Sample Category Title

Cliff Notes: RBA to Hold and FOMC to Hike

Key insights from the week that was.

Recent developments have led us to change our view on the RBA and FOMC ahead of their respectively policy meetings next week.

The Australian Q1 CPI report delivered a downside surprise on underlying inflation, the trimmed mean measure print of 1.2% (6.6%yr) well below the market’s expectation and our own. This was largely associated with a broad-based step-down in the pace of goods inflation, from 9.5%yr to 7.6%yr, with softness emerging more clearly, particularly across food, recreation, clothing/footwear and household contents. While annual services inflation recorded a large increase (6.1%yr from 5.5%yr) due to a surge in health care costs and housing utilities – components which were likely ‘trimmed’ out of the underlying measure – the easing in annual headline inflation, according to the RBA’s February forecasts, is running ahead of expectations.

Given these developments, as discussed by Chief Economist Bill Evans, we now expect that the RBA will extend their policy pause in May, keeping the cash rate at 3.60%, a level which we now believe will prove the peak for this tightening cycle. With inflation set to remain in a clear down-trend and slack to emerge in the labour market over coming months, we anticipate that the scope for further interest rate increases will fade in time. Nevertheless, a tightening bias from the Board is to be expected near-term given inflation is still elevated and the labour market historically tight.

Offshore, the week also began quietly, with the US’ regional Fed surveys and housing partials the only data of note. All but one of the regional surveys showed a marked deterioration in activity and sentiment for US business in April. These outcomes were corroborated by a downside surprise for core durable orders and shipments which declined for a second consecutive month in March. Taken together, these outcomes point to business rapidly shifting to a defensive posture. We expect this trend to persist and result in a further marked deceleration in job creation and wage growth through 2023 as well as continued weakness in business investment.

While consumption showed strength in Q1, rising 3.7% annualised versus GDP’s 1.1% overall gain, the detail of the GDP report and monthly PCE data makes clear that this momentum was highly concentrated in durables spending and was front-loaded in January. February subsequently saw a marginal decline and, assuming an unrevised February outcome, the Q1 outcome points to another small decline in the month of March. More broadly, the deceleration evident for employment and wage growth, sub-par consumer confidence and challenging housing affordability all speak to a lengthy period of weakness in consumption. It is unsurprising then that businesses stopped accruing inventory in Q1. The potential for inventory stocks to be sold down will linger as a downside risk to growth through the remainder of 2023.

Increasingly then it seems likely that the contraction in GDP we have been forecasting for the second half of 2023 will meet the broader NBER definition of recession. Moreover, risks to the recovery are skewing sharply to the downside given the weakened state of the US banking sector and the clear need for regulatory reform to increase oversight of smaller banks. While FOMC member communication ahead of the pre-meeting blackout suggests members see a need to take out a little more insurance against inflation risks in the near term, one more 25bp hike is now expected at their May meeting, the remainder of the year is expected to show a US economy under significant stress, with growing downside risks. As a result, we expect this last hike to be taken back in December and, with inflation around target on an annualised based by December, a further 200bps of cuts through 2024. Our end-2024 forecast for the fed funds rate is consequently unchanged at 2.875%.

Weekly Focus – All Eyes on Big Central Banks

The markets are tuning in for a very exciting central bank week. Both the Fed and the ECB continue their tightrope walking, weighing stubborn inflation against rising financial stability risks. This week provided a sharp reminder of the latter, as the share price for First Republic bank plunged to record lows after their Q1 earnings report showed depositors had withdrawn more than USD 100bn. Maintaining the balance of central bank concerns, though, German public sector reached a wage agreement where the average increase is estimated at a whopping 11.5% over the next two years.

