Sample Category Title

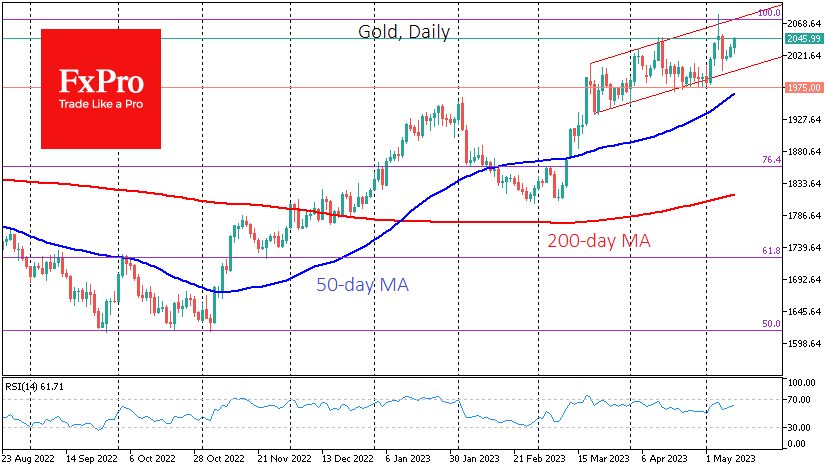

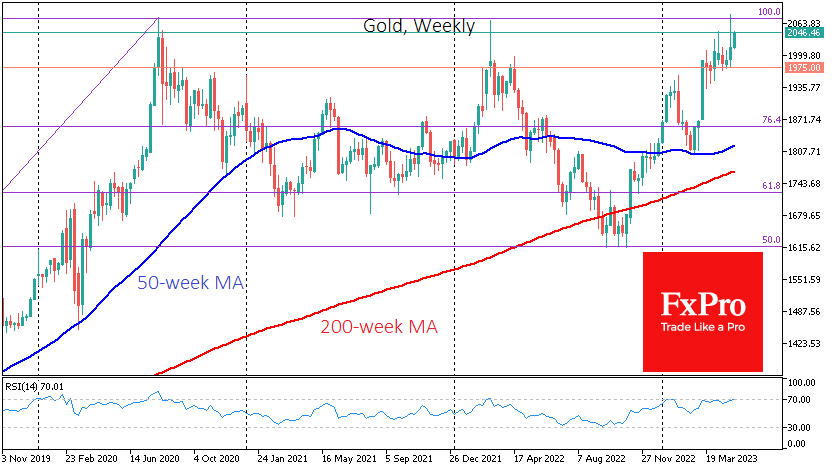

Gold Needs Correction Before Another Leg Up

Gold showed very high volatility on Thursday and Friday, rising to $2081 and falling below $2000 in less than 48 hours. However, the price remained within the uptrend that has been in place since the second half of March.

The sharp rise and fall in gold at the end of last week had a close inverse correlation with US regional banks. Their problems triggered a short squeeze after the close of the regular session on Wednesday. However, the rapid recovery of the banks on Friday caused a sharp pullback.

Banks, by their very nature, are vulnerable to public sentiment. And from that point of view, the outflow of deposits from regional banks will likely stop with outside intervention, so the list of bankruptcies is still being determined.

The much more difficult question is whether gold will continue to be in demand of bad news about banks. The gold rallies on the convulsions of regional credit institutions were more about a liquidity crisis, and gradually capital may flow back into dollar-denominated debt assets, which are currently offering impressive yields.

However, it is worth taking a step back to realise that the banks’ problems are not the only driver for gold. Investors should also bear in mind the trend towards increasing purchases of gold as a reserve by emerging market central banks, which are also exposed to the risk of being hit by US or EU sanctions that block settlement in dollars and euros.

We also noted earlier a strong technical disposition in gold, whose price is approaching historical highs much more smoothly than in 2020 or 2022, leaving more strength for a breakout.

An important bullish signal for gold could be a weekly close above $2035, the highest close in history. However, a much smoother ride with a touch of the lower end of the uptrend range around $2000 is seen as a more likely scenario before the uptrend resumes.

