Sample Category Title

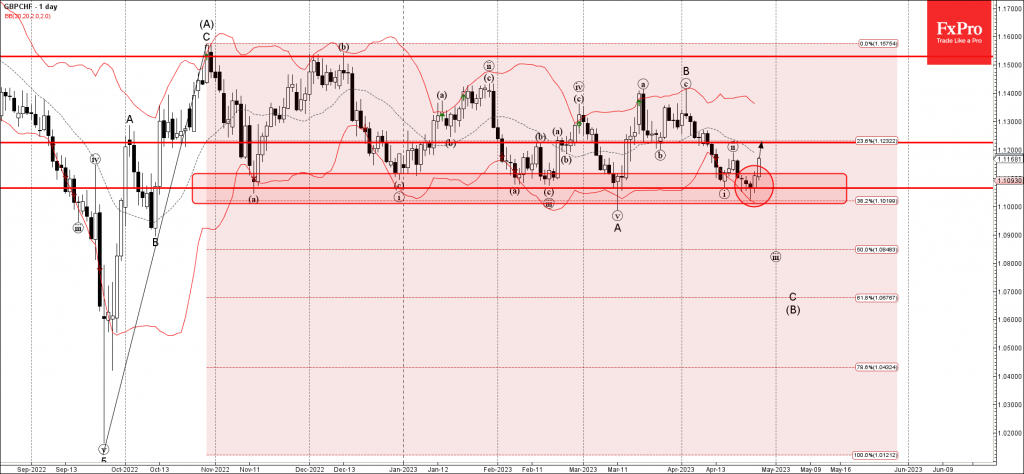

GBPCHF Wave Analysis

- GBPCHF reversed from long-term support level 1.1065

- Likely to rise to resistance level 1.1225

GBPCHF currency pair recently reversed up from the long-term support level 1.1065 (which has been reversing the pair from November), standing near the lower daily Bollinger Band.

The upward reversal from the support level 1.1065 stopped the C-wave of the medium-term ABC correction (B) from October.

Given the strong Swiss franc sales, GBPCHF currency pair can be expected to rise further toward the next resistance level 1.1225.

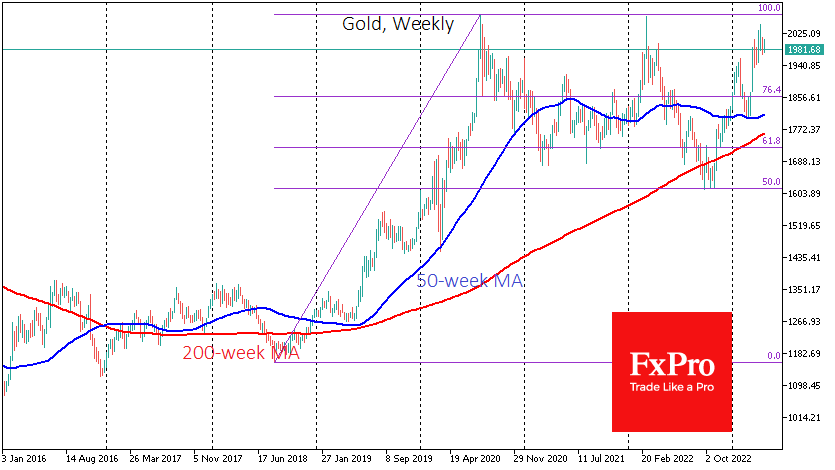

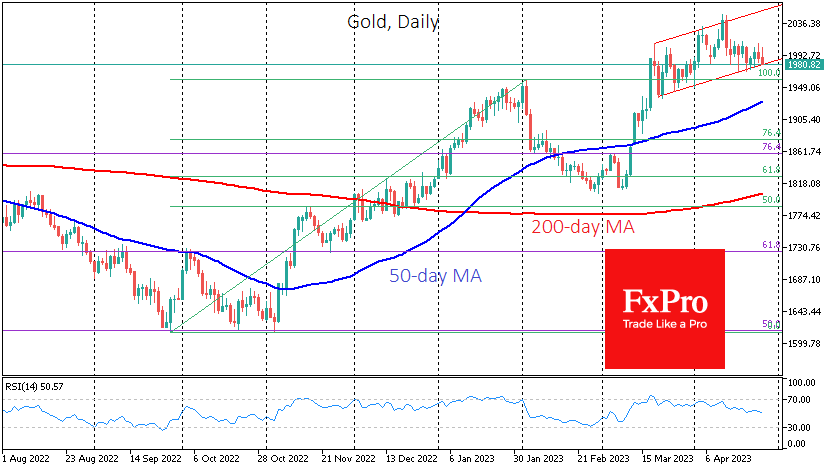

A Gold Bull cycle is not over yet

Gold has flirted with $2000 three times in the last three years. This time, however, it is more likely that the bulls will soon be able to hold higher for longer, as gold’s rally now has a slightly different character.

In 2020, interest in gold was an investor response to unprecedented monetary and fiscal easing. When the price reached the psychologically important $2000 level, the gold rally was more than 70% of the cycle low. The rally’s most furious phase began when gold broke through significant resistance at $1800, but the new buying potential was largely exhausted. As a result, the liquidation of short positions that saw gold rewrite its all-time high at $2075 was followed by a prolonged period of profit-taking, despite the continued rally in other risky assets.

