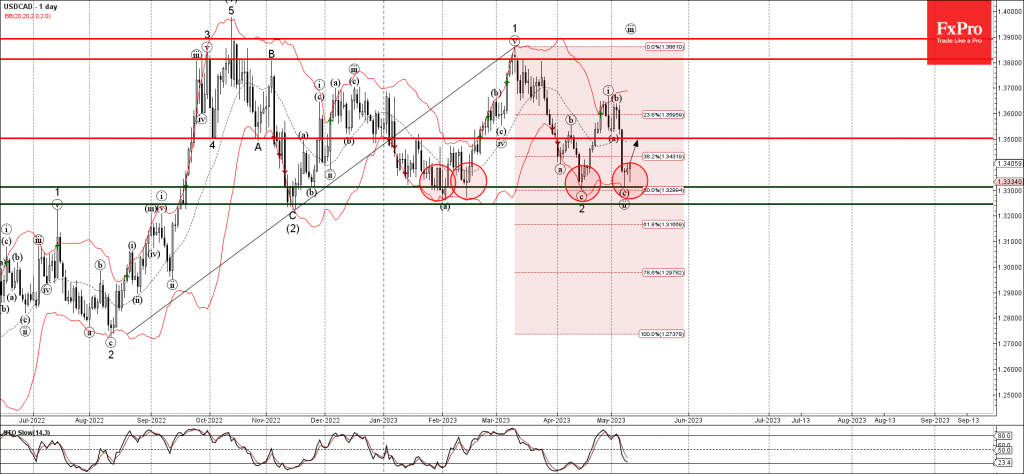

USDCAD Wave Analysis

- USDCAD reversed from support level 1.3310

- Likely to rise to resistance level 1.3500

USDCAD recently reversed up from the key support level 1.3310 (which has been steadily reversing the price from November).

The support level 1.3310 was further strengthened by the lower daily Bollinger Band and by the 50% Fibonacci correction of the upward impulse from August.

Given the bullish divergence on the daily Stochastic, USDCAD can be expected to rise further toward the next resistance level 1.3500.

Pound Swings After US Inflation Ticks Lower

- US inflation ticks lower to 4.9%

- BoE expected to raise rates by 25 bp on Thursday

US inflation dips lower

The US inflation report for April showed a very small decline. Headline CPI ticked lower to 4.9%, down from 5.0% in March and the consensus estimate of 5.0%. The core rate eased to 5.5%, matching the consensus estimate and a drop below the March reading of 5.6%. On a monthly basis, headline CPI rose from 0.1% to 0.4%, matching the consensus estimate. The core rate was unchanged and also matched the consensus estimate.

The inflation report indicated that inflation remains stubbornly high and the disinflation process is moving at a snail’s pace. The Fed has managed to curb inflation significantly, but it seems that bringing inflation down to the 2% target will be tricky and one or two more rate hikes will not achieve that target.

BoE expected to raise rates

The Bank of England holds its meeting on Thursday and is expected to raise rates by 25 basis points to 4.50%. The BoE’s fight against inflation hasn’t gone according to plan, as inflation is hovering above 10%. Still, the BoE remains optimistic and has projected that inflation will fall rapidly in the second half of the year. The BoE’s tightening has exacerbated the cost-of-living crisis and policymakers are looking to provide some relief by winding up the current rate-tightening cycle with a final rate hike either on Thursday or at the June meeting.

GBP/USD Technical

- There is resistance at 1.2676 and 1.2785

- 1.2573 and 1.2495 are providing support

Will Gold Continue Conquering Uncharted Territories?

With investors remaining convinced that the Fed will start cutting interest rates at some point later this year, US Treasury yields and the dollar have stayed subdued, which combined with concerns surrounding the banking sector and the US debt ceiling, allowed gold to hit a new record high on Thursday, before strongly pulling back on Friday. Will the precious metal rebound and extend its uptrend into new uncharted territories or is Friday’s retreat a sign that the uptrend is running out of fuel?

