Sample Category Title

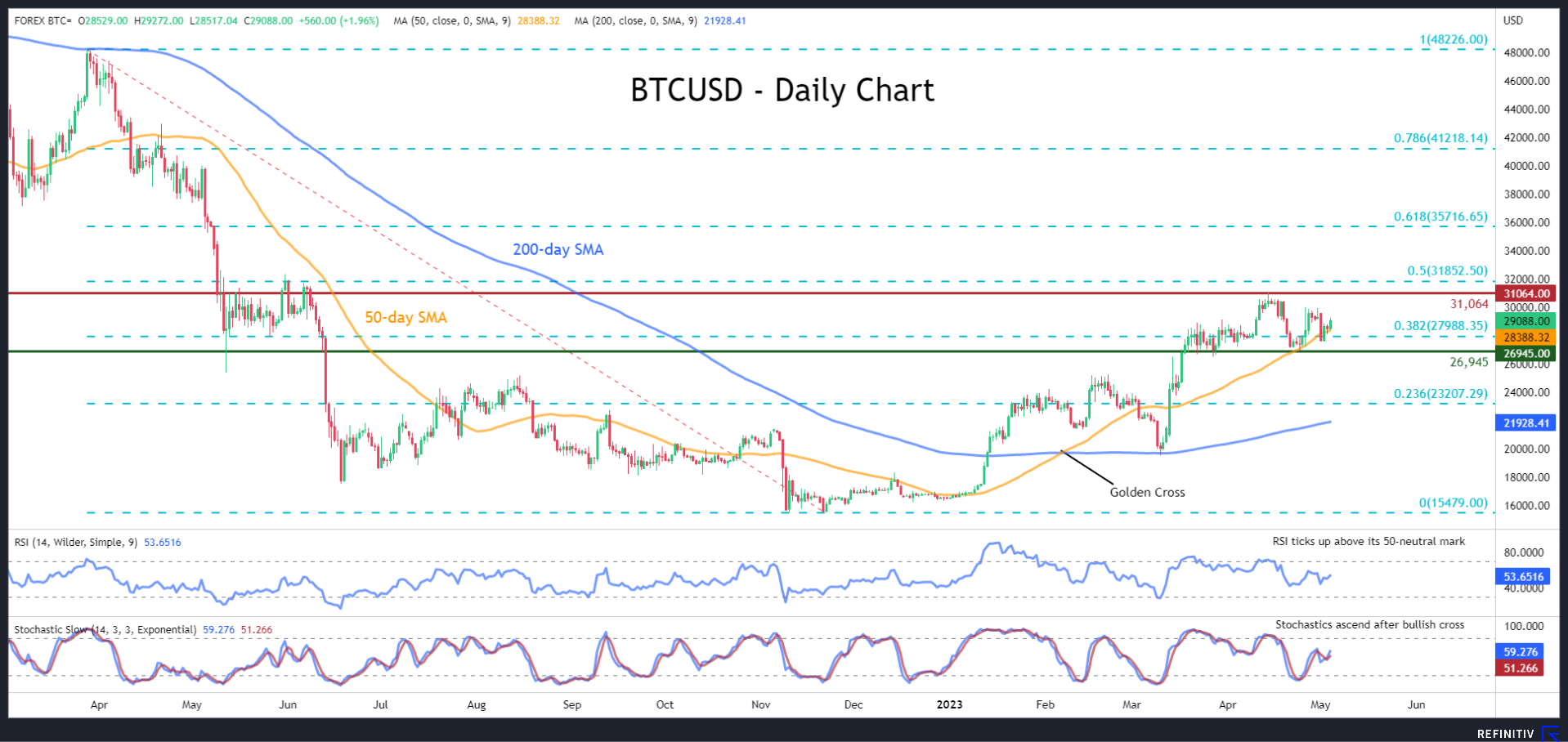

BTCUSD Recoups Losses after Slicing Through 50-day SMA

BTCUSD (Bitcoin) has been gaining ground after it managed to jump back above its 50-day simple moving average (SMA). However, should this latest rebound fail to strengthen, the price would be on track to extend its structure of lower highs, which is a bearish technical signal.