Sunset Market Commentary

Markets

Markets traded with a cautious bias going into the US CPI release, with European equities and the euro incurring modest losses. European yields lost a few bps even as ECB’s Lagarde reiterated that the ECB has further ground to cover. US yields traded mixed going into the release. US inflation in April printed very close to expectations at 0.4% M/M and 4.9% Y/Y for the headline (from 5%) and 0.4% M/M and 5.5% for the core measure (from 5.6%). A 0.4% monthly rise still suggests sticky prices. However, a core measure for services calculated by Bloomberg, stripping out energy and housing, eased to 0.1% M/M and 5.1% Y/Y. At least at this stage, markets apparently saw this mix as soft enough to justify at least a prolonged Fed pause ‘potentially’ to be followed by a first interest rate cut post summer (25 bps discounted for the end September meeting). US yields currently eased between 7 bps (5-y) and 3.0 bps (30-y). The setback in German yields stays more modest at about 4bps across the curve. The easing of core inflation, annex decline in core yields this time supports equities. European indices reversed initial losses (EuroStoxx 50 little changed, S&P opened 0.8% higher). Brent oil tries to regain the $77.5 p/b short term resistance.

Contrary to what was often the case of late, the reaction in FX was al least as significant as what happened in bond and equity markets. EUR/USD just before the release almost touched yesterday’s correction low near 1.094, but revisited the 1.10 barrier (currently 1.0985). DXY still failed to build on a tentative bottoming pattern again trading in the 101.35 area (to be compared with a short term bottom near 100.8). Even the yen gains with USD/JPY immediately after the CPI release tumbling a full big figure (currently 134.65). EUR/JPY also dropped below the 148 handle despite equities rebounding intra-day. Sterling initially remained well bid as UK yields ahead of tomorrow’s BoE meeting. However, EUR/GBP tested the 0.8675 area before trying to build an intra-day bottoming pattern. The National bank of Poland as expected left its policy rate unchanged at 6,75%. No communication has been delivered currently. The zloty already was in excellent shape before the NBP decision and accelerated post the US CPI release. At EUR/PLN 4.52, the zloty trades at the strongest level against the euro since February 2022.

News & Views

Norwegian inflation proves extremely sticky. The headline April number barely eased from 6.5% to 6.4% on a rapid 1.1% monthly pace. Underlying inflation (adjusted for tax changes and excluding energy prices) even accelerated with a monthly 1% jump lifting the yearly figure from 6.2% to 6.3%. Categories registering some of the sharpest price increases were recreation & culture (1.8%), furnishings, household equipment & routine maintenance (1.5% m/m) and housing and utilities (0.8%). Food and non-alcoholic beverages jumped 2.5% m/m. The April outcome not only topped analyst estimates, it was also (way) more than the Norges Bank projected in March (5.6% headline, 6.1% core). It raises serious questions to the Scandinavian central bank’s projected terminal rate of just 3.5% in June. Norwegian swap yields surge between 4.6 and 7.8 bps with the front underperforming. Money markets assume a peak policy rate of 4% at the very least. The Norwegian krone appreciates a tad to EUR/NOK 11.48, testing resistance at 11.50.

Hungarian inflation eased more or less as expected from 25.2% to 24% in April though the monthly dynamics stayed at a strong 0.7%. Core inflation eased as well, from 25.7% to 24.8%. Food prices stabilized in April (0% m/m) and prices of fuels (-0.7%) and electricity, gas and other fuels (-0.8%) even declined month over month. The more sticky services inflation, however, rose by 1.7%. And despite the Hungarian forint’s recent appreciation, tradeable goods prices are still up by about 1% m/m for the fourth month straight. KBC Economics expects inflation to ease sub 20% by July and to moderate to around 13% by September before returning to single digits in December. The Hungarian central bank last month cut the top-end of the interest rate corridor, a move that kicked off the cutting cycle. Barring renewed selling pressure on the forint, the MNB is expected to lower the 18% de facto policy rate (O/N tender rate) already this month (May 23). The currency is testing important resistance around the EUR/HUF 370 recent highs today but that’s at least partially due to a weaker euro (and declining core bond yields).

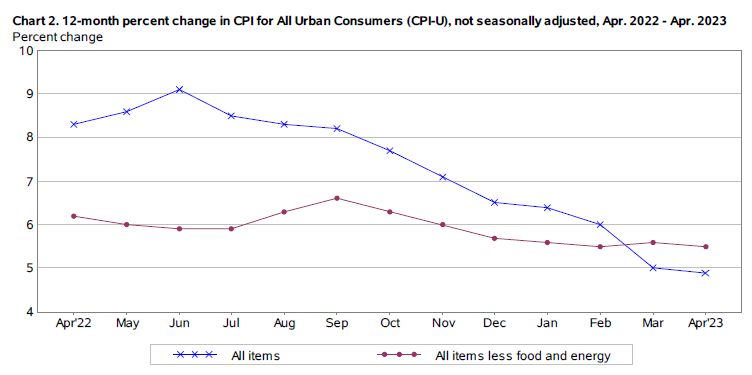

US: Inflation Remains Stubbornly Elevated, But April Data Shows Encouraging Signs

The Consumer Price Index (CPI) increased 0.4% month-on-month (m/m) in April, meeting the consensus forecast. The 12-month change slipped to 4.9% – down from 5.0% in March.