Gold hits record high after Fed pause hints

At last week’s FOMC decision, policymakers delivered the broadly anticipated 25bps hike, but they watered down their forward guidance. They removed the part saying that some additional policy firming may be appropriate and instead said that in determining whether more hikes may be needed, they will consider the cumulative tightening of monetary policy, the lags with which policy affects the economy and inflation, and incoming economic and financial developments.

The softening of forward guidance pushed the US dollar lower initially, but the currency found some footing during Powell’s press conference, perhaps as he refused to close the door to a June hike. Having said that though, it was all south for the greenback thereafter as market participants were convinced that a pause is the most likely outcome for June. Just the next day, gold managed to hit a new all-time high at $2,072.19, surpassing its previous record hit in August 2020.

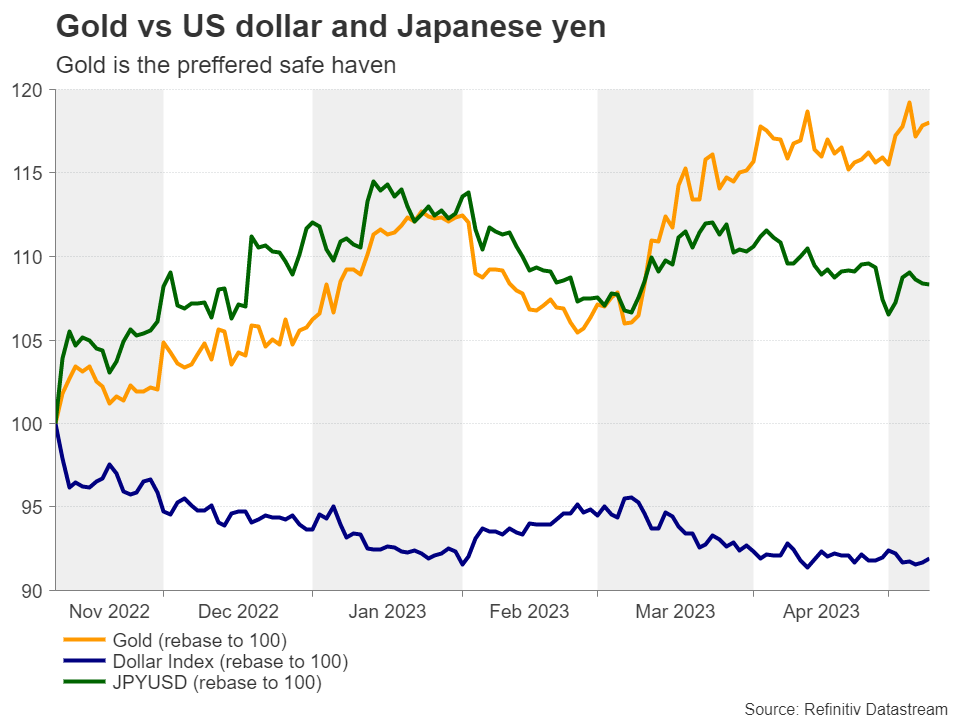

The best safe haven in town

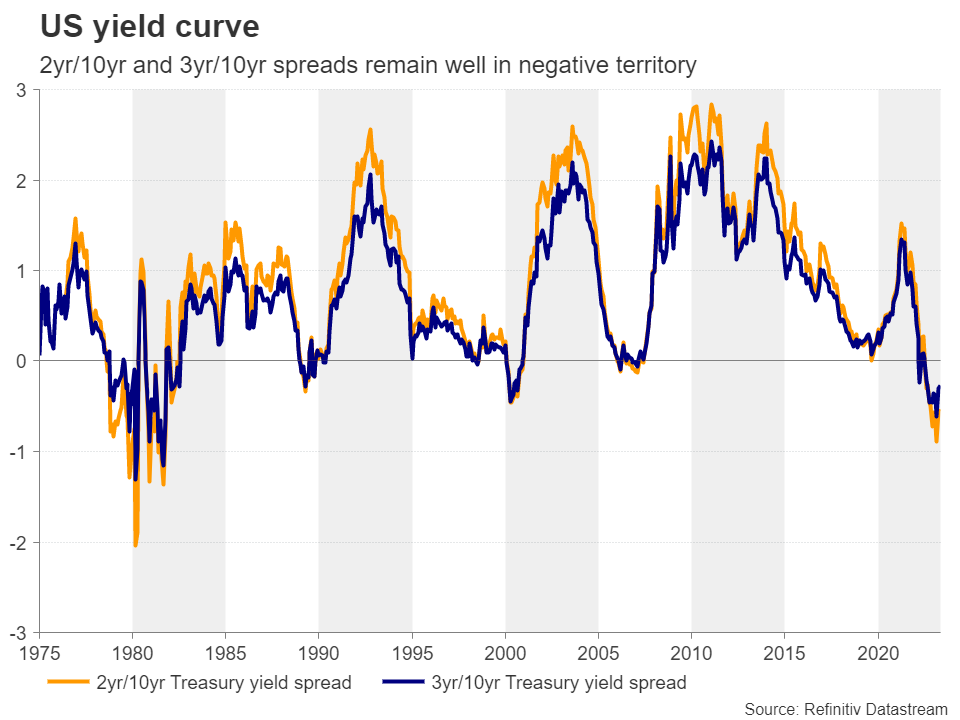

Now investors are pricing in nearly 65bps worth of rate reductions by the end of the year, with the first quarter-point cut almost fully baked in the cake for September. This suggests that investors remain fearful that the Fed’s aggressive tightening could still throw the US economy into recession, and this is also evident by the inverted yield curve, where both the 2yr/10yr and 3yr/10yr spreads remain well in negative territory after hitting their lowest levels since 1981.

Yes, equities have remained relatively supported, but this may have been due to expectations of lower interest rates resulting in higher present values for high-growth firms. Gold is reflecting investors anxiety much better, as the steep rally to a new record high points to more bullish forces than just a weak US dollar. With Treasury yields coming off their October highs due to Fed cut bets, and the BoJ still not deciding on another step towards normalization, the US dollar and the Japanese yen seem to have forgotten their safe-haven suits in the closet. Currently, the precious metal may be the only choice for those looking for safety.

For how much longer will it keep shining?

