Sample Category Title

What Will Happen with the Euro? An Economic Perspective

Against the background of the gradual de-dollarization of the global economic system, the question of replacing the US national currency is increasingly being raised. Some experts have already started talking about the euro as such a replacement. This is unlikely, especially in the economic and geopolitical configuration of the EU, which is now present on the world stage. What is wrong with the EU, and what fate awaits the euro? About all this in our article today.

You die today; I’ll die tomorrow.

In the novel "Gulag Archipelago" by the Russian writer Alexander Solzhenitsyn, the phrase "You die today, and I'll die tomorrow" is often encountered. It quite well describes the relationship between the "world's policeman," the United States, its world reserve currency, the dollar, and the main satellites of the United States - the countries of the European Union.

In the modern dollar-centric model of the economy, the cure for any disease (financial crisis) is to throw additional liquidity into the market.

An example of this "treatment" can be seen in the last three significant crises through which the modern economy has gone and which should be familiar to you.

The subprime crisis of 2008.

Having provoked the formation of a massive bubble in the real estate market through the uncontrolled emission of derivatives, the US increased the money supply quite dramatically (the money supply M2 "jumped" upward in early 2008 and 2009) and simultaneously began a long cycle of key rate cuts, bringing it almost to zero level.

Considering that the US is a net importer, this, in turn, triggered a gradual reduction of the key rate in the EU itself to 1% and a gradual devaluation of the Euro against the dollar (the maximum value of the EURUSD pair was reached in 2008 - 1.6038).

The lack of an alternative to the dollar led to a sharp increase in investments in US treasuries (read: US debt). Whereas before the subprime crisis, the Debt/GDP ratio did not exceed 70%, after 2009, the Debt/GDP ratio jumped to 82% and kept growing.

COVID-19 crises.

The US followed the same path, but it was more aggressive this time, injecting more than $4.5 trillion into the system. After the 4-year cycle of raising the rate, it was sharply lowered again. By this time, the EU economy no longer had room to maneuver in the form of a key rate. Since 2008, the EU has barely stopped its downward cycle, and the euro had devalued 16.3% against the US dollar by then.

2022 crises.

The pandemic ended no sooner than the crisis of 2022, which began with the conflict between Russia and Ukraine. This crisis uncovered rather apparent problems that could not have been focused on before but only accumulated over time. Firstly, it is a problem of cheap energy resources on which low inflation in developed economies was based, which, in turn, allowed to keep rates low and not sterilize the liquidity accumulated in the system for a long time. Secondly, China and partly India have gained strength and are now the leading players in the geopolitical arena, posing a threat to the dominance of the US and, consequently, to the supremacy of the US dollar.

The issue of survival for the US in this situation is a question of joining forces with its major allies in the EU and using their economies to ensure its sustainability. Presumably, the US is aware that "world redistribution" is already taking place and is simply trying to take the most advantageous geopolitical and economic position in the long term.

The EU and the euro can play an extremely secondary role in this situation. By their actions against one of the EU's key energy suppliers, Russia, European politicians confirmed their adherence to American market principles. Against the refusal to purchase energy from Russia, the EU market has become fully controlled by American oil companies, demonstrating a massive increase in profits. In 2022 the revenue of Exxon Mobil grew by more than 40%, the revenue of Chevron - by 57%, and the revenue of Shell - by almost 46%.

That's the point of the phrase, "Die today, and I'll die tomorrow."

What is wrong with the EU?

Why can't the EU and its currency challenge the US? Disregarding European politicians' geopolitical aspects and personal characteristics and focusing solely on the economic component, the answer is quite simple - the heterogeneity of the economies.

For 40 years, the EU has been so focused on expanding its borders and integration that economic issues have been left "out of the picture. At the same time, if we look at the GDP of the 27 countries of the European Union, the image is as follows:

The gap between the first EU economy (Germany) and the second (France) was about 50% in 2021. If we compare Germany, for example, with Greece, the gap is about 20 times. Germany's current debt-to-GDP ratio is 66.3%, while Greece's is 171.4%. The ratio in Spain (not the smallest economy in the EU) is 113.2%. In other words, the phrase that "the German burgher pays for everything" is not unreasonable. This is a factor.

Next, it is the US debt to the EU. Collectively, the EU holds about 1:15 of the US foreign debt. Banker Jean Paul Getty used to say that "If you owe the bank $100, that's your problem. If you owe the bank $100,000,000, it's the bank's problem." This fully applies to the US, where the EU is acting as the bank. The problem with the current crisis is that, on the one hand, the US cannot afford not to raise the key rate because inflation will accelerate. On the other hand, by raising the rate too much, the US is increasing the cost of servicing its debt, thereby increasing the budget deficit. Where to get the money to cover the deficit? Right - by issuing more treasuries and selling them to its allies.

As the economic system defragments, a gradual redistribution of the major holders of US debt will begin. The consequence will be an increase in the US debt to the EU, which should hurt EURUSD.

