Sample Category Title

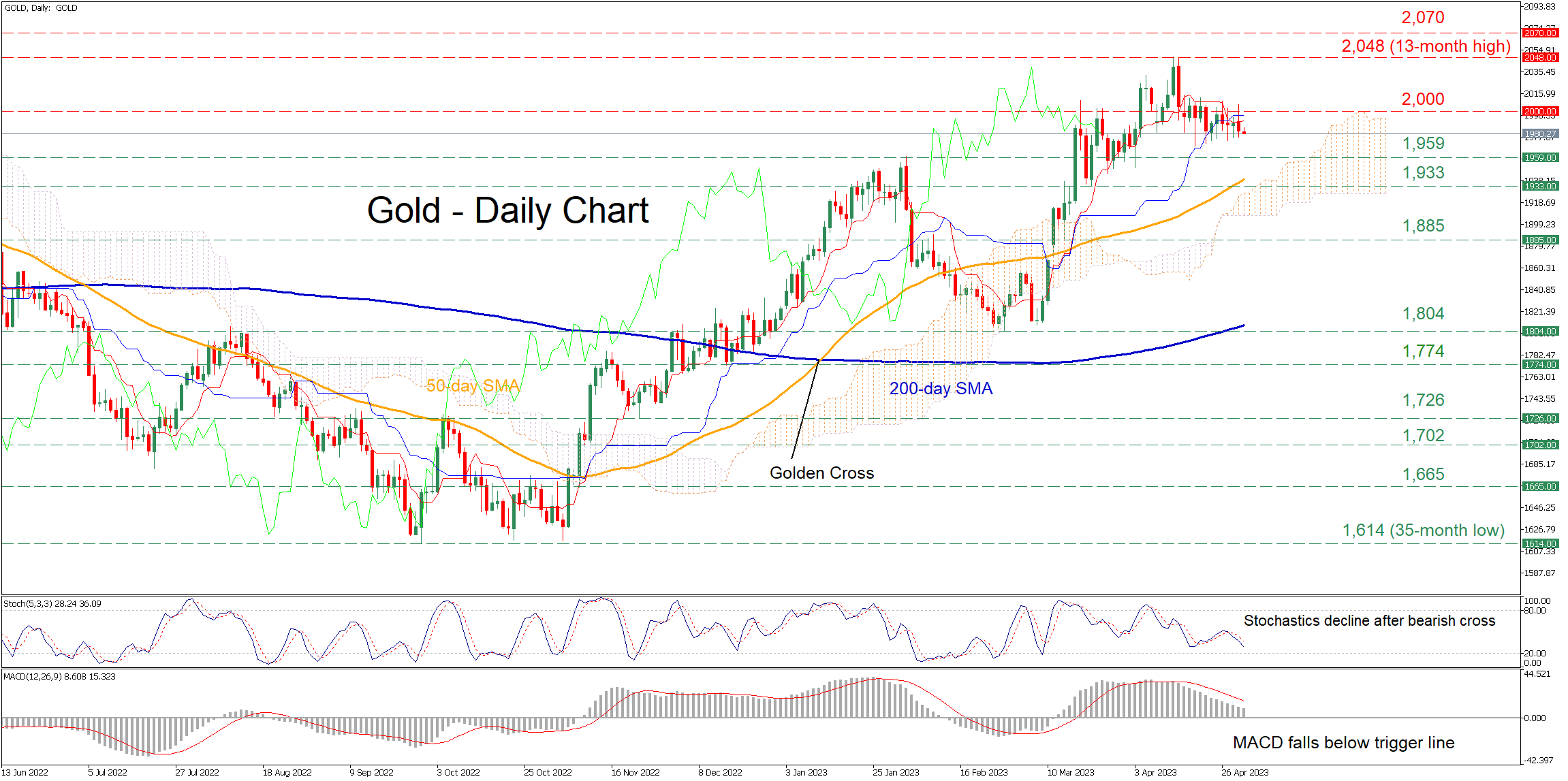

Gold Remains Rangebound Beneath 2,000

Gold experienced a remarkable surge since early March, forming a series of higher highs to peak at the 13-month high of 2,048. However, bullion quickly retraced lower, falling below the 2,000 mark and trading without a clear direction in the past few daily sessions.