In early 2022, gold was in demand, first on fears of capital depreciation and soon after on geopolitics, and we saw a rise of over 15% in less than five weeks. It then failed to make new all-time highs and peaked at $2072. A decisive monetary policy reversal by the Fed and other central banks dragged the price down. Gold bottomed in September-October on signals that the Fed was slowing the rate hikes and that interest rates might soon peak.

We then saw a very rapid return to historical highs – much faster than the other asset classes, which fell in 2022 and bottomed around the same time.

Early last month, we saw a more reliable reason to buy gold – the market’s reaction to the banks’ problems. Gold gained traction as the end of the tightening cycle approached. Moreover, bank problems leading to economic growth issues are a significant reason for the Fed to turn its policy towards easing.

Gold rallied sharply in March, and the market possibly unwound this overheating in the recent 3% correction from the $2048 highs. The sequence of lower highs in 2020, 2022 and 2023 is worrying. But the series of higher local lows over the past five weeks is worth noting. Moreover, all this consolidation is taking place at higher levels than in previous similar episodes, reflecting more interest in buying gold.

The historical tendency for the dollar to weaken at a similar stage in the monetary cycle is also worth considering.

In addition to technical analysis, gold buying is also justified by geopolitics, which remains tense and keeps the idea of a move towards supranational stores of value.

Fed Preview: One More Hike – Cuts Still Far Away

Fed Preview: One More Hike - Cuts Still Far Away

- We expect the Fed to deliver a final 25bp hike next week and then maintain the Fed Funds rate at 5.00-5.25% for the remainder of the year.

- Powell is unlikely to close the door for further hikes, but even with nominal rates on hold, we expect the monetary policy stance to continue tightening towards H2.

- We see modest upside risks to short-term yields, i.e. out to 6M, but with no updated projections, markets' focus will remain on macro data.

We expect the Fed to deliver a final hike of the tightening cycle bringing the Fed Funds Rate to 5.00-5.25%. With no updated projections and markets already pricing in around 20bp ahead of the meeting, the main emphasis will be on Powell's verbal guidance.

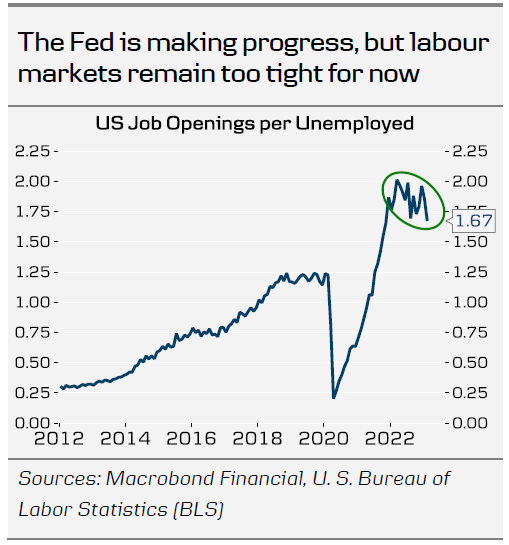

We doubt Powell will fully close the door for further hikes in the summer, and see some room for the markets to speculate with higher rates. The Flash PMIs suggested that banking sector turmoil's immediate negative consequences for the broader economy have been limited, yet December Fed Funds pricing remains 110bp below early March peak.

We still think maintaining rates at modestly restrictive levels for longer strikes the best balance between avoiding a hard landing and ensuring inflation comes down for good. As service sector inflation remains too fast, we see little room for easier policy anytime soon. Minutes from the February meeting showed that FOMC participants are well aware of the risk of allowing financial conditions to ease prematurely. In the March SEPs, 7 out of 18 preferred hiking rates above 5.00-5.25% even amid the high uncertainty at the time.

Even if the Fed ends the hiking cycle next week, we expect it to tighten monetary policy further rest of the year. The market discounts around 60-65bp of rate cuts before the end of the year. Hence, the inverted curve allows the Fed to tighten monetary policy passively by keeping the Fed Funds rate unchanged. In addition, short-term consumer inflation expectations have been on a downwards trend. A further drop in inflation expectations will push real interest rates higher and deliver further passive monetary tightening. Finally, we look for the Fed to continue quantitative tightening even if the hiking cycle ends.

In the press conference, Powell will likely be asked about the debt ceiling, but we think he will simply reiterate that it is the congress' duty to ensure US avoids a default. A failure to do so could lead to a sharp tightening in financial conditions, which would naturally warrant a reaction from the Fed, but hinting about potential support would create moral hazard.

For markets, we do not expect the meeting to be a game changer, as the pricing for the summer meetings is well in line with our view, and as the renewed uncertainty around First Republic Bank this week reminded that visibility much beyond remains low.

