Sample Category Title

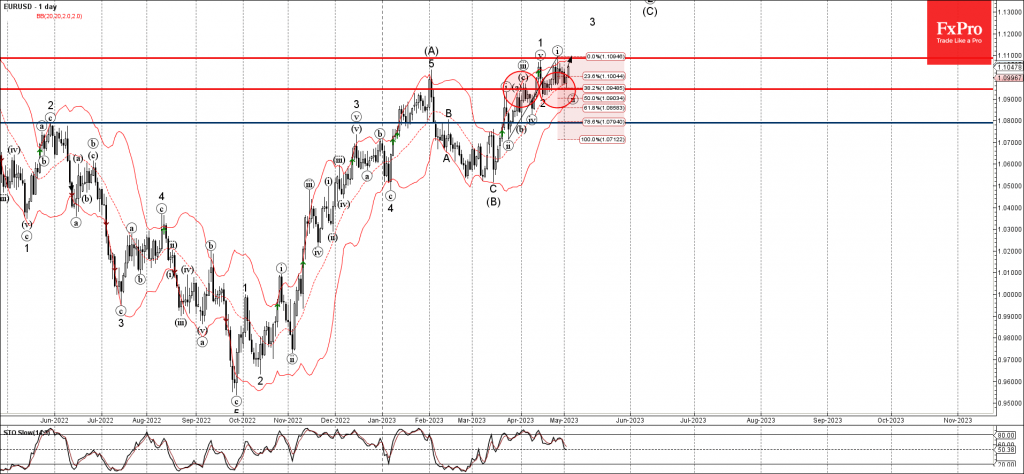

EURUSD Wave Analysis

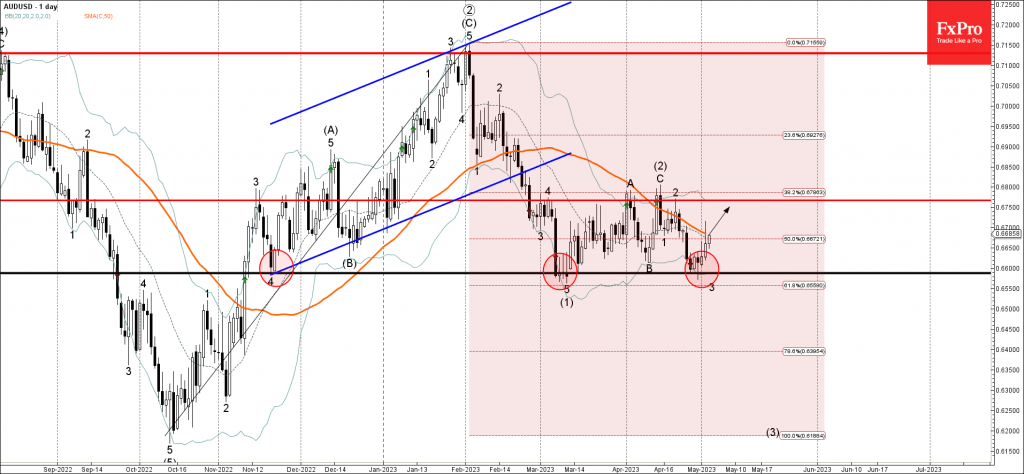

- EURUSD reversed from key support level 0.6600

- Likely to rise to resistance level 0.6750

EURUSD currency pair recently reversed up from the support level 1.0945 (former key resistance from March and April).

The upward reversal from the support level 1.0945 is currently forming the daily Japanese candlesticks reversal pattern Morning Star.

Given the prevailing uptrend, EURUSD can be expected to rise further toward the next resistance level 1.1100 (which stopped the previous impulse waves 1 and (i)).

AUDUSD Wave Analysis

- AUDUSD reversed from key support level 0.6600

- Likely to rise to resistance level 0.6750

AUDUSD currency pair recently reversed up strongly from the key support level 0.6600 (which has been reversing the pair from November), standing close to the lower daily Bollinger Band and the 61.8% Fibonacci correction of the sharp upward impulse from October.

The upward reversal from the support level 0.6600 stopped the previous short-term impulse wave 3 of the impulse wave (3) from April.

