Sample Category Title

EURUSD Retests 13-month High Ahead of ECB Meeting

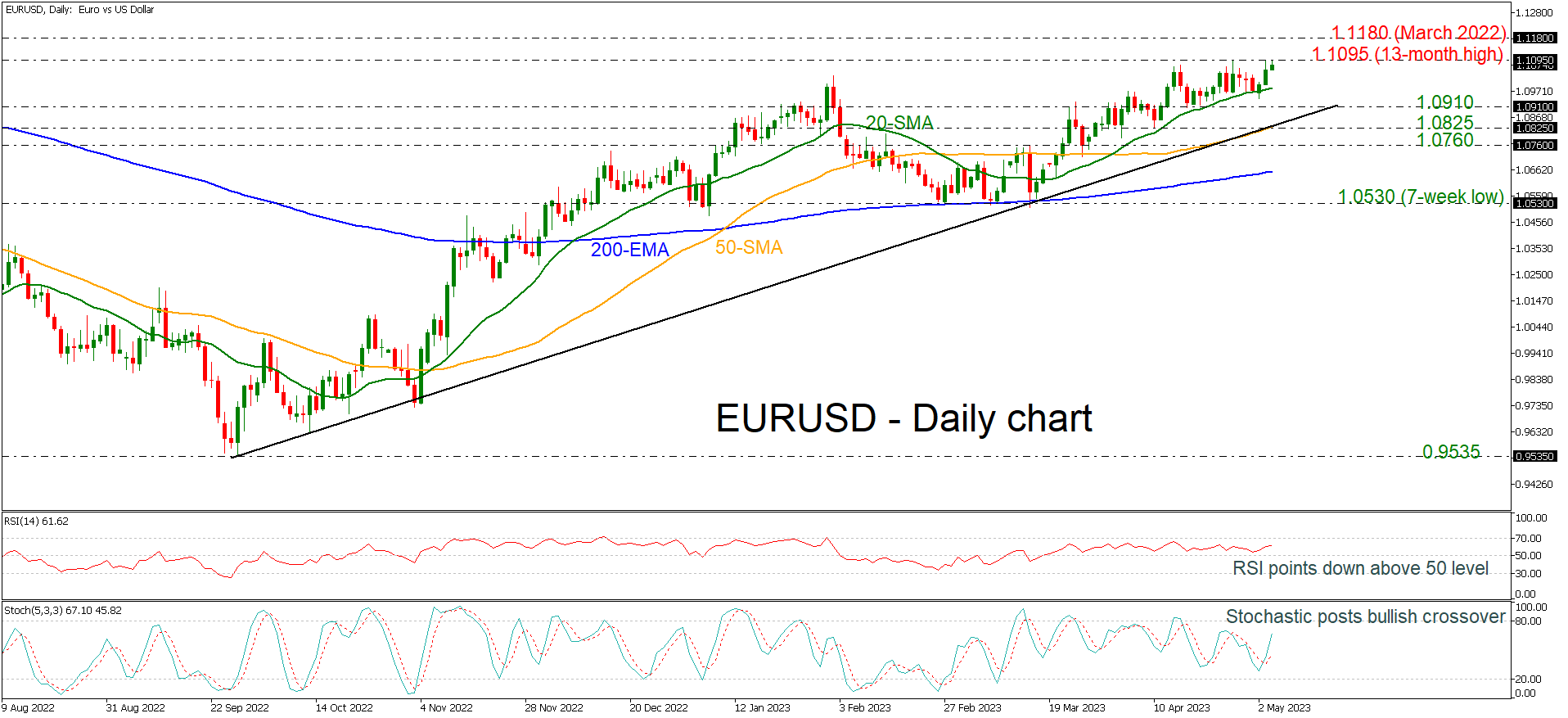

EURUSD is attempting once more to climb above the 13-month high of 1.1095, endorsing the long-term upside structure. This outlook is reinforced by the RSI, which is rising and remaining above its neutral threshold of 50. In addition, the stochastic oscillator displayed a bullish crossover between its %K and %D lines and is approaching the overbought area.

In the event of an upward price movement, the immediate 13-month high of 1.1095 that coincides with the 200-weekly simple moving average (SMA) may act as a barrier before the March 2022 high of 1.1180 can be challenged. Above these levels, the 1.1500 psychological mark, registered in February 2022 may halt bullish actions.

On the other hand, any declines should reach the 20-day SMA at 1.0980 prior to encountering the subsequent obstacles at 1.0910 and 1.0825, which are located close to the 50-day SMA. A drop below the long-term uptrend line could pave the way for the 1.0760 support and, more significantly, the 200-day EMA at 1.0650, thereby neutralizing the outlook.

To conclude, given that the pair is trading above the short-term SMAs and the uptrend line, the market appears to be in a bullish phase.

Asian Stock Markets Rejoiced Post-FOMC

- US stock indices spooked by Fed Chair Powell’s “hawkish” comments.

- USD sold off while safe haven currencies, JPY & CHF in demand.

- Asian stock market outperformed while Hong Kong indices rebounded from the key 200-day moving average.

No surprise from the US central bank, Federal Reserve’s policy meeting outcome yesterday where the Fed hiked its policy Fed funds rate by 25 basis points as expected, its 10th hike in this current tightening cycle to a target range of 5% to 5.25%.

Most importantly, it has signalled a potential pause on its current interest hiking cycle via a change of tonality in its monetary policy statement; it no longer says it “anticipates” further rates will be needed, only that it will watch incoming data to determine if more hikes “may be appropriate.”

The surprising bit came during Fed Chairman Powell’s press conference where he made several “hawkish” comments that implied the current stance of the Fed’s operating modus to be skewed towards inflation targeting rather than to address the potential credit crunch from the US regional banking turmoil that can lead to slower economic growth and a weak labour market;

“Conditions in the banking sector have improved.”