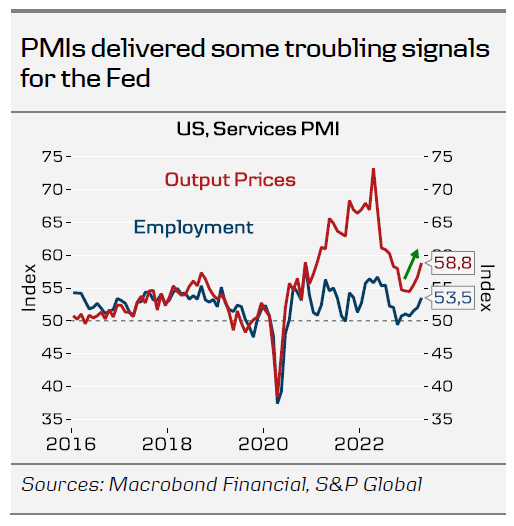

Rather, we will pay close attention to ISM, JOLTs and the Jobs Report, where we expect NFP to settle at a moderating, yet still upbeat +200k on the back of recovering labour supply and rising PMI employment indices. We generally see some upside risks to short USD rates, and forecast lower EUR/USD towards the latter half of the year, but next week the ECB meeting will likely be relatively more important for the latter.

ECB Preview: The Art of Compromise

Next week, the ECB will meet to deliver another rate hike in its hiking cycle that started in July last year. This time, the question is whether it will slow the hiking pace to 25bp or continue to hike once more by 50bp. We believe it will be a 50bp compromise deal with no specific forward guidance (nor guidance on balance sheet normalisation in H2 yet), but repeating a data-dependent approach to future policy decisions.

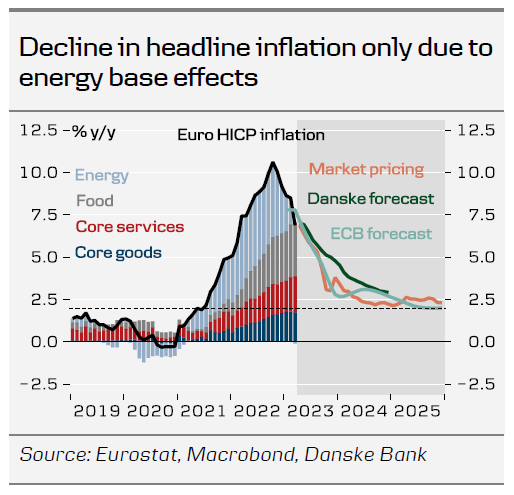

Economic developments since the ECB meeting, coinciding with the banking turmoil, have shown resilient economic activity and another record-high core inflation print. Headline inflation has declined on the back of base effects, but the stickiness of core inflation and wages should pave the way for another 50bp rate hike, in our view.

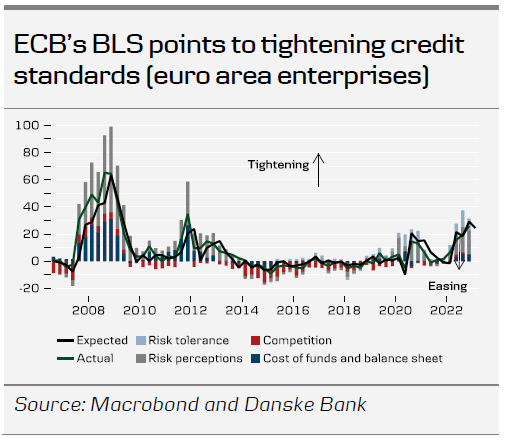

On Tuesday 2 May, the ECB and Eurostat will publish the last and important data releases ahead of the meeting. The Bank Lending Survey (BLS) and loan growth data will likely deteriorate compared with previous releases, while inflation is set to bring another high print (core around 5.7%). A significant surprise in any of the releases could change the market pricing and hence probabilities of a 25bp or 50bp rate hike outcome.

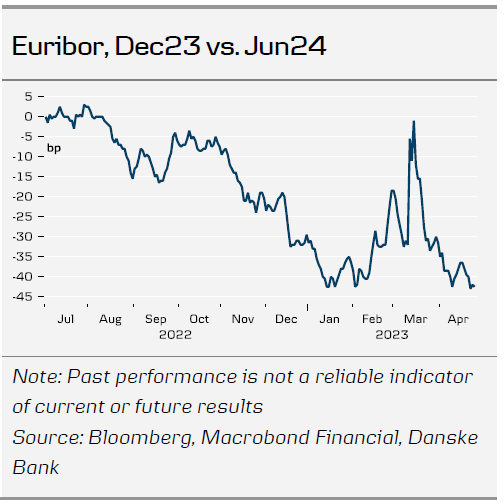

Refraining from delivering a 50bp rate hike at this meeting is set to result in a dovish market reaction, with easing financial conditions to follow. We recommend to receiving the Dec-23 euribors and pay the Jun-24 euribors at -42bp with a target of -20.

