Sample Category Title

Euro Shrugs CPI Release, Traders Turn Cautious Ahead of Key Events

Forex traders are probably starting to put up guards ahead of the key events in FOMC rate tomorrow, ECB on Thursday, and NFP on Friday. Australian Dollar remains the top performer today, bolstered by RBA's unexpected rate hike. However, there is no follow through buying after the initial spike. Meanwhile, Yen is attempting a recovery, though momentum appears weak. Sellers have shifted their attention to Canadian Dollar today, while European majors also show some weakness. Notably, Euro has shown no reaction to the released CPI data.

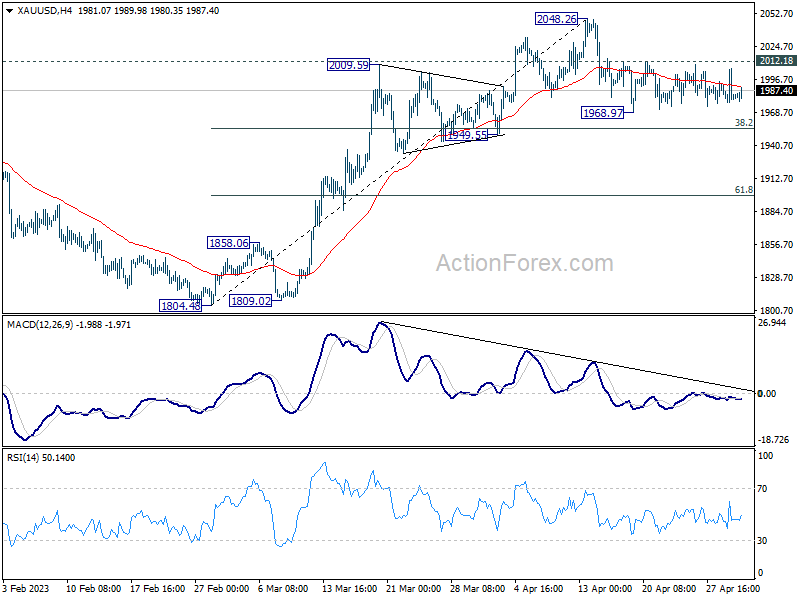

From a technical perspective, Gold will be in spotlight for the remainder of the week. The corrective pattern from 1968.97 implies that the pullback from 2048.26 is not yet complete. Downside breakout is mildly favored towards 1949.55 support zone (38.2% retracement of 1804.48 to 2048.26 at 1955.13). For now, robust support is expected in this area, which could lead to rebound. However, firm break of this support zone may trigger accelerated decline towards 61.8% retracement at 1897.60. If this scenario unfolds, it could coincide with a deeper correction in EUR/USD, pushing through 1.0908 support level .

In Europe, at the time of writing, FTSE is down -0.09%. DAX is down -0.33%. CAC is down -0.56%. Germany 10-year yield is up 0.0472 at 2.360. Earlier in Asia, Nikkei rose 0.12%. Hong Kong HSI rose 0.20%. China Shanghai SSE rose 1.14%. Singapore Strait Times rose 0.35%. Japan 10-year JGB yield rose 0.0201 to 0.423.

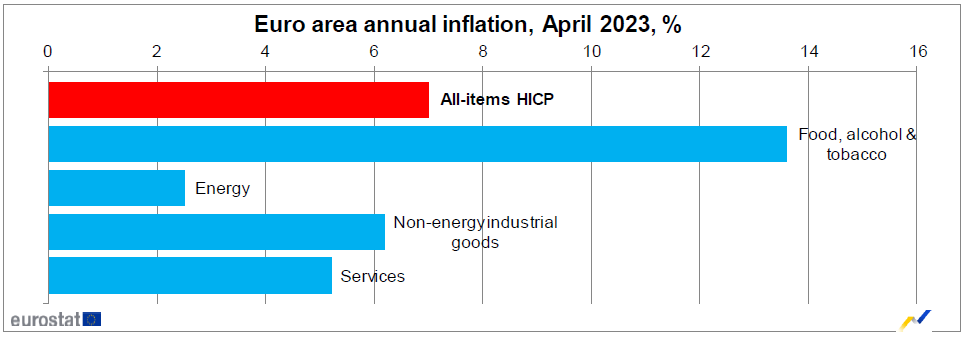

Eurozone CPI rose to 7.0% yoy in Apr, core CPI down to 5.6% yoy

Eurozone CPI accelerated from 6.9% yoy to 7.0% yoy in April, above expectation of 6.9% yoy. CPI core (all item excluding energy, food, alcohol & tobacco) slowed from 5.6% yoy to 5.7% yoy, below expectation of 5.7% yoy.