The momentum indicators currently suggest that near-term risks are tilted to the upside. Specifically, the RSI jumped above its 50-neutral mark, while the stochastic oscillator is ascending after posting a bullish cross.

Should buyers reclaim the 30,000 psychological mark and push the price higher, the 10-month peak of 31,064 could serve as initial resistance. Surpassing this region, Bitcoin may challenge 31,852, which is the 50.0% Fibonacci retracement of the 48,226-15,479 downleg. An upside violation of that territory could set the stage for the 61.8% Fibo of 35,716.

On the flipside, if the price drops beneath its 50-day SMA, the 38.2% Fibo of 27,988 might curb further retreats. Should that floor collapse, the bears could aim for the April low of 26,945. Failing to halt there, the king of cryptocurrencies could descend towards the 23.6% Fibo of 23,207.

In brief, BTCUSD has been attempting a rebound in the past few daily sessions after finding support at the 50-day SMA. Nevertheless, a fresh higher high is needed to revive bulls’ hopes for a sustained uptrend.

Bitcoin Aims Higher

Market picture

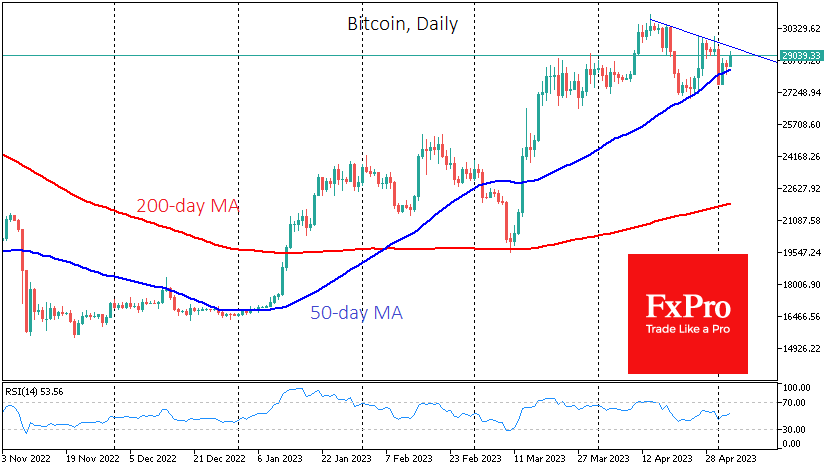

The crypto market has risen 1.5% in the last 24 hours to reach a capitalisation of $1.2 trillion. Almost all the gains have come since the start of the day, coinciding with a fresh bout of fear surrounding US regional banks.

US index futures have risen modestly since the start of the day as the banking problems bring a monetary policy reversal closer. And that is another reason for buyers, in this case, medium-term buyers, to be happy.

The bulls in Bitcoin have pushed the price to $29K, consolidating above the 50-day moving average. This is an essential signal of a medium-term uptrend. Short-term attention is focused on the $29.4K area, where Bitcoin fell earlier this month, and resistance runs through the local highs of mid to late April. A move higher would pave the way for another test of highs for almost a year.

According to Santiment, bitcoin whales increased their holdings of the first cryptocurrency by 64,000 BTC in April, contrary to the view that the final direction of the asset’s movement has yet to take shape. Major investors continue to believe that there are growth prospects for BTC.

News background

Former Coinbase CTO Balaji Srinivasan lost a $1 million bet on Bitcoin’s rise. He bet BTC would reach $1 million by 17 June but conceded defeat before the deadline. “I burned a million to show everyone how the US government is printing trillions of dollars out of thin air,” the businessman tweeted.

The US president’s administration has proposed a 30% tax on crypto miners to make them more aware of the damage they are doing to the climate. The proposed tax will raise about $3.5 billion over ten years.

Robert Francis Kennedy Jr, a nephew of the 35th US President John F. Kennedy, criticised the SEC and FDIC for their “war on cryptocurrencies”, which he said had led to a banking crisis in the country.

The introduction of retail central bank digital currencies (CBDCs) will lead to “many unintended consequences”, said IMF chief Kristalina Georgieva. Florida Governor Ron DeSantis has vowed to ban the digital dollar in his state.