Strong services economy keeps ECB's inflation concerns alive

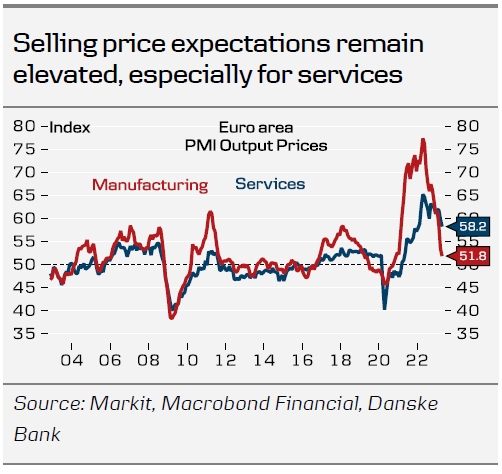

Despite banking sector jitters and the ECB's ongoing tightening efforts, the euro area economy has continued to show remarkable resilience since the March meeting. Business surveys suggest the economy picked up momentum at the start of Q2, with the services sector in particular (accounting for 73% of GDP) driving the ongoing improvement. The labour market remains tight and firms' hiring activity continues to increase, especially amid services providers, where jobs growth picked up to the fastest rate since July 2007. This is pressuring wages, as demonstrated by the latest collective wage agreement for German public sector employees, which expects wage growth of 11.5% over the next two years. The decline in headline inflation in recent months remains almost entirely due to energy base effects, while core and food prices have continued their uptrend. With this dynamic, the ECB can hardly declare 'mission accomplished' on inflation in our view. With easing input cost inflation, consumer goods inflation showed signs of peaking in March. But the same cannot be said for services inflation, where rising wage costs play a greater role, taking over as the prime core inflation driver. Selling price expectations and most underlying inflation measures point to a peak in core inflation in the next 1-2 months, but they also suggest 'sticky' core inflation will remain a concern for the ECB for some time, setting the scene for further rate hikes. We still expect the ECB's monetary tightening to take its toll on the economic outlook (see Nordic Outlook – Unchartered territory, 4 April), but in contrast to markets, our forecasts show core inflation still above the ECB's target by the end of 2024, with the green transition and higher than expected wage growth still presenting upside risks.

2 May releases and banking turmoil

The March monetary policy meeting took place at the height of the banking turmoil last month. A key discussion point at the May meeting will therefore be how much tightening of financial conditions the banking turmoil in itself has triggered. On Tuesday 2 May, the ECB and Eurostat will publish the last and important release ahead of the meeting. The upcoming Bank Lending Survey has received significant attention by the GC members in recent communication, as they want to see the results before making up their mind on the size of the rate hike. We take it as given that the BLS will point to tightening credit standards, as the ECB is already in a tightening cycle, which means that we see the focus of this BLS to be on what additional tightening the recent turmoil has added. On 2 May we also get the loan growth data for March, which we also view as important for the decision, as the ECB mulls the transmission of monetary policy to the real economy. A significant surprise in any of the releases could change the market pricing and hence probabilities of a 25bp or 50bp rate hike outcome. If the BLS and the risk perception aspect as well as the loan growth developments to March deteriorate substantially, we see markets pricing out the probability of a 50bp rate hike, while a rise in underlying inflation would lead to an upward revision of the rate hike size, beyond 40bp.

A 'dovish' 50bp or 'dovish' 25bp hike

There should be little doubt that any ECB decision at the coming meetings will be a compromise. At the March meeting a 'very large majority' supported the 50bp rate hike and comments since then from GC members such as Stournaras, Panetta, and Visco call for a more cautious approach to monetary policy tightening. While only the most hawkish GC member Holzmann has voiced clear support for 50bp, the members of the 'hawkish camp' have said that a 50bp rate hike should be considered. In light of the incoming data, we see that option to gain the most support. However, that also means that any decision taken at the upcoming meetings will not be unanimous, which we also discussed in COTW: Unanimity is utopia, 21 April. This divergence of views will likely keep realised volatility in markets high in the short-term.

If President Lagarde wants to send a hawkish signal, we believe a 50bp rate hike is a prerequisite, but that alone is not sufficient as markets are forward looking by nature. That means that she also needs to back it up with hawkish arguments on the labour market, wage growth, and the stickiness of underlying inflation. But even in that case, we see a risk of markets reacting with lower yields, as this will likely be the final 50bp rate hike from the ECB. A 50bp rate hike would implicitly also be a signal for a July hike in our reading. Hence, the risk for lower medium-to long-term rates, irrespective of the hiking, is prominent, in a bearish flattening move of the curves. If the ECB chooses to go for a 25bp rate hike, we also see the risk for a dovish market interpretation with a bullish steepening, given that the ECB has refrained from giving guidance for the coming meetings, and thereby letting the prevailing market narrative of lower rates / central bank pivot continue. With a 25bp rate hike, we find it difficult for Lagarde to communicate a rate hike beyond June, which could take around 15bp out of the peak policy rate pricing, and in this case we see further lowering on the real rates and as such easing of the monetary policy stance.

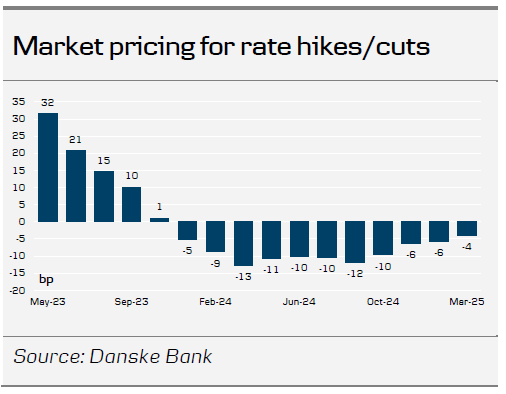

70% probability of 25bp and 30% probability for 50bp

Markets are currently pricing 32bp for next week's meeting, well below our baseline expectation of a 50bp rate hike. Looking beyond the most imminent meetings with 21bp for June and 15bp for July, the peak policy rate is priced to be 3.78% after summer, which we find to be on the low side. At the same time, markets are pricing a sharp rate cut process to commence next year, where markets are pricing 82bp altogether, and more than half of that already in H1 24. We like to pay that segment (for less rate cuts), and therefore recommend to receiving the Dec-23 euribors and pay the Jun-24 euribors at -42bp with a target of -20 and a stop loss of -52bp. We remain open for further rate cuts to come in September.