Looking at the main components, food, alcohol & tobacco is expected to have the highest annual rate in April (13.6%, compared with 15.5% in March), followed by non-energy industrial goods (6.2%, compared with 6.6% in March), services (5.2%, compared with 5.1% in March) and energy (2.5%, compared with -0.9% in March).

Eurozone PMI manufacturing finalized at 45.8, 35-month low

Eurozone PMI Manufacturing was finalized at 45.8 in April, a 35-month low. The index was also below the 50 no-change mark for a tenth straight month. PMI Manufacturing Output was finalized at 48.5, a 4-month low.

PMI Manufacturing of all major states declined in the month, and recorded contractionary reading except Greece (52.4). Ireland (48.6), France (45.6), the Netherlands (44.9), Germany (44.5) and Austria (42.0) were all at 35-month low. Spain was at 3-month low of 49.0 while Italy was at 6-month low at 46.8.

UK PMI manufacturing finalized at 47.8, remained in the doldrums

UK PMI Manufacturing was finalized at 47.8 in April, slightly down from March's 47.9. Output, new orders, employment and stocks of purchases all contracted and vendor lead times improved (a sign of weaker demand for inputs hurting suppliers).

Rob Dobson, Director at S&P Global Market Intelligence, said: "The UK manufacturing sector remained in the doldrums at the start of the second quarter. Output and new orders contracted, as manufacturers felt the impacts of client uncertainty, destocking and tightening cost controls. There was no escape from the subdued mood of the market, with both domestic and export customers remaining reticent to commit to new contracts."

RBA Lowe: The board is not on pre-set course

RBA Governor Philip Lowe reiterated in a speech that after today's 25bps rate hike, "some further tightening of monetary policy may be required". But he added the decision will "depend upon how the economy and inflation evolve", and the central bank is "not on a pre-set course". The Board will pay close attention to developments in the global economy, household spending, inflation and labor market outlook.

Lowe also explained today's decision, and noted that while there was "confirmation" that inflation has peaked, " it will be some time yet before inflation is back in the target range." Labor market is "still very tight" and service inflation is "uncomfortably persistent abroad".

He warned, "if people think inflation is going to remain high then, understandably, they will adjust their behaviour." Firms will be more willing to put up their prices and workers will seek larger pay rises. If this adjustment in expectations were to happen, high inflation would become entrenched and the end result would be even higher interest rates and a poorer outlook for jobs.

RBA defies expectations with rate hike, may still require further tightening

In a surprising move, RBA raises cash rate target by 25bps to 3.85%, contrary to market expectations of a hold. Nevertheless, RBA softened its tightening bias, stating, "some further tightening of monetary policy may be required," depending on "how the economy and inflation evolve."

Despite acknowledging that Australian inflation "has passed its peak" and "recent data showed a welcome decline," the central bank still expects inflation to be at 4.25%, slowing to 3% in mid-2025. That is, "it takes a couple of years before inflation returns to the top of the target range". RBA added that services price inflation remains "still very high and broadly based" with upside risks, while goods inflation is decelerating.

RBA projects the economy to grow by 1.25% in 2023 and around 2% over the year to mid-2025. With anticipated below-trend economic growth, unemployment rate is forecast to gradually increase to around 4.5% in mid-2025.

RBNZ Hawkesby: Not currently seeing widespread financial distress amongst households or businesses

According to RBNZ Financial Stability Report, debt servicing costs for households with mortgages are expected to more than double by the end of the year. Despite this, household balance sheets remain resilient, with most having substantial equity buffers. Early-stage arrears have increased but remain low compared to post-Global Financial Crisis levels. Banks' strong capital positions allow them to support customers, and borrowers facing stress are encouraged to seek assistance from their banks.

"We are not currently seeing widespread financial distress amongst households or businesses, which reflects the strength in the economy and labour market to date. However, more borrowers may fall behind on their payments this year, given the ongoing repricing of mortgages and expected weakening in the labour market,"Deputy Governor Christian Hawkesby says.