In the context of persistent core price pressures and in the absence of a systemic crisis, we keep our central bank calls unchanged and expect the Fed to deliver their final 25bp hike, see Fed preview: One more hike - cuts still far away, 27 April. Powell is unlikely to close the door for further hikes, but even with nominal rates on hold, we expect the monetary policy stance to continue tightening towards H2 as lower inflation expectations drive higher real rates. The JOLTS jobs openings will be released just ahead of the FOMC and it will be interesting to see whether labour demand has continued to ease. As we have highlighted before, recent job gains have been more driven by a recovery in labour supply, not by a further uptick in demand. We get a fresh snapshot on Friday when the US jobs report for April is released. Our call is for a slightly moderating but still solid jobs growth of 200k.

The ECB on Thursday is likely to deliver a 50bp hike unless bank lending survey and loan growth data due on Tuesday change the picture dramatically, see ECB Preview - The art of compromise, 27 April. We believe it will be a compromise deal with no specific forward guidance (nor guidance on balance sheet normalisation in H2 yet), but repeating a data-dependent approach to future policy decisions.

Not that big central banks would take their cues from the little ones, but this week, Riksbank opted for a cautious approach, and while hiking by 50bp as expected, signalled a softer rate path going forward. The dovish surprise sent the krona sharply weaker and has left EUR/SEK hovering around 11.40 level (our 12M forecast). For now, we keep our call for another 50bp hike in June but recognise that risks are tilted towards a smaller hike, including the possibility of extending the hiking cycle into September, see Flash comment Riksbank - Dovish hike, 26 April. The Bank of Japan, in turn, kept its yield curve control policy unchanged as expected. We continue to expect BoJ to loosen the grip on the yield curve at the June or July meeting.

Next week, we expect the Chinese PMIs for April to paint a mixed picture with a recovery in Caixin manufacturing after the big drop in March, while the official PMI is likely to correct lower after reaching a very high level in March. The convergence in the two is in line with our view of a recovery in the Chinese economy. Note that as a result from a very strong Q1 performance, we have raised our growth forecast and now expect the Chinese GDP to expand by 6.2% in 2023 (prev. 5.5%). Our estimate for 2024 is lowered to 5.0% from 5.2%. Read more on China Macro Monitor - 2023 growth revised up to 6.2%, 24 April.

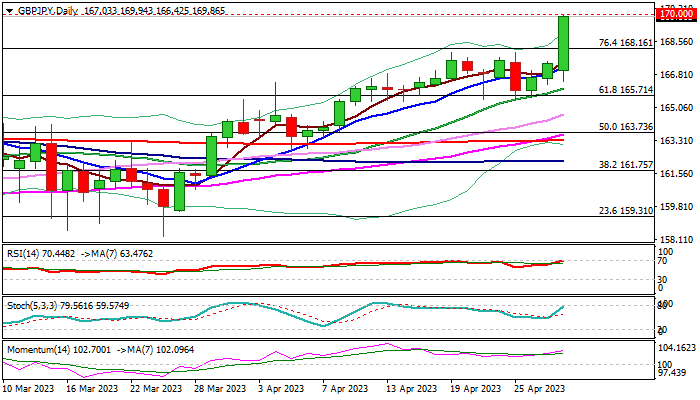

GBP/JPY: Rises to New 2023 Peak in Post-BOJ Acceleration

The GBPJPY cross surged to five-month high (also new 2023 peak), advancing 1.6% until early US session on Friday, as yen was sold across the board after the Bank of Japan kept firm dovish stance.

The biggest daily gains since Jan 4 surged through Fibo barrier at 168.16 (76.4% retracement of 172.11/155.35) and broke former tops of Nov 23 / Dec 13 at 169.00/169.27 respectively, pressuring psychological 170 level.

This marks the last obstacle en-route to key resistance at 172.11 (peak of Oct 31, the highest Feb 2016).

Larger bulls are likely to take a breather in coming sessions as 14-d momentum and RSI are at the border of overbought zone, suggesting that traders may collect some profits from three-day rally which accelerated on Friday.

