Sample Category Title

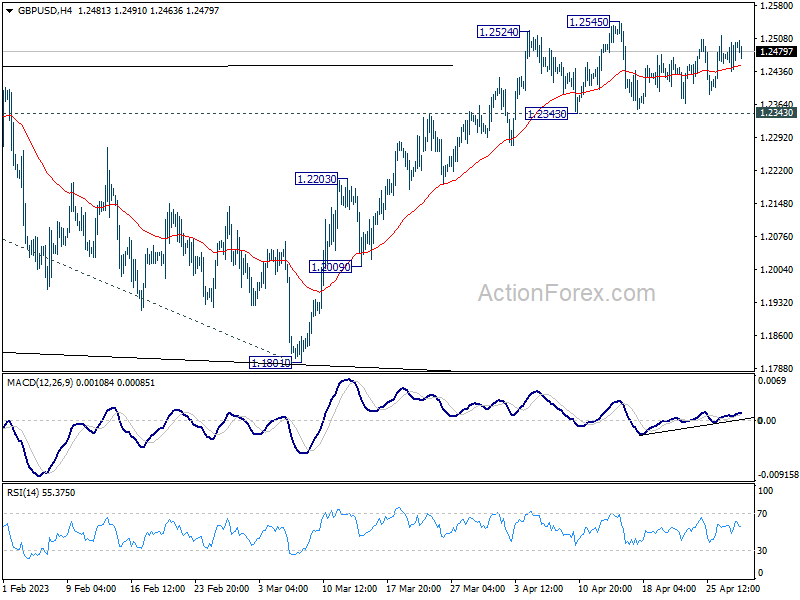

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2456; (P) 1.2479; (R1) 1.2520; More...

Intraday bias in GBP/USD remains neutral as consolidation from 1.2545 is still extending. Outlook remains bullish with 1.2343 support intact. On the upside, above 1.2545 will target 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. However, considering bearish divergence condition in 4H MACD, firm break of 1.2343 will confirm short term topping, and turn bias back to the downside for deeper pullback.