Energy prices rose 0.6% m/m as higher gasoline prices (+3.0 m/m) more than offset the pullback in energy service costs (-1.7% m/m). Food prices were again flat on the month, pushing the year-ago measure down to 7.7%.

Core inflation (excludes food & energy) was up 0.4% m/m – meeting the consensus forecast. Compared to last April, core inflation remains elevated at 5.5% – only a tenth of percentage point below it's March reading.

Price growth across services (+0.4% m/m) held steady in April. Shelter inflation cooled for the second straight month, rising by 0.4% m/m, with gains spread across rent of primary residence (+0.6% m/m) and owners' equivalent rent (+0.5% m/m). Lodging away from home (-3.0% m/m) was lower on the month, ending what had been five consecutive months of gains.

- Non-housing services were up 0.1% m/m, a meaningful deceleration from the 0.3%-0.4% month-on-month gains seen in each of the five prior months.

Core goods prices rose by 0.6% m/m – an acceleration from March's 0.2% m/m gain. Most goods categories were higher on the month, with used vehicle prices rising by a noticeable 4.4% m/m – snapping what had been nine consecutive months of declines.

Key Implications

There were definitely some encouraging signs in this morning's CPI numbers. The continued deceleration in shelter costs suggests that we are starting to see some passthrough from last year's pullback in rental rates, which should continue for the next several months. Meanwhile, price growth across non-housing services decelerated to its slowest month-on-month pace of growth in nearly two years.

That said, we need to balance this morning's good news with the fact that goods prices have accelerated for a second consecutive month and have (again) become a source of inflationary pressure. And while the slowing in shelter costs is encouraging, more recent market-based measures of rent have shown that average rental costs have again turned higher and are already back to last year's highs. This suggests the disinflationary pressure from shelter could be fleeting.

At the May interest rate announcement, the Fed signaled that they were nearing the end of its tightening cycle, but left the door open to further rate increases should the economic data continue to surprise to the upside. At this point, it's still too early to say if another hike is in the cards, particularly given the uncertainties surrounding the recent tightening in lending standards and the potential knock-on effects it may have on the real economy. But one thing is for certain. Current market pricing, which shows rate cuts beginning as early as September, appear out of step with the recent flow of economic data. Any outward push on rate cut pricing should help to pressure yields higher, effectively doing some of the heavy lifting for the Fed.

