Sample Category Title

Dollar Weakens Against Europeans Following Inflation Data, Yen Continues Post-BoJ Selloff

Dollar is facing renewed pressure against European majors in early US trading sessions due to faster-than-expected declines in headline inflation. However, it continues to hold strong against Japanese Yen, which remains the worst performer for both the day and the week. Yen is continuing the post-BoJ selloff, with no signs of stopping as of yet. Euro is weaker compared to British Pound the Swiss Franc after mixed GDP data, while the Australian and Canadian dollars are not faring much better.

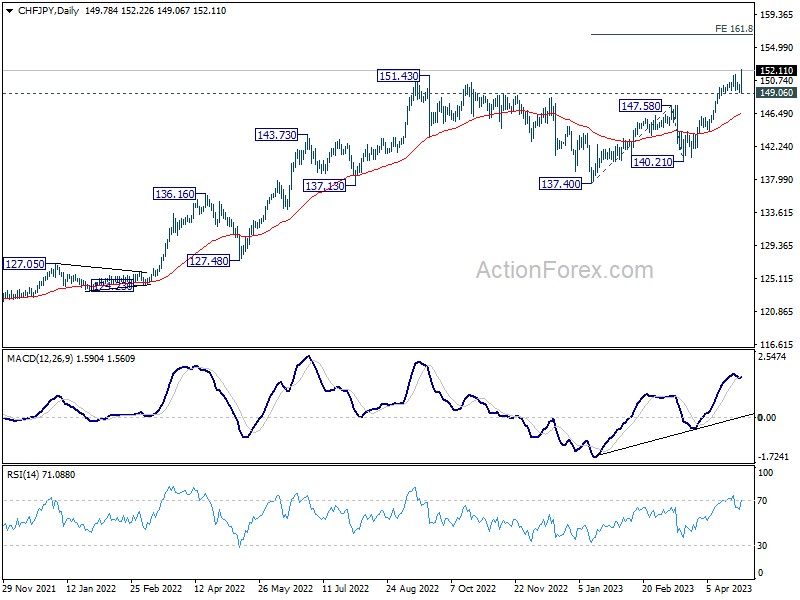

On the technical side, CHF/JPY broke through 151.43 high convincingly today, a resumption of the long-term uptrend. Near-term outlook will remain bullish as long as 149.06 support level holds. The cross could now enter acceleration phase, targeting 161.8% projection of 137.40 to 147.58 from 140.21 at 156.68.

In Europe at the time of writing, FTSE is up 0.13%. DAX is up 0.20%. CAC is down -0.42%. Germany 10-year yield is down -0.1117 at 2.350. Earlier in Asia, Nikkei surged 1.40%. Hong Kong HSI rose 0.27%. China Shanghai SSE rose 1.14%. Singapore Strait Times dropped -0.35%. Japan 10-year JGB yield tumbled sharply by -0.0713 to 0.389.

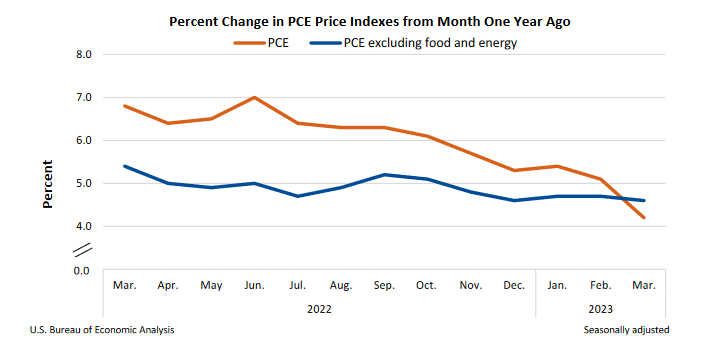

US PCE inflation slowed to 4.2% yoy, core PCE slightly down to 4.6% yoy

US personal income rose 0.3% mom or USD 67.9B in March, above expectation of 0.2% mom. The increase in income primarily reflected increases in compensation, personal income receipts on assets, and rental income of persons that were partly offset by decreases in proprietors' income and personal current transfer receipts

Personal spending rose less than 0.1% mom or USD 8.2B, better than expectation of -0.1% mom contraction. The increase reflected a USD 44.9 billion increase in spending for services that was partly offset by a USD 36.7 billion decrease in spending for goods

For the month PCE price index increased 0.1% mom. Excluding food and energy, PCE price index increased 0.3% mom. Prices for goods decreased -0.2% mom and prices for services increased 0.2%. Food prices decreased -0.2% and energy prices decreased -3.7% mom.