Pullback should offer better buying opportunities, with extended dips expected to find support above 168.00 zone (broken Fibo 76.4% level at / former tops of Apr 19/25) to keep bulls in play.

Res: 170.00; 170.95; 172.11; 174.98.

Sup: 137.00; 168.36; 168.00; 167.18.

Canada’s Economy Continues to Grow in February, Points to a Slight Decline in March

The Canadian economy expanded by 0.1% month/month (m/m) in February, below Statistics Canada's flash estimate of 0.3% m/m. The flash estimate showed a -0.1% m/m change for March. January's GDP was revised up a tenth of a percent to 0.6% m/m.

February's increase in activity was roughly balanced, with output expanding in 12 of the 20 industries. Both the service-producing and goods producing sectors rose by 0.1% m/m.

The gain on the goods side was narrowly led by the construction sector (+0.3% m/m), as it advanced for a fifth straight month. Residential building construction was the top contributor for the month (+0.3% m/m). Agricultural activity contracted for a fifth straight month (-0.9% m/m).

On the services side, healthy gains in education services (+0.5% m/m), professional/scientific/tech. (+0.6% m/m), and information & culture (+0.4% m/m), were offset by a decline in wholesale trade (-1.3% m/m). Losses in the sector were focused in the motor vehicles parts and accessories subsector, declining 4.4% m/m, its lowest level since June 2020.

Key Implications

Canadian growth continues to exhibit strength. With today's print and the flash estimate for March, first quarter GDP is tracking at an annualized rate of 2.5%. This is broadly aligned with the Bank of Canada's most recent 2.3% estimate for Q1 growth.

Today's GDP numbers corroborate the BoC's recent guidance that monetary policy may need to be 'restrictive for longer'. This doesn't necessarily mean additional rate hikes are on the table, but it does provide further evidence that the start of rate cuts are less likely to occur in 2023. Our view is that the BoC will hold the policy rate into 2024 as lagged effects of interest rate hikes still need time to work their way through the economy.

The federal public service strike, affecting some 100,000 workers, enters into its tenth day and negotiations are still ongoing. By loose estimation, a strike of this duration could shave 0.2 percentage points (ppts) off of April's GDP. However, as workers come back on the job, growth in subsequent months would be boosted.

US: Spending Remains Steady, PCE Deflator Trends Lower in March

Personal income grew 0.3% month-on-month (m/m) in March, equal to February's growth and above market expectations for a more modest 0.2% m/m gain. Compensation of employees (+0.3% m/m) accounted for most of the growth, in addition to upticks in dividend and rental income.

Subtracting inflation and taxes, real personal disposable income rose 0.3% m/m in March, accelerating from 0.2% in February.

Personal consumption was unchanged from the previous month, falling slightly from 0.1% m/m in February. This was above the 0.1% decrease expected by the consensus. Services spending rose by 0.4% m/m, while goods spending fell by 0.6% m/m.

- Housing & utilities and health care were the largest contributors in the services sector.

- Declines in motor vehicles & parts and gasoline & other energy goods weighed on goods spending.

Adjusting for inflation, real spending was unchanged from February, above the consensus estimate for a 0.1% decline. In real terms, goods spending fell 0.4% m/m, while services spending rose 0.1%.

The personal consumption price deflator rose 0.1% m/m, and 4.2% on a year-on-year (y/y) basis – slightly above the expected 4.1% y/y reading but slower than the 5.1% y/y reading in February.

The Fed's preferred measure of inflation – core PCE – rose 0.3% m/m. This was on par with expectations and equal to the 0.3% m/m uptick in February. On an annual basis, price gains decelerated to 4.6% y/y from the upwardly revised 4.7% y/y print the previous month. This was slightly above market expectations of 4.5% y/y.

The personal saving rate was 5.1% in March, above the upwardly revised 4.8% reading in February.

Key Implications

The first quarter's spending came in at a 3.7% quarter-on-quarter (annualized) pace, cooling from the fourth quarter of 2022. January's weather-induced bump in spending proved to be short-lived, as consumption growth has flat-lined over the past two months. Moving forward, we expect this to continue into the second quarter.