“We’re committed to our inflation target of 2%.”

“The labour market remains very tight.”

“The case of avoiding a recession is more likely than having one.”

Overall, the US stock market did not respond positively to such comments and sold off with all three major indices ending the US session with losses; S&P 500 (-0.70%), Nasdaq 100 (-0.64%) and Dow Jones Industrial Average (-0.80%).

The underperformers were the financials and banks with the SPDR S&P Regional Banking ETF plummeting by -1.80% as fears of further stress on the balance sheets of the US regional banks persist. Not helping much to alleviate such fears was the latest negative news flow from PacWest Bancorp, a California-based mid-sized US bank that saw its share price plunged by -50% in after-hours trading when it announced that it was exploring a strategic sale.

A rate cut is priced in for the September FOMC

Despite the hawkish tonality from Fed Chair Powell, markets are still expecting a Fed pivot to kickstart a fresh interest rate cut cycle before 2023 ends. Based on the CME Watch FedWatch tool derived from pricing data implied by the 30-day Fed Funds futures has indicated an 89% chance of a 25 basis points rate cut during the 20 September 2023 FOMC meeting.

This heightened expectation of a first Fed funds rate cut in September has led the front end of the US Treasury yield curve which is more sensitive to changes in monetary policy to drop more than the longer end; the 2-year US Treasury yield dropped by 16 basis points to close yesterday US session at 3.81%, a five-week low.

USD sold off & safe haven currencies, JPY and CHF in demand

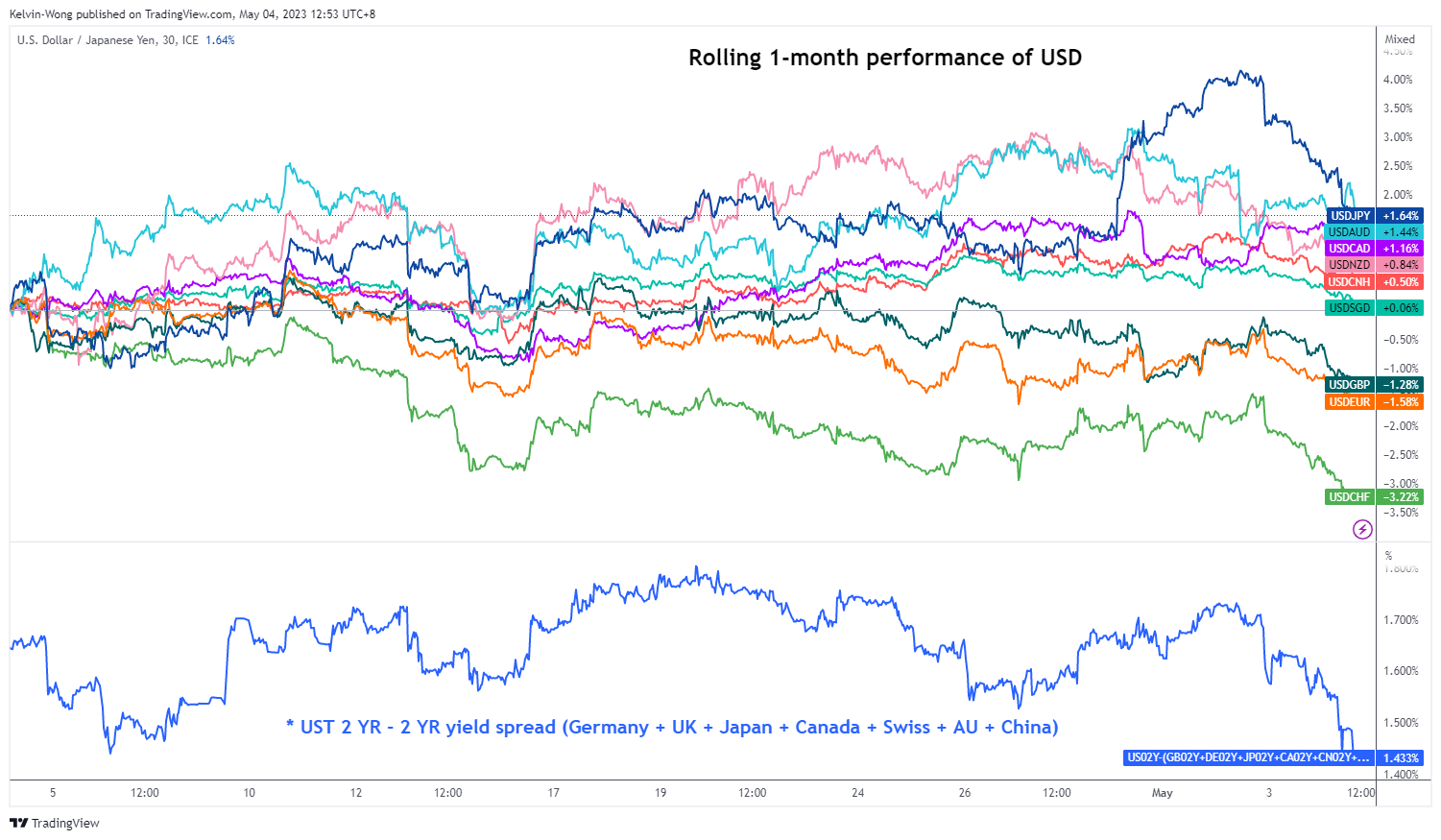

Fig 1: Rolling 1-month performance of USD against major currencies with CNH & SGD as of 4 May 2023

(Source: TradingView, click to enlarge chart)

The recent drop in the 2-year US Treasury yield has led to a further compression of the 2-year US Treasuries yield premium against the rest of the world; US yield over a basket of equally weighted sovereign yields of Germany, United Kingdom, Japan, Canada, Switzerland, Australia, and China has shrunk to 1.43% from 1.73% seen at the start of this week.

