Sample Category Title

Australian Dollar Soars as RBA Resumes Rate Hike; Yen Remains Under Pressure

Australian Dollar surges after RBA surprised the markets by resuming rate hike today. In addition, tightening bias is maintained even though the tone is softened. New Zealand and Canadian Dollars trail closely, boosted by a slightly positive risk sentiment. On the other hand, Japanese Yen continues to be the runaway loser in the market. Dollar is reversing some of this week's gains. European majors are mixed, with Sterling on the weaker side than Euro and Swiss Franc.

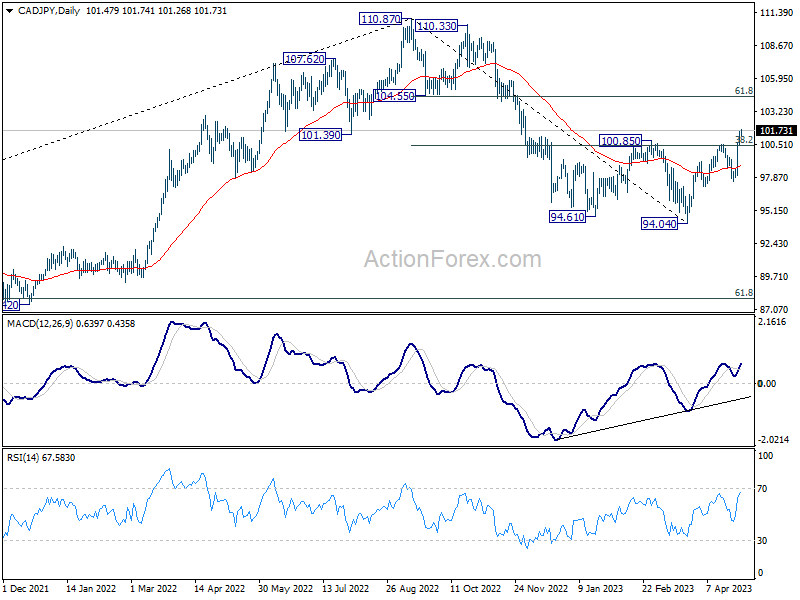

In terms of technical developments, Yen's performance will likely remain a focal point in the markets. CAD/JPY's break of 100.85 resistance suggests that the entire decline from 110.87 has concluded at 94.04, potentially leading to further rallies up to the 61.8% retracement of 110.87 to 94.04 at 110.62. A firm break above this level could prompt a retest of 110.87 high. Depending on the overall Yen selloff elsewhere, there is possibility of breaking through 110.87 as CAD/JPY aligns with the broader outlook of other Yen crosses.

In Asia, at the time of writing, Nikkei is up 0.24%. Hong Kong HSI is up 0.09%. China Shanghai SSE is up 1.14%. Singapore Strait Times is up 0.37%. Japan 10-year JGB yield is up 0.0202 at 0.423. Overnight DOW dropped -0.14%. S&P 500 dropped -0.04%. NASDAQ dropped -0.11%. 10-year yield rose 0.122 to 3.574.

RBA defies expectations with rate hike, may still require further tightening

In a surprising move, RBA raises cash rate target by 25bps to 3.85%, contrary to market expectations of a hold. Nevertheless, RBA softened its tightening bias, stating, "some further tightening of monetary policy may be required," depending on "how the economy and inflation evolve."

Despite acknowledging that Australian inflation "has passed its peak" and "recent data showed a welcome decline," the central bank still expects inflation to be at 4.25%, slowing to 3% in mid-2025. That is, "it takes a couple of years before inflation returns to the top of the target range". RBA added that services price inflation remains "still very high and broadly based" with upside risks, while goods inflation is decelerating.

RBA projects the economy to grow by 1.25% in 2023 and around 2% over the year to mid-2025. With anticipated below-trend economic growth, unemployment rate is forecast to gradually increase to around 4.5% in mid-2025.