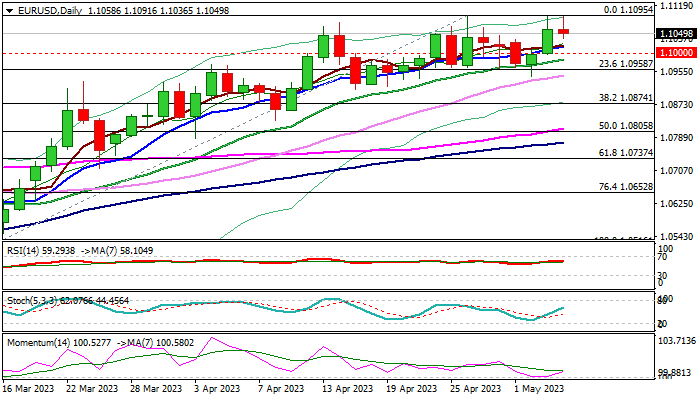

EUR/USD: Bulls Remain Fully in Play But Need Break of Key 1.1095 Barrier to Resume

The Euro is holding firm tone and trading near 2023 high (1.1095) in European trading on Thursday, ahead of ECB policy decision.

Post-Fed rally on Wednesday on 25 bps hike but dovish US central bank’s stance, pushed the price into the upper part of near-term range, though with insufficient strength to break key barrier at 1.1095.

Traders await further signals from the ECB, which is on track to raise interest rates for the seventh time in a row, with open debate about the size of hike, as 25 and 50 bps are both on the table.

Markets slightly favor 25 bps increase, which will signal a slowdown after three straight hikes by 50 basis points but will likely not signal an end of tightening cycle, in which the central bank raised rates by a record 350 bps since July 2022, as primary aim to bring inflation to 2% target is still away and more policy tightening is likely to be expected in the near future.

Technical structure on daily chart remains firmly bullish as moving averages are in positive configuration and the price is gaining bullish momentum.

I addition, false break of key near-term support at 1.0960 (Fibo 23.6% of 1.0516/1.1095) generated bullish signal on formation of a bear-trap pattern, as well as leaving a higher base after a multiple failure at this zone.

Immediate bullish bias is expected to remain while the price stays above psychological 1.10 support and keep focus firmly at the upside for eventual break of 1.1095 pivot, which would signal a continuation of a larger uptrend from 0.9535 (2022 low) towards targets at 1.1195/1.1274 (200WMA / Fibo 61.8% retracement of 1.2349/0.9535 downtrend).

Res: 1.1095; 1.1154; 1.1195; 1.1274.

Sup: 1.1020; 1.1000; 1.0960; 1.0909.

EUR/USD Edges Lower, ECB Expected to Raise Rates

- ECB expected to raise rates by 25 bp

- Federal Reserve hikes rates by 25 bp

- Powell signals a pause in June

EUR/USD is trading quietly on Thursday, ahead of the ECB decision later today.

ECB expected to hike, but by how much?

All eyes are the ECB, which is expected to raise rates at today’s meeting. The burning question remains will the central bank increase rates by 25 or 50 basis points? The eurozone April inflation report, published Tuesday, didn’t provide any insights as both the headline and core readings barely moved and were very close to the estimates. Headline CPI came in at 7.0% and the core rate at 5.6%, which is well above the 2% target and much too high for the ECB.

The Bank has been aggressive in its rate-tightening cycle and raised rates by 50 bp in March. Another 50-bp increase would help in the fight against inflation but also raise the likelihood of a recession due to the economy slowing down too abruptly. The markets are leaning closer to a 25-bp hike (80% probability) over a 50-bp increase (20% probability).

The Federal Reserve raised rates by 25 bp on Wednesday, to the surprise of no one. Investors were more interested in what is coming next, and Jerome Powell did hint that this hike would be the final one after 10 straight rate hikes. The rate statement was somewhat dovish, with the Fed removing the phrase “some additional” rate hikes might be needed. It changed the language that said that it would examine various factors in “determining the extent” that further hikes would be needed.

Powell sounded more hawkish in the press conference, saying that higher interest rates had not sufficiently slowed down the economy, the labour market or inflation. Just to be crystal clear, Powell said that “inflation pressures continue to run high, and the process of getting inflation back down to 2% has a long way to go”.