From the same month one year ago, PCE price index March slowed from 5.1% yoy to 4.2% yoy, below expectation of 4.6% yoy. Excluding food and energy, PCE price index ticked down from 4.7% yoy to 4.6% yoy, above expectation of 4.6% yoy. Prices for goods increased 1.6 yoy and prices for services increased 5.5% yoy. Food prices increased 8.0% yoy and energy prices decreased 9.8% yoy.

Canada GDP grew 0.1% mom in Feb, but down -0.1% in Mar

Canada GDP grew 0.1% mom in February, below expectation of 0.2% mom. Both services-producing industries and goods-producing industries edged up 0.1%. Overall, 12 of 20 subsectors increased.

Advance information indicates that real GDP edged down -0.1% in March. This advance information indicates a 0.6% increase in real GDP by industry in the first quarter of 2023.

Eurozone GDP rose 0.1% qoq in Q1, EU up 0.3 qoq

Eurozone GDP grew 0.1% qoq in Q1, matched expectations. EU GDP rose 0.3% qoq. Germany GDP stalled in Q1 (price, seasonally and calendar adjusted), below expectation of 0.1% qoq growth. France's Q1 GDP growth came in at a modest 0.2% qoq, slightly outperforming market expectations of 0.1% qoq.

Swiss KOF dropped to 96.4, the economy cannot find its footing

Swiss KOF Economic Barometer dropped from 99.2 to 96.4 in April, dipping slightly lower under its medium-term average value. KOF said, "at the moment, the Swiss economy cannot really find its footing."

The majority of the indicator bundles are affected by the softening. In particular, the indicators for manufacturing, services, hospitality and private consumption. In contrast, the outlook for foreign demand is stable and that for financial and insurance services is brightening.

BoJ stands pat, to take 1-1.5 yrs to review monetary policy

BoJ keeps monetary policy unchanged as widely expected, by unanimous vote. Under the yield curve control, short-term policy interest rate is held at -0.10%. 10-year JGB yield will be kept at around 0% with bond purchases without upper limit. 10-year JGB yield will continue to be allowed to fluctuate in range of around plus and minus 0.50% from 0% level.

The central bank maintained the pledge to continue with Quantitative and Qualitative Monetary Easing with Yield Curve Control for "as long as it is necessary" for meeting inflation target in a "stable manner". It "will not hesitate to take additional easing measures if necessary". BoJ will conduct a "broad-perspective review of monetary policy", with a planned time frame of around 12 to 18 months.

In the new economic projections, while core inflation forecasts were upgraded, it's not expected to sustain at the 2% level throughout the horizon.

- Real GDP forecasts (versus January estimates):

- Fiscal 2023 at 1.4% (down from 1.7%).

- Fiscal 2024 at 1.2% (up from 1.1%).

- Fiscal 2025 at 1.0% (new)

- CPI Core forecasts (versus January estimates):

- Fiscal 2023 at 1.8% (up from 1.6%).

- Fiscal 2024 at 2.0% (up from 1.8%).

- Fiscal 2025 at 1.6% (new).

- CPI Core-Core forecasts (versus January estimates):

- Fiscal 2023 at 2.5% (up from 1.8%).

- Fiscal 2024 at 1.7% (up from 1.6%).

- Fiscal 2025 at 1.8% (new).

Japan industrial production rose 0.8% mom, with signs of moderate pick up

Japan's industrial production expanded for the second consecutive month, recording a 0.8% mom growth in March, surpassing the expected 0.4% mom increase. The growth was driven by output in eight sectors, led by motor vehicles, while declines were observed in seven sectors, including electronic components and devices.

The Ministry of Economy, Trade and Industry upgraded its basic assessment for the month, stating that industrial production was "showing signs of moderately picking up" as parts supply shortages continued to ease. This is a marked improvement from the previous month's assessment of "weakening." The ministry also projects a further 4.1% growth in industrial production for April and a -2.0% decline in May.

Other economic indicators released include 7.2% yoy increase in retail sales for March, surpassing expectations of 6.5% yoy. However, unemployment rate rose for the second month in a row, reaching 2.8%, above expectation of 2.5%.

April, Tokyo core CPI, which excludes fresh food, accelerated from 3.2% to 3.5% yoy, exceeding expectations of 3.2% yoy. Core-core CPI, which excludes fresh food and fuel costs, accelerated from 3.4% to 3.8% year-on-year, marking the highest rate since April 1982.

