Sample Category Title

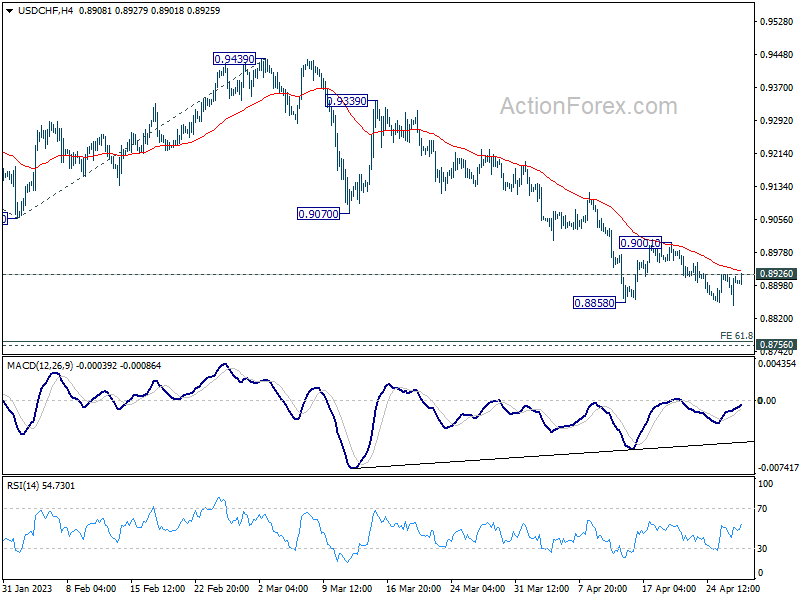

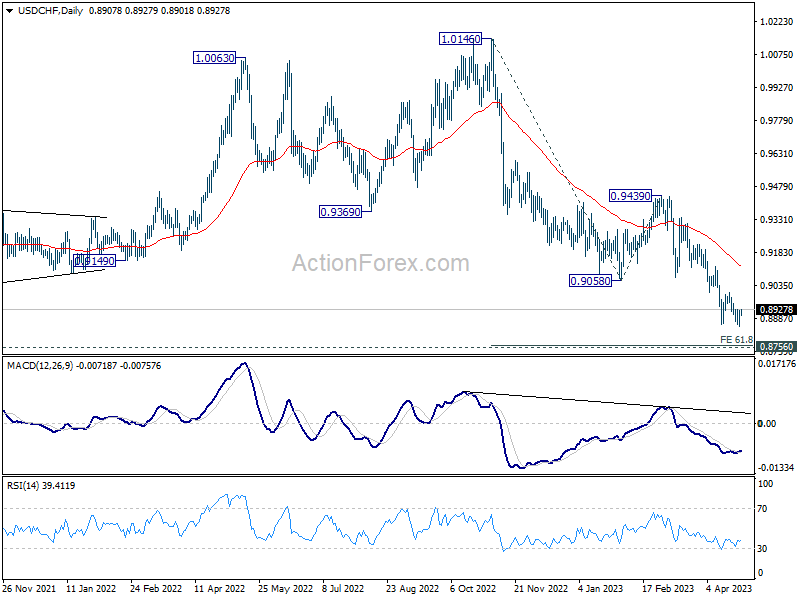

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8869; (P) 0.8897; (R1) 0.8943; More...

Intraday bias in USD/CHF is turned neutral again first with breach of 0.8926 minor resistance. On the downside, another decline through 0.8858 will resume the whole fall from 1.0146 to 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support. Strong support is expected there to bring rebound, at least on first attempt. On the upside, break of 0.9001 should confirm short term bottoming.

In the bigger picture, fall from 1.1046 (2022 high) is in progress for 0.8756 support (2021 low). But overall, this fall is still seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