AUDUSD can be expected to rise further toward the next resistance level 0.6750 (which stopped the previous waves 4, A, (2) and 2).

FOMC Signal a Conditional Pause

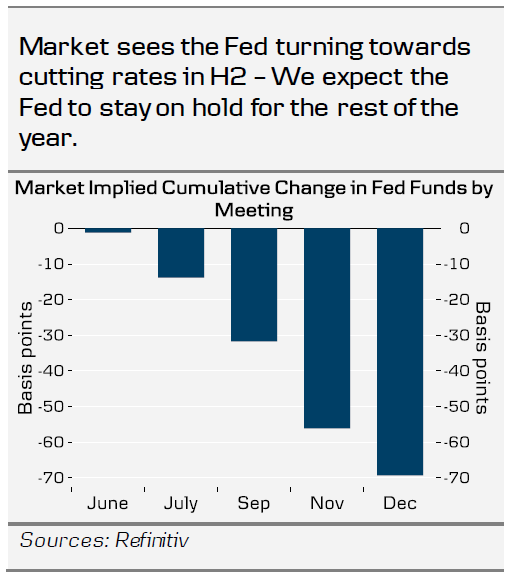

As long as current trends persist, May’s hike is likely to prove the last in this cycle. We expect the first cut in December.

The outcome of the May FOMC meeting was broadly as anticipated, with the fed funds rate increased by 25bps to a mid-point of 5.125% and a conditional pause signalled.

Most notable was the change in the statement language regarding the outlook for monetary policy, with March’s “The Committee anticipates that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive” replaced by “In determining the extent to which additional policy firming may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments”. The effect of quantitative tightening was also recognised, so too the uncertain scale of the contractionary effect of developments in the banking sector and associated regulatory reform.

These factors were also repeatedly highlighted by Chair Powell in the press conference, as was the fact that the fed funds rate is now at the level the March Committee consensus regarded as the peak for this cycle. While subjective and based off a central forecast of continued growth, from Chair Powell’s remarks, arguably the Committee believe the risk spectrum for the outlook is tilting to the downside.

As above, this is not to say the FOMC believe the economy is headed for recession, or that rate cuts will soon be required. Rather, they are sanguine on the outlook for both inflation and growth. Underlying their expectation is resilient employment demand, a tight labour market, and continued above-average gains for wages; combined, these factors look to be viewed as an offset to the drag on households from above-target inflation and contractionary financial conditions. At the same time, the FOMC is recognising that slack is beginning to build in the labour market and broader economy, with: wage growth coming down with inflation; activity data consistent with GDP growth well below trend; and businesses increasingly taking a defensive posture with respect to investment.

Regarding the baseline view for policy, the key question is how quickly US CPI inflation returns to target. From the March FOMC forecasts, it is clear that Committee members remain hesitant to declare victory on this front, with the low end of the central tendency range for 2023 3.0%yr (median 3.3%yr) and, in their view, inflation not back at target until end-2025. These expected outcomes argue for a long period of on-hold policy to fend off inflation risks. That said, the Committee’s view is predicated on continued growth in the economy in 2023 and a relatively quick return to trend growth through 2024 and 2025. Increasingly, the partial data for activity and the assumed consequences of developments in the banking sector stand against this view.

While our own forecasts for growth are broadly in line with the low-point of the Committee’s central tendency range from March, we view the risks as skewed to the downside, with the real prospect of recession. Our own take on the composition of inflation is also more constructive, with annual headline inflation seen at 2.5%yr end-2023 following a circa 2.0% annualised gain through the second half of 2023. Below-trend growth through 2024 (at least) suggests inflation pressures will remain modest over the remainder of the forecast period. It is our view therefore that the FOMC will be able to begin to cut rates in December 2023, and that the pace of easing will remain rapid through 2024, 50bps per quarter leaving the fed funds rate at 2.875% by year end. A low for the fed funds rate of 2.125% is seen by mid-2025.

Note the FOMC’s March forecasts point to a 3.1% fed funds rate at end-2025 and 2.5% in the medium-term, so our expectation is for a materially different policy outcome than the Committee’s. However, it is also worth emphasising that the market has already moved a long way towards our expectation, the US 10yr yield having fallen from a peak of 4.24% to 3.34% currently, we believe on its way to 2.50% in 2025.