Technical analysis

Technically EURUSD is in a global downtrend. The trend line is heading down, and all moving averages are also falling.

The movement during the last eight months can be considered a correction. The price broke the 50% Fibo correction level and almost reached 1.2226 (61.8% of Fibo correction).

With a higher probability, the price will keep falling.

Conclusion. EURUSD outlook.

We now see two possible global scenarios, both unfavorable for EUR.

Scenario 1. Even more integration of the US and the EU.

In this scenario, it is possible to increase the borrowings of the EU countries, i.e., to further increase the European economy's dependence on the American one.

Scenario 2. The disintegration of certain EU countries. Partial disintegration of the EU.

This scenario is possible only if there is a major internal political crisis within individual countries of the European bloc and if the United States "releases" such a "rebel" from its influence. This is an unlikely path, but it is still possible in the very distant future.

ECB Set to Raise Rates, But By How Much?

All eyes will be on the European Central Bank rate decision on Thursday at 12:15 GMT. A rate increase is all but certain, yet its size is still up for debate. Market pricing is leaning towards 25bps, but some traders are still betting on a bigger 50bps move. The compromise might be the smaller rate hike accompanied by hawkish language, which could take some steam out of the high-flying euro.

Euro shines bright

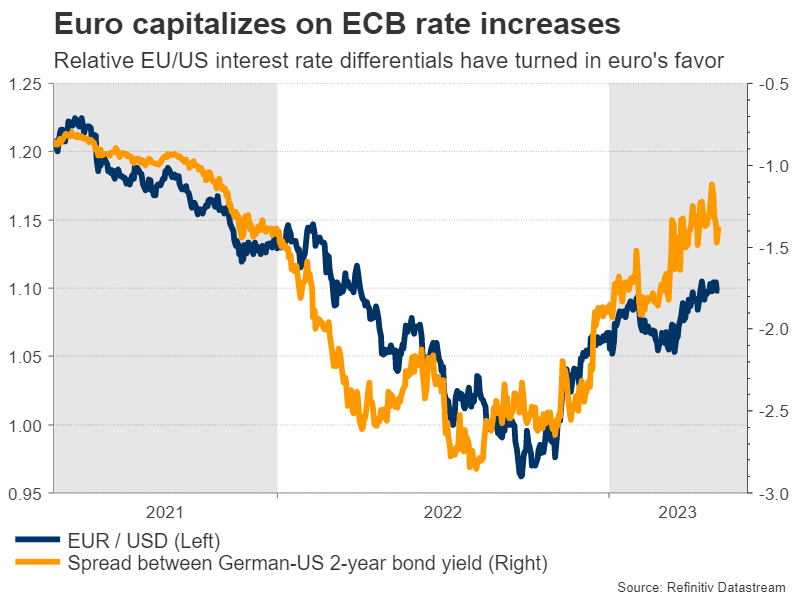

The euro has been among the best-performing major currencies this year, as most of the negative factors that haunted the single currency last year have either eased or vanished. Europe got through the winter without suffering a recession, energy prices have fallen sharply, China has reopened, and most importantly the ECB has come a long way in raising interest rates.

One of the euro's main disadvantages over the last decade was the ECB's negative interest rate policy, which made the Eurozone unattractive as an investment destination. This has changed dramatically, with ECB rates currently standing at 3% and market pricing projecting them to go as high as 3.6% in this cycle.

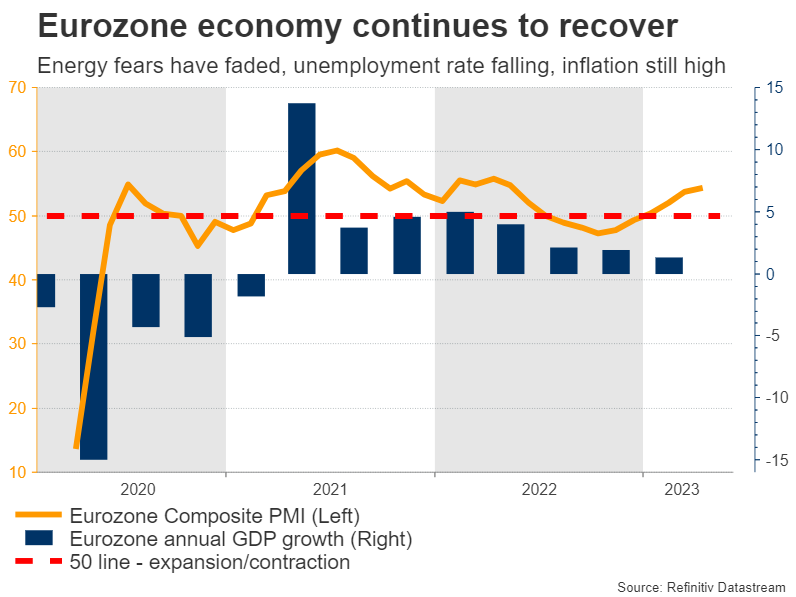

But it's not just interest rates, as the euro area is also enjoying a burst of economic momentum. Business surveys point to an economy that is accelerating, inflation continues to rage with support from consumer demand, and the strength in the labor market has helped fuel wage growth.