The shrinkage of the US yield premium factor explains the current weakness seen in the US dollar as for the heightened overnight demand for the JPY and CHF, it can be attributed to the typical “flight to safe haven” sentiment due to persistent share price weakness of the US regional banks that triggered a resurgence of systemic risk and heightened geopolitical tensions in the on-going Russia-Ukraine conflict where the Kremlin was hit by a drone attack.

Interestingly, last Friday’s gains of the USD/JPY induced by the Bank of Japan’s dovish monetary policy stance have been wiped out as it dropped by 330 pips from its recent 2 May high of 137.77 to 134.50 and traded below the key 200-day moving average at this time of the writing.

Asian stock indices outperformance against the US

Fed Chair Powell spooked US stock traders post-FOMC press conference while the Asian stock market rejoiced today. Most of the Asian benchmarks have recorded intraday gains with Hong Kong being the top performer; Hang Seng Index (+1%), Hang Seng China Enterprise Index (+1.6%) and Hang Seng TECH Index (+0.6%). Even the mainland China CSI 300 recorded just a minor loss of -0.1% after it reopened today from its Labour Day Golden Week holiday despite a consensus forecast miss on the China Caixin Manufacturing PMI that contracted to 49.5 in April from 50.0 printed in March.

Two primary reasons that account for today’s Asian stock indices’ robust performances. Firstly, it is the broad-based USD dollar weakness that also led to a drop in the USD/CNH (offshore yuan) to print a 5-day low of 6.8965 which implied a lower cost of funding on US dollar-dominated corporation debts in Asia.

Secondly, it is momentum driven; both Hang Send Index and Hang Seng China Enterprise Index have managed to retest and staged a rebound right at their respective 200-day moving averages yesterday where it has triggered by positive follow-through today supported by a weaker US dollar. Short-term traders chased such bullish technical signals which in turn created a positive feedback loop.

Hong Kong 33 Technical Analysis – Positive elements sighted at key 200-day moving average

Fig 2: Hong Kong 33 trend as of 4 May 2023 (Source: TradingView, click to enlarge chart)

The recent multi-week decline of -7% seen on the Hong Kong 33 Index (a proxy for the Hang Seng Index futures) from its 17 April 2023 high of 20,873 has managed to retest, staged a rebound and formed a “higher low” right at its key 200-day moving average where it has traded above it since 22 March 2023.

Current price actions suggest the Index may now have started to evolve into a short-term ascending channel in place since the 20 March 2023 low of 18,831 which implies a potential short-term uptrend may be in progress above the 19,500 key short-term pivotal support.

A clearance above the 20,300 intermediate resistance may see the next resistance coming in at 21,020 in the first step. However, a break with a four-hour close below 19,500 invalidates the short-term uptrend to expose the next support at 18,900.

Fairly Calm Build-up to ECB Policy Meeting

Markets

The Fed yesterday raised policy rates by the expected 25 bps to 5-5.25%. The job market is robust, unemployment low and inflation elevated. At the same time, the recent banking stress did result in tighter credit conditions of which the impact remains uncertain. This brought about a more neutral policy guidance. The Committee no longer formally anticipates “some additional policy firming” but it does not rule it out outright either: “In determining the extent to which additional policy firming may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.” In practice this means the Fed, at least temporary, hit the pause button in the tightening cycle. Markets went further and called the end. Chair Powell during the press conference pushed back against the idea of rate cuts by the end of the year, referring to expectations of inflation to decline only slowly. But markets doubled down nonetheless, pricing in about 75 bps by the end of the year. US yields were pressured lower across the curve with changes between 3 bps (30-y) to 15.6 bps (2-y). The move down was reinforced by a Bloomberg report that PacWest, another regional bank under market scrutiny, is weighing “strategic options”, including a sale. Similar headlines preceded First Republic Bank’s eventual takeover. PacWest’s share tumbled 60% in after-market trading, putting markets on edge. The dollar slid. EUR/USD came close to the YtD high of 1.1095 but eventually closed at 1.106 with most of the appreciation having occurred in the run-up to the Fed meeting. The trade-weighted index eased to 101.34. The yen was yesterday’s star performer. USD/JPY fell below 135 with the intraday move covering almost two big figures. US indices ended between 0.46% and 0.80% in the red.

Yesterday’s fall-out on Asian markets this morning is relatively limited, meaning a fairly calm build-up to this afternoon’s ECB policy meeting. Admittedly, Japan is closed for business. Money markets expect Frankfurt to ease the tightening pace and raise rates by 25 bps to 3.25%. Analyst estimates shifted from 50 bps last week to 25 bps as well, following this week’s inflation numbers and BLS. We do not think that an acceleration to 7% headline inflation and near-record core inflation of 5.6% justifies a downshift of the pace just yet. And while the BLS did reveal a significant further tightening of credit conditions, it didn’t come as a huge negative surprise. It is indeed what the ECB and its policy is aiming for. In contrast to the Fed, the ECB won’t hint at a pause anytime soon. That clearer tightening bias should both support German/European yields and the euro. EUR/USD is currently testing the YtD high. It won’t take much euro strength for a break higher. That brings 1.1274 (61.8% retracement of the 2021-2022 decline) on the radar.