RBNZ Hawkesby: Not currently seeing widespread financial distress amongst households or businesses

According to RBNZ Financial Stability Report, debt servicing costs for households with mortgages are expected to more than double by the end of the year. Despite this, household balance sheets remain resilient, with most having substantial equity buffers. Early-stage arrears have increased but remain low compared to post-Global Financial Crisis levels. Banks' strong capital positions allow them to support customers, and borrowers facing stress are encouraged to seek assistance from their banks.

"We are not currently seeing widespread financial distress amongst households or businesses, which reflects the strength in the economy and labour market to date. However, more borrowers may fall behind on their payments this year, given the ongoing repricing of mortgages and expected weakening in the labour market,"Deputy Governor Christian Hawkesby says.

"Recent profitability and strong capital positions puts banks in a good position to take a long-term view and support their customers. We encourage borrowers encountering stress to talk to their banks, as hardship programmes may be available, and some customers may be able to temporarily switch to interest-only payments or increase the remaining term of their loan."

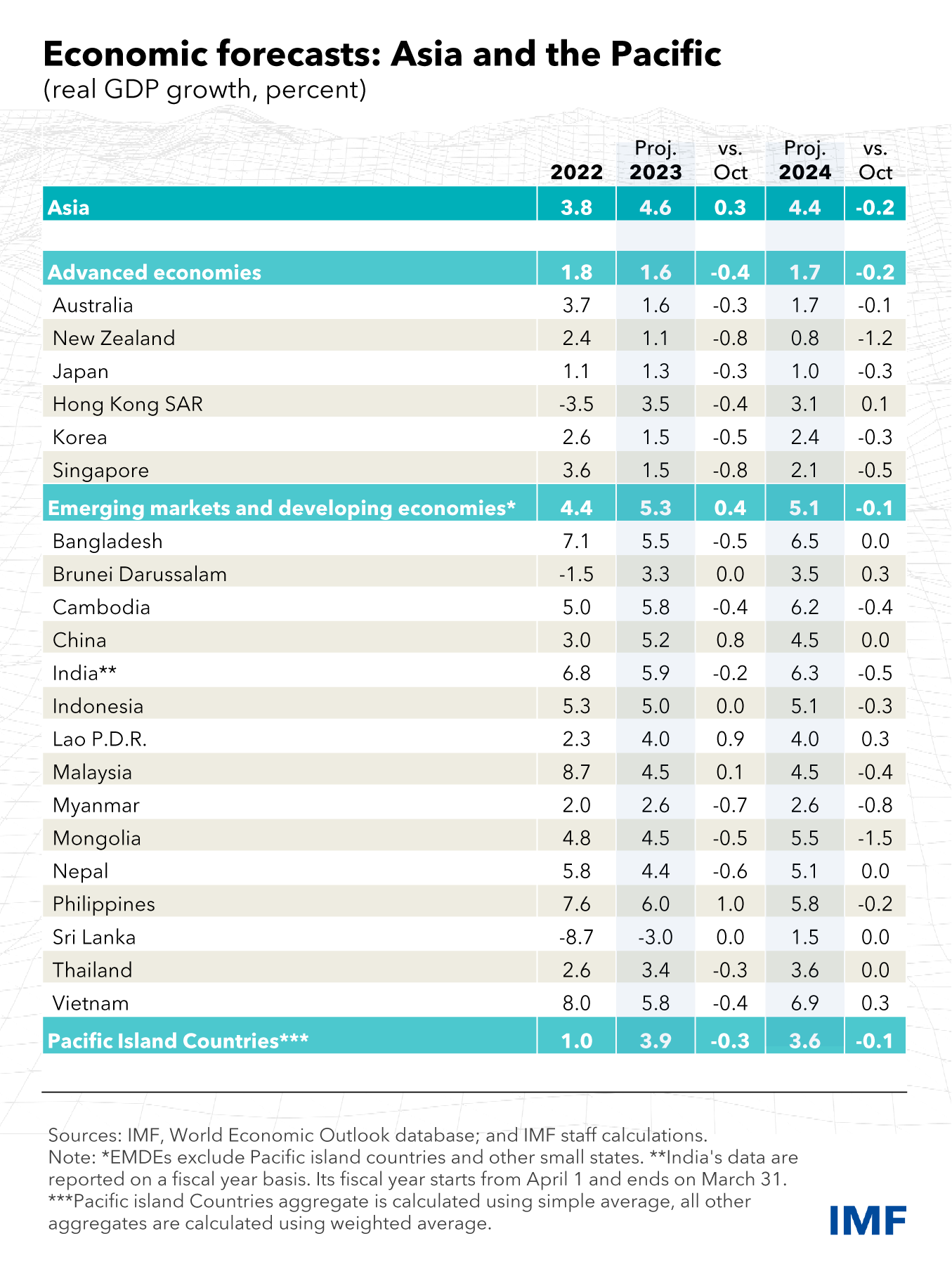

IMF raises 2023 Asia growth forecasts on strong emerging markets

IMF raised its 2023 growth forecast for Asia by 0.3% to 4.6%, outpacing the 3.8% growth rate in 2022. For 2024, the growth projection has been slightly downgraded by -0.2% to 4.4%.