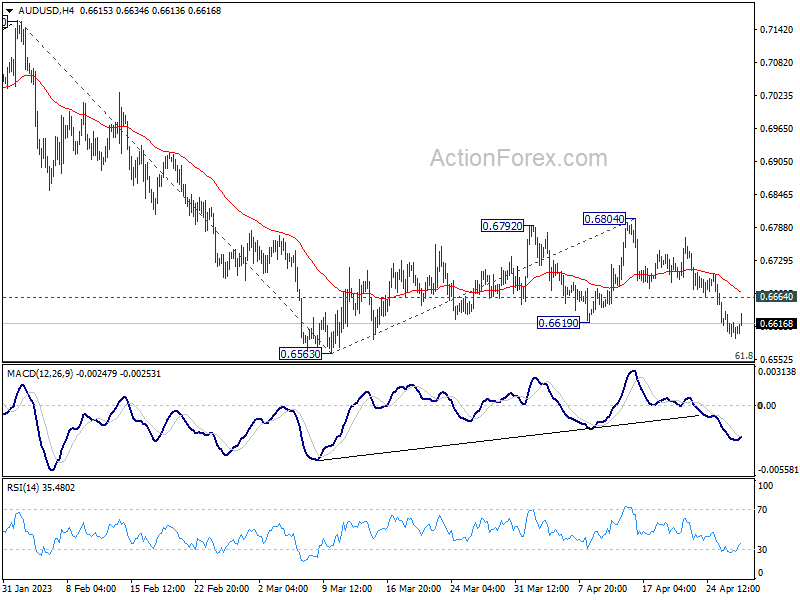

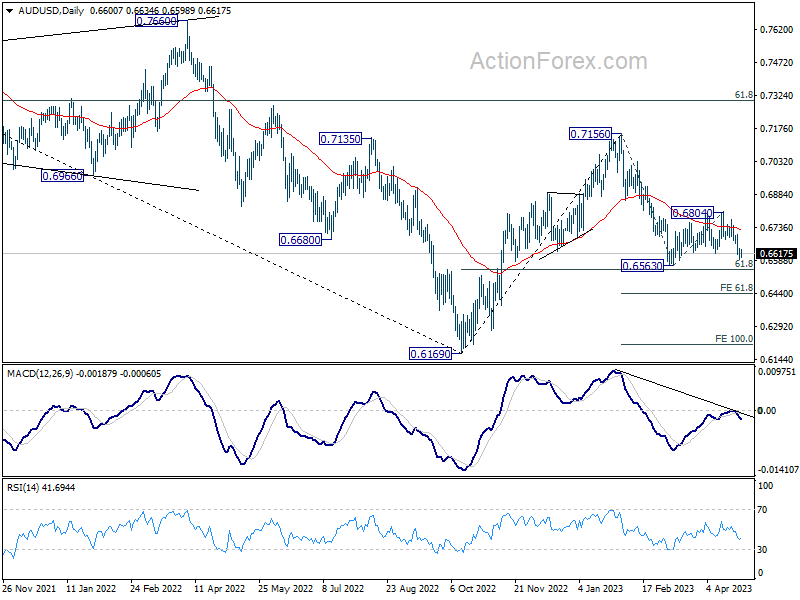

AUD/USD Daily Report

Daily Pivots: (S1) 0.6584; (P) 0.6611; (R1) 0.6631; More...

Intraday bias in AUD/USD remains on the downside despite some loss of downside momentum. Consolidation pattern from 0.6563 should have completed at 0.6804, and larger decline from 0.7156 is ready to resume. Firm break of 0.6563 will bring deeper decline through 0.6546 fibonacci level to 61.8% projection of 0.7156 to 0.6563 from 0.6804 at 0.6438 next. On the upside, though, above 0.6664 minor resistance will delay the bearish case and turn intraday bias neutral first.

In the bigger picture, as long as 61.8% retracement of 0.6169 to 0.7156 at 0.6546 holds, the decline from 0.7156 is seen as a correction to rally from 0.6169 (2022 low) only. Another rise should still be seen through 0.7156 at a later stage. However, sustained break of 0.6546 will raise the chance of long term down trend resumption through 0.6169 low.