"Recent profitability and strong capital positions puts banks in a good position to take a long-term view and support their customers. We encourage borrowers encountering stress to talk to their banks, as hardship programmes may be available, and some customers may be able to temporarily switch to interest-only payments or increase the remaining term of their loan."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0949; (P) 1.0992; (R1) 1.1021; More...

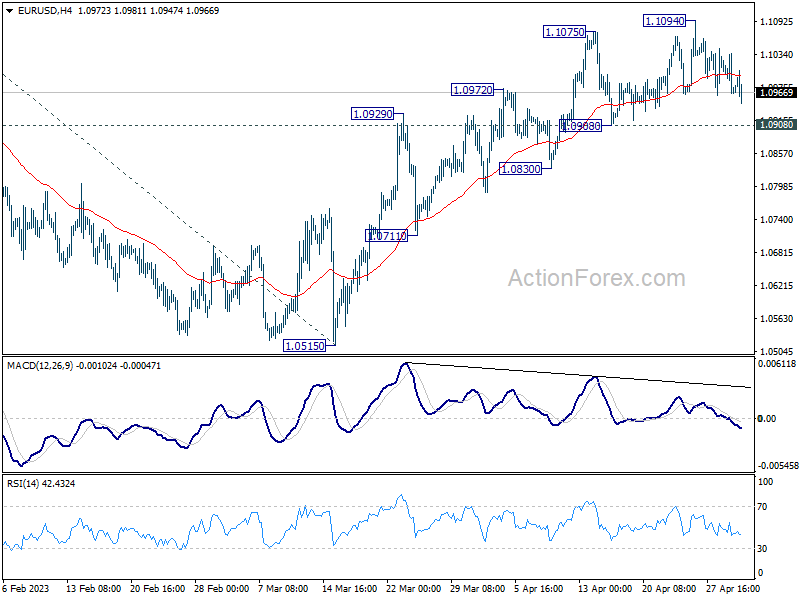

EUR/USD is staying in sideway consolidation below 1.1094 and intraday bias remains neutral. Further rally is expected as long as 1.0908 support holds. Break of 1.1094 will resume larger up trend to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441 However, considering bearish divergence condition in 4H MACD, break of 1.0908 support will indicate short term topping and turn bias back to the downside.

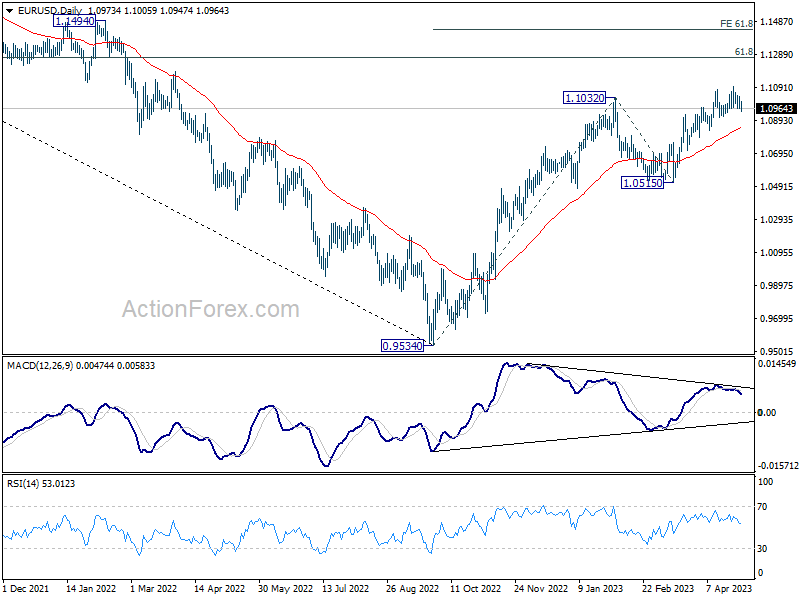

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Apr | -1.70% | -1.50% | -1.00% | |