ECB conundrum

Turning to the upcoming rate decision, investors are leaning towards a smaller rate increase of 25bps, assigning this scenario an implied probability of around 80%. The alternative is for a bigger move of 50bps, which markets have attached a 20% probability to.

If the decision was only based on the quality of economic data releases, there is a serious case for the ECB to raise by 50bps. Economic growth remains resilient, core inflation has been stickier than expected, while the declining unemployment rate and strengthening wage dynamics are not consistent with inflation falling back to its target anytime soon.

However, there are two issues that might make the ECB cautious. Firstly, the recent turbulence in the banking system argues for slower loan growth, which as the Fed argued recently, has similar effects to raising rates. Secondly, the full impact of previous rate increases hasn't been felt yet, so some ECB members might be wary of overdoing it, and inflicting unnecessary damage on the economy.

As per usual, the decisions of the ECB Governing Council are taken through compromise, given the different views among its members. In this case, a middle-of-the-road solution may be to raise rates by 25bps, but accompany that move with hawkish language hinting at more rate increases in future meetings.

Market reaction

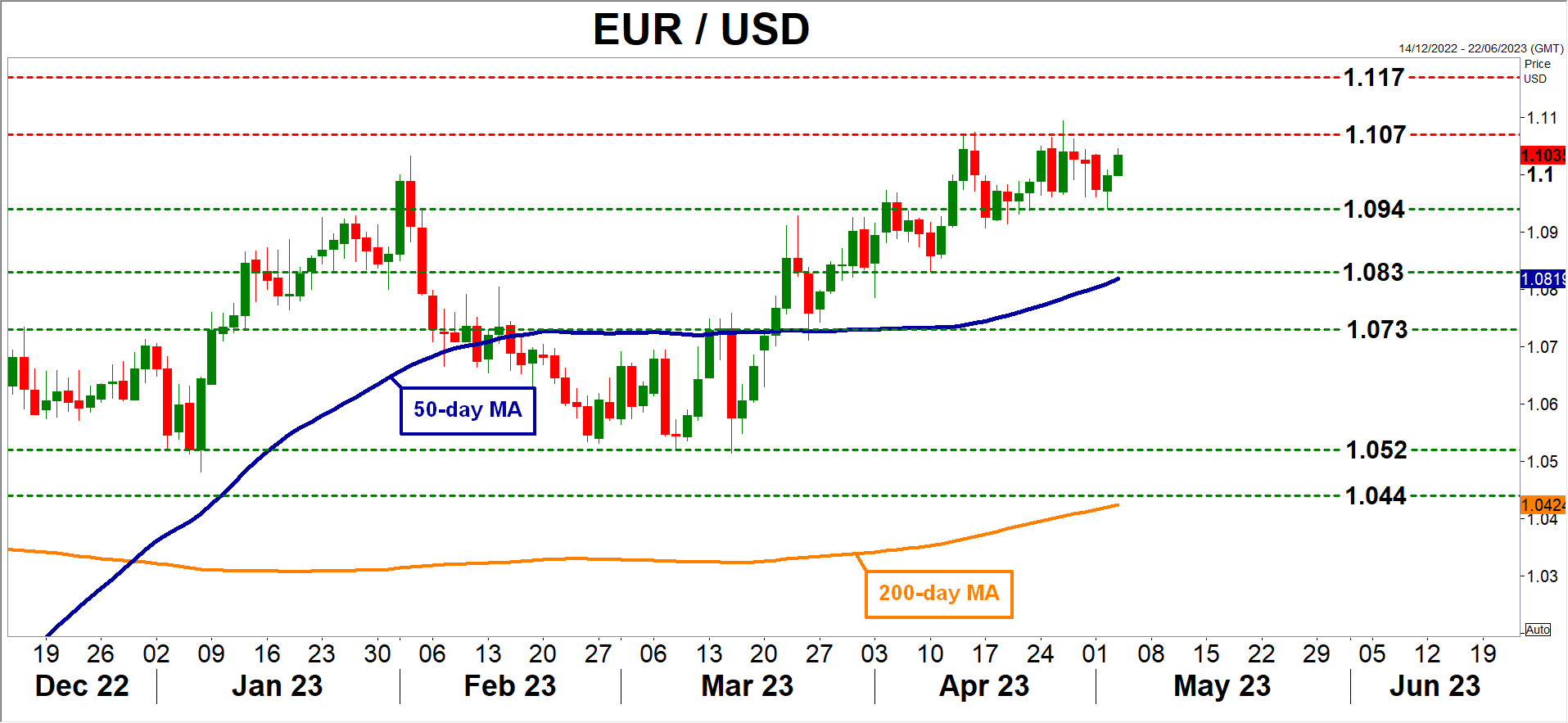

Considering how markets have priced this decision, such an outcome might be slightly bearish for the euro. It would signal the ECB has started to get cold feet, likely giving rise to speculation that the end of the tightening cycle is imminent. In this scenario, euro/dollar could edge lower, with the first obstacle for the bears likely to be the 1.0940 zone.