The momentum indicators currently suggest that bullish forces are subsiding but have not surrendered yet. Specifically, the stochastic oscillator is declining after posting a bearish cross, while the MACD histogram fell below its red signal line but remains positive. Nevertheless, the price is currently way beyond the Ichimoku cloud, hinting that the short-term picture has not turned bearish yet.

If bullish pressures fade completely and the price moves to the downside, the February resistance region of 1,959 could serve as initial support. Dipping beneath that zone, gold could descend to challenge 1,933 before the 1,885 hurdle comes under examination. Should that barricade fail, the 2023 low of 1,804 could prove a tough obstacle for the price to overcome.

Alternatively, should buyers regain the upper hand, the 2,000 psychological mark might provide immediate resistance. A violation of that crucial level could pave the way for the 13-month high of 2,048. Failing to stop there, further advances may cease at the March 2022 high of 2,070 registered after Russia’s invasion of Ukraine.

Overall, gold has been trading sideways for the past two weeks, appearing unable to adopt a clear directional impetus. Therefore, a fresh higher high or lower low is needed for this neutral technical picture to alter.

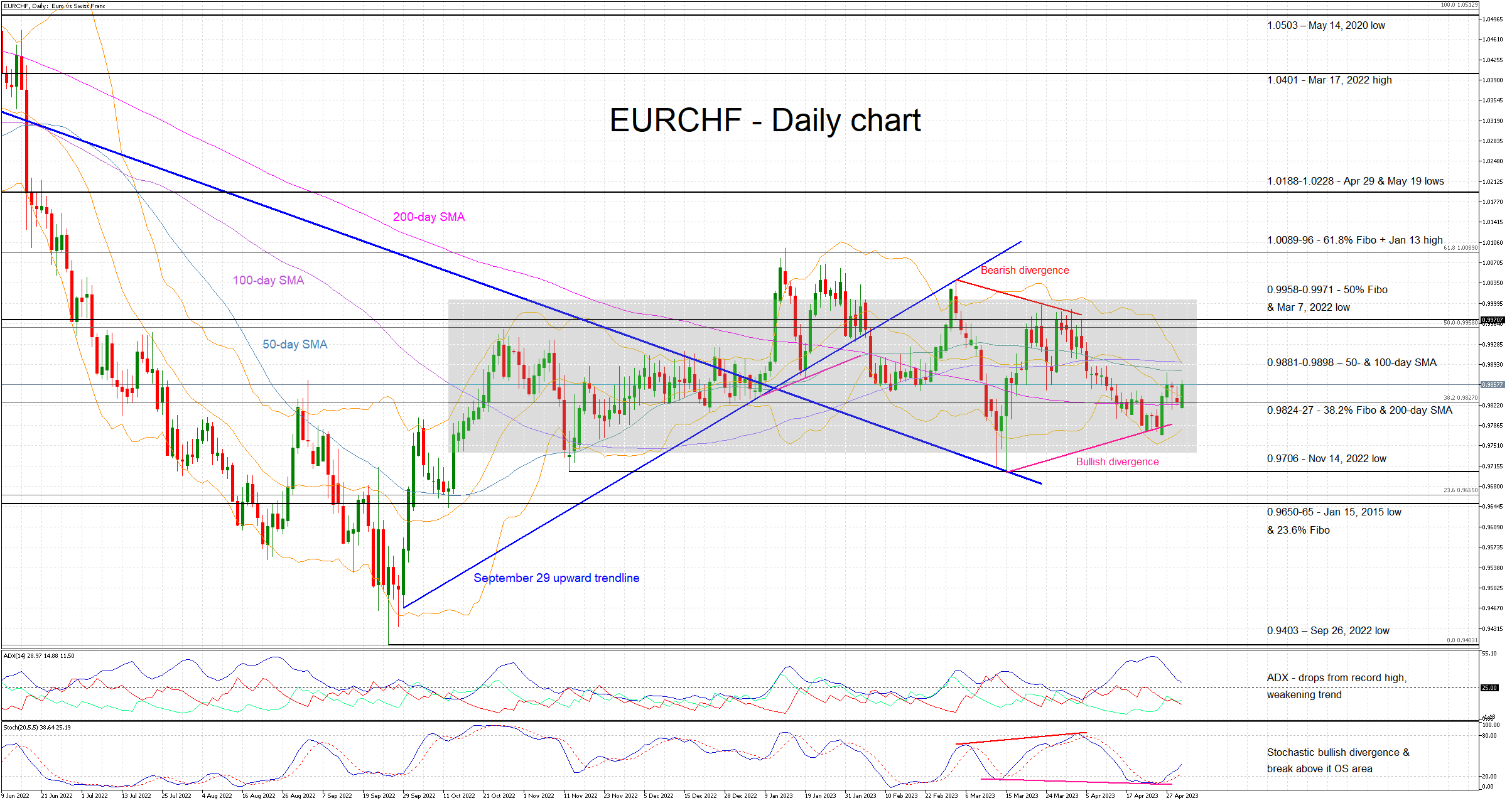

EURCHF Moves Higher, But Overall Picture Remains Mixed