| 04:30 | AUD | RBA Interest Rate Decision | 3.85% | 3.60% | 3.60% | |

| 06:00 | EUR | Germany Retail Sales M/M Mar | -2.40% | 0.40% | -1.30% | |

| 07:00 | CHF | SECO Consumer Climate Q2 | -30 | -22 | -30 | |

| 07:30 | CHF | Manufacturing PMI Apr | 45.3 | 50 | 47 | |

| 07:45 | EUR | Italy Manufacturing PMI Apr | 46.8 | 49 | 51.1 | |

| 07:50 | EUR | France Manufacturing PMI Apr F | 45.6 | 45.5 | 45.5 | |

| 07:55 | EUR | Germany Manufacturing PMI Apr F | 44.5 | 44 | 44 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr F | 45.8 | 45.5 | 45.5 | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | 2.50% | 3.10% | 2.90% | |

| 08:30 | GBP | Manufacturing PMI Apr F | 47.8 | 46.6 | 46.6 | |

| 09:00 | EUR | Eurozone CPI Y/Y Apr P | 7.00% | 6.90% | 6.90% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr P | 5.60% | 5.70% | 5.70% | |

| 14:00 | USD | Factory Orders M/M Mar | 0.80% | -0.70% |

EUR/USD Shrugs as Eurozone Inflation Steady

- Eurozone inflation almost unchanged

- German retail sales fall by 2.5%

- Markets upwardly revise odds of Fed hike to 96%

EUR/USD is trading quietly at 1.0966, down 0.09%.

German retail sales fall by 2.5%

The German consumer continues to hold tight to the purse strings, as March retail sales declined by 2.4%, compared to a consensus of 0.4% and -1.3% in February. This marked the fourth decline in five months. On an annualized basis, retail sales plunged by 8.6%, lower than the consensus of -6.1% and the February read of -7.1%. The numbers are not pretty any way you slice them, and the German recovery will be slow if consumer spending does not rebound. Germany’s manufacturing PMI remained in contraction mode in March with a reading of 44.5, above the consensus of 44.0 but lower than the February reading of 44.7.

Eurozone inflation shows little change

The ECB meets on Thursday and is expected to raise rates by 25 basis points, but there is an outside chance of a second-straight 50-bp hike. Today’s release of eurozone CPI for April was hotly anticipated but showed little change and won’t be a factor in the ECB decision. Headline CPI ticked higher to 7.0%, compared to 6.9% in March, which was also the consensus. Core CPI nudged lower to 5.6%, compared to 5.7% in March and the consensus of 5.6%. The central bank is determined to put the inflation genie back in the bottle, but another 50-bp hike would raise the danger of the economy cooling down too quickly and tipping into recession.

The Federal Reserve holds its meeting on Wednesday and market pricing of a 25-basis point hike has jumped to 96%, up from 75% just a week ago. Economic activity has cooled, as evident in Q4 GDP which slowed to 1.1%, but the Fed wants to see inflation, in particular the core rate, fall more quickly.

EUR/USD Technical

- EUR/USD is testing support at 1.0967. Below, there is support at 1.0893

- There is resistance at 1.1088 and 1.1157

RBA Lowe: The board is not on pre-set course

RBA Governor Philip Lowe reiterated in a speech that after today's 25bps rate hike, "some further tightening of monetary policy may be required". But he added the decision will "depend upon how the economy and inflation evolve", and the central bank is "not on a pre-set course". The Board will pay close attention to developments in the global economy, household spending, inflation and labor market outlook.

Lowe also explained today's decision, and noted that while there was "confirmation" that inflation has peaked, " it will be some time yet before inflation is back in the target range." Labor market is "still very tight" and service inflation is "uncomfortably persistent abroad".

He warned, "if people think inflation is going to remain high then, understandably, they will adjust their behaviour." Firms will be more willing to put up their prices and workers will seek larger pay rises. If this adjustment in expectations were to happen, high inflation would become entrenched and the end result would be even higher interest rates and a poorer outlook for jobs.