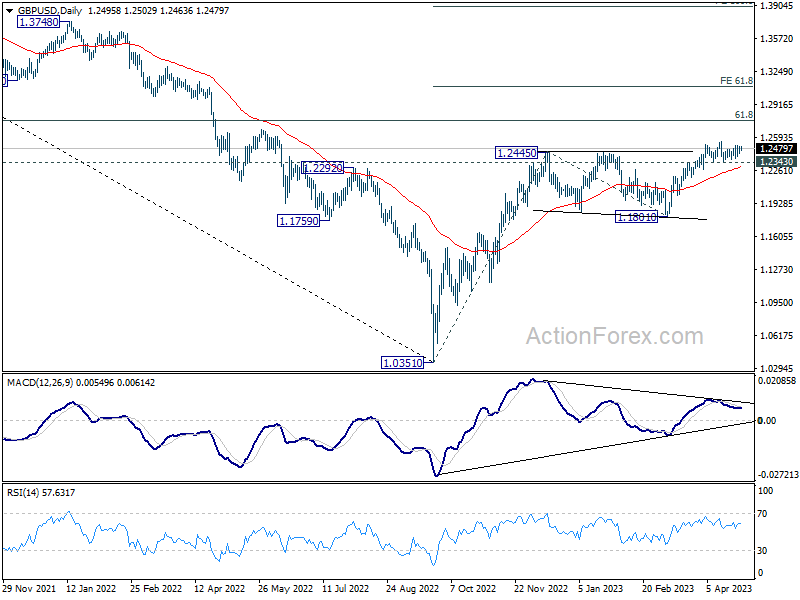

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

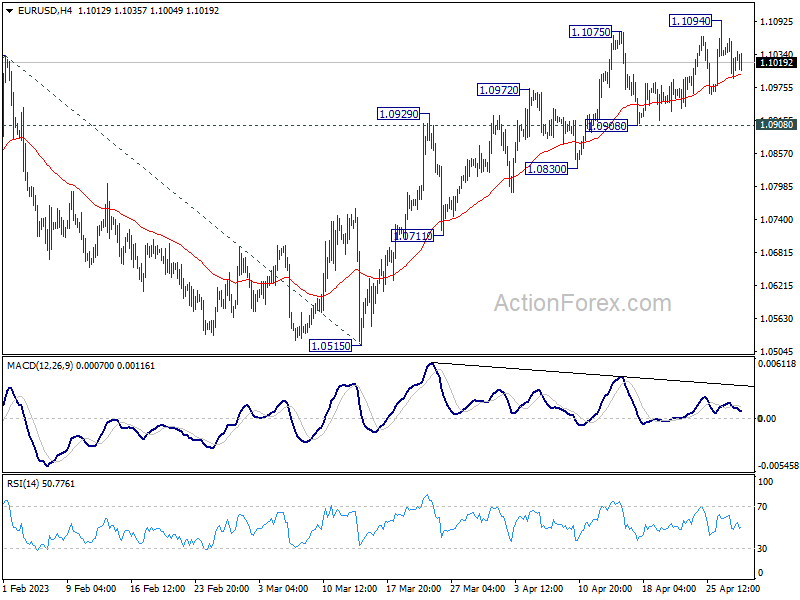

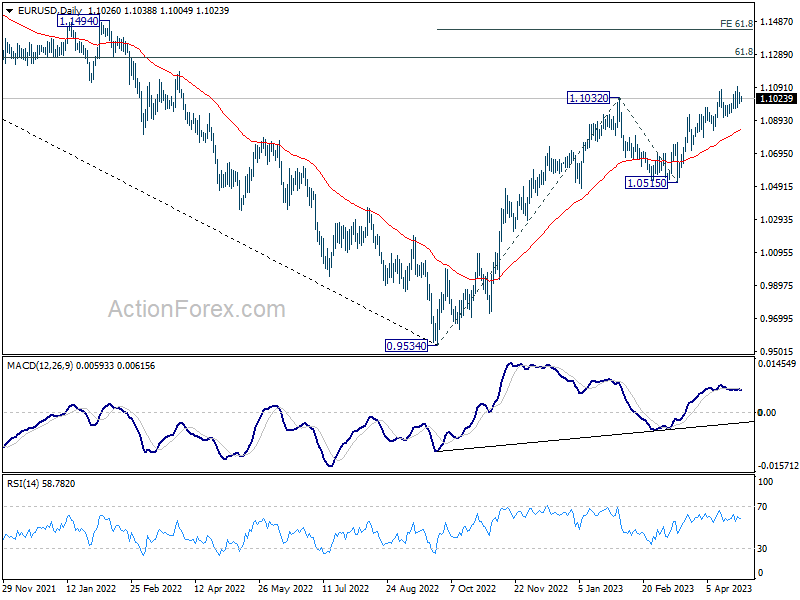

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0993; (P) 1.1028; (R1) 1.1064; More...

EUR/USD is still extending the consolidation pattern from 1.1094 and intraday bias remains neutral. But further rally is expected as long as 1.0908 support holds. Break of 1.1094 will resume larger up trend to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