On the other hand, if the ECB rolls out a 50bps rate increase, that would come as a surprise for investors and the euro will likely enjoy further upside. In euro/dollar, such a move might propel the pair above the 1.1070 region, which capped multiple advances in recent weeks.

All told, the pair has been in an uptrend for more than half a year now, although a clear close above 1.1070 is required to signal trend continuation.

Note that the Federal Reserve will also announce its own rate decision on Wednesday, ahead of Thursday's ECB meeting, and could also impact euro/dollar.

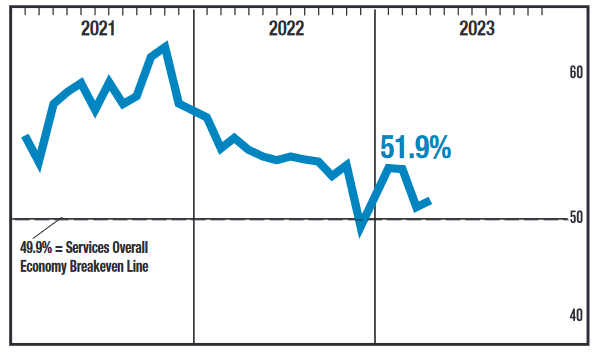

ISM Shows Steady-Eddie Services Sector in April

The ISM Services PMI index rose slightly, in line with expectations in April to 51.9 percent, up from 51.2 in March. That marks the fourth consecutive month of expansion in the services sector.

However, the business activity sub-index cooled to 52, down from 55.4 in March.

The new orders rose to 56.1, recovering almost half of the weakening in March (52.2). However, pulling back the lens, new orders remain below their peak 60+ readings in 2021.

The prices paid component was basically flat, at 59.6 in April, holding on to the substantial improvement seen in March. After a meaningful increase in 2021, the prices paid index is back in line with mid-2020 readings.

The employment sub-component fell slightly to 50.8 in April from 51.3 in March, but hung onto expansionary territory.

Fourteen out of 18 industries expanded in April, up one from March.

Key Implications

According to the ISM Services PMI there was a slight uptick in the growth rate of the services sector in April. It was due mostly to the increase in new orders, and ongoing improvement in both capacity and supply logistics. However, some respondents are "wary of potential headwinds associated with inflation and an economic slowdown." Looking at overall activity, the slowing trend that has been ongoing since 2021 remains intact.

This indicator plays a very quiet second fiddle to the FOMC rate decision out at 2pm today. But, it underscores a challenge for the Fed in wrestling inflation back down to the 2% target – the resilience of the services sector. Slowing is gradually occurring, but the Fed needs to see the services sector, and then services inflation cool further, before they can ease up on their hawkish monetary policy stance.