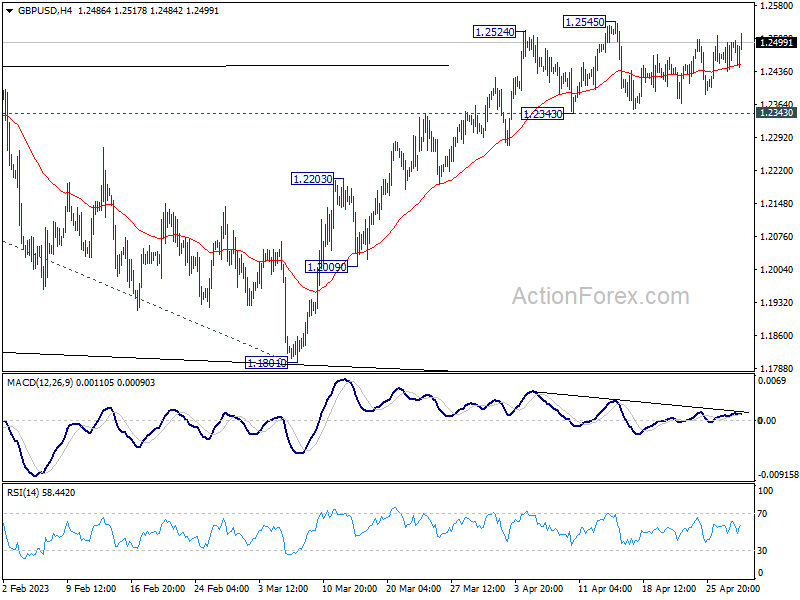

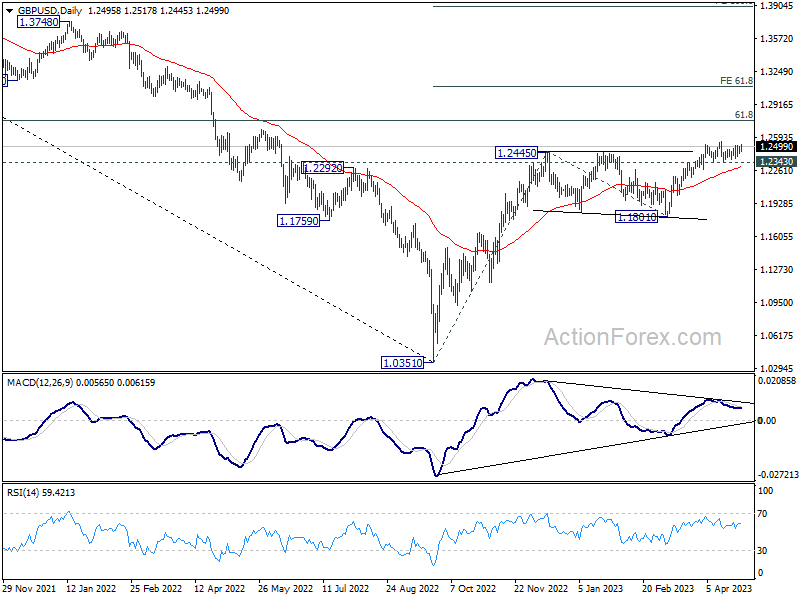

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2456; (P) 1.2479; (R1) 1.2520; More...

GBP/USD extends the near term choppy recovery but stays below 1.2545 resistance. Intraday bias remains neutral at this point. Outlook remains bullish with 1.2343 support intact. On the upside, above 1.2545 will target 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. However, considering bearish divergence condition in 4H MACD, firm break of 1.2343 will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Apr | 3.50% | 3.20% | 3.20% | |

| 23:50 | JPY | Industrial Production M/M Mar P | 0.80% | 0.40% | 4.60% | |

| 23:50 | JPY | Retail Trade Y/Y Mar | 7.20% | 6.50% | 6.60% | 7.30% |

| 23:30 | JPY | Unemployment Rate Mar | 2.80% | 2.50% | 2.60% | |

| 01:30 | AUD | Private Sector Credit M/M Mar | 0.30% | 0.30% | 0.30% | |

| 01:30 | AUD | PPI Q/Q Q1 | 1.00% | 1.50% | 0.70% | |

| 01:30 | AUD | PPI Y/Y Q1 | 5.20% | 5.80% | 5.80% | |

| 04:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 05:00 | JPY | Housing Starts Y/Y Mar | -3.20% | -3.70% | -0.30% | |

| 05:30 | EUR | France GDP Q/Q Q1 P | 0.20% | 0.10% | 0.10% | |

| 06:00 | EUR | Germany Import Price Index M/M Mar | -1.10% | -0.90% | -2.40% | |

| 06:30 | CHF | Real Retail Sales Y/Y Mar | -1.90% | 0.40% | 0.30% | -0.50% |

| 07:00 | CHF | KOF Leading Indicator Apr | 96.4 | 98 | 98.2 | 99.2 |

| 07:55 | EUR | Germany Unemployment Change Mar | 24K | 10K | 16K | |

| 07:55 | EUR | Germany Unemployment Rate Mar | 5.60% | 5.60% | 5.60% | |

| 08:00 | EUR | Germany GDP Q/Q Q1 P | 0.00% | 0.10% | -0.40% | |

| 08:00 | EUR | Italy GDP Q/Q Q1 P | 0.50% | 0.20% | -0.10% | |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.10% | 0.10% | 0.00% | |