News Headlines

The Czech National Bank kept its policy rate unchanged at 7%. Unlike previous meetings, three (vs one) out of seven governors voted in favour of hiking rates by 25 bps. The Bank Board will wait for further data and will assess them. It will decide at its next meeting whether rates will remain unchanged or increase. The threat of inflation expectations becoming unanchored, the related risk of a wage-price spiral and expansionary fiscal policy are the key upside inflation risks. In its updated baseline scenario, the CNB expects inflation to average 11.2% in 2023 (from 10.8% in February) before falling to 2.1% in 2024 (unchanged). This suggests that real interest rates are to become distinctly positive for the first time in many years as the CNB pushes back against premature market expectations regarding the timing of a first rate cut. A stronger than expected Czech koruna in the meantime did part of the lifting, creating tighter monetary conditions. The CNB now pencils in an average EUR/CZK rate of 23.7 for this year compared to 24.5 in February. Next year, the average expected FX rate stands at 24.30. The central bank raised its GDP forecasts for this year and next from respectively -0.3% and 2.2% to +0.5% and 3%, but remains cautious on consumption and notes slowdown in growth of bank loans to households and firms. Czech swap rates added up to 25 bps at the front end of the curve yesterday with the 10-yr segment around 10 bps higher. The Czech koruna profited only modestly in a volatile risk environment and ahead of today’s ECB decision with at EUR/CZK 23.50 holds near strongest CZK-levels since 2008.

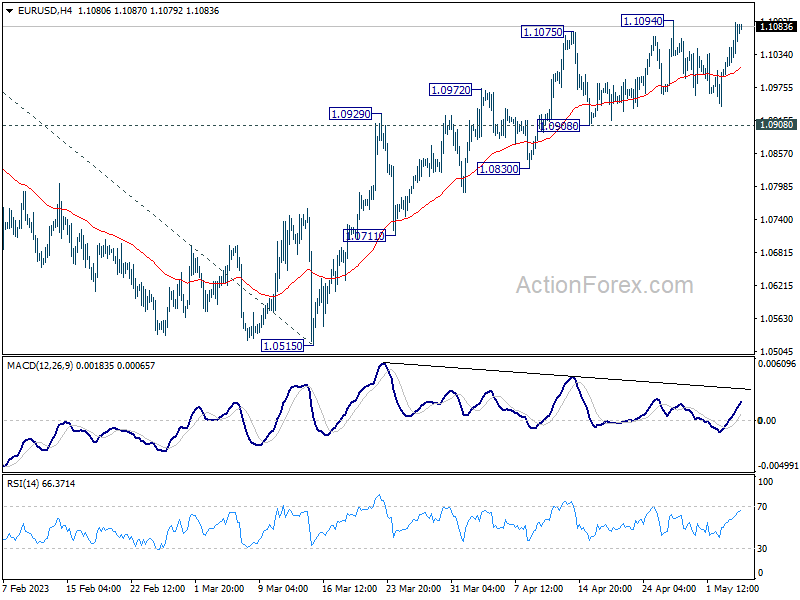

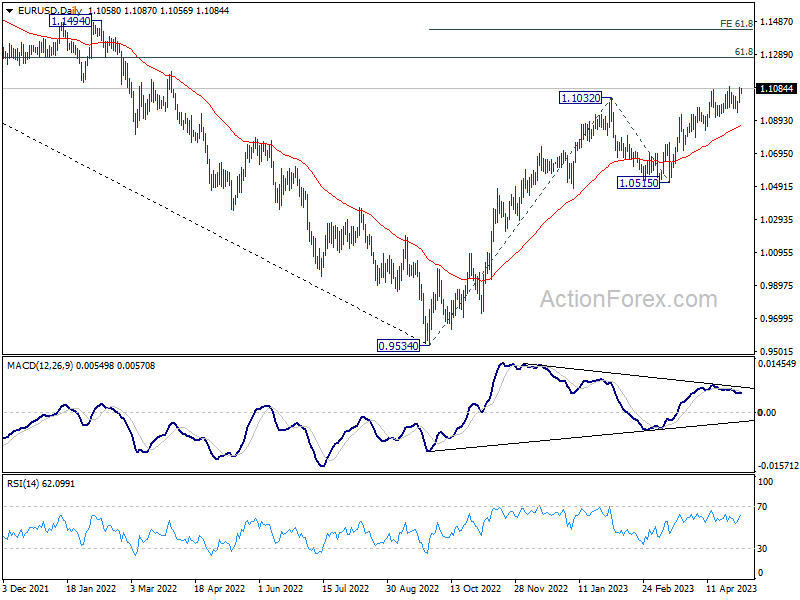

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1010; (P) 1.1051; (R1) 1.1103; More...

EUR/USD is still held below 1.1094 resistance despite current recovery. Intraday bias remains neutral first but further rise is expected. On the upside, firm break of 1.1094 will resume larger up trend to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441 However, considering bearish divergence condition in 4H MACD, break of 1.0908 support will indicate short term topping and turn bias back to the downside.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

Dollar Down after Fed, Gold Eyes Record, Euro Awaits ECB

Dollar was sold off broadly overnight after Fed indicated openness to a pause in tightening after raising interest rate by 25bps. Yet, selloff is relatively limited after Chair Jerome Powell ruled out a rate cut this year. Indeed, major stock indexes ended slightly lower, as weighed by persistent concerns over regional banks in the US.

Indeed, Canadian Dollar is the worst performer for the week so far, as dragged down by the steep decline in oil prices. Dollar is only second worst, followed by Sterling. Swiss Franc and Yen are the best performers as supported by decline in global benchmark yields, and risk-off sentiment. Euro is mixed for now, awaiting ECB rate decisions.