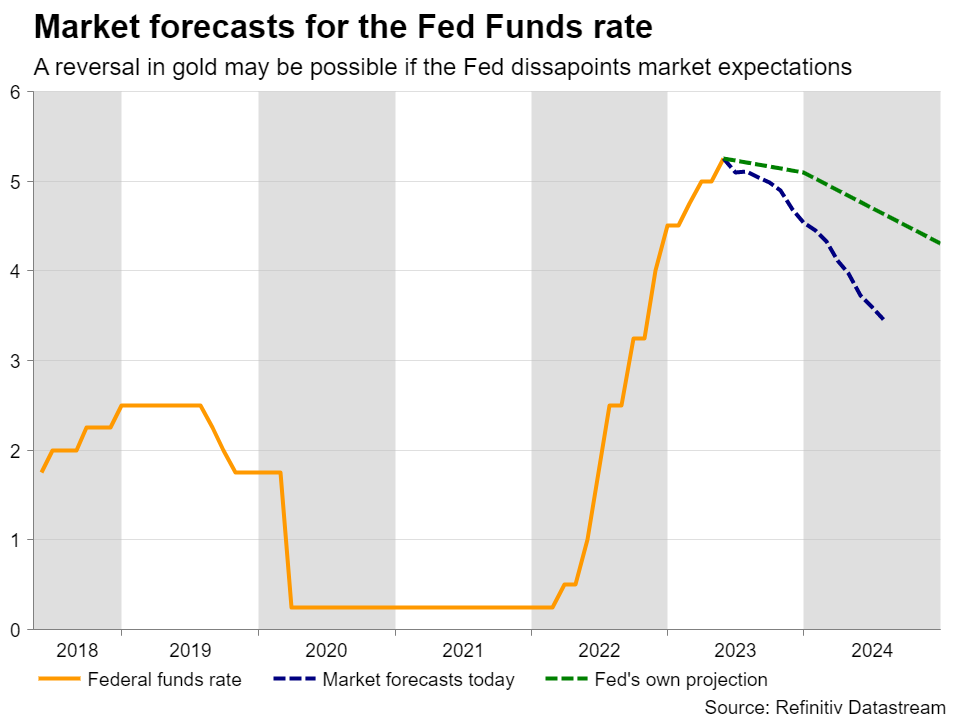

However, the big question nowadays may be: For how much longer can the precious metal continue to shine? In its simplest form, the answer is: Until the dynamics that paint the bright picture begin to change. For example, even if the market continues to ignore the Fed’s warnings that no cuts are warranted this year, that cannot last forever. A June hike and/or keeping interest rates untouched beyond September – when the first cut is expected – could very well upset current expectations and trigger a rally in Treasury yields and the US dollar, which is a negative blend for gold. And if this is accompanied by better-than-expected US data that dismiss recession worries, the precious metal could lose more allure.

Friday’s employment report for April came in strong and the Fed’s loan survey on Monday eased fears of a credit crunch, but the yield curve inversion is far from suggesting that the concerns about the future of the US economy have totally vanished. The ongoing stalemate in the US Congress over raising the debt ceiling is also a viable reason for staying cautious, while traders may be worried regarding other economies as well, like China, where last week’s disappointing PMIs suggested that after the post-reopening boost, the engines of the world’s second largest economy are now struggling to gather momentum. Thus, for now the outlook of the precious metal likely remains positive, at least for another month or two.