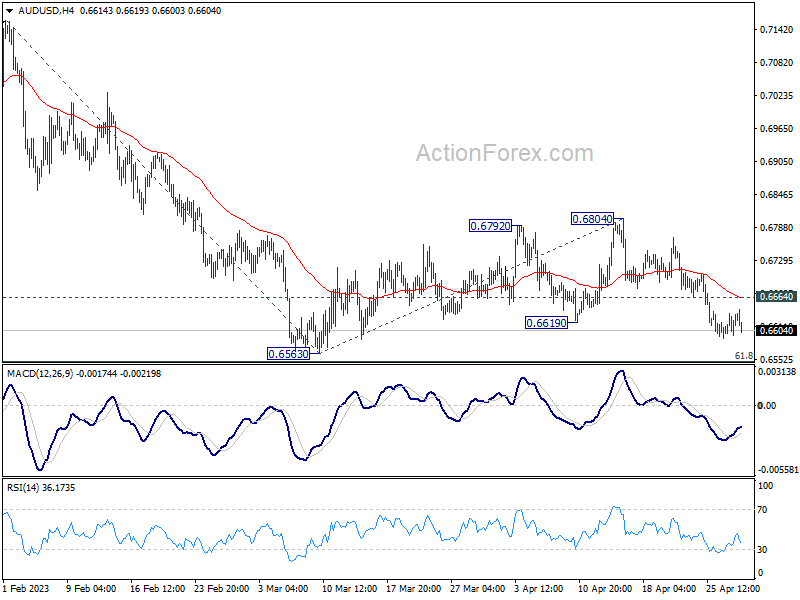

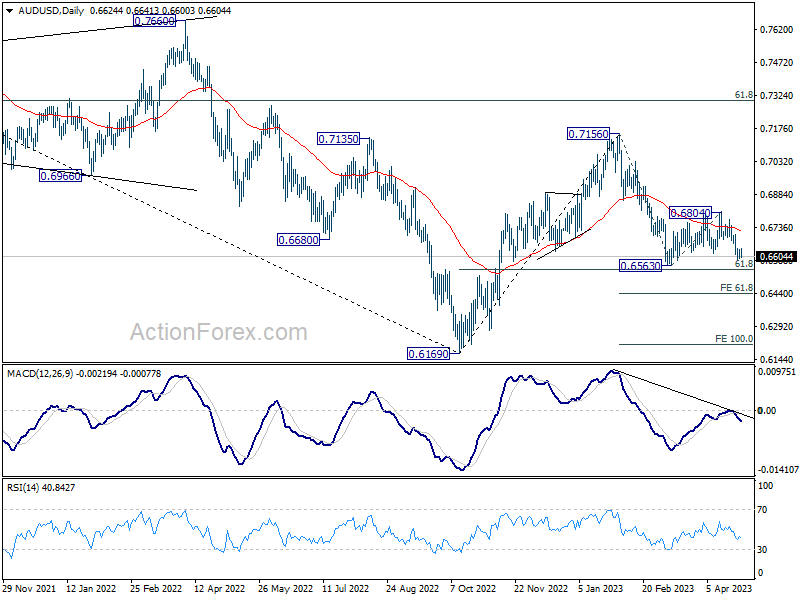

AUD/USD Daily Report

Daily Pivots: (S1) 0.6606; (P) 0.6621; (R1) 0.6645; More...

Further decline is still expected in AUD/USD with 0.6664 minor resistance intact, despite loss of downside momentum. Consolidation pattern from 0.6563 should have completed at 0.6804, and larger decline from 0.7156 is ready to resume. Firm break of 0.6563 will bring deeper decline through 0.6546 fibonacci level to 61.8% projection of 0.7156 to 0.6563 from 0.6804 at 0.6438 next. On the upside, break 0.6664 minor resistance will turn bias to the upside to extend the consolidation pattern with another rising leg.

In the bigger picture, as long as 61.8% retracement of 0.6169 to 0.7156 at 0.6546 holds, the decline from 0.7156 is seen as a correction to rally from 0.6169 (2022 low) only. Another rise should still be seen through 0.7156 at a later stage. However, sustained break of 0.6546 will raise the chance of long term down trend resumption through 0.6169 low.