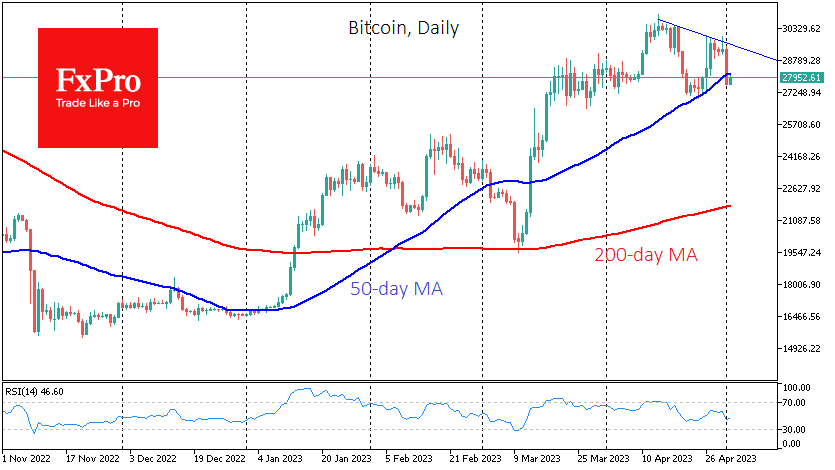

Bitcoin’s Dangerous Fall

Market picture

Bitcoin fell all day yesterday, losing around 6% to $27.6K, raising the question of whether we are seeing the start of a prolonged decline.

Bitcoin closed below its 50-day moving average on Monday. The price stays below that curve and is stuck at $28.0K after rising 1.3% to today. If it can’t quickly surpass it again, Bitcoin’s fall below $27K will pave the way for a move to $22K, where the 200-day passes, which became a turning point in March.

Twitter analyst Bluntz, who predicted a bear market bottom for BTC in 2018, expects Bitcoin to fall to $25K. In his view, the first cryptocurrency is unlikely to break $30,000 soon. BTC has completed a 5-wave and is now in a corrective A-B-C formation.

News background

Cryptocurrencies will outperform other asset classes amid the continued devaluation of fiat currencies and the ongoing banking crisis, Real Vision CEO Raul Pal said following the bankruptcy of First Republic Bank (FRB).

Peter Brandt, tech analyst and head of Factor LLC, believes Bitcoin will soon overtake all other cryptocurrencies and “bury all the imposters”. He pointed to the chart of the BTC dominance index, which he believes is poised for a breakout after two years of consolidation.

According to Santiment’s research, crypto asset prices in April were “very broadly dispersed” and barely correlated with each other.

Investors Cautious Ahead of Fed and ECB Later in the Week

Investors appear to be treading carefully ahead of some key interest rate announcements this week, most notably the Fed on Wednesday but also the ECB one day later.

Eurozone inflation data for April didn't throw up any nasty surprises a couple of days before the central bank makes its decision, rising slightly to 7% as expected, while core stayed stubbornly high at 5.6%. A 25 basis point rate hike is now heavily backed with one or two more to come over the following months.

RBA may not be done with rate hikes despite brief pause

The RBA surprised markets by hiking the cash rate by 25 basis points to 3.85%. The move came after the central bank paused its tightening cycle at the previous meeting and inflationary pressures appeared to have eased slightly. That wasn't enough to put minds at ease though and the RBA warned further hikes may be necessary.

Even with the latest hike, the central bank believes it will take a couple of years to return inflation to its 2-3% target, with low unemployment and the prospect of sustained higher wage and price pressures outweighing the benefits of keeping the cash rate at 3.6%. The Aussie dollar spiked after the announcement and markets are pricing in a 50% chance of another hike at one of the upcoming meetings.

HSBC looks to return cash to shareholders as it benefits from higher interest rates

HSBC shares are up more than 5% on Tuesday after the company announced strong first-quarter earnings - boosted by the purchase of SVB UK - a $2 billion share buyback, and the resumption of quarterly dividends. The results were driven by higher interest rates which lifted its net interest margin, something the bank is particularly sensitive to. All things considered, it was a good quarter for HSBC but with favourable one-off events boosting its profitability, there remains a lot of work to do to win over some shareholders.

More backlash as BP reports strong profits in Q1

BP reported bumper profits again in the last quarter, buoyed once more by higher oil and gas prices, albeit to a much lesser extent than we were seeing last year. Profits overall have come down quite a lot from last year's peaks but at £4 billion for the first quarter remain extremely healthy. While the results will draw more criticism around excess profits on the back of the war in Ukraine and further calls for higher tax rates as households continue to pay sky-high energy bills, the only thing they seem to ensure for now is more share buybacks and higher dividend payments.

Were fears of Oil deficit premature?