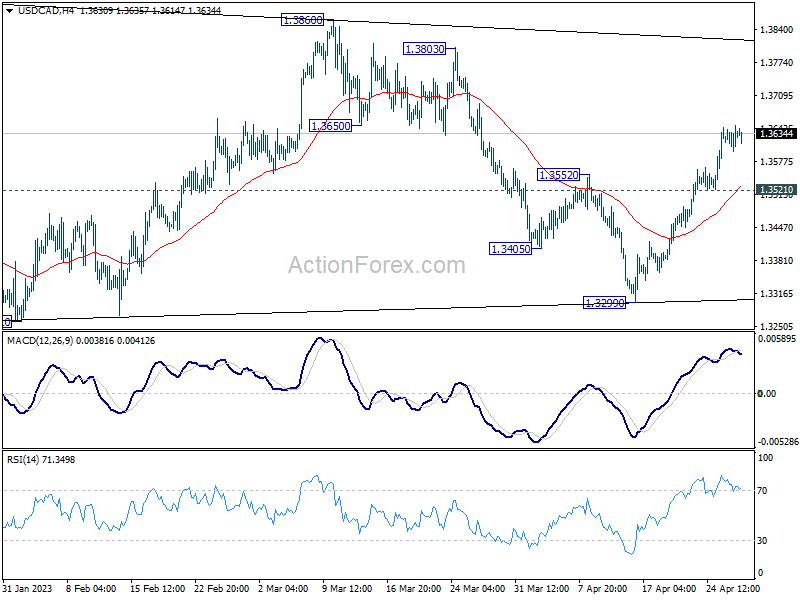

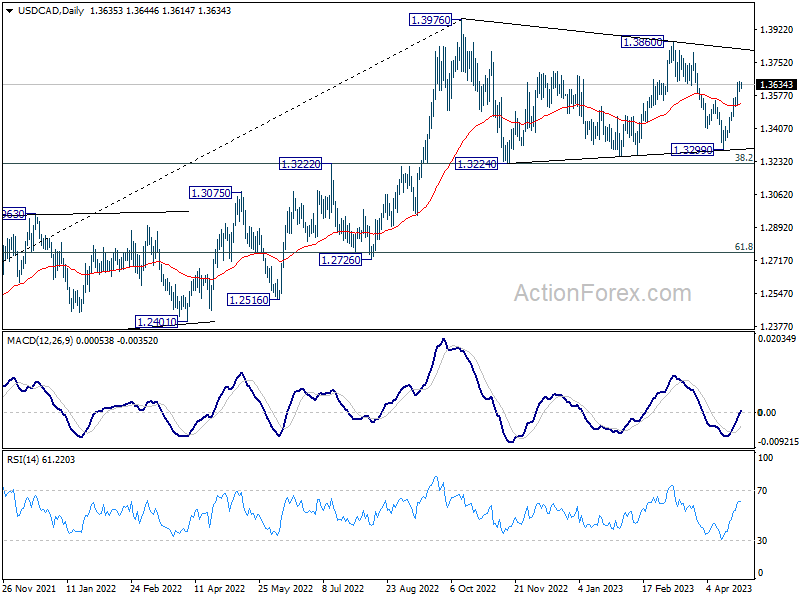

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3607; (P) 1.3629; (R1) 1.3658; More....

Intraday bias in USD/CAD remains on the upside despite some loss of upside momentum. As note before, the correction pattern from 1.3976 could have completed with three waves to 1.3299. Further rally should be seen to 1.3860/3976 resistance zone. Decisive break there will resume larger up trend. On the downside, below 1.3521 minor support will delay the bullish case and turn intraday bias neutral first.

In the bigger picture, the up trend from 1.2005 (2021 low) is still in progress. Break of 1.3976 will confirm resumption and target 61.8% projection of 1.2401 to 1.3976 from 1.3261 at 1.4234. Firm break there will pave the way to long term resistance zone at 1.4667/89 (2016, 2020 highs). On the downside, sustained break of 55 W EMA (now at 1.3302) is needed to confirm medium term topping. Otherwise, outlook will remain bullish even in case of deep pull back.