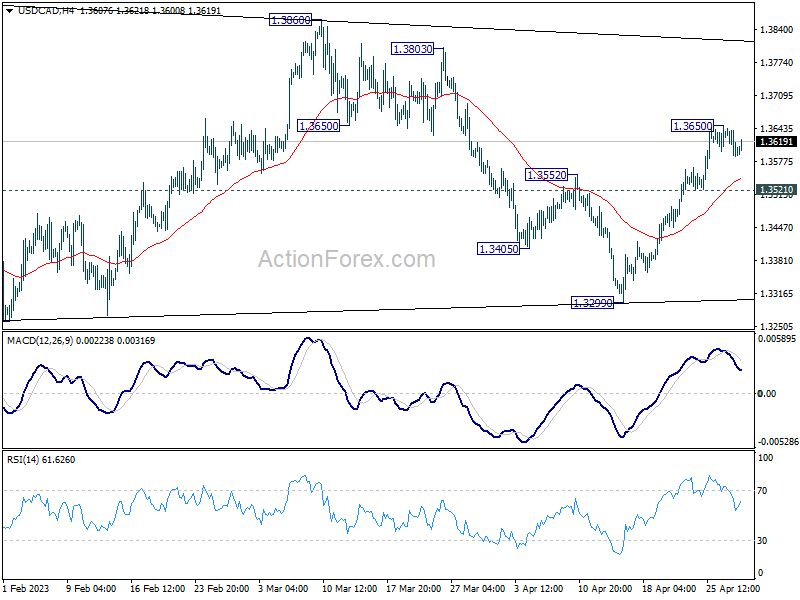

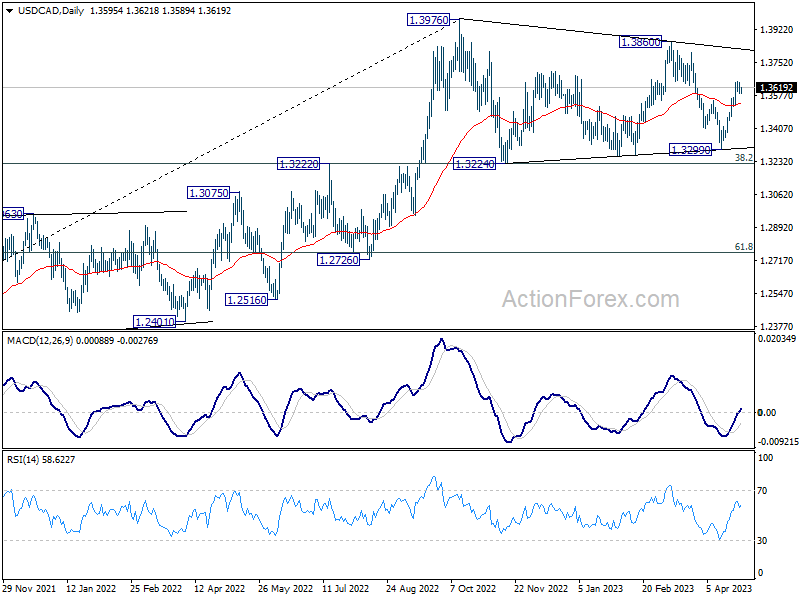

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3571; (P) 1.3609; (R1) 1.3629; More....

A temporary top should be conformed at 1.3650 with current retreat. Intraday bias in USD/CAD is turned neutral first. Overall, the correction pattern from 1.3976 could have completed with three waves to 1.3299. Above 1.3650 will resume the rise from 1.3299 to 1.3860/3976 resistance zone. Decisive break there will resume larger up trend. However, break of 1.3521 support will dampen this bullish case.

In the bigger picture, the up trend from 1.2005 (2021 low) is still in progress. Break of 1.3976 will confirm resumption and target 61.8% projection of 1.2401 to 1.3976 from 1.3261 at 1.4234. Firm break there will pave the way to long term resistance zone at 1.4667/89 (2016, 2020 highs). On the downside, sustained break of 55 W EMA (now at 1.3302) is needed to confirm medium term topping. Otherwise, outlook will remain bullish even in case of deep pull back.