Inflation remains elevated as month-to-month movements in core inflation have failed to show a material shift downward, with the 3-month moving average holding at 0.4% in March. We expect that the Fed will opt to raise rates by 25 basis points at next week's meeting before pausing to gauge the cumulative impact of policy tightening.

Sunset Market Commentary

Markets

After a brief rebound yesterday, yields again turned south today. Growth and inflation data published in several EMU member states understandably painted somewhat of a diffuse picture. Growth rebounded more than expected in Spain (0.5% Q/Q, 3.8% Y/Y), Italy (0.5% Q/Q, 1.8% Y/Y) and Portugal (1.6% Q/Q and 2.5% Y/Y). French growth printed as expected (0.2% Q/Q, 0.8% Y/Y). Germany (0.0% Q/Q and -0.2% Y/Y WDA) and Austria (-0.3% Q/Q) disappointed. In the end, EMU growth only reached 0.1% Q/Q and 1.3% Y/Y vs 0.2% Q/Q expected. Aside from a slightly disappointing growth performance, markets were even more focused on members states’ inflation data. Spanish HICP inflation reaccelerated (0.6% M/M and 4.1% Y/Y from 3.3%). Still the rise was less than expected and core inflation eased from 7.5% to 6.6%. French HICP inflation printed marginally stronger than expected at 0.7%M/M and 6.9%. German inflation slowed more than anticipated (HICP 0.6% M/M and 7.6% Y/Y). The monthly rise in most countries still suggests that the inflationary dynamics is far from eradicated. However, markets concluded that today’s data might help tilt the debate at next week’s ECB meeting more towards a 25 rather than a 50 bps hike. The final word in this debate is for the EMU (core) CPI estimate and the Euro Area bank lending survey, both scheduled for release next Tuesday. Still German yields after the morning data ease up to 10+ bps across the curve. US data, brought no big surprise. The US Q1 Employment cost index rose 1.2%, slightly more than expected. March spending and income data, annex the March core inflation deflator (0.3% M/M 4.6% Y/Y) were too close to expectations to change the bond friendly market sentiment. US yields currently are ceding between 2 bp (2-y) and 7 bps (10 & 30-y). Bunds outperform with yields declining between 10.5 bps (5- 10-y) and 8.5 bps (30-y). Markets now only see chances of about 10-15% for a 50 bps ECB rate hike next week. We think that this is quite a ‘minimalistic’ assessment. The combination of the EMU avoiding a recession and the easing yields this time didn’t help European equites, even after strong WS gains yesterday evening, as a negative guidance from Amazon (amongst others) dented sentiment. The Eurostoxx 50 is ceding about 0.5%. US indices opened marginally lower (0.1-0.3% lower). Oil stabilize/gains marginally after steep decline earlier this week ($ 79.2 p/b).

A sharp decline in European yields, persistent uncertainty on future (global) growth and a risk-off sentiment, initially looked as turning out USD positive. DXY tried to break out of a downtrend channel, but a part of the initial gains evaporated as the US session evolves (currently 101.85 from 101.50 area). EUR/USD slipped temporarily below the 1.10 but returned to the big figure level. Cycle/commodity related currencies (EUR/NOK 1.1078 (also cf infra), AUD 0.658, USD/CAD 1.364) mostly trade in the defensive. The yen is losing heavily as market don’t expect a BOJ policy change anytime soon after the first policy meeting under new BOJ governor Ueda. USD/JPY jumped two big figures, north of 136(05). EUR/JPY (149.60) nears the end 2014 top (149.78). Sterling trades marginally stronger against the dollar (1.25) and outperforms the euro with EUR/GBP extensively testing the 0.88 handle.