| 12:00 | EUR | Germany CPI M/M Apr P | 0.40% | 0.60% | 0.80% | |

| 12:00 | EUR | Germany CPI Y/Y Apr P | 7.20% | 7.30% | 7.40% | |

| 12:30 | CAD | GDP M/M Feb | 0.10% | 0.20% | 0.50% | |

| 12:30 | USD | Personal Income M/M Mar | 0.30% | 0.20% | 0.30% | |

| 12:30 | USD | Personal Spending Mar | 0.00% | -0.10% | 0.20% | 0.10% |

| 12:30 | USD | PCE Price Index M/M Mar | 0.10% | 0.30% | 0.30% | |

| 12:30 | USD | PCE Price Index Y/Y Mar | 4.20% | 4.60% | 5.00% | 5.10% |

| 12:30 | USD | Core PCE Price Index M/M Mar | 0.30% | 0.30% | 0.30% | |

| 12:30 | USD | Core PCE Price Index Y/Y Mar | 4.60% | 4.50% | 4.60% | 4.70% |

| 12:30 | USD | Employment Cost Index Q1 | 1.20% | 1.10% | 1.00% | |

| 13:45 | USD | Chicago PMI Apr | 43.7 | 43.8 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Apr F | 63.5 | 63.5 |

Canada GDP grew 0.1% mom in Feb, but down -0.1% in Mar

Canada GDP grew 0.1% mom in February, below expectation of 0.2% mom. Both services-producing industries and goods-producing industries edged up 0.1%. Overall, 12 of 20 subsectors increased.

Advance information indicates that real GDP edged down -0.1% in March. This advance information indicates a 0.6% increase in real GDP by industry in the first quarter of 2023.

US PCE inflation slowed to 4.2% yoy, core PCE slightly down to 4.6% yoy

US personal income rose 0.3% mom or USD 67.9B in March, above expectation of 0.2% mom. The increase in income primarily reflected increases in compensation, personal income receipts on assets, and rental income of persons that were partly offset by decreases in proprietors' income and personal current transfer receipts

Personal spending rose less than 0.1% mom or USD 8.2B, better than expectation of -0.1% mom contraction. The increase reflected a USD 44.9 billion increase in spending for services that was partly offset by a USD 36.7 billion decrease in spending for goods

For the month PCE price index increased 0.1% mom. Excluding food and energy, PCE price index increased 0.3% mom. Prices for goods decreased -0.2% mom and prices for services increased 0.2%. Food prices decreased -0.2% and energy prices decreased -3.7% mom.

From the same month one year ago, PCE price index March slowed from 5.1% yoy to 4.2% yoy, below expectation of 4.6% yoy. Excluding food and energy, PCE price index ticked down from 4.7% yoy to 4.6% yoy, above expectation of 4.6% yoy. Prices for goods increased 1.6 yoy and prices for services increased 5.5% yoy. Food prices increased 8.0% yoy and energy prices decreased 9.8% yoy.

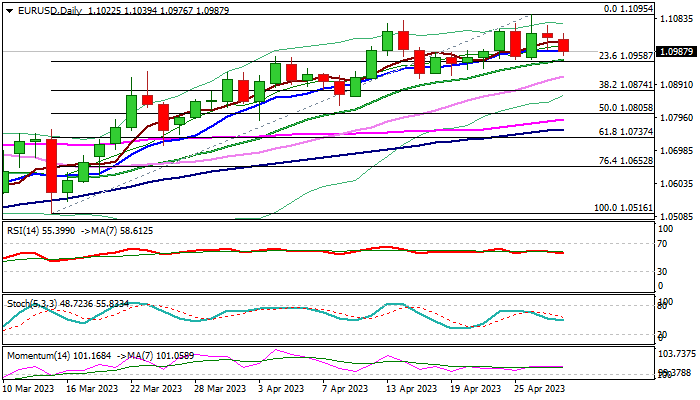

EUR/USD: Larger Bulls Likely to Regain Traction after a Shallow Pullback

The Euro dips below 1.10 support on Friday, extending pullback from new 2023 high (1.1095) into second consecutive day.

Stronger dollar on Friday morning pressured the single currency, along with weak EU / German GDP data for Q1, though markets remain cautious ahead of today’s key event – US PCE data, closely watched by Fed.

The pullback was so far seen as a healthy correction of a larger uptrend, as daily studies are bullish, with dips expected to find firm ground at 1.0960 zone (rising 20DMA / Fibo 23.6% of 1.0516/1.1095 rally) which would offer better levels to re-join bullish market for fresh push higher.