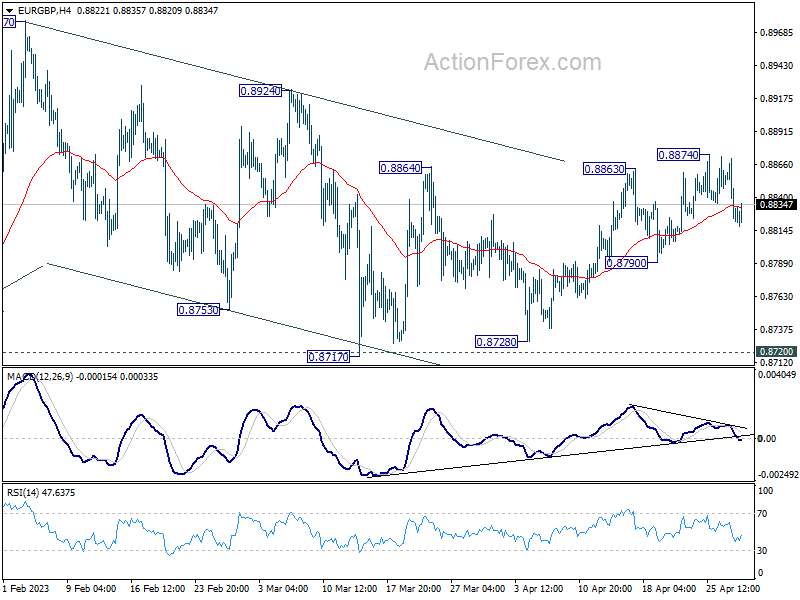

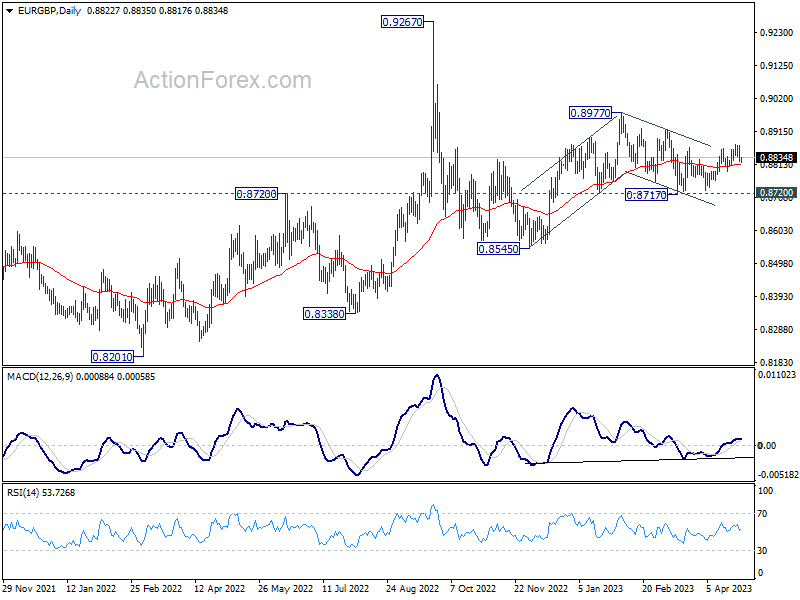

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8807; (P) 0.8840; (R1) 0.8856; More...

Intraday bias in EUR/GBP remains neutral first and further rally is mildly in favor as long as 0.8790 support holds. Choppy decline from 0.8977 could have completed already. Above 0.8874 will target 0.8924 resistance first. Firm break there will target 0.8977 high next. However, break of 0.8790 will turn bias back to the downside for retesting 0.8717 support again.

In the bigger picture, outlook remains rather mixed for now, except that price actions from 0.9267 (2022 high) are part of the long term range pattern from 0.9499 (2020 high). With 0.8720 support intact, rise from 0.8545 is in favor to continue through 0.8977. However, firm break of 0.8720 will argue that such rebound has completed, and open up deeper fall through this support level.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6573; (P) 1.6680; (R1) 1.6824; More...

Intraday bias in EUR/AUD remains neutral for consolidation below 1.6785. Downside of retreat should be contained by 1.6444 resistance turned support to bring rally resumption. On the upside, break of 1.6785 will resume larger up trend to 100% projection of 1.4281 to 1.5976 from 1.5254 at 1.6949.

In the bigger picture, the solid break of 1.6389/6434 cluster resistance (38.2% retracement of 1.9799 to 1.4281 at 1.6389) argues that whole down trend from 1.9799 (2020 high) has completed at 1.4281 (2022 low). Further rise should be seen to 61.8% retracement at 1.7691 next. For now, outlook will stay bullish as long as 1.5976 resistance turned support holds, even in case of deep pull back.