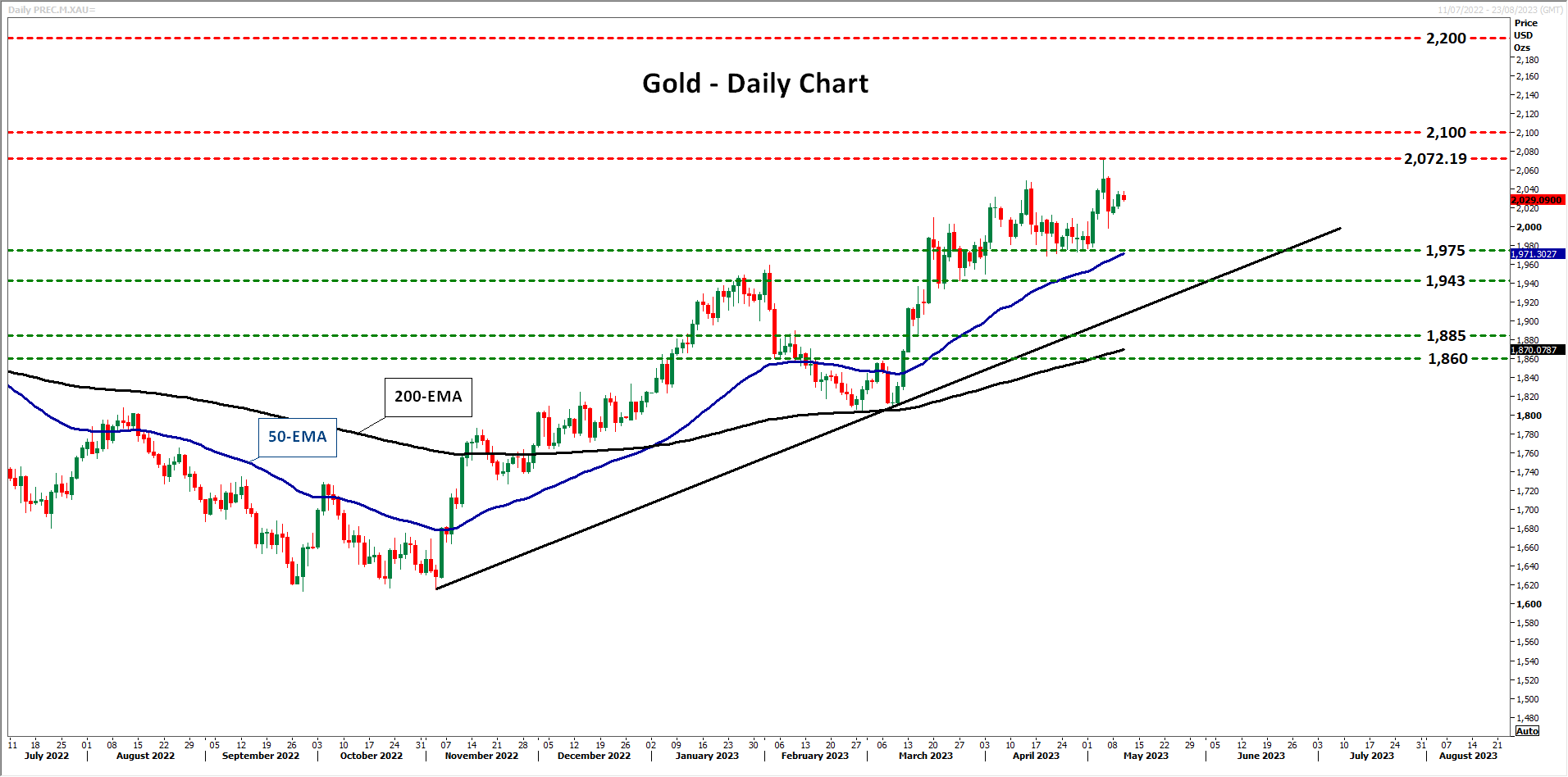

Technical picture still points to uptrend

From a technical standpoint, despite pulling back after hitting a new record high, gold remains above both its 50- and 200-day exponential moving averages (EMAs), as well as above the tentative uptrend line drawn from the low of November 3. This keeps the prevailing uptrend intact.

If the bulls are strong enough to regain control from above the strong support zone of $1,975, they may be able to reach and breach the record of $2,072.19, entering uncharted territory. With no prior highs or inside swing lows to mark new resistances, a wise choice may be to mark round numbers like $2,100 and $2,200.

On the downside, the move signaling that the bears may have stolen all the bulls’ swords may be a decisive dip below the $1,943 barrier, marked by the low of March 27. Such a slide may also signal the break below the aforementioned uptrend line and perhaps pave the way towards the low of March 15 at $1,885.

BoE Expected to Hike, Then What?

The BOE is the last of the major banks hiking this cycle, and the expectation is that it will follow its peers - with a twist. Last week, the ECB and the Fed both hiked by a quarter of a point, but then implied that further rate hikes would be data dependent. The ECB bias was for another hike, the Fed for a pause; but both left the door wide open for this being the top of the rate hiking cycle.

The BOE, on the other hand, is facing persistently high inflation and likely doesn't have the luxury to imply it's at the terminal rate. The latest report showed inflation in the double digits, while the BOE had forecast that inflation would come down precipitously during the last quarter.

Patience is running out

The BOE might have been the first to start hiking, but its plodding pace of hikes have apparently let inflation keep rising. Unlike the ECB and Fed, where rate decisions votes have been unanimous, the vote from the BOE to keep up the pressure on inflation has been divided. The current theory among central bankers is that it's the expectation for lower inflation that drives down prices.