Oil prices appear to have stabilized in recent days, not far from the middle of the range they traded within from early December to March. The post-OEPC+ gains have now been wiped out which suggests traders are now of the belief that the economic outlook has deteriorated to the extent that the output cut won't create the deficit that was feared when some were calling for $100 oil. Of course, a lot can change over the coming weeks and months and almost certainly will but for now, it seems the outlook for oil prices is as it was.

Gold consolidates ahead of FOMC decision

Gold has gone into consolidation in the run-up to tomorrow's FOMC decision as traders await the latest views from the central bank in light of recent data and the fallout from the mini-banking crisis. Markets suggest a 25 basis point hike is locked in and while that could arguably prove to be a mistake, it looks the easiest option at this stage.

What messaging accompanies the rate hike will determine whether we could see a move back above $2,000 and a run at record highs around $2,070. The Fed must be concerned about the tightening of credit conditions in the aftermath of the collapse of three banks but it clearly doesn't want to soften its rhetoric until it has to. The result could be a sharp, sudden pivot from a policy perspective over the coming months but as far as tomorrow is concerned, a "wait-and-see" or "meeting-by-meeting" approach may be preferred. Whether that will be perceived to be dovish enough, we'll have to wait and see.

Is Bitcoin set to give back some of its incredible 2023 gains?

Bitcoin appeared to be finding some form again late last week but a more than 6% decline on Monday followed days of it hitting resistance around $30,000. Whether that will be sufficient to trouble those that were hopeful that a sustained recovery is underway isn't clear but a break below $27,000 could spell trouble in the short-term.