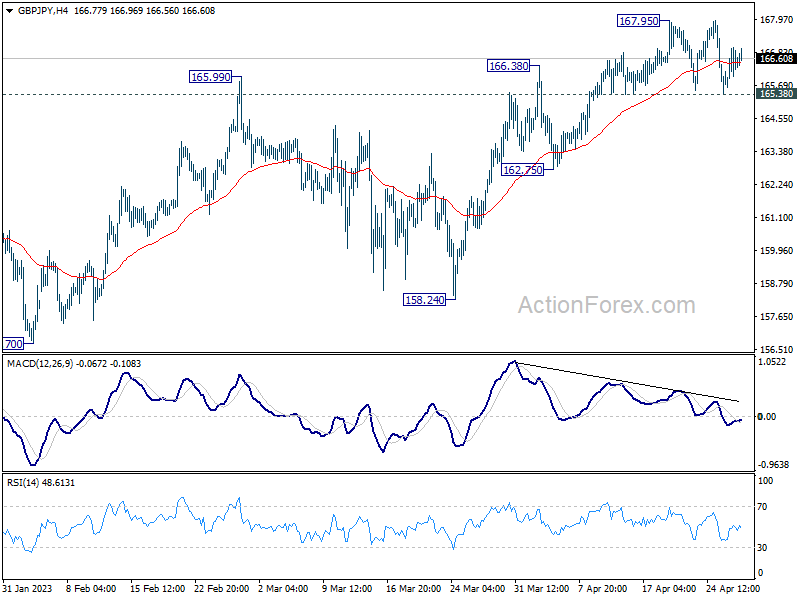

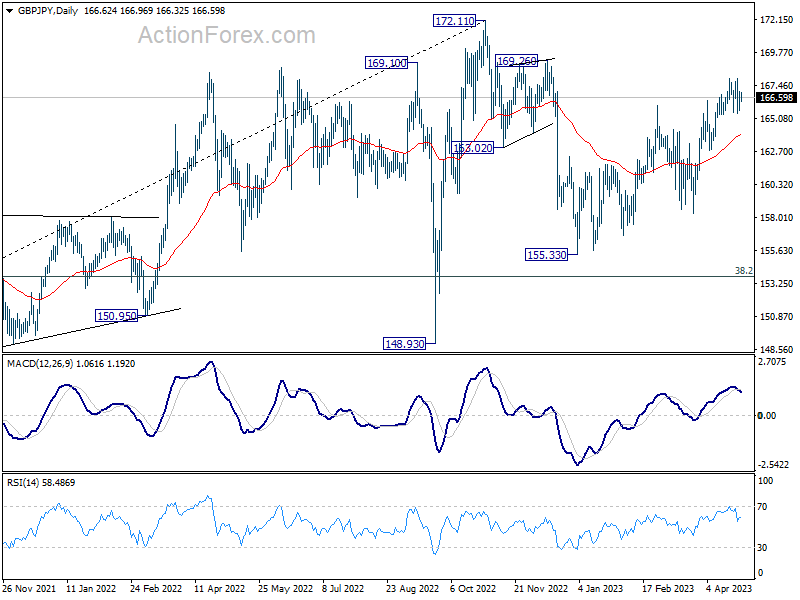

GBP/JPY Daily Outlook

Daily Pivots: (S1) 165.86; (P) 166.44; (R1) 167.23; More...

Range trading continues in GBP/JPY and intraday bias stays neutral first. Further rally is expected as long as 165.38 support holds. On the upside, break of 167.95 will resume the rebound from 155.33 to 169.26 resistance. However, firm break of 165.38 will argue that the corrective pattern from 172.11 is starting another falling leg. Intraday bias will be back on the downside for 162.75 support and below.

In the bigger picture, as long as 38.2% retracement of 123.94 (2020 low) to 172.11 (2022 high) at 153.70 holds, medium term bullishness is retained. That is, larger up trend from 123.94 (2020 low) is still in progress. Break of 172.11 high to resume such up trend is expected at a later stage.