EURCHF is edging higher today, bouncing off a support area defined by the 200-day simple moving average (SMA) and the 38.2% Fibonacci retracement of the June 9, 2022 – September 26, 2022 downtrend respectively. The recent upleg could be the product of the recent bullish divergence that formed between the EURCHF lows and the stochastic oscillator, which has the potential to further impact price action.

A smile has most likely appeared on the bulls’ faces, especially if one adds the stochastic’s recent move. It has broken above its moving average and its oversold area, and it is moving higher in a vertical fashion. However, the Average Directional Movement Index (ADX) is just a tad above its 25-threshold, pointing to a weakening trend. Nevertheless, it is worth noting that the SMAs' convergence and the relative tightening of the Bollinger bands remain in play at this juncture.

Should the bulls decide to push the market higher, the next key resistance area will come at the 50- and 100-day SMAs at the 0.9881-0.9898 area. The 61.8% Fibonacci retracement and the January 13, 2023 high at the 1.0089-1.0096 range could then prove tougher to crack.

On the other hand, the bears would have to deal with the 0.9824-27 range first, populated by the 38.2% Fibonacci retracement and 200-day SMA. The lower boundary of the current rectangle at 0.9741 comes next, very close to the November 14, 2022 low at 0.9706 that appears to be a stronger support area, as seen at the mid-March breakout.

To sum up, EURCHF bulls might feel a bit more confident on the back of the current stochastic oscillator move. But the overall technical picture remains mixed, especially as the price action continues to be confined by the recent rectangle.