The growth forecast for advanced economies in the region was downgraded by -0.4% to 1.6% in 2023 and by -0.2% to 1.7% in 2024. Meanwhile, emerging markets and developing economies experienced an upgraded growth forecast of 0.3% to 5.3% in 2023, although their 2024 projections were downgraded by -0.1% to 5.1%.

IMF highlighted that "Asia's domestic demand has so far remained strong despite monetary tightening, while external appetite for technology products and other exports is weakening".

However, the organization warned that "Global growth is poised to decelerate as rising interest rates and Russia's war in Ukraine weigh on activity. Inflation remains stubbornly high, and banking strains in the United States and Europe have injected greater uncertainty into an already complex economic landscape."

Looking ahead

Germany retail sales, Swiss SEO consumer climate and PMI manufacturing; Eurozone PMI manufacturing final and CPI flash, and UK PMI manufacturing final will be released in European session. Later in the day, US will publish factory orders.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6603; (P) 0.6635; (R1) 0.0.6663; More...

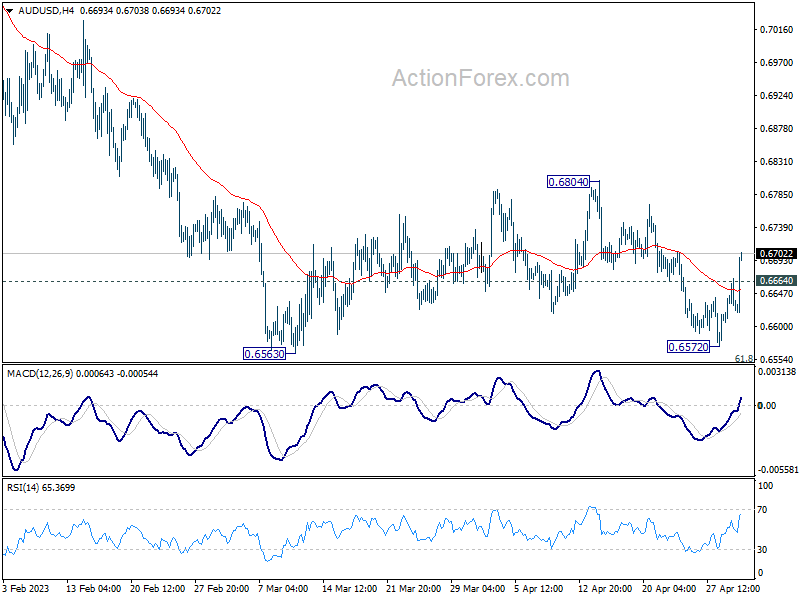

AUD/USD's extended rebound and break of 0.6664 minor resistance suggests that fall from 0.6804 has completed ahead of 0.6563 low. Intraday bias is back on the upside for stronger rise. Still, outlook remains bearish as long as 0.6804 resistance holds, and down trend resumption through 0.6563 low is in favor at a later stage. Nevertheless, sustained break of 0.6804 should indicate completion of whole fall from 0.7156, and turn near term outlook bullish for retesting this high instead.