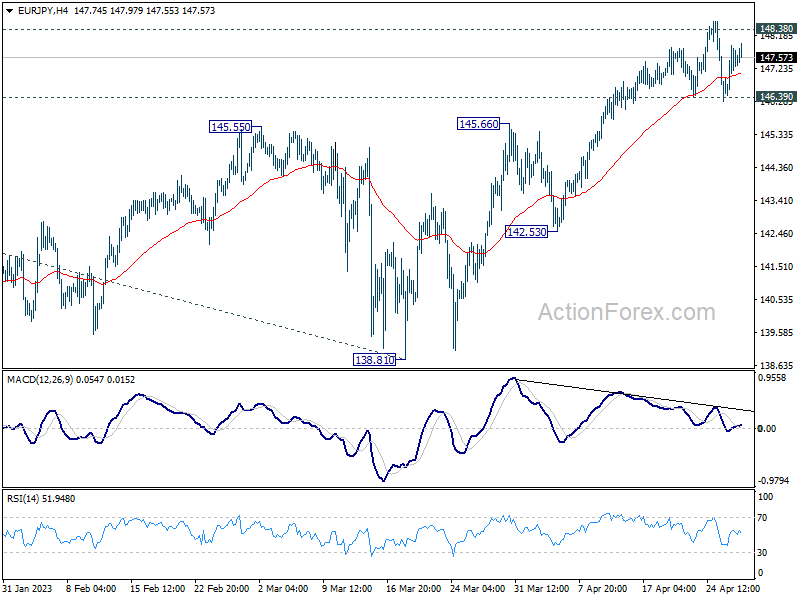

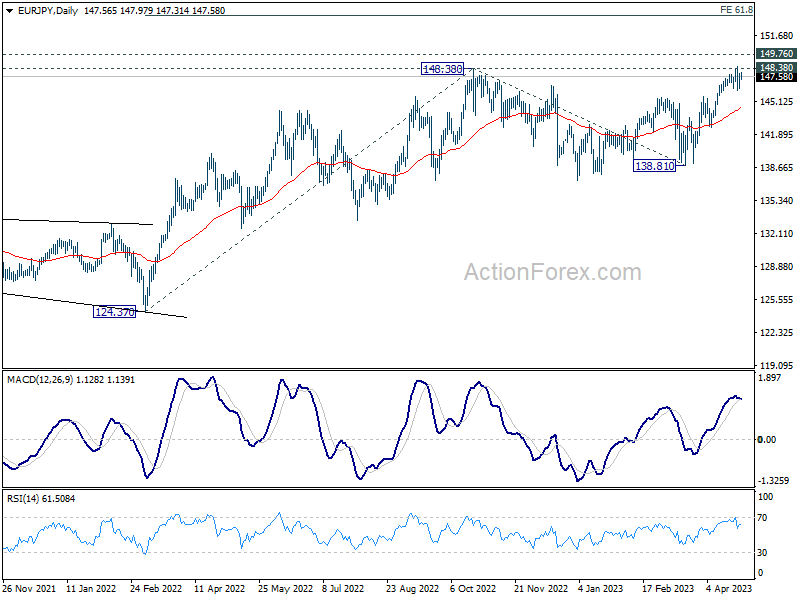

EUR/JPY Daily Outlook

Daily Pivots: (S1) 146.71; (P) 147.31; (R1) 148.17; More....

Intraday bias in EUR/JPY remains neutral for the moment. On the upside, decisive break of 148.38 will resume larger up trend, and next target will be 149.76 long term resistance. However, sustained trading below 146.39 will indicate rejection by 148.38, and bring deeper fall to extend the corrective pattern from there.

In the bigger picture, as long as 55 W EMA (now at 140.70) holds, larger up trend from 114.42 (2020 low) is still in progress for 149.76 long term resistance (2014 high). Decisive break there will resume long term up trend from 94.11 (2012 low). Next target is 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64.