In terms of the risks to the policy view, we must emphasise in conclusion that, while recent data has been constructive for our forecast of policy easing from the turn of the year, incoming data must prove the case. Services inflation has to undergo a significant deceleration, requiring shelter inflation to dissipate quickly. Employment growth and wage gains also must slow further. Although downside risks are more probable, as long as the labour market remains strong, their scale is likely to be limited. So the chance of an earlier or more aggressive rate cutting cycle than we have forecast seems slim at this stage.

Fed Review – A Balanced End to the Hiking Cycle

- The Fed delivered a 25bp hike as widely expected by both consensus and markets. We think this marks the end of the Fed's hiking cycle.

- Powell struck a very balanced tone in the press conference, not closing the door for another hike, but also emphasizing that policy is now clearly restrictive.

- EUR/USD was largely unchanged. We make no changes to our Fed call, see no rate cuts this year and expect EUR/USD to fall to 1.06 in 6M.

The Fed delivered a balanced message to the markets by hiking rates by 25bp hike, but also removing the section of the press statement saying that 'The Committee anticipates that some additional policy firming may be appropriate'. Powell did not close the door for further hikes, but we think this marks the end of the Fed's hiking cycle.

Powell did not provide any estimates on how much the banking sector turmoil has affected the policy rate considerations, but he referred to the upcoming May release of the Senior Loan Officer Opinion Survey, noting that the slowing pace of lending has been 'broadly consistent' with the Fed's expectations.

The combination of positive real yields, continuing QT and some credit tightening means that overall financial conditions are now restrictive . Furthermore, simply maintaining nominal policy rates at the current level continues to passively tighten monetary policy due to the yield curve inversion. And as oil prices have moved lower, a further decline in inflation expectations could help push real yields even higher.

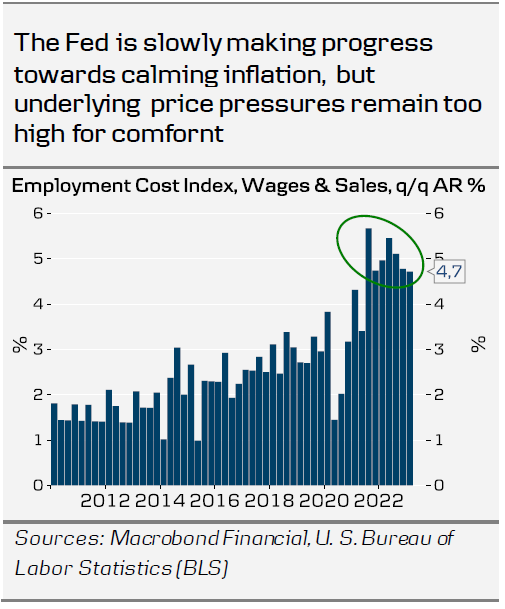

Powell noted that it is also still too early to discuss rate cuts. Core services CPI ex. housing & healthcare rose by 0.61% m/m in March, while wages & salaries in the Employment Cost Index rose by 1.2% q/q in Q1. The Fed still faces the risk of inflation stabilizing at a too elevated level, even if wage pressures from labour markets seem to be gradually easing.

Powell was also asked about the debt ceiling, and while some participants had raised it as a risk to the outlook, Powell simply underscored that the Fed cannot protect the economy from a default, largely as expected.

Most leading indicators have pointed towards accelerating growth momentum in April, and many price indicators have also picked up. Markets do not foresee the Fed making changes in June, but the main risk for another hike lies in the two CPI prints ahead of the meeting. For April CPI next week, we forecast +0.4% m/m for headline and +0.3% m/m for core, although the Cleveland Fed sees some upside risks to our estimate.

For now, we stick to our view that the Fed will maintain rates unchanged for the remainder of the year. Markets remained relatively stable throughout the meeting, with EUR/USD stabilizing around 1.1050. With markets pricing around 72bp worth of cuts for the rest of the year, if we are right in our call, relative rates should add broad support to the USD in H2. Combined with relative terms of trade, growth differentials and relative unit labour cost, we expect EUR/USD to head lower towards 1.06 in 6M. That said, a hawkish 50bp hike from the ECB tomorrow could still drive the cross higher in the near-term.