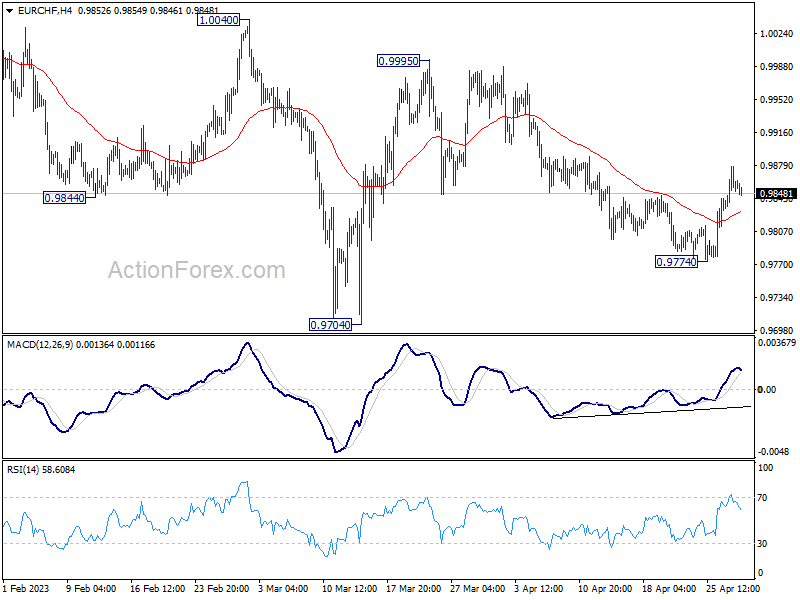

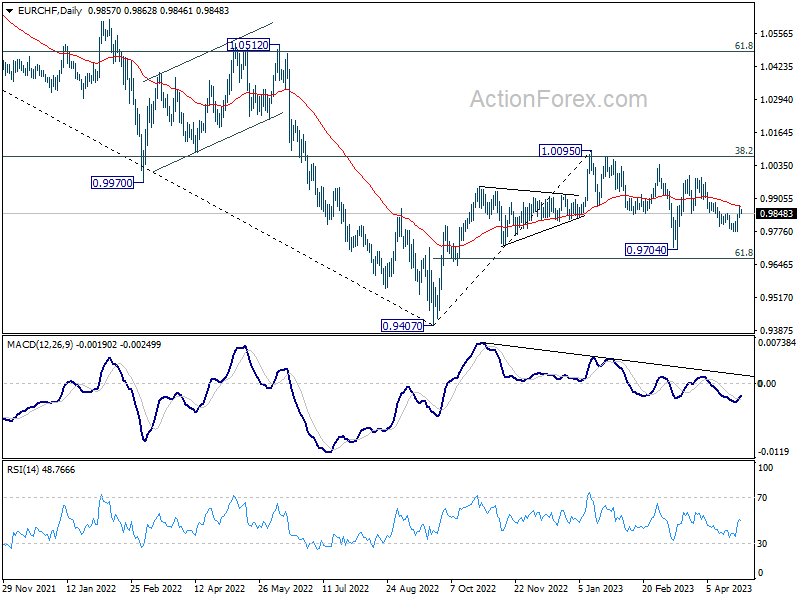

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9839; (P) 0.9859; (R1) 0.9885; More...

Intraday bias in EUR/CHF stays on the upside at this point. Decline form 0.9995 should have completed at 0.9774 already, well ahead of 0.9704 low. Current development also revives the case that whole correction from 1.0095 has completed at 0.9704. Sustained trading above 55 D EMA (now at 0.9875) will affirm this bullish case, and target 0.9995 resistance next.

In the bigger picture, prior rejection by 55 W EMA (now at 0.9989) and 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. That is, down trend from 1.2004 is not completed yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