News & Views

The Norwegian central bank said that it will purchase FX on behalf of the government equivalent to NOK 1400 mn per day in May 2023. That’s down from 1500mn/day in April and the lowest amount of monthly FX purchases since March 2022. However, from 2014 until early 2022, the Norges Bank was a net seller of FX/buyer of NOK. Investors hoped that the amount of FX purchases would fall faster with EUR/NOK spiking from 11.70 to nearly 11.85 on the release. It’s the weakest NOK-level since the height of pandemic early 2020. The krone is the worst performing G10 currency against both the euro and the dollar YTD. The Norges Bank FX transactions are conducted as the Norwegian government receives revenues from petroleum activities in both NOK and FX. Part is used to finance the budget deficit and part is saved in FX in the Government Pension Fund Global.

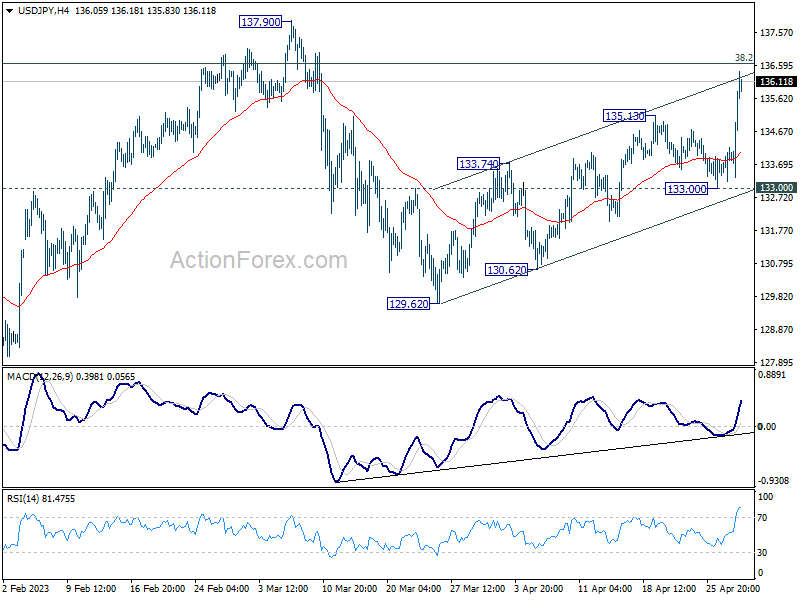

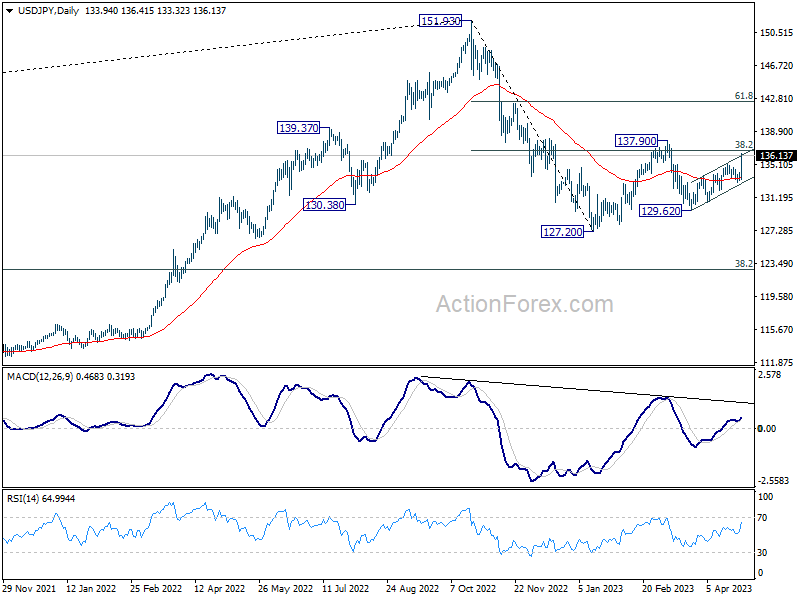

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 133.42; (P) 133.81; (R1) 134.38; More...