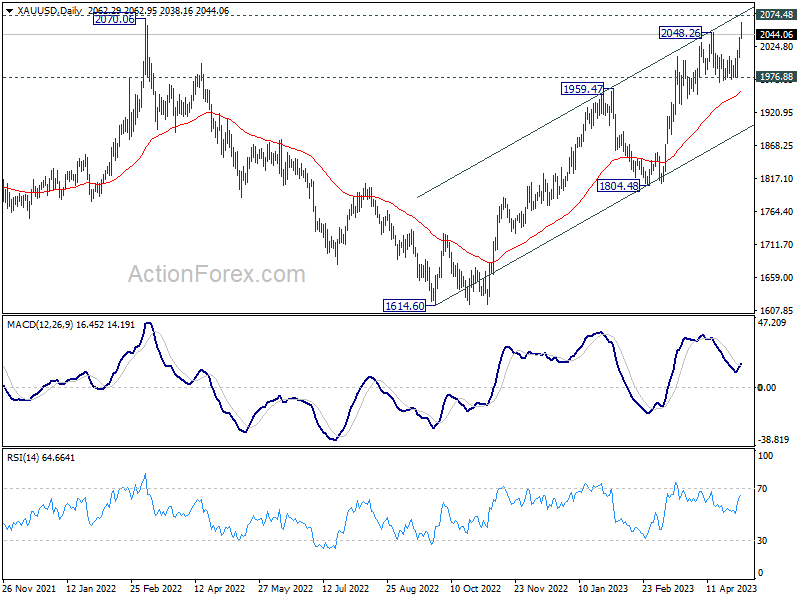

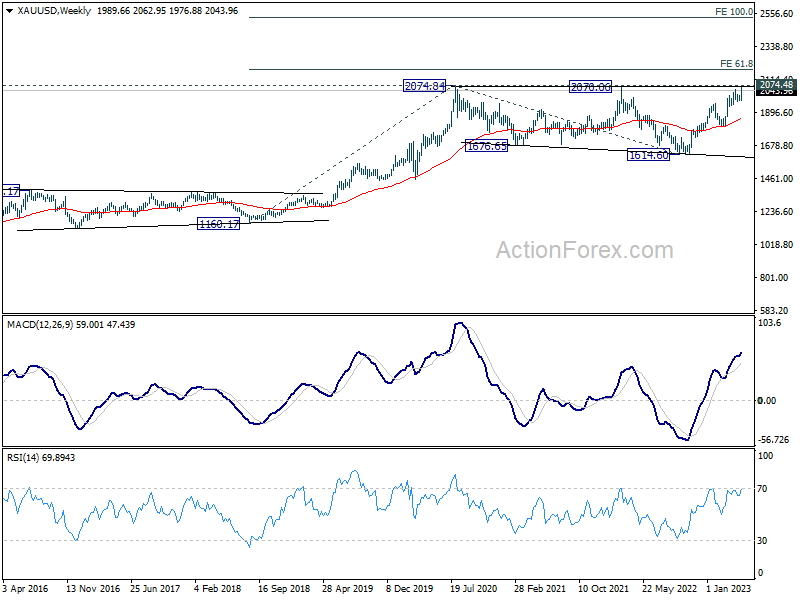

Technically, Gold rode on Dollar weakness and risk-aversion, breaking through 2048.26 short term top overnight. Immediate focus is now on 2074.48 record high. Decisive break there will confirm long term up trend resumption. Next medium term target will be 61.8% projection of 1160.17 to 2074.84 from 1614.60 at 2179.86. In any case, near term outlook will stay bullish as long as 1976.88 support holds.

In Asia, at the time of writing, Japan is still on holiday. Hong Kong HSI is up 0.98%. China Shanghai SSE is up 0.65%. Singapore Strait Times is down -0.09%. Overnight, DOW dropped -0.80%. S&P 500 dropped -0.70%. NASDAQ dropped -0.46%. 10-year yield dropped -0.036 to 3.403.

Fed Powell leaves door open for June pause but rules out rate cut

US stocks, treasury yields, and Dollar closed lower following FOMC rate decision and post-meeting press conference. Although Fed opened the door for a possible pause in June, no confirmation was provided, and a rate cut by year-end was ruled out.

Despite softening its hawkish tone, Fed Chair Jerome Powell did not explicitly confirm a pause following yesterday's 25bps rate hike. Powell noted that "we're closer, or maybe even there" regarding the terminal rate of the current tightening cycle. From June onward, policy decisions will be made on a "meeting-by-meeting" basis, with Fed "prepared to do more" if necessary.

Powell also dismissed the possibility of a rate cut this year. He said, "We on the committee have a view that inflation is going to come down not so quickly, it will take some time," and "in that world, if that forecast is broadly right, it would not be appropriate to cut rates" this year.

Regarding the economy, Powell expressed optimism, stating, "the case of avoiding a recession is in my view more likely than that of having a recession."

Additional readings on FOMC:

- FOMC Signal a Conditional Pause

- Fed Review – A Balanced End to the Hiking Cycle

- FOMC Raises Rates by 25 bps But Signals "Hawkish Pause"

DOW is holding above 32233.85 near term support after the pull back this week. It's probably also trying to draw support from 55 D EMA (now at 33359.36). Another rally is still in favor through 34712.28 resistance to 61.8% projection of 68220.94 to 34712.28 from 31429.82 at 35169.54. However, firm break of 332.33.85 will argue that the pattern from 34712.28 has started another falling leg back towards 31429.82 support. Now that there is no breakthrough after FOMC, the markets will look into tomorrow's non-farm payroll for inspirations.

IMF Srinivasan highlights uncertainty in Japan's monetary policy and potential impacts

Krishna Srinivasan, director of IMF's Asia and Pacific Department, has expressed concerns over uncertainty in Japan's monetary policy direction amid rising inflation.

He stated in a press briefing, "Japanese government bond yields have increased notably since October. Changes in Japan's monetary policy that lead to further increases in government bond yields could have global spillovers through Japanese investors, who have large investment positions in debt instruments abroad."

Srinivasan also warned that portfolio rebalancing by these investors could potentially trigger a rise in global yields, "causing portfolio outflows for some countries".

Regarding China, he noted that over the medium term, a slowdown in productivity and investment is expected, which would lower growth below 4 percent by 2028. This could have profound adverse implications for the rest of the region, given their strong trade linkages with China.

Srinivasan also highlighted the risk of the global economy fragmenting into trading blocs, saying, "If this happens, the larger exposures will be to Asian economies that currently export significantly to the US and Europe, and those that are currently part of global value chains that see them export intermediate goods to China for use in Chinese exports."