A rate cut, anyone? Powell said in his remarks that the inflation outlook does not support a rate cut. The markets disagree and have priced in an 81% rate cut in September (51% chance of 25-bp cut and 30% of 50-bp cut). Inflation is on its way down, but the pace of the deceleration could well determine if the Fed trims rates before the end of the year.

EUR/USD Technical

- EUR/USD tested resistance at 1.1088 earlier. The next resistance line is 1.1157

- 1.1025 and 1.0956 are providing support

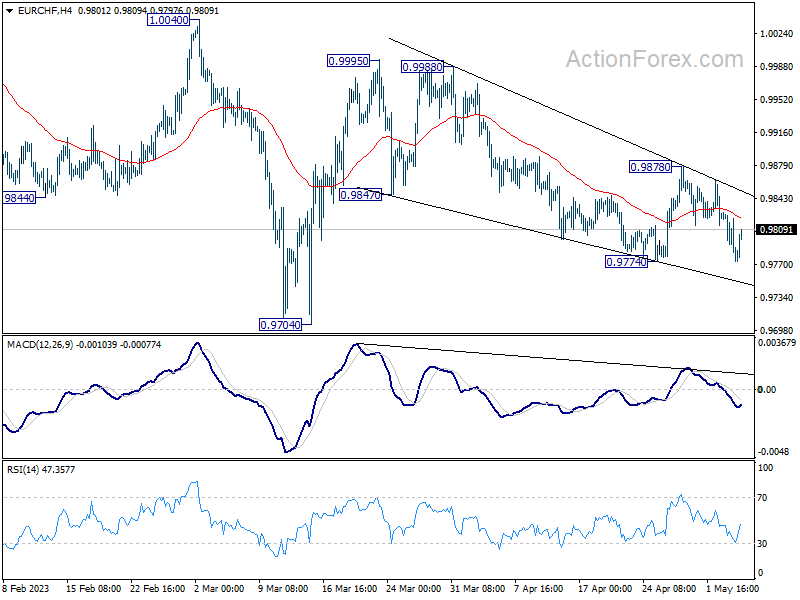

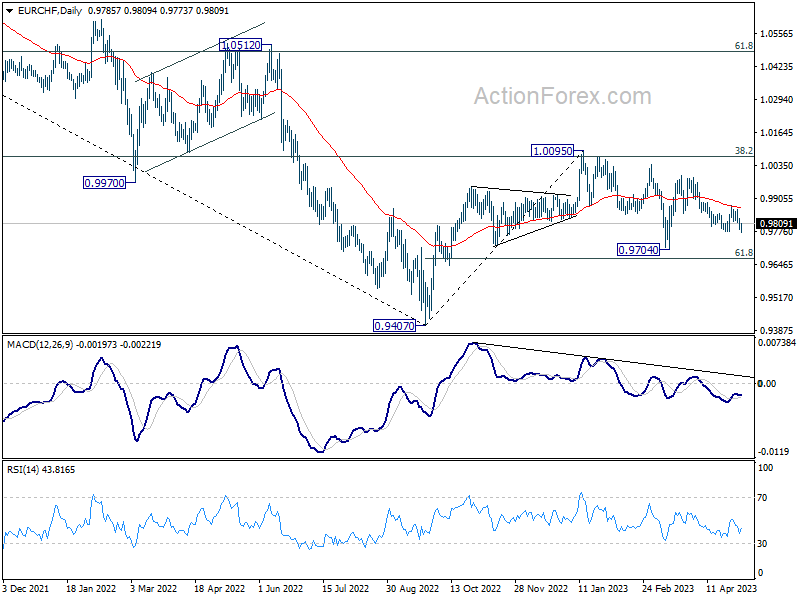

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9765; (P) 0.9797; (R1) 0.9813; More...

Despite a breach of 0.9774, EUR/CHF quickly recovered. While fall from 0.9995 could extend lower, downside should be contained well above 0.9704. Outlook is unchanged that whole correction from 1.0095 has completed at 0.9704. Break of 0.9878, and sustained trading above 55 D EMA (now at 0.9869) will affirm this bullish case, and target 0.9995 resistance next.

