Sample Category Title

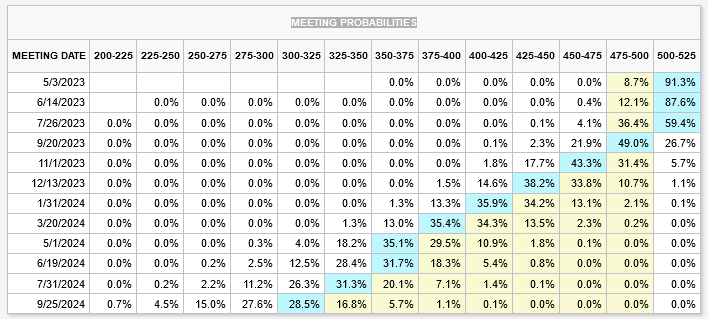

Fed to hike 25bps today, but pause afterwards?

Fed is widely anticipated to deliver another 25bps rate hike today, bringing federal funds rate target to 5.00-5.25%. Despite ongoing concerns over regional banks in the US, Fed appears unconcerned about overall financial stability. Service prices remain sticky, even as inflation appears to be declining.

With market pricing in near 90% chance of the 25 bps move, surprises seem unlikely. However, after this increase, fed fund futures indicate an almost 100% chance of no change in June, with the path beyond that trending downward. FedChair Jerome Powell may stay non-committal in the post-meeting press conference, and point to June's new economic projections for guidance. But a more explicit pause signal could boost risk markets.

Here are some readings on FOMC:

- Fed Hike, Then What?

- Will the Fed Hike Rates for the Last Time?

- Fed Preview: One More Hike – Cuts Still Far Away

- April Flashlight for the FOMC Blackout Period: Is the Tightening Cycle Coming to an End?

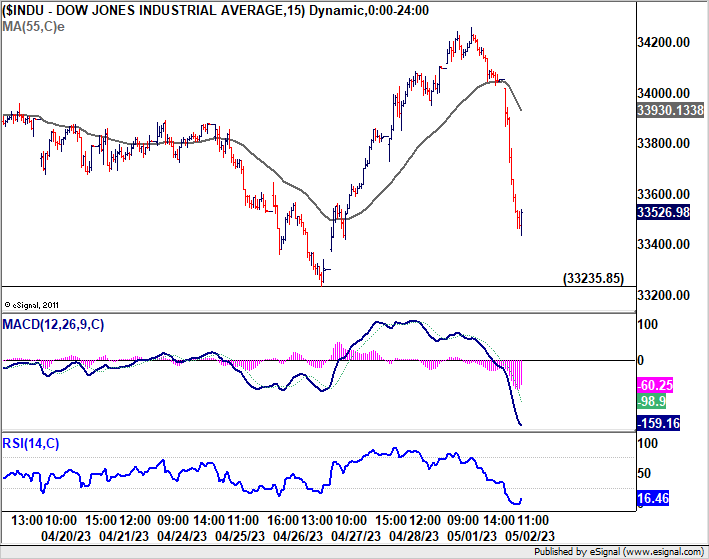

As for US stocks, despite initial selloff yesterday, major indexes recovered some ground and close down around -1% only. NASDAQ is still struggling to break through 12269.55 resistance. But near term bias will remain on the upside as long as 11798.77 support holds. The real test lies in 38.2% retracement of 16212.22 to 10102.61 at 12436.48. Decisive break there will be a solid bullish sign that should push for at least a test on 13181.08 cluster resistance. Nevertheless, firm break of 11798.77 support could prompt near term reversal, and steeper selloff back to 10982.80 support and possibly below.