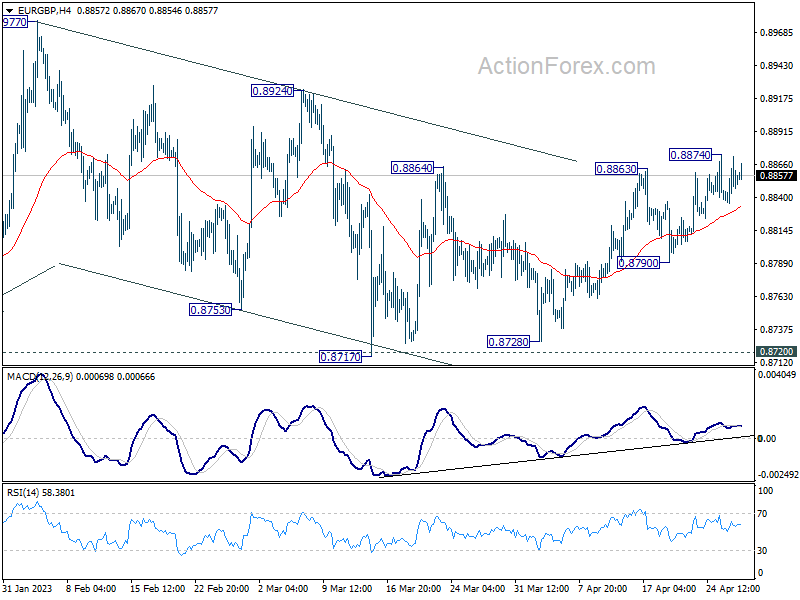

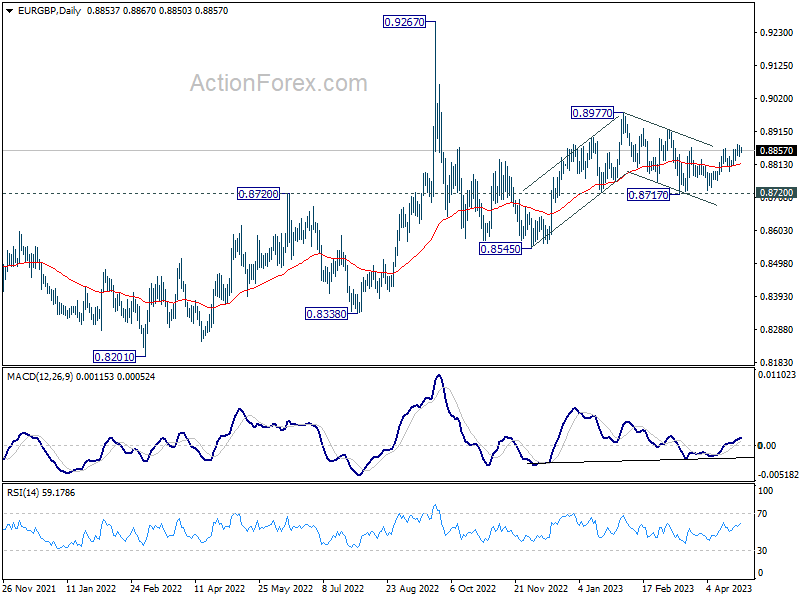

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8835; (P) 0.8855; (R1) 0.8873; More...

EUR/GBP is staying in consolidation below 0.8874 and intraday bias remains neutral first. Further rally will remain in favor as long as 0.8790 support holds. Choppy decline from 0.8977 could have completed already. Above 0.8874 will target 0.8924 resistance first. Firm break there will target 0.8977 high next.

In the bigger picture, outlook remains rather mixed for now, except that price actions from 0.9267 (2022 high) are part of the long term range pattern from 0.9499 (2020 high). With 0.8720 support intact, rise from 0.8545 is in favor to continue through 0.8977. However, firm break of 0.8720 will argue that such rebound has completed, and open up deeper fall through this support level.

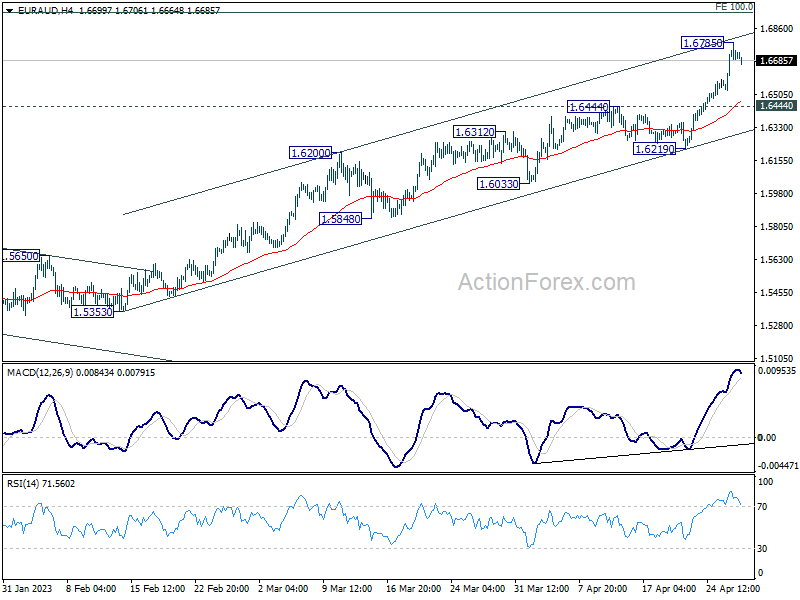

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6573; (P) 1.6680; (R1) 1.6824; More...

Intraday bias in EUR/AUD is turned neutral with current retreat and some consolidations could be seen first. Downside should be contained by 1.6444 resistance turned support to bring rally resumption. Break of 1.6785 will resume larger up trend to 100% projection of 1.4281 to 1.5976 from 1.5254 at 1.6949.

In the bigger picture, the solid break of 1.6389/6434 cluster resistance (38.2% retracement of 1.9799 to 1.4281 at 1.6389) argues that whole down trend from 1.9799 (2020 high) has completed at 1.4281 (2022 low). Further rise should be seen to 61.8% retracement at 1.7691 next. For now, outlook will stay bullish as long as 1.5976 resistance turned support holds, even in case of deep pull back.