FOMC Raises Rates by 25 bps But Signals “Hawkish Pause”

Summary

- As widely expected, the FOMC raised its target range for the fed funds rate by 25 bps today. The Committee has now hiked rates by 500 bps since March 2022, the fastest pace of monetary tightening since the early 1980s.

- The FOMC "remains highly attentive to inflation risks," and Chair Powell noted in his post-meeting press conference that "we are prepared to do more if greater monetary policy restraint is warranted."

- But the Committee does not appear to be pre-committing to another rate hike on June 14. In its March 22 statement, the FOMC said that it "anticipates that some additional policy firming may be appropriate." Today's statement dropped the reference to "anticipates." Rather, the statement said "in determining the extent to which additional policy firming may be appropriate..."

- The Committee could indeed hike rates by 25 bps on June 14, but that decision will depend crucially on incoming data over the next six weeks. In our view, the bar to a rate hike on June 14 is higher than it has been at past meetings since March 2022.

- In sum, we would characterize today's meeting as a "hawkish pause."

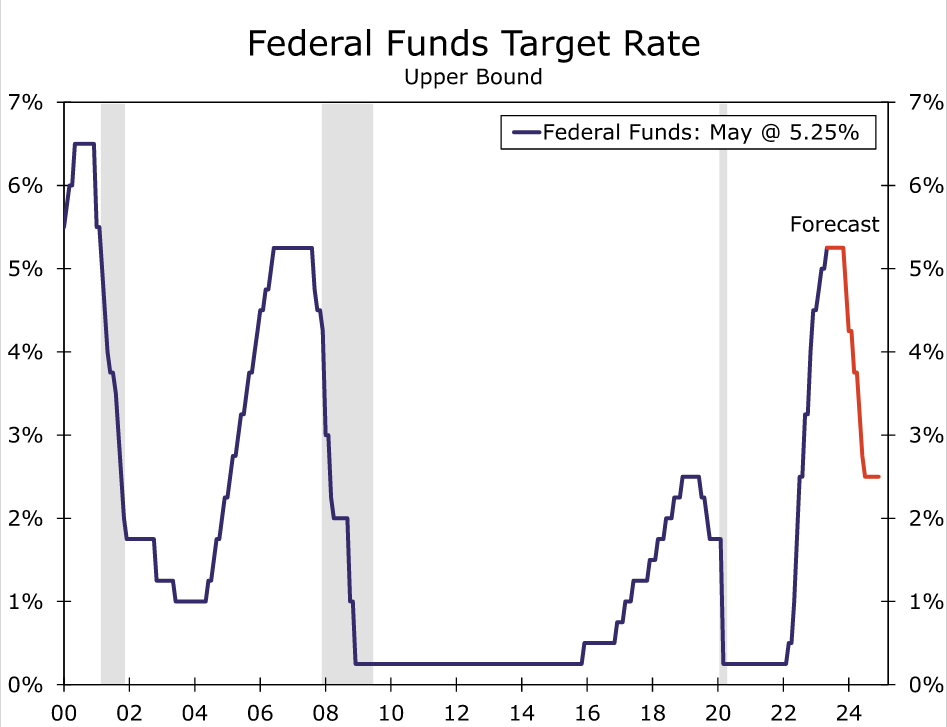

As widely expected, the Federal Open Market Committee (FOMC) decided unanimously today to hike rates by 25 bps, which brings its target range for the federal funds rate to 5.00%-5.25% (Figure 1). The Committee has now hiked rates by 500 bps since March 2022, the fastest pace of monetary tightening since the early 1980s. In explaining its decision to increase the target range again, the FOMC noted that "job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated." This characterization of the current state of the U.S. economy is essentially unchanged from the March 22 statement.

In light of the recent turmoil in the American banking system, the Committee continued to express its confidence that the "banking system is sound and resilient." That said, when it last met on March 22, the FOMC thought that the turmoil was "likely to result in tighter credit conditions." Today's statement implied that credit conditions have indeed tightened, which "are likely to weigh on economic activity, hiring, and inflation." In other words, the FOMC seems resigned to headwinds on growth in coming quarters.