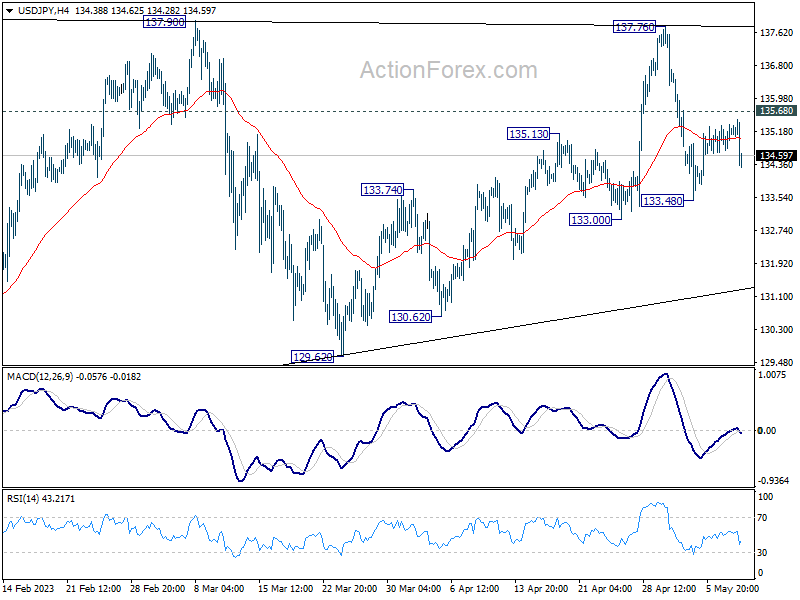

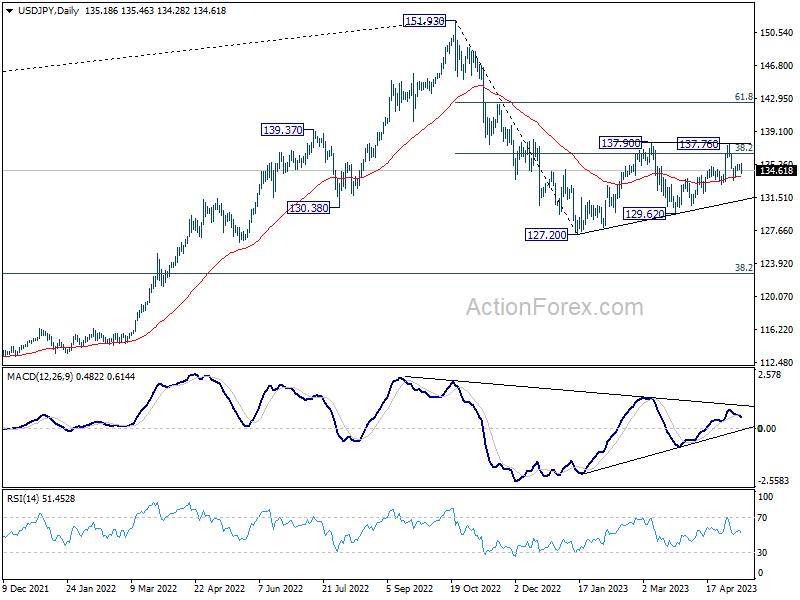

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 134.85; (P) 135.11; (R1) 135.49; More...

USD/JPY dips notably but stays above 133.48 support. Intraday bias stays neutral at this point. With 135.68 minor resistance intact, deeper decline is mildly in favor. Fall from 137.76 is seen as the third leg of the pattern from 137.90. Below 133.48 will target 133.00 first, break will target 129.62 support. Still, as long as 129.62 holds, larger rebound from 127.20 is still in favor to resume at a later stage. On the upside, above 135.68 minor resistance will turn bias back to the upside for 137.76/90 instead.

In the bigger picture, price actions from 151.93 high are currently seen as a corrective pattern to the long term up trend. The first leg should have completed at 127.20. Rebound from there is seen as the second leg. Sustained break of 38.2% retracement of 151.93 to 127.20 at 136.34 will bring stronger rebound to 61.8% retracement at 142.48. Meanwhile, break of 129.62 will argue that the third leg is starting through 127.20 low.

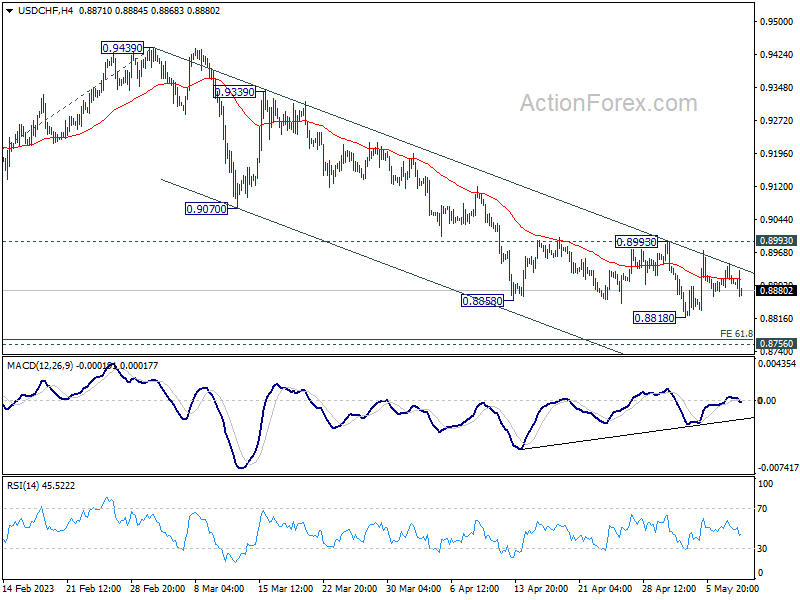

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8881; (P) 0.8912; (R1) 0.8936; More...