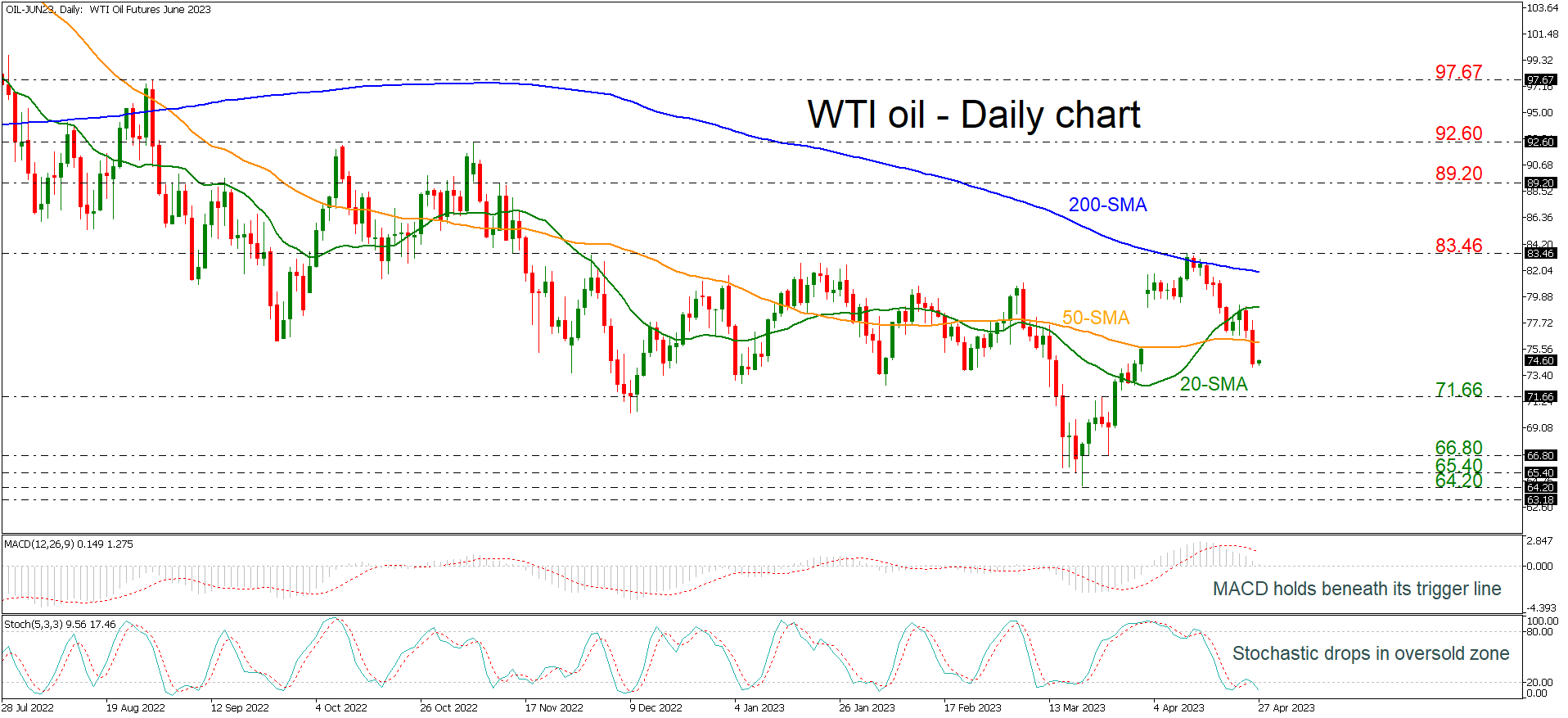

WTI Crude Oil DipsFurther from 200-day SMA

WTI crude oil futures have been underperforming over the last couple of weeks after the pullback off the 83.46 resistance and the 200-day simple moving average (SMA). The market recouped the bullish gap posted on April 3 and the selling interest continues, something confirmed by the technical oscillators. The MACD is easing beneath its trigger line, while the stochastic is diving towards the oversold territory.

Immediate support to further losses could come from the 71.66 inside swing high from March 23 ahead of the crucial lines such as 66.80, 65.40 and 64.20.

Otherwise, a successful climb above the 20- and the 50-day SMAs could drive the commodity until the 200-day SMA at 81.90 before meeting the previous peak of 83.46. Any bullish attempts higher could switch the outlook to a more positive one, hitting the 89.20 resistance level.

In brief, oil prices are looking neutral in the medium-term timeframe as they failed to exhibit any bearish or bullish tendencies. A lower low below 64.20 or a jump above 83.46 could reveal the next direction.

WTI Remains Under Pressure

USD/CHF grinds recent bottom

The US dollar struggles as lacklustre capital goods orders suggest an economic slowdown. The pair is in a precarious situation with tentative breaks below the recent bottom at 0.8860. The bears may see a rebound as an opportunity to sell into strength. 0.8950 is the closest resistance in this regard. Only a clean cut above the psychological level of 0.9000 would improve the market mood and add a building block to a reversal. Otherwise, momentum selling may take over again and send the greenback to January 2021’s low at 0.8760.