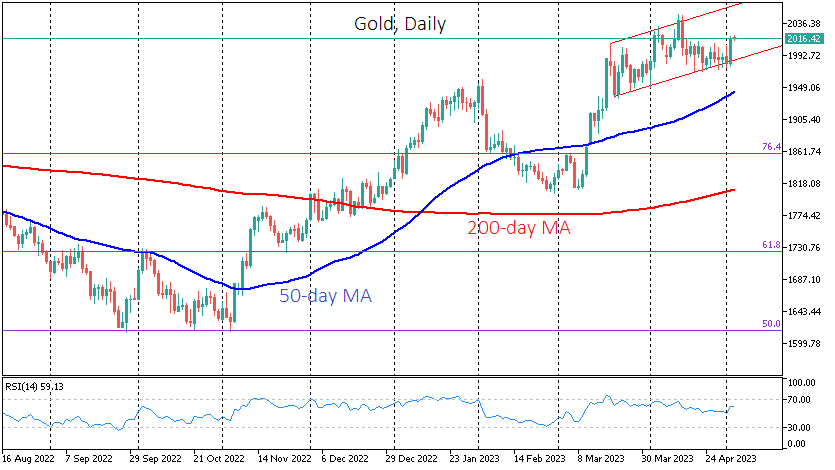

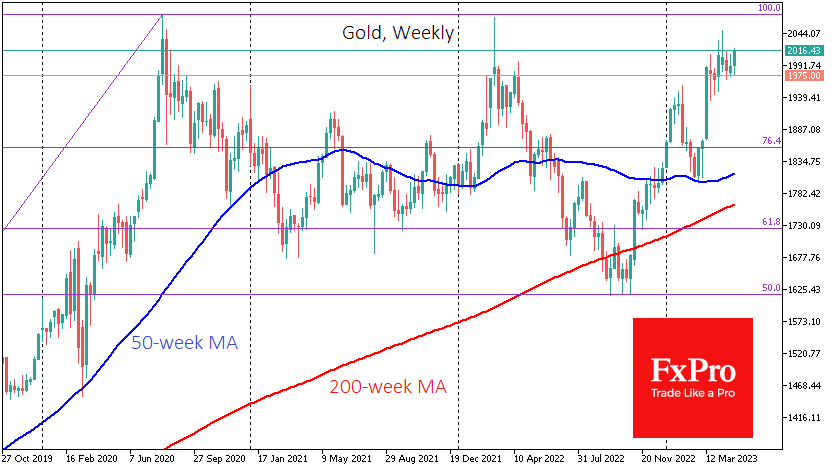

A Promising Gold Trend

The price of gold rose by almost 2% on Tuesday after reports of another round of regional bank problems in the US. Quite quickly, the price stabilised around $2015. This surge allowed gold to bounce back from the lower end of the uptrend range, within which the price has been moving since March 22. However, it is a less significant reaction compared to what we have seen since March 9, as it is uncommon for the financial markets to experience an equally strong surge in response to the same cause twice.

Before that, since the end of April, we have seen very persistent buying of gold on declines into the $1975 area. Yesterday’s move brought the price back to the middle of the upside range, which has existed since March 22. Yesterday’s momentum took the price to almost four-week highs, above several local highs in recent days.

The upper boundary of that range is now near $2065, which brings it very close to a third test of the all-time highs above $2070. But there is an important difference between the way the price has behaved the previous two times and now.

In July 2020 and February 2022, gold entered the most violent phase of its rally from levels just above $1800. This acceleration is often the last phase of the rally when the market is driven by extreme greed and bearish capitulation. In both cases, the price declined for a long time after that, pulling back below $1700.

This year’s rally started from roughly the same levels near $1800, but that was preceded by a prolonged correction after a failed attempt to take $2000 in January. In addition, since the end of March, the gold movement has become more cautious, and in April, it added just over 1%. Thus, the upward momentum in gold is not bearish capitulation but investor and speculator demand.

Notably, the buying boundary on declines – near $1975 – runs near a critical resistance level seen in August 2020 and April 2022, when sellers prevented gold from rallying again after the surge. The market dynamics suggest that the recent retreat to the $2000 level is a prologue to further gains rather than the end of an extended rally, as was previously the case. This suggests we will soon see prices above $2050 (previous high area) and increased chances of going above $2075 with a renewal of historical highs in the coming weeks.

US ISM services rose to 51.9, corresponds to 0.7% annualized GDP growth

US ISM Services PMI rose from 51.2 to 51.9 in April, below expectation of 53.1. Looking at some details, business activity/production dropped from 55.4 to 52.0. New orders rose from 52.2 to 56.1. Employment dropped from 51.3 to 50.8. Prices rose from 59.5 to 59.6.

ISM said: "There has been a slight uptick in the rate of growth for the services sector, due mostly to the increase in new orders and ongoing improvements in both capacity and supply logistics. The majority of respondents are mostly positive about business conditions; however, some respondents are wary of potential headwinds associated with inflation and an economic slowdown."

"The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for April (51.9 percent) corresponds to a 0.7-percent increase in real gross domestic product (GDP) on an annualized basis."

Sunset Market Commentary

Markets

The looming Fed meeting meant subdued trading on financial markets which even a much stronger than expected April ADP jobs report couldn’t change for the better. Job creation rose by 296k, almost double the 150k expected and a sharp increase from last month’s 142k. Leisure and hospitality lead the advance (+154k), followed by education and health services (+69k) and trade, transportation and utilities (+32k). The goods sector printed 50k+ jobs in natural resources and mining and in the construction sector. Manufacturing employment eased 38k. Pay growth continued its nearly year-long slowdown. ADP chief economist Richardson concludes that “employers are hiring aggressively while holding pay gains in check as workers come off the sidelines. Our data also shows fewer people are switching jobs.” US bond yields tried to leave the intraday lows further behind after the release but the move lacked strong legs. Current changes vary between -3.6 bps (5-y) and -2 bps (2-y). German Bunds underperform marginally, with yields flat at the front and losing 1.3 bps at the very long end. European data was confined to a lower than expected March unemployment rate. At 6.5%, the bloc even hit a new all-time low. European equities recouped up to 0.8% (EuroStoxx 50) of the losses incurred during yesterday’s risk-off but half of that evaporated in the meantime. US indices open with minor gains. Japan’s yen takes the lead on FX markets. USD/JPY falls from 136.55 to 135.42. EUR/JPY eases sub 150. The USD in general inches lower. EUR/USD rises towards 1.104 and the trade-weighted index slips to 101.59. Oil prices are under heavy selling pressure for a second day straight, pushing prices well below the level before OPEC+’s unexpected output cut end March. One barrel of Brent now sells for $73. The mid-March lowest close since end 2021 ($72.97) is under attack.