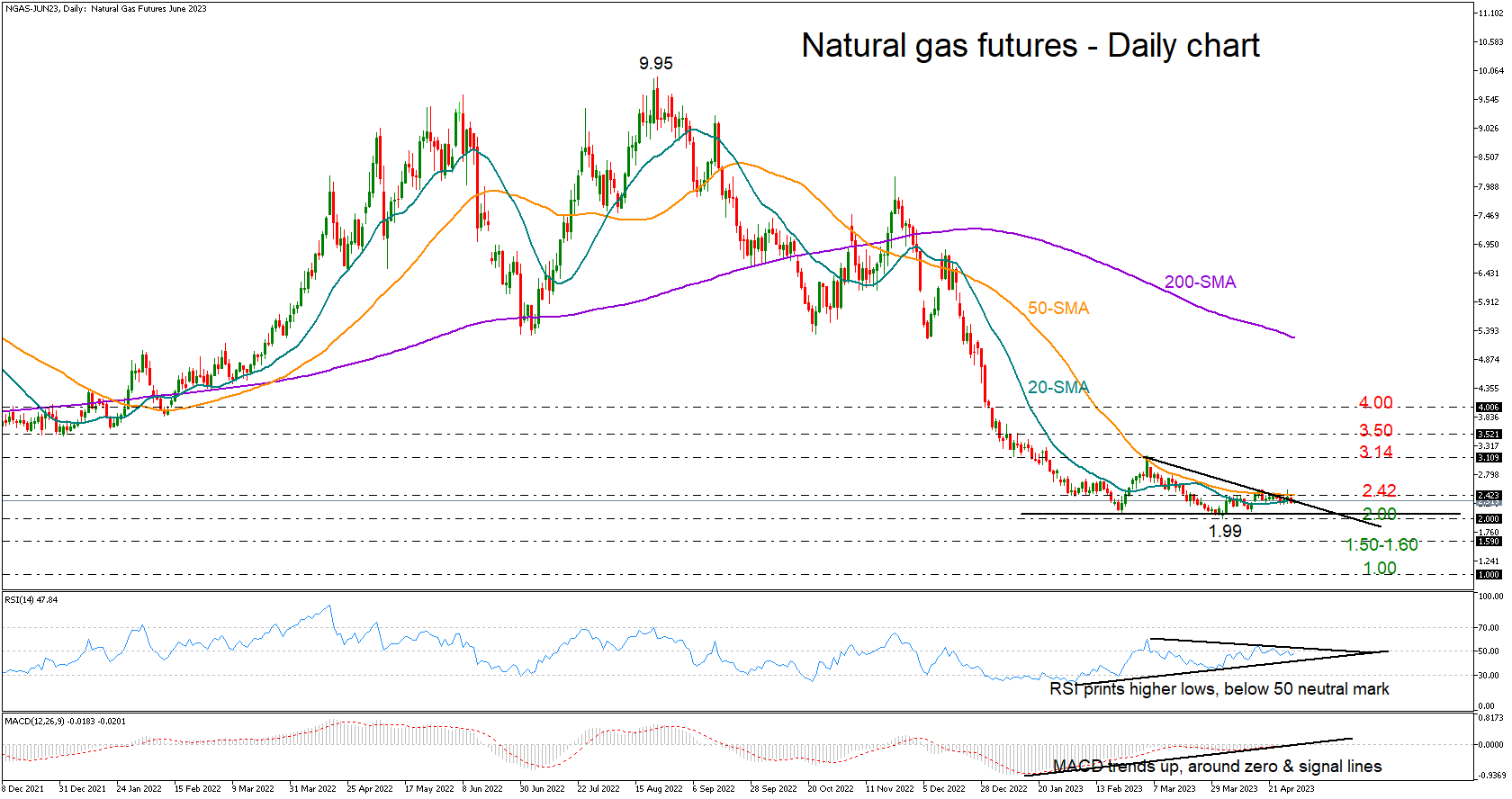

Are Natural Gas Futures Set for a Bullish Reversal?

Natural gas futures (June delivery) have been range bound over the past two months, consolidating the downtrend from August’s highs near the 2.00 round level.

The sideways move is developing within a descending triangle and at the bottom of a downtrend, which is technically an ideal setup for a bullish trend reversal. Meanwhile, the RSI and the MACD have been making higher lows during the same period, reflecting fading selling forces too.

Still, buyers may remain patient until the price successfully exits the triangle on the upside through the 2.42 level. The 50-day simple moving average (SMA) is currently flattening in the same region, while slightly lower, the 20-day SMA is adding a strong footing under the price. Should the price find enough support to run above the triangle, the spotlight will immediately turn to the previous high of 3.14, a break of which is needed to confirm an actual bullish trend reversal. Another successful battle here may produce a new leg up to 3.50, while a faster increase could target the 4.00 psychological mark.

In the bearish scenario, where the sell-off worsens below the triangle and the 2.00 number, the price may depreciate towards the 2016 and 2020 floor of 1.60-1.50. Even lower, the bears would aim for the crucial 1.00 level.

In brief, natural gas futures seem to be trading within a bullish formation that may provide a foundation for a bullish trend reversal. A break above 2.42 could boost buying appetite, though only a decisive extension above 3.14 would mark a new higher high in the short-term picture.

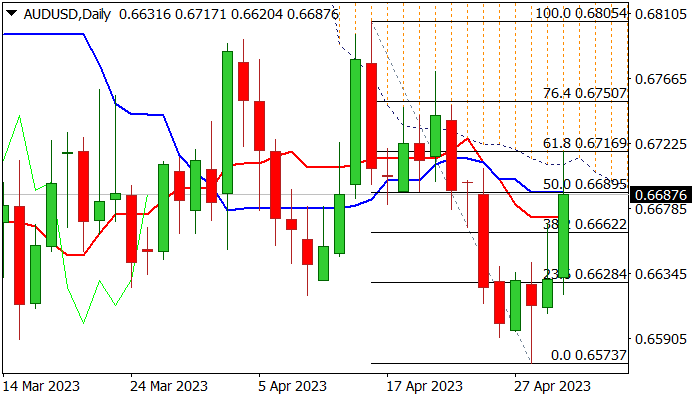

Aussie Soars after RBA Shocks with 25-bp Hike

- RBA unexpectedly raises rates by 25 bp

- AUD/USD jumps 1%

- Federal Reserve widely expected to follow with 25 bp hike

The Australian dollar has racked up sharp gains today. In the European session, AUD/USD is trading at 0.6691, up 0.93%.

RBA surprises with 25 bp hike, Aussie surges

The Reserve Bank of Australia has a knack for surprising the markets, and today’s rate hike certainly qualified. The markets had widely expected that the RBA would pause rates for a second straight month, but the central bank defied expectations and delivered a 25-basis point hike. This brought the benchmark cash rate to 3.85%. The Australian dollar surged by 0.95% in response to the move.