GBP/USD tests key resistance

The pound bounces as traders reduce their demand for safe haven assets. On the daily chart, the price is consolidating its gains at the confluence of the supply-turned-demand zone and the 30-day SMA, which suggests that the bias remains bullish. After finding support over 1.2380, a close above the previous swing high of 1.2540 where strong resistance has been felt may flush out remaining selling interests and pave the way for a breakout rally towards 1.2600. The RSI’s overbought condition may temporarily limit the upside.

US Oil struggles for support

WTI crude dived as recessionary worries outweigh supply constraints. From the daily chart’s perspective, the current correction has more than filled the gap from early April and is yet to stabilise with a decisive break below 75.00 near the start of the April surge indicating lingering weakness. 72.70 is the next support as the RSI goes oversold once again. The bulls must clear 77.10 and the top of the brief rally at 79.00 before a sustained recovery could materialise, or the commodity could be vulnerable to a new round of sell-off.

Temporary First Republic-Related Stress to Fade Further

Markets

First Republic shares remain in tailspin, but spillover to other markets was way smaller than on Tuesday. The new sell-off in the stock came after CNBC reported that the US government is currently unwilling to intervene for the bank. Bank advisors are working on a deal including an attempt for a capital raise after big banks helped restore confidence in the lender (like they tried earlier by depositing several billion dollars at the beleaguered lender). Key US equity indices opened with small gains but only Nasdaq managed to maintain them by the closing bell (+0.5%). Main European indices lost 0.5% to 1%. Technical elements are at play as well after the EuroStoxx50 bumped into YTD highs and resistance around 4400. US equity futures this morning are again positively oriented following strong after-market Meta earnings. Core bonds attempted to add to Tuesday’s gains, but threw the towel in the US session. US yields added 4.5 to 5 bps across the curve. Changes on the German yield curve ranged between -3.5 bps at the front end and +4 bps at the very long end. Eco data (disappointing core US durables) played no part in yesterday’s story line. The dollar turned back in the soft spot with EUR/USD temporary accelerating beyond the YTD highs to set a new one at 1.1095. The pair eventually closed at 1.1041. Similar technical EUR-accelerations were visible and stood firm against the likes of AUD, NZD and CAD. The EUR/SEK move was more inspired by the Riksbank’s dovish 50 bps rate hike.

Focus now turns to GDP and inflation numbers today and especially tomorrow. Belgian inflation kicks off the national European releases today with the focal point tomorrow at French/Spanish/German inflation figures. The US eco calendar contains US Q1 GDP data today and March PCE deflators, Q1 employment cost index and Chicago PMI tomorrow. The data won’t derail Fed plans to lift policy rates by 25 bps next week, but could make or break our base case for a 50 bps ECB hike. Apart from EMU inflation, we’ll see Q1 GDP and the ECB’s credit and lending survey as well ahead of Thursday’s policy meeting. Overall, we expect the temporary First Republic-related stress to fade further with especially European yields supported by the upcoming ECB meeting. The narrowing short term yield differential between the US and Europe should keep EUR/USD supported as well.

News and views

The US House of Representatives yesterday passed a bill to raise the government debt ceiling currently at $31.4tn. The vote passed with only a narrow majority of 217-215 and is seen as a political victory for the Republican House speaker, Kevin McCarthy. The House Bill would raise to borrowing authority by $1.5tn or being extended till March 2024, whichever comes first. However, the bill also includes spending cuts that are unacceptable for the Democratic party. So, it won’t pass in Senate or meet a veto from President Biden. The White House press Secretary already indicated that Biden won’t approve the spending cuts. As the stalemate persist, the US government is at risk of defaulting on its payments somewhere on summer (potentially end July) depending on the inflow of tax receipts.

Minutes of the previous Bank of Canada meeting showed that immediate focus of the decision was on whether to increase the policy rate or keeping it unchanged at 4.5%. As part of this discussion, the governing council also considered how long the policy rate would need to remain elevated in order to return inflation to target. Economic resilience and persistence of elevated core inflation, concern that the evolution of inflation from 3% to 2% in H2 2023 and 2024 could prove more difficult and the need to be forward looking and not wait too long to ensure that monetary policy was restrictive enough were arguments to raise rates sooner rather than later. The case to maintain the policy rate at 4.5% reflected the Governing Council’s view that headline inflation is coming down quickly in line with the Bank’s forecast and that more evidence would be needed to assess whether monetary policy was sufficiently restrictive. The GC agreed that it was important to continue to signal that it was prepared to increase the policy rate further if needed. It also assessed that cutting rates later this year isn’t the most likely scenario.