Fundamentals are likely to be a key market driver on Friday, with core US PCE at / below forecasts to signal that inflation is losing traction,

This scenario will be supportive for Euro as weaker inflation would make the dollar less attractive for traders.

On the other hand, stronger than expected PCE figures would signal that inflationary pressure is rising again and lift the dollar.

Caution on break below 1.0960 zone as this would increase downside risk of testing pivotal supports at 1.0909 (Apr 17 trough) and 1.0874 (Fibo 38.2% of 1.0516/1.1095), loss of which would signal deeper correction.

Res: 1.1015; 1.1039; 1.1075; 1.1095.

Sup: 1.0960; 1.0909; 1.0874; 1.0831.

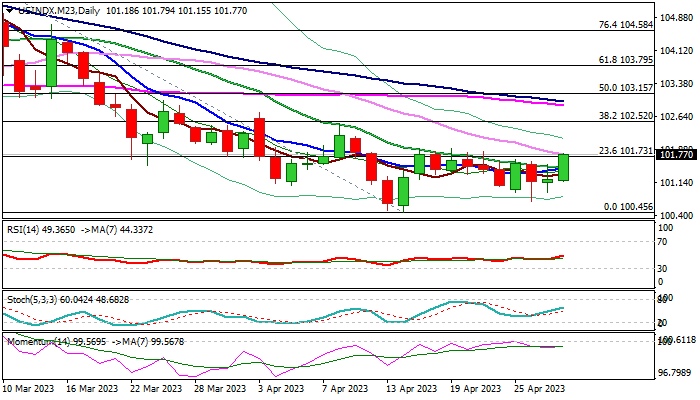

Dollar Advances on Dovish BOJ, Weaker Euro – Markets Await Release of Key US PCE Report

The US dollar index rose to one-week high in European session on Friday, lifted by dovish BOJ, after the currency escaped from stronger negative consequences from much weaker than expected US Q1 GDP, as consumer spending accelerated on rising inflation, partially offsetting negative impact.

Expectations that the Fed would opt for another 25 basis points hike before putting its tightening cycle on hold for the rest of the year contributed to keeping the greenback afloat.

Technical picture on daily chart shows signs of improvement but remains bearish overall, with negative signals from weakening monthly studies and the index being on track for the second consecutive monthly loss.

Fresh advance needs a sustained break of the lower platform at 101.90 zone (Apr 17/21 tops) to sideline persisting downside risk and generate initial bullish signal for continuation of recovery leg from 100.45 (new 2023 low posted on Apr 14).

The dollar was also underpinned by weaker Euro, as data released today showed that inflation in in the euro bloc remains elevated, German economy stagnated in the first three months of the year, while Eurozone economy grew at a slower pace than expected.

Traders await release of US Core PCE price index, Fed’s preferred inflation gauge, which is expected to show unchanged rise of 0.3% m/m in March and annualized figure is expected to tick to 4.5% from 4.6%.

Initial signs that inflation is easing would put the greenback under pressure, while stronger drop could be expected on downside surprise in March.

Conversely, the greenback would rise on signals that inflation is gaining pace again.

Res: 101.53; 101.88; 102.22; 102.46.

Sup: 101.07; 100.66; 100.00; 99.30.

USD/JPY Surges after BoJ Maintains Policy, Inflation Rises

- Bank of Japan maintains monetary policy

- BoJ removes forward guidance and announces policy review

- Tokyo Core CPI rises higher than expected

- USD/JPY soars

USD/JPY has jumped 1.3% today and is trading at 135.74. Earlier, the yen touched a low of 135.86, its lowest level since March 10th.

BoJ holds policy but changes guidance

Today’s Bank of Japan meeting was closely watched, as New Governor Ueda chaired his first meeting. As expected, there were no dramatic announcements about a shift in policy, but the yen still dropped sharply, as those investors that had hoped for a hint of monetary tightening in the short term were disappointed.

The BoJ announced that key policy settings will stay the same. Interest rates will remain at -0.10% and the yield curve control (YOC) scheme on 10-year government bonds will maintain a band of 0.50% on either side of the 0% target. There was no surprise here, as Ueda has stated on numerous occasions and again this week that he would not change these policy settings.

At the same time, the central bank modified its future guidance, removing its pledge to maintain rates at “current or lower levels”. The BoJ said it would “patiently continue with monetary easing” while saying it would conduct a broad review of monetary policy, which it expects to take one to one-and-half years.

The takeaway from the BoJ meeting is that the markets can expect more of the same in the short term, but there is the possibility of a shift in policy down the road. Ueda stated earlier in the week that if inflation and wage growth were to accelerate faster than expected, he would consider the possibility of tightening policy. Ueda does not seem as glued to current policy as his predecessor Kuroda, but the new Governor is unlikely to make any moves absent a major change in economic conditions.