In our view, the most notable part of today's statement was the section outlining the outlook for policy going forward as the FOMC watered down its language regarding the need for additional monetary tightening. In its March 22 statement, the Committee said that it "anticipates (our emphasis) that some additional policy firming may be appropriate..." In the statement the FOMC released today, the Committee dropped "anticipates" and simply said "in determining the extent to which additional policy firming may be appropriate..." In other words, additional tightening may be needed—Chair Powell said in his opening statement of the post-meeting press conference that "we are prepared to do more if greater monetary policy restraint is warranted"—but the FOMC does not appear to be pre-committing to another rate hike on June 14.

That decision on June 14 will depend crucially on "economic and financial developments" over the next six weeks. The Committee will also continue to assess "the cumulative tightening of monetary policy" which it has already undertaken as well as "the lags with which monetary policy affects economic activity and inflation." In our view, the Committee is signaling a hawkish pause in the tightening cycle. That is, the FOMC could clearly hike rates again, especially in light of the sentence in the statement reiterating that Committee members remain "highly attentive to inflation risks." However, the bar to hike again on June 14 appears higher than it has been at past meetings since March 2022.

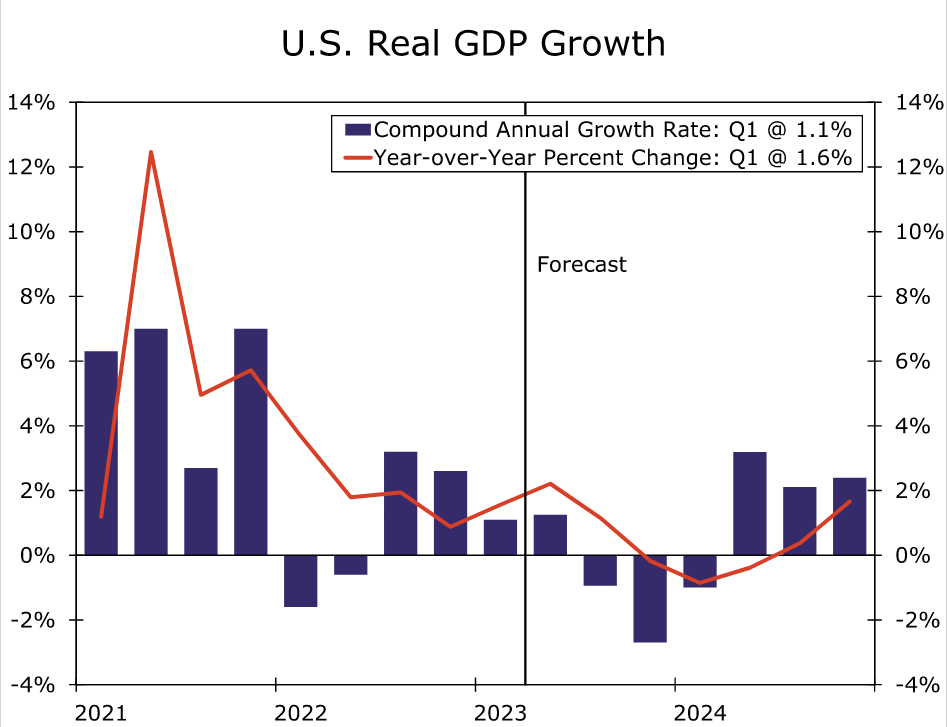

We anticipate that the FOMC will indeed remain on hold on June 14. By the time the July 26 meeting rolls around, we believe that incoming data on economic activity will be soft enough to keep the Committee on hold again. We forecast that real GDP will start to contract, albeit at a gradual rate, starting in the third quarter (Figure 2). This weakness in economic activity should continue to stay the FOMC's hand at its meetings in September and November. But as the downturn in the economy gathers pace and as the Fed becomes more convinced that inflation is heading back toward 2% on a sustained basis, we look for the FOMC to begin an easing cycle at the very end of this year/early next year (Figure 1).