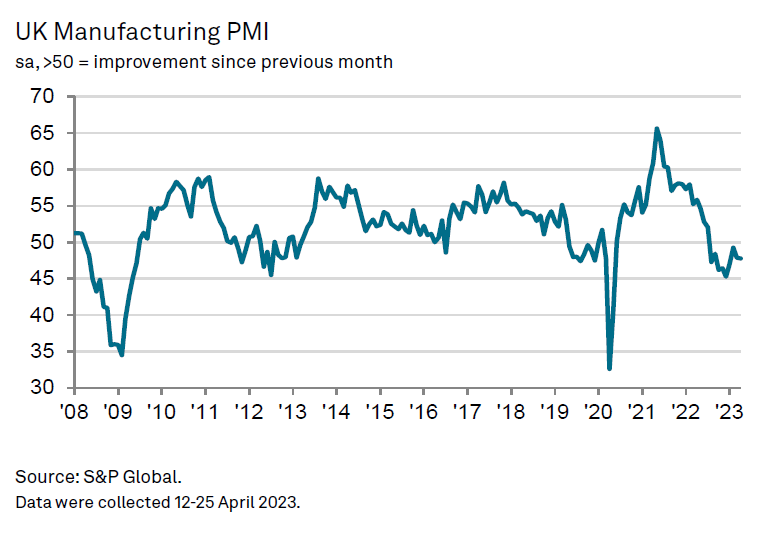

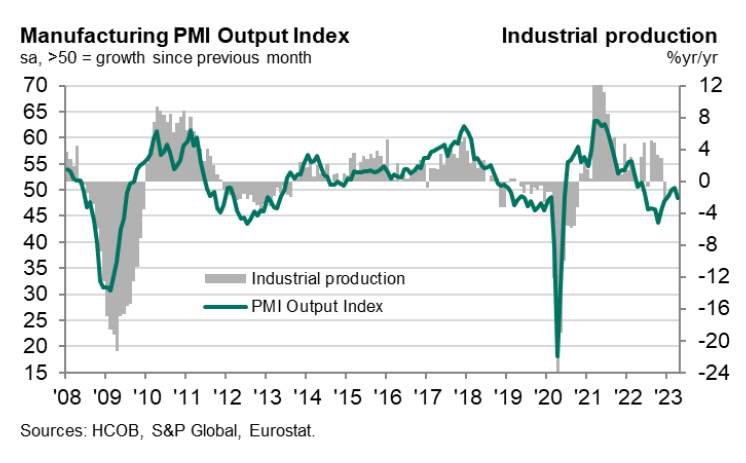

UK PMI manufacturing finalized at 47.8, remained in the doldrums

UK PMI Manufacturing was finalized at 47.8 in April, slightly down from March's 47.9. Output, new orders, employment and stocks of purchases all contracted and vendor lead times improved (a sign of weaker demand for inputs hurting suppliers).

Rob Dobson, Director at S&P Global Market Intelligence, said: "The UK manufacturing sector remained in the doldrums at the start of the second quarter. Output and new orders contracted, as manufacturers felt the impacts of client uncertainty, destocking and tightening cost controls. There was no escape from the subdued mood of the market, with both domestic and export customers remaining reticent to commit to new contracts."

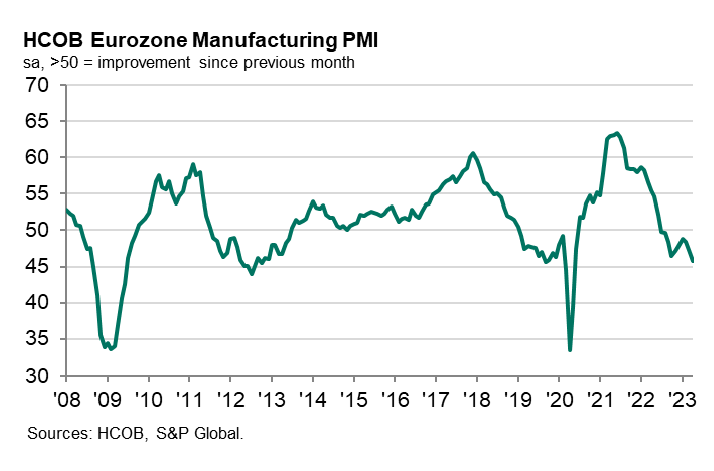

Eurozone PMI manufacturing finalized at 45.8, 35-month low

Eurozone PMI Manufacturing was finalized at 45.8 in April, a 35-month low. The index was also below the 50 no-change mark for a tenth straight month. PMI Manufacturing Output was finalized at 48.5, a 4-month low.

PMI Manufacturing of all major states declined in the month, and recorded contractionary reading except Greece (52.4). Ireland (48.6), France (45.6), the Netherlands (44.9), Germany (44.5) and Austria (42.0) were all at 35-month low. Spain was at 3-month low of 49.0 while Italy was at 6-month low at 46.8.