No change in USD/CHF's outlook as consolidation from 0.8818 is still in progress. Intraday bias remains neutral for the moment. While down trend from 1.0146 could still extend lower, strong support should be seen from 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support, to bring rebound, at least on first attempt. On the upside, break of 0.8993 resistance will indicate short term bottoming, on bullish convergence condition in 4H MACD, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

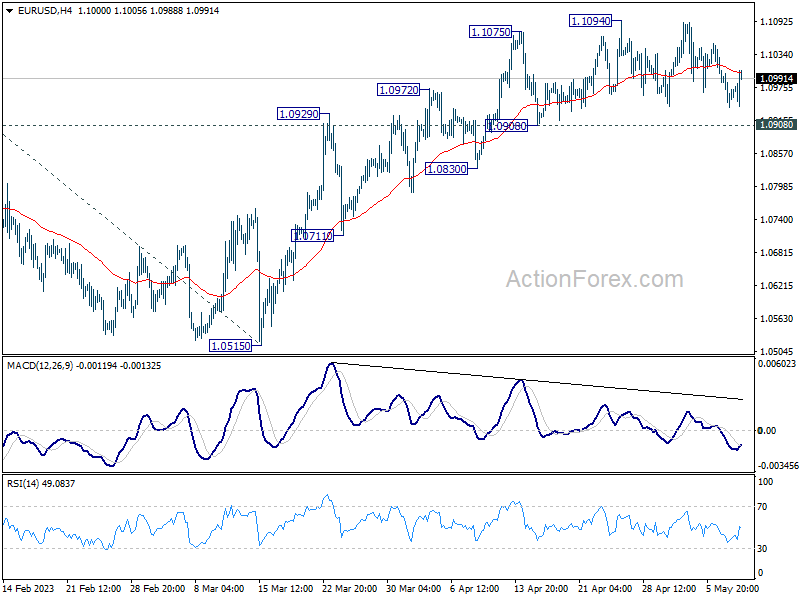

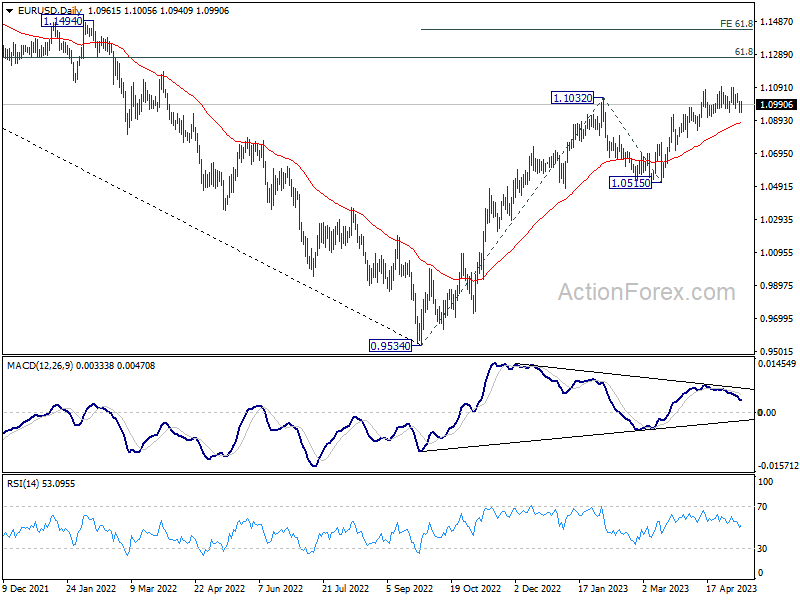

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0932; (P) 1.0970; (R1) 1.0999; More...

Intraday bias in EUR/USD remains neutral for the moment as consolidation from 1.1094 is extending. With 1.0908 support intact, further rally could be seen. On the upside, firm break of 1.1094 will resume larger up trend to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441 However, considering bearish divergence condition in 4H MACD, break of 1.0908 support will indicate short term topping and turn bias back to the downside.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