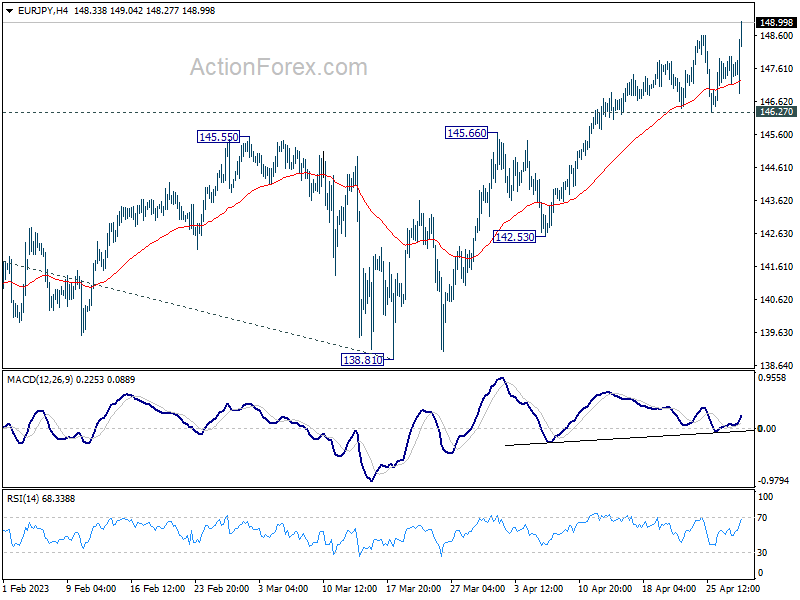

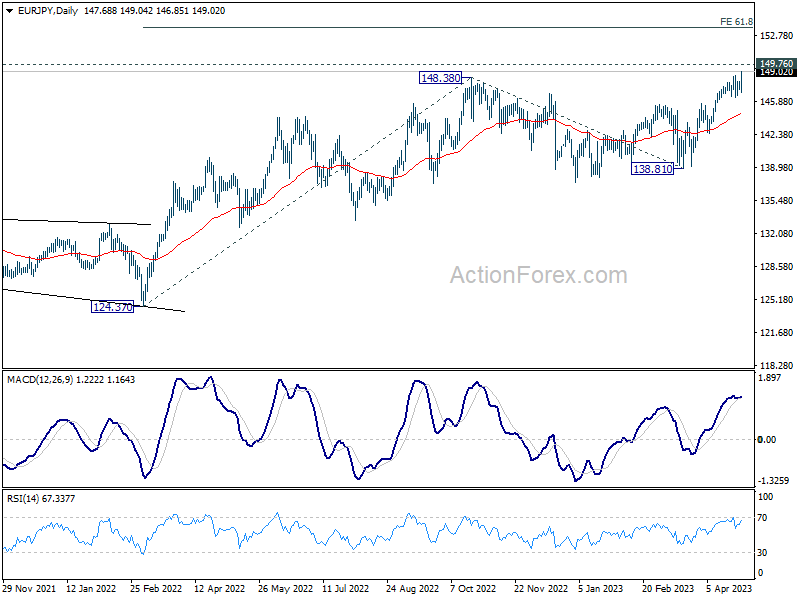

EUR/JPY Daily Outlook

Daily Pivots: (S1) 147.27; (P) 147.63; (R1) 148.11; More....

EUR/JPY's rally finally resumes and the break of 148.38 resistance should now confirms resumption of larger up trend. Intraday bias is back on the upside for 149.76 long term resistance next. Break will target 153.64 projection level. Meanwhile, outlook will now stay bullish as long as 146.27 support holds, in case of retreat.

In the bigger picture, as long as 55 W EMA (now at 140.70) holds, larger up trend from 114.42 (2020 low) is still in progress for 149.76 long term resistance (2014 high). Decisive break there will resume long term up trend from 94.11 (2012 low). Next target is 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64. This will remain the favored case as long as 138.81 support holds.

Bank of Japan Left Key Parameters of Policy Unchanged But Changed Forward Guidance

Markets

US Q1 GDP figures came in as somewhat of a shocker for those betting that it will soon be back to lower rates for the Fed after delivering a final 25 bps rate hike next week. For the first time in over a month, markets reacted to underlying dynamics rather than to headline weakness. Quarterly annualized growth of 1.1% came in below consensus (1.9% Q/Qa) but the key consumption component accelerated to a 2-y high of 3.7% Q/Qa. Importantly, there was a very big drag from inventories with business investments being the only real weak point. Core PCE deflators accelerated unexpectedly from 4.4% Q/Q to 4.9% Q/Q, the fastest since Q1 2022. So the data suggest that the US economy remains more resilient, inflation more stubborn and so far signs of the feared credit crunch are absent. In turn, these could result in some hawkish linings in the Fed statement and Powell’s press conference next week which will go against current market positioning (rate cuts later this year). March income and spending data and the Q1 employment cost index are likely the centerpieces at today’s US eco calendar and will be interpreted in a same way as US GDP numbers yesterday. Monthly PCE deflators (March) can be derived after yesterday’s quarterly number with the April Chicago PMI likely to play second fiddle as well.

US Treasuries underperformed German Bunds. US yields closed 4.8 bps (30-yr) to 11.9 bps (2-yr) higher. The US 2-yr and 10-yr yields respectively closed above 4% and 3.5%. Changes on the German curve ranged between +4.2 bps (30-yr) and +6.5 bps (3-yr). US stock markets rallied 1.57% (Dow) to 2.43% (Nasdaq). Yesterday’s data were strong enough to put aside imminent recession fears, but not strong enough to prompt the Fed into an extra rate hike for example in June. The US dollar loved the immediate interest rate response with EUR/USD diving from 1.1050 to 1.10, but the greenback struggled with positive risk sentiment during the US session and with the same dilemma as stocks. For EUR/USD to end the week below 1.10, it will probably need to come via a weaker euro (not our base case). Today’s EMU calendar eyes attractive with Q1 GDP figures, but also national inflation numbers in Germany, France and Spain. Especially the direction of core inflation will be closely watched and could be decisive in tilting the odds (currently 80-20) to either a 25 bps or a 50 bps ECB rate hike next week. We stick with our 50 bps rate hike call on grounds of trends in core and wage inflation, the still relatively low current interest rate level, a resilient economy and tight labour market and backed by several ECB members putting the possibility on the table. Apart from the April EMU CPI number, the ECB’s Q1 credit and lending survey will be released as well next week ahead of Thursday’s policy meeting.