Intraday bias in USD/JPY remains on the upside for the moment. Decisive break of channel resistance, (now at 136.26). will raise the chance of resumption of whole rise from 127.20, and target 137.90 resistance and above. For now, further rally will remain in favor as long as 133.00 support holds, in case of retreat.

In the bigger picture, price actions from 151.93 high are currently seen as a corrective pattern to the long term up trend. The first leg should have completed at 127.20. Rebound from there is seen as the second leg. Sustained break of 31.8% retracement of 151.93 to 127.20 at 136.34 will bring stronger rebound to 142.48. Meanwhile, break of 129.62 will argue that the third leg is starting to 61.8% projection of 151.93 to 127.20 from 137.90 at 122.61.

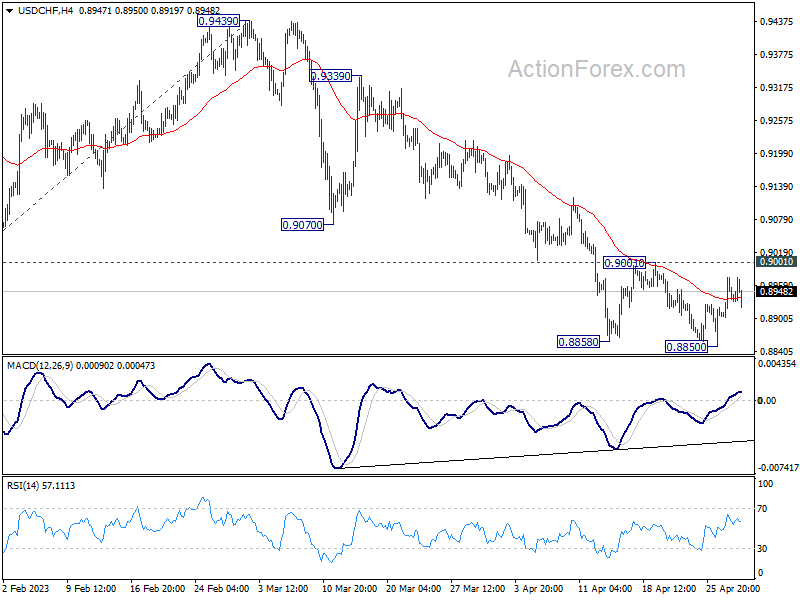

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8905; (P) 0.8941; (R1) 0.8978; More...