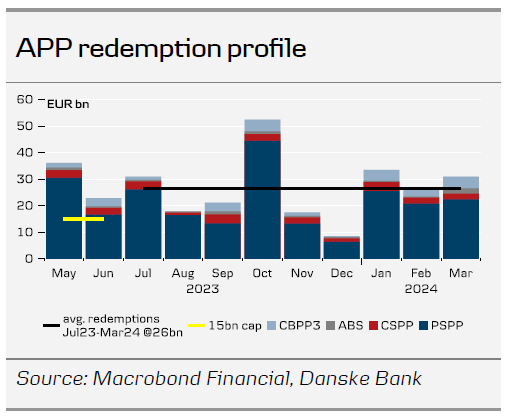

No discussion of future decisions

At the March meeting, the ECB refrained from giving explicit guidance for the May policy meeting, but outlined the reaction function that consists of 1) its assessment of the inflation outlook in light of the incoming economic and financial data; 2) the dynamics of underlying inflation; and 3) the strength of monetary policy transmission. We do not expect firm guidance for June to be delivered next week. That also means no guidance for the APP bond holding normalisation at this meeting, but a discussion and a decision to be announced at the June meeting. At that meeting, we expect a full end to APP reinvestments starting 1 July until the first rate cut from the ECB (which we pencil in for summer 2024). This amounts to an increase from on average EUR15bn to EUR26bn/month. Earlier this month, sources reported that a growing consensus in the GC was for a full end to APP reinvestments. Note that the PEPP reinvestments in full are still expected at least until December 2024– in line with current guidance.

FX reaction will likely be EUR positive in case of a 50bp rate hike

A 50bp rate hike will likely contribute to a broad EUR appreciation on impact, although it depends on the sequential growth outlook priced by markets.

The EUR/USD has been on an upward trajectory over the past two months supported by general growth optimism in the euro area, likely fuelled by the reopening in China, implying significant outperformance in euro area risk assets. Furthermore, lower energy prices and narrowing of rates spread between the US and the euro area have likely also been a tailwind for the cross, especially the latter.

Overall, we still have a bearish stance on the EUR/USD in the medium- to long-term, as rate hiking cycles generally are approaching an end, we think focus will increasingly turn from relative rates differentials to relative growth differentials. We are particularly sceptical about the longevity of the euro area optimism, although we acknowledge that there is a possibility of it continuing in the short-term, adding to tactical topside risk in EUR/USD in conjunction with further narrowing of relative rates spread on the back of the ECB meeting. That said, we still expect the EUR/USD to head lower based on relative terms of trade, real rates, and relative unit labour costs. The Fed meeting on 3 May – the day before the ECB meeting – is also worth having in mind, where our expectation of a 25bp rate hike is almost fully priced by markets. We forecast the cross to remain range bound in the next 1-3M, but expect it to decline to 1.06 and 1.03 on a 6-12M horizon.

Sunset Market Commentary

Markets

Since the early March collapse of Silicon Valley Bank, investors reacted in an asymmetric manner to eco figures. They cherrypicked the slightest disappointments to strengthen their case of a nearby Fed policy rate peak and policy rate cuts starting in H2 2023 to accommodate the economy. Today, in a change of heart, they forfeited on the opportunity to boost their dovish cases after US GDP grew less than expected in Q1 (1.1% Q/Qa from 2.6% in Q4 2022 and vs 1.9% forecast). A look under the hood showed personal consumption accelerating from 1% Q/Qa to 3.7% Q/Qa (vs 4% expected, but nevertheless the fastest pace since Q2 2021) with joe sixpack spending on both goods and services. The consumer does hold up well despite inflation, the Fed’s tightening trajectory and uncertainty around financial stability. A very tight labour market, wage growth and a pandemic build-up in savings provide sufficient counterweight for the moment. Underlying US Q1 GDP was also much stronger when taking into account that inventories took off 2.26 percentage points from the growth rate. Government spending (especially defense) and trade contributed a bit to growth with business investment the only real disappointment. Q1 price deflators printed on the topside as well with especially core PCE rising by the fastest pace since Q1 2022 (4.9% Q/Q from 4.4% in Q4 2022 and vs 4.7% expected). They suggest upside risks to tomorrow’s March monthly deflators. Simultaneously with GDP figures, US weekly jobless claims increased less than expected (230k vs 248k forecast from 246k). Solid underlying growth and stubborn price pressure pulled US Treasuries lower, underperforming German Bunds. US yields currently add 2.6 bps (30-yr) to 8.3 bps (2-yr). The US 2-yr yield turns back above 4% with the 10-yr yield back above 3.5%. German yields add 3 to 3.5 bps across the curve. US eco data and yield dynamics pulled EUR/USD from levels around 1.1050 down to 1.10. We only expect a longer stay below 1.10 should tomorrow’s national EMU CPI data print on the soft side thereby reducing the market implied probability of a 50 bps ECB rate hike next week (currently around 25%). US equity futures already pointed to a positive stock market opening following stronger Q1 Meta earning and got an additional boost on US economic strength. They open up to 1% higher for Nasdaq.