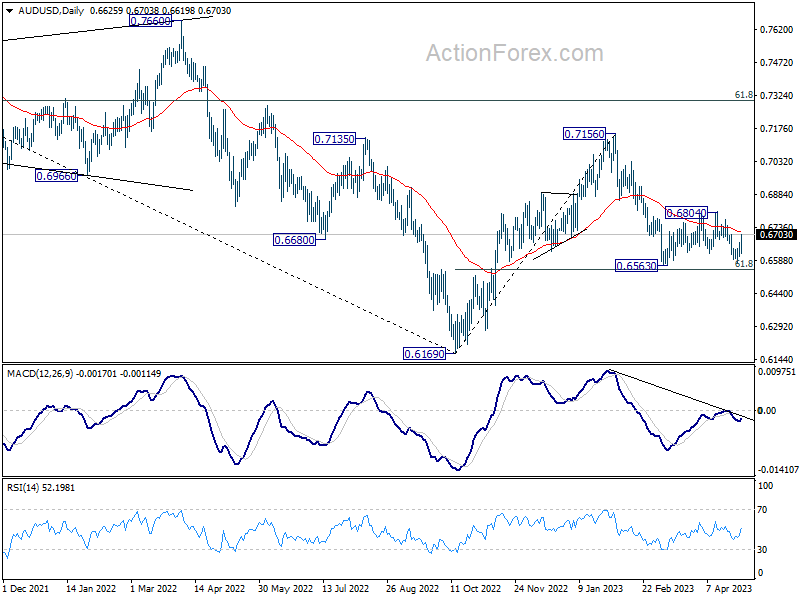

In the bigger picture, as long as 61.8% retracement of 0.6169 to 0.7156 at 0.6546 holds, the decline from 0.7156 is seen as a correction to rally from 0.6169 (2022 low) only. Another rise should still be seen through 0.7156 at a later stage. However, sustained break of 0.6546 will raise the chance of long term down trend resumption through 0.6169 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Apr | -1.70% | -1.50% | -1.00% | |

| 04:30 | AUD | RBA Interest Rate Decision | 3.85% | 3.60% | 3.60% | |

| 06:00 | EUR | Germany Retail Sales M/M Mar | 0.40% | -1.30% | ||

| 07:00 | CHF | SECO Consumer Climate Q2 | -22 | -30 | ||

| 07:30 | CHF | Manufacturing PMI Apr | 50 | 47 | ||

| 07:45 | EUR | Italy Manufacturing PMI Apr | 49 | 51.1 | ||

| 07:50 | EUR | France Manufacturing PMI Apr F | 45.5 | 45.5 | ||

| 07:55 | EUR | Germany Manufacturing PMI Apr F | 44 | 44 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Apr F | 45.5 | 45.5 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | 3.10% | 2.90% | ||

| 08:30 | GBP | Manufacturing PMI Apr F | 46.6 | 46.6 | ||

| 09:00 | EUR | Eurozone CPI Y/Y Apr P | 6.90% | 6.90% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr P | 5.70% | 5.70% | ||

| 14:00 | USD | Factory Orders M/M Mar | 0.80% | -0.70% |

RBA defies expectations with rate hike, may still require further tightening

In a surprising move, RBA raises cash rate target by 25bps to 3.85%, contrary to market expectations of a hold. Nevertheless, RBA softened its tightening bias, stating, "some further tightening of monetary policy may be required," depending on "how the economy and inflation evolve."

Despite acknowledging that Australian inflation "has passed its peak" and "recent data showed a welcome decline," the central bank still expects inflation to be at 4.25%, slowing to 3% in mid-2025. That is, "it takes a couple of years before inflation returns to the top of the target range". RBA added that services price inflation remains "still very high and broadly based" with upside risks, while goods inflation is decelerating.

RBA projects the economy to grow by 1.25% in 2023 and around 2% over the year to mid-2025. With anticipated below-trend economic growth, unemployment rate is forecast to gradually increase to around 4.5% in mid-2025.