In the bigger picture, prior rejection by 55 W EMA (now at 0.9972) and 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. That is, down trend from 1.2004 is not completed yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

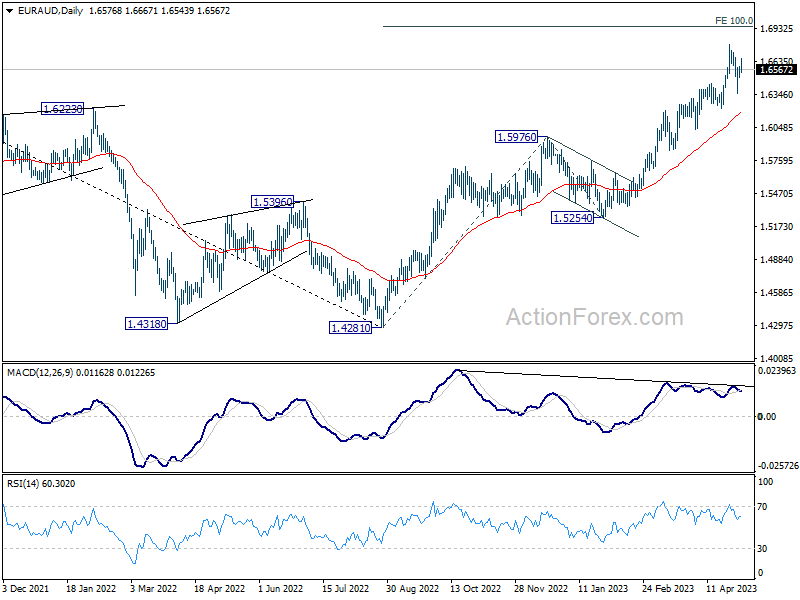

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6521; (P) 1.6557; (R1) 1.6614; More...

EUR/AUD is staying in consolidation from 1.6785 and intraday bias remains neutral. Further rally is expected as long as 1.6219 support holds. Break of 1.6785 will resume larger up trend to 100% projection of 1.4281 to 1.5976 from 1.5254 at 1.6949. However, firm break of 1.6219 will argue that larger correction is on the way.

In the bigger picture, the solid break of 1.6434 resistance argues that whole down trend from 1.9799 (2020 high) has completed at 1.4281 (2022 low). Further rise should be seen to 61.8% retracement of 1.9799 to 1.4281 at 1.7691 next. For now, outlook will stay bullish as long as 1.5976 resistance turned support holds, even in case of deep pull back.

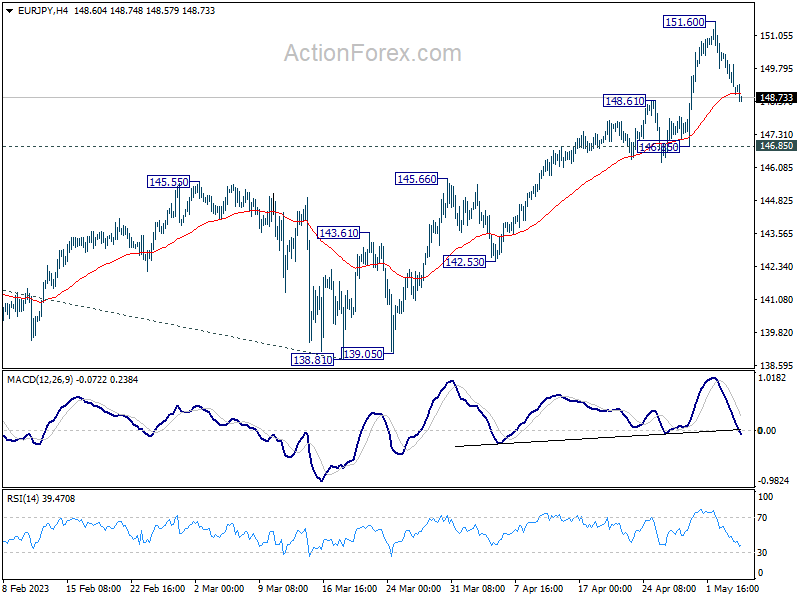

EUR/JPY Daily Outlook

Daily Pivots: (S1) 148.68; (P) 149.53; (R1) 149.99; More....

Intraday bias in EUR/JPY remains neutral as consolidation from 151.60 is extending. Downside should be contained by 146.85 support to bring another rally. Break of 151.60 will resume larger up trend to 153.64 projection level. Nevertheless, firm break of 146.85 will confirm short term topping and turn bias to the downside for deeper pull back.