News & Views

Belgian inflation decelerated further from 6.67% to 5.60% in April. Energy decreased sharply again, declining 17.08% y/y and subtracting 2.36% of total inflation. Food prices still add 3.19 ppts (16.64% y/y but slightly lower than the 17.02% last month) and are by far the biggest contributor to headline inflation. Core inflation for the first time since September 2021 eased, from 8.57% to 8.28% y/y. Price pressures in services were slightly less intense than in March, rising 6.80% vs 7.06%. If April indeed marks the start of the disinflationary process (of core inflation), question now is how quickly (or not) it runs. In other Belgian news, GDP expanded at 0.4% q/q in 2023 Q1 with the pace picking up from the previous quarter’s 0.1%, the NBB’s preliminary estimate revealed. Belgium’s economy is now 1.3% bigger than the same period last year. The services sector outperformed, with value added rising 0.7%, followed by construction (0.4%). Value added in the industrial sector shrunk 0.6%.

Swedish GDP grew 0.2% q/q in Q1 of this year following a -0.6% contraction in 2022Q4. That’s more than the stagnation expected by analysts but slightly below the country’s central bank own estimate (+0.3% q/q). The economy grew 0.3% y/y in Q1. The numbers are a preliminary estimate, compiled with more limited statistics than the regular quarterly national accounts (due May 30). They do reveal economic momentum is slowing down. The monthly GDP reading in January still printed at a strong 1.6% m/m but was then followed by -1.1% in February and -0.2% in March. This suggests the Riksbank’s tightening efforts are gradually filtering through. It has, however, still some way to go with inflation at levels well above the 2% target. Just yesterday, the central bank lifted policy rates by 50 bps to 3.5% and, much to the SEK’s disappointment, only projected an additional 25 bps hike in July or September. The Swedish crown shrugged at today’s numbers with EUR/SEK hovering near multiyear lows at around 10.38.

U.S. Growth Slips to 1.1% in Q1, Though Details Show a Strong Gain in Consumer Spending

Real GDP expanded by 1.1% quarter-on-quarter (q/q, annualized) in the first quarter of 2023 – a marked deceleration from last quarter's 2.6% – and well below the consensus forecast of 1.9%.

Consumer spending grew by a robust 3.7% – a meaningful acceleration from Q4's gain of 1.0%. Spending on goods rose 6.5%, largely the result of a sharp rebound in durables (+16.9%), while non-durables edged higher by just 0.9%. Service spending was up by 2.3%.

Non-residential business investment expanded by a modest 0.7%, as a pullback in equipment spending (-7.3%) was more than offset by a robust gain in structures (+11.2%) and more modest growth in intellectual property products (+3.8%).

Residential investment declined for an eighth consecutive quarter - falling by 4.2%. That said, declines moderated in Q1 as home construction appeared to stabilize while home sales turned modestly higher.

Both exports (+4.8%) and imports (+2.9%) were higher last quarter, though a larger gain in the former meant that net trade made a small (+0.1 percentage point) contribution to headline growth.

Government spending rose 4.7%, thanks to gains at both the federal (+7.8%) and state & local (+2.9%) levels.

After making an outsized contribution to growth last quarter, inventory investment subtracted 2.3 percentage points from Q1 growth.

Core PCE – the Fed's preferred inflation metric – rose to 4.9% q/q (annualized) in Q1, slightly stronger than the consensus forecast of 4.7%.

Key Implications

First quarter GDP came in well below the consensus forecast, largely owing to an outsized decline in inventory accumulation. Putting that aside, final domestic demand rose by a robust 3.2% – a meaningful acceleration from last quarter's 0.7% gain.

Much of the strength on the domestic front was the result of a very strong reading on consumer spending. While warmer weather may have had some influence – particularly for January where there was an outsized gain in spending activity – a sturdy labor market alongside some easing in inflationary pressures are helping to support real household incomes and sustain a robust pace of consumer spending.

We have already started to see some evidence of cooling in the labor market, while other higher frequency data points indicate a further softening in economic activity heading into the second quarter. We expect these pressures to intensify over the coming months as the cumulative impact of higher interest rates and some tightening in bank lending standards exert a more meaningful drag on domestic demand, pushing growth to a near stall speed as early as Q2.