(RBA) Statement by Philip Lowe, Governor: Monetary Policy Decision

At its meeting today, the Board decided to increase the cash rate target by 25 basis points to 3.85 per cent. It also increased the rate paid on Exchange Settlement balances by 25 basis points to 3.75 per cent.

Inflation in Australia has passed its peak, but at 7 per cent is still too high and it will be some time yet before it is back in the target range. Given the importance of returning inflation to target within a reasonable timeframe, the Board judged that a further increase in interest rates was warranted today.

The Board held interest rates steady last month to provide additional time to assess the state of the economy and the outlook. While the recent data showed a welcome decline in inflation, the central forecast remains that it takes a couple of years before inflation returns to the top of the target range; inflation is expected to be 4½ per cent in 2023 and 3 per cent in mid-2025. Goods price inflation is clearly slowing due to a better balance of supply and demand following the resolution of the pandemic disruptions. But services price inflation is still very high and broadly based and the experience overseas points to upside risks. Unit labour costs are also rising briskly, with productivity growth remaining subdued.

The recent Australian data also confirmed that the labour market remains very tight, with the unemployment rate at a near 50-year low. Many firms continue to experience difficulty hiring workers, although there has been some easing in labour shortages and the number of vacancies has declined a little.

The Board's priority remains to return inflation to target. High inflation makes life difficult for people and damages the functioning of the economy. And if high inflation were to become entrenched in people's expectations, it would be very costly to reduce later, involving even higher interest rates and a larger rise in unemployment. Medium-term inflation expectations remain well anchored, and it is important that this remains the case. Today's further adjustment in interest rates will help in this regard.

Wages growth has picked up in response to the tight labour market and high inflation. At the aggregate level, wages growth is still consistent with the inflation target, provided that productivity growth picks up. The Board remains alert to the risk that expectations of ongoing high inflation contribute to larger increases in both prices and wages, especially given the limited spare capacity in the economy and the historically low rate of unemployment. Accordingly, it will continue to pay close attention to both the evolution of labour costs and the price-setting behaviour of firms.

The Board is still seeking to keep the economy on an even keel as inflation returns to the 2–3 per cent target range, but the path to achieving a soft landing remains a narrow one. The central forecast is for the economy to continue growing, albeit at a below-trend pace; GDP is forecast to increase by 1¼ per cent this year and around 2 per cent over the year to mid-2025. Given the expected below-trend growth in the economy, the unemployment rate is forecast to increase gradually to be around 4½ per cent in mid-2025.

A significant source of uncertainty continues to be the outlook for household consumption. The combination of higher interest rates, cost-of-living pressures and the earlier decline in housing prices is leading to a substantial slowing in household spending. While some households have substantial savings buffers, others are experiencing a painful squeeze on their finances. There are also uncertainties regarding the global economy, which is expected to grow at a below-average rate over the next couple of years.

Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will depend upon how the economy and inflation evolve. The Board will continue to pay close attention to developments in the global economy, trends in household spending and the outlook for inflation and the labour market. The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that.

IMF raises 2023 Asia growth forecasts on strong emerging markets

IMF raised its 2023 growth forecast for Asia by 0.3% to 4.6%, outpacing the 3.8% growth rate in 2022. For 2024, the growth projection has been slightly downgraded by -0.2% to 4.4%.

The growth forecast for advanced economies in the region was downgraded by -0.4% to 1.6% in 2023 and by -0.2% to 1.7% in 2024. Meanwhile, emerging markets and developing economies experienced an upgraded growth forecast of 0.3% to 5.3% in 2023, although their 2024 projections were downgraded by -0.1% to 5.1%.

IMF highlighted that "Asia's domestic demand has so far remained strong despite monetary tightening, while external appetite for technology products and other exports is weakening".

However, the organization warned that "Global growth is poised to decelerate as rising interest rates and Russia's war in Ukraine weigh on activity. Inflation remains stubbornly high, and banking strains in the United States and Europe have injected greater uncertainty into an already complex economic landscape."