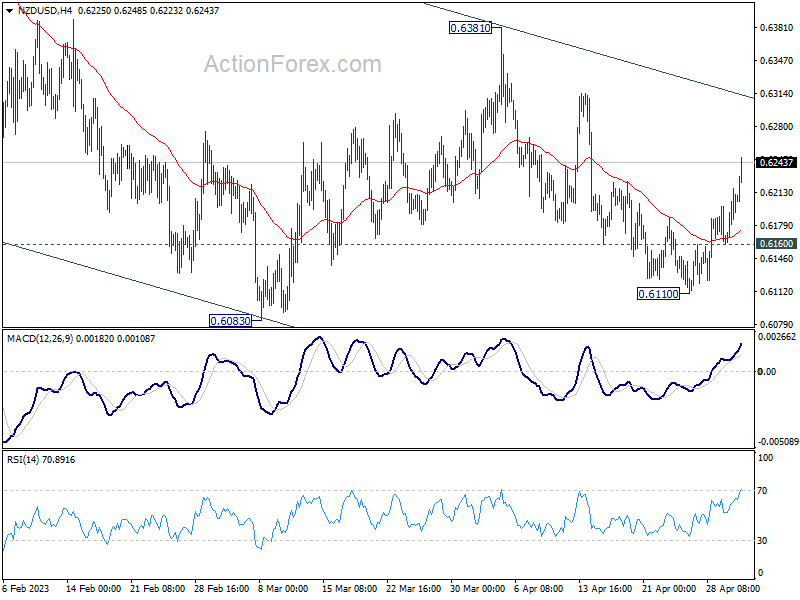

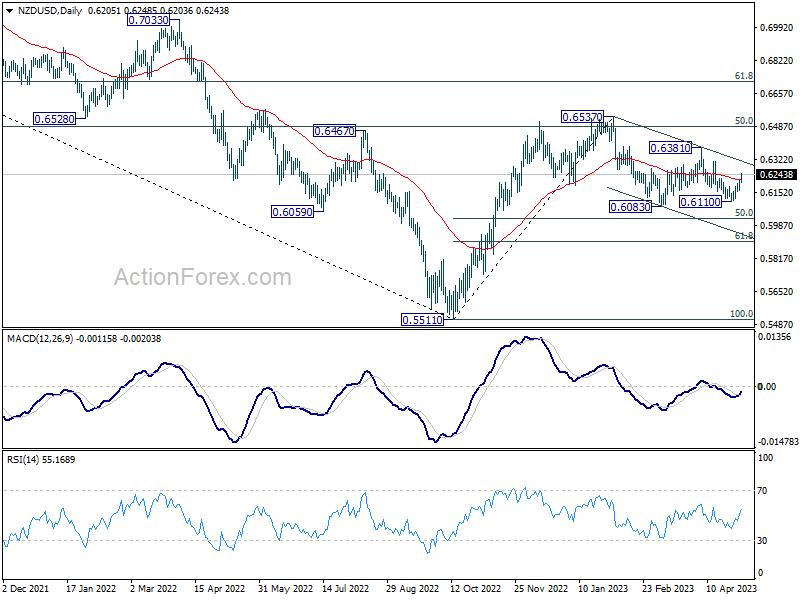

NZD/USD jumps as strong job data supports another RBNZ hike

New Zealand Dollar surges broadly today, as strong job growth data together with record annual wages growth basically seal the deal for another RBNZ rate hike on May 24.

Technically, NZD/USD's fall from 0.6381 should have completed at 0.6110 already, and further rise is now in favor back towards this resistance. The favored case is that current rise is merely the third leg of the sideway pattern from 0.6083. Outlook remains bearish as long as 0.6381 resistance holds, for resumption of the corrective decline from 0.6537 at a later stage. Break of 0.6160 minor support should bring deeper fall through 0.6083.

Nevertheless, firm break of 0.6381 will argue that the correction from 0.6537 has completed, and the whole rally from 0.5511 might then be ready to resume through 0.6537 high.