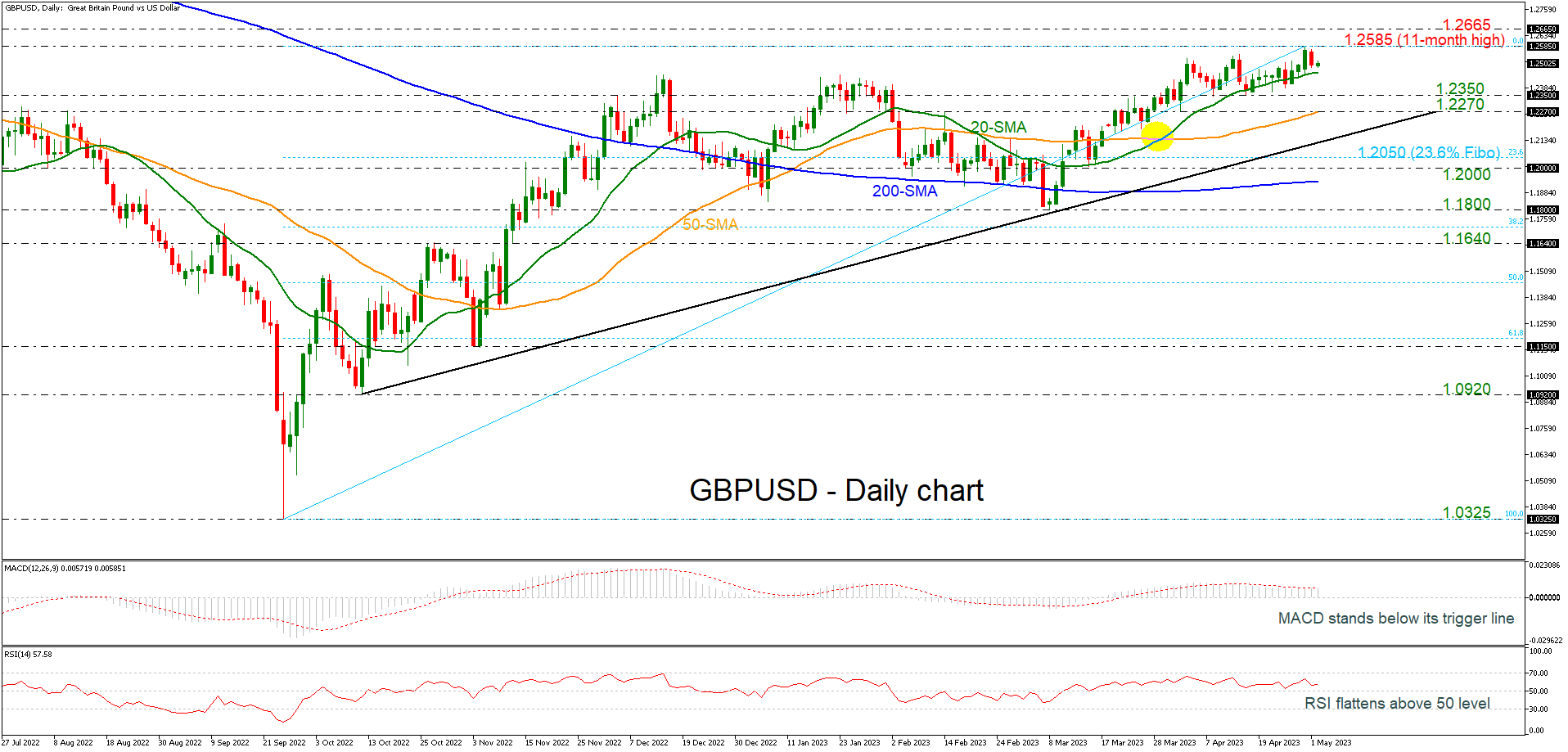

GBPUSD Meets 1.2500 after Hitting 11-month High

GBPUSD is retreating after the climb towards a new eleven-month high of 1.2585 in the previous week and is finding significant support near the 20-day simple moving average (SMA). Currently, the market remains well above the long-term uptrend line, indicating more gains. The MACD oscillator is moving sideways in the positive territory, while the RSI is ticking marginally higher above the neutral threshold of 50.

More upside pressures could open the way for a retest of the previous high of 1.2585 ahead of the 1.2665 resistance, registered in May 2022. Above this hurdle, the 200-weekly SMA, which hovers near the next resistance of 1.2855, may halt the bullish moves.

Alternatively, any downside movements could re-challenge the 20-day SMA at 1.2450 before slipping towards the 1.2270-1.2350 support region, which encapsulates the 50-day SMA too. Beneath these levels, the ascending trend line around 1.2170 could act as a turning point for traders ahead of resting near the 23.6% Fibonacci retracement level of the up leg from 1.0325 to 1.2585 at 1.2050.

All in all, GBPUSD is continuing to maintain an upside structure and only a plunge below the uptrend line and the 200-day SMA at 1.1940 could switch the outlook to bearish.

Surprise RBA Hike Revives Hawks, as US Bank Stress Wanes

JP Morgan swallowed the First Republic Bank (FRC) on Monday and will assume all its deposits.