Ahead of the BoJ meeting there was an interesting note from Barclays which said that the yen could regain its status as a safe-haven currency, which has been taken over by the US dollar. Barclays said that if the BoJ normalizes policy and central banks cut rates due to a weak global economy, rate differentials would tighten and the yen would move higher. Barclays is projecting that the yen will rise to 123 by the end of next year, and the stronger currency could re-establish itself as a safe haven.

Overshadowed by the BoJ meeting, Tokyo Core CPI rose in April, an indication that high inflation is alive and well. The indicator rose from 3.2% to 3.5%, above the market consensus of 3.2%.

USD/JPY Technical

- USD/JPY tested resistance at 1.3585 earlier today. The next resistance line is 1.3657

- 134.99 and 1.3427 are providing support

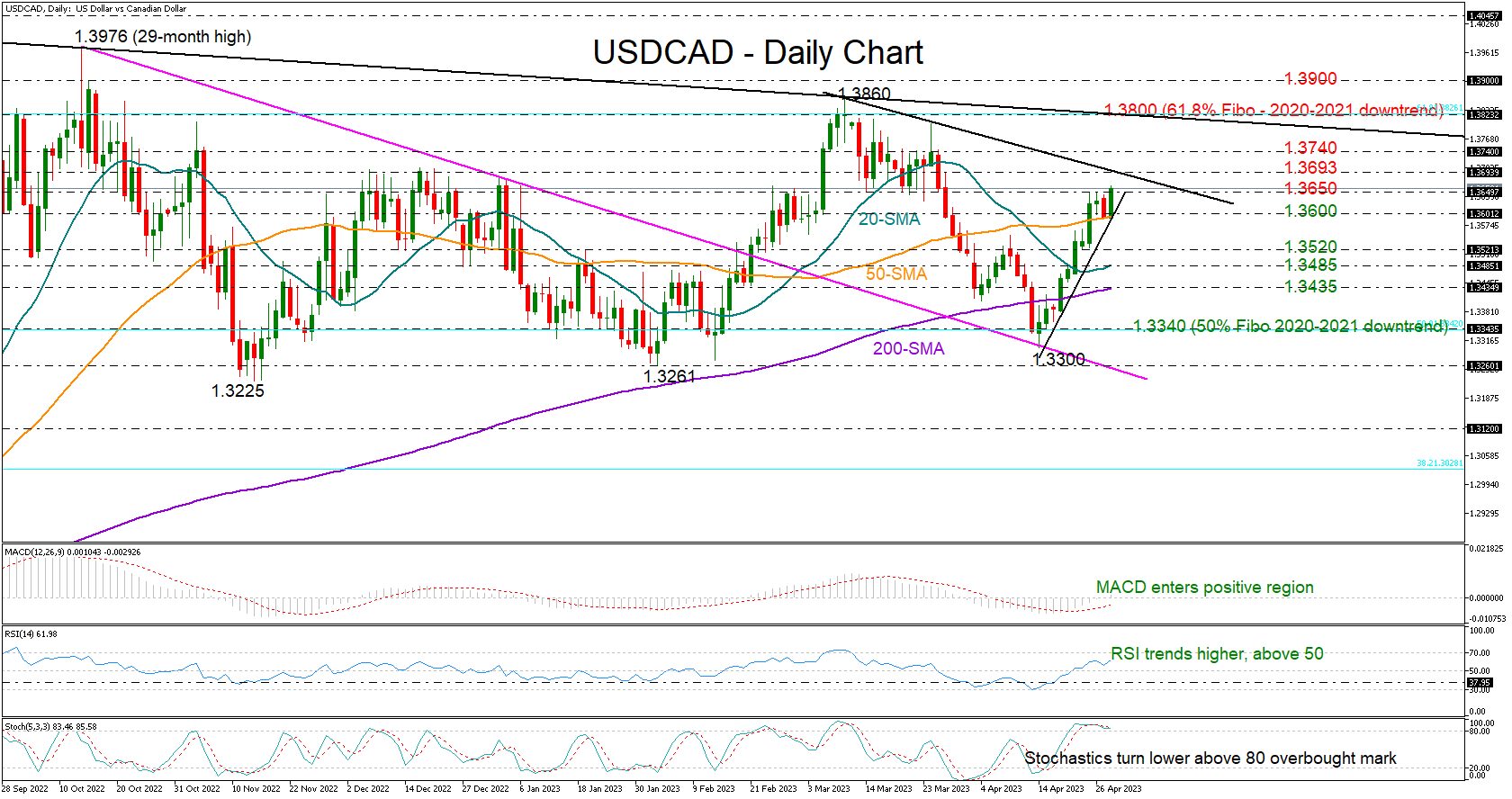

USDCAD Brings Weekly Resistance Back into Play

USDCAD bounced on the 50-day simple moving average (SMA) early on Friday to recoup Thursday’s losses and fight against the weekly resistance of 1.3650.