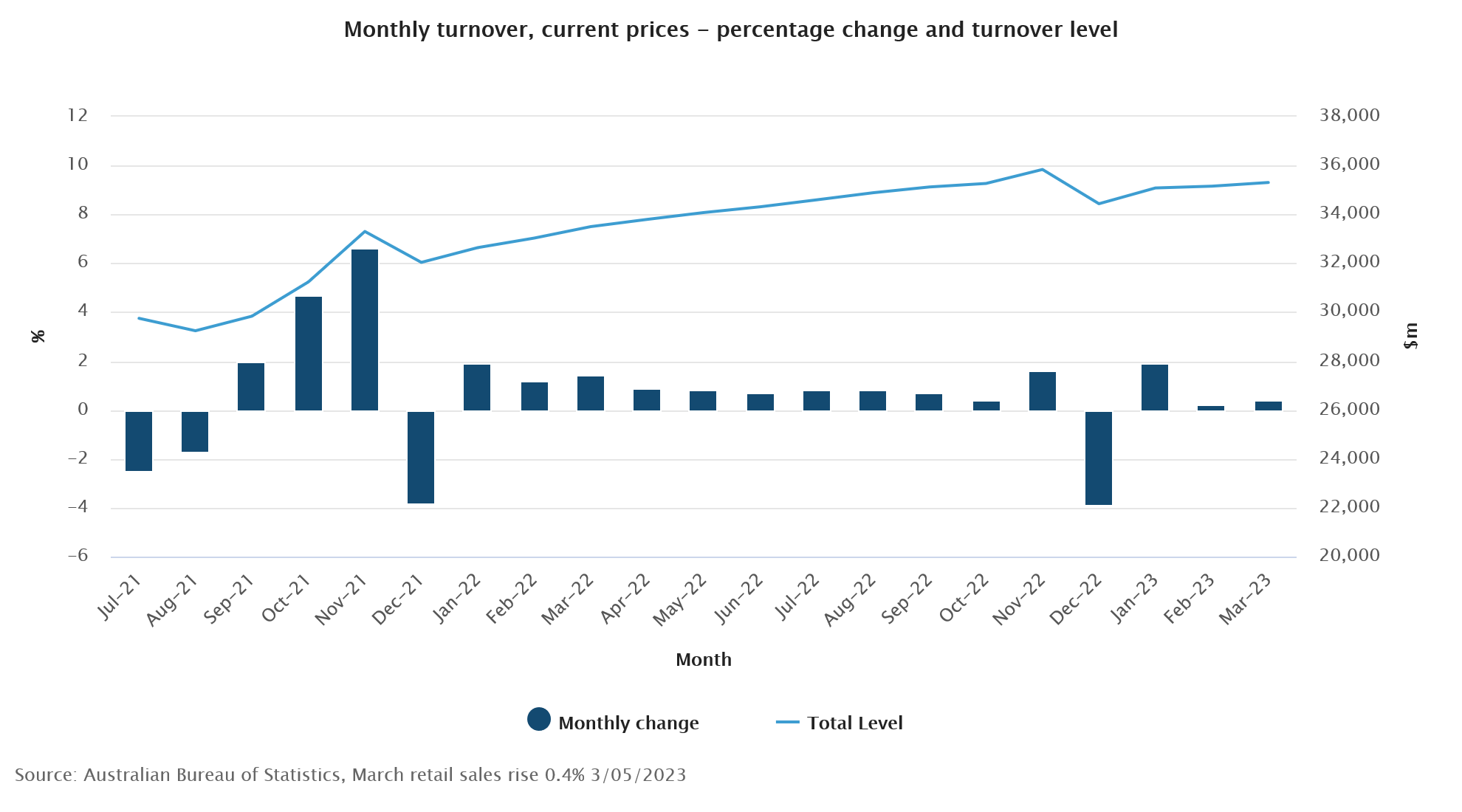

Australian retail sales exceed expectations, rising 0.4% mom in Mar

Australia's retail sales turnover increased by 0.4% mom to AUD 35.3m in March, surpassing expectations of 0.2% mom. Year-on-year, sales turnover was up by 5.4% compared to the same month a year ago.

Ben Dorber, Australian Bureau of Statistics Head of Retail Statistics, noted that while retail sales recorded a third consecutive rise in March, pull-back in spending on discretionary goods has kept monthly turnover at a similar level to six months ago.