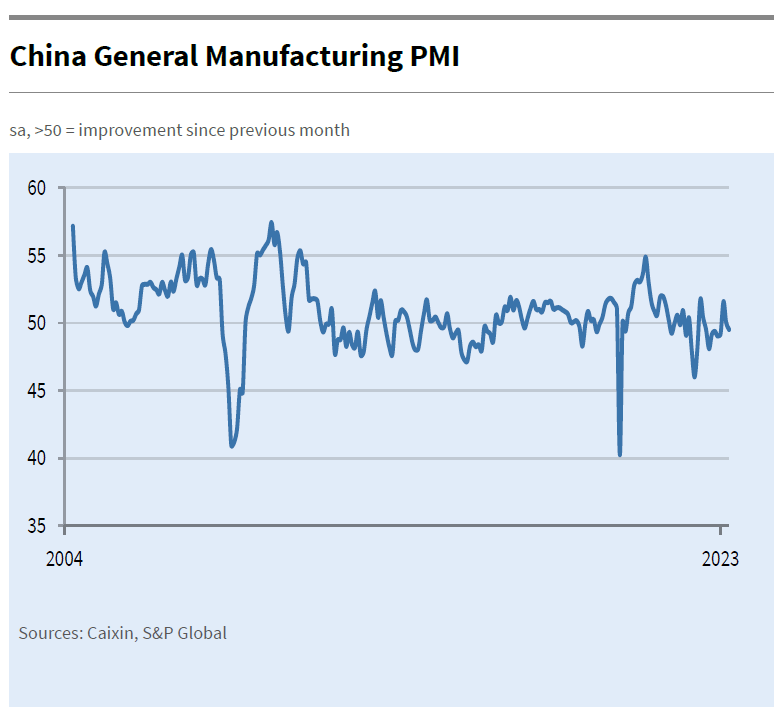

China Caixin PMI manufacturing contracts in Apr, demand softens and prices plunge

China's Caixin PMI Manufacturing dropped to 49.5 in April, down from 50.0 and below the expected 50.8, marking the first contraction reading in three months. According to Caixin, output expanded only marginally due to softening demand conditions. Input costs and selling prices fell at the quickest pace in over seven years.

Wang Zhe, Senior Economist at Caixin Insight Group said: "In a nutshell, manufacturing activity weakened in April. Manufacturing supply saw a marginal slowdown of expansion, demand dipped month-on-month, the labor market worsened further, logistics was relatively smooth, inventories remained stable, and prices plunged. Despite all these factors, businesses maintained high confidence in the economic outlook."

ECB to hike today, 25bps or 50bps?

As ECB gears up for its seventh consecutive interest rate hike in a row today, market participants are divided on the size of the increase. While the majority expect a 25bps hike, which would bring the main refinancing rate to 3.75% and the deposit rate to 3.25%, a 50bps move cannot be totally ruled out.

The size of the hike carries significant implications for the market. A 50bps increase would suggest that the tightening cycle could extend beyond June, even if it slows down then. However, a 25bps hike would create more ambiguity for July meeting. Ultimately, the path forward will still heavily depend on the next round of economic projections, only available at June meeting.

Suggested readings on ECB:

- ECB Set to Raise Rates, But By How Much?

- How Will ECB Meeting Affect EUR?

- ECB Preview: The Art of Compromise

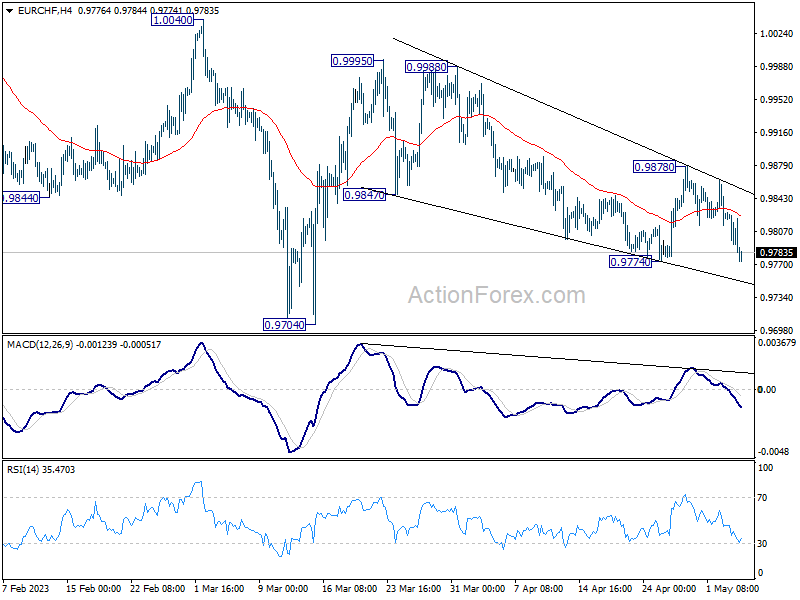

EUR/CHF's recovery from 0.9774 has been underwhelming, stalling at 0.9878 before reversing course. It seems that price actions from 0.9995 are forming a triangle consolidation pattern. While a break below 0.9774 cannot be ruled out, any downside should be limited. Conversely, breaking 0.9878 resistance would indicate that the rise from 0.9704 is set to resume through 0.9995. Let's see how it plays out.

Looking ahead

Other than ECB rate decision, Germany trade balance, Eurozone PMI services final and PPI, UK PMI services final and M4 money supply will be featured in European session. Later in the day, US will release jobless claims and trade balance. Canada will release trade balance and Ivey PMI.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1010; (P) 1.1051; (R1) 1.1103; More...