Fed Done Hiking Rates, Dollar Bears in Control, Commodities Mixed

- Pricing of swaps were volatile during the FOMC decision, settling at a 6.3% for a quarter-point hike at the June 14th meeting

- Dollar weaker across the board as the yen surges 1.1%

- Oil crushed as supply and demand indicators remain bearish

The Fed’s tenth straight rate hike will likely be the last one in this cycle. The Fed is concerned that tighter credit conditions will weigh on economic activity and hiring, while helping maintain disinflation trends. Credit tightening is about to cripple the economy and it appears that as long as we don’t get a perfect storm of hotter-than-expected labor and inflation data, the Fed will keep rates on hold for at the very least till the end of the year.

The lag with shelter prices and weakening economic activity should assure inflation will fall below 4% before the end of summer, possibly making a run at the 3% handle. The Fed should be in a position to keep a lengthy hold until early next year.

FOMC Statement:

The Fed raised rates by a quarter-point, bringing the target range to 5.00-5.25%. The Fed removed the text that said “some additional policy firming may be appropriate.” and replaced it with that they will closely monitor incoming information in determining the extent to which additional policy firming may be appropriate to return inflation to 2% time. They are waiting to see the impact of this rating hiking cycle and what happens with the current credit crunch.

The Fed is done hiking rates unless banking jitters completely disappear leading up to the June 14th meeting, Congress is able to make meaningful progress with the debt ceiling, and if soft landing calls become the consensus. Inflation might show signs of stickiness going into the summer, but it should broadly still come down.

FOMC Press Conference

Powell remains hopeful that the US can avoid a recession, noting that his forecast is fore modest growth. Debt ceiling risks did not play a role in today’s decision. Powell noted, “We on the committee have a view that inflation is going to come down, not so quickly, it will take some time. In that world, if that forecast is right, it would not be appropriate to cut rates.”

Powell acknowledged that it is possible that we’ll have what would be a mild recession. Powell seemed like he was trying to be hawkish, but he didn’t get the job done.

FX

The dollar is getting crushed as the end of the Fed’s tightening cycle is likely here. Emerging market FX will have a nice run here as the interest rate differential should widely remain in their favor. The Mexican peso rose to the highest levels since 2017.

The euro is having a nice rally as the focus shifts to the ECB and their tougher battle with inflation.

Oil

Crude prices tried to pare losses after the dollar tumbled following a dovish Fed statement. The end of the Fed’s hiking cycle is here as policymakers become more worried about economic activity. If the Fed is worried, that is bad news for the economy and the crude demand outlook. The focus will shift to OPEC+ and they might be in a position where if they want to stabilize prices, they need to deliver on previously announced production cuts and signal that more are coming.

Gold

The journey to record highs has been a long one for gold, but if the Fed is truly done lifting rates, further tightening of credit conditions could be the key catalyst. Gold is rising as the Fed’s dovish hike may have sealed the fate for the dollar. The Fed could be forced to hike again, but that would require a stronger driving force than the cumulative impact of their 10 rate hikes and fresh economic and financial developments.

Bitcoin

Not all risky assets are rallying post-Fed, Bitcoin is struggling as investors anticipate possibly further support to alleviate banking stress. Bitcoin still remains anchored, unlikely to rally above the $30,000 level until the US gets some regulatory clarity.

Fed Chair Jerome Powell press conference live stream

https://www.youtube.com/watch?v=T-hWy7EMfzo

Fed hikes 25bps, soften hawkish stance but no clear indication of pause

FOMC raises federal funds rate target by 25bps to 5.00-5.25% as widely expected, on unanimous vote. Hawkish stance is softened but there is no explicit indication of a pause in the accompanying statement.

Fed said, "In determining the extent to which additional policy firming may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments."

That compared to March statement that "The Committee anticipates that some additional policy firming may be appropriate"

Also, Fed maintained the pledge that "The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals".

(FED) Federal Reserve Issues FOMC Statement

Economic activity expanded at a modest pace in the first quarter. Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 5 to 5-1/4 percent. The Committee will closely monitor incoming information and assess the implications for monetary policy. In determining the extent to which additional policy firming may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Austan D. Goolsbee; Patrick Harker; Philip N. Jefferson; Neel Kashkari; Lorie K. Logan; and Christopher J. Waller.