Capital flew out of US treasuries yesterday as bank stress waned, the S&P500 closed slightly lower yesterday, but it made a positive attempt to the 4186 mark, the highest since February this year. Nasdaq 100 advanced to the highest level this year despite the rising US yields yesterday.

The Federal Reserve (Fed) begins its two-day policy meeting in relatively calmer conditions.

Many think that this week’s 25bp hike will mark the Fed’s tightening cycle, but the surprise hike from the Reserve Bank of Australia (RBA) this morning hints that it may not be the case.

Elsewhere, the eurozone will reveal its quarterly survey of bank lending which will show how the recent bank stress impacted credit growth in Europe, and the flash CPI figures for April. Both data are extremely important for shaping the expectations regarding what the European Central Bank (ECB) will do this Thursday.

https://www.youtube.com/watch?v=6B_eO5xsr9Q

Investors Brace for Packed Week of Risk Events

Asian equities were mixed on Tuesday with some markets closed as investors braced for a heavy event week packed with top-tier data releases and key central bank meetings. European futures are signalling a mixed open with market players awaiting the start of the Fed meeting and rate decision on Wednesday. In the currency space, the dollar edged lower while AUD surged after the Reserve Bank of Australia (RBA) unexpectedly raised interest rates. Gold prices continue to be trapped within a range while oil prices remained pressured by concerns about China’s economic outlook.

The new few days could be explosively volatile for markets due to the Fed and ECB meetings, as well as key data including the US ISM Services and Friday’s monthly non-farm payrolls report. Some volatility can already be seen in the FX space after the RBA surprised markets by hiking rates by 25 basis points this morning. Aussie bulls dominated the scene following the news, rallying over 1% against the dollar to punch above 0.6700. Given how the overall tone of the RBA statement sounded hawkish with the central bank warning of more hikes to come, this could support the aussie moving forward.

Dollar braces for Fed decision and NFP cocktail

The past few weeks have been rough for the dollar thanks to expectations around the Fed pausing rate hikes after the FOMC meeting on Wednesday. Markets widely expect the central bank to raise interest rates by 25 basis points this week, taking the upper band of the Fed funds rate to 5.25%. Investors will be closely scrutinising the statement and Powell’s press conference for any confirmation that a pause in hikes is on the table. Should Powell adopt a more cautious tone, this could whack the dollar, pulling the DXY back towards major support at 100.79.

The next major risk event for the dollar will then be April’s non-farm payrolls report on Friday. Markets expect the US economy to have created 180k jobs in April, which is less than the prior month, while the unemployment rate is seen rising to 3.6%. If the US jobs report is stronger than market forecasts, this may support expectations around the Fed keeping US rates higher for longer. However, if the jobs data disappoints, this could feed bets around the Fed pausing hikes before eventually cutting rates. That outcome could result in further dollar weakness.

Currency spotlight – EUR/USD

This could be a wild week for EURUSD thanks to the Fed and ECB rate decisions, as well as top- tier data from Europe and the United States. The ECB is also expected to hike interest rates by 25bp, on Thursday. But it may be wise to keep an eye on the latest eurozone CPI numbers and Bank Lending Survey released on Tuesday which could influence what the central bank does.

Taking a look at the technical picture, EURUSD seems trapped within a range with bears eyeing support at 1.0950. A break below this level could signal a decline toward 1.0910 and 1.0845. Alternatively, if 1.0950 proves to be reliable support, prices may venture back toward 1.1075 resistance.

Commodity Spotlight – Gold

Gold prices struggled for direction on Tuesday, in what felt like the calm before the storm. Prices remain trapped within a range and waiting for a fresh fundamental spark to trigger a breakout. The array of heavy risk events this week, ranging from the Federal Reserve decision and NFP among other key releases could inject fresh life into gold.

In the meantime, prices are tracking sideways between $1970 and $2015 with the major psychological level of $2,000 at the centre. A strong breakout above $2015 may encourage a move toward the April high at $2047. Alternatively, a breakdown below $1970 could open the doors toward $1950 and $1935, respectively.

RBA Update: An Unexpected Hike Triggered a Squeeze on AUD/USD

- RBA surprised the market with a 25 basis points hike to bring the policy cash rate to 3.85%

- Emphasis on inflation targeting over concerns about the heightened risk of slower growth

- AUD/USD breached above the 50-day moving average, resurgence of short-term upside momentum.