The services ISM (expected at 51.8, up from 51.2) is still due after wrapping up this report. It’s impact on market is bound to be limited with the upcoming Fed meeting. Chair Powell is expected to raise rates by 25 bps to 5-5.25%, in line with the March dot plot, before most likely announcing a pause in the tightening cycle. The statement in all likelihood will keep the door for further tightening open. Optionality and flexibility are key. In the current mindset however, we doubt the market will interpret today’s decision as anything other than a dovish hike that marks the end of and not a pause in this cycle. This may put downward pressure on yields, in particular at the front end of the curve. The (in our view misplaced) idea of rate cuts in the second half of this year may gain further traction. Currently some 60 bps of them are priced in by end 2023. The US 2-y yield camps south of the 4% barrier at the time of writing and it’s unlikely that it is going to recover that level post-Fed. 3.55% (March panic low) marks first support. In the 10y yield we’re looking at 3.24% (April YtD low). The US dollar faces additional losses. EUR/USD may test the current YtD intraday high of 1.1095. This level serves as an intermediate resistance level only, with the first, real reference located at 1.1274.

News & Views

The Hungarian parliament voted in favour of judiciary reforms including government limits to make appeals to the Constitutional Court, an automatic distribution of cases among judges and stronger remits for the council of judges to supervise the courts. The package of reforms are part of the so-called supermilestones imposed by the EU Commission to tackle long-standing concerns over rule of law and democratic standards. Others include lack of compliance when it comes to LGBTQ rights, academic freedom and asylum and concerns about corruption. EC Budget & Administration Commissioner Hahn last week said that approval could unlock about €13bn in cohesion funding (part of a €21.5bn package). The EC now needs to give its political blessing. The Hungarian forint loses some ground today in a likely buy-the-rumour, sell-the-fact move. EUR/HUF recently tested the YTD lows in the low 370-area and rebounds to 376.

French Finance Minister Le Maire today announced an extension of the three-month anti-inflation campaign – trimestre anti-inflation – which started early March and was due to end on June 15. Under the campaign, French retailers agreed to charge the lowest possible amount for some essential food items. Le Maire called on food manufacturers to help with lowering prices as wholesale prices are coming down. He guestimates that the trimestre anti-inflation so far led to a 5%-7% decline in affected items.

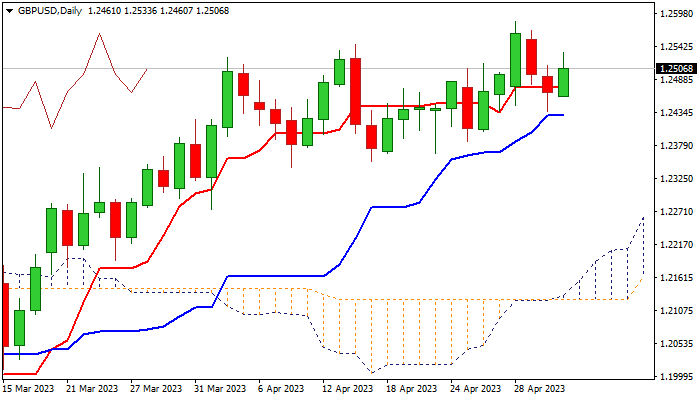

GBP/USD: Cable Stands at Front Foot and Look for Clearer Direction Signals from Fed

Cable regained traction and bounced above 1.2500 mark on Wednesday, lifted by weaker dollar ahead of Fed decision.

Fresh advance generates initial signal that two-day pullback from new 2023 high (1.2583) might be over, as today’s acceleration retraced 61.8% of 1.2583/1.2435 correction.

Series of higher highs and higher lows suggest that larger uptrend from 1.1802 (2023 low of Mar 8) remains intact, although more evidence would be required to confirm that bulls are back to play after correction.

However, near-term outlook is still unclear, as markets await releases of US private sector labor data (ADP) and Services PMI, ahead of key event – Fed rate decision, due later today, which are likely to provide clearer direction signals.

Today’s close above daily Tenkan-sen (1.2475) would keep alive slight bullish bias, with lift and close above 1.2550 (Fibo 76.4% of 1.2583/1.2435) to confirm and open way for retest of 2023 high (1.2583).

On the other hand, loss of daily Tenkan-sen would increase pressure and risk break of pivotal daily Kijun-sen (1.2429) which would open way for deeper correction.

Res: 1.2533; 1.2550; 1.2583; 1.2666.

Sup: 1.2475; 1.2460; 1.2429; 1.2386.

All Eyes on Fed as Investors Fret About US Regional Banks

The Federal Reserve will announce its latest interest rate decision later today and investors will be hanging on their every word in light of recent banking sector instability.

Today was always likely to mark the end of the US central bank's tightening cycle - not that it has explicitly signaled this - but we've now reached a stage in which every rate hike could have unwanted and unintended consequences.

Turbulence in the banking system in March is evidence of that and the rescue of First Republic Bank by JP Morgan in recent days, and the sell-off that followed in other regional banks, suggests significant stress remains.

Which begs the question, why would the Fed opt to tighten at all today when it can see that the financial system is under strain, credit conditions have tightened as a result and the lag with which monetary policy operates means they don't yet fully understand what the full impact of their recent rate hikes has been.