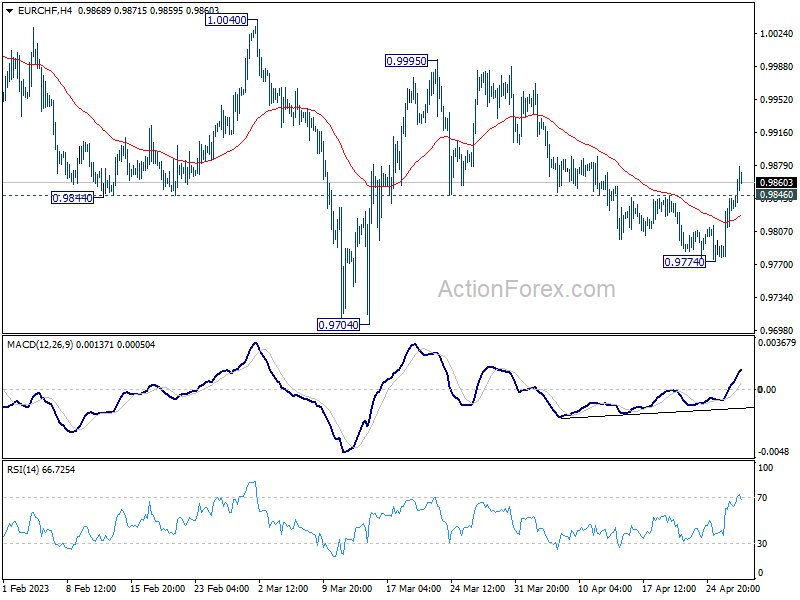

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9798; (P) 0.9821; (R1) 0.9864; More...

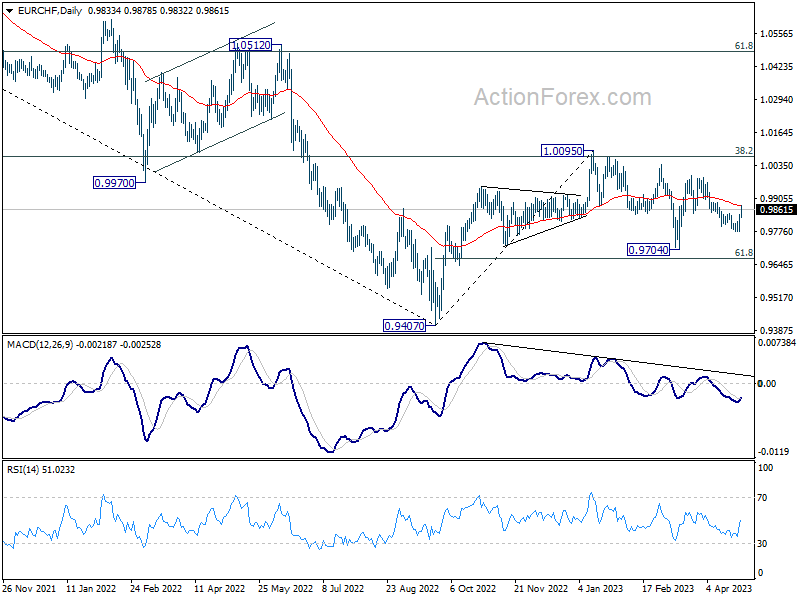

EUR/CHF's break of 0.9846 resistance suggests that fall form 0.9995 has completed at 0.9774, well ahead of 0.9704 low. The development also argue revive the case that whole correction from 1.0095 has completed at 0.9704. Intraday bias is back on the upside. Sustained trading above 55 D EMA (now at 0.9876) will affirm this bullish case, and target 0.9995 resistance next.

In the bigger picture, prior rejection by 55 W EMA (now at 0.9989) and 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. That is, down trend from 1.2004 is not completed yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