Dorber also noted the importance of analyzing quarterly retail sales volumes, set to be released next week, in order to understand the impact of consumer prices on recent turnover growth, particularly as CPI data showed high inflation levels despite slower growth in March quarter.

Full Australia retail sales release here.

New Zealand’s financial system well-positioned for higher interest rate environment

In May 2023 Financial Stability Report, RBNZ Governor Adrian Orr highlighted that the country's financial system is well-placed to handle the higher interest rate environment and international financial disruptions. Global inflation continues to persist at levels significantly above central banks' policy targets. Although central banks have recently slowed pace of tightening, the full impact of previous tightening measures remains to be seen.

Governor Orr explained that "to date there have been limited signs of distress in banks' lending portfolios, with only a small share of borrowers falling behind on their payments." This resilience, he said, reflects ongoing strength of the labor market and the ability of borrowers to adjust their spending or use previous savings and repayment buffers.

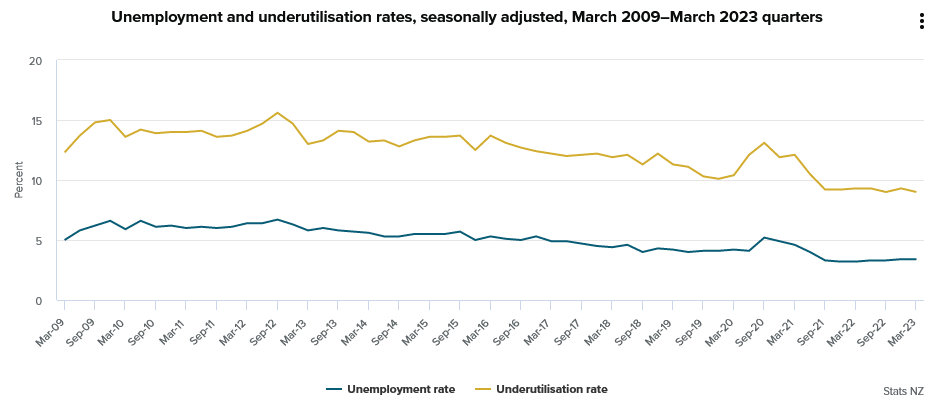

New Zealand employment growth exceeds expectations; unemployment rate remains low

New Zealand employment data for Q1 showcased a 0.8% qoq increase, surpassing expectation of 0.4% qoq growth. Unemployment rate remained steady at 3.4%, defying expectations of rise to 3.5% and staying close to record low of 3.2% made in Q1 2022. Additionally, employment rate climbed from 69.3% to 69.5%, while labor force participation rate rose from 71.8% to 72.0%. Both employment and participation rates reached their highest levels since records began in 1986.

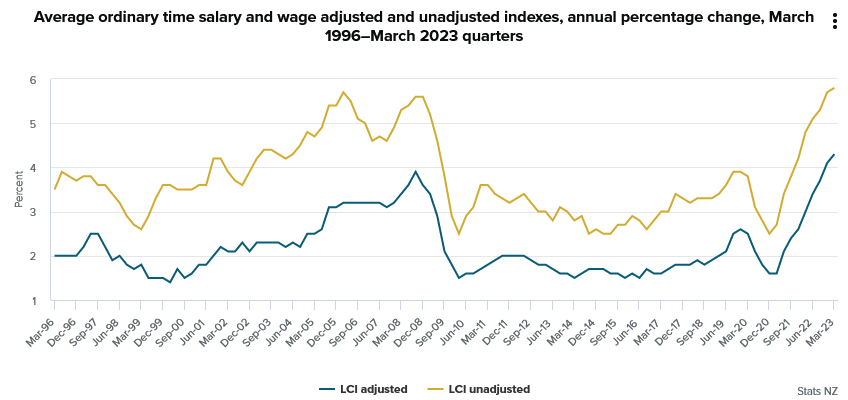

All sector wage inflation was at 1.0%, 4.3% yoy. "Annual wage cost inflation is at its highest level since the series began in 1992, up from 4.1 percent in the year to the December 2022 quarter," business prices manager Bryan Downes said. "This aligns with other wage measures, like the unadjusted LCI and average hourly earnings, both of which also had the largest annual increases on record."