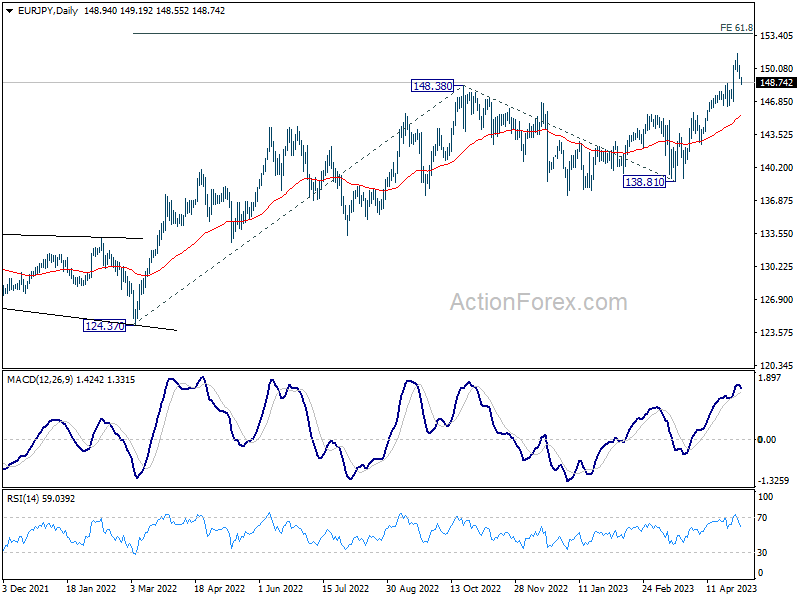

In the bigger picture, current development indicates that rise from 114.42 (2020 low) is in progress. Next target is 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64. Sustained break there will pave the way to 100% projection at 162.82. For now, medium term outlook will remain bullish as long as 138.81 support holds, even in case of deep pull back.

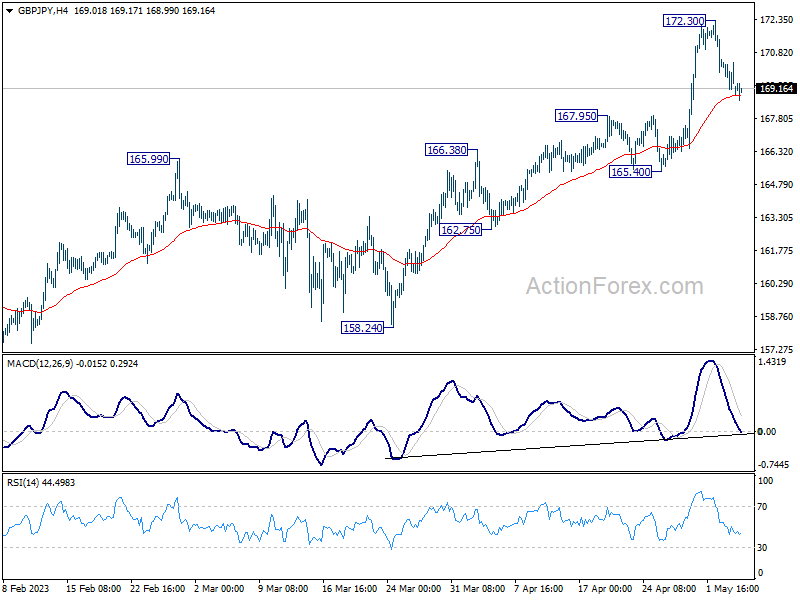

GBP/JPY Daily Outlook

Daily Pivots: (S1) 168.88; (P) 169.64; (R1) 170.14; More...

Intraday bias in GBP/JPY stays neutral for the moment as consolidation from 172.30 is extending. Downside should be contained by 167.95 resistance turned support to bring another rally. On the upside, break of 172.30 will resume larger up trend to 100% projection of 148.93 to 172.11 from 155.33 at 178.51. Nevertheless, firm break of 167.95 should confirm short term topping, and turn bias back to the downside for deeper pull back to 165.40 support instead.