EUR/USD is still held below 1.1094 resistance despite current recovery. Intraday bias remains neutral first but further rise is expected. On the upside, firm break of 1.1094 will resume larger up trend to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441 However, considering bearish divergence condition in 4H MACD, break of 1.0908 support will indicate short term topping and turn bias back to the downside.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Mar | 7.00% | -9.00% | -9.40% | |

| 01:30 | AUD | Trade Balance (AUD) Mar | 15.27B | 13.00B | 13.87B | |

| 01:45 | CNY | Caixin Manufacturing PMI Apr | 49.5 | 50.8 | 50 | |

| 06:00 | EUR | Germany Trade Balance (EUR) Mar | 17.1B | 16.0B | ||

| 07:45 | EUR | Italy Services PMI Apr | 56 | 55.7 | ||

| 07:50 | EUR | France Services PMI Apr F | 56.3 | 56.3 | ||

| 07:55 | EUR | Germany Services PMI Apr F | 55.7 | 55.7 | ||

| 08:00 | EUR | Eurozone Services PMI Apr F | 56.6 | 56.6 | ||

| 08:30 | GBP | Mortgage Approvals Mar | 46K | 44K | ||

| 08:30 | GBP | Services PMI Apr F | 54.9 | 54.9 | ||

| 08:30 | GBP | M4 Money Supply M/M Mar | 0.10% | -0.40% | ||

| 09:00 | EUR | Eurozone PPI M/M Mar | -1.40% | -0.50% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Mar | 13.20% | |||

| 12:15 | EUR | ECB Main Refinancing Rate | 4.00% | 3.50% | ||

| 12:30 | CAD | Trade Balance (CAD) Mar | 1.0B | 0.4B | ||

| 12:30 | USD | Initial Jobless Claims (Apr 28) | 235K | 230K | ||

| 12:30 | USD | Trade Balance (USD) Mar | -68.9B | -70.5B | ||

| 12:30 | USD | Nonfarm Productivity Q1 P | -0.70% | 1.70% | ||

| 12:30 | USD | Unit Labor Costs Q1 P | 8.40% | 3.20% | ||

| 12:45 | EUR | ECB Press Conference | ||||

| 14:00 | CAD | Ivey PMI Apr | 59 | 58.2 | ||

| 14:30 | USD | Natural Gas Storage | 51B | 79B |

ECB to hike today, 25bps or 50bps?

As ECB gears up for its seventh consecutive interest rate hike in a row today, market participants are divided on the size of the increase. While the majority expect a 25bps hike, which would bring the main refinancing rate to 3.75% and the deposit rate to 3.25%, a 50bps move cannot be totally ruled out.

The size of the hike carries significant implications for the market. A 50bps increase would suggest that the tightening cycle could extend beyond June, even if it slows down then. However, a 25bps hike would create more ambiguity for July meeting. Ultimately, the path forward will still heavily depend on the next round of economic projections, only available at June meeting.

Suggested readings on ECB:

- ECB Set to Raise Rates, But By How Much?

- How Will ECB Meeting Affect EUR?

- ECB Preview: The Art of Compromise

EUR/CHF's recovery from 0.9774 has been underwhelming, stalling at 0.9878 before reversing course. It seems that price actions from 0.9995 are forming a triangle consolidation pattern. While a break below 0.9774 cannot be ruled out, any downside should be limited. Conversely, breaking 0.9878 resistance would indicate that the rise from 0.9704 is set to resume through 0.9995. Let's see how it plays out.

IMF Srinivasan highlights uncertainty in Japan’s monetary policy and potential impacts

Krishna Srinivasan, director of IMF's Asia and Pacific Department, has expressed concerns over uncertainty in Japan's monetary policy direction amid rising inflation.

He stated in a press briefing, "Japanese government bond yields have increased notably since October. Changes in Japan's monetary policy that lead to further increases in government bond yields could have global spillovers through Japanese investors, who have large investment positions in debt instruments abroad."

Srinivasan also warned that portfolio rebalancing by these investors could potentially trigger a rise in global yields, "causing portfolio outflows for some countries".

Regarding China, he noted that over the medium term, a slowdown in productivity and investment is expected, which would lower growth below 4 percent by 2028. This could have profound adverse implications for the rest of the region, given their strong trade linkages with China.

Srinivasan also highlighted the risk of the global economy fragmenting into trading blocs, saying, "If this happens, the larger exposures will be to Asian economies that currently export significantly to the US and Europe, and those that are currently part of global value chains that see them export intermediate goods to China for use in Chinese exports."

China Caixin PMI manufacturing contracts in Apr, demand softens and prices plunge

China's Caixin PMI Manufacturing dropped to 49.5 in April, down from 50.0 and below the expected 50.8, marking the first contraction reading in three months. According to Caixin, output expanded only marginally due to softening demand conditions. Input costs and selling prices fell at the quickest pace in over seven years.

Wang Zhe, Senior Economist at Caixin Insight Group said: "In a nutshell, manufacturing activity weakened in April. Manufacturing supply saw a marginal slowdown of expansion, demand dipped month-on-month, the labor market worsened further, logistics was relatively smooth, inventories remained stable, and prices plunged. Despite all these factors, businesses maintained high confidence in the economic outlook."

Fed Powell leaves door open for June pause but rules out rate cut

US stocks, treasury yields, and Dollar closed lower following FOMC rate decision and post-meeting press conference. Although Fed opened the door for a possible pause in June, no confirmation was provided, and a rate cut by year-end was ruled out.

Despite softening its hawkish tone, Fed Chair Jerome Powell did not explicitly confirm a pause following yesterday's 25bps rate hike. Powell noted that "we're closer, or maybe even there" regarding the terminal rate of the current tightening cycle. From June onward, policy decisions will be made on a "meeting-by-meeting" basis, with Fed "prepared to do more" if necessary.

Powell also dismissed the possibility of a rate cut this year. He said, "We on the committee have a view that inflation is going to come down not so quickly, it will take some time," and "in that world, if that forecast is broadly right, it would not be appropriate to cut rates" this year.

Regarding the economy, Powell expressed optimism, stating, "the case of avoiding a recession is in my view more likely than that of having a recession."