First Impressions: NZ Labour Market March Quarter 2023

The New Zealand labour market remains hot, if past its peak. Unemployment held steady at 3.4% and annual wage growth continued to pick up.

March quarter 2023 labour market surveys

- Unemployment rate: 3.4% (prev: 3.4%, Westpac f/c: 3.4%)

- Employment change: +0.8% (prev: +0.5%, f/c: +0.8%)

- Labour costs (private, ordinary time): +1.0% (prev: 1.1%, f/c: 1.1%)

- Average hourly earnings (private, ordinary time): +1.9% (prev: 0.9%, f/c: 1.3%)

The unemployment rate held steady at 3.4% in the March quarter. That was in line with our forecast, and marginally stronger than the 3.5% that the market and the Reserve Bank were expecting. The number of people employed rose by 0.8%, also in line with our view (and the December quarter was revised up from 0.1% to 0.5%).

The growth in employment is in part being driven by the fact that there are more people around to hire. The resurgence of migrant inflows saw the working-age population rise by 0.5% over the March quarter, compared to zero growth a year ago.

Even so, employment is still outstripping population growth. The remainder was driven by attracting more people into the labour force – the participation rate rose from 71.7% to 72.0%, another new record high.

The wage measures were strong, but a mixed bag relative to forecasts. The Labour Cost Index rose by 1% for the quarter, a touch lower than the 1.1% rise last quarter. Private sector labour costs were up 0.9%, while the public sector was up 1.3% as collective pay agreements, particularly in healthcare, came into effect.

On an annual basis the LCI was up by 4.3%, compared to 4.1% last quarter. Wage growth tends to be one of the most lagging aspects to the economic cycle, so it’s not surprising that we’d see annual wage growth continuing to accelerate at this point even as consumer price inflation has clearly passed its peak.

The Quarterly Employment Survey (QES) measure of average hourly earnings rose by 1.9% for the quarter, with annual growth picking up from 7.4% to 7.6%. This measure is quite choppy from quarter to quarter, so we don’t put much weight on the fact that it was higher than what we had pencilled in. But it does highlight that what workers are receiving in hand is now keeping up with the rising cost of living.

Overall, the details of these surveys can be summed up by looking at the unemployment rate. The labour market is tight (3.4% is still very low compared to history), albeit past its hottest point (compared to the record low of 3.2% last year), and it isn’t deteriorating in any meaningful way yet. Wage pressures haven’t yet peaked on an annual basis, but are getting close to that point.