With that in mind, it would be perfectly reasonable to pause today especially when we're already starting to see signs of the labour market softening and inflation easing. And you can see that investors are of the view that a rate hike today is a mistake as they see a high likelihood of it being reversed over the next couple of meetings. Hardly a vote of confidence.

And yet, it still looks extremely likely which makes the Fed's communication alongside it all the more important. It must now pivot away from promising further rate hikes towards a more neutral stance or we could see further turbulence in financial markets, particularly in those regional banks that still look vulnerable.

Bank woes send Oil prices tumbling once more

Oil prices have been crushed again over the last 24 hours as US regional bank shares sold off heavily and fuelled fears of a more significant economic downturn this year. The warning signs are there that investors are extremely anxious about the global economic prospects, particularly the US, and the data is slowly catching up which should deter the Fed from hiking today but it in all likelihood won't.

The US may be heading for recession and they may not be alone which doesn't bode well for crude demand. Oil prices are heading back to the March lows which will no doubt frustrate OPEC+ so soon after cutting output. Will the group be tempted to hold an emergency meeting or wait to see how the situation develops? They've denied being price driven in the past but it's clear that's not entirely true. Another surprise intervention could act as a further deterrent to sell-offs in the future on the belief the cartel will simply jump in again.

New record highs incoming for Gold?

Gold jumped back above $2,000 on Tuesday as investors fretted about the prospect of further disruption in US regional banks, pushing US yields lower and weighing on the dollar. In other words, investors are expecting a swift u-turn from the central bank in light of what we've seen in the US banking sector in recent months and yesterday's moves have further solidified that view.

A dovish Fed today, either in the form of a surprise pause or a hint at rate cuts this year, maybe even a neutral shift, could further support gold and maybe even trigger a run at record highs which are now not that far away. The interesting thing will be how markets would respond if the Fed sticks to its hiking script of recent months because aside from exacerbating the pain on the economy, it would also surely necessitate an even more aggressive shift a little later on.

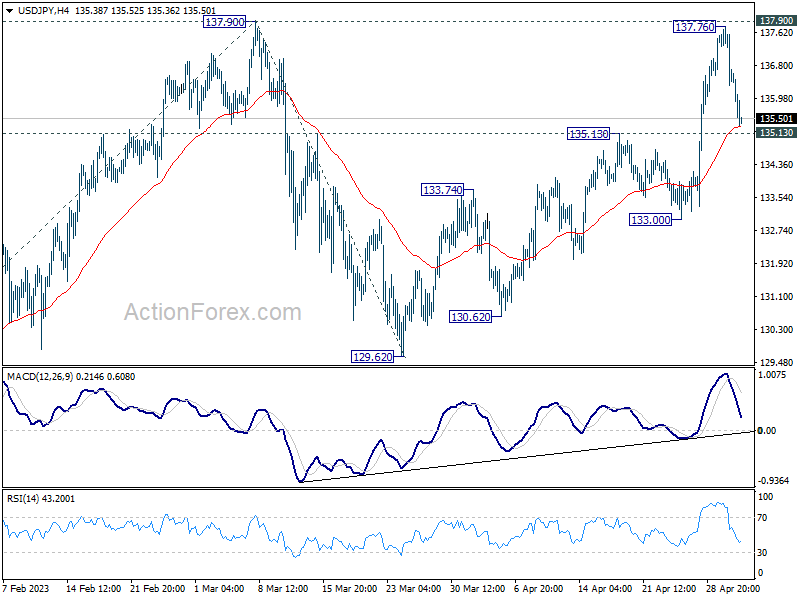

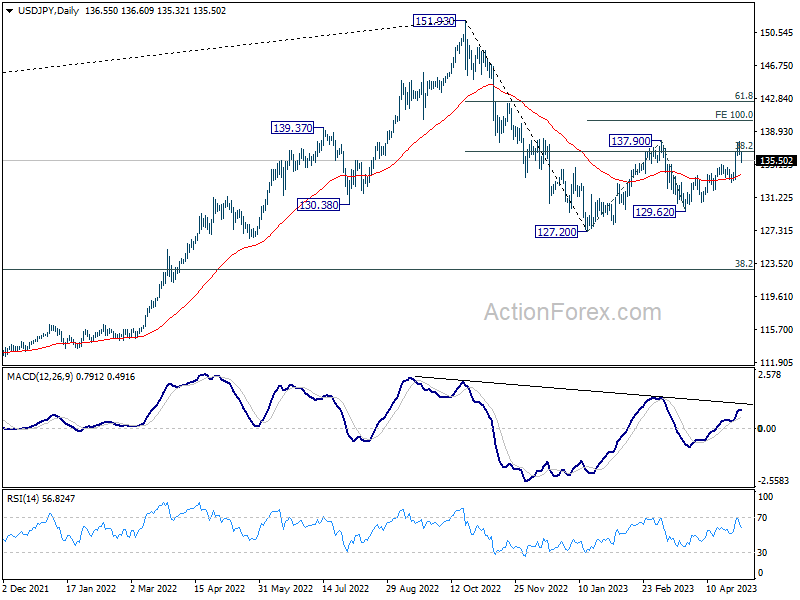

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 135.43; (P) 136.00; (R1) 136.88; More...