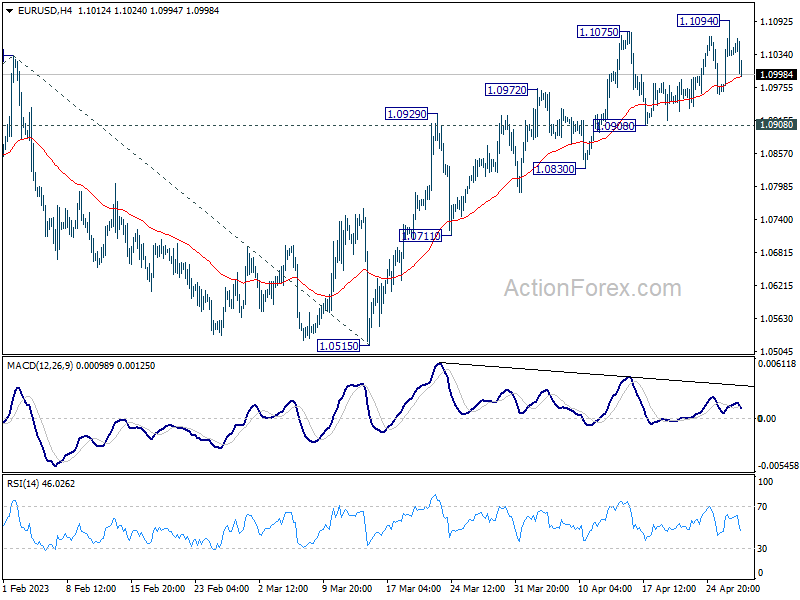

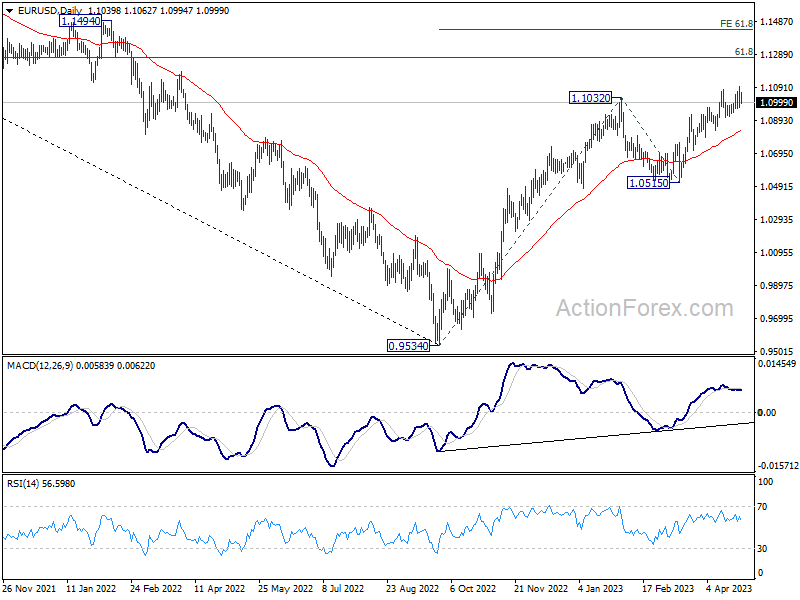

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0972; (P) 1.1034; (R1) 1.1100; More...

Intraday bias in EUR/USD is turned neutral with current retreat. Some consolidations could be seen first. But further rally is expected as long as 1.0908 support holds. Break of 1.1094 will resume larger up trend to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

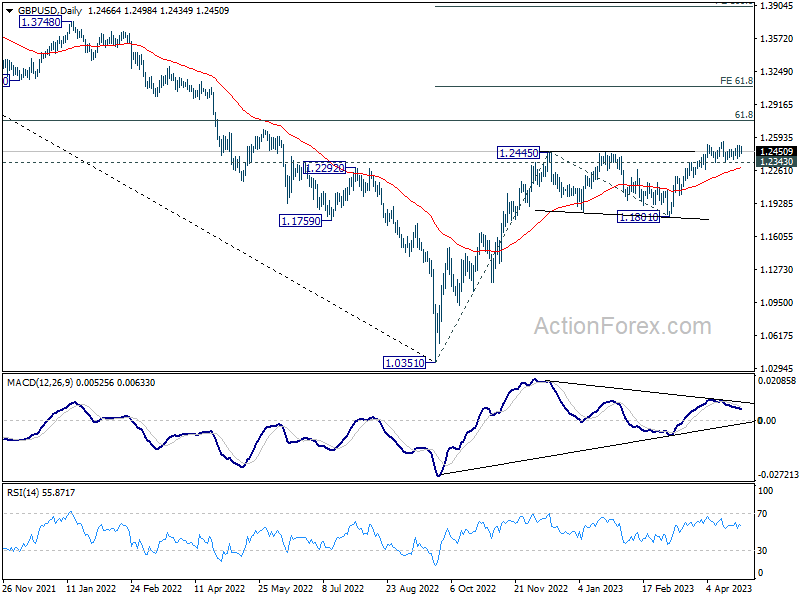

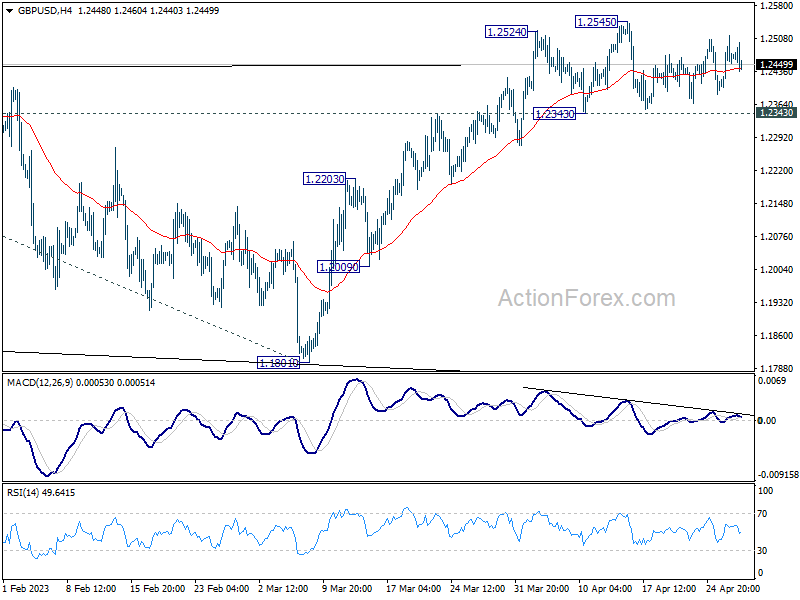

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2409; (P) 1.2462; (R1) 1.2521; More...

GBP/USD is staying in sideway consolidation and intraday bias stays neutral. Also, outlook remains bullish with 1.2343 support intact. On the upside, above 1.2545 will target 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. However, considering bearish divergence condition in 4H MACD, firm break of 1.2343 will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.