RBNZ Hawkesby: Not currently seeing widespread financial distress amongst households or businesses

According to RBNZ Financial Stability Report, debt servicing costs for households with mortgages are expected to more than double by the end of the year. Despite this, household balance sheets remain resilient, with most having substantial equity buffers. Early-stage arrears have increased but remain low compared to post-Global Financial Crisis levels. Banks' strong capital positions allow them to support customers, and borrowers facing stress are encouraged to seek assistance from their banks.

"We are not currently seeing widespread financial distress amongst households or businesses, which reflects the strength in the economy and labour market to date. However, more borrowers may fall behind on their payments this year, given the ongoing repricing of mortgages and expected weakening in the labour market,"Deputy Governor Christian Hawkesby says.

"Recent profitability and strong capital positions puts banks in a good position to take a long-term view and support their customers. We encourage borrowers encountering stress to talk to their banks, as hardship programmes may be available, and some customers may be able to temporarily switch to interest-only payments or increase the remaining term of their loan."

Elliott Wave View Suggests Silver (XAGUSD) Correction Still Ongoing

Silver (XAGUSD) ended cycle from 3.10.2023 with wave 1 at 26.08 as the 45 minutes chart below shows. The metal is now correcting cycle from 3.10.2023 low in wave 2. Internal subdivision of wave 2 is unfolding as a double three Elliott Wave structure. Down from wave 1, wave a ended at 24.78 and wave b rally ended at 25.31. Wave c lower ended at 24.62 which completed wave (w). Corrective rally in wave (x) ended at 25.48. The metal resumes lower in wave (y) with internal subdivision as a zigzag. Down from wave (x), wave a ended at 24.76 and wave b ended at 25.35. Wave c lower ended at 24.47 which completed wave (y) and ((w)) in higher degree.

From there, the metal formed wave ((x)) connector with internal subdivision as a double three in lesser degree. Up from wave ((w)), wave (w) ended at 25.22 and pullback in wave (x) ended at 24.49. Wave (y) higher ended at 25.9 which completed wave ((x)) in higher degree. The metal then turns lower in wave ((y)) with internal subdivision as a zigzag. Down from wave ((x)), wave (a) ended at 24.86. Expect rally in wave (b) to fail in 3, 7, or 11 swing for further downside. Potential target lower is 100% – 161.8% Fibonacci extension of wave ((w)) which comes at 23.31 – 24.29 area. Near term, as far as pivot at 26.08 high stays intact, expect rally to fail in 3, 7, 11 swing for further downside.