USD/JPY's retreat from 137.76 extends lower today but stays above 135.13 resistance turned support. Intraday bias remains neutral first. Further rally will remain in favor as long as 135.13 resistance turned support holds. Decisive break of 137.90 will resume whole rebound from 127.20, and target 100% projection of 127.20 to 137.90 from 129.62 at 140.32. However, firm break of 135.13 will turn bias back to the downside for 133.00 support and below.

In the bigger picture, price actions from 151.93 high are currently seen as a corrective pattern to the long term up trend. The first leg should have completed at 127.20. Rebound from there is seen as the second leg. Sustained break of 31.8% retracement of 151.93 to 127.20 at 136.34 will bring stronger rebound to 61.8% retracement at 142.48. Meanwhile, break of 129.62 will argue that the third leg is starting through 127.20 low.

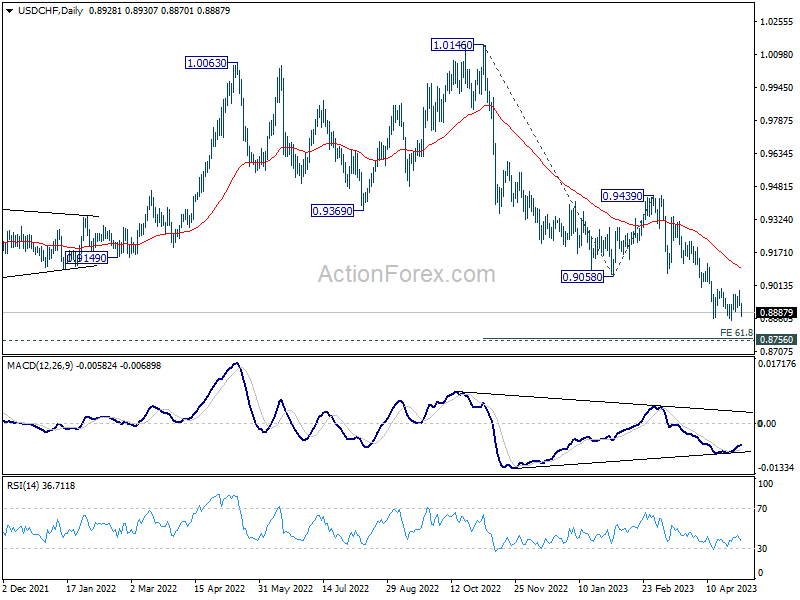

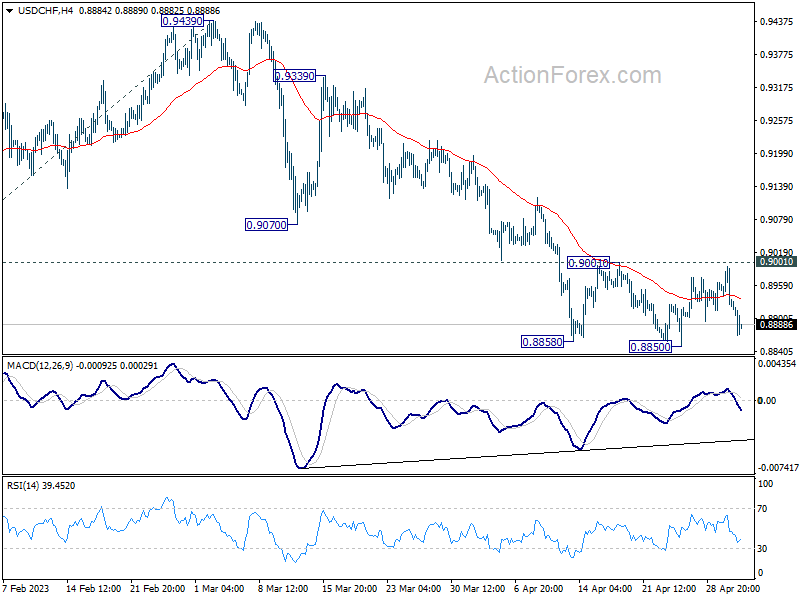

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8880; (P) 0.8906; (R1) 0.8951; More...

Intraday bias in USD/CHF remains neutral for the moment. On the upside, decisive break of 0.9001 resistance should confirm short term bottoming at 0.8850. Intraday bias will be back on the upside 55 D EMA (now at 0.9094). Sustained break there will be a strong sign of bullish reversal. On the downside, break of 0.8850 will resume larger fall from 1.0146, to 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support. Strong support is expected there to bring rebound, at least on first attempt.

In the bigger picture, fall from 1.1046 (2022 high) is in progress for 0.8756 support (2021 low). But overall, this fall is still seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.