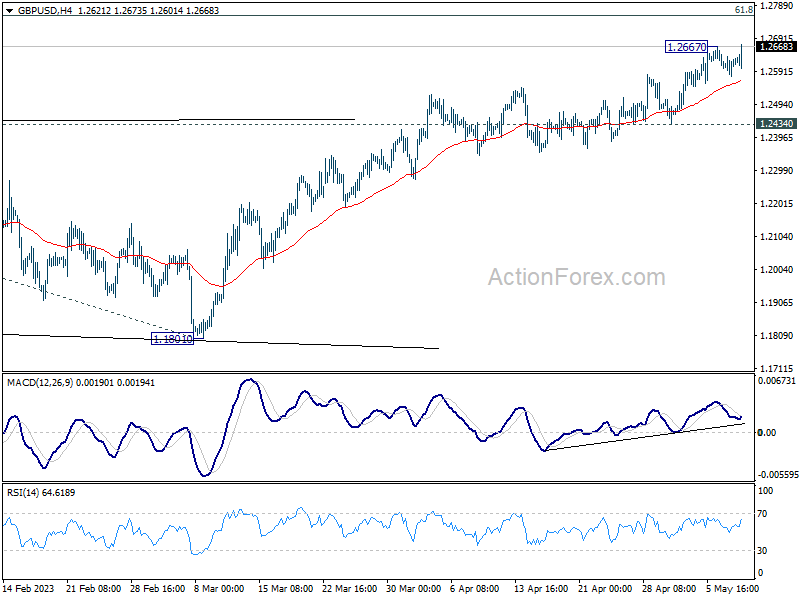

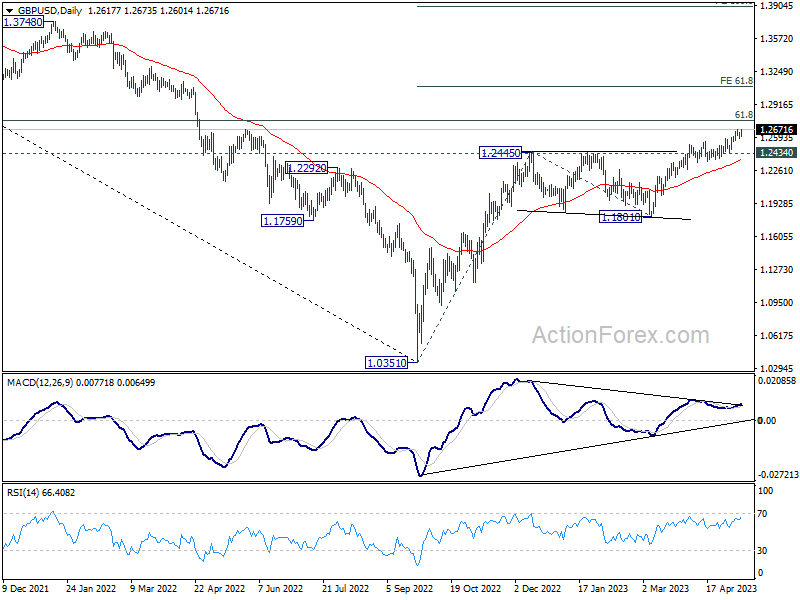

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2587; (P) 1.2613; (R1) 1.2648; More...

GBP/USD's up trend resumes by breaking 1.2667 temporary top. Intraday bias is back on the upside. Current rise should now target 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. In any case, outlook will remain bullish as long as 1.2434 support holds.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