Silver 45 Minute Elliott Wave Chart

XAGUSD Elliott Wave Video

https://www.youtube.com/watch?v=TjLqxrHPjbY

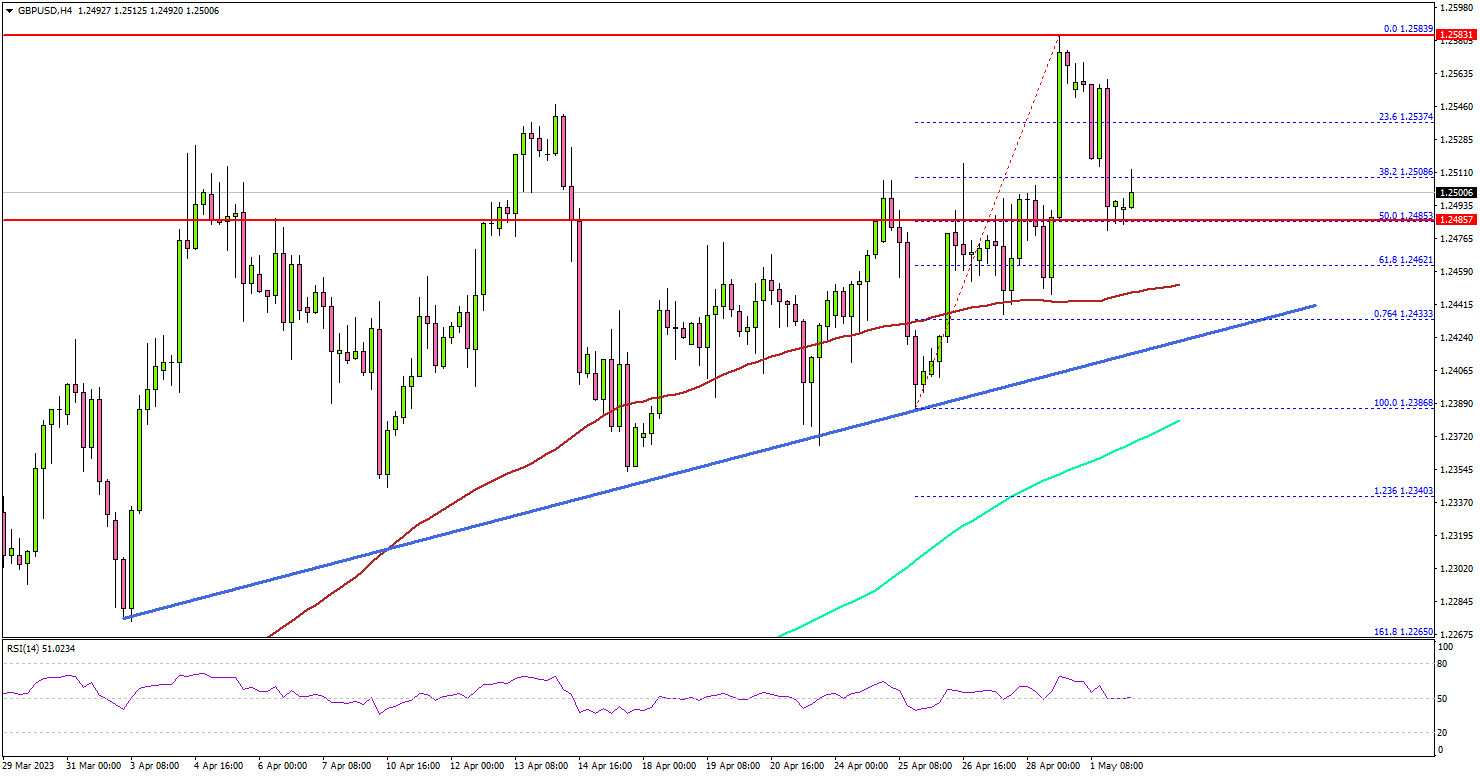

GBP/USD Holds Uptrend Support, USD/JPY Extends Rally

Key Highlights

- GBP/USD corrected lower from the 1.2580 zone.

- A key bullish trend line is forming with support near 1.2430 on the 4-hour chart.

- USD/JPY extended its rally and climbed above the 137.00 level.

- Gold price is struggling to gain pace for a move above $2,000.

GBP/USD Technical Analysis

The British Pound remained in a positive zone above the 1.2400 level against the US Dollar. GBP/USD even climbed above the 1.2520 and 1.2550 resistance levels.

Looking at the 4-hour chart, the pair traded to a new multi-week high at 1.2583 before it faced sellers. There was a minor downside correction below the 1.2550 level, but the pair is trading well above the 100 simple moving average (red, 4 hours).

There is also a key bullish trend line forming with support near 1.2430 on the same chart. The trend line is close to the 100 simple moving average (red, 4 hours).

If there is a downside break below the trend line, the pair might slide toward the 1.2400 support zone or the 200 simple moving average (green, 4 hours). The next major support sits near the 1.2340 level.

Immediate resistance on the upside is near the 1.2550 level. The next key resistance is near the 1.2580 level. A clear upside break and close above the 1.2580 resistance might start a strong increase. The next key resistance is near the 1.2620 zone. Any more gains might send the pair toward 1.2700.

Looking at USD/JPY, there were strong bullish moves and the pair even climbed to a new multi-month high above the 137.00 level.

Economic Releases

- Euro Zone CPI for April 2023 (YoY) (Prelim) - Forecast +6.9%, versus +6.9% previous.

- Euro Zone Core CPI for April 2023 (YoY) (Prelim) - Forecast +5.7%, versus +5.7% previous.

- US Factory Orders for March 2023 (MoM) - Forecast +0.8%, versus -0.7% previous.