The theory argues that central banks need to have the "credibility" to fight inflation, which means that market makers have confidence that the necessary rate hikes will happen. A disunited front, and vacillating vote counts, can be seen as hurting that sense of commitment to bring prices down. At least some analysts and traders are likely to be looking at the split vote as a sign that the BOE won't raise rates high enough, or will bring them down too soon, to keep prices in check.

What to expect

With a unanimous expectation that the BOE will hike by 25bps, the focus is likely to be on the vote split. MPC members Tenreyo and Dhingra have consistently voted against raising rates, arguing that dealing with the economy should be the first priority. If other members were to join in, with a 3-6 split, then investors might take it as a sign that the BOE is about to give up on its slow rate hiking path. That could substantially weaken the pound.

Barring this occurrence, the BOE is expected to reiterate its stance that more policy action might be necessary to calm inflation. The forecast for price growth outlook is likely to be updated, but for many traders, that might be just the BOE catching up with reality, and unlikely to change market expectations.

Breaking stagflation

With high inflation and near-zero growth, the UK is in a particularly difficult position for policymakers: Stagflation. Traditionally, the only way to break out of that is through some kind of recession, either induced by monetary policy to bring down inflation, or a credit crisis driven by high inflation.

The BOE's refusal to pick either of those options can be seen as trying to kick the can down the road to where it will be an even bigger problem. For traders, however, it means cable is likely to remain under pressure, unless Bailey surprises with some extra degree of hawkishness.