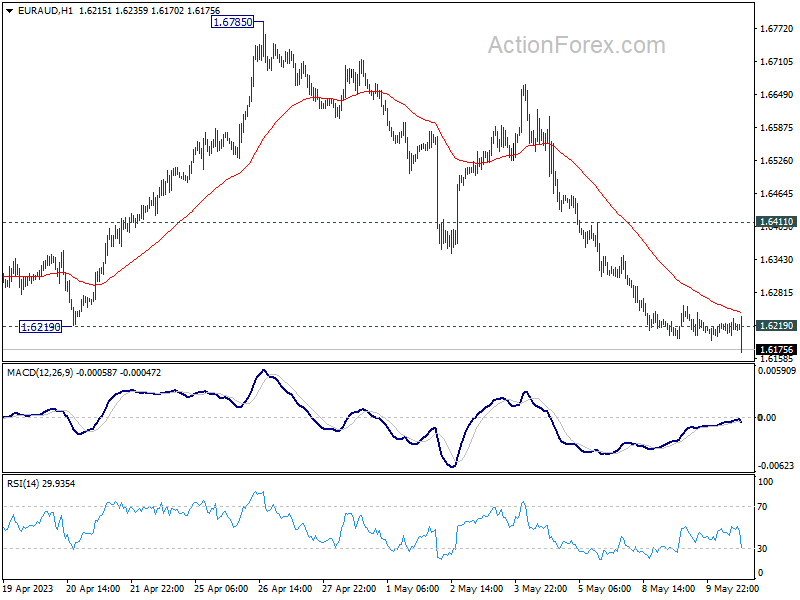

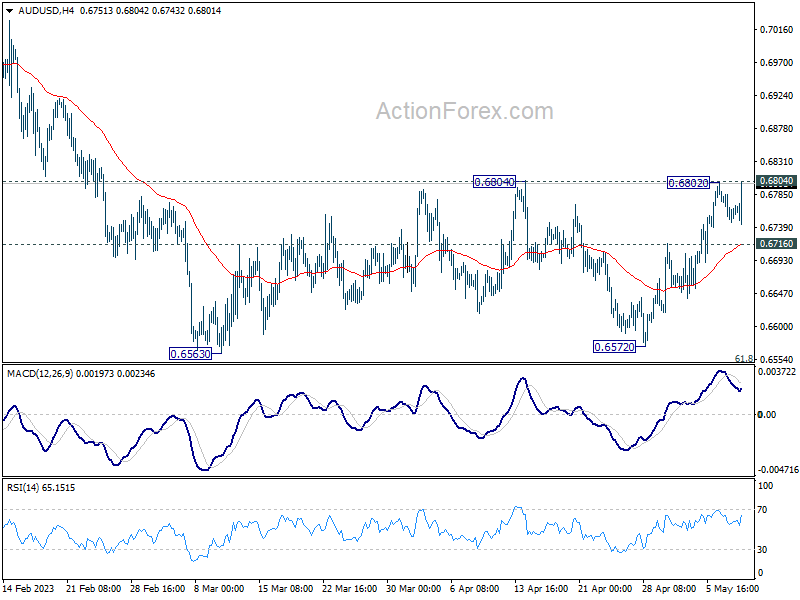

Dollar and Yield Down after US CPI, Aussie Firming Up

Dollar finds itself on the back foot in early US trading as data showed both headline and core CPI slowed in April. This data release has also sent 10-year yield plummeting below 3.5% mark. Japanese Yen is finding some strength, bolstered by the drop in yields. On the other hand, commodity currencies are regaining their footing, emerging as the strongest contenders at present, while European majors lag significantly. Euro, in particular, continues to show a lackluster response to hawkish comments from ECB officials.

From a technical perspective, EUR/AUD pair seems to be gaining downside momentum, potentially breaking away from 1.6219 support level finally. Given that the drop from 1.6785 may be a correction of the entire uptrend that began at 1.4281, deeper decline back the 1.5976 resistance-turned-support level is anticipated.

Meanwhile, AUD/USD pair's key resistance at 0.6804 should be closely watched. Sustained breach of this level would cement Aussie's near-term bullishness and could trigger a rally towards 0.7156 resistance level in AUD/USD.

In Europe, at the time of writing, FTSE is down -0.08%. DAX is down -0.25%. CAC is down -0.20%. Germany 10-year yield is down -0.064 at 2.284. Earlier in Asia, Nikkei dropped -0.41%. Hong Kong HSI dropped -0.53%. China Shanghai SSE dropped -1.15%. Singapore Strait Times dropped -0.02%. Japan 10-year JGB yield dropped -0.0090 to 0.416.

US CPI ticked down to 4.9% yoy in Apr, core CPI down to 5.5% yoy

In April, US headline CPI slowed from 5.0% yoy to 4.9% yoy, below expectation of 5.0% yoy. That was the smallest 12-month increased since April 2021. Core CPI (all items less food and energy) slowed from 5.6% yoy to 5.5% yoy, matched expectations. Energy index was down -5.1% yoy while food index was up 7.7% yoy.

For the month, CPI rose 0.4% mom while Core CPI also rose 0.4% mom. Both matched expectations. Energy index rose 0.6% mom. Food index was unchanged.

ECB Lagarde: We still have more ground to cover

ECB President Christine Lagarde said in a Nikkei interview, "we are determined to tame inflation, to bring it back to our 2% medium-term target in a timely manner." She acknowledged that "we have made a sizable adjustment already. But we still have more ground to cover".

Highlighting the importance of data, Lagarde said, "Our reaction function will be anchored in the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission, and this will dictate our decisions going forward."

She emphasized ECB's focus on headline inflation as the critical measure to ensure price stability. "That's our thermometer, that's what we are committed to doing," she stated.

However, Lagarde also pointed to the relevance of additional inflation measures. "Core" inflation is one such measure, but others exist, such as those that exclude more volatile items or focus more on domestic inflation pressures.

She explained, "It's to arrive at the 'heart' of inflation, the most persistent element in those price indexes that can help us understand where headline inflation is likely to settle in the medium term."

Lagarde cautioned that significant upside risks to inflation outlook still exist, and the path of inflation remains uncertain. Therefore, she stressed the need for the ECB to be "extremely attentive to those potential risks."

ECB Nagel: We're coming to the home stretch, but we need to stay stubborn

In an interview with Deutschlandfunk radio, Bundesbank President Joachim Nagel painted a cautiously optimistic picture of ECB's monetary policy landscape, implying that restrictive measures were beginning to bear fruit.

"We're coming to the home stretch in the sense that we are reaching the area in monetary policy that's considered restrictive," Nagel noted, suggesting that ECB's tightened policy stance was close to hitting its intended mark. He asserted his confidence that the monetary policy was indeed manifesting its effect.

However, he was quick to emphasize that ECB's task was far from complete. "But we are not done hiking yet," he added, "There is still work to be done on core inflation."