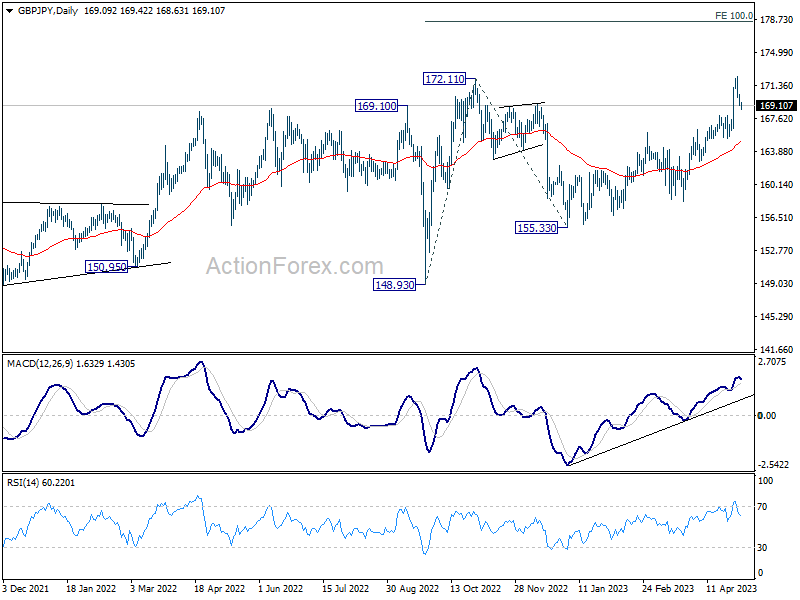

In the bigger picture, based on current momentum, up trend from 123.94 (2020 low) is likely ready to resume. Next target is 161.8% projection of 122.75 (2016 low) to 156.59 (2018 high) from 123.94 at 178.69. This will now remain the favored case as long as 165.40 support holds, in case of retreat.

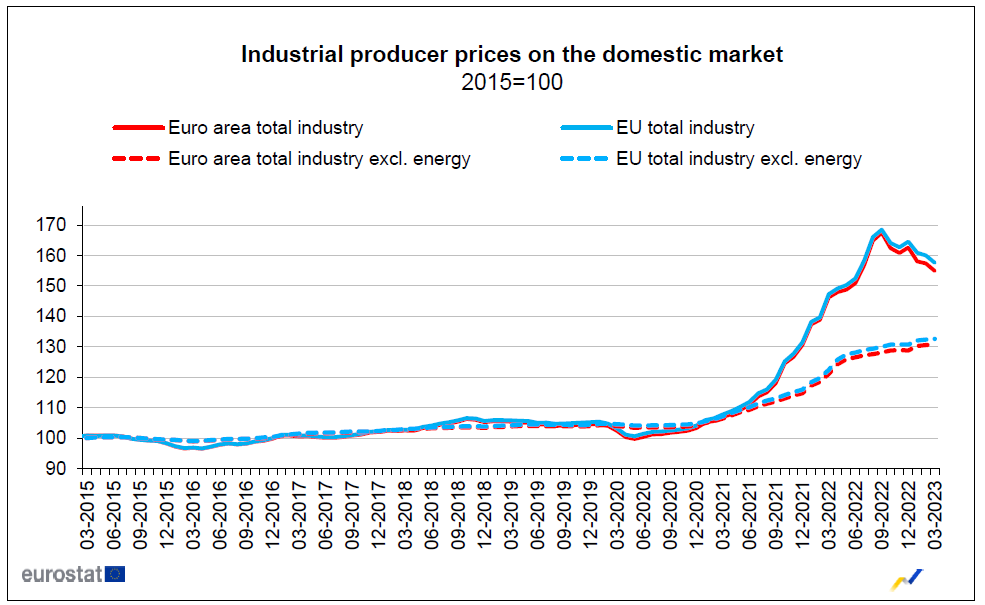

Eurozone PPI at -1.6%mom, 5.9% yoy in Mar

Eurozone PPI came in at -1.6% mom, 5.9% yoy in March, versus expectation of -1.4% mom, 5.9% yoy. For the month, industrial producer prices decreased by -4.8% in energy sector and by -0.4% for intermediate goods, while prices increased by 0.2% for capital goods, by 0.3% for durable consumer goods and by 0.9% for non-durable consumer goods. Prices in total industry excluding energy increased by 0.2%.