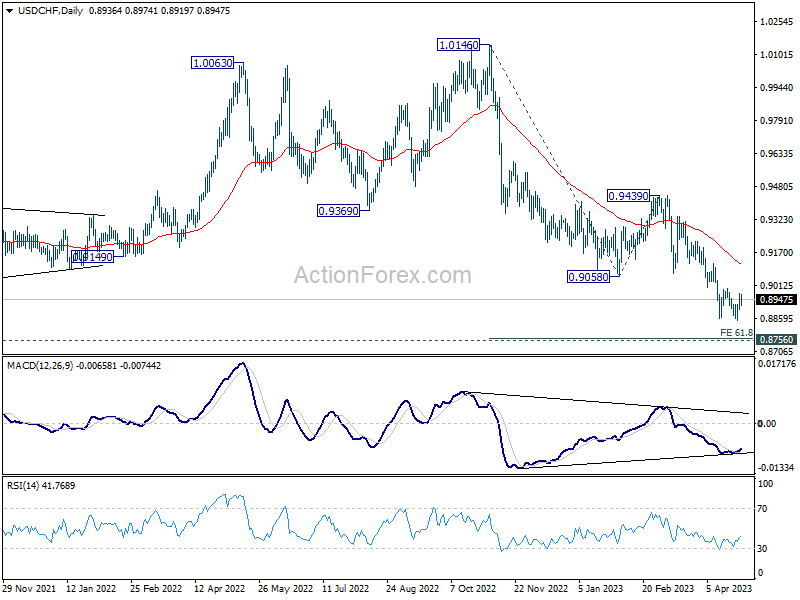

USD/CHF is still bounded in range of 0.8850/9001 and intraday bias stays neutral. On the upside, decisive break of 0.9001 resistance should confirm short term bottoming at 0.8850. Intraday bias will be back on the upside 55 D EMA (now at 0.9120). Sustained break there will be a strong sign of bullish reversal. On the downside, break of 0.8850 will resume larger fall from 1.0146, to 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support. Strong support is expected there to bring rebound, at least on first attempt.

In the bigger picture, fall from 1.1046 (2022 high) is in progress for 0.8756 support (2021 low). But overall, this fall is still seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

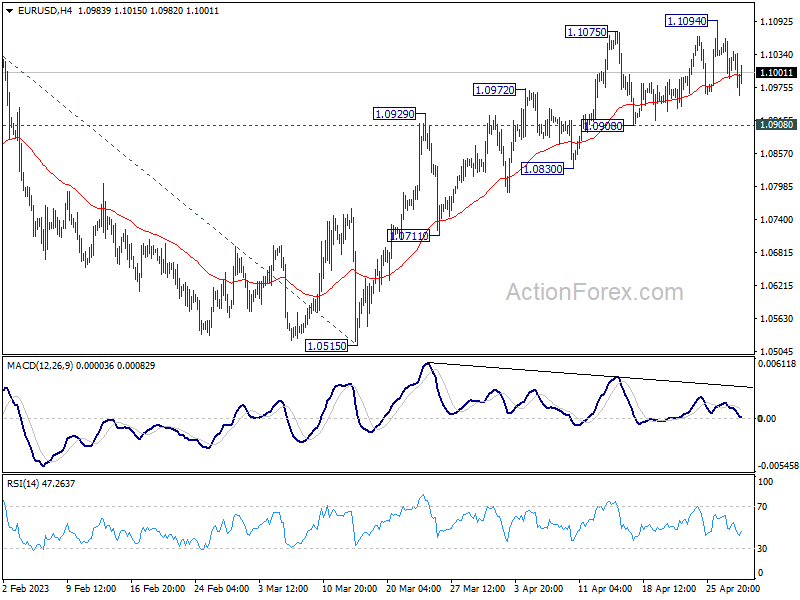

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0993; (P) 1.1028; (R1) 1.1064; More...

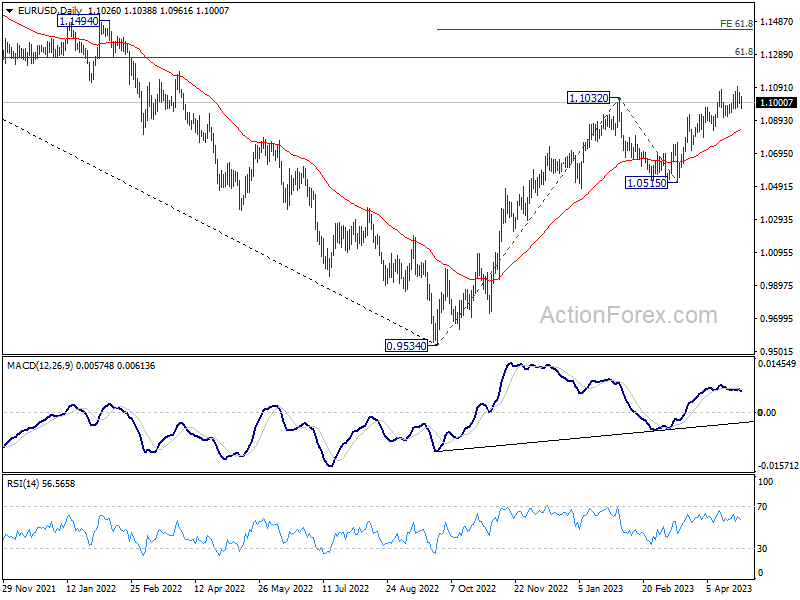

Intraday bias in EUR/USD remains neutral for consolidation below 1.1094. But further rally is expected as long as 1.0908 support holds. Break of 1.1094 will resume larger up trend to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