RBA Governor Lowe defended the hike in his rate statement, saying that inflation “at 7% is still too high” and that a rate increase is needed in order to bring inflation back down to the target of 2%. The decision to raise rates was made despite last week’s inflation release, which showed inflation fell from 7.8% to 7.0% in the first quarter. The robust labour market and the sharp increase in immigration were factors in favor of a hike that the RBA took into account.

The rate hike is not only adding to the misery of households who have mortgage payments but is also raising concerns that the RBA may end up over-tightening and the economy could have a hard landing. The RBA was heavily criticised for allowing inflation to climb out of control and policy makers may be gun shy about ending the current rate cycle while inflation is so high.

The Federal Reserve holds its meeting on Wednesday and market pricing of a 25-basis point hike has jumped to 96%, up from 75% just a week ago. Unlike the RBA decision, I don’t expect the Fed to defy expectations and take a pause at tomorrow’s meeting. The RBA hike raised concerns about a hard landing, and we are hearing similar concerns that another Fed hike will raise the likelihood of the US economy tipping into recession.

AUD/USD Technical

- AUD/USD has pushed past resistance at 0.6632 and tested resistance at 0.6690 earlier. Above, there is resistance at 0.6896

- 0.6558 and 0.6500 are providing support

AUD/USD: Aussie Dollar Rallies on Unexpected RBA Rate Hike

Australian dollar rose over 1% on Tuesday, lifted by unexpected 25 basis points rate hike by the Reserve Bank of Australia and hawkish stance which signals that more hikes could be expected, in efforts to curb persistently high inflation.

Aussie dollar jumped to the highest since Apr 21, retracing 61.8% of 0.6805/0.6573 bear-leg and sidelining risk of retesting key support at 0.6563 (2023 low posted on Mar 10).

Daily technical studies improved on the latest rally as 14-d momentum is breaking into positive territory and RSI/Stochastic are in steep ascend, however bulls face headwinds from the base of very thick daily cloud (spanned between 0.6708 and 0.6860), as the action cracked cloud base but quickly returned, with daily Tenkan-sen/Kijun-sen still in bearish setup and adding to warning signals.

Firm break of cloud base and nearby Fibo 61.8% of .6805/0.6573 (0.6716) is needed to keep bulls intact for further advance.

Failure under cloud base will signal consolidation, with bullish bias expected while the price stays above 0.6662 (10DMA/broken Fibo 38.2%).

Loss of 0.6662 pivot would initial signal recovery stall and make the downside more vulnerable.

Res: 0.6708; 0.6716; 0.6750; 0.6805.

Sup: 0.6672; 0.6662; 0.6628; 0.6591.

Eurozone CPI rose to 7.0% yoy in Apr, core CPI down to 5.6% yoy

Eurozone CPI accelerated from 6.9% yoy to 7.0% yoy in April, above expectation of 6.9% yoy. CPI core (all item excluding energy, food, alcohol & tobacco) slowed from 5.7% yoy to 5.6% yoy, below expectation of 5.7% yoy.

Looking at the main components, food, alcohol & tobacco is expected to have the highest annual rate in April (13.6%, compared with 15.5% in March), followed by non-energy industrial goods (6.2%, compared with 6.6% in March), services (5.2%, compared with 5.1% in March) and energy (2.5%, compared with -0.9% in March).

Unexpected Interest Rate Hike In Australia Strengthens AUD

According to Reuters, market participants were waiting for a pause in a series of interest rate hikes, as the data showed a slowdown in inflation. However, the Reserve Bank of Australia on Tuesday raised the rate by 25 basis points.

"Inflation in Australia has passed its peak, but at 7 percent is still too high and it will be some time yet before it is back in the target range," said governor Philip Lowe.

As a result, the Australian dollar jumped by about 1% against major currencies. It's a tumultuous start to the week after May 1, which was a public holiday for the financial industry in many countries. Note that news from the Reserve Bank of New Zealand, as well as from the Fed, is expected tomorrow.

Meanwhile, the daily chart of AUDUSD shows a promising bullish pattern — a false bearish breakdown (1) of the lower border of the rising channel. In the most favorable scenario for the bulls, the rate may continue to rise towards a (3) year high, however (2) resistance at 0.678 is on the way — it will help to reveal how strong the demand in the AUDUSD market is really strong.