EU PPI came in at -1.5% mom, 7.0% yoy. The largest monthly decreases in industrial producer prices were recorded in Greece (-7.3%), Ireland (-4.6%) and Lithuania (-4.0%), while the highest increases were observed in Cyprus (+2.4%), France (+2.0%) and Croatia (+0.5%).

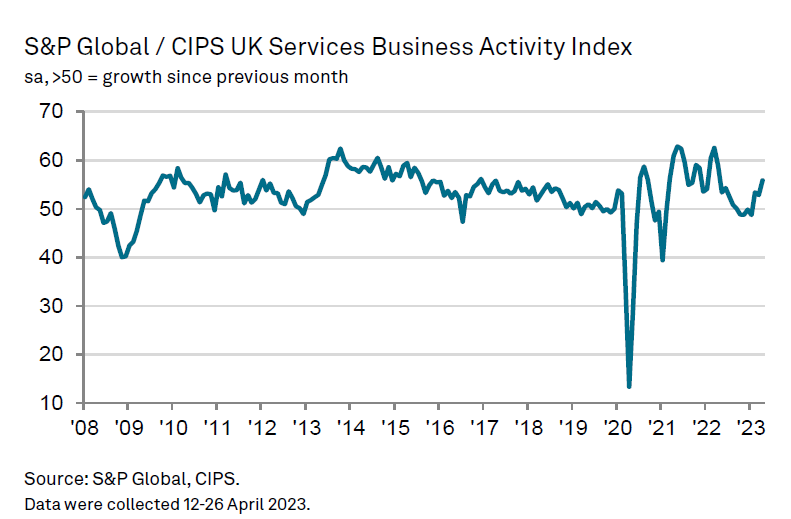

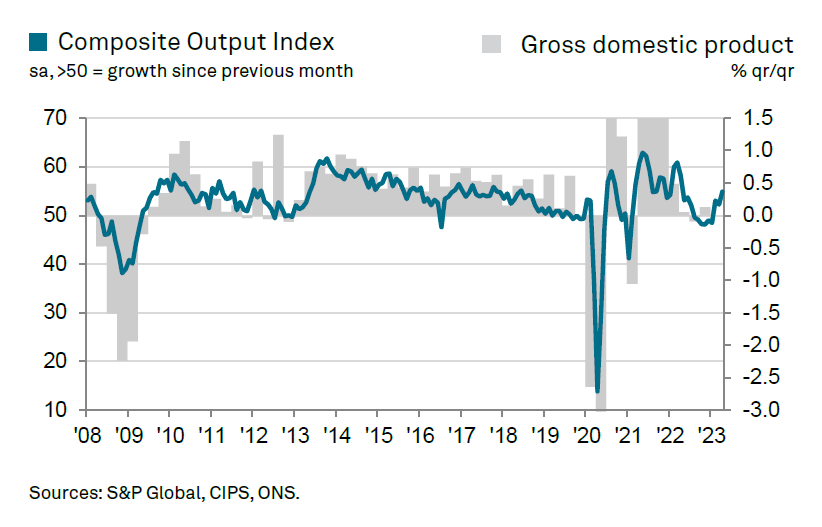

UK PMI services finalized at 55.9, reignited inflationary pressures

UK PMI Services were finalized at 55.9 in April, marking a significant increase from March's 52.9 and the highest reading since April 2022. S&P Global highlighted that demand conditions continued to improve, with higher salary payments contributing to steeper cost inflation. PMI Composite was finalized at 54.9, up from March's 52.2.

Tim Moore, Economics Director at S&P Global Market Intelligence, stated, "A strong rate of service sector growth meant that the UK economy started the second quarter of 2023 in positive fashion. Overall private sector output expanded at the fastest pace for one year, despite another fall in manufacturing production during April."

Moore added that service providers experienced the steepest upturn in new work for 13 months, as resilient consumer spending combined with a turnaround in demand for business services to boost overall order books. However, he also noted that the swift rebound in customer demand appears to have reignited inflationary pressures, with around 34% of the survey panel reporting a rise in their prices charged in April, roughly three times higher than the pre-pandemic average.