News Headlines

In the first meeting presided by the new Governor Ueda, the Bank of Japan left the key parameters of its policy unchanged but changed its forward guidance. The short-term policy rate remains at -0.1%. The BOJ in its Yield Curve Control policy will continue to buy an unlimited amount of government bonds to keep the 10-y government bond yield at around 0%, with a tolerance band for the yield to deviate by 50 bps plus or minus the target level. In its forward guidance, the BOJ deleted the reference to the impact of Covid 19. It also didn’t repeat that ’it expects short- and long term policy interest rates to remain at their present or lower levels’. The guidance now reads: ‘The bank will continue to maintain stability of financing, mainly for firms, and financial markets, and will not hesitate to add easing measures if necessary’. The BoJ also announced to conduct a broad-perspective review of monetary policy as this policy over the previous 25 year has resulted in various easing measures that have interacted with and influenced with areas of Japan’s economic activity, prices and the financial sector. The BOJ indicates a planned time for the review of around one to one and a half years. The Japanese 10-y government yield dropped from 0.485% to 0.43% after the BOJ policy announcement. The yen weakened with USD/JPY trading near 134.75 rising from the 134 area. Before the announcement of the BOJ policy decision, Tokyo April CPI figures printed again stronger than expected with the headline rising from 3.3% Y/Y to 3.5% Y/Y. Core inflation (ex food and energy) even accelerated from 3.4% to 3.8%. Other data series showed better than expected March retail sales (0.6% M/M and 7.2% Y/Y) and above consensus March production data (0.8% M/M and -0.7% Y/Y).The jobless rate on the other hand rose to 2.8% from 2.6%, but the participation rate also improved from 62.1% to 62.6%.

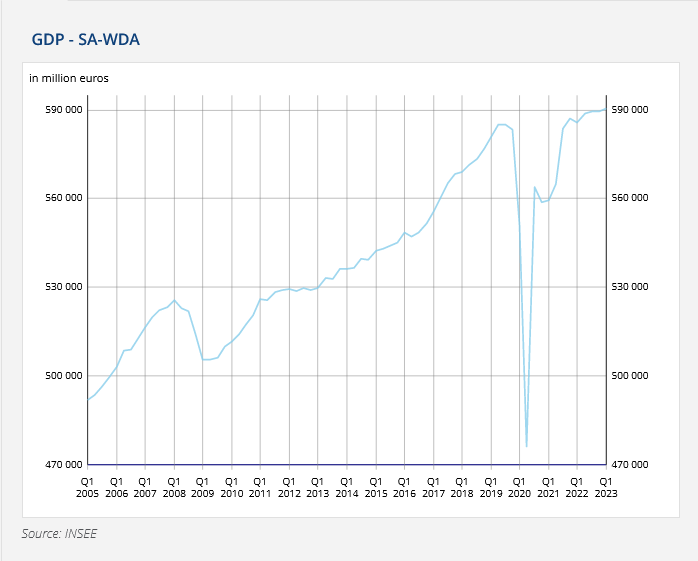

France’s Q1 GDP sees modest growth of 0.2% qoq

France's Q1 GDP growth came in at a modest 0.2% qoq, slightly outperforming market expectations of 0.1% qoq.

Final domestic demand (excluding inventories) contributed negatively to GDP growth, albeit less so than in the previous quarter (-0.1 points in Q1 2023 after -0.4 points). This was due to household consumption stabilizing (0.0% after -1.0%), while gross fixed capital formation (GFCF) experienced a minor decline (-0.2% after 0.0%).

In contrast, foreign trade provided a positive contribution to GDP growth (+0.6 points after +0.2 points). Imports decreased this quarter (-0.6% after +0.1%), while exports remained strong (+1.1% after +0.9%).

Lastly, the contribution of inventory changes to GDP growth was negative this quarter (-0.3 points after +0.2 points in Q4 2022).