Additional readings on FOMC:

- FOMC Signal a Conditional Pause

- Fed Review – A Balanced End to the Hiking Cycle

- FOMC Raises Rates by 25 bps But Signals "Hawkish Pause"

DOW is holding above 32233.85 near term support after the pull back this week. It's probably also trying to draw support from 55 D EMA (now at 33359.36). Another rally is still in favor through 34712.28 resistance to 61.8% projection of 68220.94 to 34712.28 from 31429.82 at 35169.54. However, firm break of 332.33.85 will argue that the pattern from 34712.28 has started another falling leg back towards 31429.82 support. Now that there is no breakthrough after FOMC, the markets will look into tomorrow's non-farm payroll for inspirations.

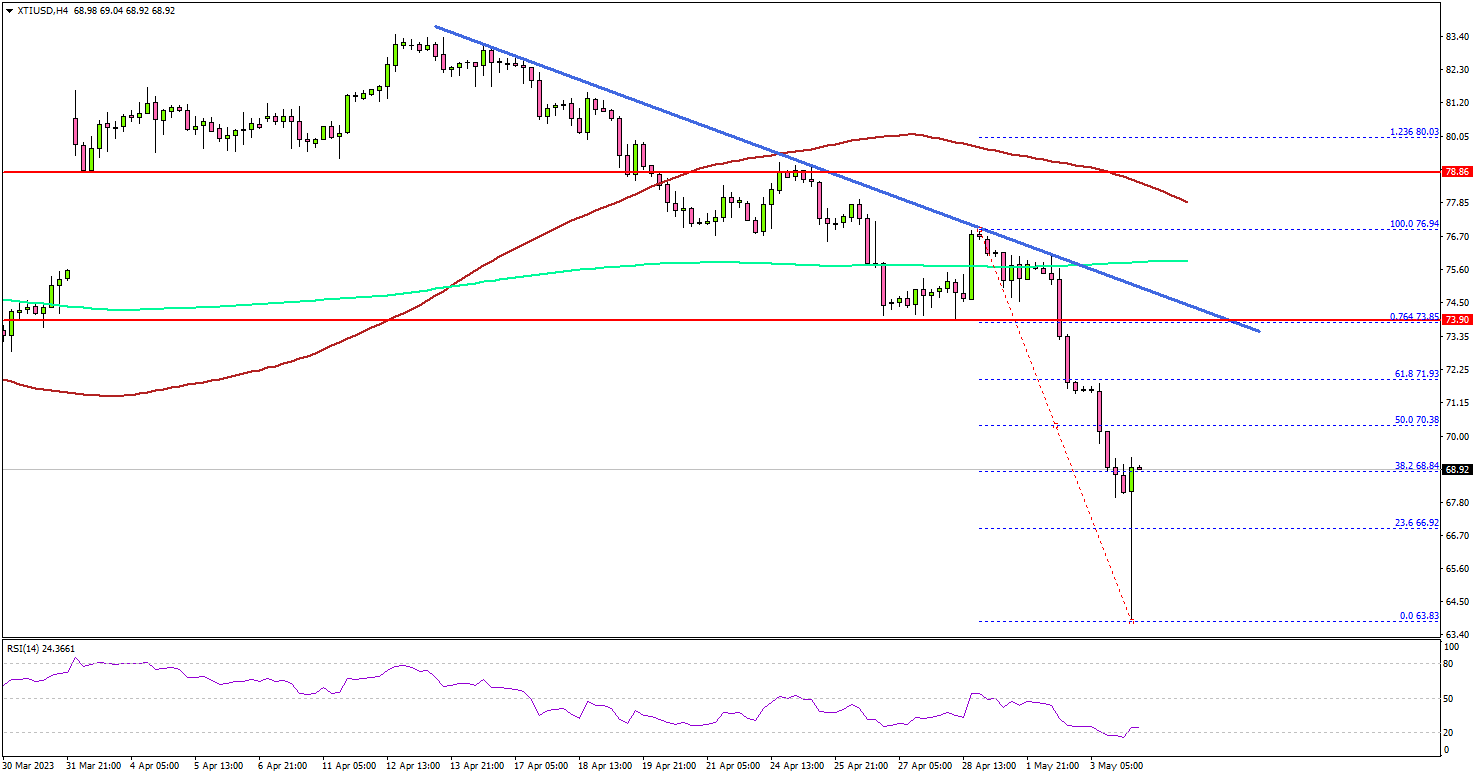

Crude Oil Price Nosedives, Fed Hiked Rates Again

Key Highlights

- Crude oil prices started a fresh decline below the $75 support.

- A major bearish trend line is forming with resistance near $74.00 on the 4-hour chart.

- EUR/USD and GBP/USD remained in a positive zone.

- The Fed increased interest rates from 5% to 5.25%.

Crude Oil Price Technical Analysis

Crude oil prices struggled to start a fresh increase above $78 against the US Dollar. The price remained in a bearish zone and gained momentum below the $75 support.

Looking at the 4-hour chart of XTI/USD, the price settled below the $72.50 support zone, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

The decline was such that the price even dropped below the $70 support. The current price action suggests chances of more losses below the $68 support. The next major support sits near the $66.20 level.

Any more losses might call for a test of the $65.00 support zone in the coming sessions. On the upside, the price is facing resistance near the $70.50 level.

The next major resistance is near the $72.00 zone. Besides, there is a major bearish trend line forming with resistance near $74.00 on the same chart. A clear move above the trend line resistance might send the price toward the $77 resistance.

Looking at EUR/USD, the pair remained in a positive zone above the 1.0975 support and might aim for more upsides toward 1.1120.

Economic Releases to Watch Today

- US Goods and Services Trade Balance for March 2023 - Forecast $-63.3B, versus $-70.5B previous.

- US Initial Jobless Claims - Forecast 240K, versus 230K previous.