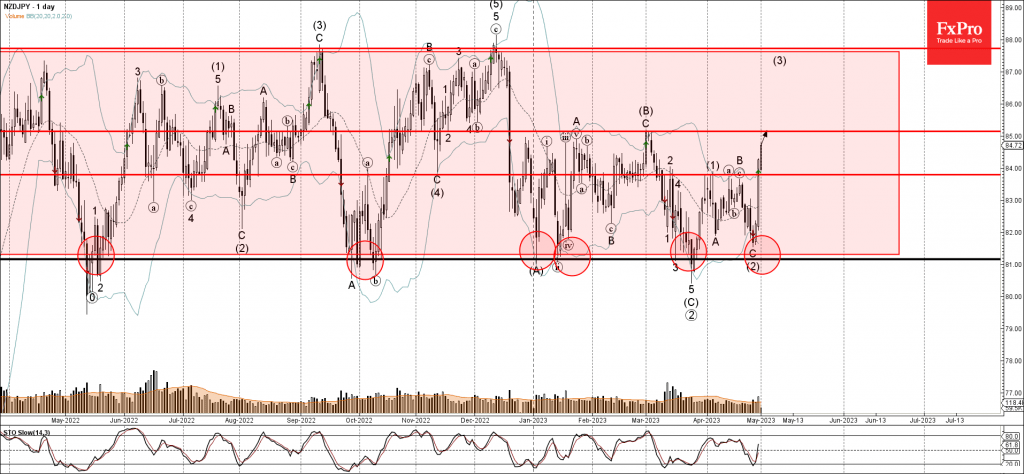

NZDJPY Wave Analysis

- NZDJPY broke resistance level 83.80

- Likely to rise to resistance level 85.00

NZDJPY currency pair recently broke above the resistance level 83.80 (which stopped the previous waves 2, (1), (a) and B).

The breakout of the resistance level 83.80 continues the active medium-term impulse wave (3) from the end of April.

NZDJPY currency pair can be expected to rise further toward the next resistance level 85.00 (top of wave (B) from the start of March).

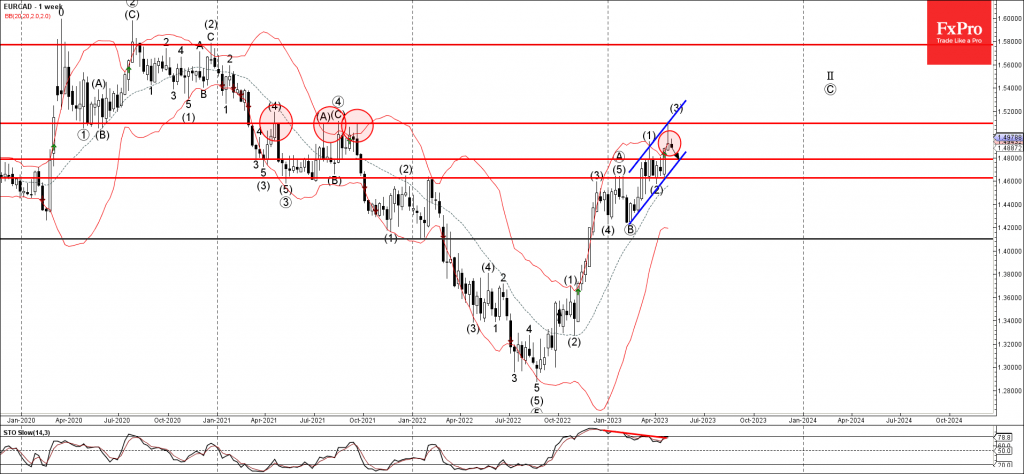

EURCAD Wave Analysis

- EURCAD reversed from long-term resistance level 1.5095

- Likely to fall to support level 1.4800

EURCAD currency pair previously reversed down strongly from the long-term resistance level 1.5095 (which has been steadily reversing the pair from the start of 2021).

The resistance level 1.5095 was strengthened by the resistance trendline of the weekly up channel from the start of this year.

Given the triple bearish divergence one the weekly Stochastic indicator, EURCAD currency pair can be expected to fall further toward the next support level 1.4800.