The odds are leaning on the bullish side as the RSI is maintaining an upward trajectory above its 50 neutral mark and the MACD is trying to enter the positive area. Yet some caution is necessary as the stochastic oscillator seems to have already peaked in the overbought region.

Should the bulls clear the 1.3650 resistance, the next stop could be near the tentative short-term descending trendline seen around 1.3693. Piercing through this wall, the price could then rise towards the 1.3740 constraining zone, a break of which could lift the price straight up to the tough 1.3800 barrier. This is where the 61.8% Fibonacci retracement of the 2020-2021 downtrend and the long-term resistance line from the 2020 top are placed. Hence, a close higher is expected to bolster buying appetite, likely up to the 1.3900 hurdle taken from October 2022.

Alternatively, a backward flip may initially test the 50-day SMA at 1.3600 and the steep ascending trendline from April’s lows. If that floor collapses, the price may tumble towards the 1.3520 barrier, while lower, the 20- and 200-day SMAs at 1.3485 and 1.3435 respectively may attract some attention ahead of the 50% Fibonacci mark of 1.3340.

In brief, USDCAD seems to have enough fuel in the tank to drive higher, though traders may wisely wait for a decisive close above 1.3650, and more importantly, beyond 1.3693 before they boost their buying orders.

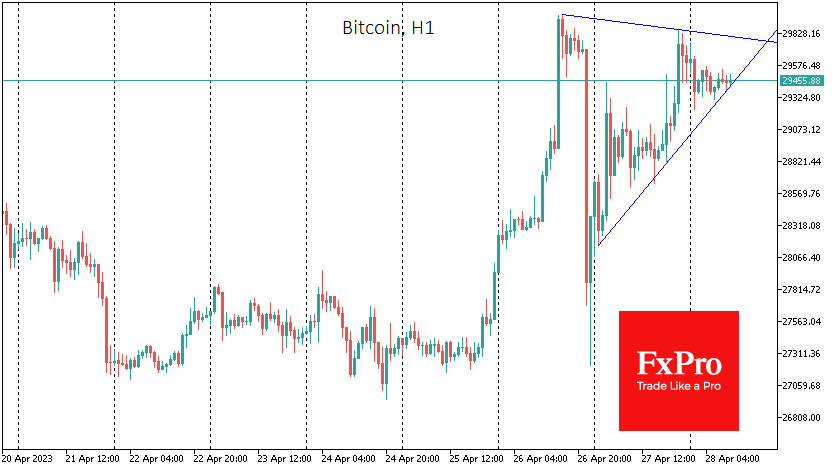

Bitcoin’s Short-Term Triangle

Market Picture

Crypto market capitalisation is up 0.85% in the last 24 hours to 1.21 trillion, in the middle of its range over the previous two weeks. The Crypto Fear and Greed Index rose 5 points to 64, establishing itself in greed territory and showing that sentiment is recovering faster than capitalisation.

Bitcoin attempted to approach $30K again on Thursday but hit lower highs than on Wednesday, although it didn’t pull back as hard. Notably, the Nasdaq high tech index was up an impressive 2.75%.

Bitcoin continues to form triangles in the short term and has a reasonably clear support line. At the same time, an impressive supply of sellers is preventing the price from fixing above the psychologically important $30K price.

Kaiko points to the increasing correlation between BTC and gold. The cryptocurrency’s dependence on precious metals has grown since early March. The banking crisis and the risks of financial turmoil are scaring investors around the world and causing them to buy up safe-haven assets.

According to CryptoQuant, bitcoin’s leverage ratio has reached an all-time low of 0.195. This reduces the volatility of the spot VC market, which is becoming less sensitive to futures market activity.

News background

Ethereum options volume and open interest on the CME hit all-time highs following the successful Shapella hardfork.

The Hong Kong Securities and Futures Commission (SFC) said it is preparing rules for licensing crypto exchanges and will introduce them next month. Turning Hong Kong into a crypto hub could provide liquidity for cryptocurrency growth and become a new rally driver, according to Blockfin Academy.

Investment in bitcoin startups has outpaced the rest of the crypto industry in terms of investment in 2022, according to a report by Trammell Venture Partners (TVP). However, the first cryptocurrency has yet to be widely accepted.

The Google Cloud platform has partnered with the Polygon project to accelerate the adoption of “key Polygon protocols” in enterprise infrastructure and tools and “increase bandwidth” in gaming, supply chain and DeFi.

Eurozone GDP rose 0.1% qoq in Q1, EU up 0.3 qoq

Eurozone GDP grew 0.1% qoq in Q1, matched expectations. EU GDP rose 0.3% qoq.