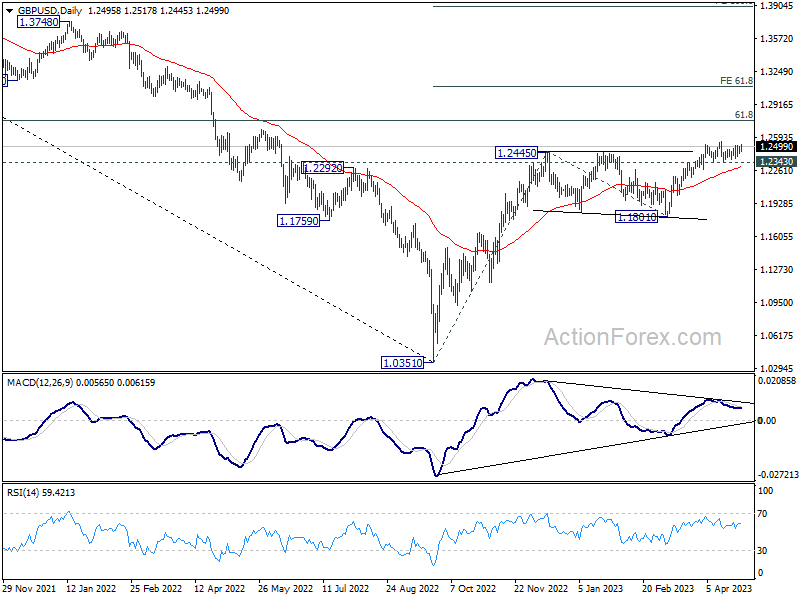

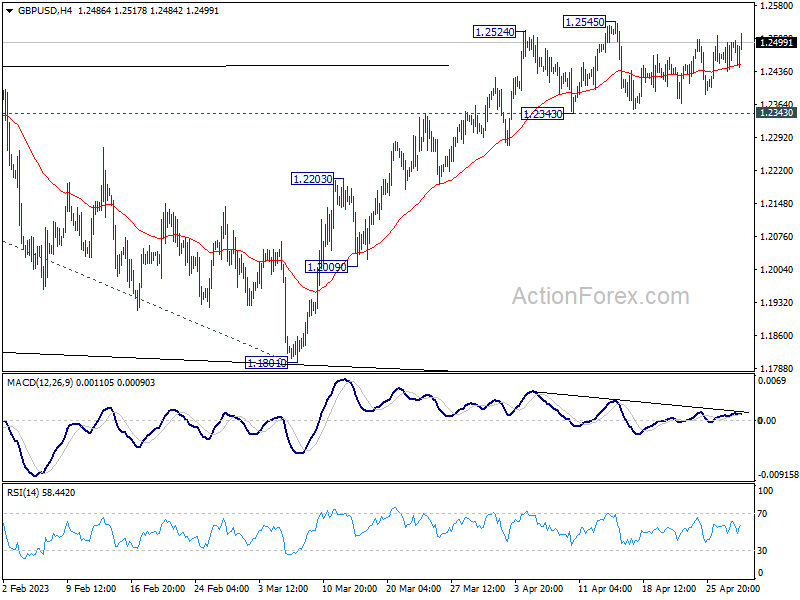

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2456; (P) 1.2479; (R1) 1.2520; More...

GBP/USD extends the near term choppy recovery but stays below 1.2545 resistance. Intraday bias remains neutral at this point. Outlook remains bullish with 1.2343 support intact. On the upside, above 1.2545 will target 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. However, considering bearish divergence condition in 4H MACD, firm break of 1.2343 will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.