The Reserve Bank of Australia (RBA) has surprised market participants’ view of a second consecutive pause of its key policy cash rate with a hike of 25 basis points to bring it to 3.85%.

Concerns about sticky inflation and entrenched high inflationary expectations

The accompanying RBA Governor Philip Lowe’s statement has indicated fears of sticky inflation via services and rising unit labour costs despite both the headline and trimmed mean CPI cooled from a 30-year high in Q1 2023; the current concerns are medium-term inflationary expectations remain well anchored and the risk of having to hike interest rates higher for longer later to reduce the high inflation expectations entrenched in peoples’ minds outweighs the benefits of keeping the cash rate unchanged at 3.6%; as it may cause a larger rise in unemployment.

Secondly, RBA is also concerned that the risk of ongoing high inflationary expectations contributes to larger increases in both prices and wages given that the current limited space capacity in the economy and a close to a 50-year low rate of seasonally adjusted unemployment at 3.5%.

Thirdly, it emphasizes priority remains to return inflation to the target at 3% to 2%; the central forecasts remain that it takes a couple of years before inflation hit the upper limit of the target range; inflation growth is expected to slow down to 4.5% by end of 2023 and 3% in the middle of 2025.

RBA forward guidance has become “wishy-washy”

Going forward, it seems RBA has a wishy-washy stance on its forward guidance, and right now, the emphasis is on inflation targeting rather than addressing the negative knock-on effects from tightening monetary policy lags toward economic growth amid a slowing global economy reinforced by the latest weak China’s manufacturing PMI data despite acknowledgment that the path to achieving a soft landing remains a narrow one.

AUD/USD moved higher ex-post RBA decision

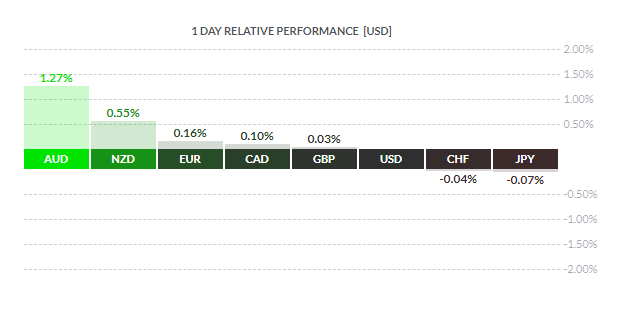

The AUD/USD has squeezed up higher and rallied by 1.27% and 89 pips from its current intraday low of 0.8890: making it the strongest performer against the US dollar among the major currencies at today’s Asian session at this time of the writing.

Fig 1: major currencies intraday performance against USD as of 2 May 2023 (Source: finviz.com , click to enlarge chart)

The AUD/USD has squeezed up higher and rallied by 1.27% and 95 pips from its current intraday low of 0.8890: making it the strongest performer against the US dollar among the major currencies at today’s Asian session at this time of the writing.

It has now breached above the 50-day moving average acting as a resistance at 0.6680 which may trigger a further short-term upside momentum. The next resistance is coming in at around 0.6800 which is the medium-term range top in place since 4 April 2023 while key short-term support lies at 0.6580

USD Attempts to Bounce

GBP/USD seeks support

The US dollar recoups some losses ahead of the FOMC this Wednesday. The latest horizontal consolidation has managed to stay above the 30-day SMA and suggests that the bias remains bullish in the medium-term. A surge above the recent high of 1.2540 would resume the upward trajectory, making May 2022’s high of 1.2660 as the next threshold. As the RSI cools down, trend followers are expected to offer support around 1.2450 which coincides with the 20-day SMA. 1.2370 is key in keeping the momentum intact.

EUR/JPY continues to climb

The Japanese yen extended losses after the BOJ hinted at continuing monetary easing. The latest surge has propelled the pair above the December 2014 high of 149.00 and the psychological level of 150.00, which may keep the yen under pressure for a prolonged period of time. With the RSI easing from its overbought condition, the bulls may see in a pullback an opportunity to stake in ahead of a new round of rally. 148.90 is the closest support with 147.00 as a second layer. A close above 151.50 would carry the momentum further.