Among the Member States for which data are available for the first quarter of 2023, Portugal (+1.6%) recorded the highest increase compared to the previous quarter, followed by Spain, Italy and Latvia (all +0.5%). Declines were recorded in Ireland (-2.7%) as well as in Austria (-0.3%). The year-on-year growth rates were positive for all countries except for Germany (-0.1%).

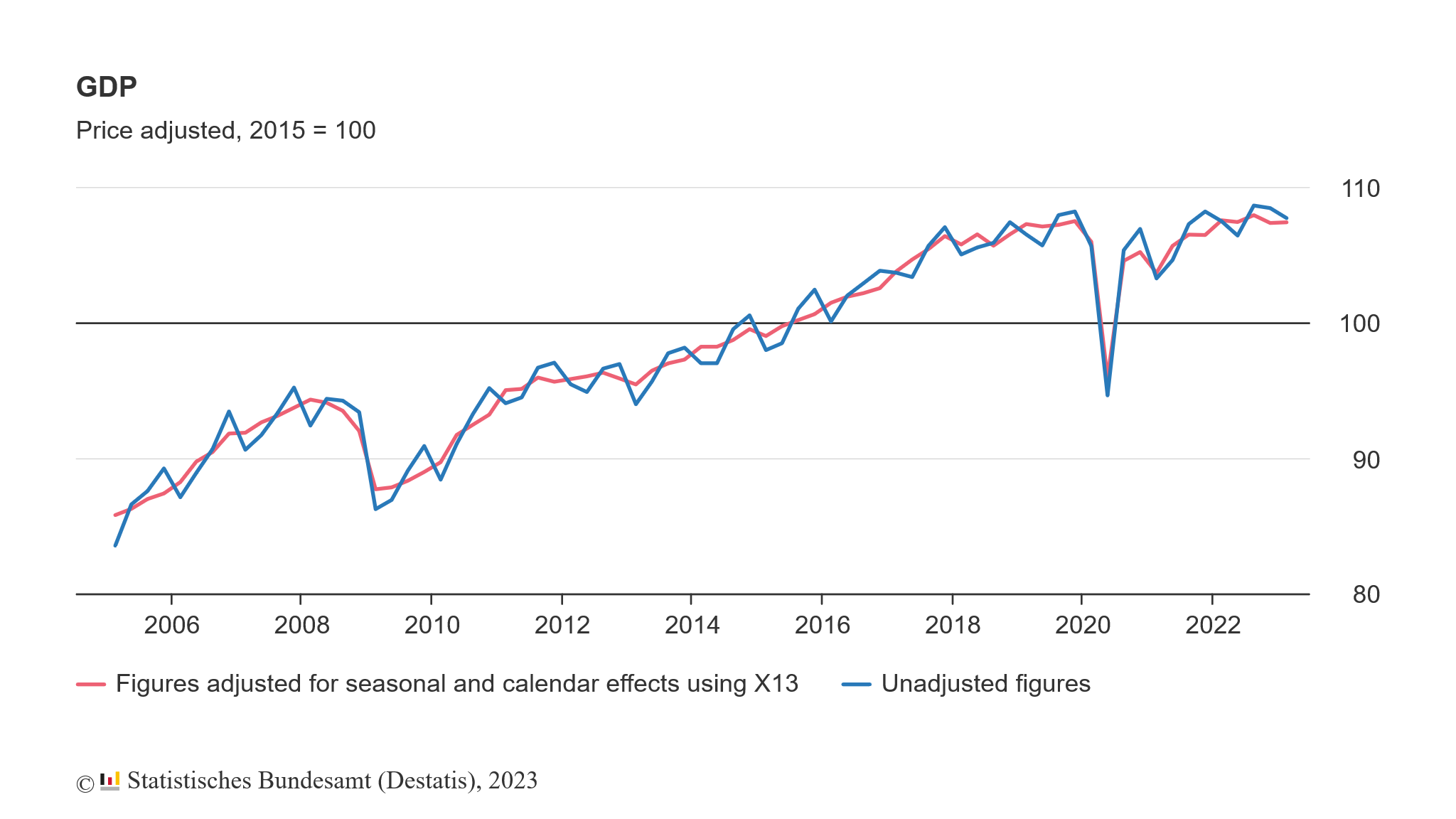

Germany GDP stalled in Q1, worst than expectations

Germany GDP stalled in Q1 (price, seasonally and calendar adjusted), below expectation of 0.1% qoq growth. GDP was up a price adjusted 0.2% compared with the first quarter of 2022. The price and calendar adjusted GDP was -0.1% lower because there was one working day more than in the same period a year earlier.

The final consumption expenditure of both households and government declined at the beginning of 2023, according to the Federal Statistical Office (Destatis). Positive contributions, in contrast, came from capital formation and exports.