Nagel emphasized the importance of staying the course with the current monetary policy, urging persistence. "We need to stay stubborn," he said, reinforcing his commitment to seeing the central bank's measures through.

Addressing concerns about the potential impact of the ongoing banking sector upheaval in the US on German banks, Nagel sought to allay fears. "German banks are in a fundamentally solid position," he assured, indicating that he did not share the prevailing apprehensions over the stability of German banks.

ECB Stournaras: We can't yet say how many more rate hikes will happen

In an interview with Greece's Imerisia, ECB Governing Council member Yannis Stournaras indicated that while the end of the tightening cycle was in sight, it was not yet complete.

"We're close to the end," Stournaras remarked. But, "we're not there yet, so I agree with Madame Lagarde that we still have some distance to go."

Stournaras acknowledged the inherent uncertainty in projecting the number of additional rate hikes, with such decisions being heavily influenced by inflation forecasts, economic growth and the state of financial conditions.

"We can't yet say how many more rate hikes will happen," he said, tempering expectations for a concrete timeline. "As things stand today and if nothing dramatically changes, we can say that in 2023 rate hikes will end."

He also emphasized the persistence of current or potentially higher rates, a measure deemed necessary until inflation approaches the 2% target. "Rates will remain where they are today or higher for some time until inflation comes very close to the 2% target," he clarified.

BoJ Ueda: Too early to discuss exit strategy from massive stimulus

In an address to parliament today, BoJ Governor Kazuo Ueda stressed that it is premature to debate the specifics about exit strategy from the substantial stimulus program, which includes unloading its extensive holdings of exchange-traded funds.

He asserted that the central bank will discuss the exit strategy from its ultra-accommodative monetary policy and communicate this to the public only when conditions favor achieving stable inflation.

Governor Ueda pointed out that BoJ's ETF purchases have significantly contributed to bolstering consumption and capital expenditure. "We buy ETFs as part of our massive stimulus programme," he stated, suggesting that these purchases are critical components of Japan's broader economic stimulus efforts.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2587; (P) 1.2613; (R1) 1.2648; More...

GBP/USD's up trend resumes by breaking 1.2667 temporary top. Intraday bias is back on the upside. Current rise should now target 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. In any case, outlook will remain bullish as long as 1.2434 support holds.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Mar P | 97.50% | 97.90% | 98.00% | |

| 06:00 | EUR | Germany CPI M/M Apr F | 0.40% | 0.40% | 0.40% | |

| 06:00 | EUR | Germany CPI Y/Y Apr F | 7.20% | 7.20% | 7.20% | |

| 08:00 | EUR | Italy Industrial Output M/M Mar | -0.60% | 0.20% | -0.20% | |

| 12:30 | CAD | Building Permits M/M Mar | 11.30% | 2.30% | 8.60% | |

| 12:30 | USD | CPI M/M Apr | 0.40% | 0.40% | 0.10% | |

| 12:30 | USD | CPI Y/Y Apr | 4.90% | 5.00% | 5.00% | |

| 12:30 | USD | CPI Core M/M Apr | 0.40% | 0.30% | 0.40% | |

| 12:30 | USD | CPI Core Y/Y Apr | 5.50% | 5.50% | 5.60% | 5.50% |

| 14:30 | USD | Crude Oil Inventories | -2.2M | -1.3M |

US CPI ticked down to 4.9% yoy in Apr, core CPI down to 5.5% yoy

In April, US headline CPI slowed from 5.0% yoy to 4.9% yoy, below expectation of 5.0% yoy. That was the smallest 12-month increased since April 2021. Core CPI (all items less food and energy) slowed from 5.6% yoy to 5.5% yoy, matched expectations. Energy index was down -5.1% yoy while food index was up 7.7% yoy.

For the month, CPI rose 0.4% mom while Core CPI also rose 0.4% mom. Both matched expectations. Energy index rose 0.6% mom. Food index was unchanged.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a fresh increase from the 133.50 support zone. The US Dollar slowly moved higher above the 134.65 resistance zone against the Japanese Yen.

It is now consolidating above the 50-hour simple moving average. Immediate resistance on the upside is near the 135.35 level. The first major resistance is near the 135.65 level, above which the pair might start a decent increase.

The next major resistance is near the 137.30 zone. A clear break above the 137.30 resistance could push the price further higher toward 138.00.

If there is a fresh decline, support is near a bullish trend line at 135.00 and the 50-hour simple moving average. The next support sits near the 134.65 zone, below which there is a risk of more downsides toward the 133.50 level.