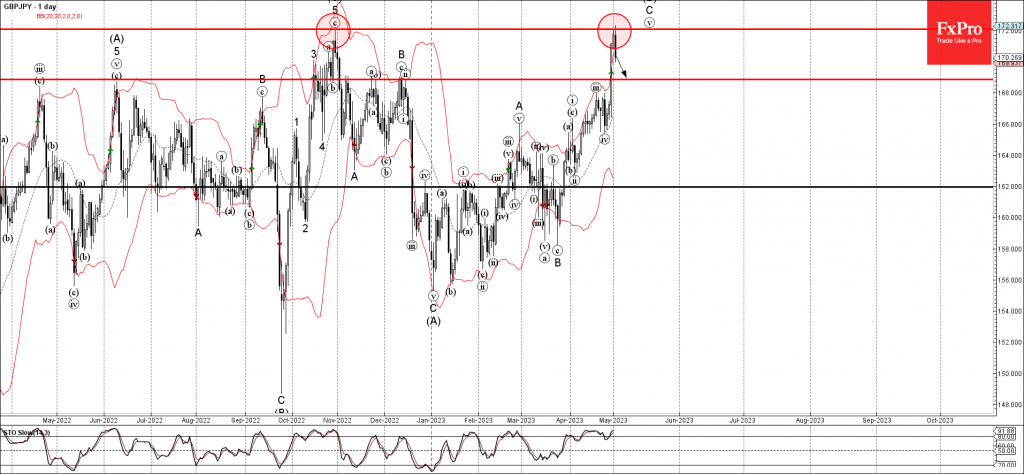

GBPJPY Wave Analysis

- GBPJPY reversed from long-term resistance level 172.00

- Likely to fall to support level 168.85

GBPJPY currency pair recently reversed down strongly from the long-term resistance level 172.00 (former multi-month high from October), standing above the upper daily Bollinger Band.

The downward reversal from the resistance level 172.00 stopped the previous short-term impulse waves 3 and (v) of wave C from March.

Given the overbought daily Stochastic, GBPJPY can be expected to fall further toward the next support level 168.85 (former resistance from November and December).

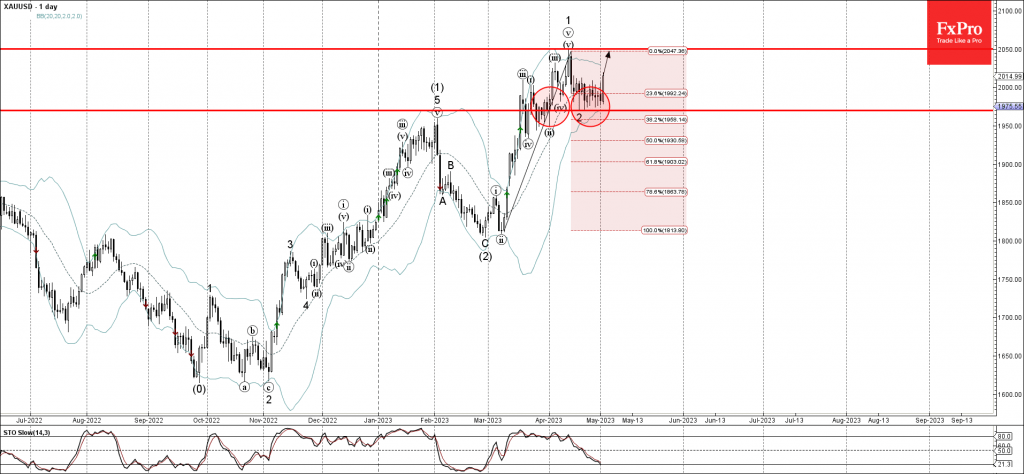

Gold Wave Analysis

- Gold reversed from key support level 1970.00

- Likely to rise to resistance level 2050.00

Gold earlier reversed up sharply from the key support level 1970.00, standing close to the 38.2% Fibonacci correction of the upward impulse from March.

The upward reversal from the support level 1970.00 started the active short-term impulse wave 3.

Given the clear daily uptrend, Gold can be expected to rise further toward the next resistance level 2050.00 (top of the previous impulse wave 1).

DOW down over 500 pts on debt ceiling and banking worries

Traders are growing increasingly cautious as US stocks open significantly lower today, with selloff gaining momentum throughout the early part of the session. At the time of writing, DOW is down by over -500 points. This decline appears to be a delayed response to Treasury Secretary Janet Yellen's warning that the department "will be unable to continue to satisfy all of the government's obligations" as early as June 1, unless Congress raises or suspends the debt limit beforehand. Yellen communicated this warning in a letter to House Speaker Kevin McCarthy. In addition, concerns surrounding regional banks persist, with major bank shares falling by more than -2.5%.

For now, DOW is still holding above near term structural support at 33233.85, which is close to 55 D EMA at 33351.58. The rise from 31429.82 is still intact for extending at a later stage through 34712.28 resistance. Nevertheless, break of 33233.85 will suggest that the corrective pattern from 34712.28 is extending with another falling leg before completion. Let's see if the deciding move would happen before or after FOMC rate announcement tomorrow.