GER 40 clears resistance

Equity markets steady as JPMorgan took control of ailing First Republic Bank. A tentative break below 15720 caused a little profit-taking but was not enough to spook most buyers. Then a follow-up rebound has managed to lift offers at the recent top of 15910, prompting sellers to cover their positions and indicating that the recent whipsaws were merely a consolidation phase ahead of a bullish continuation. 16100 is the next level to clear before a test of the all-time high at 16300. On the downside, 15850 is the first support.

RBA Spiced Up This Morning’s Asian Session

Markets

European financial markets enjoyed a long weekend up until yesterday but Wall Street was open for business. The US during pre-market trading hours announced JPMorgan will take over First Republic Bank in an auction run by federal regulators. The troubled California-based bank brought back general bank sector nervousness ever since its quarterly results last week revealed a >$100bn depositor flight. The deal puts the unrest to bed just days ahead of the Fed policy meeting (Wednesday). US yields advanced in early dealings with an acceleration kicking in after the manufacturing ISM came in better than expected. The headline figure rose from 46.3 to 47.1 vs 46.8 anticipated. That’s still in contraction territory but the gauge not sliding any further is a preliminary positive sign. The recovery was broad-based across subseries. Most of them nevertheless stayed sub 50 except for prices paid (53.2) and employment (50.2). US rates at the end of the day sprinted between 12.9 and 15.1 bps higher with a minor underperformance at the belly of the curve. The 2y yield surpassed the 200dMA and in doing so created some distance with the 4% support area. The US dollar rallied against most of its peers. DXY (trade-weighted) closed near recent highs at around 102.15. EUR/USD slid towards the lower bound of the upward trading range around 1.097. US equities didn’t stray too far away. Major indices closed with negligible losses.

The RBA spiced up this morning’s Asian session by unexpectedly hiking policy rates to 3.85% (cfr. below) and keeping the door open for more as inflation remains way too high (7% y/y in Q1). Aussie yields and dollar surge. AUD/USD tries to recapture 0.67. Stocks in the Asian-Pacific region mostly gain with China outperforming. The RBA’s surprise adds to the FRB solution and the tentative bottoming out of the US manufacturing ISM. European inflation figures later today are to elongate the list of hawkish arguments for central banks to stay the tightening course, in this case for the ECB on Thursday. The April headline number is expected to come in at 6.9%, matching the March figure that was heavily impacted through base effects. A 0.7% monthly pace reveals expectations for a still very strong inflationary dynamic. Some countries last week showed national core inflation easing (eg. Belgium, Spain), leading consensus to lower their estimate for the European-wide figure to 5.6%. That would imply a marginal easing from the 5.7% seen in March. Even if that would materialize, it’s unlikely to sooth ECB governors. Apart from the April EMU CPI number, the ECB’s Q1 credit and lending survey will be released today. This survey is at least as important in making or breaking the case for another 50 bps rate hike. Given that markets currently discount no more than a 25 bps move, an above-consensus CPI and/or a resilient credit survey surely won’t go unnoticed.

News and views

The Reserve Bank of Australia (RBA) surprised markets by lifting its main policy rate by 25 bps to 3.85% following a pause last month. The central bank wanted some additional time to assess the state of the economy and the outlook. Australian inflation has passed its peak, but at 7% is still too high and it will be some time yet before it is back in the target range of 2-3%. RBA forecasts put inflation a 4.5% this year (from 4.75% in February) and 3% mid-2025. Especially services inflation and briskly rising unit labour costs are a cause of concern. The Australian labour market remains very tight with unemployment at a near 50-yr low (3.5%). The RBA remains alert to the risk that expectations of ongoing high inflation contribute to larger increases in both prices and wages, especially given the limited spare capacity in the economy and the historically low rate of unemployment. Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will depend upon how the economy and inflation evolve. Household spending is an RBA-worry which could prompt a new pause. Australian swap yield added 5.6 bps (30-yr) to 22.5 bps (2-yr) this morning. The Aussie dollar benefits from the unexpected yield support with AUD/USD rising from the low 0.66 area to above 0.67. For now, the YTD support are just below 0.66 survives.